Managing partnership tax audits is a notoriously complex endeavor, often leaving partners conflicted over who should bear the burden of direct IRS communications and decision-making. Before selecting a resolution path, it is crucial to position this challenge within the context of modern tax compliance, particularly how regulatory shifts have transformed traditional administrative roles.

Utilizing a formal Tax Matters Partner (TMP) designation agreement template grants your entity vital operational clarity and liability protection. As a key educational stipulation, however, partners must recognize that these templates must be carefully tailored to distinguish between legacy TEFRA rules and current Partnership Representative requirements. For example, a robust agreement must include concrete clauses addressing indemnification limits and removal protocols.

In the following sections, we will outline the essential components of an effective designation template, evaluate key draft variations, and guide you in selecting the right framework to safeguard your partnership.

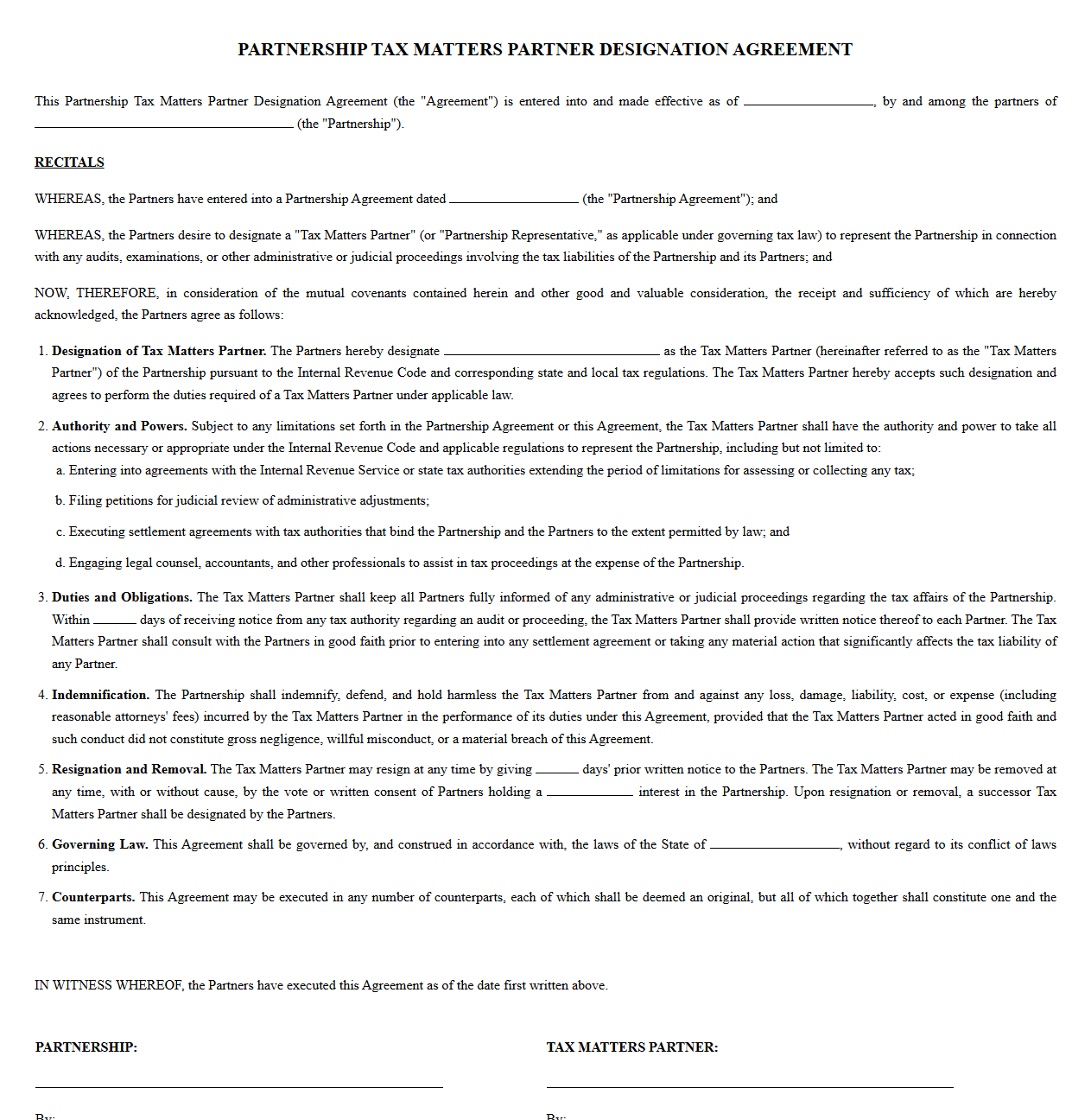

Partnership Tax Matters Partner Designation Agreement

Download: .PDF

Download: .PDF

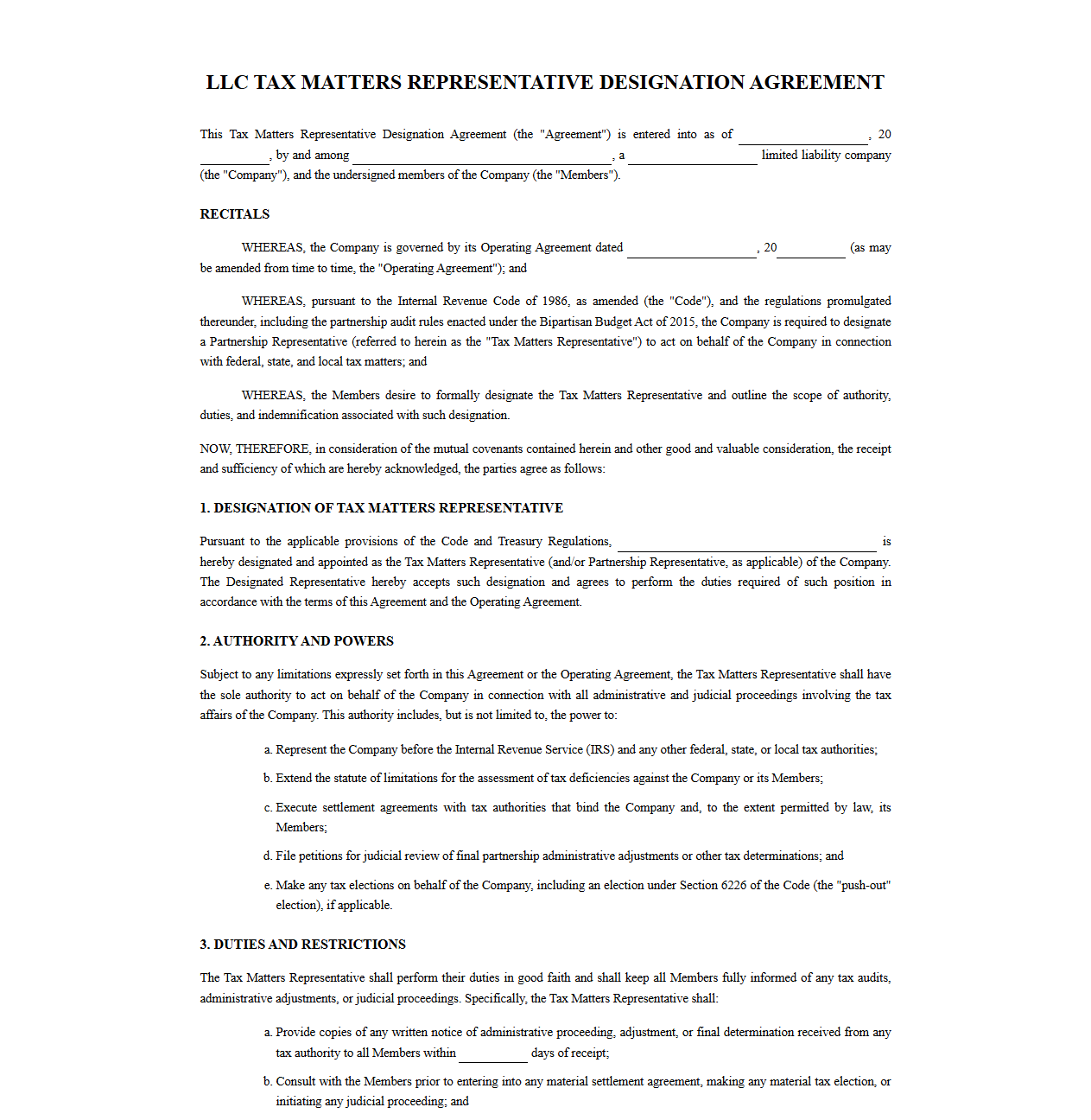

LLC Tax Matters Representative Designation Agreement

Download: .PDF

Download: .PDF

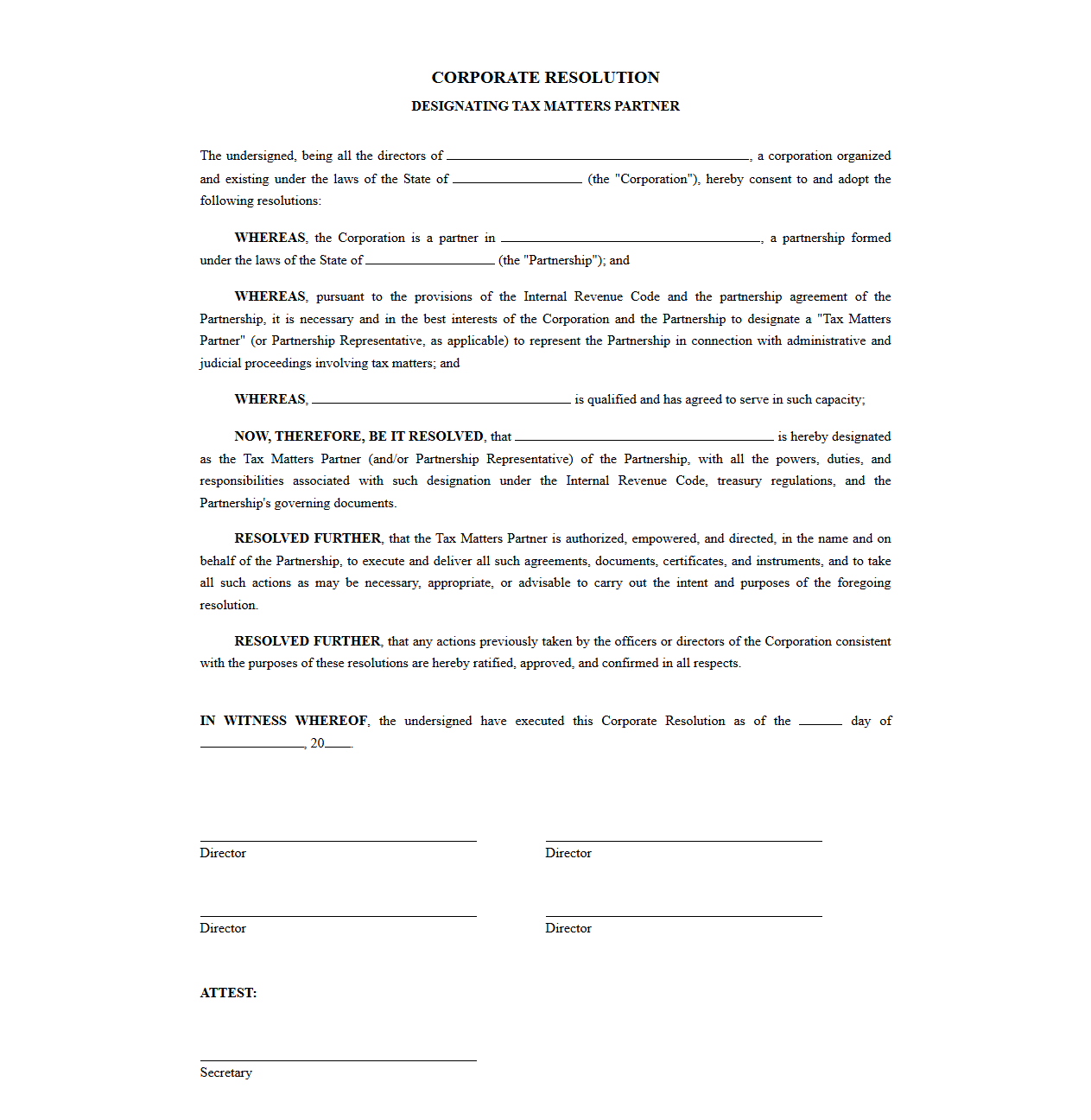

Corporate Resolution Designating Tax Matters Partner

Download: .PDF

Download: .PDF

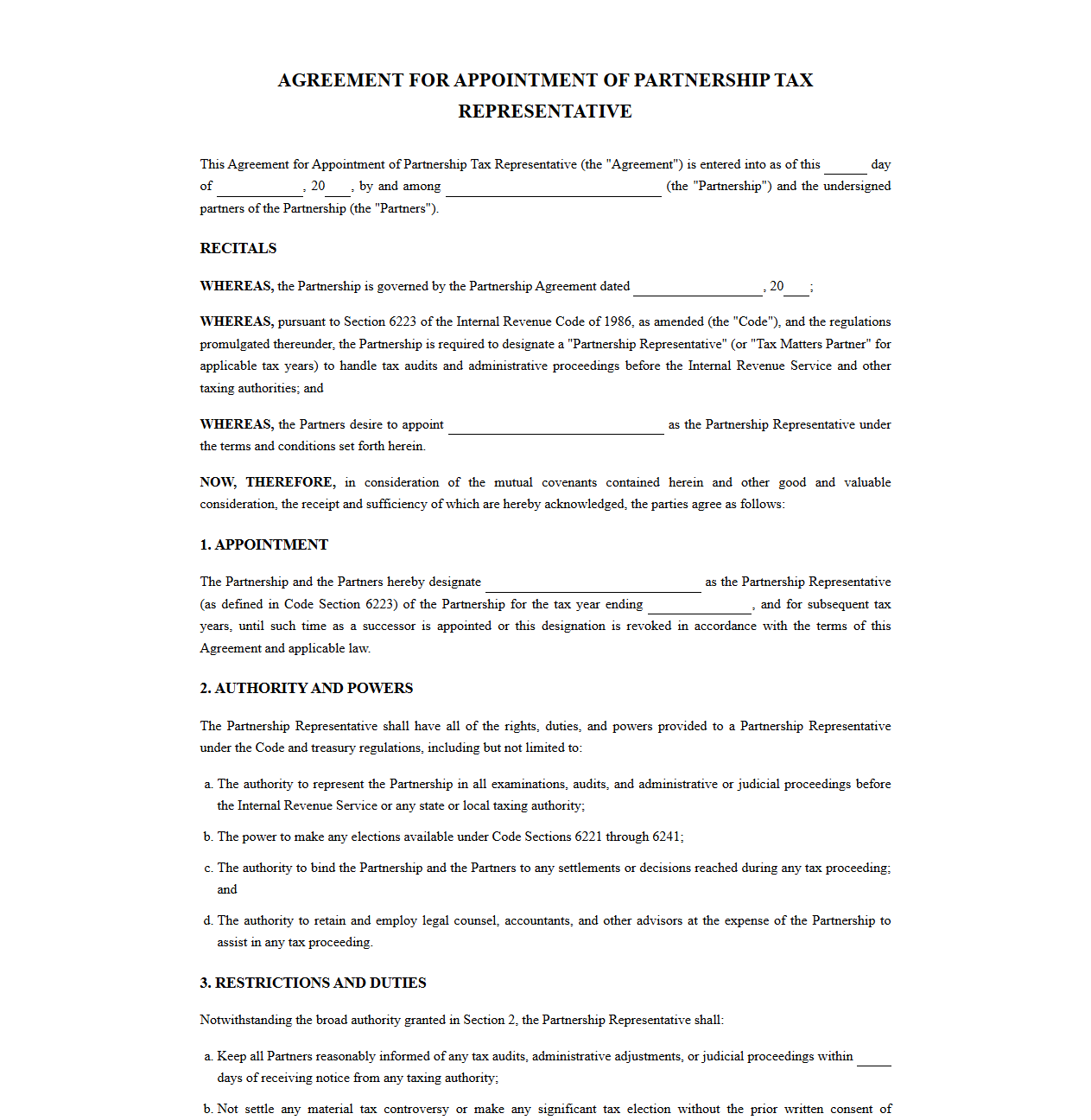

Agreement for Appointment of Partnership Tax Representative

Download: .PDF

Download: .PDF

LLC Agreement Amendment for Tax Matters Partner Designation

Download: .PDF

Download: .PDF

Consent Action of Partners Designating Tax Matters Partner

Download: .PDF

Download: .PDF

General Partnership Tax Matters Partner Appointment Contract

Download: .PDF

Download: .PDF

Multi-Member LLC Tax Matters Partner Designation Template

Download: .PDF

Download: .PDF

Joint Venture Tax Matters Partner Designation Agreement

Download: .PDF

Download: .PDF

Understanding Partnership Tax Representation and the Role of the TMP

Partnerships offer immense operational flexibility, but they also present unique challenges when navigating the complexities of federal tax compliance. Because a partnership is a pass-through entity, the Internal Revenue Service (IRS) does not tax the entity directly; instead, profits and losses flow through to individual partners. To streamline the audit process, the IRS established the role of the Tax Matters Partner (TMP) under the Tax Equity and Fiscal Responsibility Act of 1982 (TEFRA). This designated individual serves as the primary liaison between the partnership and the tax authority, managing administrative proceedings and representing the collective interest of the business.

Choosing the correct representative is critical for a partnership's ongoing financial health. The decisions made by this representative during an audit can have cascading financial consequences for every member of the venture. Without a competent and legally recognized spokesperson, a partnership risks administrative chaos, missed deadlines, and unfavorable tax adjustments that could have been avoided through strategic advocacy and timely communication.

The Legal Authority and Responsibilities of a Tax Matters Partner

The Tax Matters Partner holds significant legal authority and carries strict fiduciary responsibilities to the partnership and its members. This role is not merely administrative; the actions of the TMP can legally bind the entire partnership and its partners during federal tax proceedings.

The core legal powers and duties typically assigned to a TMP include:

- Extending the Statute of Limitations: The power to sign waivers to extend the period during which the IRS can assess tax deficiencies against the partnership.

- Binding Settlement Agreements: The authority to enter into settlement agreements with the IRS that can bind partners who are not actively participating in the audit.

- Filing Petitions for Judicial Review: The exclusive right to file petitions in the U.S. Tax Court, federal district courts, or the Court of Federal Claims to contest IRS adjustments.

- Information Dissemination: The mandatory obligation to keep all partners informed of the progress of any administrative or judicial tax proceedings.

Why a Formal TMP Designation Agreement is Essential

Operating a partnership without a formal, written agreement designating the representative and outlining their limitations presents severe operational and financial risks. If a partnership fails to designate a representative formally, the IRS reserves the right to select one on the partnership's behalf, which may result in an ill-equipped or unwilling partner thrust into a highly technical legal role.

A structured designation agreement protects individual minority partners by establishing clear boundaries on what the representative can do without majority consent. It ensures transparency, prevents unilateral decisions that could disproportionately harm specific partners, and serves as a vital dispute-resolution mechanism during high-stakes federal tax audits.

Warning: In Medical & Business Facilities Ltd. v. Commissioner, the lack of clear, formal documentation regarding the designation and authority of the tax representative led to protracted litigation over whether a partner had the legal capacity to bind the partnership, resulting in costly delays and unexpected liabilities.

Essential Clauses in a Tax Matters Partner Designation Template

To ensure robust legal protection, a high-quality partnership agreement or standalone amendment must contain specific, well-drafted contractual provisions.

Notice and Reporting Requirements

This clause, often titled the Notice of Administrative Proceedings Clause, mandates that the representative notify all partners in writing within a specified number of days (e.g., five business days) of receiving any communication or notice of audit from the IRS.

Partner Approval Thresholds

The Consent and Approval Threshold Clause prevents the representative from entering into binding settlements, extending the statute of limitations, or filing lawsuits without obtaining a predefined majority vote (such as 51% or 75%) from the partnership's voting interests.

Removal and Succession Protocols

The Resignation and Removal of Representative Clause outlines the exact procedures for replacing the representative, whether due to voluntary resignation, incapacity, or removal by a vote of the partners, ensuring the partnership is never left without legal representation.

How to Choose the Right Agreement Template for Your Partnership

Partnerships vary widely in size, complexity, and operational scope. A template designed for a simple, family-owned business will not provide the necessary guardrails for a multi-tiered joint venture with institutional investors. It is essential to select a template that aligns with your specific organizational structure and state regulations.

| Partnership Type | Key Template Features Needed | Complexity Level |

|---|---|---|

| Family Partnerships | Simple voting rules, straightforward notice clauses, and minimal administrative overhead. | Low |

| Mid-Sized Professional Firms | Detailed indemnification clauses, clear succession plans, and structured dispute resolution. | Moderate |

| Multi-Tiered Joint Ventures | Complex consent thresholds, coordination with tiered entity representatives, and strict regulatory compliance. | High |

Pitfalls to Avoid: Generic Templates and Outdated BBA Rules

One of the most dangerous mistakes a partnership can make is using an outdated template. The passage of the Bipartisan Budget Act (BBA) of 2015 fundamentally transformed partnership audit procedures. For tax years beginning after December 31, 2017, the IRS replaced the Tax Matters Partner (TMP) framework with the Partnership Representative (PR) regime.

Unlike the old TMP rules, the new Partnership Representative has the unilateral authority to bind the partnership under the BBA, and there is no longer a statutory requirement for the IRS to notify other partners of audit proceedings. Using a pre-2018 generic template that references a "Tax Matters Partner" rather than a "Partnership Representative" under the BBA rules can leave your partnership legally exposed, as the old safeguards and terminology do not apply to modern IRS audits.

Best Practices for Finalizing and Executing Your TMP Agreement

To ensure your partnership's tax representation agreement is legally enforceable and operationally sound, follow a structured execution process.

By taking these deliberate steps, partners can protect their personal assets, secure clear communication lines during audits, and maintain full control over their federal tax representation.

- Achieve Partner Consensus: Present the draft agreement to all partners to discuss and agree upon the scope of authority, notice periods, and approval thresholds.

- Obtain Professional Legal Review: Have a qualified tax attorney review the document to ensure compliance with the Bipartisan Budget Act of 2015 and state-specific partnership laws.

- Formalize the Execution: Have all partners sign and date the agreement, then securely store the executed document with the partnership's permanent corporate records.

- Complete IRS Filings: Properly designate the chosen representative on the partnership's annual tax return (Form 1065) in accordance with current IRS instructions.

Leave a comment