Discovering a material accounting error after financial statements are finalized is a high-stress scenario that can quickly escalate into costly liability disputes and fractured client relationships. Before addressing conflict resolution, however, firms must recognize how modern regulatory scrutiny and complex compliance standards have dramatically amplified the stakes of everyday bookkeeping.

Utilizing structured indemnification agreements grants practice leaders invaluable peace of mind by legally defining the boundaries of financial exposure. Please note the stipulation that while these templates provide a robust foundation for risk mitigation, they must be reviewed by legal counsel to align with local jurisdictional statutes. Whether you are addressing minor tax filing discrepancies or significant ledger mismatches, having formal protection in place is essential.

In this guide, we will analyze the key components of liability waiver clauses, provide customizable indemnification templates, and outline best practices for executing these agreements with clients.

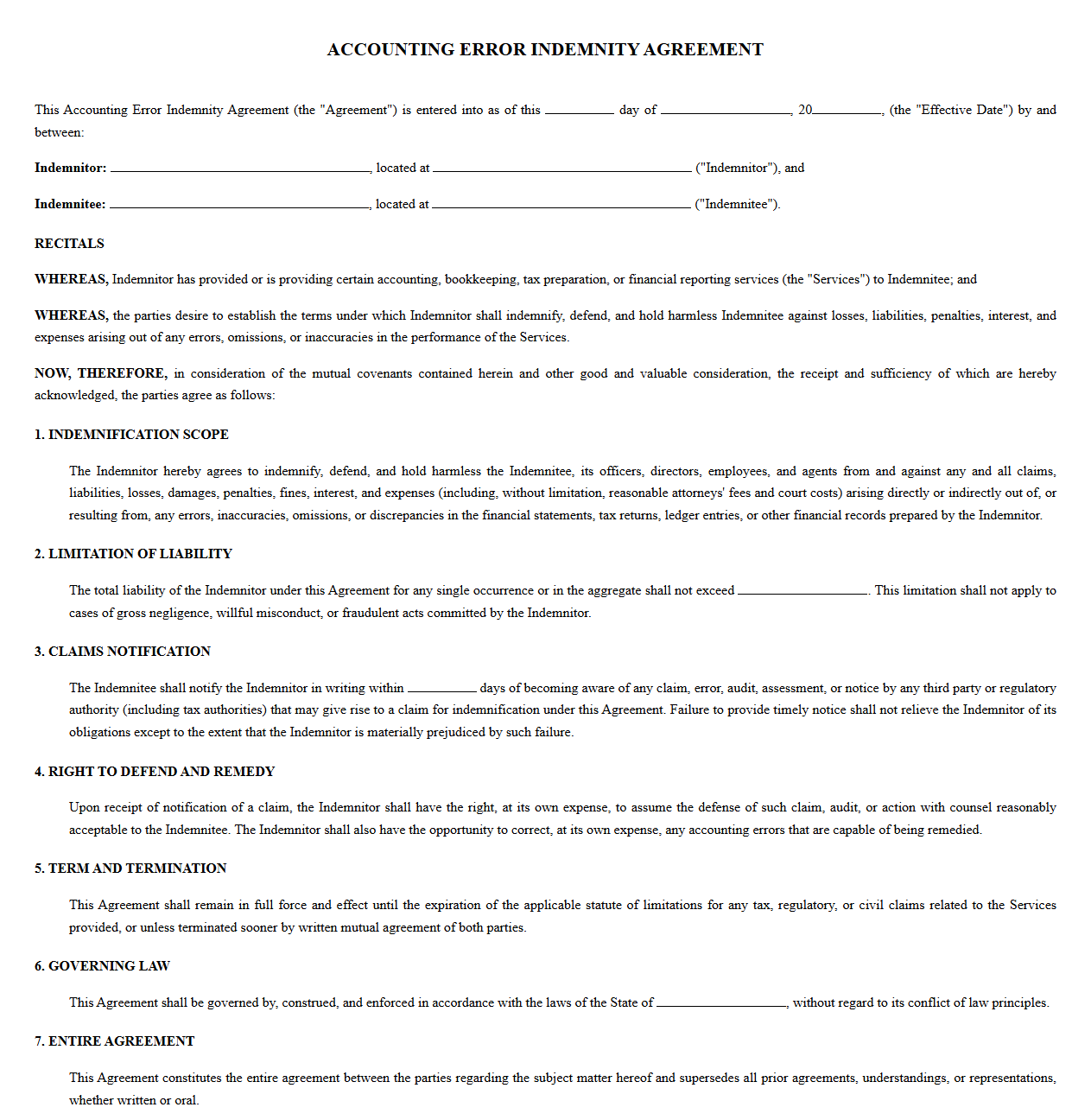

Accounting Error Indemnity Agreement Template

Download: .PDF

Download: .PDF

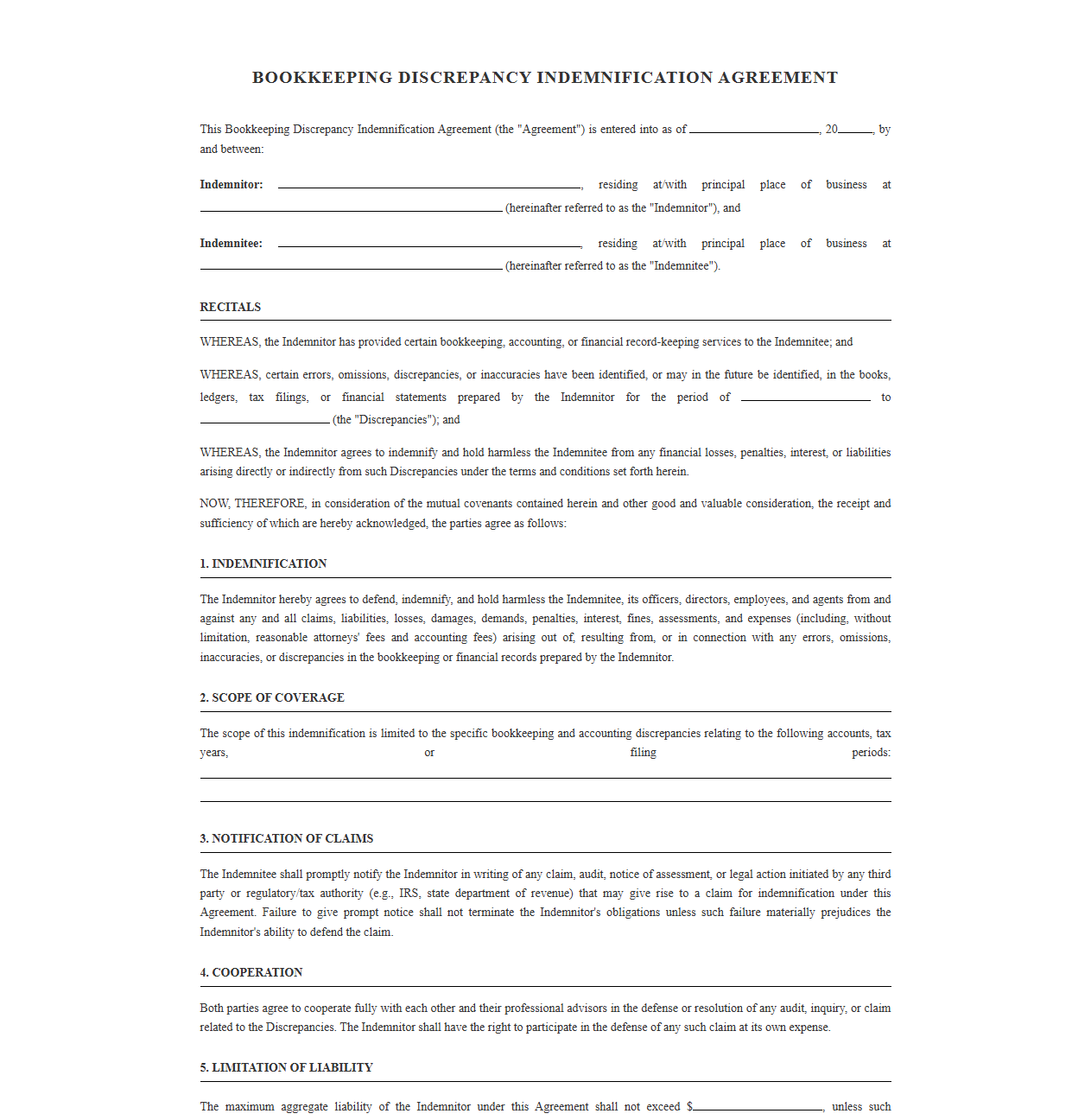

Bookkeeping Discrepancy Indemnification Agreement Form

Download: .PDF

Download: .PDF

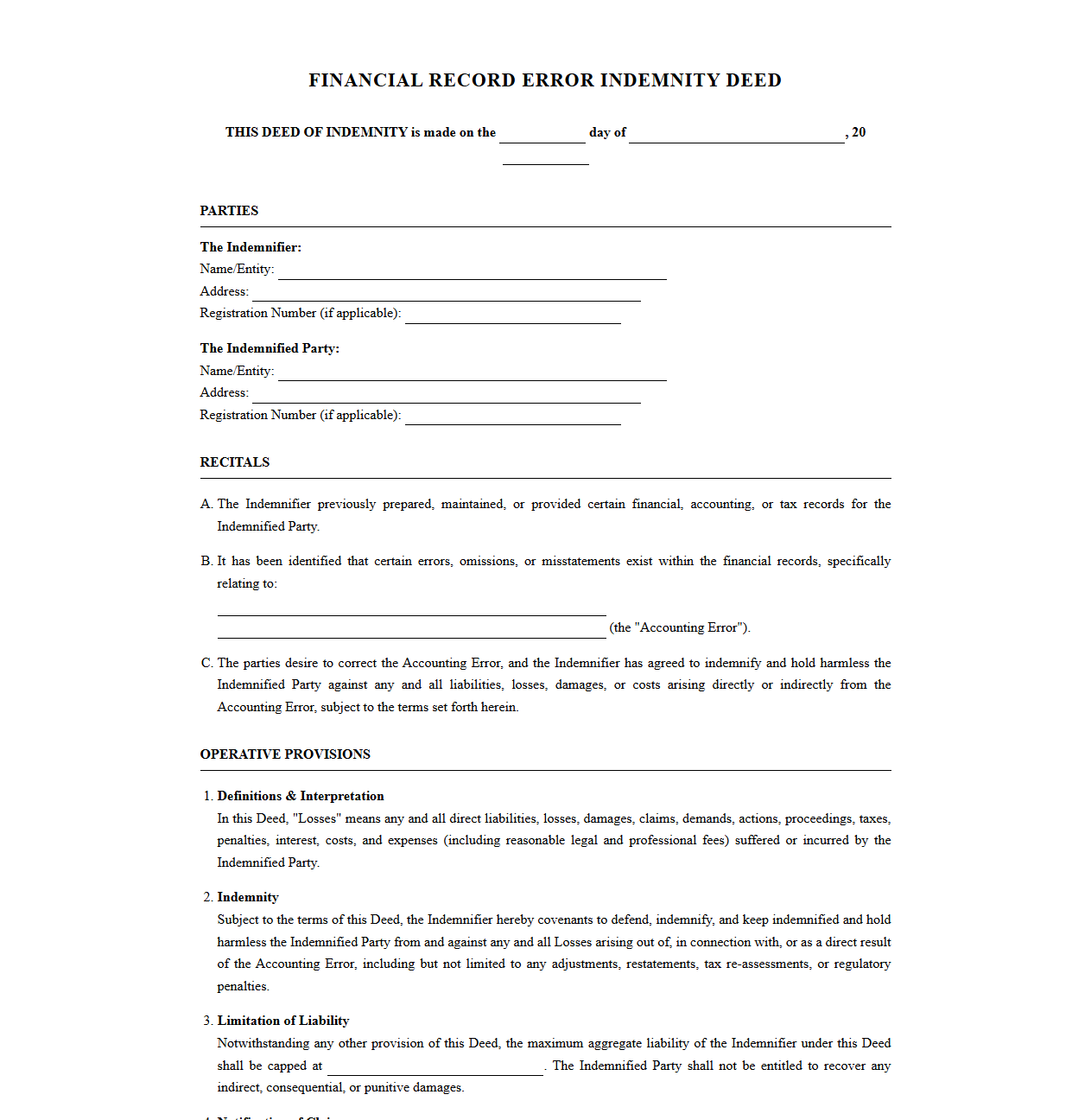

Financial Record Error Indemnity Deed

Download: .PDF

Download: .PDF

Accounting Mistake Indemnity Contract Template

Download: .PDF

Download: .PDF

Financial Statement Error Indemnification Agreement

Download: .PDF

Download: .PDF

Audit Error Indemnity Letter Template

Download: .PDF

Download: .PDF

Tax and Accounting Error Indemnification Agreement

Download: .PDF

Download: .PDF

General Ledger Mistake Indemnity Form

Download: .PDF

Download: .PDF

Corporate Accounting Error Indemnification Release

Download: .PDF

Download: .PDF

The Cost of Calculation: Understanding Accounting Liability

In the world of corporate finance, a misplaced decimal point or a miscategorized transaction is rarely just a simple clerical mistake. For modern businesses, even minor accounting errors can quickly cascade into catastrophic financial liabilities. A single slip on a balance sheet can lead to severe tax penalties, breached loan covenants, depleted cash reserves, and damaged investor relations.

Because financial data drives critical strategic decisions, the stakes of bookkeeping precision are incredibly high. A single undetected ledger error can expose a business to regulatory fines and lawsuits that far exceed the annual cost of the accounting services themselves. To survive in this high-risk environment, both financial service providers and their clients must implement robust risk mitigation strategies, beginning with clear, legally binding contractual protections.

The Shield of Indemnity: What is an Indemnification Clause?

Within financial services, bookkeeping, and accounting, an indemnification clause serves as a vital legal shield. It is a contractual agreement where one party promises to compensate the other for specific losses, damages, or legal costs arising from errors, omissions, or breaches of contract during the delivery of financial services.

For independent bookkeepers and accounting firms, this clause prevents a client from shifting the entirety of their business losses onto the financial professional due to an honest oversight. Conversely, for clients, it ensures that gross negligence or intentional misconduct by a hired professional will not leave the business holding the bag. Legally, indemnity is defined as a mechanism to allocate risk safely between contracting parties.

"Indemnity is a contract by which one engages to save another from a legal consequence of the conduct of one of the parties, or of some other party."

Anatomy of a Financial Indemnity Agreement

A well-drafted financial indemnification clause must be precise and tailored to the unique risks of financial reporting. Standard boilerplate templates rarely provide adequate protection because they fail to account for the specific complexities of tax laws and ledger management. A robust agreement must clearly define how liability is capped and how claims are processed.

To ensure comprehensive protection, every financial indemnity agreement should contain the following essential elements:

- Scope of Liability: Explicitly defines which specific acts, errors, or omissions (such as clerical data entry mistakes versus deliberate fraud) trigger the indemnification obligations.

- Liability Caps: Establishes a maximum monetary limit on the indemnifying party's financial exposure, often tied to a multiple of the professional fees paid under the contract.

- Notice Requirements: Outlines the exact timeframe and formal process by which the indemnified party must notify the other of a potential claim or audit discrepancy.

- Defense of Claims: Clarifies who controls the legal defense of a third-party claim and how legal fees and court costs are allocated between the parties.

Template 1: Standard Bookkeeping Error Indemnification Clause

This standard clause is designed for independent bookkeepers, freelancers, or small bookkeeping firms looking to limit their exposure to minor, unintentional clerical ledger mistakes during routine data entry.

Section X. Indemnification for Bookkeeping Services.

The Client agrees to indemnify, defend, and hold harmless the Bookkeeper from and against any and all claims, liabilities, losses, damages, or expenses (including reasonable attorneys' fees) arising out of or resulting from clerical, arithmetic, or data entry errors in the financial records maintained by the Bookkeeper, except to the extent that such errors are the direct result of the Bookkeeper's gross negligence, willful misconduct, or fraud. Under no circumstances shall the Bookkeeper's total aggregate liability for any errors or omissions exceed the total fees actually paid by the Client to the Bookkeeper under this Agreement during the twelve (12) months preceding the date the claim arose.

Template 2: Mutual Tax Liability Indemnity Agreement

This mutual indemnification agreement is drafted for corporate tax preparation, joint ventures, or high-stakes consulting where both the client and the tax professional share responsibility for data accuracy, audit representation, and regulatory compliance.

Section Y. Mutual Tax Indemnification and Audit Representation.

(a) Practitioner Indemnity: The Tax Practitioner shall indemnify and hold the Client harmless from any direct penalties or interest assessed by tax authorities to the extent such penalties result solely from the Practitioner's failure to apply clear statutory guidelines, provided the Client supplied complete and accurate source documentation.

(b) Client Indemnity: The Client agrees to indemnify and hold the Tax Practitioner harmless from any tax deficiencies, penalties, interest, or legal costs resulting from incomplete, inaccurate, or misleading financial data, records, or oral representations provided by the Client for the purposes of tax return preparation.

(c) Mutual Limitation: Neither party shall be liable to the other for any indirect, consequential, or punitive damages, including lost profits, arising from audit outcomes or tax disputes.

Best Practices for Deploying Financial Indemnity Templates

Simply copying and pasting a template into your contract is not enough to guarantee legal safety. Indemnity clauses must be systematically integrated into your onboarding workflows to ensure they are legally binding and actionable.

Follow these operational steps to deploy these protective clauses effectively within your business:

- Integrate into Master Service Agreements (MSAs): Place these clauses directly in your primary engagement letters or MSAs rather than in separate, easily misplaced addenda.

- Clearly Define Client Obligations: Ensure your agreement states that your financial work is entirely dependent on the accuracy of the source documentation provided by the client.

- Establish a Clear Audit Protocol: Outline a specific procedure for how tax audits or IRS inquiries will be handled, including who will communicate with tax authorities and who covers representation fees.

- Keep Signatures Up to Date: Ensure that any modifications to the scope of work or indemnity limits are signed by authorized representatives of both parties before work begins.

Final Safeguards: Legal Review and Insurance Alignment

While templates provide an excellent foundation for risk management, they cannot replace professional, jurisdiction-specific legal counsel. Contract laws vary significantly across states and countries, and a clause that is enforceable in one jurisdiction may be deemed unconscionable and void in another.

Before finalizing any contract, you must have a qualified attorney review your indemnification clauses to ensure they comply with local laws and align precisely with your Professional Liability Insurance (Errors & Omissions) policy limits. Only when your contracts, your legal review, and your insurance policy work in perfect harmony can you truly protect your business from the catastrophic costs of financial errors.

Leave a comment