Navigating corporate transactions involves managing a minefield of hidden financial risks, where unexpected indirect tax liabilities can quietly erode deal value and disrupt post-merger integration. Before addressing mitigation strategies, organizations must recognize that global tax authorities are intensifying audits, leaving zero margin for error in asset or share transfers.

Implementing a structured indirect tax indemnity agreement grants transaction parties absolute fiscal certainty and protects stakeholders from retroactive assessments. However, effective risk management stipulates that these agreements must not rely on generic boilerplate clauses; they must precisely outline pre-closing liabilities and survival periods. For example, explicitly addressing outstanding cross-border VAT exposures or unrecorded state sales taxes provides concrete proof of robust risk allocation.

In this guide, we will analyze the essential components of these protective agreements and introduce customizable templates designed to secure your transactions against unforeseen tax liabilities.

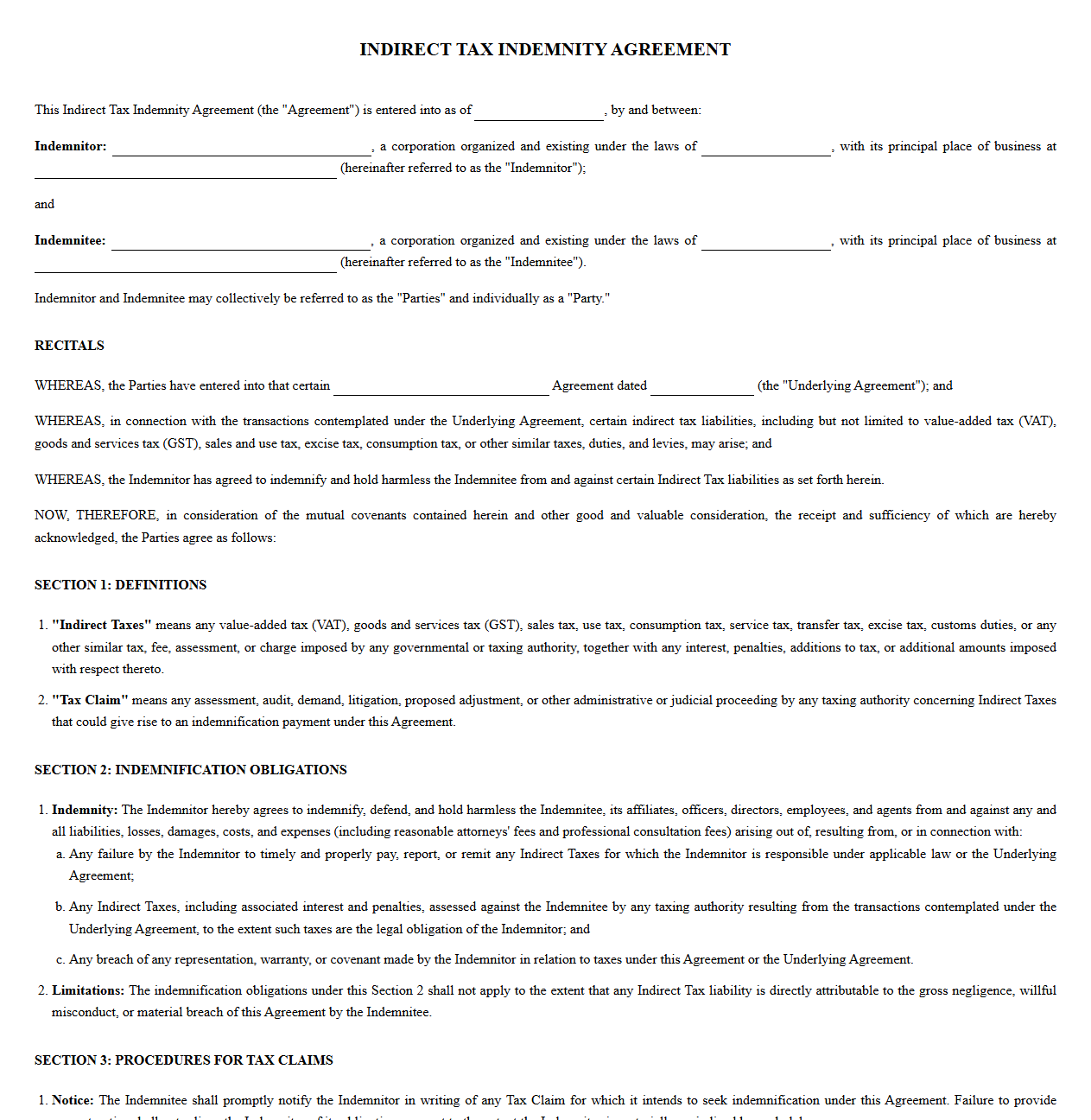

Indirect Tax Indemnity Agreement Template

Download: .PDF

Download: .PDF

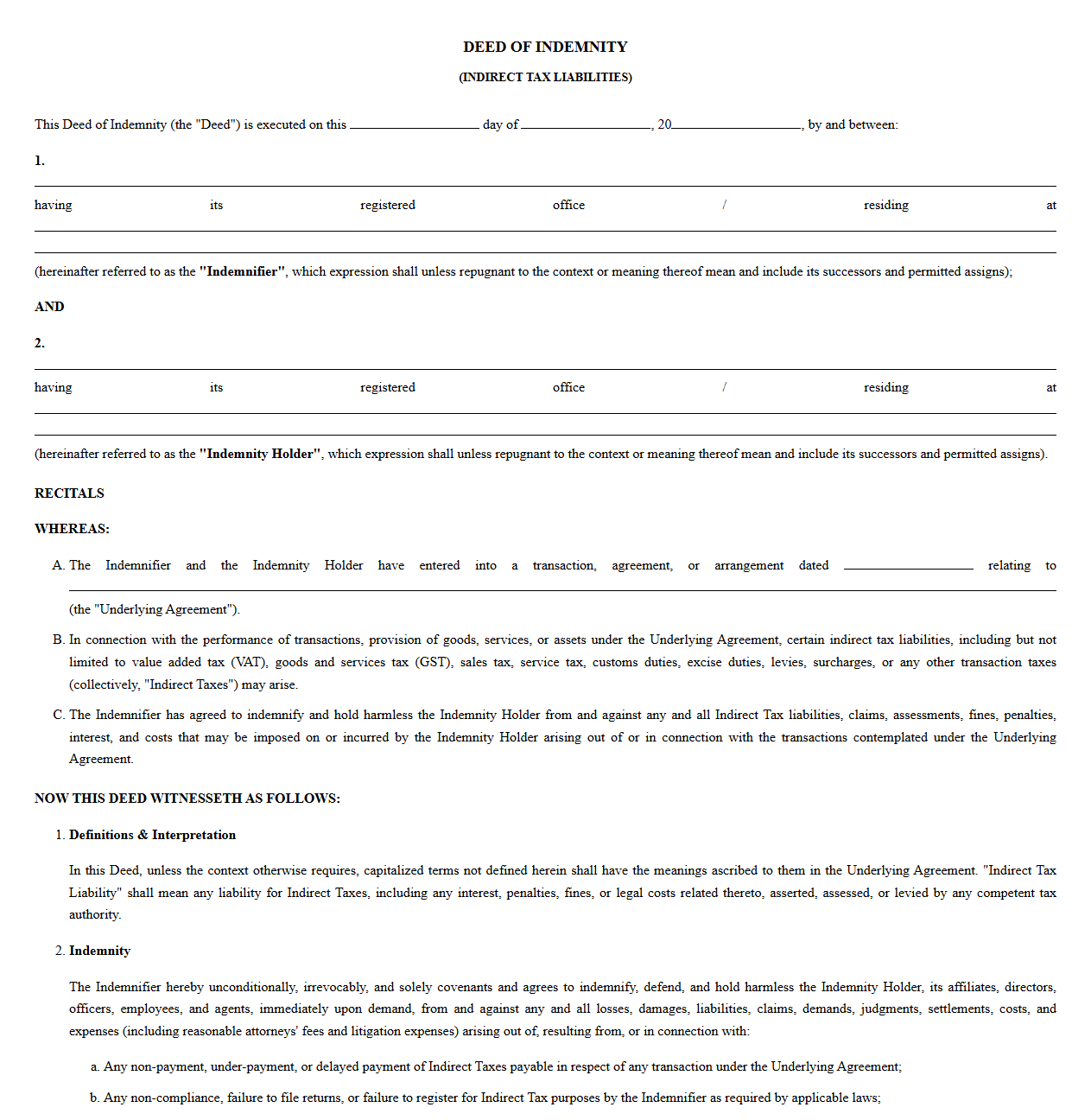

Deed of Indemnity for Indirect Tax Liabilities

Download: .PDF

Download: .PDF

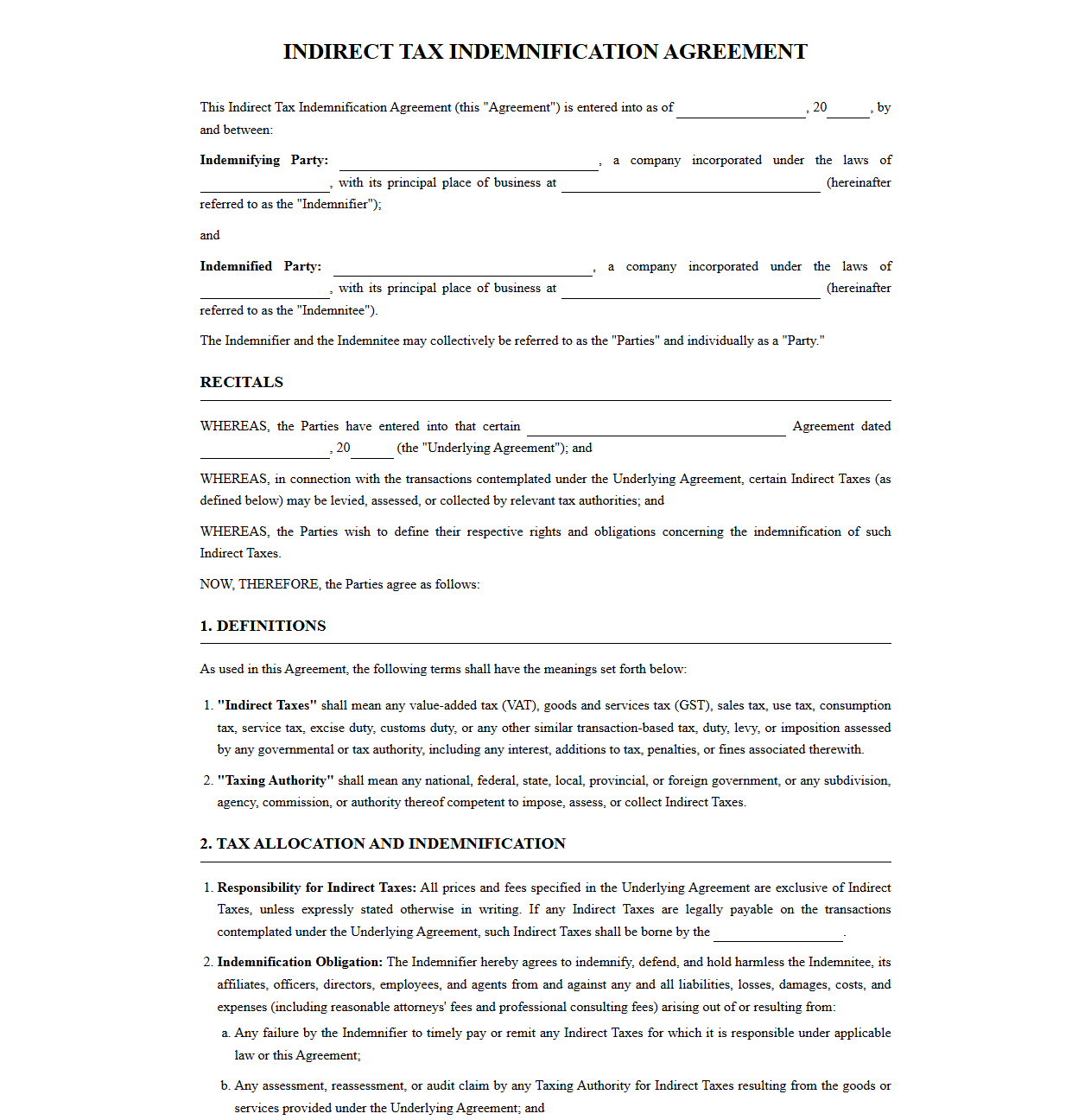

Indirect Tax Indemnification Clause and Agreement

Download: .PDF

Download: .PDF

Agreement for VAT and GST Indemnification

Download: .PDF

Download: .PDF

Mutual Indirect Tax Indemnity Agreement

Download: .PDF

Download: .PDF

Corporate Indirect Tax Indemnification Agreement

Download: .PDF

Download: .PDF

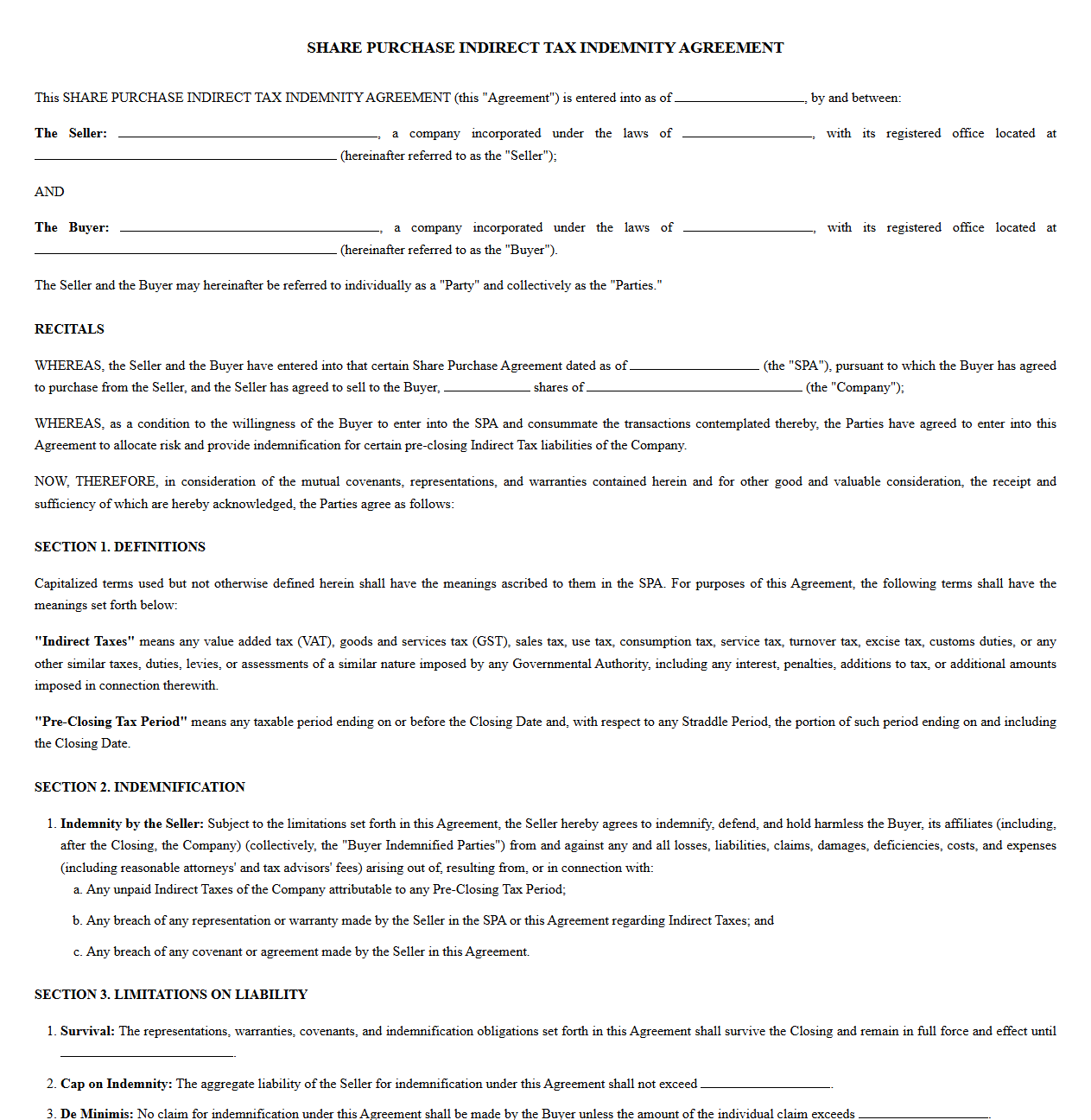

Share Purchase Indirect Tax Indemnity Agreement

Download: .PDF

Download: .PDF

Transactional Indirect Tax Indemnification Contract

Download: .PDF

Download: .PDF

Cross-Border Indirect Tax Indemnity Agreement

Download: .PDF

Download: .PDF

Understanding Indirect Tax Liabilities in Corporate Transactions

In the high-stakes arena of mergers, acquisitions, and major corporate restructurings, dealmakers often focus their due diligence on direct income taxes, overlooking the silent balance-sheet disruptor: indirect taxes. Value Added Tax (VAT), Goods and Services Tax (GST), and local sales and use taxes are transactional by nature. This means a single historical misclassification, an undocumented exemption, or an unfiled return across multiple jurisdictions can quietly compound into catastrophic retroactive liabilities.

Unlike income taxes, which are based on net profitability, indirect taxes apply to gross transaction values. When an acquired business has failed to comply with its compliance obligations, the purchasing entity inherits these historical exposures. Safeguarding against these hidden liabilities is not merely a box-checking exercise; it is a critical component of capital preservation and transactional risk management that ensures the projected valuation of the deal remains intact post-closing.

The Strategic Role of Tax Indemnity Agreements

An indirect tax indemnity agreement serves as a primary financial shield during corporate transitions. By formally allocating the financial responsibility for pre-transaction tax mistakes, this legal instrument shifts the burden of unexpected audits and assessments back to the party who operated the business during that timeframe. It effectively draws a clear line in the sand between the buyer's and seller's respective periods of ownership.

For buyers, a robust indemnity clause ensures that the negotiated purchase price is not artificially inflated by subsequent tax assessments. For sellers, it establishes a defined threshold of liability, allowing both parties to close the transaction with high financial certainty. Rather than letting unresolved tax exposure stall a deal, the indemnity agreement provides a contractually binding mechanism to resolve potential disputes without disrupting ongoing business operations.

Essential Definitions and Scope of Tax Liabilities

- "Indirect Taxes" means any value added tax (VAT), goods and services tax (GST), sales tax, use tax, consumption tax, transfer tax, excise duty, or other similar transactional levy imposed by any governmental authority, including any interest, penalties, or additions to tax associated therewith.

- "Pre-Closing Tax Period" refers to any taxable period ending on or before the closing date of the transaction, as well as the portion of any straddle period ending on the closing date, determining the temporal boundary of the seller's primary tax liability.

- "Excluded Taxes" encompasses any taxes specifically designated as the sole responsibility of the buyer post-closing, or liabilities arising from voluntary changes in accounting methods or business operations initiated by the buyer after the transaction concludes.

Allocation of Tax Liabilities and Seller Representations

The allocation of tax liabilities relies heavily on the "representations and warranties" made by the seller. These are binding statements of fact regarding the historical tax health of the target company. The seller must represent that all indirect tax returns have been accurately filed, all due taxes have been paid, and no audits are currently pending. If any of these representations prove false, it triggers the indemnification clause, allowing the buyer to claim compensation for resulting losses.

"The Seller hereby represents and warrants that the Company has timely filed all required Indirect Tax returns in all material jurisdictions, has paid all outstanding Indirect Taxes due, and has maintained sufficient documentation, including exemption certificates, to support all untaxed transactions during the Pre-Closing Tax Period."

Indemnification Claims and Dispute Resolution Procedures

- The buyer must provide prompt written notice to the seller upon receiving any audit notice, assessment, or demand from a tax authority concerning a Pre-Closing Tax Period.

- The seller shall have the right, at its own expense, to assume and control the defense of any third-party tax audit or proceeding, provided they acknowledge their indemnification obligation in writing.

- The buyer retains the right to participate in the defense at its own cost, and the seller may not settle any tax claim that adversely impacts the buyer's post-closing operations without the buyer's prior written consent.

- If a dispute arises regarding the interpretation or calculation of an indemnification claim, the parties will submit the matter to an independent, mutually agreed-upon accounting firm for final and binding resolution.

Survival Periods and Liability Caps in Indemnity Clauses

Indemnity obligations do not last indefinitely. Parties must negotiate "survival periods," which dictate how long after closing a buyer can bring a claim for indirect tax breaches. While general representations might survive for only 12 to 24 months, tax representations typically survive until the expiration of the applicable statutory period of limitations plus a short buffer. Furthermore, sellers often negotiate "caps" to limit their maximum aggregate liability, alongside "baskets" or "deductibles" that prevent minor claims from being brought until a specific financial threshold is exceeded.

Best Practices for Drafting and Implementing Tax Indemnity Templates

Corporate legal teams must avoid treating tax indemnity templates as static, one-size-fits-all documents. Templates must be actively customized to align with the specific jurisdictional footprint, digital services delivery models, and physical nexus of the target company. It is vital to ensure that the indemnification provisions are seamlessly integrated with the broader purchase agreement, particularly regarding the coordination of survival periods, limits of liability, and the definition of losses.

To secure maximum protection, legal teams should engage localized tax specialists early in the due diligence phase, clearly separate indirect tax indemnities from general indemnities to bypass standard commercial caps, and meticulously draft the definitions of covered taxes to prevent loopholes that could shift the burden back to the acquiring entity.

Read More

Leave a comment