Winding down a business partnership often triggers intense administrative friction, particularly when navigating the overlapping demands of state laws and IRS regulations. Before partners can successfully part ways, they must establish a clear, legally binding framework that addresses outstanding liabilities and equity distribution. Utilizing a structured Partnership Dissolution and Tax Liquidation Agreement secures crucial asset protection and mitigates the risk of future costly tax audits.

While high-quality templates provide an invaluable compliance roadmap, they are designed as foundational frameworks rather than universal solutions; partners must still customize them to align with specific state statutes. Robust templates must feature concrete clauses-such as detailed capital account adjustment provisions and debt allocation schedules-to ensure an equitable wind-down. This guide examines the essential components of these legal templates, outlining how to execute a seamless dissolution while safeguarding your financial interests.

Partnership Dissolution and Tax Liquidation Agreement Template

Download: .PDF

Download: .PDF

Deed of Partnership Dissolution with Tax Liquidation Provisions

Download: .PDF

Download: .PDF

Agreement for Terminating Partnership and Settling Tax Liabilities

Download: .PDF

Download: .PDF

Partnership Winding Up and Tax Liquidation Agreement Form

Download: .PDF

Download: .PDF

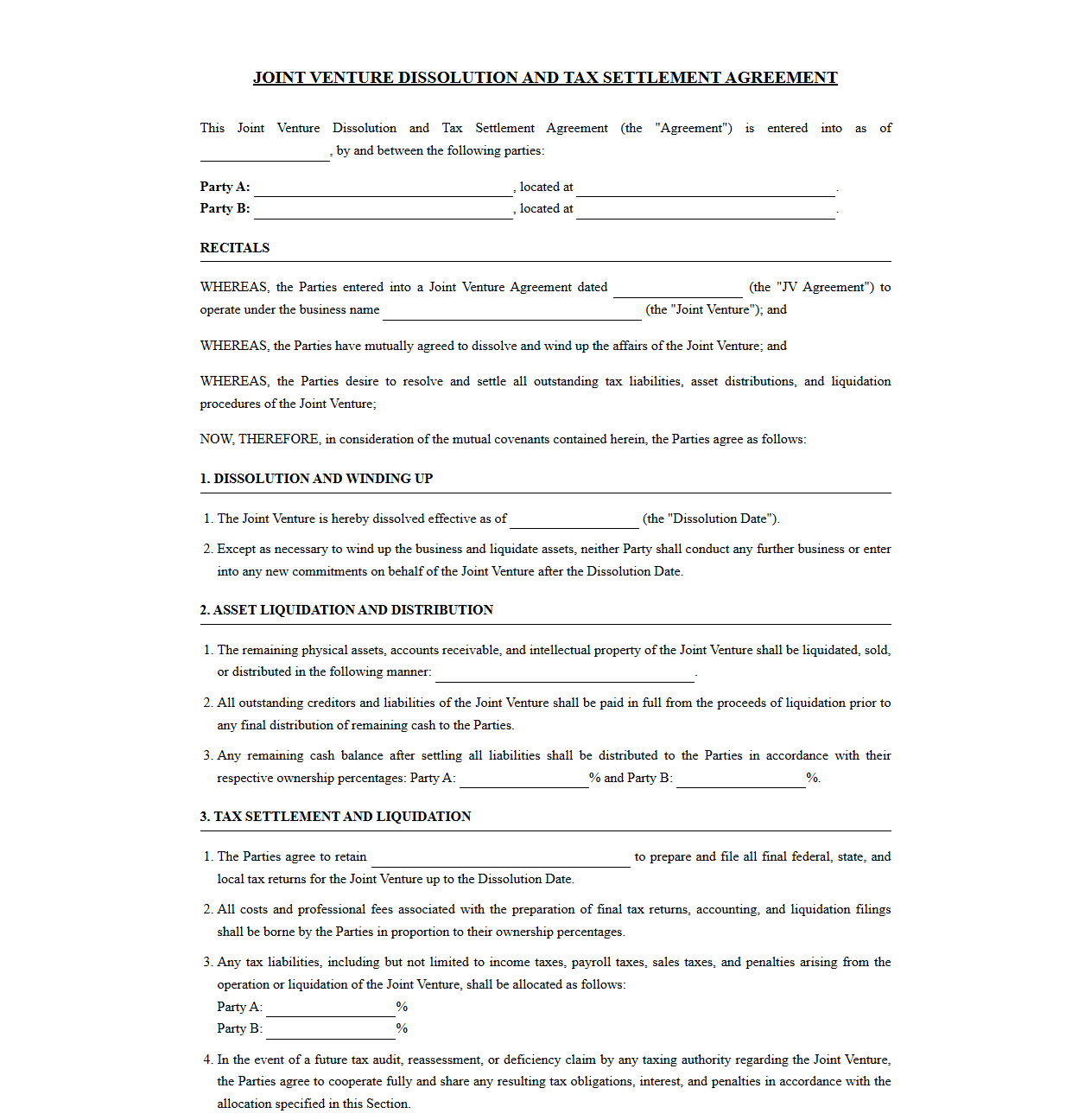

Joint Venture Dissolution and Tax Settlement Agreement Template

Download: .PDF

Download: .PDF

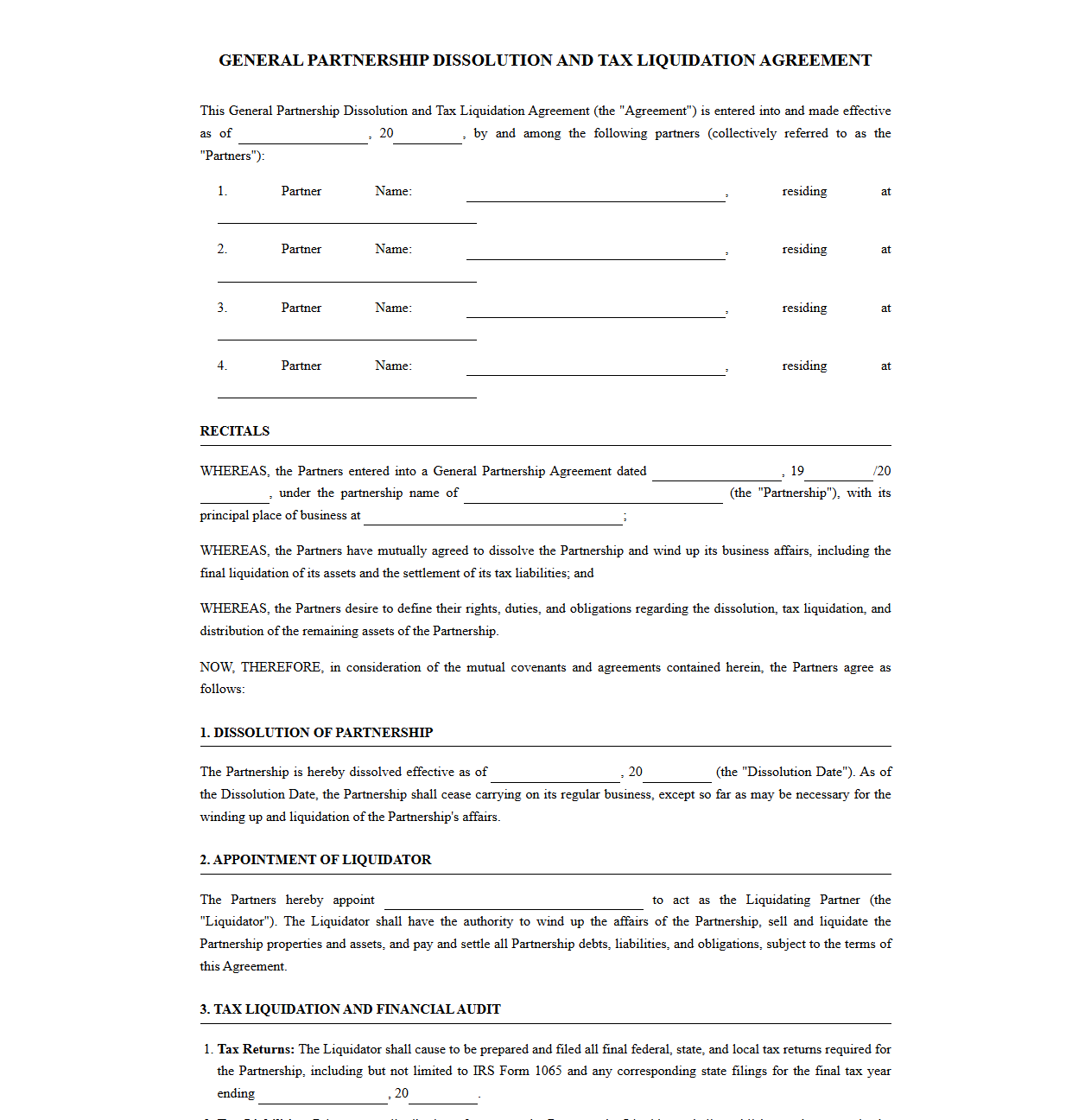

General Partnership Dissolution and Tax Liquidation Contract

Download: .PDF

Download: .PDF

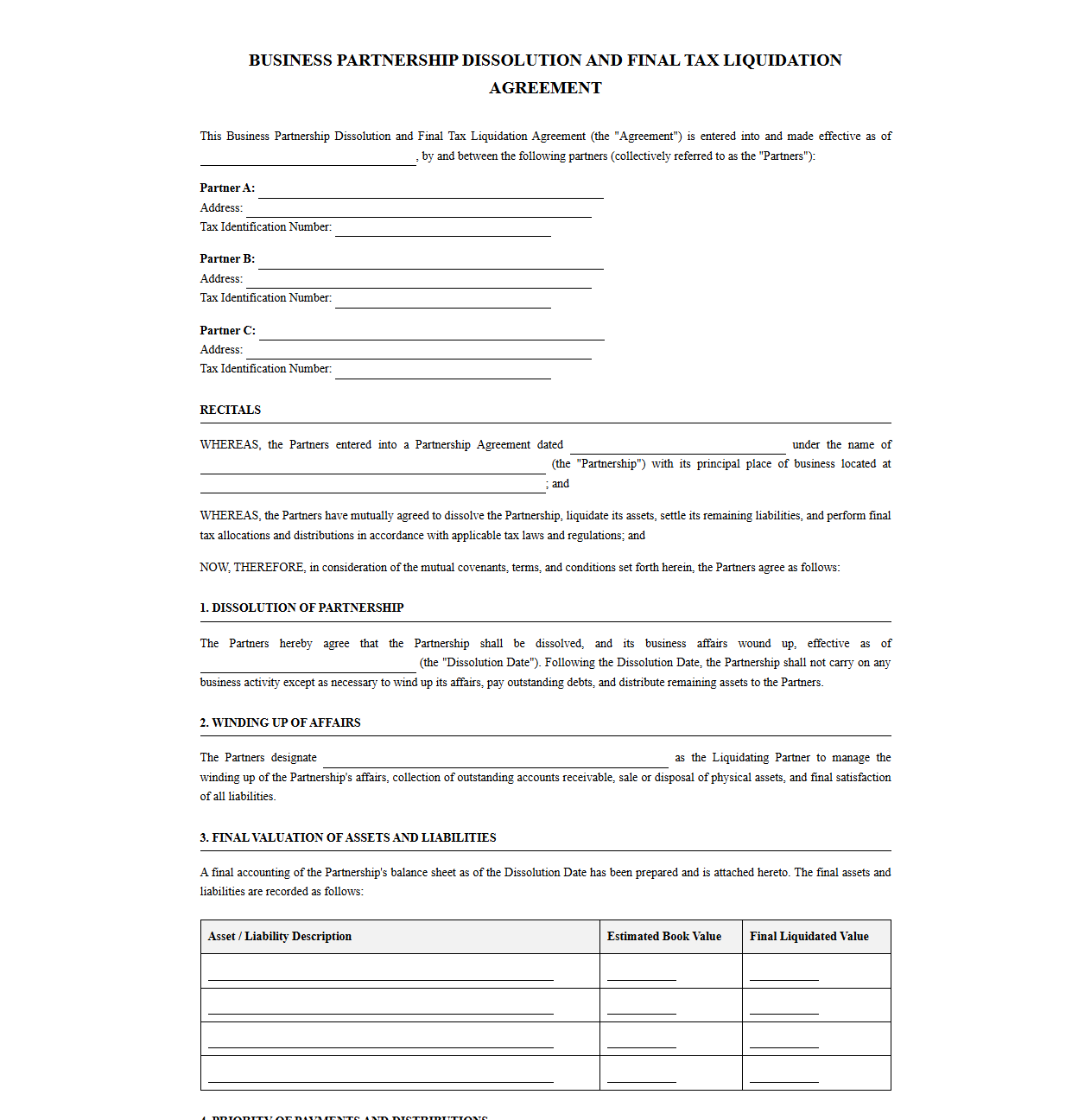

Business Partnership Dissolution and Final Tax Liquidation Agreement

Download: .PDF

Download: .PDF

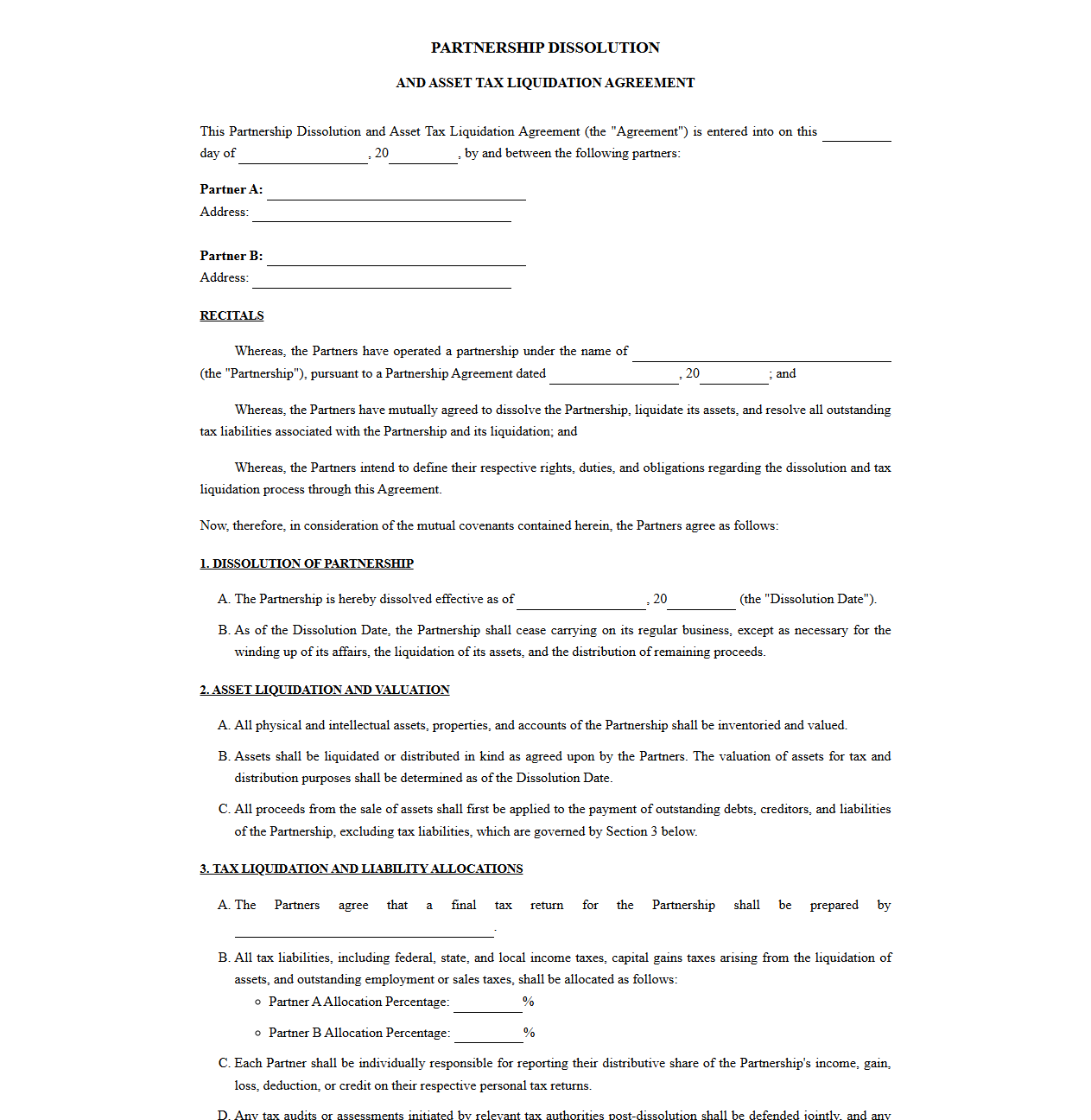

Agreement for Partnership Dissolution and Asset Tax Liquidation

Download: .PDF

Download: .PDF

Understanding the Landscape of Partnership Dissolution

Winding down a business partnership is rarely a simple walk away. It is a highly sensitive transition filled with emotional complexities and intense legal hurdles. When partners decide to part ways, years of shared effort, financial codependency, and mutual dreams must be carefully unraveled. Without a clear path forward, the process can quickly devolve into costly litigation and permanently damaged relationships.

To navigate this transition smoothly, partners must rely on structured legal agreements. These formal documents act as a roadmap, ensuring that every financial obligation, intellectual property right, and physical asset is addressed. By establishing clear terms before the final split, business owners can protect their personal interests and preserve their professional legacies.

Demystifying the Tax Liquidation Agreement

While a standard dissolution agreement focuses on ending the business relationship, a tax liquidation agreement specifically targets the winding down of the entity's financial structure. Its primary purpose is to outline exactly how the partnership's assets will be liquidated and how the resulting tax consequences will be shared among the partners.

A tax liquidation agreement acts as a legally binding bridge between the operational shutdown of a company and its final tax reporting requirements.

The key difference lies in the scope. A standard dissolution agreement handles the broad strokes of ending the entity, such as operational termination and public announcements. In contrast, the tax liquidation agreement is a highly technical document focused on tax basis adjustments, capital accounts, and ensuring that the internal revenue service receives accurate final filings.

Essential Components of a Dissolution Template

A robust dissolution template protects all parties involved by clearly defining the terms of the separation. Without these specific clauses, partners risk facing unexpected liabilities long after the business has closed its doors.

To ensure a comprehensive separation, the template must contain several critical provisions:

- Debt Allocation: Defining who is responsible for outstanding business loans, vendor lines of credit, and lease agreements.

- Asset Division: A clear breakdown of how physical inventory, intellectual property, and liquid cash will be distributed.

- Release of Liability: A clause that releases each partner from future claims related to the business operations once the dissolution is complete.

Navigating Tax Liabilities and IRC Compliance

The liquidation of a partnership triggers significant tax implications that require careful planning. Partners must navigate complex rules regarding capital gains and losses when assets are distributed. The tax consequences often depend heavily on each partner's unique tax basis in the partnership.

Compliance with the Internal Revenue Code (IRC) is non-negotiable during this process. Specifically, transactions must adhere to Section 731, which governs the recognition of gain or loss on distribution of partnership property. Additionally, partners must carefully calculate their outside basis to avoid unexpected tax liabilities, ensuring all distributions align with Section 704(b) regulations concerning substantial economic effect.

Equitable Asset Valuation and Distribution Methods

Before any assets can be distributed, the partnership must establish an accurate and objective valuation of its holdings. This includes tangible property, such as machinery and real estate, as well as intangible assets like brand equity and proprietary software. Legal methodologies ensure that these valuations are fair and legally defensible.

- First, secure independent, certified appraisals for all physical and intellectual property to establish fair market value.

- Next, settle all outstanding creditor claims and business debts using the partnership's liquid cash reserves.

- Finally, distribute the remaining assets to partners in accordance with their capital account balances and the percentage of ownership outlined in the partnership agreement.

Customizing Templates for Your Specific Business Structure

No two businesses are identical, which means cookie-cutter templates are rarely sufficient. The legal and tax responsibilities of your entity depend heavily on its structure. You must tailor your dissolution documents to fit your specific entity type to ensure legal compliance. For instance, you can find specialized business dissolution templates online to use as a starting point.

For Limited Liability Partnerships (LLPs), the focus is often on protecting partners from joint liability for professional malpractice. In a Limited Liability Company (LLC), the dissolution must align with the operating agreement and state-specific LLC statutes. For General Partnerships, where liability is joint and several, the agreement must be incredibly precise regarding debt division to prevent one partner from bearing the entire financial burden.

Executing the Agreement and Final Filings

Once the agreement is drafted and agreed upon, the final phase of partnership dissolution begins. This step requires precise execution to ensure the business is formally and legally closed in the eyes of the law. Partners must sign the final agreement, signaling their mutual consent to the terms of the wind-down.

With the signed agreement in hand, you must file formal articles of dissolution with your state's Secretary of State office. This officially ends the business entity's legal existence. Additionally, the partnership must submit its final tax returns to federal and state authorities, checking the "final return" box to close out the tax accounts forever.

Leave a comment