Navigating the complexities of partnership tax basis adjustments often leaves partners and financial officers grappling with compliance anxiety and potential internal disputes. As partnerships naturally evolve through ownership transfers or asset distributions, maintaining equity while satisfying stringent IRS regulations requires precise, formal documentation. Our professional agreement templates grant you the structural clarity and legal safeguarding needed to execute these adjustments with absolute confidence.

Please note: while these resources establish a rigorous operational foundation, they are designed to assist-rather than substitute for-direct consultation with a qualified CPA or tax attorney. Specifically, we examine how to document critical scenarios such as Section 743(b) optional basis adjustments and Section 734(b) undistributed property distributions to prevent future tax liabilities.

In this article, we will unpack the essential clauses your documents must contain, outline the differences between adjustment types, and provide customizable templates to streamline your partnership compliance workflow.

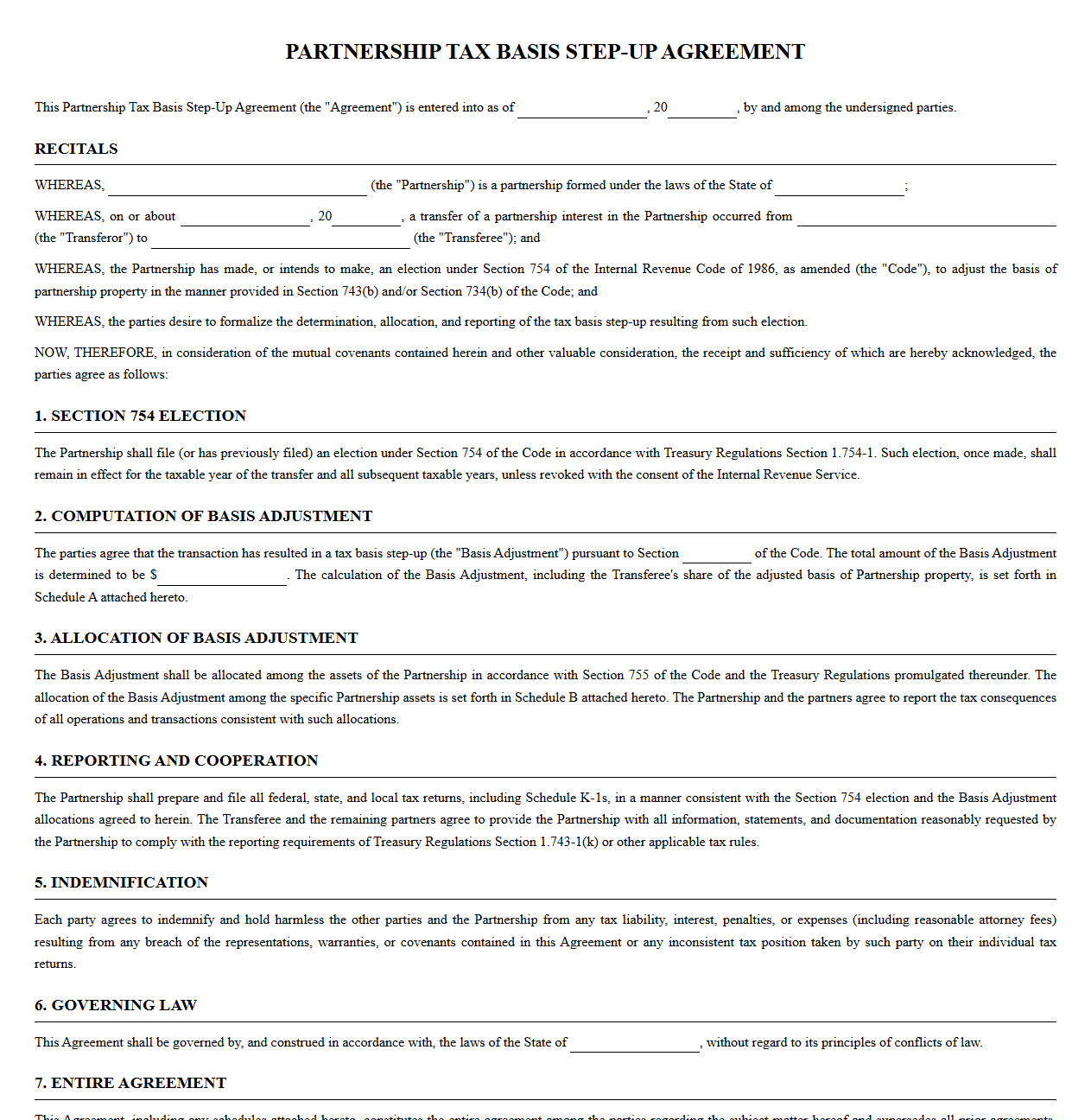

Partnership Tax Basis Step-Up Agreement Template

Download: .PDF

Download: .PDF

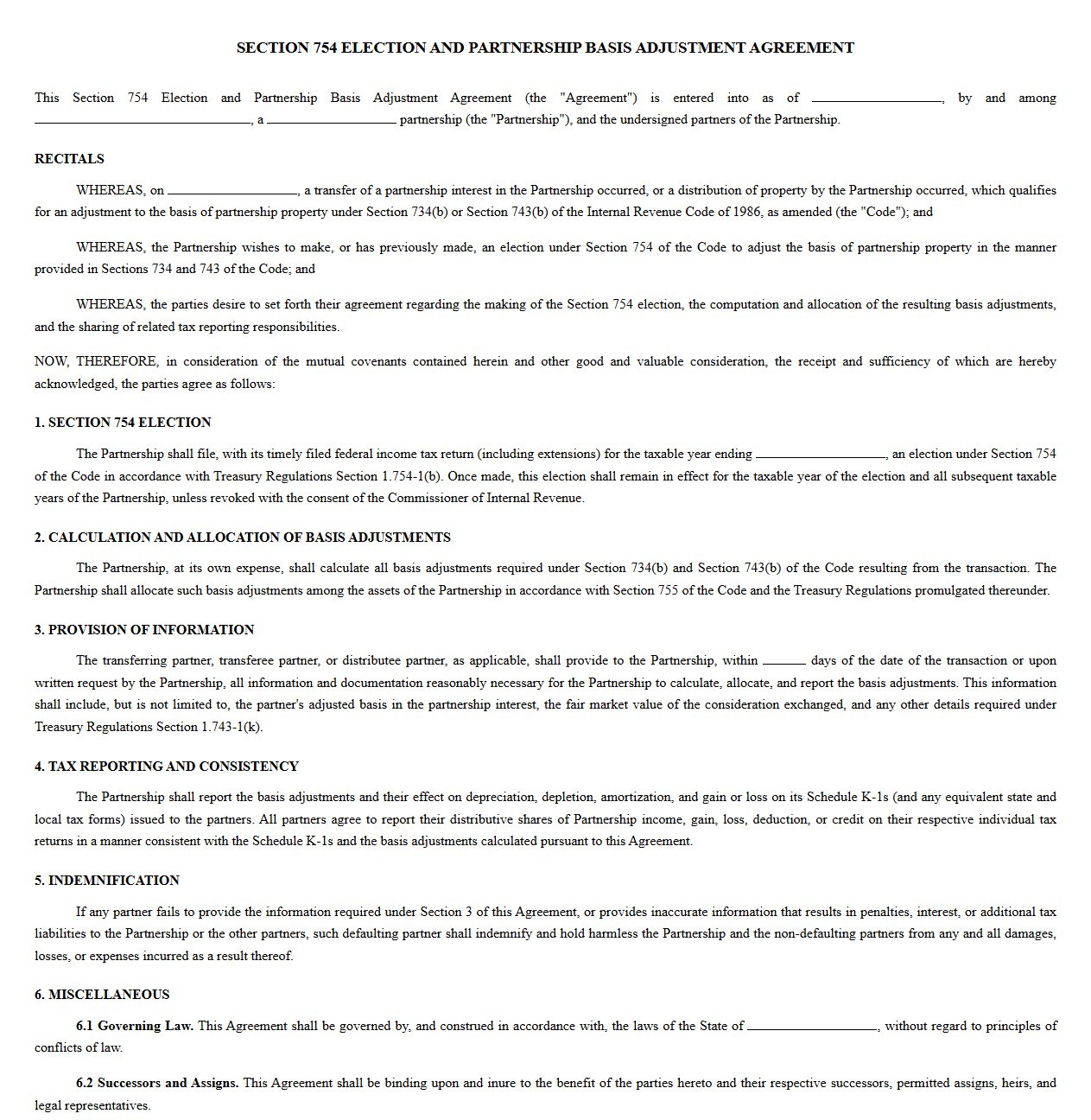

Section 754 Election Partnership Basis Adjustment Agreement

Download: .PDF

Download: .PDF

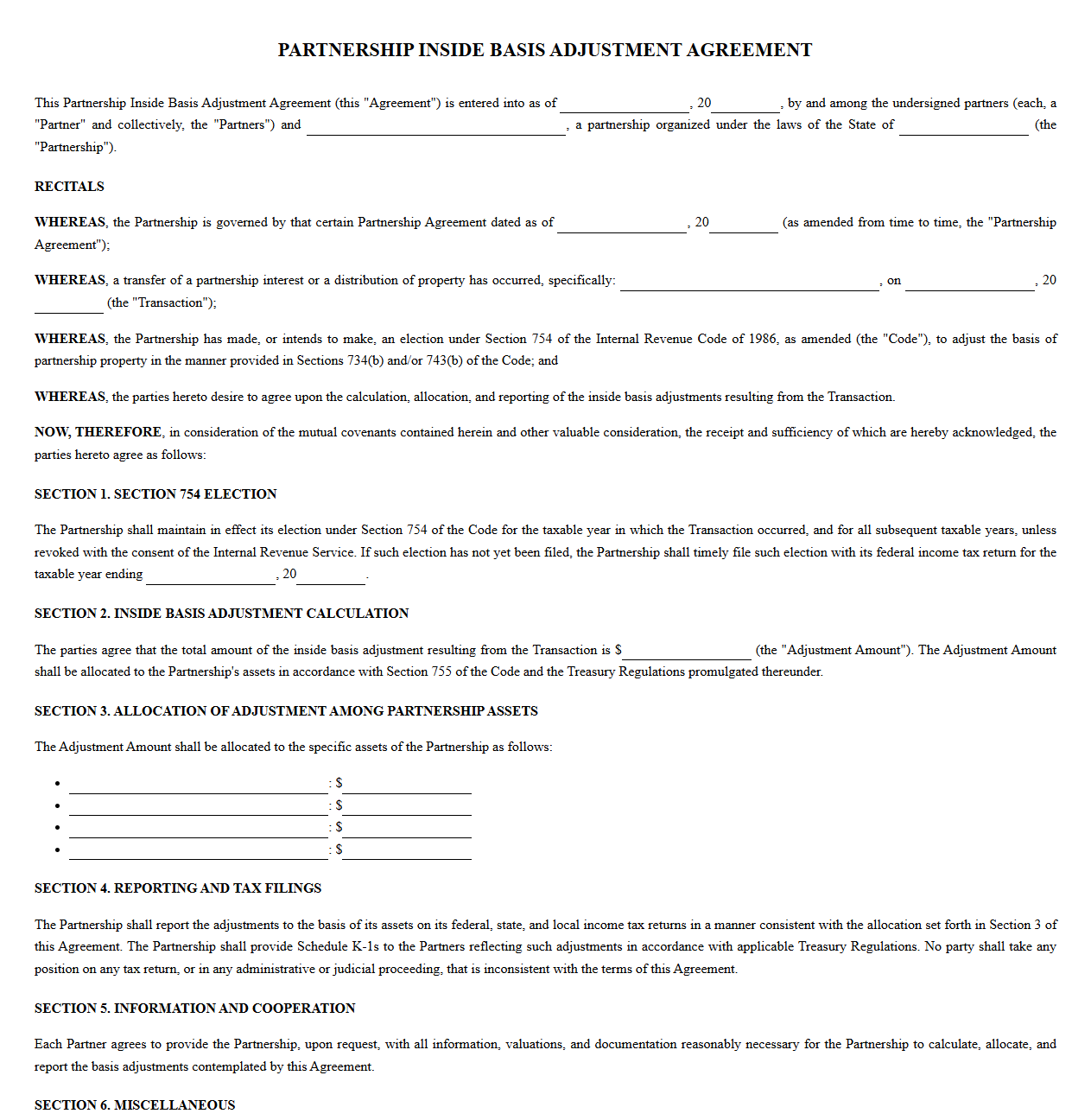

Partnership Inside Basis Adjustment Agreement Template

Download: .PDF

Download: .PDF

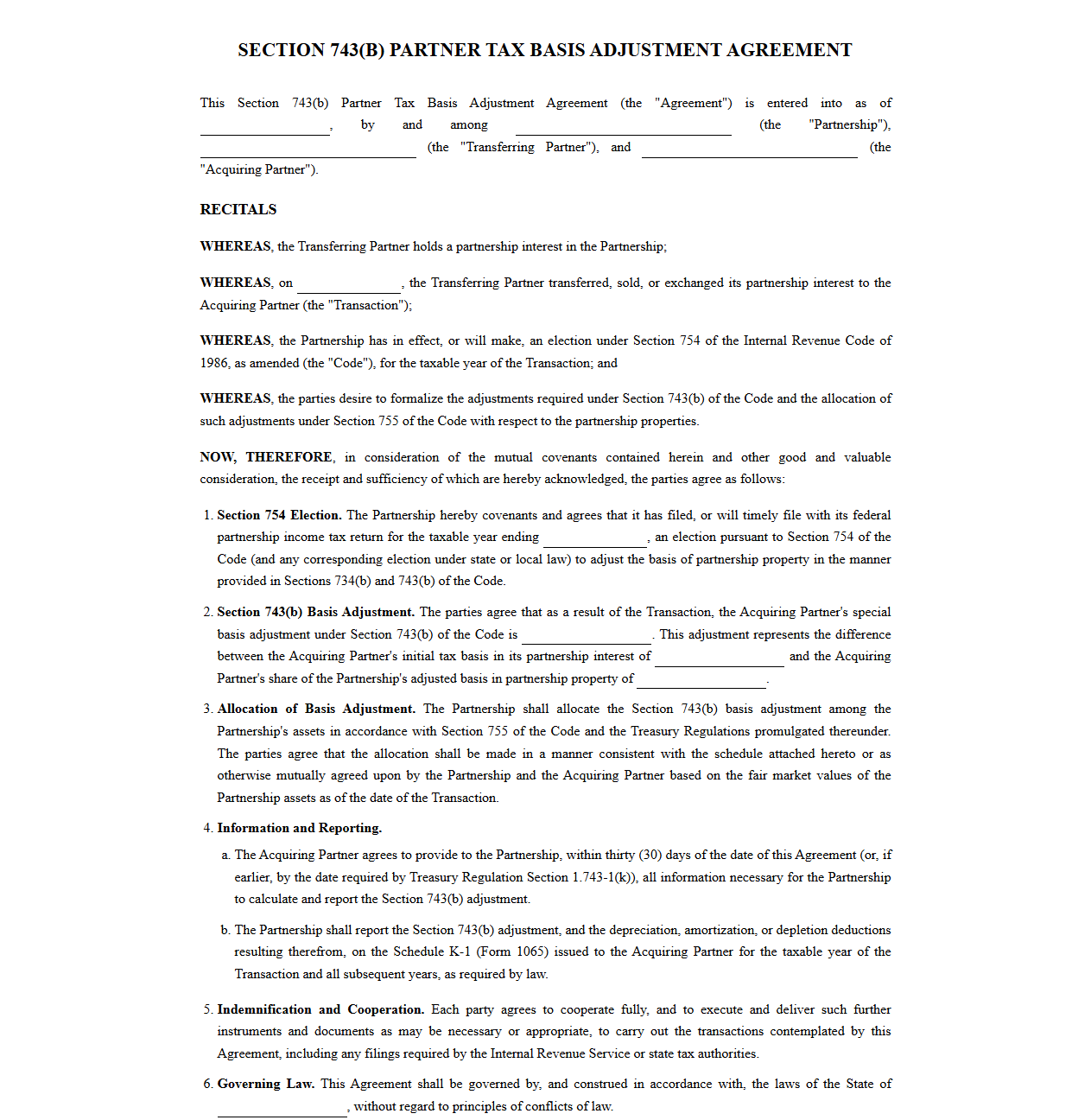

Section 743b Partner Tax Basis Adjustment Agreement

Download: .PDF

Download: .PDF

Partnership Tax Basis Revaluation Agreement Template

Download: .PDF

Download: .PDF

Section 734b Partnership Basis Adjustment Agreement

Download: .PDF

Download: .PDF

Partner Capital Account Basis Adjustment Agreement

Download: .PDF

Download: .PDF

Partnership Tax Basis Allocation and Adjustment Agreement

Download: .PDF

Download: .PDF

Understanding Partnership Tax Basis Adjustments

Navigating the complexities of partnership taxation requires a deep understanding of how partner-level and partnership-level tax attributes interact. At the center of this dynamic is the concept of tax basis adjustments, which ensure that partners are not subjected to double taxation or permitted to claim duplicate deductions. A pivotal mechanism in this arena is Internal Revenue Code Section 754, which allows partnerships to adjust the basis of partnership property when a partnership interest is transferred or when partnership property is distributed.

Implementing a Section 754 election can significantly benefit partners by aligning their inside basis (the partnership's basis in its assets) with their outside basis (the partner's basis in their partnership interest). However, because these adjustments are permanent and require sophisticated tracking, having standardized agreement templates is critical. These templates ensure strict tax compliance, establish clear administrative procedures, and maintain partner harmony by pre-determining how financial and tax discrepancies will be resolved.

The Role of the Partnership Agreement in Tax Allocations

The partnership agreement functions as the foundational legal document governing all financial and administrative aspects of the venture. Within this document, provisions outlining capital accounts maintenance rules dictate how economic activities are tracked. Specifically, to comply with Treasury Regulations, the agreement must outline how the partnership maintains capital accounts in accordance with Section 704(b) guidelines, which directly impact how basis adjustments are recognized and allocated among the partners.

Without clear language governing these allocations, a partnership risks triggering IRS audits and disputes over the substantial economic effect of its tax allocations. Standardized templates embed these complex rules directly into the organizational framework, ensuring that the partnership's tax reporting matches the actual economic arrangements of the partners. By explicitly defining these parameters, the agreement establishes a legally binding roadmap for compliance that shields the entity from administrative disruption.

Essential Clauses for Section 754 Election Templates

To ensure a Section 754 election is executed correctly and remains legally binding, specific clauses must be built into the partnership agreement template. These clauses outline the triggers for the election and the formal steps the partnership must take to notify the IRS.

An effective Section 754 template should contain the following essential clauses:

- The Election Clause: Explicit language stating that the partnership shall make an election under Section 754 of the Internal Revenue Code, which remains in effect for the taxable year and all subsequent taxable years unless revoked with IRS consent.

- Trigger Event Provisions: Clearly defined events that mandate or permit the election, such as the transfer of a partnership interest via sale, exchange, or the death of a partner, as well as specific distributions of partnership property.

- Administrative Delegation: Provisions authorizing the tax matters partner or partnership representative to execute and file the necessary statement with the partnership's timely filed federal income tax return.

- Information Cooperation: A clause requiring transferring partners to promptly provide all necessary information, including the valuation of the transferred interest, to facilitate accurate basis adjustment calculations.

Structuring Section 743(b) Adjustments for Partner Transfers

When a partner transfers their partnership interest through a sale, exchange, or inheritance, Section 743(b) adjustments are triggered, provided a Section 754 election is in place. This adjustment is personal to the transferee partner, ensuring that their share of the partnership's inside basis reflects the purchase price or fair market value of their acquired interest. Properly drafting these provisions requires a structured process for calculating and allocating the basis adjustment.

To manage this process smoothly, the agreement template should outline the following step-by-step allocation procedure:

- Determine the transferee partner's outside basis in the newly acquired partnership interest.

- Calculate the transferee's share of the partnership's common inside basis in its assets.

- Compute the difference between the outside basis and the share of inside basis to establish the total Section 743(b) adjustment amount.

- Allocate the total adjustment between the partnership's two asset classes: ordinary income assets (such as inventory and accounts receivable) and capital gain assets (such as equipment, real estate, and goodwill).

- Distribute the class-specific adjustments among the individual assets within each category to eliminate the variance between the assets' fair market values and their tax bases.

Managing Section 734(b) Adjustments for Property Distributions

Unlike partner-to-partner transfers, Section 734(b) adjustments are triggered by distributions of partnership property to a partner. When a partnership distributes cash or property that results in a gain or loss to the distributee partner, or alters the basis of the distributed property, Section 734(b) adjustments adjust the basis of the remaining partnership assets. This mechanism is vital for preserving equity among the remaining partners, ensuring they do not inherit artificial tax liabilities or lose legitimate tax benefits.

Drafting these clauses requires precise legal terminology to bind the partnership to these necessary asset adjustments. A sample legal clause for property distributions should be structured as follows:

"Upon any distribution of partnership property to a partner that triggers the application of Internal Revenue Code Section 734(b), the partnership shall adjust the adjusted basis of the remaining partnership assets in accordance with said section. Such adjustments shall be allocated among the partnership's assets pursuant to Section 755 and the regulations promulgated thereunder, ensuring that the tax basis of remaining assets reflects the economic realities of the distribution."

Dispute Resolution and Indemnification in Basis Adjustments

Because tax basis calculations involve complex valuations and intricate tax accounting, they are frequent sources of disagreement. An error in calculating a partner's basis adjustment can lead to significant tax discrepancies, resulting in IRS penalties and interest. Incorporating robust dispute resolution and indemnification clauses in tax basis templates protects the partnership from the fallout of calculation errors and filing disputes.

Templates should clearly define indemnification obligations, requiring any partner who provides inaccurate valuation data or causes a tax recalculation to indemnify the partnership for any resulting liabilities. Furthermore, the agreement must establish a dispute resolution process, such as submitting disputed basis calculations to an independent, certified public accounting firm whose determination shall be final and binding. This proactive approach safeguards the partnership's financial stability and keeps administrative workflows moving forward.

Best Practices for Reviewing and Executing Agreement Templates

Maintaining accurate tax basis templates requires ongoing diligence and adaptation. As tax laws evolve and partnerships undergo structural shifts, boilerplate agreements can quickly become outdated, leaving the entity vulnerable to compliance failures.

To keep templates aligned with changing federal tax regulations, tax professionals and partners should adopt the following best practices:

- Conduct Annual Reviews: Regularly review the partnership agreement's tax provisions to ensure compliance with updated IRS regulations and state tax laws.

- Engage Specialized Tax Counsel: Work with experienced tax attorneys and certified public accountants to draft and review Section 754 election clauses.

- Document All Adjustments: Maintain meticulous records of all Section 743(b) and Section 734(b) adjustments, attaching the required schedules to the partnership's annual tax returns.

- Standardize Partner Onboarding: Ensure new partners receive and sign off on the tax basis adjustment clauses during the acquisition of their interest, establishing clear expectations from day one.

Leave a comment