Managing partnership basis adjustments during partner transfers or distributions is notoriously complex, often leading to costly tax inefficiencies and administrative disputes. Before addressing these valuation mismatches, it is critical to understand how the IRS structures partnership taxation under Subchapter K. Fortunately, implementing a Section 754 election grants partnerships the invaluable ability to step up the tax basis of inner assets to match fair market value, instantly eliminating potential double taxation.

However, please note that this election is permanent once executed, requiring precise legal drafting within the partnership agreement rather than treating it as a routine tax filing. For instance, real estate syndicates and multi-member LLCs require distinct, specialized contract clauses to survive audit scrutiny. Below, we provide a comprehensive guide to navigating these complexities, complete with customizable agreement templates tailored for diverse business structures to ensure your next basis adjustment is legally secure.

Partnership Section 754 Election Agreement Template

Download: .PDF

Download: .PDF

LLC Section 754 Tax Election Resolution Template

Download: .PDF

Download: .PDF

Section 754 Election Consent Agreement Template

Download: .PDF

Download: .PDF

Section 754 Election Partnership Agreement Amendment

Download: .PDF

Download: .PDF

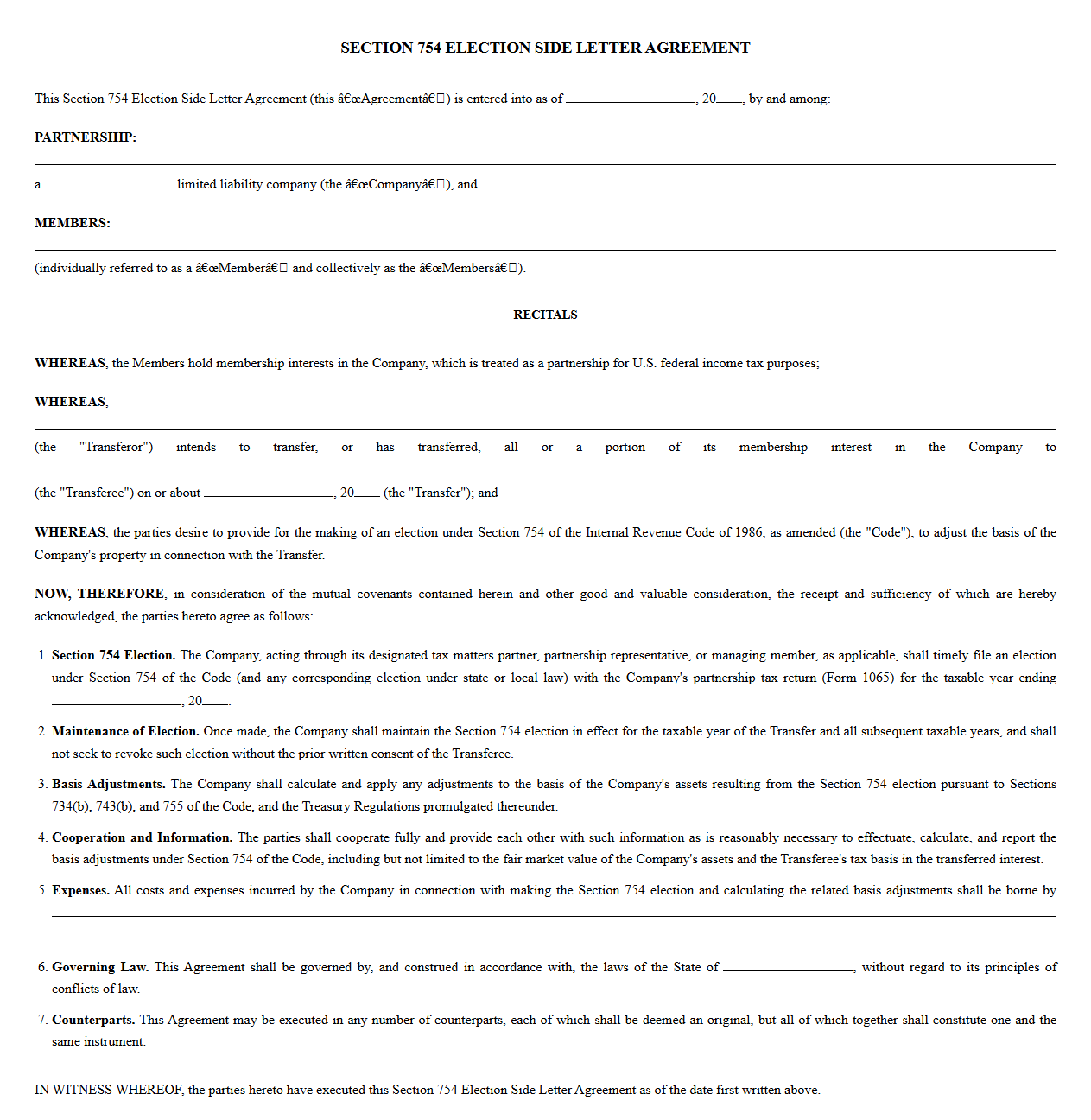

Section 754 Tax Election Side Letter Agreement

Download: .PDF

Download: .PDF

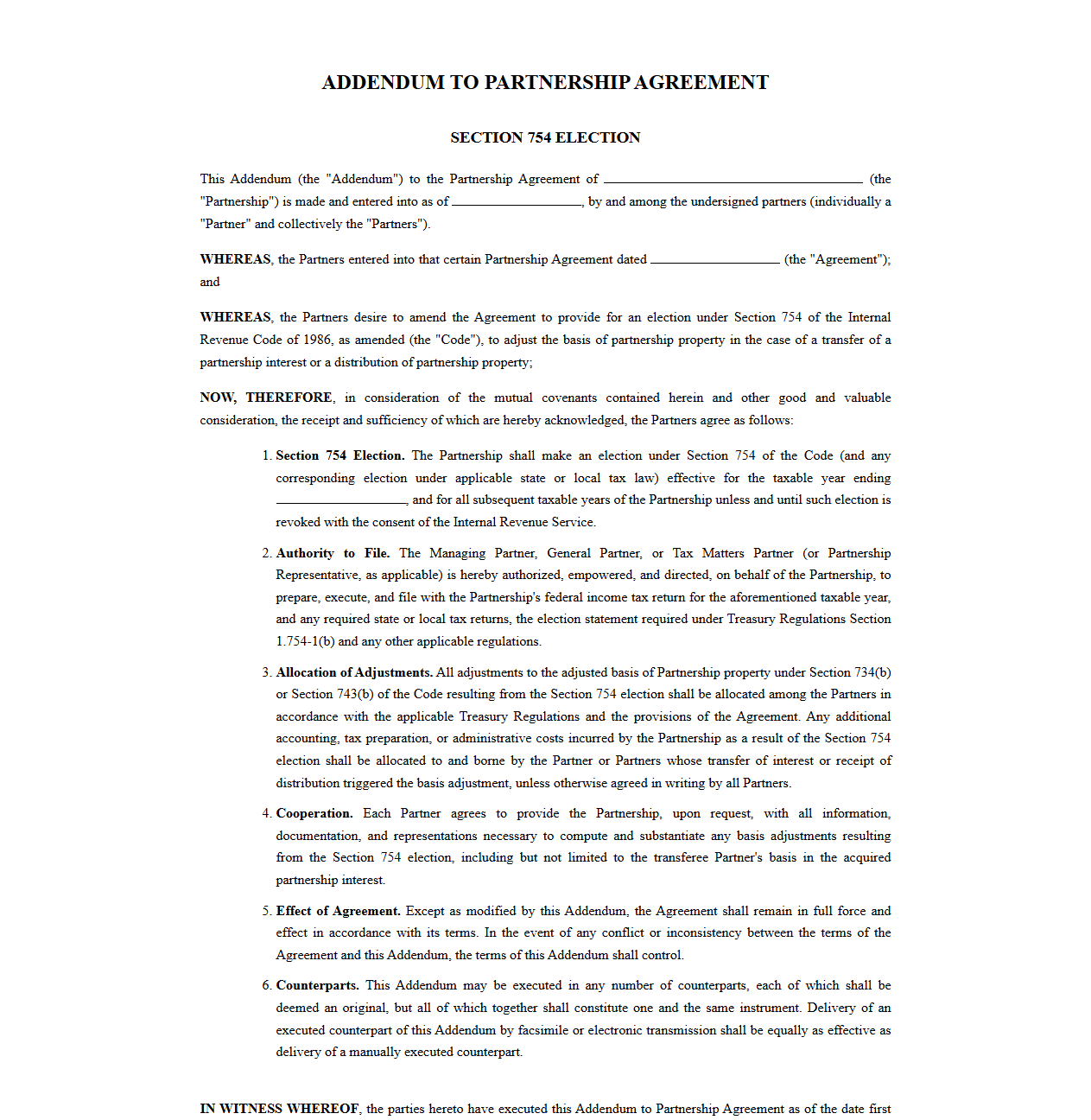

Partnership Agreement Addendum for Section 754 Election

Download: .PDF

Download: .PDF

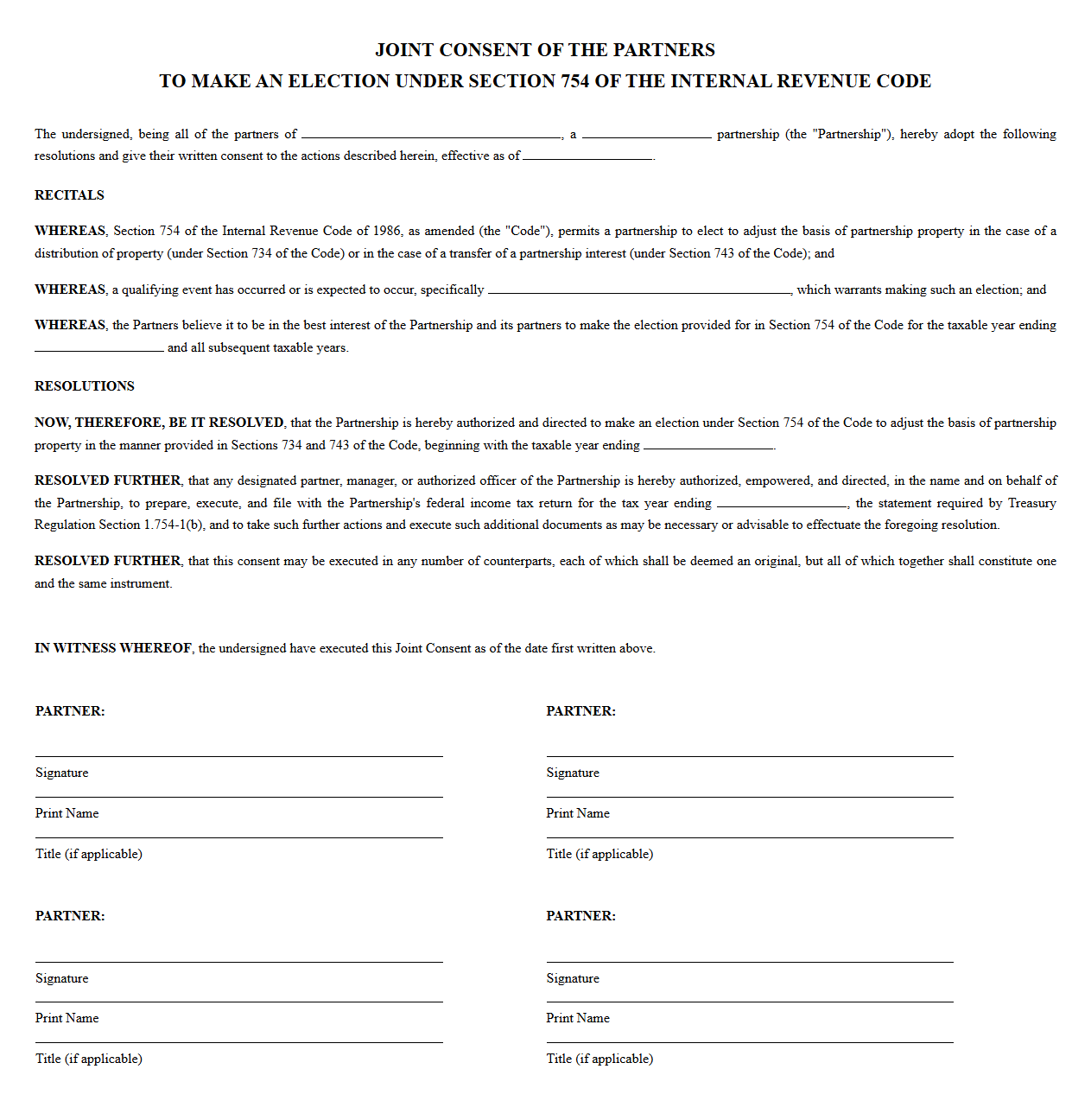

Joint Consent Template for Section 754 Election

Download: .PDF

Download: .PDF

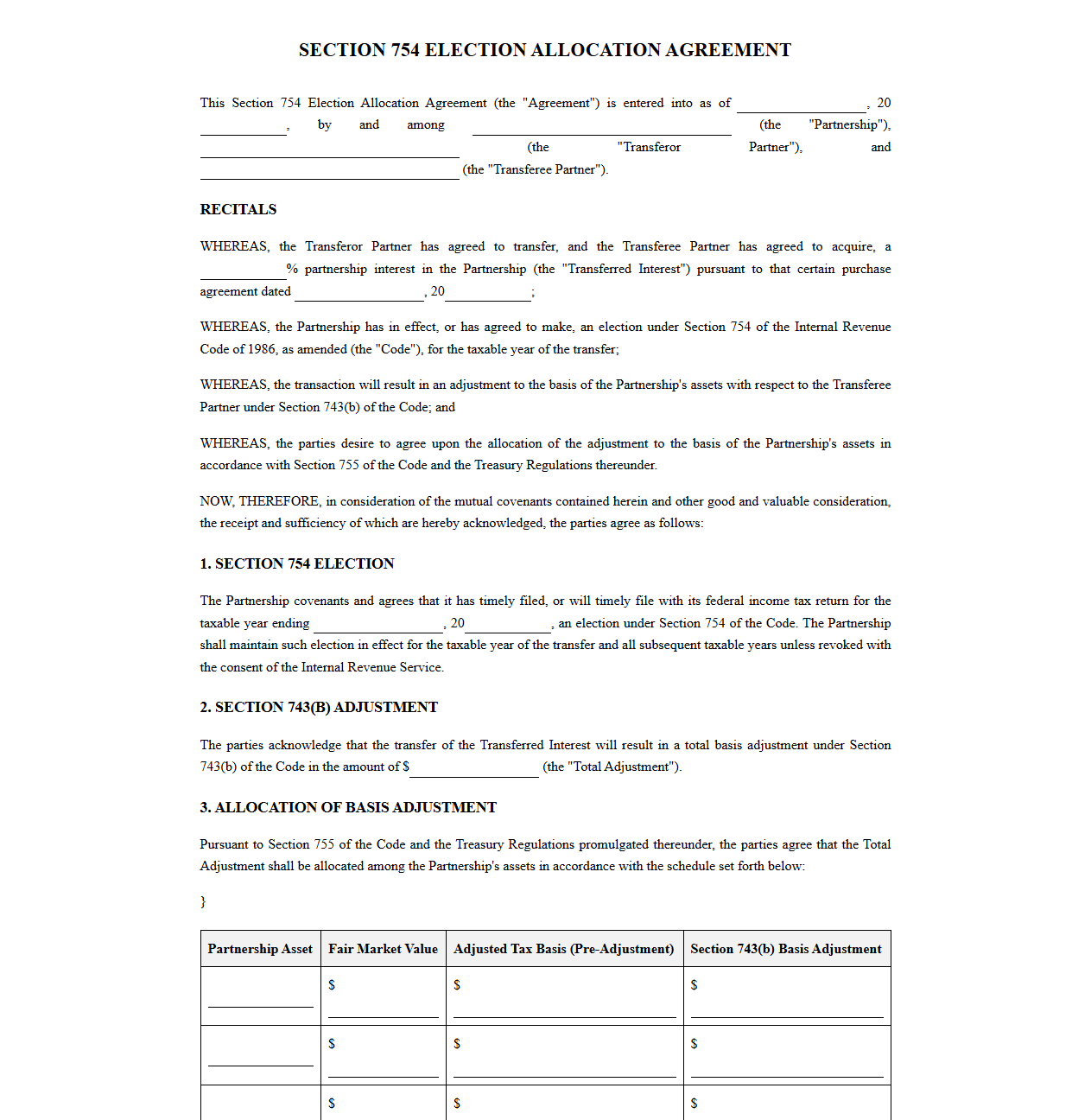

Section 754 Election Allocation Agreement Template

Download: .PDF

Download: .PDF

Understanding Section 754 Elections and Partnership Basis Adjustments

As a tax attorney, I often observe partnerships failing to reconcile the divergence between a partner's inside basis and outside basis. A Section 754 election is a powerful mechanism under the Internal Revenue Code that permits a partnership to adjust the basis of its internal assets when certain events occur. This election serves to align the purchaser's or distributee's economic reality with the partnership's tax accounting, preventing unfair tax burdens.

The primary benefit of this election is realized through Section 743(b) adjustments for incoming partner transfers and Section 734(b) adjustments for property distributions. Without a Section 754 election in place, an incoming partner who purchases an interest at a premium would face double taxation: first, paying for the appreciated value of the underlying assets upon entry, and second, paying tax again when the partnership eventually sells those assets. By utilizing these adjustments, the partnership ensures that tax consequences accurately reflect actual economic gains and losses.

Core Triggers: Partner Transfers vs. Property Distributions

To properly manage a partnership's tax attributes, practitioners must understand the two distinct operational triggers that activate Section 754 basis adjustments.

Section 743(b) Adjustments: Transfers of Partnership Interests

A Section 743(b) adjustment is triggered by the transfer of a partnership interest by sale or exchange, or upon the death of a partner. Key characteristics include:

- Partner-Specific Effect: The basis adjustment benefits or penalizes only the transferee partner, leaving the basis of the other partners unaffected.

- Purchase Price Alignment: It steps up or steps down the transferee partner's share of inside basis to match their outside basis.

Section 734(b) Adjustments: Distributions of Partnership Property

A Section 734(b) adjustment is triggered by a distribution of cash or property to a partner. Key characteristics include:

- Entity-Wide Effect: The adjustment modifies the basis of the partnership's remaining assets, affecting all remaining partners.

- Gain/Loss Recognition: It is triggered when a distributee partner recognizes gain or loss, or when the distributed property's basis changes.

Tailoring Section 754 Agreement Templates for Diverse Business Structures

Different business structures require customized drafting to address their unique asset profiles and operational dynamics.

1. Real Estate Holding LLC Clause

"The Board of Managers shall cause the Company to make and maintain an election under Section 754 of the Code. Any adjustment to the inside basis of Company real property pursuant to Section 743(b) shall be allocated strictly to the acquiring Member, and all associated appraisal and legal fees shall be borne solely by such transferee."2. Multi-Tiered Family Limited Partnership (FLP) Clause

"Upon the transfer of an interest in the Partnership by sale, exchange, or death of a Partner, the General Partner shall timely execute a Section 754 election. The General Partner is authorized to coordinate with any upper-tier or lower-tier partnerships to ensure reciprocal basis adjustments are properly executed under Section 743(b)."3. High-Growth Tech Startup Partnership Clause

"The Partners agree that the Partnership shall not file an election under Section 754 of the Code without the unanimous written consent of the Management Committee. The Management Committee shall evaluate the administrative burden of tracking basis adjustments against the tax benefits prior to granting such consent."Essential Clauses and Valuation Methodologies for the Agreement

When drafting a partnership agreement amendment to govern Section 754 elections, specific protocols must be established to handle costs and valuation methodologies.

Allocation of Costs and Valuation Protocols

- Cost Allocation: The transferee partner must bear all direct expenses, including accounting, valuation, and legal fees, incurred by the partnership to calculate and report the Section 743(b) basis adjustments.

- Valuation Methodology: The fair market value of partnership assets for basis allocation purposes must be determined in accordance with the regulations under Section 755 and Section 1060.

- Independent Appraisal: The partnership will utilize an independent, certified appraiser selected by the general partner to determine the asset values, and the appraiser's findings shall be binding on all parties.

Drafting the Official IRS Section 754 Election Statement

To make a valid Section 754 election, a partnership must attach a written statement to its timely filed Form 1065 tax return (including extensions) for the taxable year in which the transfer or distribution occurs.

Template for the Section 754 Election Statement

SECTION 754 ELECTION STATEMENT [Partnership Name] EIN: [XX-XXXXXXX] Taxable Year Ending: December 31, 2024 Pursuant to Treasury Regulation Section 1.754-1(b), the partnership hereby elects under Section 754 of the Internal Revenue Code of 1986, as amended, to apply the provisions of Section 734(b) and Section 743(b) with respect to transfers of partnership interests and distributions of property. Signed: __________________________ Name: [Authorized Partner/Manager Name] Title: Managing Partner Date: [Date]

Filing Deadlines, Extensions, and Revocation Rules

Timing is critical when executing a Section 754 election. The election must be made in a written statement attached to the partnership's timely filed return (including extensions) for the taxable year in which the transfer or distribution occurs.

Key Administrative Requirements

- The standard deadline: Governed by Treasury Regulation Section 1.754-1(b), the statement must be filed with the Form 1065 for the year the triggering transaction took place.

- Automatic Extensions: Under Section 301.9100-2, partnerships qualify for an automatic 12-month extension from the original due date of the return to file the election, provided they take corrective action promptly.

- Revocation Restrictions: A Section 754 election is binding for all subsequent taxable years unless the IRS grants permission to revoke it. Valid grounds for revocation include a material change in the partnership's business or a substantial increase in administrative burden.

Compliance Best Practices and Pitfalls to Avoid in Basis Adjustments

Maintaining long-term compliance with Section 754 election regulations requires rigorous record-keeping and proactive administration.

Essential Compliance Checklist

- Track Partner-Level Capital Accounts: Maintain rigorous separate partner-level capital accounts under Section 704(b) to reflect transferee-specific basis adjustments correctly over time.

- Monitor Mandatory Negative Adjustments: Be aware that even if a Section 754 election is not made, partnerships may be forced to make mandatory negative basis adjustments under Section 743(d) or 734(d) if there is a substantial built-in loss.

- Coordinate Multi-Tiered Structures: Always ensure that lower-tier partnerships are notified and execute matching elections to preserve the desired tax benefits.

Leave a comment