Managing tax compliance for employer-provided meals can often feel like navigating an administrative minefield. Under Internal Revenue Code Section 119, meals provided for the "convenience of the employer" are excludable from taxable wages, yet proving eligibility to auditing bodies remains a persistent hurdle for corporate finance departments.

By standardizing your substantiation process, you gain peace of mind and insulate your organization against costly tax reclassifications. However, a key stipulation remains: tax-free status is strictly contingent on documenting a valid, non-compensatory business reason for each meal. For instance, maintaining records that prove a meal was provided during a critical emergency IT outage, or due to a restrictive 30-minute lunch window, serves as concrete proof of compliance.

Below, we outline how to utilize structured expense document templates to simplify this workflow, highlighting the essential data fields and policy frameworks required to ensure seamless, audit-ready record keeping.

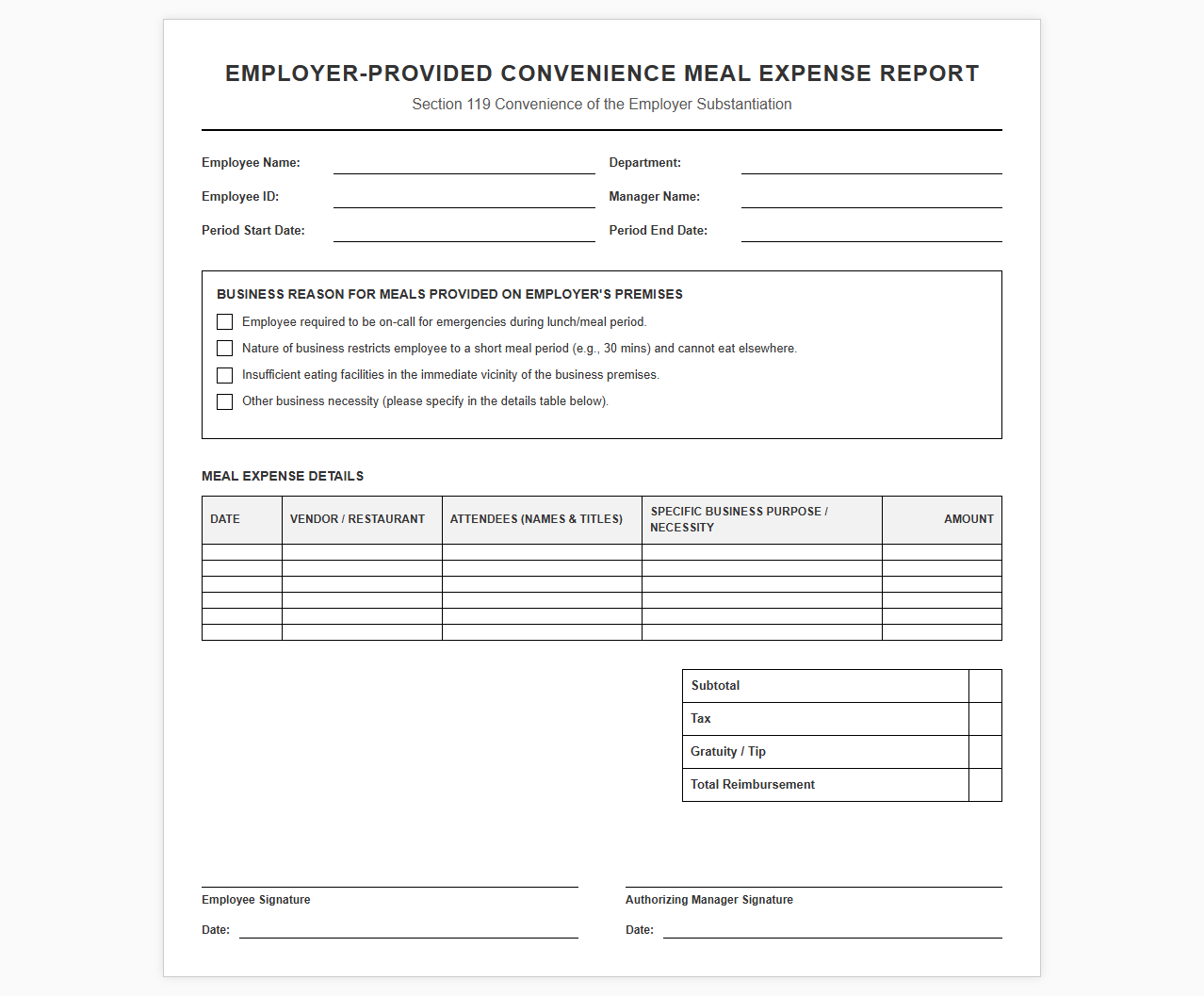

Employer-Provided Convenience Meal Expense Report Template

Download: .PDF

Download: .PDF

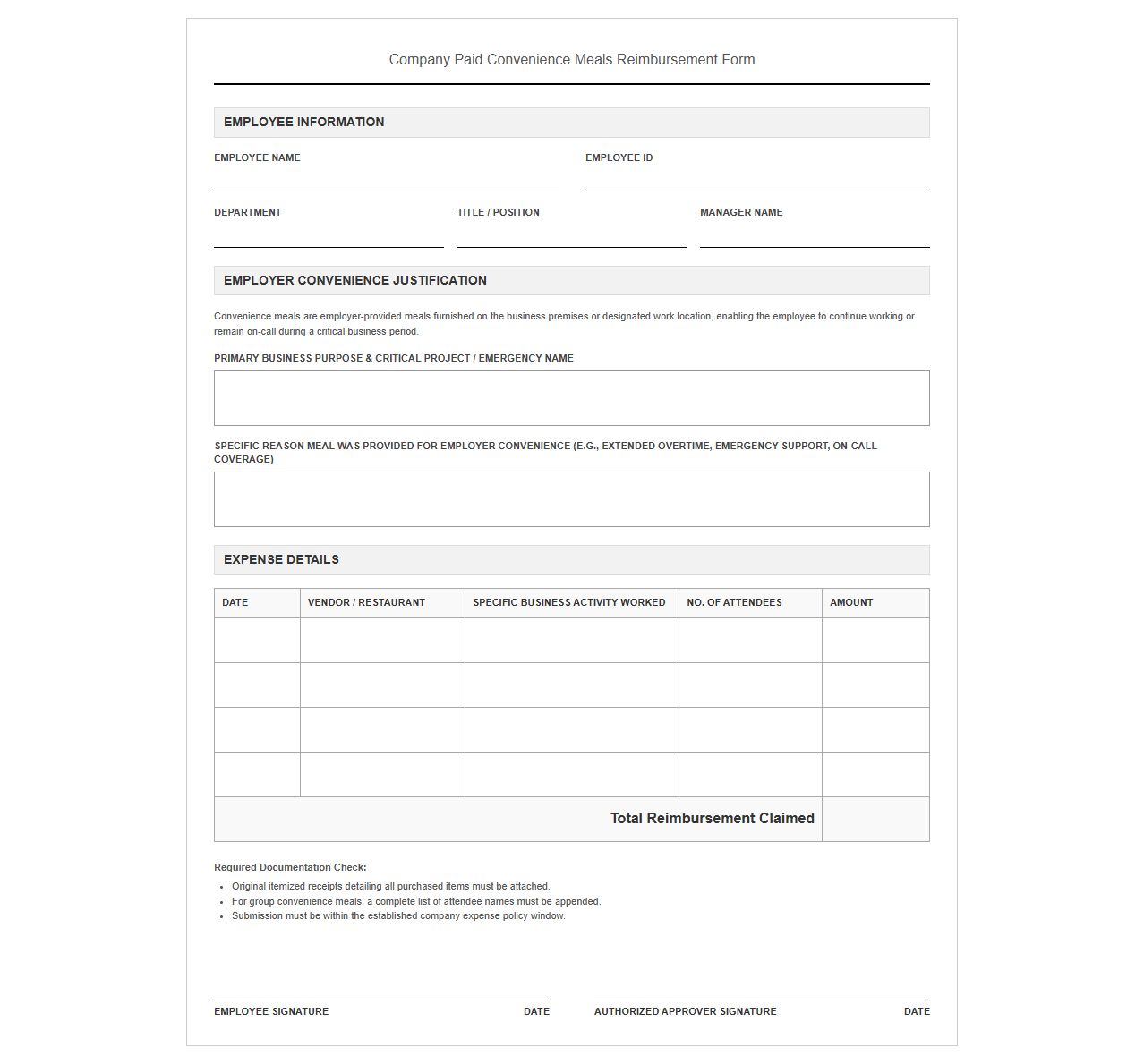

Company Paid Convenience Meals Reimbursement Form

Download: .PDF

Download: .PDF

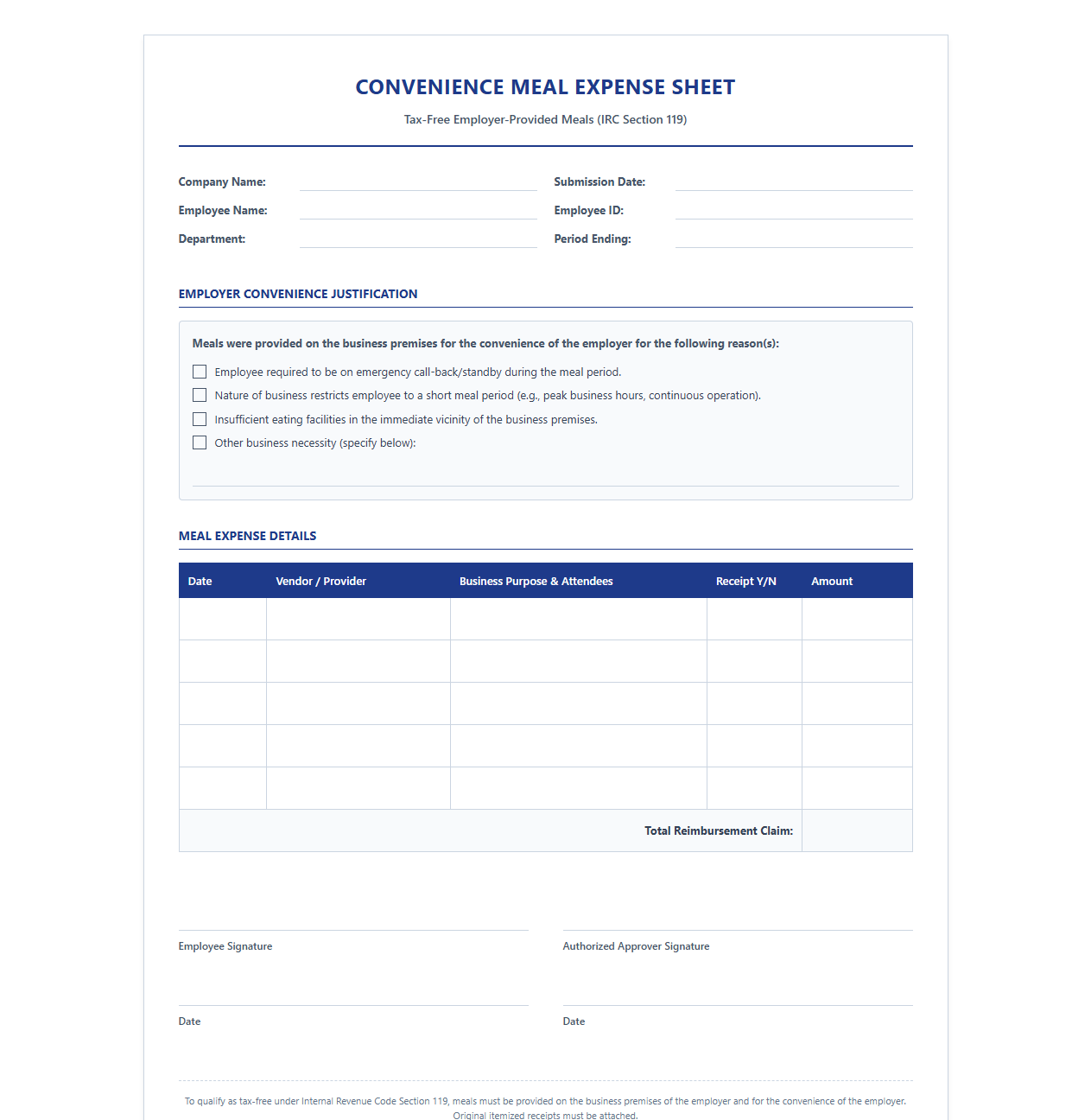

Tax-Free Employer Convenience Meal Expense Sheet

Download: .PDF

Download: .PDF

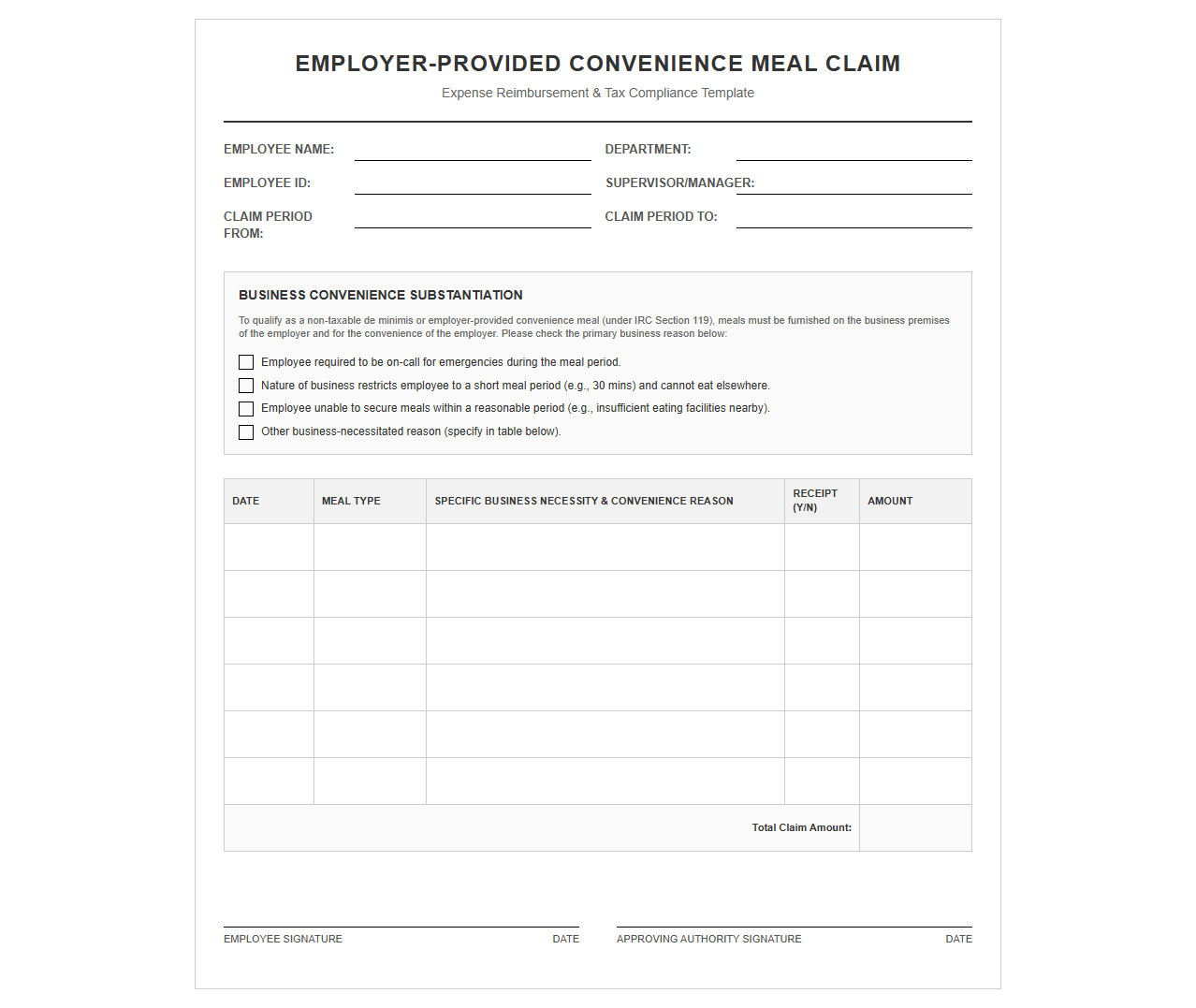

Employer Business Convenience Meal Claim Template

Download: .PDF

Download: .PDF

On-Site Employer Provided Meal Expense Tracker

![]() Download: .PDF

Download: .PDF

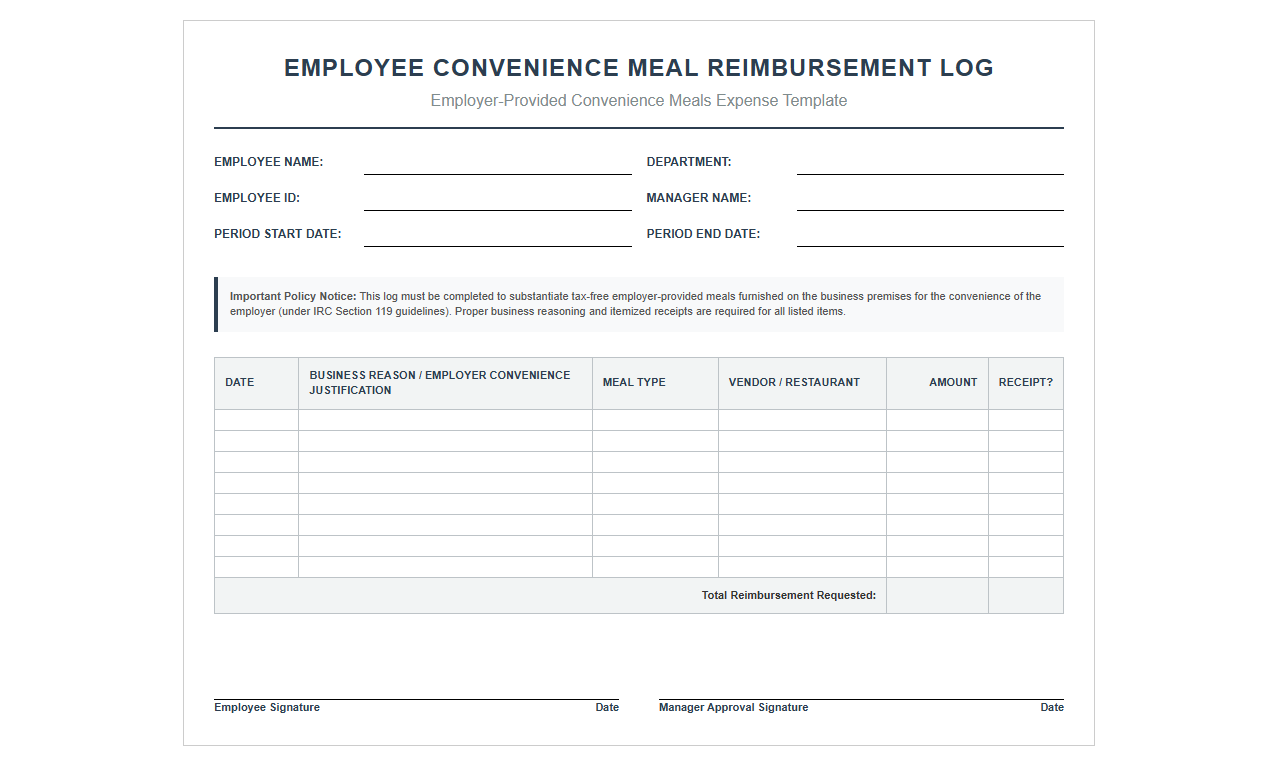

Employee Convenience Meal Reimbursement Log

Download: .PDF

Download: .PDF

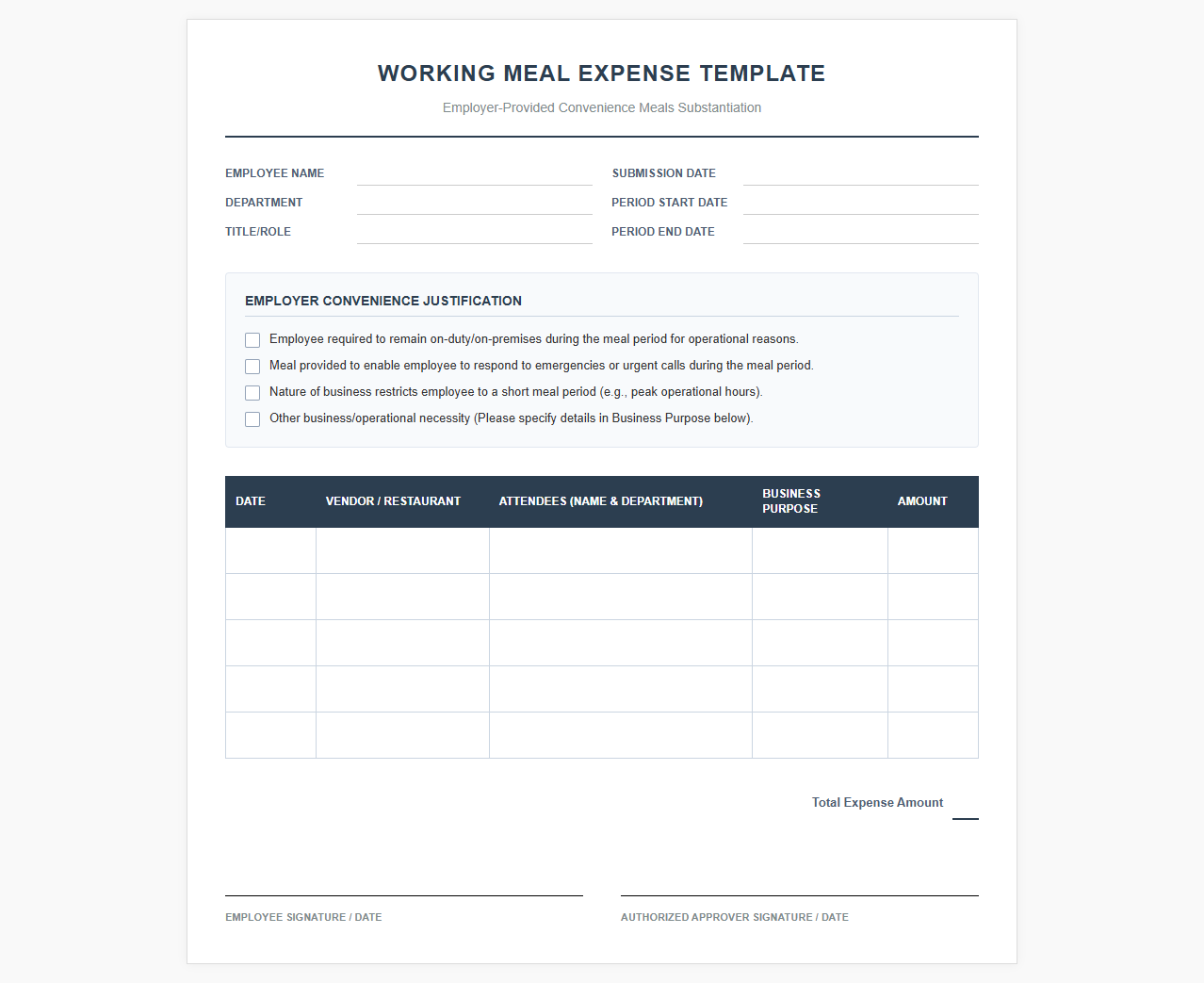

Working Meal Expense Template for Employer Convenience

Download: .PDF

Download: .PDF

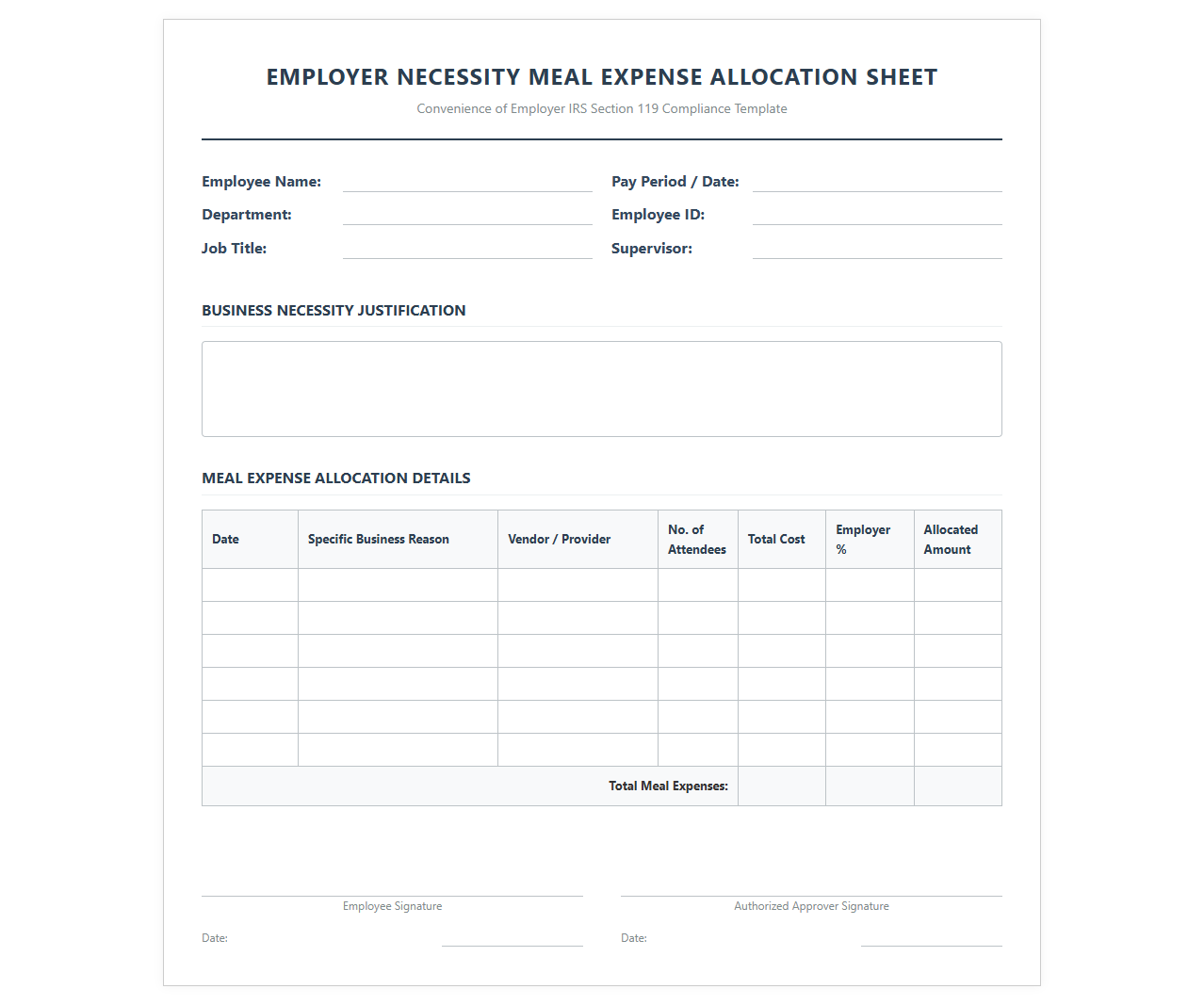

Employer Necessity Meal Expense Allocation Sheet

Download: .PDF

Download: .PDF

Navigating Tax Compliance for Employer-Provided Meals

Providing food to workers can boost morale and maintain workplace productivity, but it also triggers complex IRS scrutiny. To qualify for favorable tax treatment, employer-provided meals must meet strict federal criteria. Without rigorous documentation, these tax-free perks can quickly be reclassified as taxable compensation, leading to back taxes and penalties for both the business and its staff.

The Internal Revenue Service demands clear proof that meals served on business premises serve a legitimate business purpose rather than acting as a disguised form of untaxed pay. Robust recordkeeping is the only defense an organization has during a corporate audit, making standardized expense templates a critical necessity for financial teams.

Decoding the "Convenience of the Employer" Doctrine

Under Internal Revenue Code Section 119, meals provided to employees are excluded from gross income only if they are provided on the business premises of the employer and are furnished for the "convenience of the employer." This legal standard requires a substantial, non-compensatory business reason for offering the food.

"Meals furnished by an employer to an employee shall be excluded from the employee's gross income if the meals are furnished on the business premises of the employer and for the convenience of the employer." Internal Revenue Code Section 119(a)

Acceptable reasons include keeping emergency staff on-call during lunch hours, restricting lunch breaks due to a short peak-business window, or operating in remote locations where alternative dining options are non-existent. Personal preferences or rewarding hard work do not meet this standard.

Essential Data Fields for Your Expense Templates

To withstand IRS scrutiny, every meal document must capture precise transactional and situational data. Generic receipts are insufficient on their own; they must be accompanied by contextual metadata.

- Date and Time: Verifies the meal occurred during active work hours.

- Location: Proves the meal was served on the actual business premises.

- Business Purpose: A detailed narrative justifying the operational necessity of the meal.

- Recipient Names: Lists all employees present to verify eligibility.

- Total Cost: Itemized breakdown to ensure no non-deductible items (like alcohol) are included.

Standardizing the Documentation Workflow

Establishing a uniform procedure ensures that no transaction bypasses the compliance check. This structured workflow guides employees and administrators through the proper verification lifecycle.

- The employee purchases or receives the meal during an eligible shift on-site.

- The employee fills out the standardized expense template, attaching the itemized receipt.

- The department manager reviews the submission to confirm the business purpose aligns with operational needs.

- The finance team cross-references the submission against active tax guidelines and approves or rejects the claim.

- The approved documentation is archived in a centralized database for long-term record retention.

Digital vs. Paper Templates: Best Practices for Storage

While paper forms were once the industry standard, modern tax administration heavily favors digital systems due to the strict record retention windows mandated by tax authorities.

| Compliance Feature | Paper Templates | Digital Templates |

|---|---|---|

| Audit Readiness | Slow manual retrieval, high risk of physical loss | Instant searchability by date, employee, or department |

| Data Integrity | Faded ink, hand-written errors, missing receipts | Immutable digital trails, mandatory field enforcement |

| Storage Security | Requires physical cabinets, vulnerable to fire/water | Encrypted cloud storage with automatic backups |

Red Flags: Common Errors in Meal Expense Claims

Audit failures frequently stem from preventable mistakes in administrative oversight. One of the most common errors is documenting lump-sum totals without providing itemized breakdowns. The IRS requires itemization to confirm that unallowable charges are not blended into legitimate claims.

Another frequent issue is using vague business descriptions such as "working lunch" or "team food" without explaining the exact operational necessity. Without specific context, auditors will quickly disallow the exclusion and reclassify the meals as taxable wages.

Future-Proofing Your Corporate Meal Policies

Tax regulations and workplace environments are constantly evolving, particularly with the rise of hybrid and remote working arrangements. Corporate policies must remain agile to prevent compliance gaps from developing as the workforce distributes.

Regular training sessions for the accounting department and clear communication of policy updates to staff will safeguard your business against future regulatory adjustments.

Leave a comment