For many business owners and accountants, keeping track of daily transactions is a constant struggle, often resulting in costly entry errors, unbalanced books, and tax-season anxiety. Before implementing complex software, however, establishing a structured framework is essential, as even the most advanced systems rely on the fundamental principles of double-entry bookkeeping.

Utilizing standardized general journal ledger templates grants your organization immediate financial clarity and operational control. While these tools significantly streamline the recording process, it is important to note they are designed to organize financial data, not replace basic accounting oversight. A reliable template must include precise structural elements-such as dedicated columns for transaction dates, account titles, debits, and credits-to guarantee every entry is accurately balanced.

In this guide, we will analyze the top general journal ledger templates, discuss how to integrate them into your workflow, and share best practices for maintaining flawless financial records.

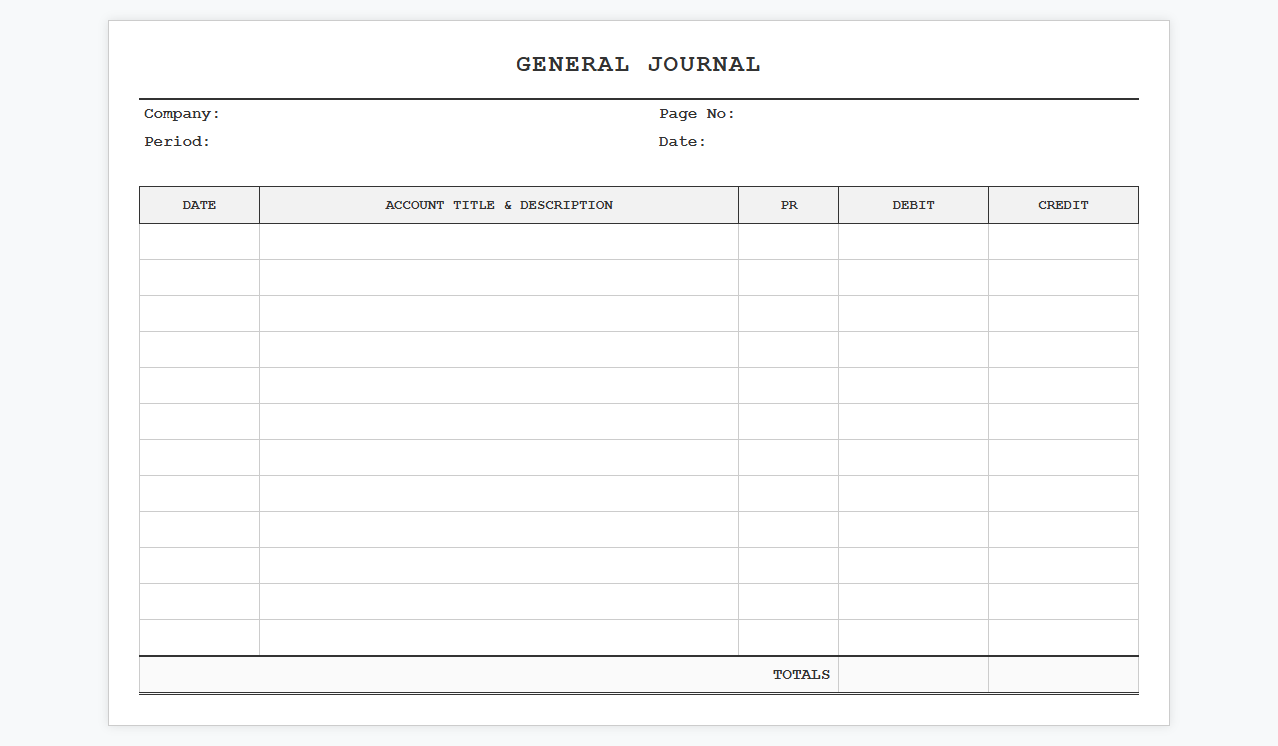

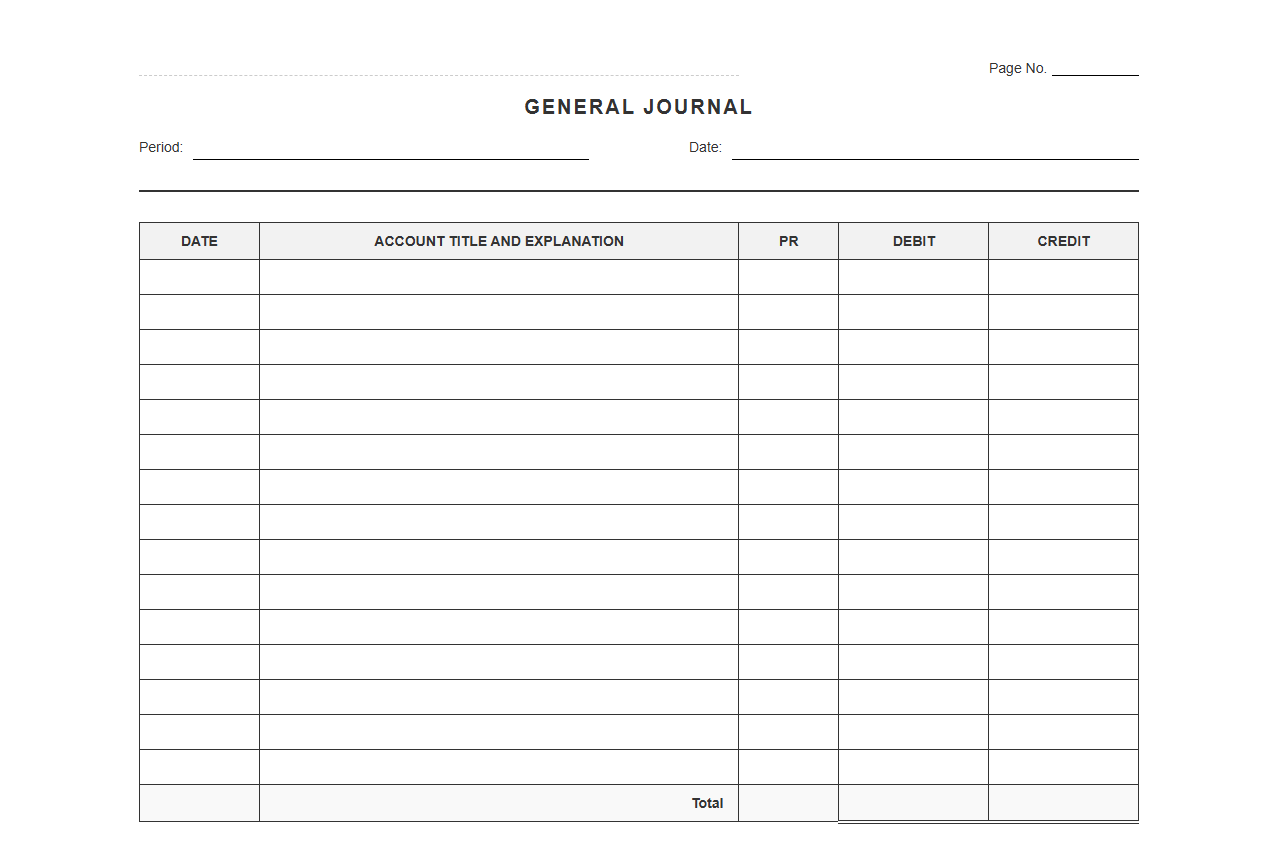

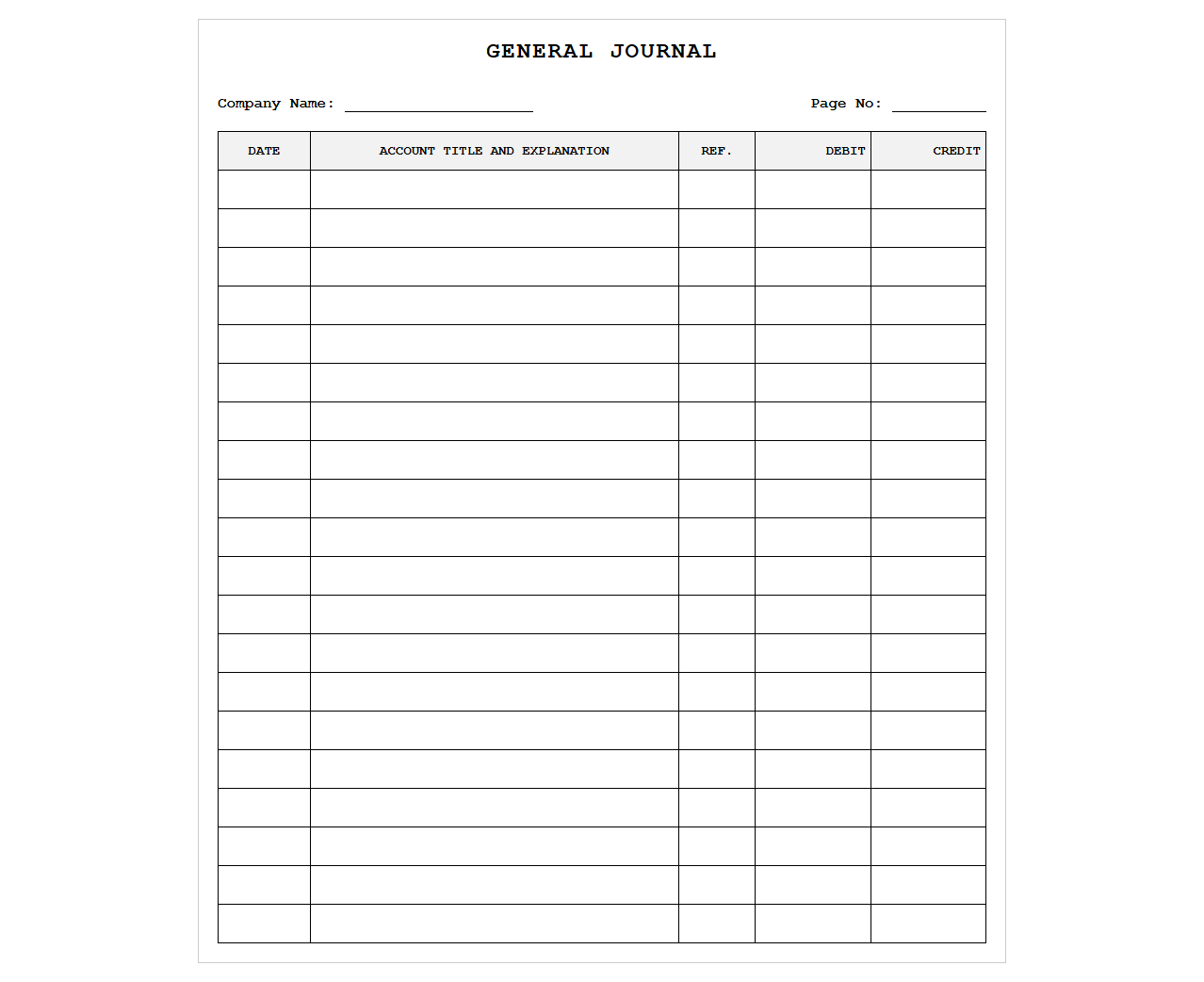

General Journal Ledger Template

Download: .PDF

Download: .PDF

Double-Entry Journal Ledger Sheet

Download: .PDF

Download: .PDF

Accounting Journal and General Ledger Template

Download: .PDF

Download: .PDF

Standard General Ledger Journal Entry Book

Download: .PDF

Download: .PDF

Financial Journal Entry Ledger Spreadsheet

Download: .PDF

Download: .PDF

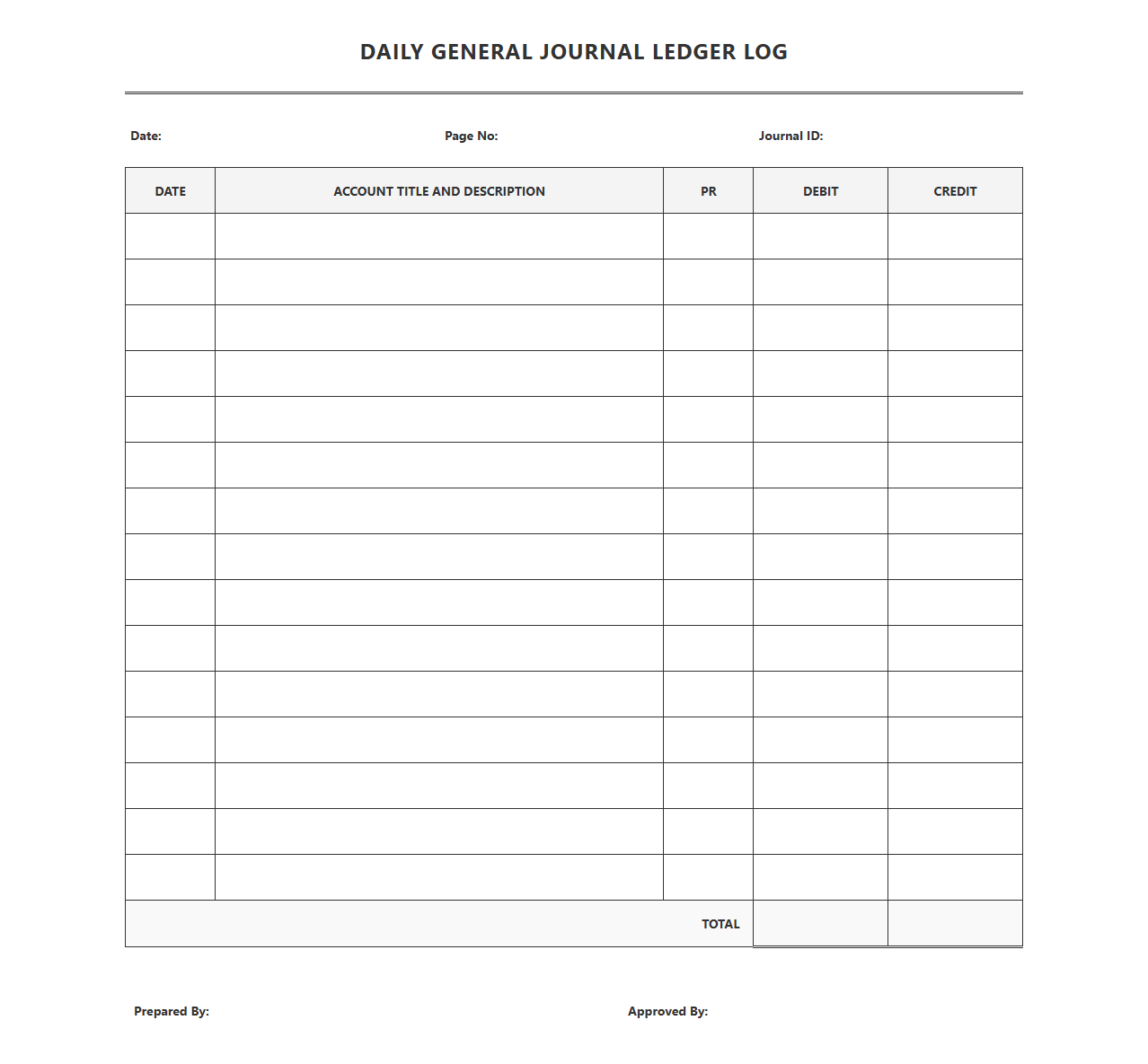

Daily General Journal Ledger Log

Download: .PDF

Download: .PDF

Business Journal Entry Ledger Format

Download: .PDF

Download: .PDF

Bookkeeping General Journal Ledger Template

Download: .PDF

Download: .PDF

The Foundation of Double-Entry Bookkeeping: Understanding the General Ledger

In the world of business finance, keeping an flawless track record of every transaction is not just a regulatory necessity; it is the cornerstone of strategic growth. At the heart of this financial architecture lies the general journal ledger. This master document acts as the central repository for all financial data, consolidating information from various sub-ledgers to provide a comprehensive view of an organization's financial health. Whether you run a budding startup or a multinational corporation, understanding this tool is crucial for maintaining accurate financial records.

Every transaction a business makes-from buying office supplies to receiving client payments-leaves a footprint. The general ledger organizes these footprints into specific accounts, categorized as assets, liabilities, equity, revenues, and expenses. By utilizing a double-entry bookkeeping system, where every debit has a corresponding credit, the ledger ensures that the fundamental accounting equation remains balanced. Maintaining this balance is absolutely essential for generating reliable financial statements that investors, creditors, and tax authorities can trust.

Anatomy of an Effective General Journal Ledger Template

To keep financial records organized, businesses rely on structured templates. A standard general journal ledger template contains several critical columns that capture the who, what, and when of every financial event. Without these core elements, tracking the origin of funds or analyzing spending patterns becomes nearly impossible.

An effective ledger template must include the following essential columns:

- Date: The exact day, month, and year when the transaction occurred, which is vital for maintaining a chronological audit trail.

- Account Name/Description: The specific account being affected (such as Cash, Accounts Receivable, or Rent Expense) along with a brief description of the transaction.

- Reference Number: A unique identifier, such as an invoice number or check number, linking the ledger entry back to the original source document.

- Debit: The monetary amount debited to the account, which increases asset/expense accounts or decreases liability/equity/revenue accounts.

- Credit: The monetary amount credited to the account, which increases liability/equity/revenue accounts or decreases asset/expense accounts.

- Running Balance: The updated net balance of the account after the debit or credit is applied, allowing for real-time financial tracking.

Key Benefits of Utilizing Standardized Ledger Templates

Adopting standardized templates for your general ledger brings a level of discipline and predictability to your accounting processes. When financial data is structured uniformly, stakeholders can easily navigate the records, reducing the time spent deciphering inconsistent bookkeeping methods. This structural consistency serves as the foundation for reliable business intelligence.

A standardized general ledger template transforms raw financial data into an organized, reliable system that protects businesses from costly reporting errors and simplifies compliance.

Using these structured frameworks significantly simplifies tax preparation. Instead of scrambling through boxes of receipts and disparate spreadsheets at the end of the fiscal year, accounting teams can extract clean, categorized data directly from the ledger. Furthermore, standardized fields reduce human error by guiding the user to input data correctly, effectively audit-proofing your organization's financial history against internal or external scrutiny.

Choosing Your Format: Digital Spreadsheets vs. Dedicated Accounting Software

As businesses grow, their bookkeeping needs evolve. Choosing between digital spreadsheets like Microsoft Excel or Google Sheets and dedicated cloud-based accounting software is a pivotal decision for any management team. Each format presents distinct advantages and limitations depending on the scale and complexity of your business operations.

| Feature / Aspect | Digital Spreadsheets (Excel/Google Sheets) | Dedicated Accounting Software |

|---|---|---|

| Cost | Low to free; typically included in standard office suites. | Monthly or annual subscription fees. |

| Ease of Use | Highly customizable, but requires manual data entry and formula setup. | Automated workflows, user-friendly dashboards, and steep learning curve for advanced features. |

| Automation | Very limited; macros can help but still require manual triggers. | High; syncs directly with bank feeds, invoices, and payment gateways. |

| Data Integrity | Prone to accidental formula deletions and human data-entry errors. | Built-in validation checks, audit trails, and secure user permissions. |

Step-by-Step Guide to Recording Transactions Accurately

To maintain flawless financial records, transactions must flow systematically from the initial point of sale through the general journal and into the ledger. Following a strict, chronological process prevents omissions and ensures your books balance perfectly at the end of every accounting cycle.

Follow these steps to record and post your financial transactions:

- Identify the transaction and collect the source document, such as a receipt, invoice, or bank statement, to verify the exact amount and date.

- Analyze the transaction to determine which accounts are affected. For example, purchasing equipment with cash affects the asset account

Equipmentand the asset accountCash. - Record the entry in the general journal. This entry must include a debit to one account and an equal credit to another. For instance, you might input

Debit: Equipment $5,000andCredit: Cash $5,000. - Post the journal entry to the respective accounts in the general ledger. This transfers the information so that individual account balances are updated.

- Calculate the new running balance for each affected ledger account by factoring in the newly posted debits or credits.

Pitfalls to Avoid: Common Ledger Reconciliation Mistakes

Even with structured templates, manual bookkeeping remains susceptible to errors. Identifying these mistakes early is paramount to maintaining the integrity of your financial reports. Two of the most frequent errors in ledger management are transposition errors and double-posting.

A transposition error occurs when two adjacent numbers are accidentally reversed-for example, writing $540 instead of $450. While this might seem like a minor slip, it can throw off your entire trial balance. Another common issue is double-posting, which happens when an accountant records the same transaction twice, leading to inflated asset or expense figures. To spot these anomalies, bookkeepers often use the "rule of nine." If the difference between your debits and credits is divisible by nine, you are likely dealing with a transposition error. Regular reconciliations against bank statements are the best line of defense against these discrepancies.

Streamlining Your Financial Workflow for Long-Term Success

Establishing clean financial data requires consistent, disciplined habits. Setting up a regular reconciliation schedule is the single most effective way to keep your general ledger accurate. Monthly reconciliations ensure that any banking discrepancies, missing invoices, or data-entry errors are caught and corrected before they compound into larger, year-end headaches.

By implementing standardized ledger templates, training staff on correct entry protocols, and scheduling routine audits, you protect your business's financial health. Clear, accurate, and organized books provide the reliable insights needed to secure funding, satisfy tax obligations, and drive confident business decisions for years to come.

Leave a comment