Managing shareholder distributions can quickly devolve into a compliance nightmare for growing enterprises. Corporate treasury and accounting teams often struggle with manual tracking errors, missed declaration dates, and mismatched equity records.

Before selecting a ledger solution, however, one must understand how evolving tax codes and diverse share classes complicate the equity landscape. Implementing structured dividend payable templates grants financial teams total visibility, drastically reducing audit risks and ensuring precise cash flow forecasting.

While these templates streamline the tracking process, they require a foundational grasp of double-entry bookkeeping to be fully effective. Specifically, they serve as concrete proof of compliance by cleanly separating cumulative preferred dividends from common stock distributions. This guide outlines the essential ledger architectures, step-by-step setup methods, and reconciliation strategies to optimize your distribution workflow.

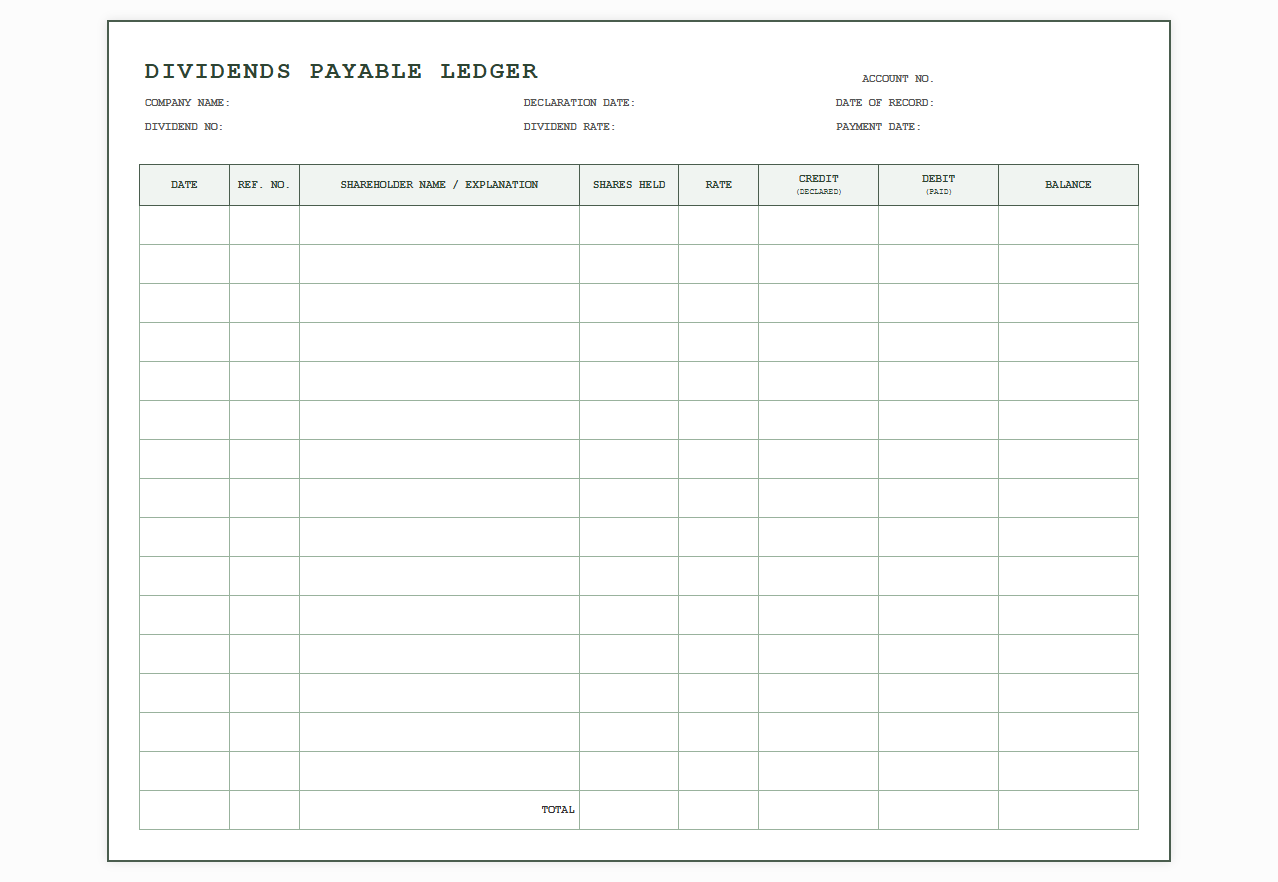

Dividends Payable Ledger Sheet

Download: .PDF

Download: .PDF

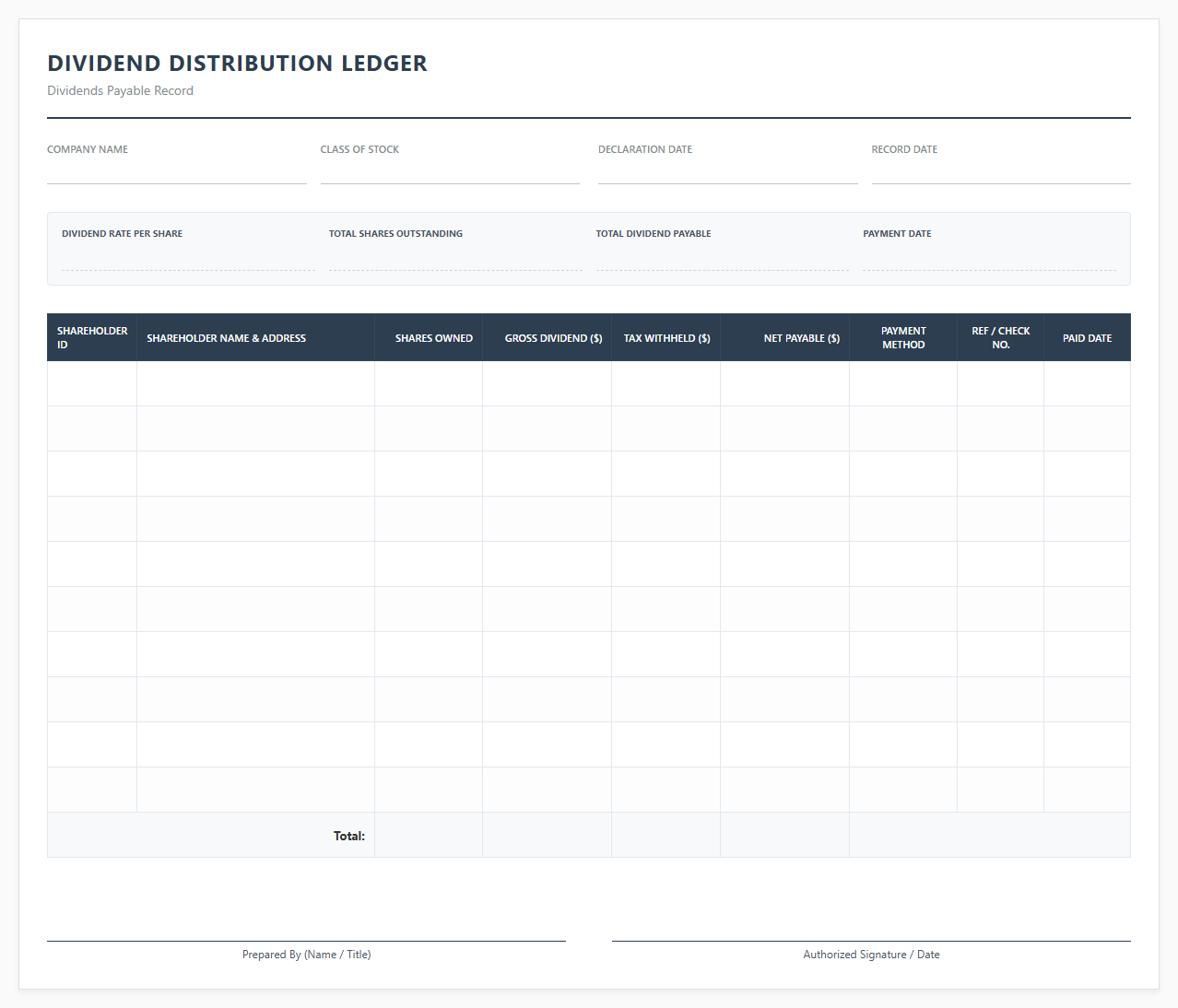

Dividend Distribution Ledger Template

Download: .PDF

Download: .PDF

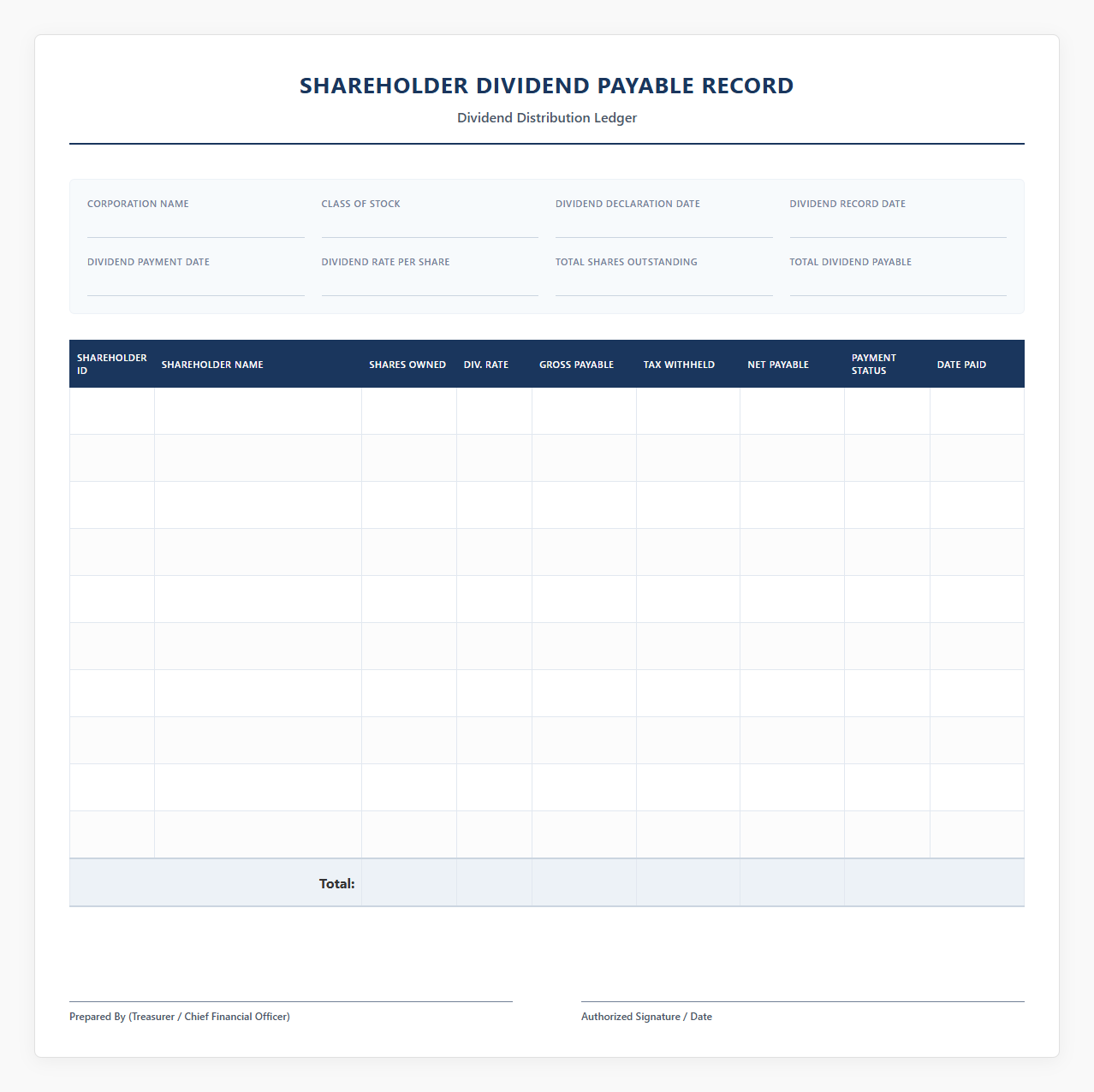

Shareholder Dividend Payable Record

Download: .PDF

Download: .PDF

Corporate Dividends Payable Tracking Ledger

![]() Download: .PDF

Download: .PDF

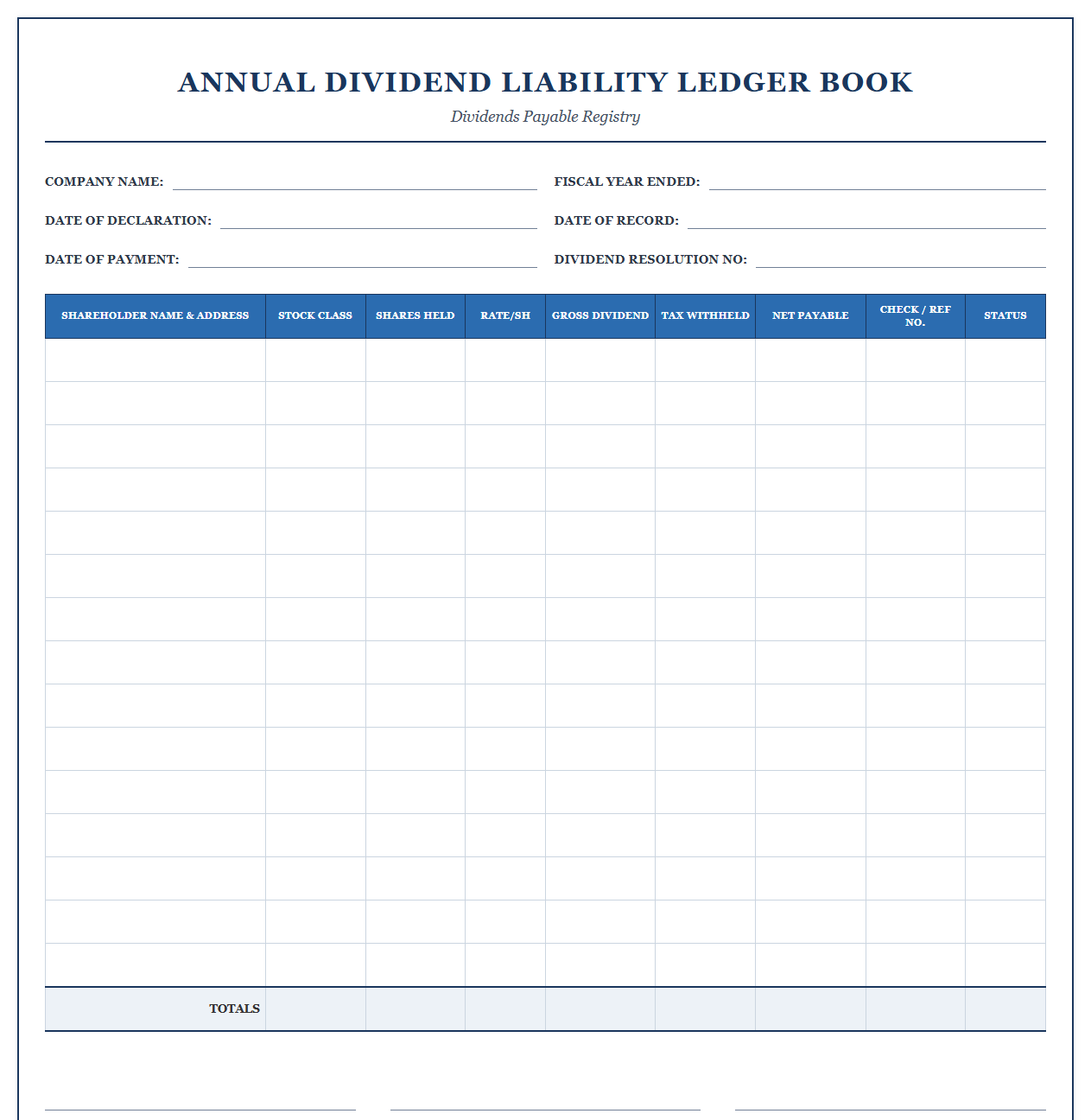

Annual Dividend Liability Ledger Book

Download: .PDF

Download: .PDF

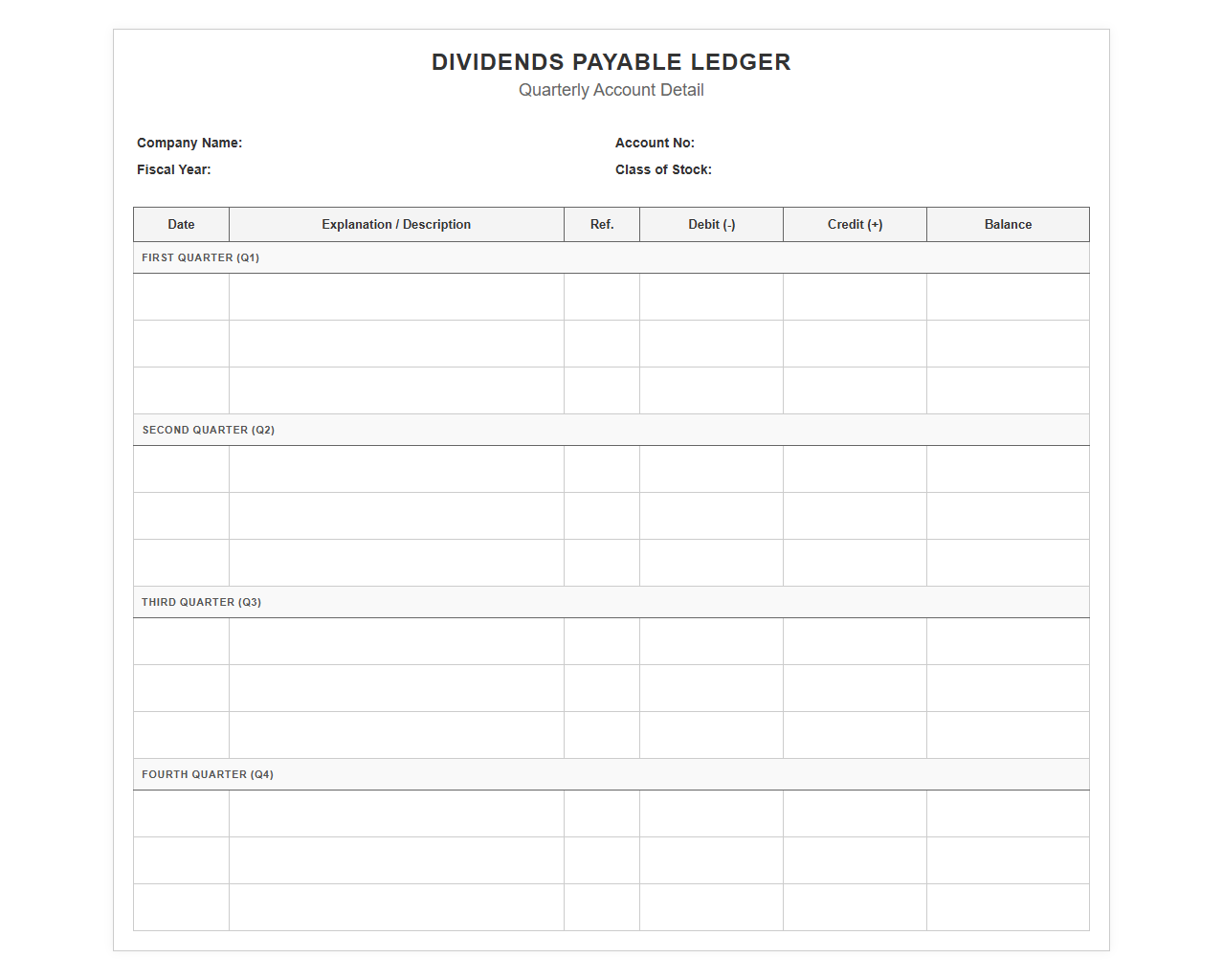

Quarterly Dividends Payable Ledger Account

Download: .PDF

Download: .PDF

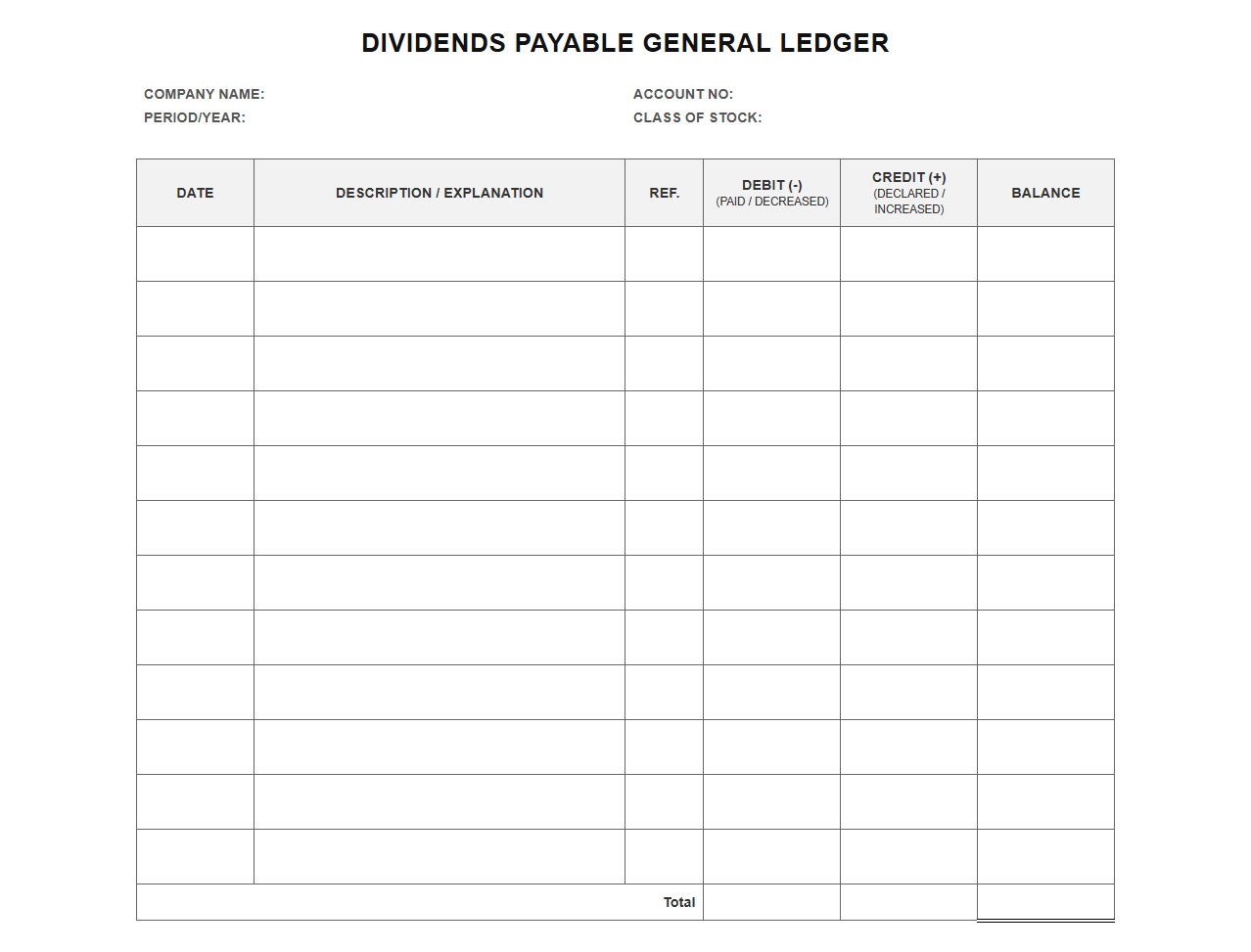

Dividend Declared and Paid General Ledger

Download: .PDF

Download: .PDF

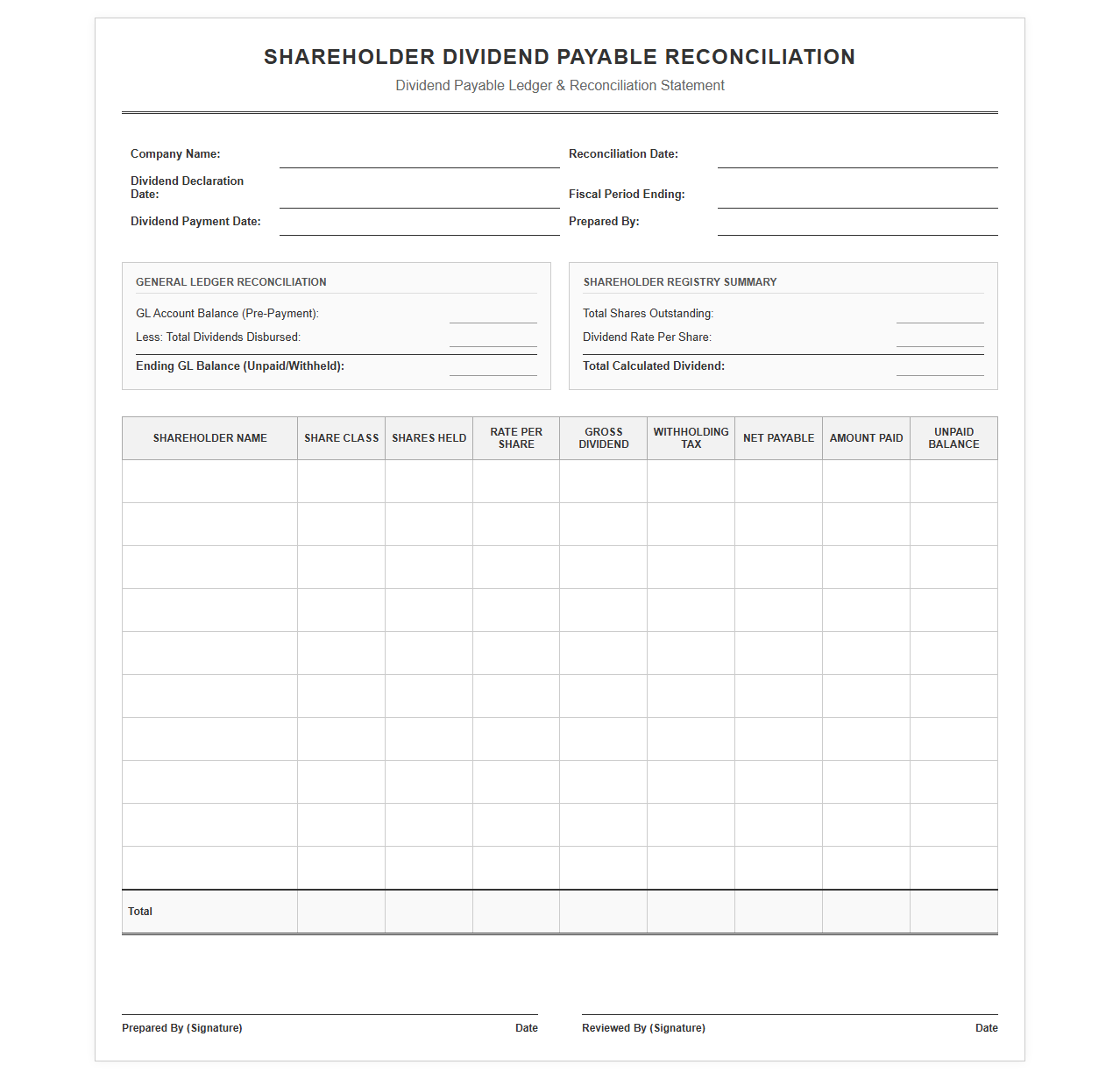

Shareholder Dividend Payable Reconciliation Template

Download: .PDF

Download: .PDF

The Role of Dividends Payable in Corporate Governance

Accurately tracking shareholder distributions and dividends payable is fundamental to robust corporate governance. When a board of directors declares a dividend, it establishes a legal liability that must be meticulously recorded. Doing so ensures regulatory compliance with federal and state laws, preventing severe penalties and maintaining market credibility.

Furthermore, precise record-keeping is vital for preserving investor trust. Shareholders rely on timely and accurate distribution payments, and any discrepancies can lead to reputational damage and legal disputes.

Core Components of an Effective Dividend Ledger

To maintain clarity and accuracy, a corporate dividend ledger must capture specific transactional milestones and shareholder details. Tracking these dates prevents payment errors and assists in resolving future audits.

- Declaration Date: The date the board of directors formally announces the dividend payment.

- Ex-Dividend Date: The cut-off date dictating whether the buyer or seller of the stock receives the upcoming dividend.

- Record Date: The date established by the corporation to determine who the registered shareholders are.

- Payment Date: The actual day the cash distribution is dispersed to shareholders.

- Shareholder Metadata: Unique identifiers, contact details, and holding balances for each equity holder.

Standard Dividend Payable Journal Entry Template

Below is a standard journal entry template mapping the debits and credits from the initial declaration of a dividend to its final disbursement.

| Date | Account Title | Debit ($) | Credit ($) |

|---|---|---|---|

| Declaration Date | Retained Earnings | XX,XXX | |

| Dividends Payable | XX,XXX | ||

| Payment Date | Dividends Payable | XX,XXX | |

| Cash | XX,XXX |

Managing Cumulative Preferred Shares and Arrears

Cumulative preferred shares require meticulous tracking because any unpaid dividends accumulate over fiscal periods as arrears. These obligations must be paid in full before any common shareholders can receive distributions.

Dividends in Arrears Formula:

Arrears = (Total Outstanding Preferred Par Value × Dividend Rate) − Dividends Paid in Current Period

Maintaining a dedicated section in the ledger prevents compliance failures regarding preferred shareholder rights.

Automating Distribution Sheets with Formulaic Workflows

To minimize manual entry errors, financial teams can build dynamic workflows linking shareholder registries directly to the dividend ledger using spreadsheet tools.

=VLOOKUP(A2, ShareholderRegistry!A:C, 3, FALSE) * DividendPerShareUsing functions like index-match or lookup formulas ensures that changes in ownership are instantly reflected in the distribution calculations.

Reconciliation Protocols and Tax Information Reporting

Regularly auditing the ledger ensures that cash disbursements align perfectly with recorded liabilities.

- Verify that the total cash cleared from the dividend bank account matches the debit total of the dividends payable account.

- Identify outstanding checks or failed direct deposits and adjust the ledger accordingly.

- Reconcile the total distributions with internal shareholder equity balances.

- Prepare and distribute Form 1099-DIV to eligible US-based shareholders to report taxable distributions.

Best Practices for Long-Term Ledger Maintenance

Proactive maintenance of your distribution records safeguards the financial integrity of the enterprise and ensures smooth administrative operations.

Leave a comment