Consolidating multi-entity books often feels like solving a puzzle with shifting pieces. For finance leaders, intercompany payables discrepancies remain a persistent drain on resources, routinely stalling month-end closes and complicating audit preparation. As organizations scale, decentralized operations naturally introduce transactional fragmentation.

Resolving this structural friction requires standardized workflows. Deploying structured ledger templates grants accounting teams immediate cross-entity visibility, reducing variance-resolution times from days to minutes. However, templates are not magic cure-alls; they require a baseline of unified intercompany policies to function. For example, mismatched USD/EUR currency inputs between a European subsidiary and a US parent can only be reconciled automatically if both entities map to identical transaction identifiers.

This article outlines how to design robust ledger templates, align your chart of accounts, and establish the governance needed to eliminate multi-entity discrepancies permanently.

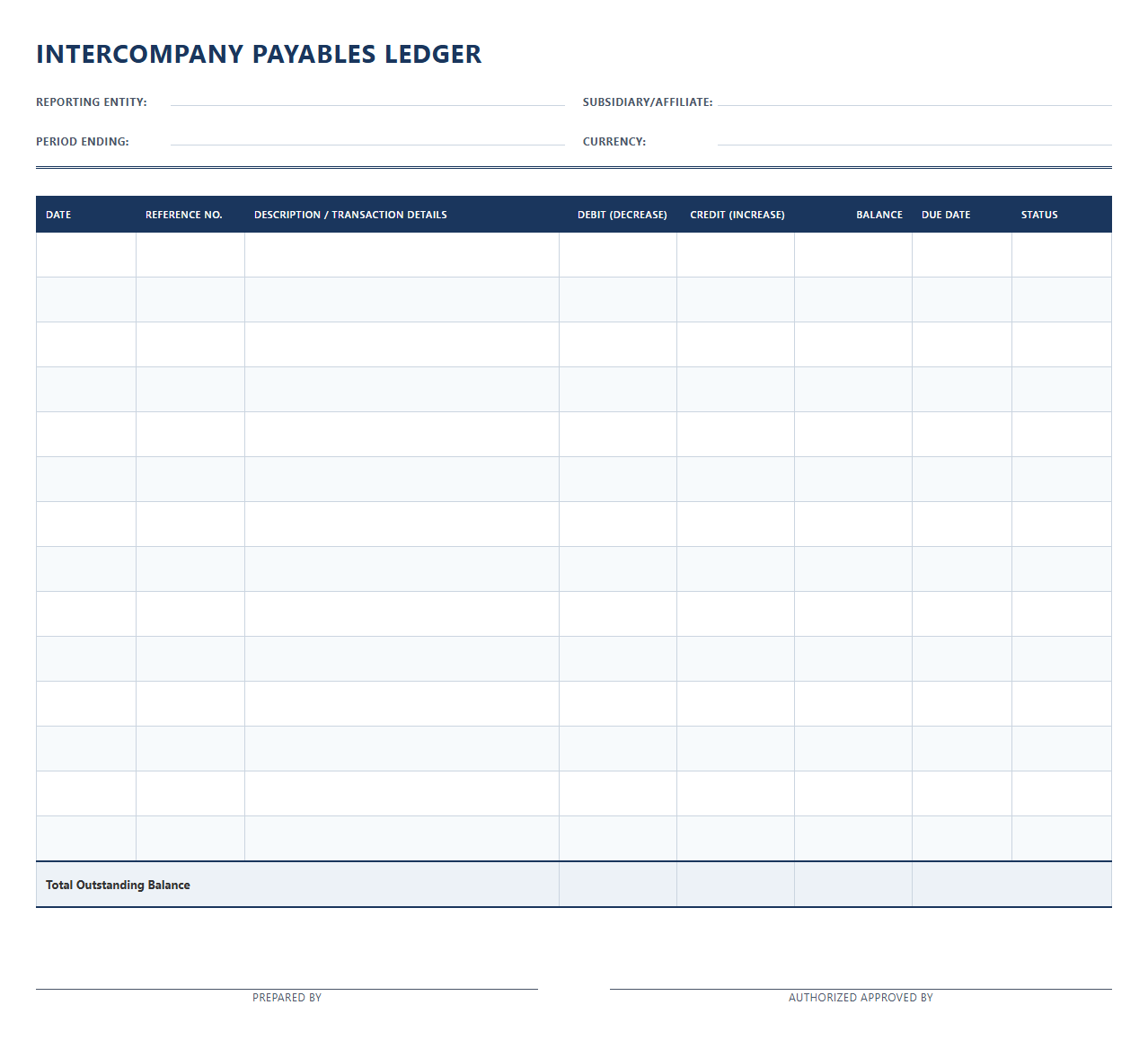

Intercompany Payables Ledger Template

Download: .PDF

Download: .PDF

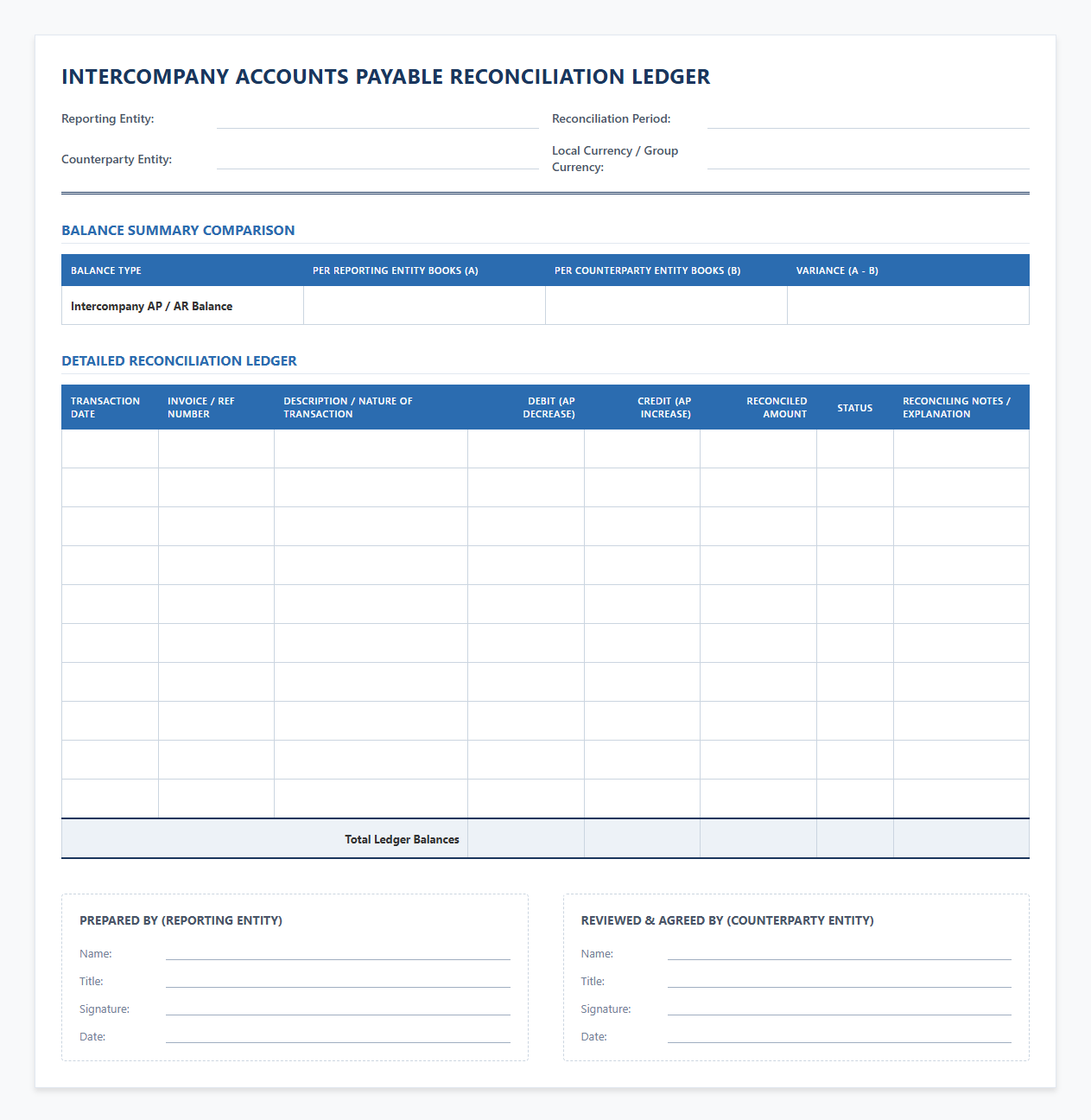

Intercompany Accounts Payable Reconciliation Ledger

Download: .PDF

Download: .PDF

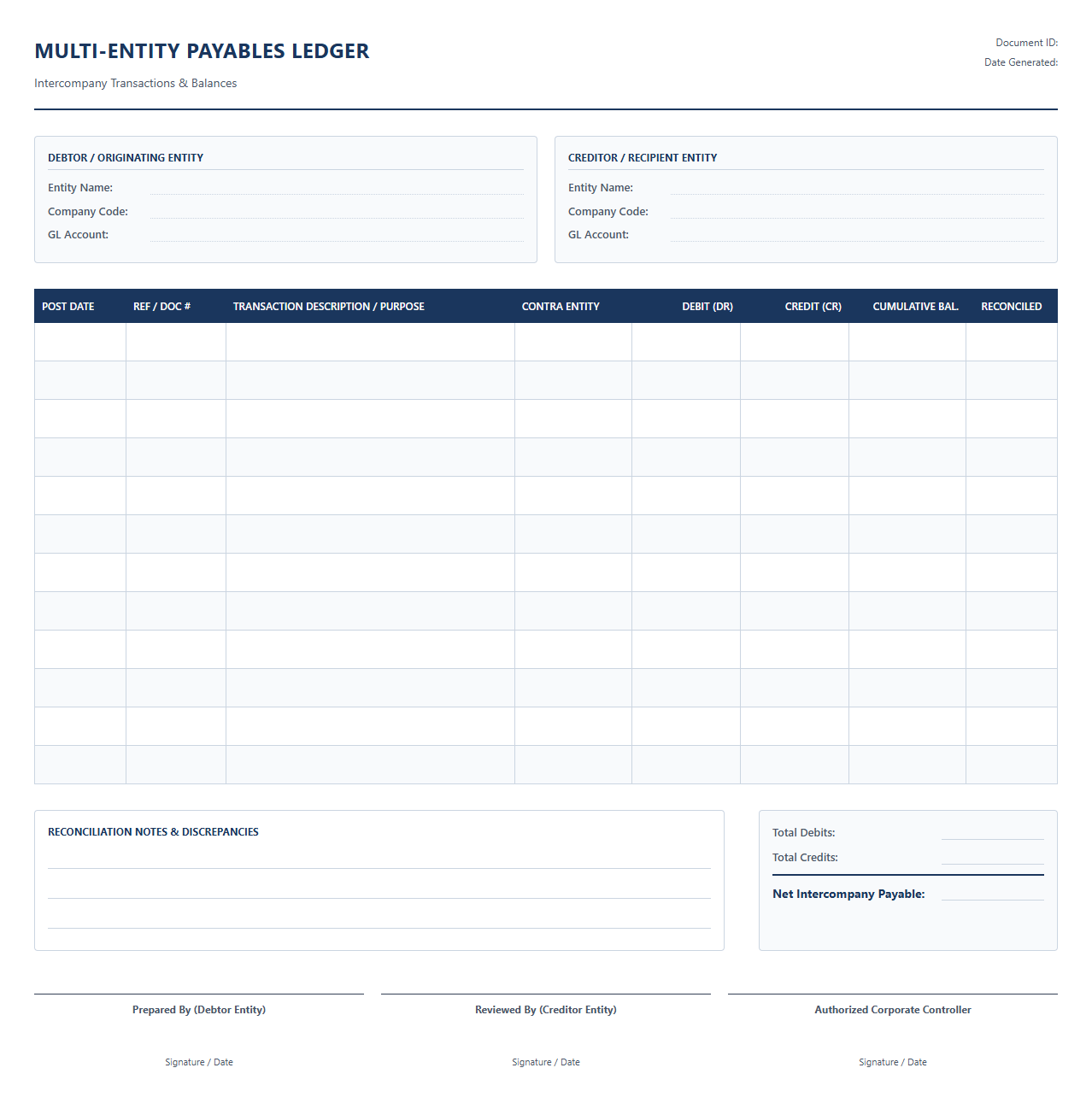

Multi-Entity Payables Ledger Template

Download: .PDF

Download: .PDF

Related Party Payables Tracking Sheet

![]() Download: .PDF

Download: .PDF

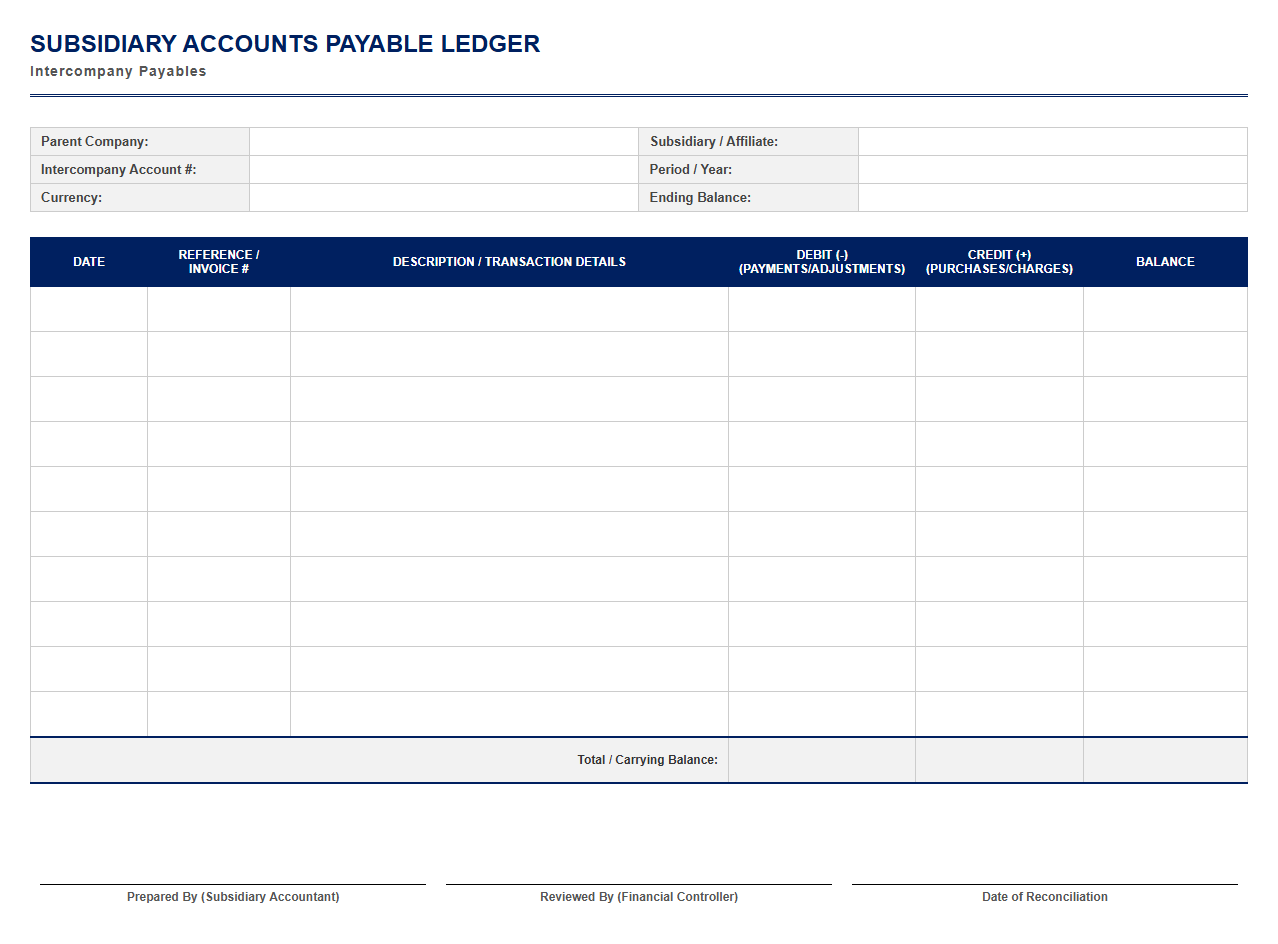

Subsidiary Accounts Payable Ledger Template

Download: .PDF

Download: .PDF

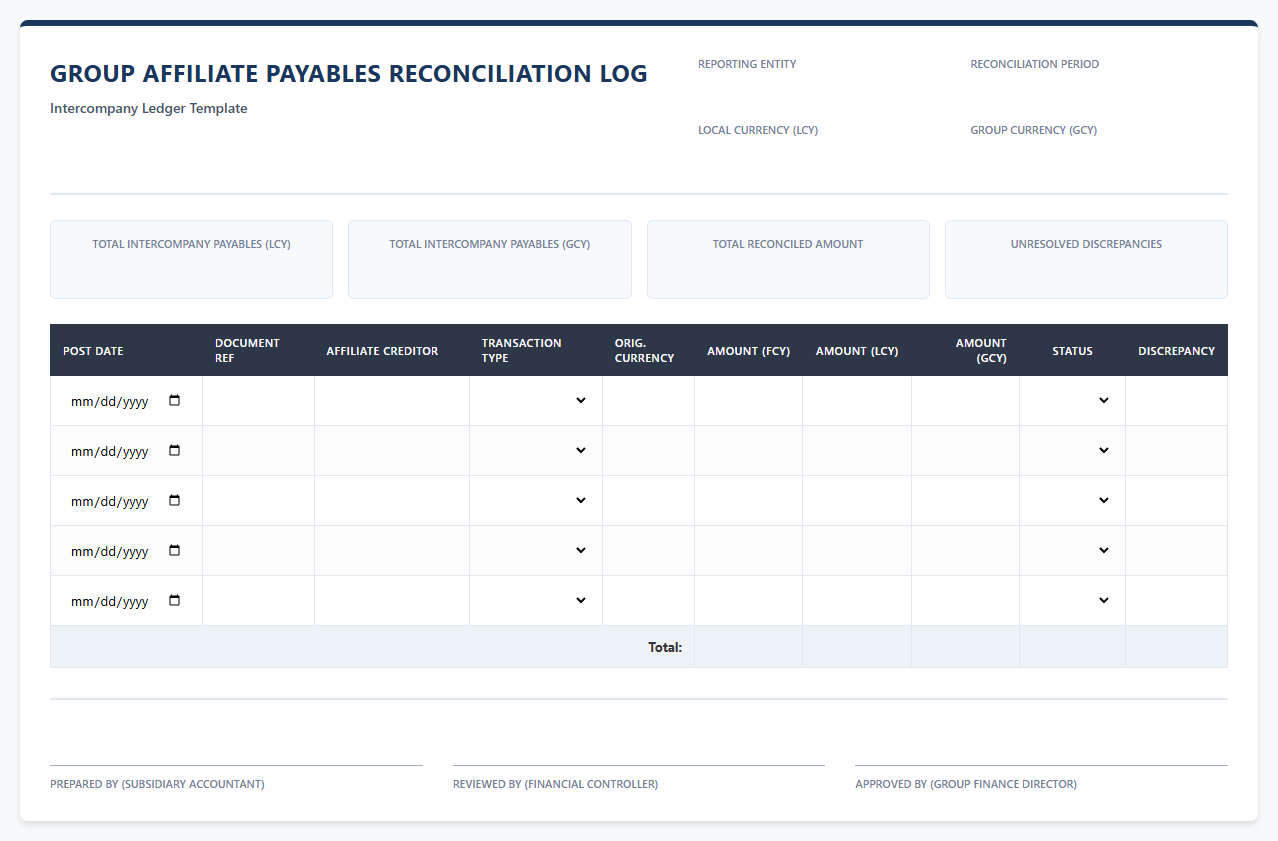

Group Affiliate Payables Reconciliation Log

Download: .PDF

Download: .PDF

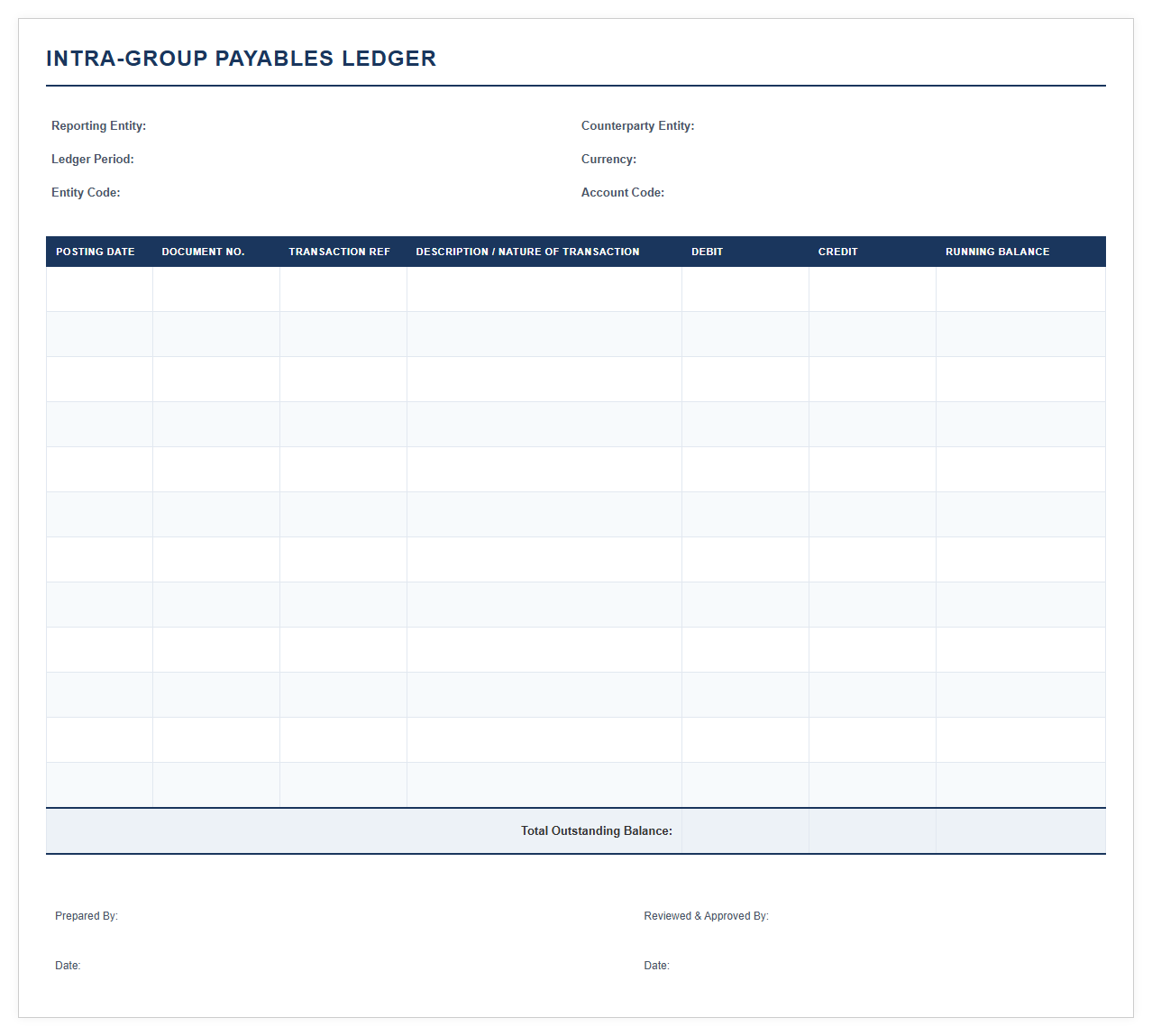

Intra-Group Payables Ledger Template

Download: .PDF

Download: .PDF

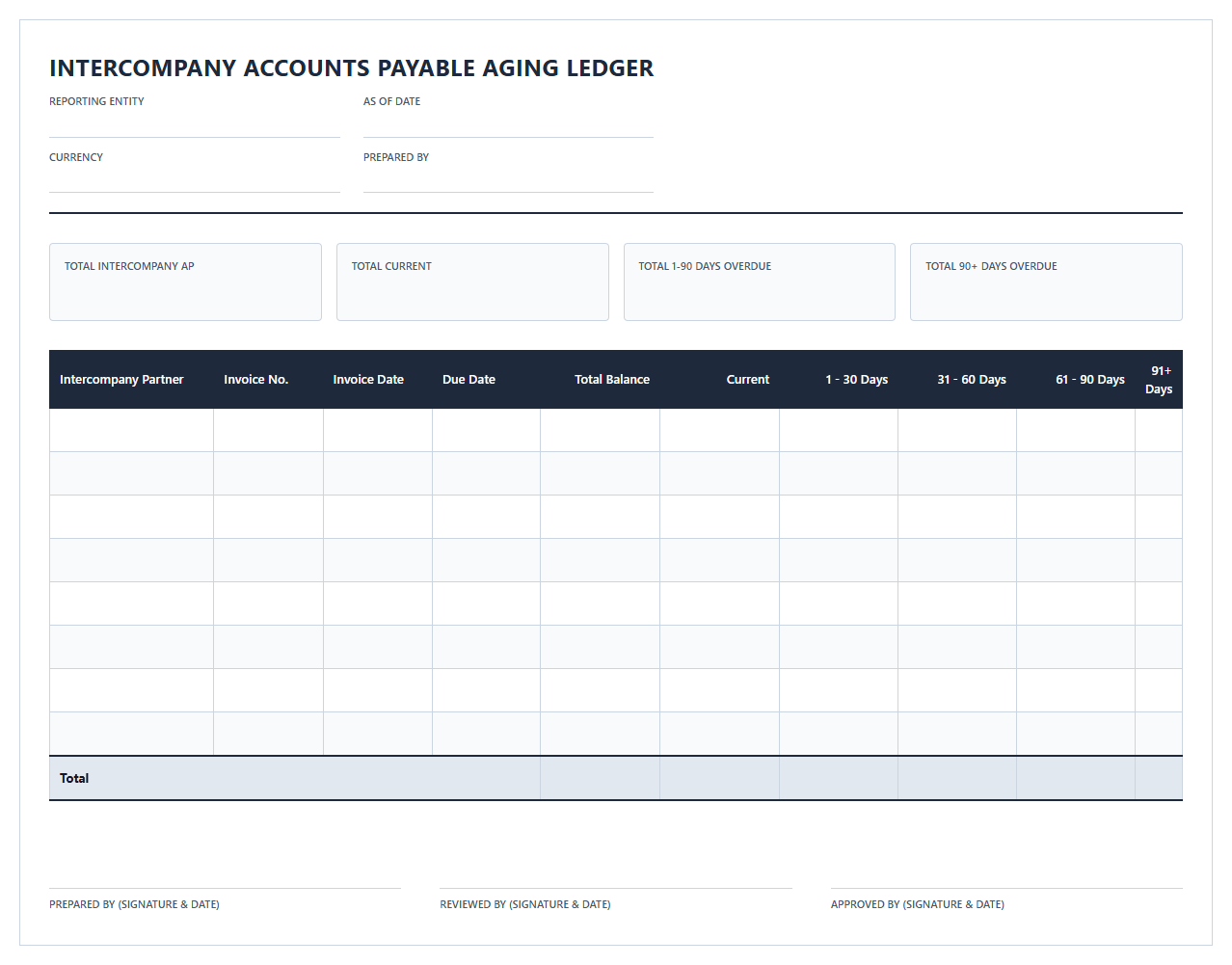

Intercompany Accounts Payable Aging Ledger

Download: .PDF

Download: .PDF

The Friction of Multi-Entity Reconciliation

Multi-entity organizations operate in a complex web of cross-border transactions, shared services, and internal supply chains. As these organizations scale, reconciling intercompany payables and receivables becomes an operational bottleneck. Discrepancies often arise from decentralized accounting systems, manual data entry, and fragmented communication channels between subsidiaries. When these discrepancies go unnoticed, they lead to extensive manual investigations, delayed financial close cycles, and inaccurate corporate reporting. The financial impact of manual errors and prolonged close periods directly erodes organizational profitability and compromises stakeholder trust.

Root Causes of Intercompany Ledger Mismatches

Understanding why ledger asymmetry occurs is the first step toward building a resilient financial ecosystem. The primary drivers of these persistent discrepancies include:

- Divergent Exchange Rates: Subsidiaries operating in different countries often use localized FX rate feeds, resulting in minor valuation differences for the same transaction upon consolidation.

- Timing Differences: A supplying entity might record revenue in one fiscal period, while the receiving subsidiary records the corresponding payable in the next period due to shipping delays or processing lags.

- Inconsistent Chart of Accounts (COA) Mapping: Lacking a unified global ledger framework, subsidiaries frequently map intercompany transactions to different accounts, creating categorization mismatches.

Blueprint of a Standardized Ledger Template

To eliminate discrepancies at the source, organizations must implement a standardized intercompany payables ledger template. This template enforces data uniformity across all subsidiaries, ensuring that every transaction is recorded with identical metadata and reference attributes.

| Field Name | Data Type | Description | Example Value |

|---|---|---|---|

| Originating Entity ID | Alphanumeric | The unique identifier of the billing subsidiary. | ENT-US-101 |

| Receiving Entity ID | Alphanumeric | The unique identifier of the paying subsidiary. | ENT-UK-202 |

| Transaction Timestamp | ISO 8601 | The UTC date and time the transaction was initialized. | 2023-11-15T14:30:00Z |

| Intercompany Reference Key | UUID | A unique, shared hash key generated to link both sides of the transaction. | ic-9a8b-7c6d-5e4f |

Managing Multi-Currency and Tax Complexities

Cross-border intercompany transactions require robust mechanisms to handle fluctuating exchange rates and diverse tax jurisdictions. Financial templates must integrate automated FX translation rules that lock in daily benchmark rates (such as those from the European Central Bank) at the exact moment of transaction execution. This prevents the small valuation discrepancies that compound into significant balance sheet imbalances during consolidation.

Establishing the Real-Time Matching Engine

Moving from retrospective reconciliation to real-time matching drastically reduces month-end friction. Organizations should configure automated workflow rules within their ERP systems to continuously reconcile intercompany postings based on predefined logic.

- Unique Key Aggregation: The matching engine extracts transactions sharing the exact same Intercompany Reference Key.

- Tolerance Threshold Evaluation: The system compares transaction amounts; values within a strict tolerance limit (e.g., less than $5.00 for minor FX variances) are auto-cleared.

- Discrepancy Flagging: Any transaction failing the key alignment or exceeding the tolerance threshold is instantly flagged and locked from general ledger posting.

Exception Handling and Dispute Resolution Frameworks

When automated matching fails, a clear governance framework prevents operational stagnation. Flagged transactions must be routed through structured escalation paths to prevent unresolved issues from lingering into the closing window. This system ensures that accountability is maintained across all entity boundaries.

"In accordance with corporate accounting policy guidelines, any flagged intercompany mismatch exceeding $10,000 must be routed to the respective controllers of both entities for resolution within 48 hours of discovery, with all communication documented directly within the centralized ledger registry."

Achieving Continuous Audit Readiness

Relying on standardized templates and real-time validation engines transforms the finance function from reactive to proactive. By embedding structural controls directly into daily transactional workflows, organizations secure an unalterable audit trail that satisfies external auditors and tax authorities alike. This systematic approach not only shrinks the month-end closing cycle from weeks to days but also establishes an ironclad foundation for transfer pricing compliance and global financial transparency.

Leave a comment