Accounting teams frequently battle tedious end-of-month discrepancies caused by manual interest accrual calculations, where a single misplaced spreadsheet formula can compromise the integrity of financial reporting. To resolve this, organizations must first establish a foundation of robust internal controls and standardized accounting frameworks before attempting to automate their workflows.

Adopting a structured interest payable ledger template grants finance departments immediate operational relief, delivering audit-ready precision and eliminating hours of redundant manual reconciliation. However, as an educational stipulation, these templates are not magic fixes; they require clean baseline data and a clear understanding of your organization's underlying debt agreements to function effectively.

For instance, a reliable template must be pre-configured to handle complex parameters such as Actual/360 day-count conventions and semi-annual compounding frequencies. In this article, we will outline how to implement these structured templates, configure key calculation variables, and permanently eliminate your accrual errors.

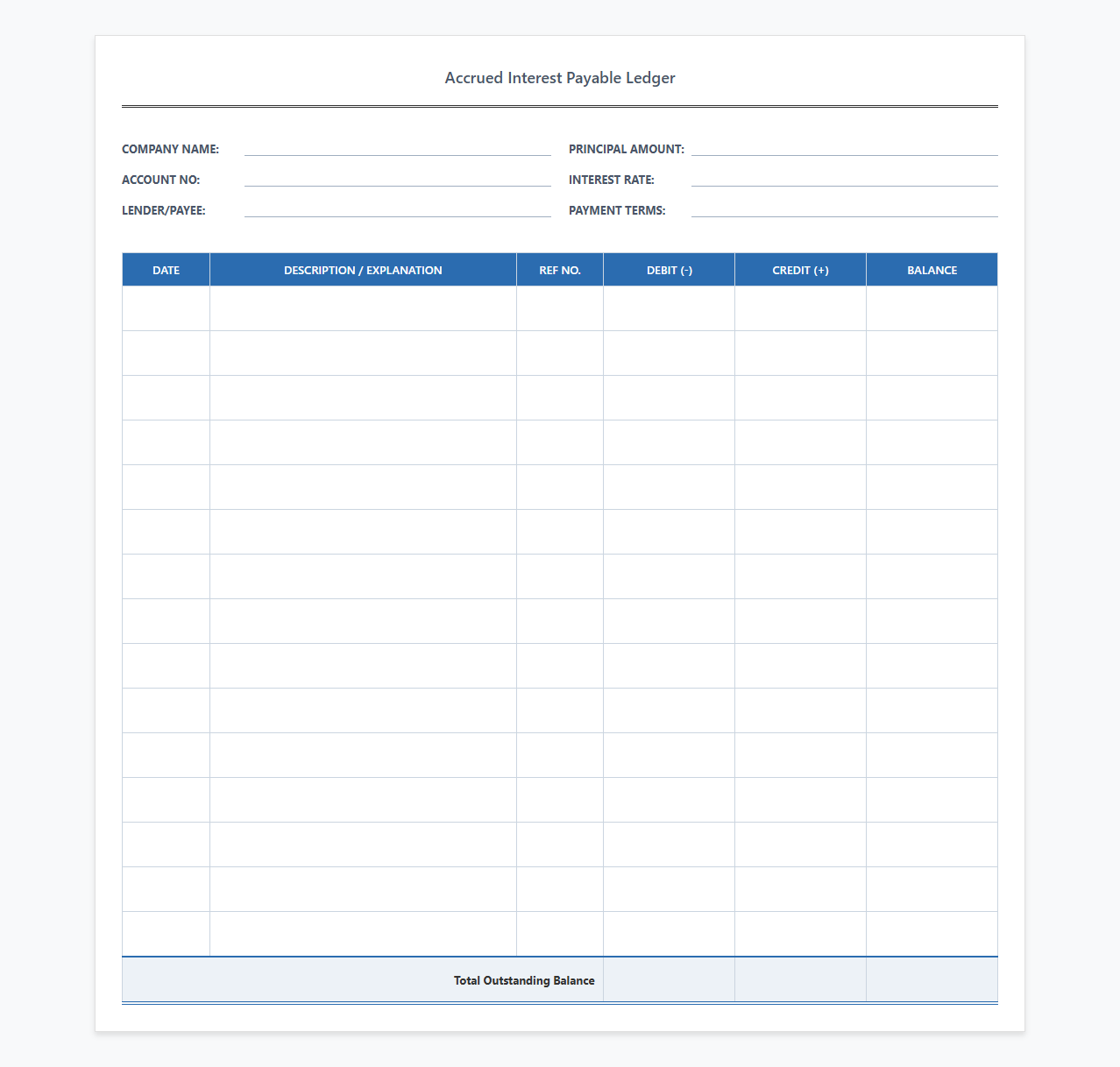

Accrued Interest Payable Ledger Sheet

Download: .PDF

Download: .PDF

Monthly Interest Payable Accounting Template

Download: .PDF

Download: .PDF

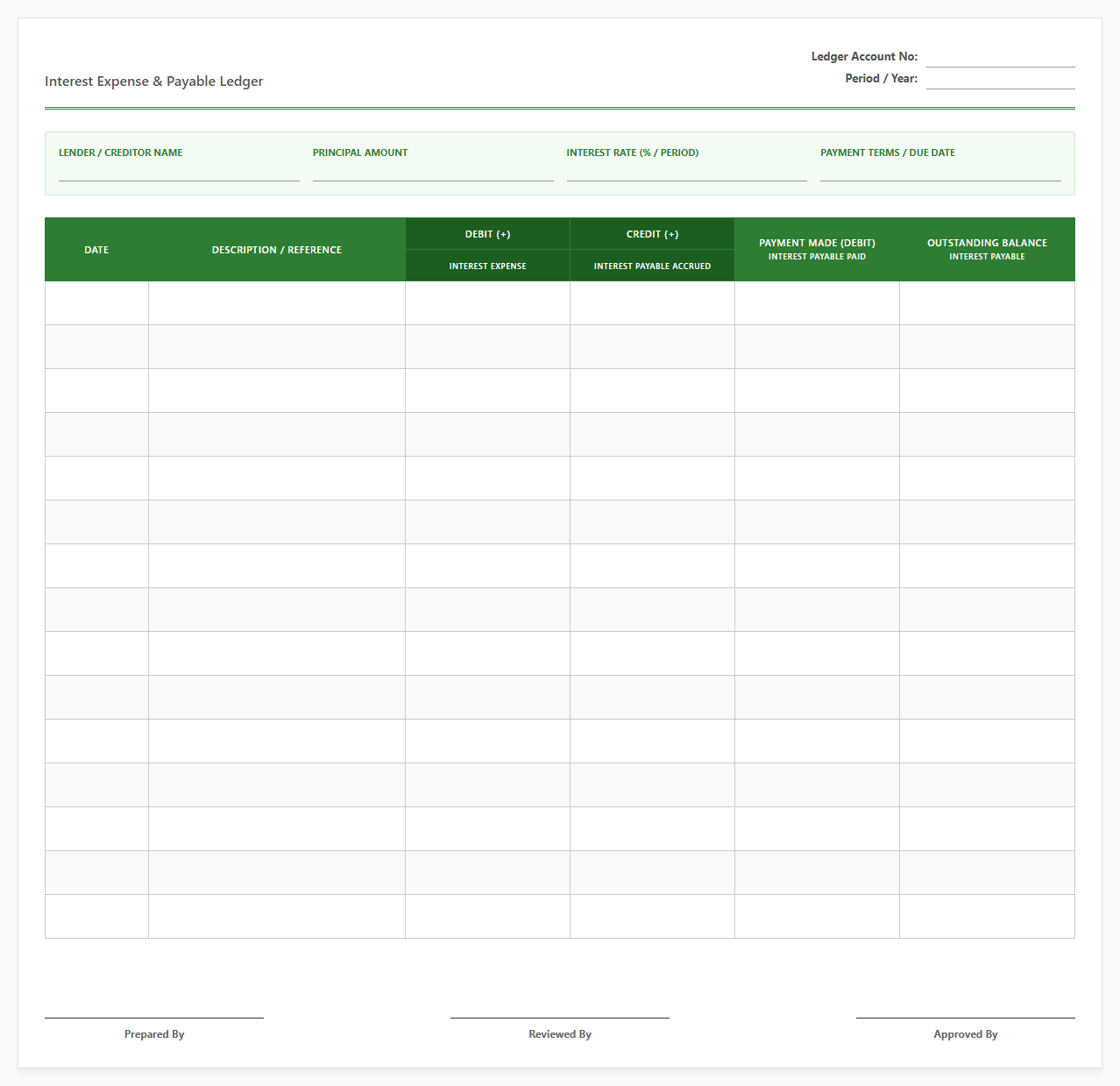

Interest Expense and Payable Ledger Excel

Download: .PDF

Download: .PDF

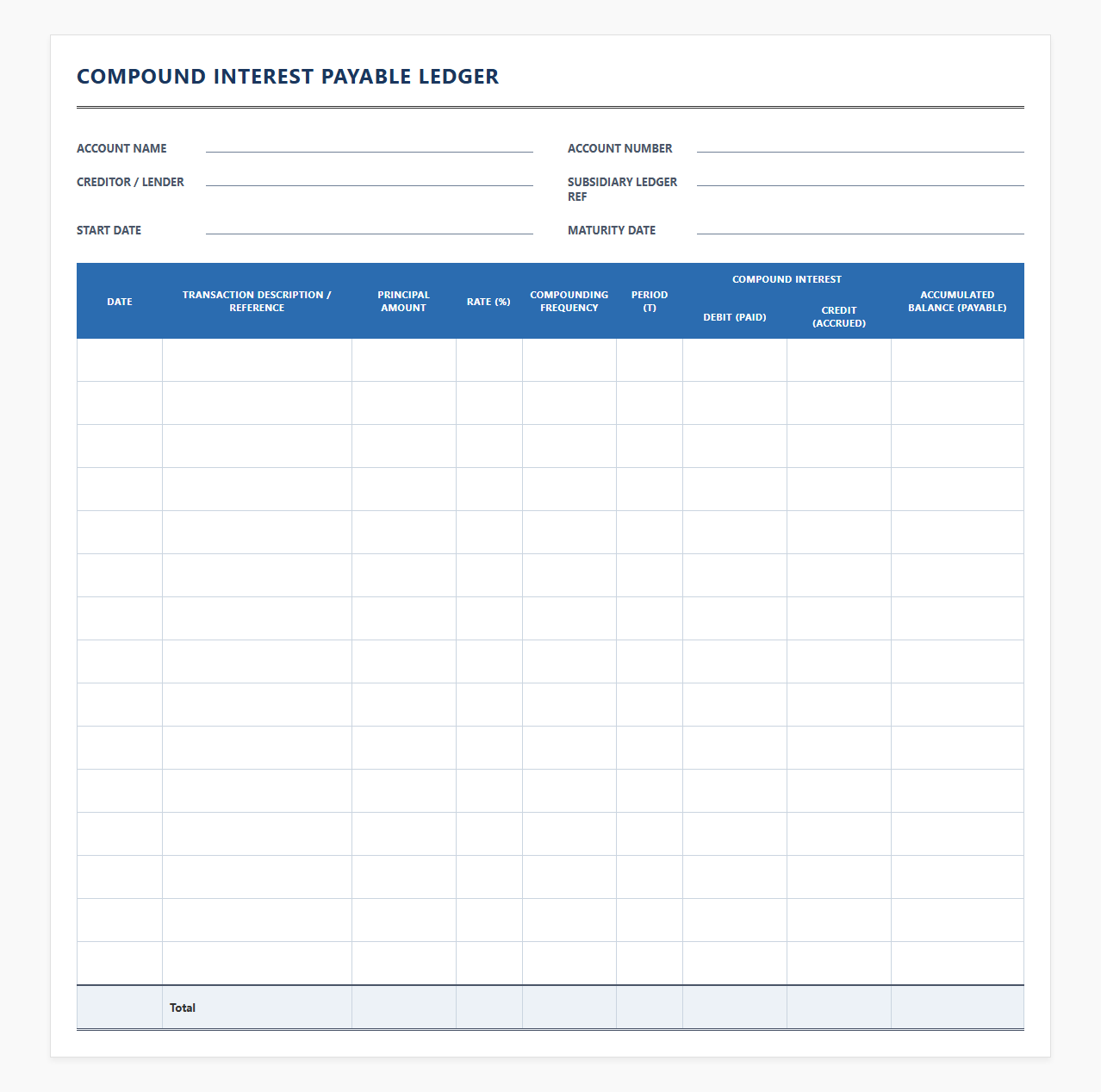

Compound Interest Payable Ledger Template

Download: .PDF

Download: .PDF

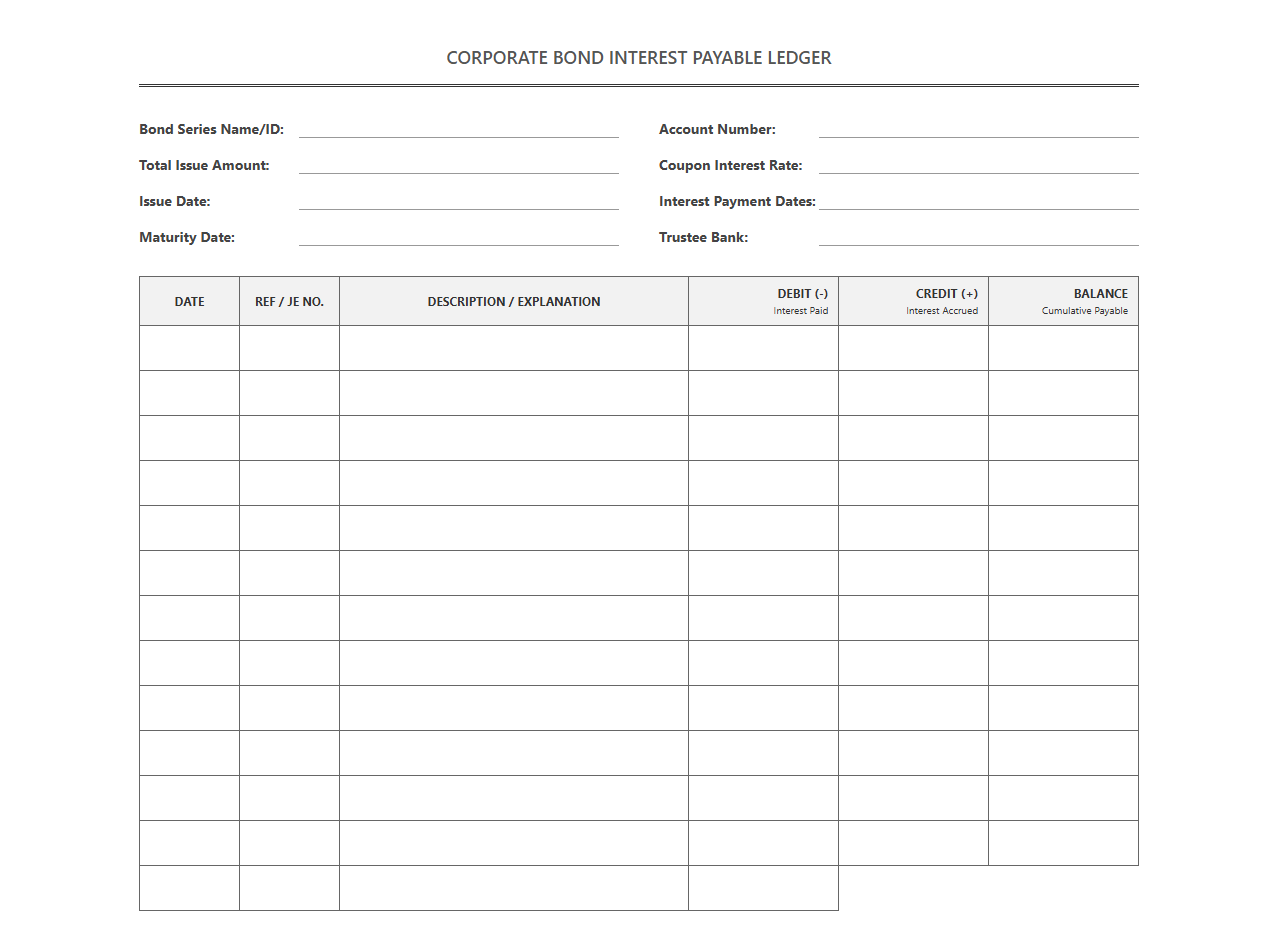

Corporate Bond Interest Payable Ledger

Download: .PDF

Download: .PDF

Loan Interest Payable Tracking Ledger

![]() Download: .PDF

Download: .PDF

Short Term Interest Payable Ledger Sheet

Download: .PDF

Download: .PDF

Annualized Interest Payable General Ledger Template

Download: .PDF

Download: .PDF

Daily Interest Accrual and Payable Ledger

Download: .PDF

Download: .PDF

The Hidden Cost of Accrual Errors in Interest Tracking

In corporate accounting, interest payable accrual errors often slip through the cracks unnoticed. These errors typically occur due to manual data entry slips, system integration gaps, or misaligned amortization schedules. When financial teams rely on outdated spreadsheets or fragmented tracking systems, the timing of interest recognition becomes distorted. Accrual discrepancies disrupt financial reporting by misstating liability balances on the balance sheet and inflating or understating interest expenses on the income statement. This lack of precision compromises the integrity of monthly closes and can trigger restatements that erode stakeholder trust.

Understanding the Interest Payable Ledger

A structured interest payable ledger serves as the single source of truth for all debt-related obligations. To maintain absolute precision, the ledger must systematically capture specific data points for every active liability.

- Unique Loan Identifier: A distinct code or name to track individual debt instruments.

- Principal Balance: The outstanding principal amount subject to interest calculation.

- Stated Interest Rate: The contractual rate applied to the principal.

- Accrual Period: The exact start and end dates for the current billing cycle.

- Day-Count Convention: The mathematical rule utilized to calculate interest.

- Accumulated Accrued Interest: The total interest expense recognized but not yet paid.

Common Triggers of Accrual Discrepancies

Discrepancies in interest payable rarely stem from single isolated events. Instead, they are frequently caused by systematic misalignments between contractual terms and general ledger configurations.

- Mismatched Payment Dates: When interest billing cycles do not align cleanly with fiscal month-end dates, teams often fail to calculate the partial-period stub interest correctly.

- Incorrect Day-Count Conventions: Utilizing a 30/360 method for a loan contracted under Actual/360 or Actual/365 rules introduces compounding variance over time.

- Shifting Interest Rates: For variable-rate debt, failing to update base rates on the exact reset date leads to immediate calculation drift.

Designing a Structured Ledger Template

To eliminate manual math errors, teams can build a standardized ledger template within Excel or their core ERP system. The structured format ensures that calculations remain consistent across all outstanding liabilities.

| Loan ID | Principal Amount | Annual Rate | Day-Count Rule | Days Accrued | Calculated Accrual |

|---|---|---|---|---|---|

| LN-2024-01 | $1,000,000 | 5.50% | Actual/360 | 30 | $4,583.33 |

| LN-2024-02 | $500,000 | 6.00% | 30/360 | 30 | $2,500.00 |

Step-by-Step Guide to Resolving Accrual Errors

When historical accrual errors are uncovered, financial teams must follow a systematic path to reconcile the differences and post correct entries.

- Extract and Aggregate: Pull all payment histories, amortization schedules, and trial balance records for the affected periods.

- Recalculate Independently: Use the standardized ledger template to run a parallel calculation of what the interest should have been.

- Identify the Variance: Compare the template's theoretical balances against the general ledger's actual ending balances to isolate the variance.

- Post Correcting Journal Entries: Adjust the interest payable liability and interest expense accounts to match the verified template calculations.

Implementing Controls and Validation Checks

Preventing future accrual errors requires embedding automated controls and logic tests directly into your sheet or accounting environment.

- Zero-Variance Validation: Implement formula-driven checks to ensure that manual inputs match physical debt agreements.

=IF(GL_Balance=Template_Balance, "Match", "Variance Alert") - Day-Count Safeguards: Restrict cell inputs in the day-count column to validated lists, preventing users from typing arbitrary rules.

- Automated Rate Feeds: Link variable interest rate inputs directly to verified external market feeds to eliminate manual updates.

Achieving Continuous Audit Readiness

A resilient interest payable ledger does more than solve monthly reporting headaches. By transitioning from manual, ad-hoc tracking to a formalized, template-driven framework, organizations secure absolute clarity over their debt obligations. Having clean, automated calculations ensures that external auditors can verify interest expenses with minimal friction. Proactive control over interest payable structures translates directly into reliable financial statements, robust compliance frameworks, and an empowered corporate treasury function that operates with complete confidence.

Leave a comment