For corporate accountants and financial controllers, reconciling month-end interest receivable is a recurring source of friction. Minor discrepancies in accrued income can quickly cascade into material reporting errors. This challenge intensifies as organizations scale, transitioning from simple savings accounts to complex debt instruments where accrual periods rarely align with calendar months.

Implementing structured ledger templates grants accounting teams the exact precision needed to eliminate these calculation errors, provided that users establish clear, standardized baseline assumptions for day-count conventions. By systematically tracking variables like 30/360 interest rules for corporate bonds or treasury bills, these tools turn complex calculations into predictable, auditable adjusting entries.

In this guide, we will examine the mechanics of interest accrual, provide customizable ledger templates, and outline step-by-step procedures for seamless month-end reconciliation.

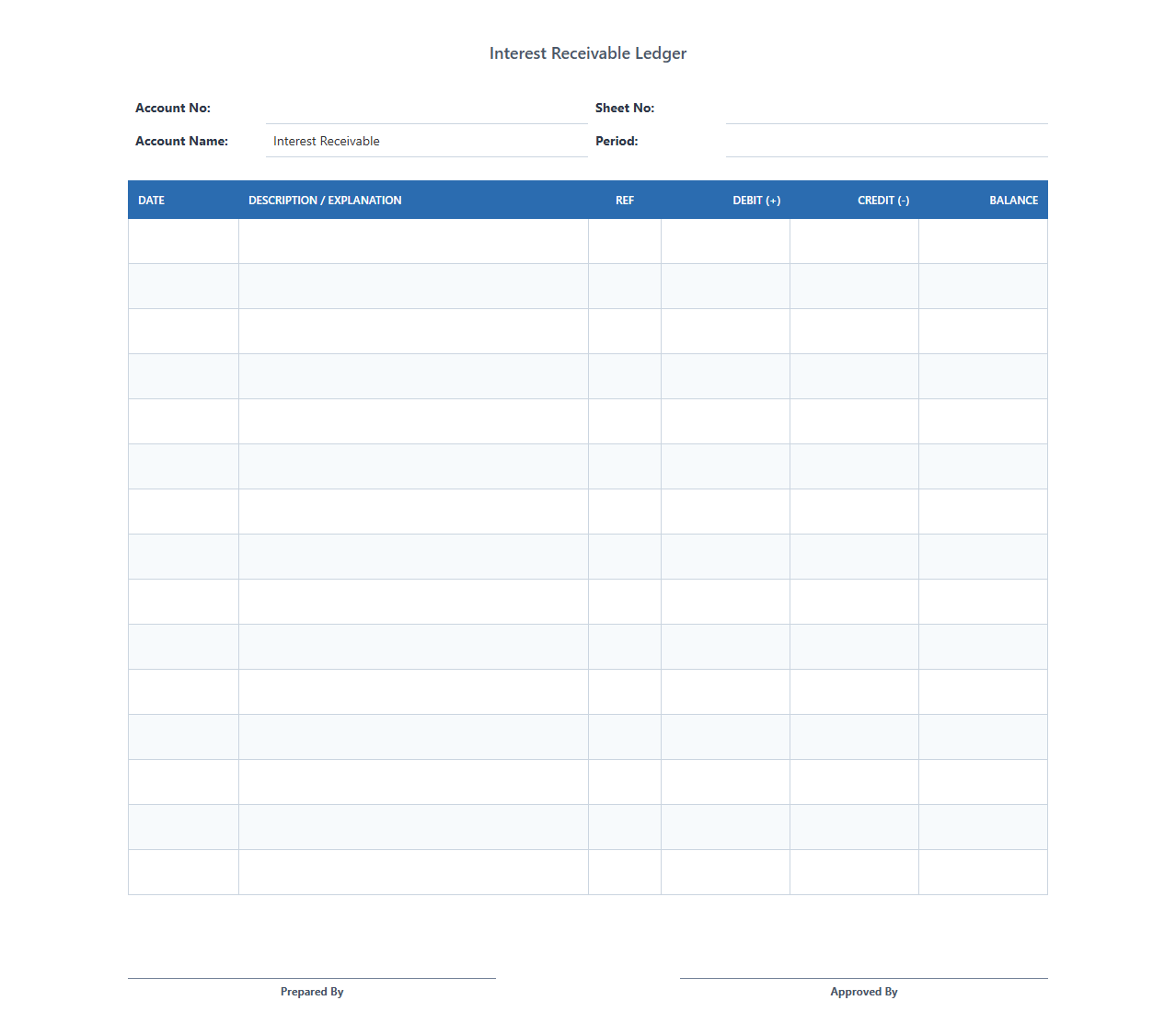

Interest Receivable Ledger Template

Download: .PDF

Download: .PDF

Accrued Interest Receivable Ledger Template

Download: .PDF

Download: .PDF

Monthly Interest Receivable Tracking Ledger

![]() Download: .PDF

Download: .PDF

Loan Interest Receivable Subsidiary Ledger

Download: .PDF

Download: .PDF

Investment Interest Receivable Account Ledger

Download: .PDF

Download: .PDF

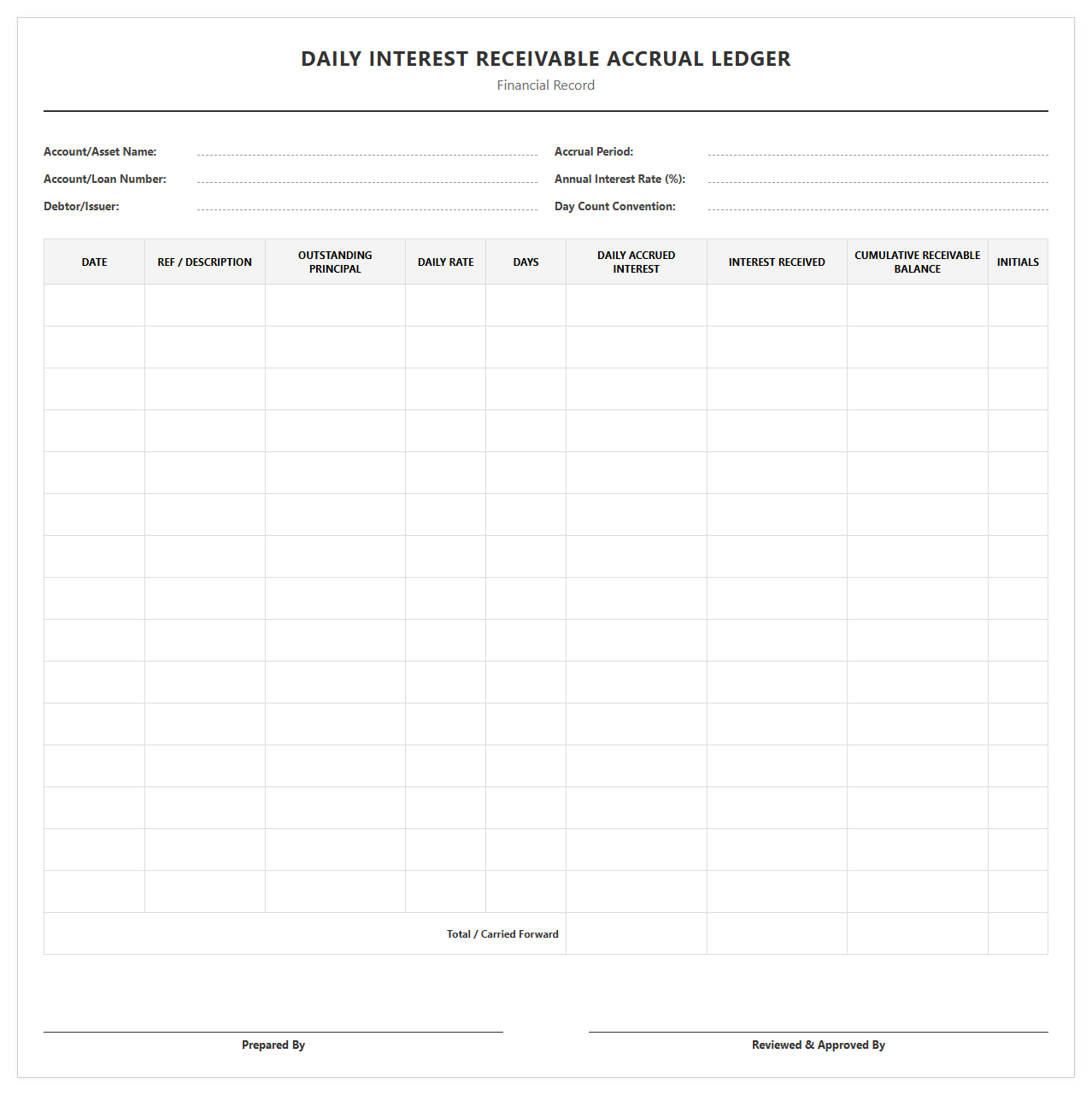

Daily Interest Receivable Accrual Ledger

Download: .PDF

Download: .PDF

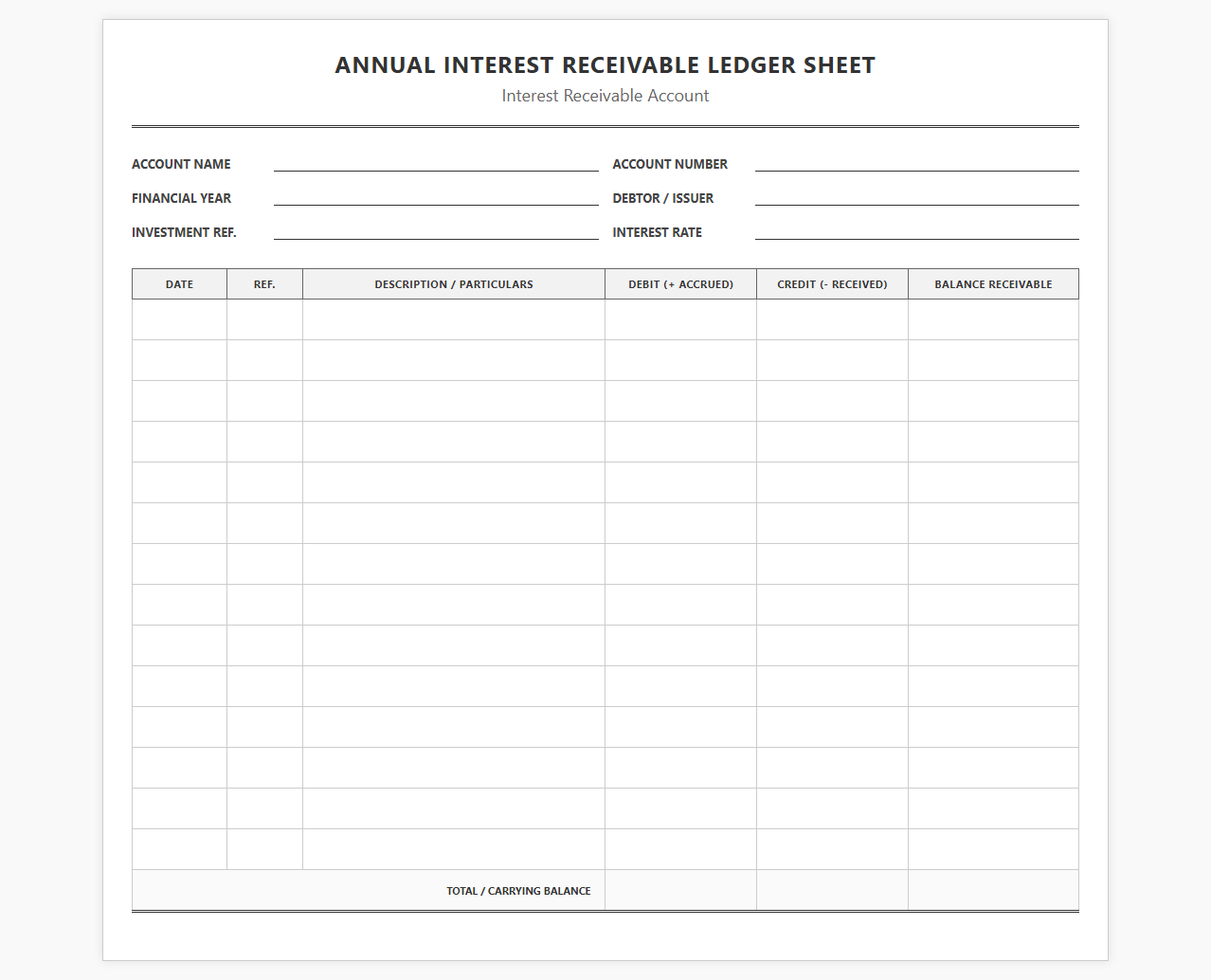

Annual Interest Receivable Ledger Sheet

Download: .PDF

Download: .PDF

Interest Revenue Receivable Accounting Ledger

Download: .PDF

Download: .PDF

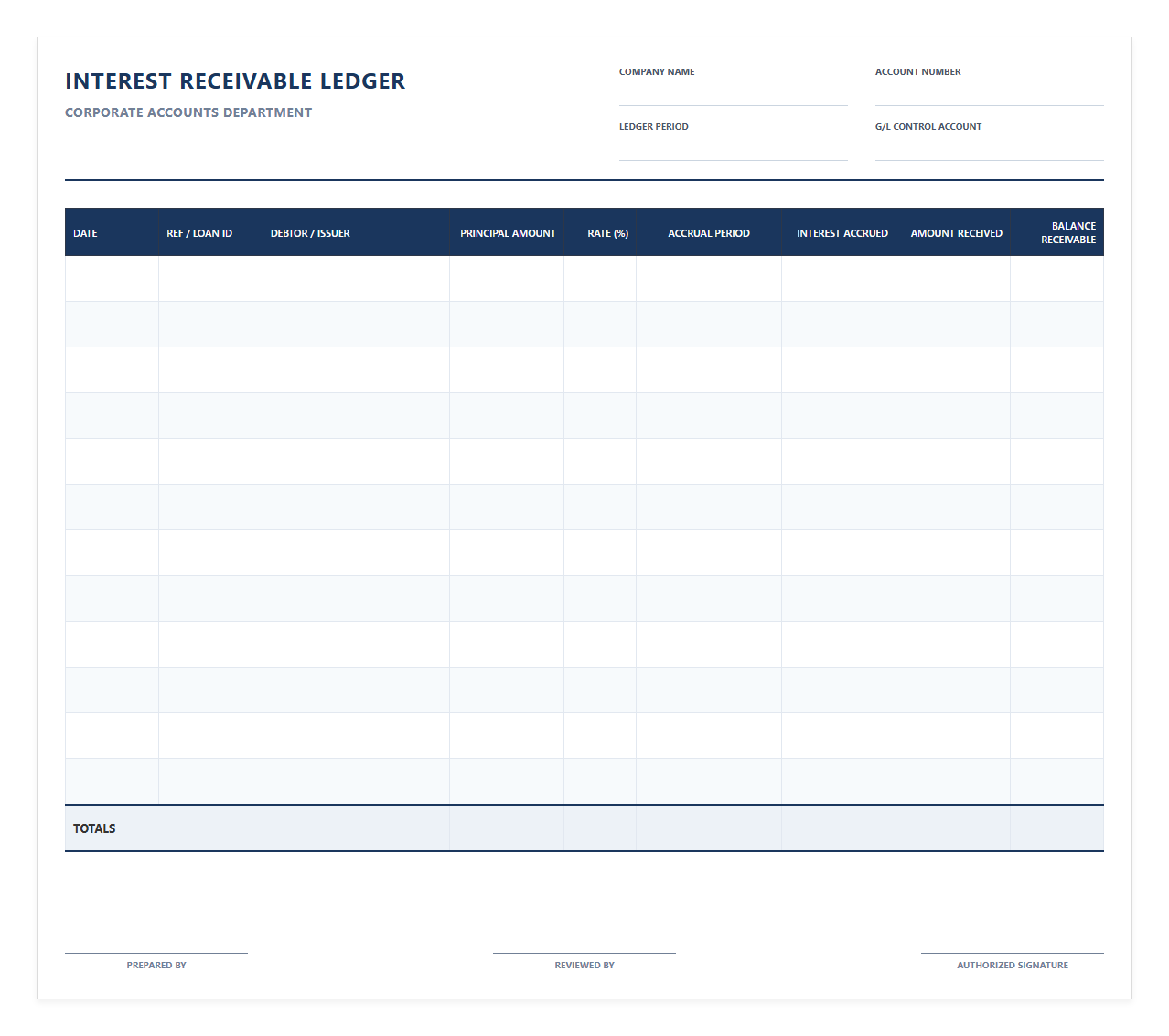

Corporate Interest Receivable Ledger Template

Download: .PDF

Download: .PDF

Understanding Accrued Income Discrepancies in Corporate Accounting

In corporate finance, even minor discrepancies in accrued interest can trigger significant cascading errors across financial statements. When interest receivable is tracked inaccurately, it misrepresents a company's current assets and net income, potentially misleading stakeholders and regulatory bodies. Precise interest receivable tracking is not merely a bookkeeping requirement; it is a critical pillar of robust financial reporting that ensures the balance sheet reflects the true economic reality of the enterprise.

The Anatomy of an Interest Receivable Ledger

An interest receivable ledger serves as the single source of truth for all earned but unpaid interest income. This specialized sub-ledger tracks outstanding financial claims, ensuring that every dollar of accrued revenue is accounted for before cash actually changes hands. To maintain maximum accuracy, a standard ledger must systematically record several core data points.

- Principal Amount: The baseline capital balance upon which interest calculations are performed.

- Interest Rate: The contractual rate, explicitly noting whether it is fixed, variable, or tiered.

- Accrual Period: The precise timeframe, specifying the start and end dates for the current calculation cycle.

- Payment Date: The scheduled calendar date when the accrued interest is contractually due to be paid.

Common Triggers of Accrued Interest Reconciliation Errors

Despite rigorous accounting standards, discrepancies frequently slip into financial records due to operational oversight or system mismatches. Identifying these triggers early is key to maintaining ledger integrity. Reconciliation errors typically stem from a few predictable operational areas:

- Mismatched Calculation Periods: Discrepancies often arise when the internal ledger uses a different day-count convention (such as Actual/360 or 30/360) than the external financial institution.

- Incorrect Compounding Assumptions: Applying simple interest formulas to accounts that utilize compound interest structures leads to compounding variances over time.

- Timing Differences in Cash Receipt Recognition: Discrepancies occur when cash payments are received near the end of a reporting period but are not recorded simultaneously by both parties, leading to cutoff errors.

A Step-by-Step Framework for Resolving Ledger Discrepancies

When discrepancies do appear, bookkeepers require a structured, logical methodology to identify and correct the underlying errors without disrupting the broader accounting system.

- Extract and Align Data: Gather the interest receivable ledger and the corresponding bank statements for the target period, ensuring both datasets cover the exact same timeframes.

- Perform a Global Recalculation: Independently calculate the expected interest using the agreed-upon principal, rate, and day-count convention to establish a baseline.

- Isolate the Variances: Compare the system-generated figures against the bank statements line by line to pinpoint the exact dates where the balances diverge.

- Investigate Timing and Adjustments: Verify whether any outstanding deposits or bank holidays caused a delay in cash application, adjusting the ledger journal entries accordingly.

Essential Features of Professional Ledger Templates

To prevent human error and streamline the reconciliation process, organizations rely on standardized ledger templates. A professional template removes manual calculation risks by integrating structural controls directly into the worksheet environment.

- Automated dynamic formulas that calculate daily, monthly, or annualized accruals instantaneously.

- Data validation rules that prevent users from entering invalid date formats or negative interest rates.

- Dedicated audit trail fields that require users to log the reason, date, and author of any manual adjustments.

Best Practices for Maintaining Accurate Interest Accruals

Preventative controls are far more efficient than retroactive corrections. Establishing proactive habits within the accounting department keeps financial data pristine year-round.

"Regular, scheduled reconciliations paired with automated validation workflows represent the gold standard for interest accrual integrity. By embedding these controls into monthly close checklists, corporate finance teams can identify and resolve minor variances before they escalate into material balance sheet adjustments."

Achieving Audit-Ready Financial Statements with Standardized Templates

Using standardized ledger templates does more than simplify daily math; it safeguards the entire organization against compliance risks. When regulatory bodies or external auditors review financial statements, they look for systematic processes and clear audit trails. Implementing structured templates ensures that every calculation is transparent, reproducible, and verifiable, paving the way for smooth year-end audits and flawless financial reporting.

Leave a comment