Managing fluctuating state and federal unemployment tax liabilities often leaves payroll administrators facing stressful audit discrepancies and calculation errors. Before investing in expensive software, businesses must first establish a clear, standardized framework to understand and track these shifting regulatory obligations.

Utilizing a dedicated Unemployment Tax Payable Ledger Template grants financial controllers absolute clarity, transforming chaotic spreadsheets into a streamlined system of record. It is important to note, however, that these templates are not magic fixes; their utility relies entirely on the consistent, accurate categorization of quarterly payroll data. For instance, a robust ledger must track specific variables like federal FUTA (Form 940) caps and localized SUTA experience rates to ensure compliance.

In this article, we will examine how to set up your ledger, avoid common reconciliation pitfalls, and leverage these templates to ensure flawless quarterly filings.

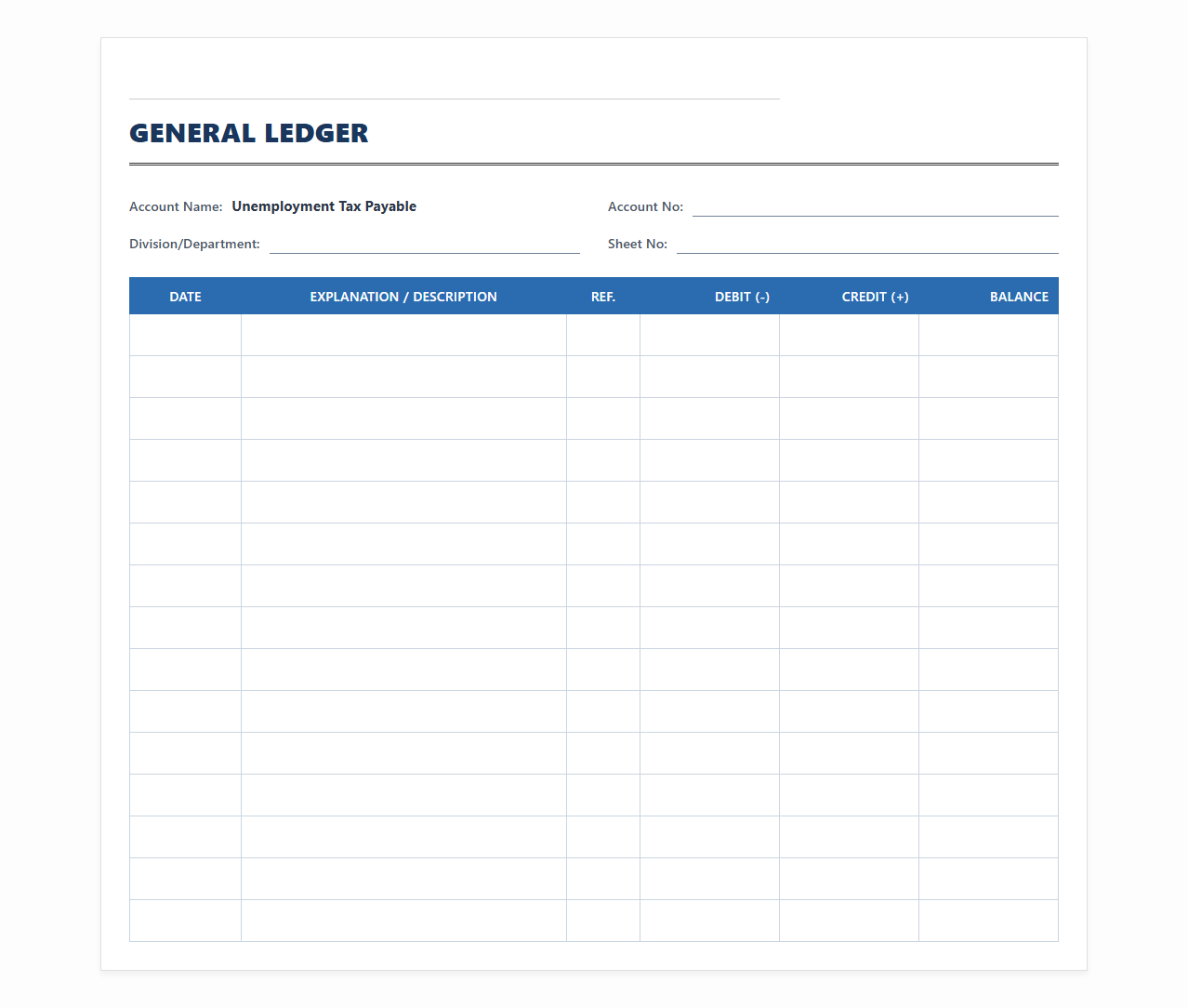

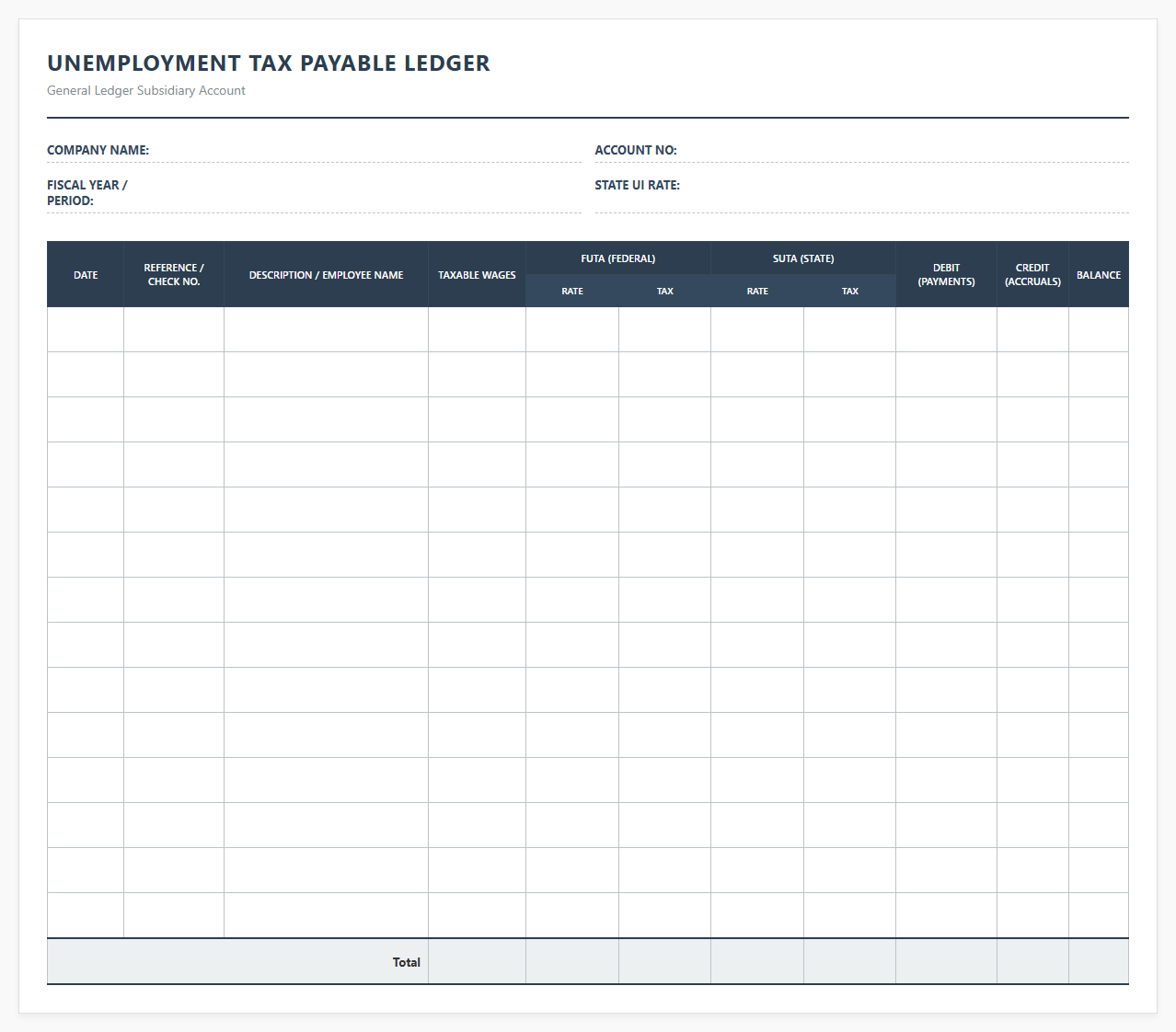

Unemployment Tax Payable General Ledger Sheet

Download: .PDF

Download: .PDF

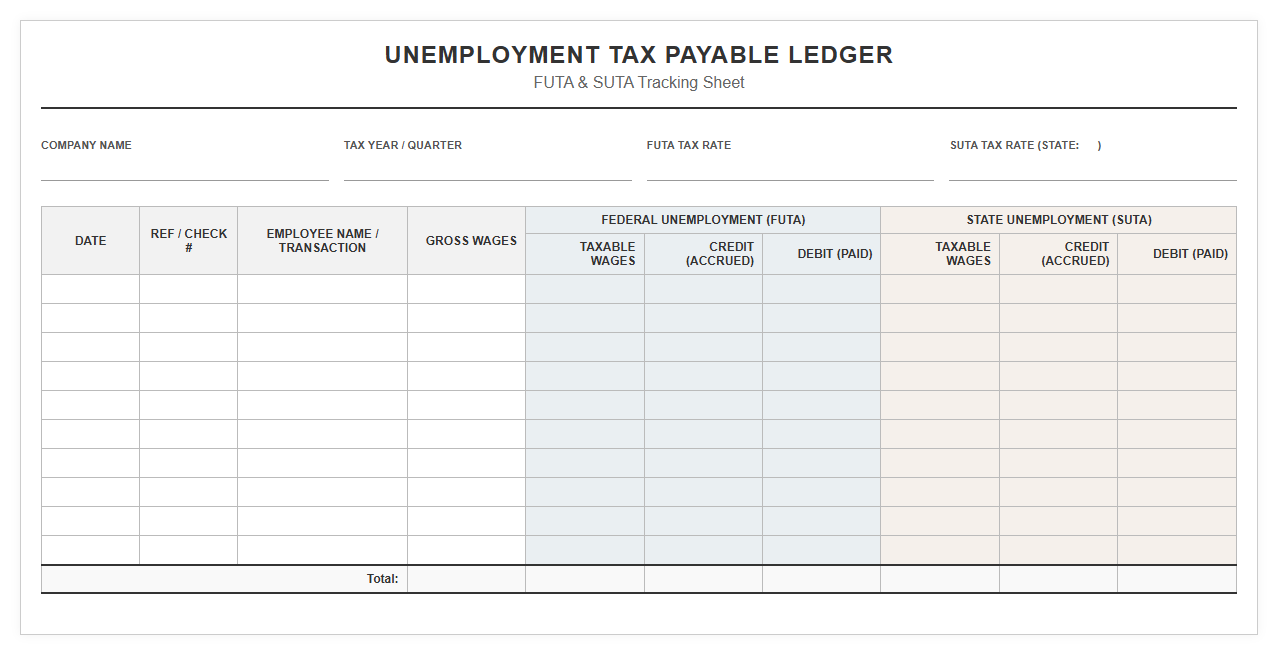

FUTA and SUTA Tax Payable Ledger Template

Download: .PDF

Download: .PDF

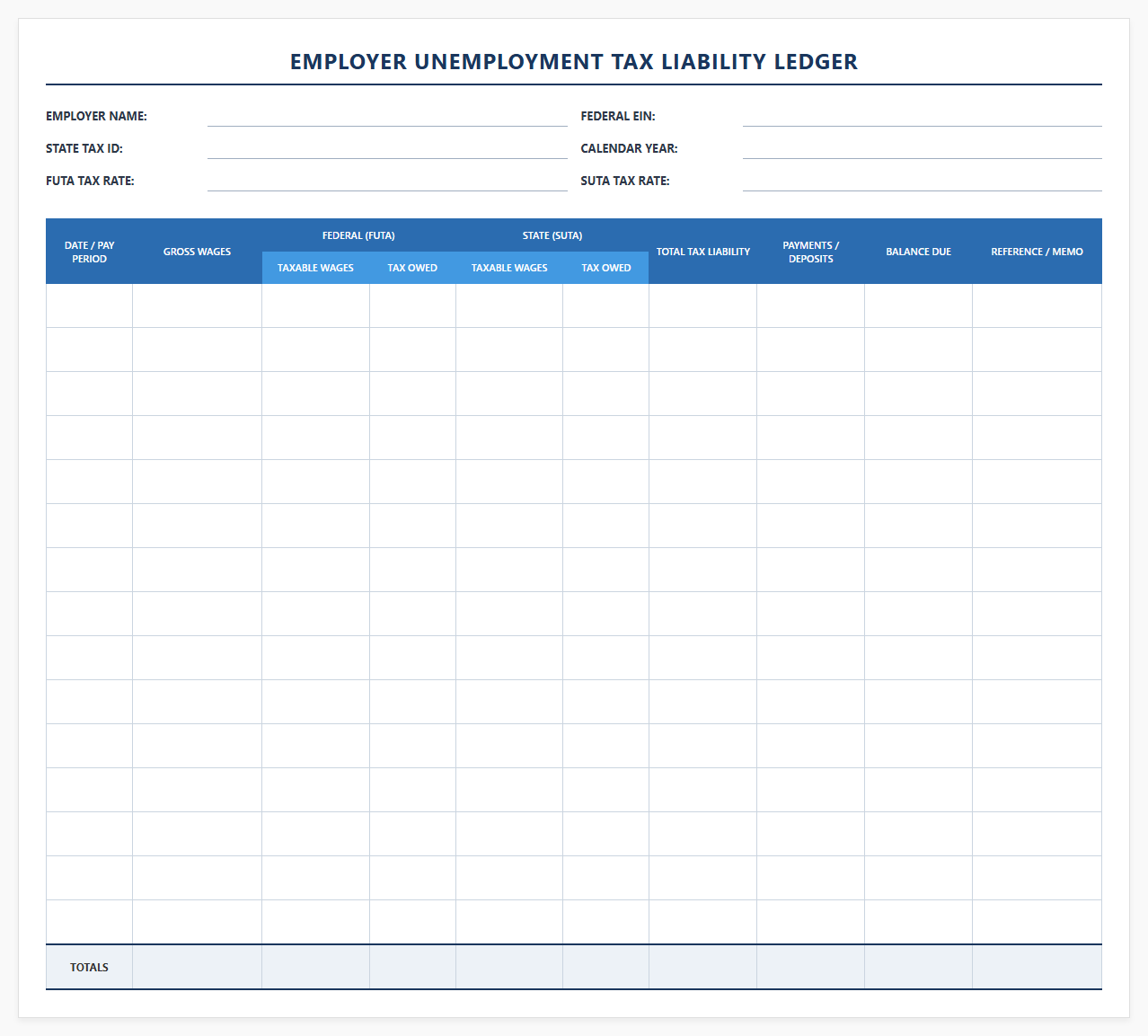

Employer Unemployment Tax Liability Ledger

Download: .PDF

Download: .PDF

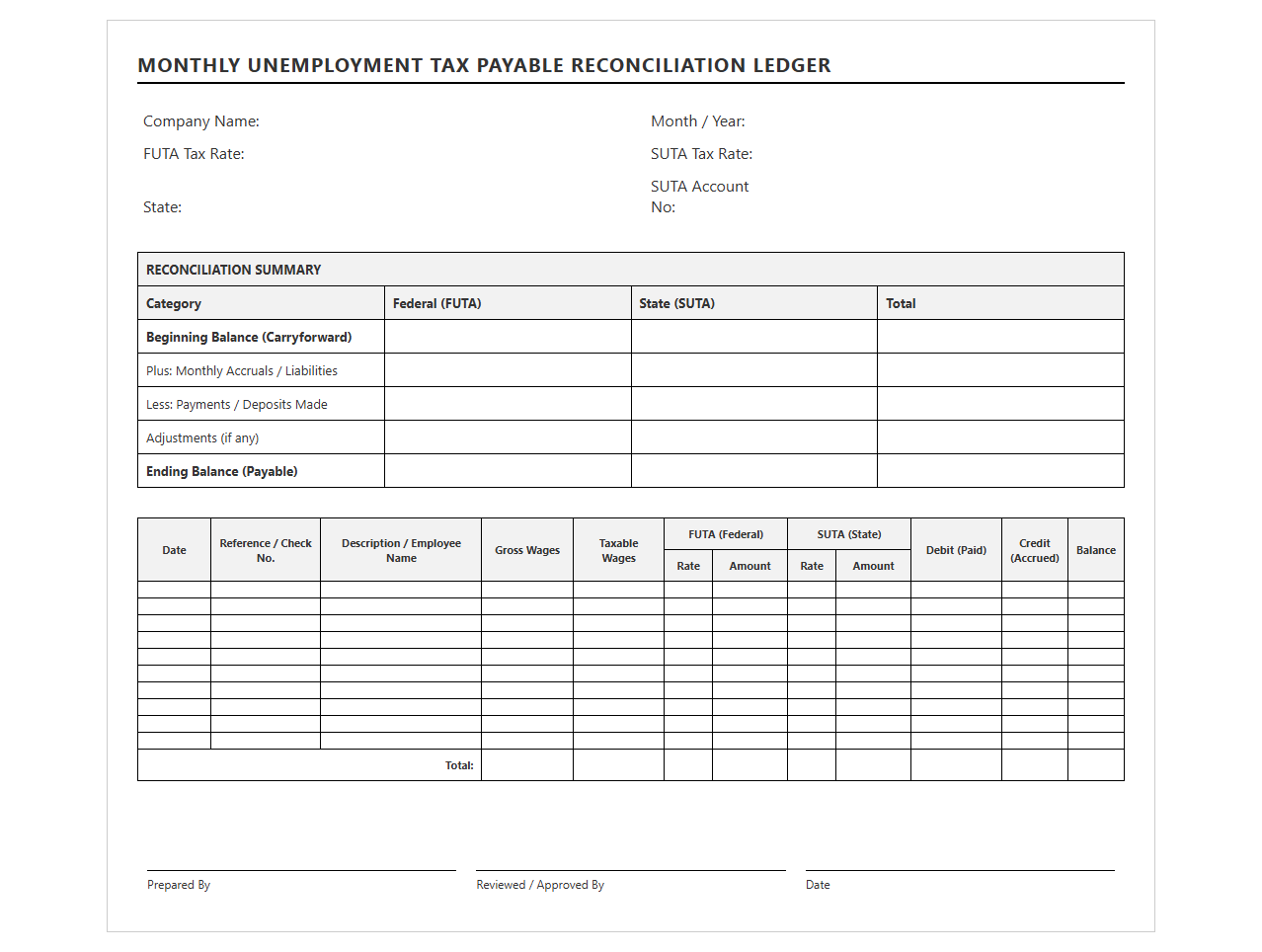

Monthly Unemployment Tax Payable Reconciliation Ledger

Download: .PDF

Download: .PDF

Payroll Unemployment Tax Payable Ledger Book

Download: .PDF

Download: .PDF

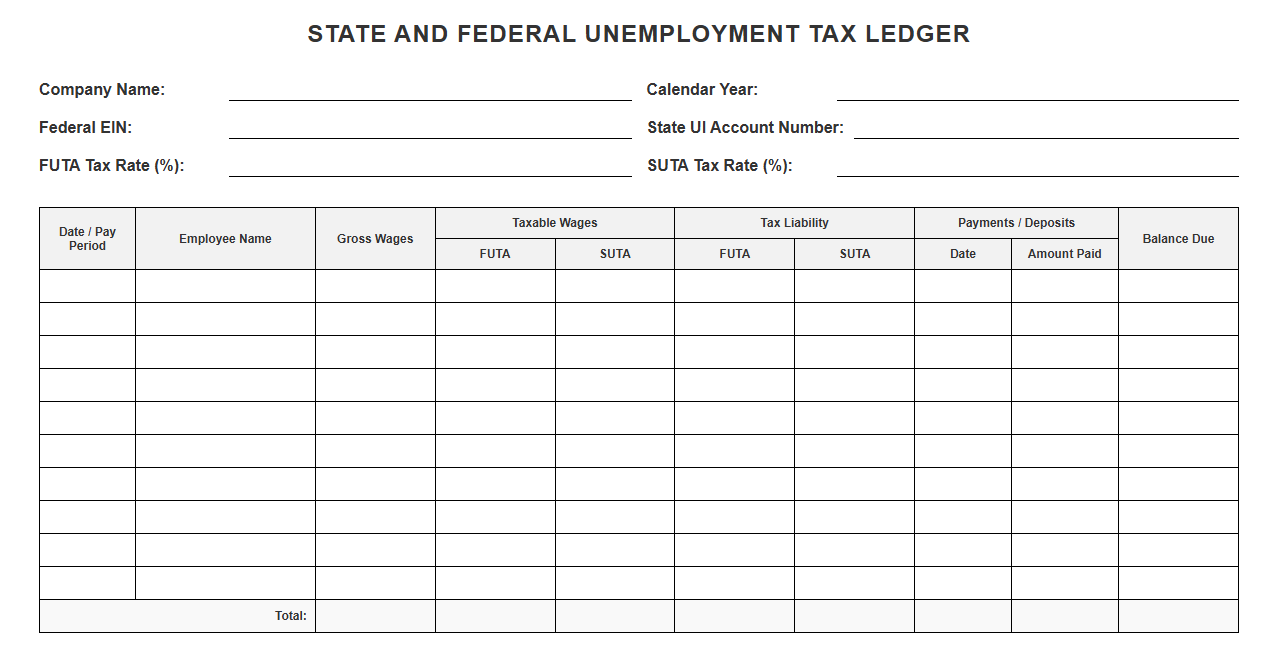

State and Federal Unemployment Tax Ledger

Download: .PDF

Download: .PDF

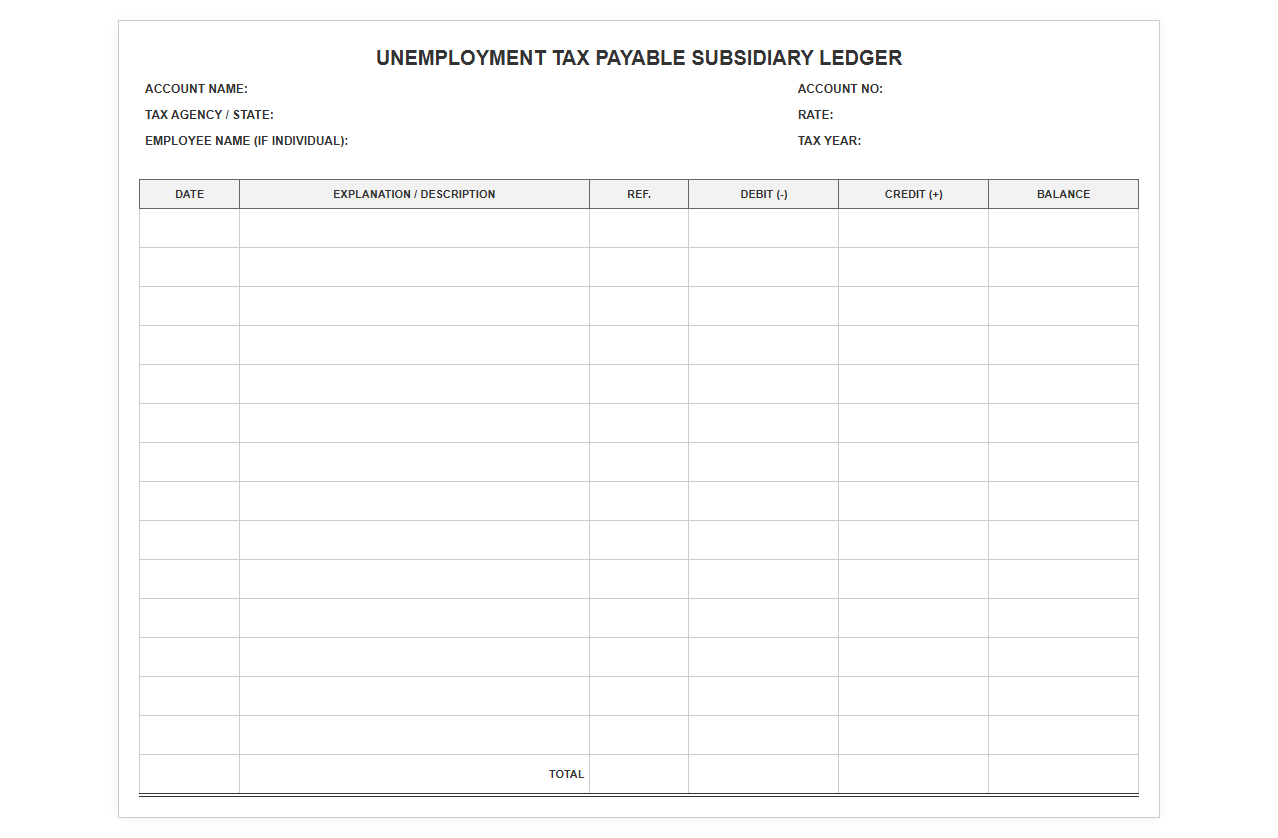

Unemployment Tax Payable Subsidiary Ledger Sheet

Download: .PDF

Download: .PDF

Annual Unemployment Tax Liability Tracking Ledger

![]() Download: .PDF

Download: .PDF

Demystifying Employer Unemployment Tax Liabilities

Employer unemployment tax liabilities represent the financial obligations businesses must pay to fund unemployment benefits for displaced workers. These liabilities are divided into federal and state levels. The Federal Unemployment Tax Act (FUTA) establishes a baseline tax rate, while the State Unemployment Tax Act (SUTA) varies by state and is influenced by an employer's industry and layoff history. Properly tracking these liabilities is critical for maintaining regulatory compliance and avoiding costly penalties.

The Role of an Unemployment Tax Payable Ledger

An Unemployment Tax Payable Ledger serves as the primary accounting tool for tracking payroll tax obligations. This dedicated subsidiary ledger allows businesses to isolate federal and state tax liabilities from general operating expenses. By utilizing this specialized tool, accounting teams can maintain financial accuracy and ensure that funds are appropriately reserved for quarterly and annual tax payments.

Essential Components of an Effective Ledger Template

- Pay Period Dates: Defines the specific timeframe for the payroll run.

- Gross and Taxable Wages: Separates total compensation from the portion subject to unemployment taxes.

- Tax Rates: Tracks individual rates for both SUTA and FUTA.

- Accrued Liabilities: Records the calculated tax amount owed for the period.

- Payment Dates: Logs when liabilities are cleared through actual payments.

Step-by-Step Guide to Recording Payroll Tax Transactions

- Input gross payroll data for the pay period to identify individual employee earnings.

- Apply the state and federal wage caps to determine the taxable portion using the formula:

Taxable Wages = Gross Wages (up to limit). - Calculate SUTA liability by multiplying taxable wages by the specific state experience rate:

SUTA Owed = Taxable Wages * SUTA Rate. - Calculate FUTA liability, accounting for any state tax credits:

FUTA Owed = Taxable Wages * FUTA Rate. - Log the accrued liabilities in the ledger, and subsequently record the payment when the funds are transferred to the tax authorities.

Reconciling Ledger Balances with Quarterly Tax Filings

Regular reconciliation is the cornerstone of robust payroll accounting. At the end of each quarter, businesses must cross-reference the accrued balances in their unemployment tax payable ledger with actual state quarterly returns and IRS Form 940. Discrepancies often arise from timing differences or calculation errors. Identifying these mismatches early ensures that the company's financial records reflect true tax obligations before submitting final filings.

Common Pitfalls in Unemployment Tax Accounting

Many businesses struggle with unemployment tax accounting due to easily preventable oversights. A common error is failing to stop tax calculations once an employee's year-to-date earnings exceed the annual wage base limit.

"Neglecting to update SUTA experience rates at the beginning of the fiscal year is a primary cause of inaccurate tax filings and unexpected state penalties."

Streamlining Compliance with Standardized Templates

Adopting a standardized ledger template significantly simplifies the management of payroll liabilities. By automating calculations and establishing a consistent structure, companies ensure high levels of audit readiness and save valuable administrative time.

Leave a comment