Managing wage garnishments is a persistent administrative burden, where a single calculation error can trigger severe regulatory penalties and damage employee trust. Before addressing these operational bottlenecks, organizations must first recognize that systemic payroll compliance relies on a foundation of airtight, auditable documentation.

Deploying structured ledger templates grants payroll departments the precise control needed to eliminate calculation errors and streamline reporting. However, an important educational stipulation remains: while these templates optimize tracking, they are tools for organization and do not replace professional legal counsel or state-specific statutory directives.

To illustrate, managing differing withholding limits for a Chapter 13 bankruptcy order versus a federal student loan levy requires distinct, rule-based tracking methods. This article will examine how standardized ledger systems can insulate your organization from compliance risks, detailing critical template structures and implementation best practices for your team.

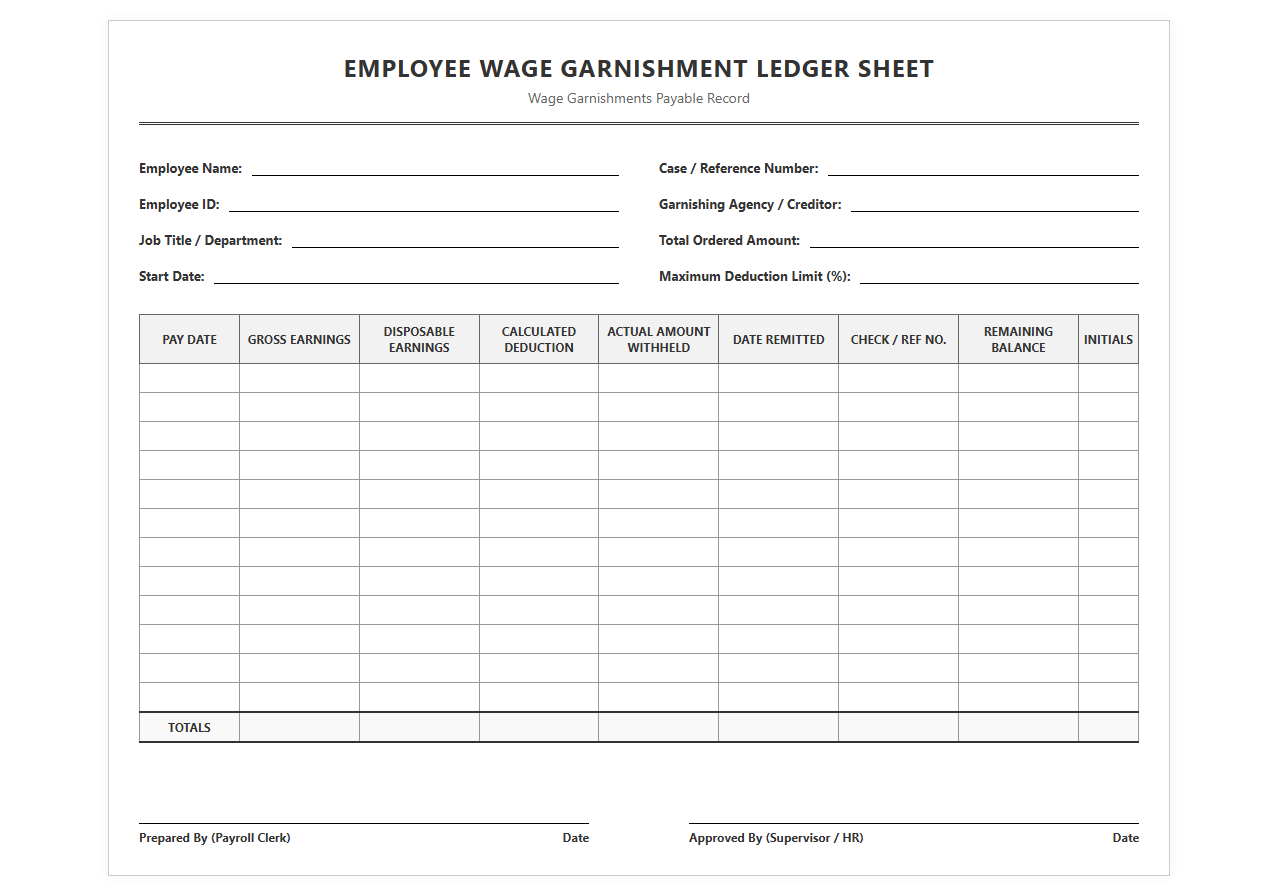

Employee Wage Garnishment Ledger Sheet

Download: .PDF

Download: .PDF

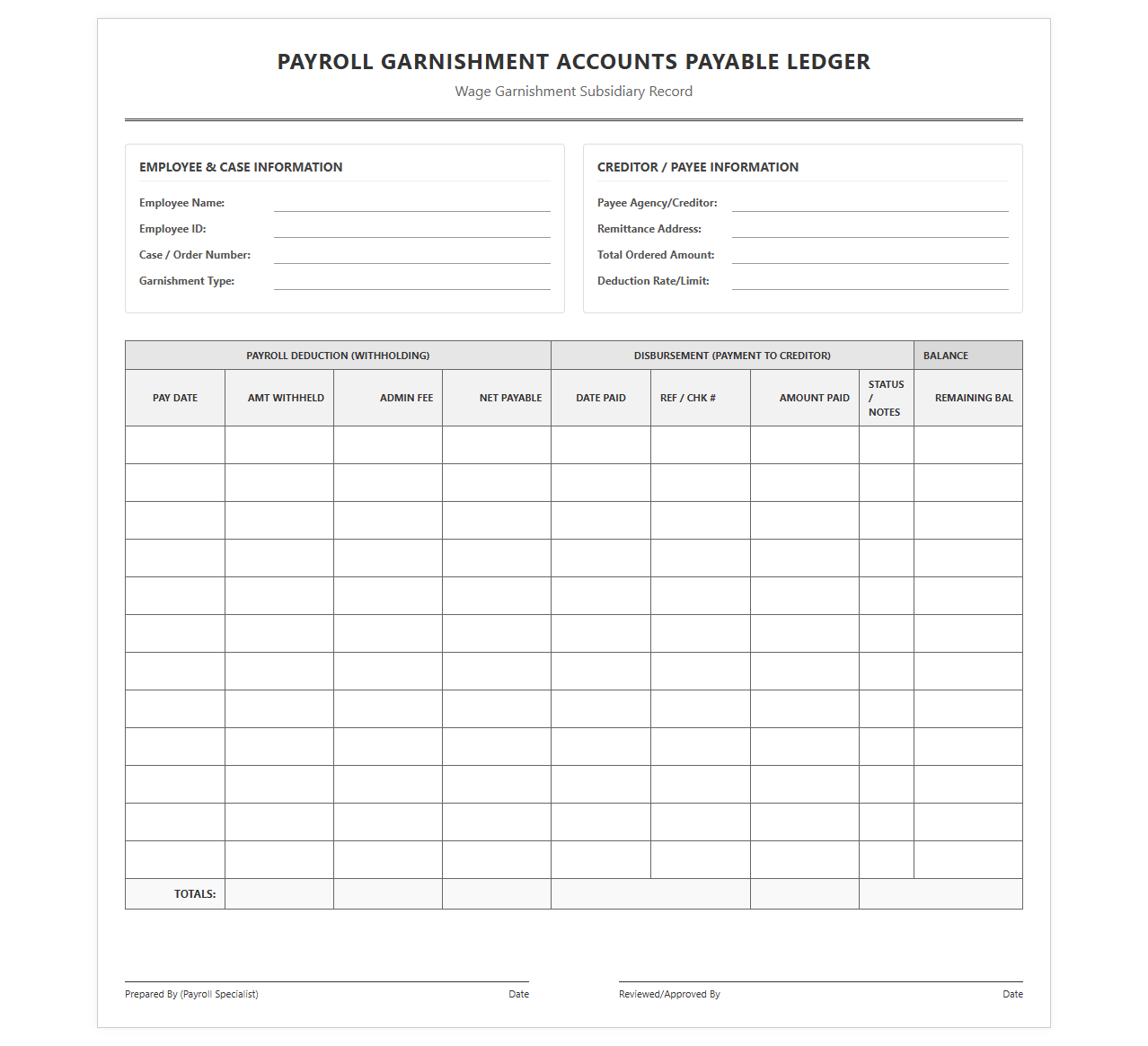

Payroll Garnishment Accounts Payable Ledger

Download: .PDF

Download: .PDF

Court-Ordered Wage Deduction Tracking Ledger

![]() Download: .PDF

Download: .PDF

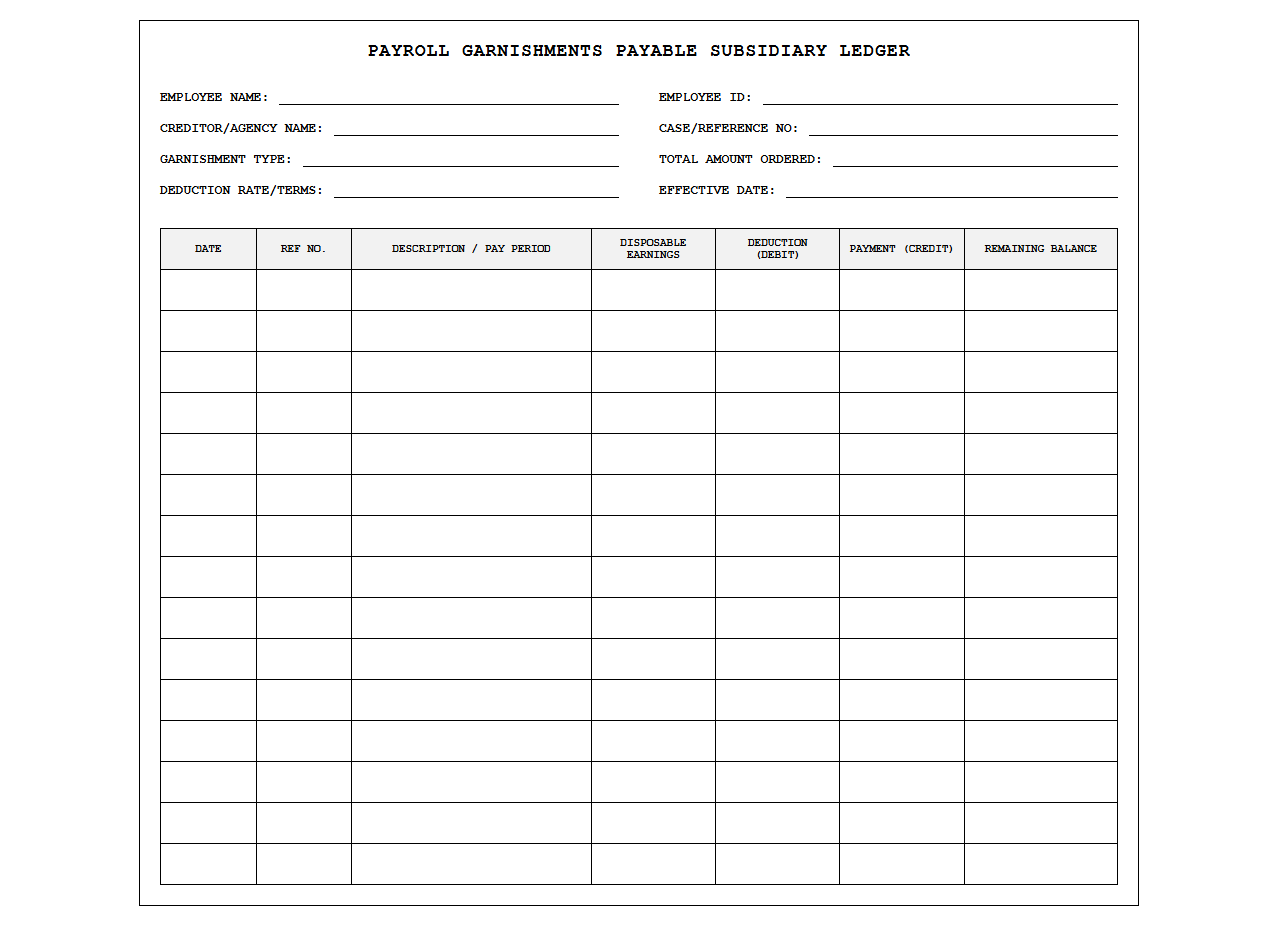

Payroll Garnishments Payable Subsidiary Ledger

Download: .PDF

Download: .PDF

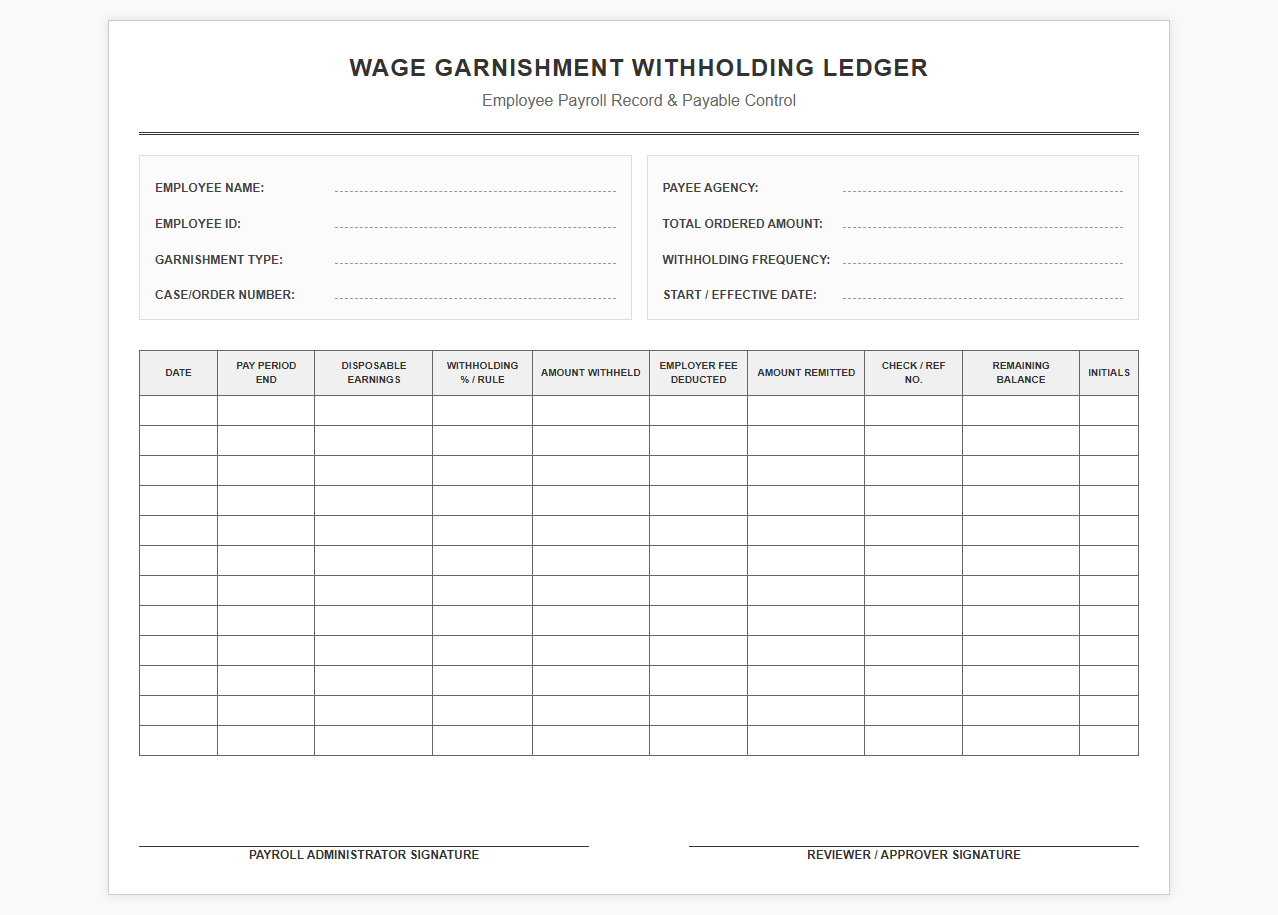

Employee Garnishment Withholding Ledger Template

Download: .PDF

Download: .PDF

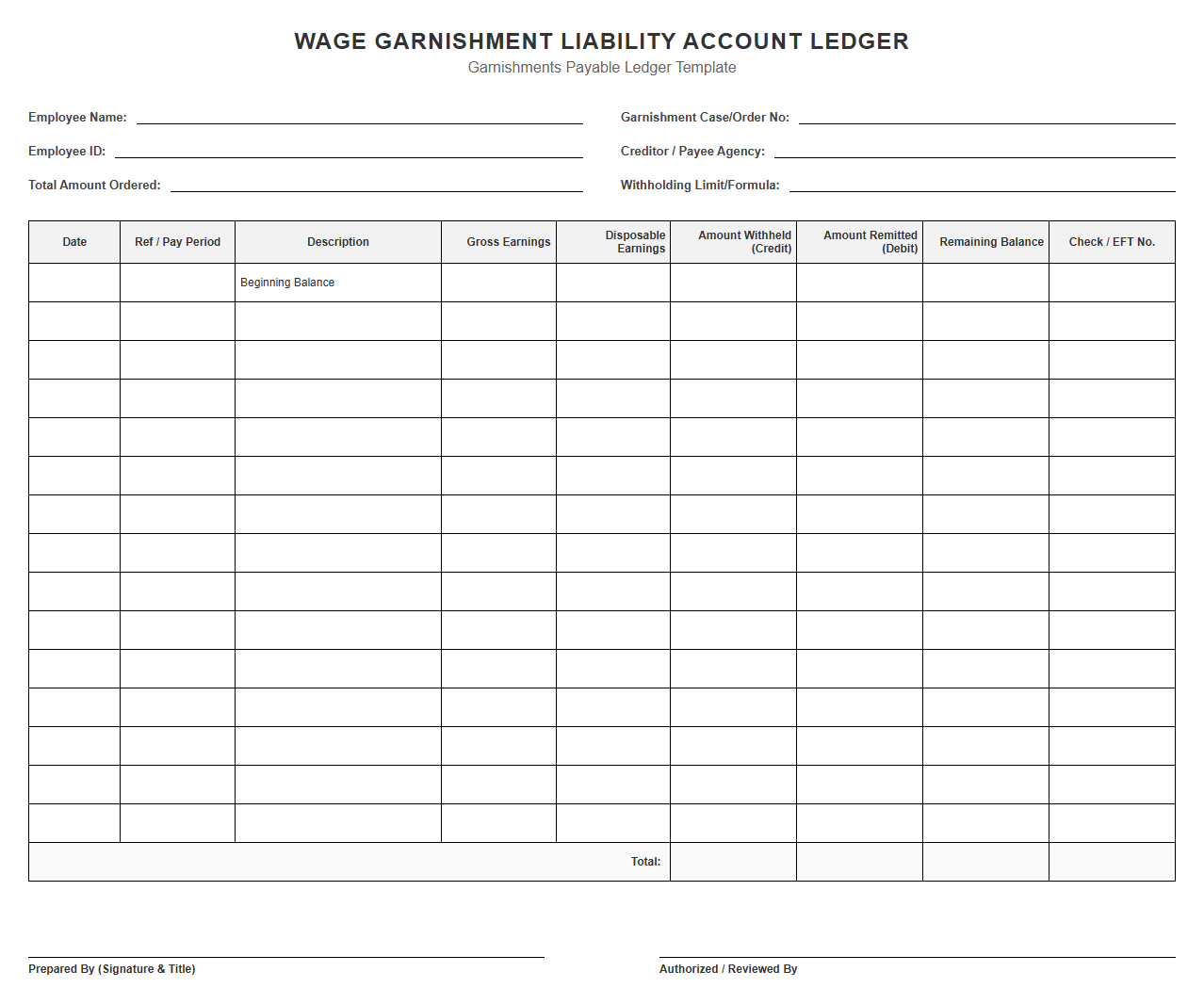

Wage Garnishment Liability Account Ledger

Download: .PDF

Download: .PDF

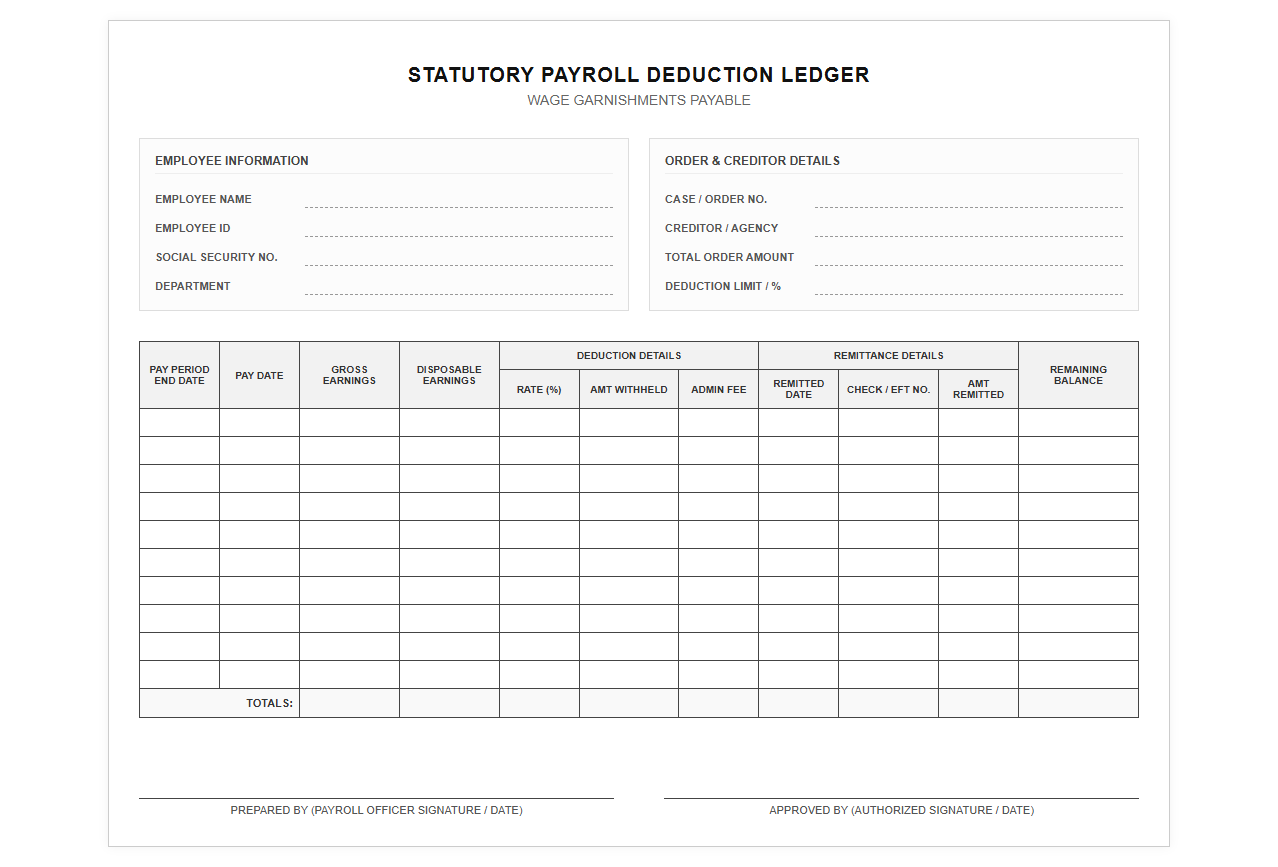

Statutory Payroll Deduction Ledger for Garnishments

Download: .PDF

Download: .PDF

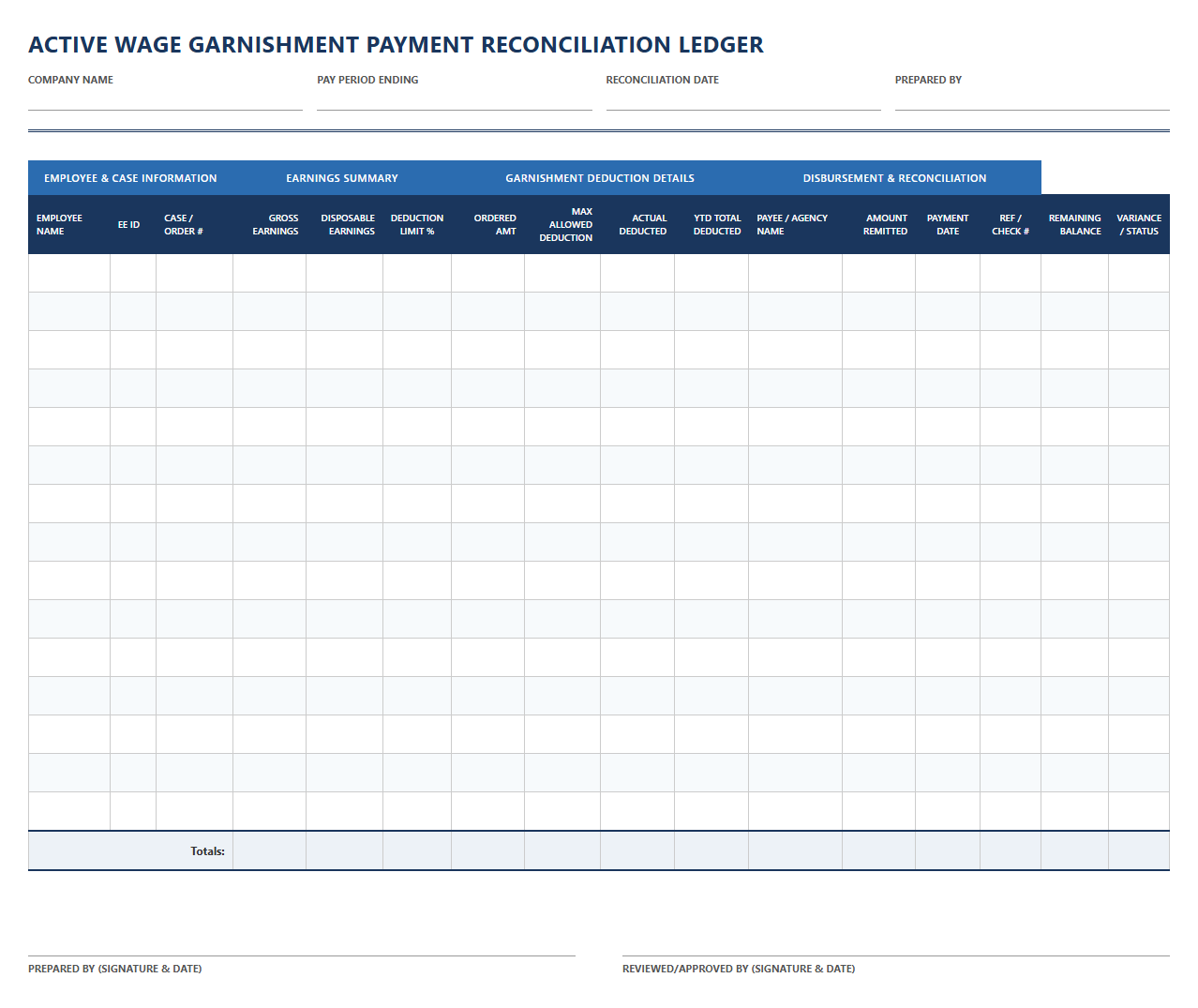

Active Wage Garnishment Payment Reconciliation Ledger

Download: .PDF

Download: .PDF

Introduction to Wage Garnishment Compliance and Ledger Controls

Wage garnishment processing is a highly regulated payroll function that carries severe financial and legal liabilities for employers who fail to comply. When an organization receives a withholding order for child support, tax levies, student loans, or creditor garnishments, it is legally bound to act as a trustee of the state or federal agency. Failing to withhold the correct amount, delaying payments, or miscalculating disposable earnings can result in direct corporate liability, statutory penalties, and costly litigation.

To mitigate these compliance hazards, organizations must establish structured ledger templates. These control frameworks act as a system of record that standardizes the calculation of disposable earnings, enforces statutory withholding limits, and tracks payment histories. By maintaining a disciplined, audit-ready ledger system, payroll departments protect the organization from operational errors and ensure strict adherence to both federal and state mandates.

Structural Architecture of a Compliant Garnishment Ledger

A compliant garnishment ledger requires a standardized, relational schema to ensure complete data segmentation and data integrity. This prevents the blending of unrelated employee garnishments and allows for granular tracking of individual withholding orders.

Employee Demographics Segment

The foundational layer of the ledger stores static employee identification metrics. This segment maps the unique identifier, such as employee_id, to the individual's payroll profile to ensure transactions are associated with the correct record.

Case Specifics Segment

This segment captures the immutable details of the legal order. Critical parameters include the court-issued case_number, the issuing jurisdiction, the total judgment balance, and the specific withholding type (e.g., child support, tax levy).

Transactional Ledger Segment

The core execution layer tracks the ongoing financial transactions for each pay cycle. This includes the calculation of disposable_earnings, the actual withheld amount, the remaining liability balance, and administrative fee tracking.

Critical Data Fields for Garnishment Tracking

| Field Identifier | Data Definition | Regulatory Relevance |

|---|---|---|

| Case ID / Order Number | The unique legal identifier issued by the court or state agency. | Ensures payments are allocated to the correct legal file. |

| Withholding Category | The classification of debt (e.g., Child Support, Federal Tax Levy, Creditor). | Determines the statutory priority and maximum withholding limits. |

| Disposable Earnings | Gross earnings minus legally mandated deductions (taxes, social security). | Serves as the basis for calculating maximum allowable garnishment. |

| CCPA Limit Percentage | The maximum withholding percentage allowed under the Consumer Credit Protection Act. | Prevents unconstitutional over-withholding of employee wages. |

| Remaining Balance | The outstanding total debt remaining on the legal order. | Signals the exact pay cycle when withholding must cease. |

Managing Competing Garnishments and Priority Logic

- Identify the classification of each incoming withholding order to determine its statutory priority level under federal and state law.

- Apply the priority hierarchy rules, which universally place child support and alimony orders at the highest level of precedence, followed by federal administrative tax levies.

- Assess the receipt date of creditor garnishments, as standard commercial debts are generally prioritized on a "first-come, first-served" basis.

- Calculate the cumulative maximum withholding threshold for the pay period under the Consumer Credit Protection Act (CCPA) to prevent over-withholding.

- Allocate available funds sequentially down the priority chain until the maximum CCPA limit is reached, ensuring any remaining lower-priority orders are safely deferred.

Calculation Methodologies for Disposable Earnings

Calculating the correct withholding amount begins with establishing disposable earnings. Unlike gross earnings or net take-home pay, disposable earnings represent gross wages minus only legally mandated deductions (such as federal income tax, state income tax, local taxes, FICA, and state disability insurance). Voluntary deductions like 401(k) contributions, health insurance premiums, and union dues do not reduce disposable earnings.

[Gross Wages] - [Mandatory Taxes/FICA] = [Disposable Earnings]

[Disposable Earnings] * [Statutory CCPA Limit %] = [Maximum Allowable Withholding]

For example, if an employee has $1,000 in disposable earnings and is subject to a standard creditor garnishment (limited to 25% under the CCPA), the maximum withholding is $250. For a child support order where the limit can rise to 50% or 60% depending on the employee's marital and dependent status, the maximum withholding on that same $1,000 of disposable earnings would be $500 or $600 respectively.

Establishing Robust Audit Trails and Reconciliation

- Conduct monthly ledger-to-payroll reconciliations to verify that all amounts withheld match the payments remitted to custodial agencies.

- Verify remaining balances at the end of every payroll run to ensure wage withholding automatically stops once the judgment is satisfied.

- Document and store all calculations used to determine disposable earnings, including explicit records of excluded voluntary deductions.

- Log the date and timestamp of all incoming garnishment orders to provide indisputable evidence of priority logic application in court.

- Perform quarterly internal audits on random samples of active garnishments to detect and correct any processing discrepancies before regulatory intervention.

Integrating Ledger Templates with Payroll Systems

Manual structured ledger templates provide the necessary blueprint for compliance, but integrating these structured architectures directly into automated ERP and payroll software is critical to eliminate human error at scale. Modern payroll systems rely on API integrations and custom database schemas to translate structured ledger rules into automated execution, ensuring calculations are performed instantly upon payroll entry.

"Integrating standardized ledger schemas into core ERP architectures transforms wage garnishment from an error-prone manual chore into a highly predictable, automated, and audit-safe operational workflow."

To learn more about implementing compliant payroll architectures and understanding federal withholding boundaries, consult the U.S. Department of Labor or review your state's specific garnishment guidelines.

Leave a comment