Managing accrued payroll liabilities often turns into a high-stakes reconciliation struggle for finance teams during month-end close. Before implementing advanced software, establishing a disciplined baseline of clear GAAP-compliant ledger tracking is essential to bridge the gap between cash outflows and earned-but-unpaid labor expenses.

Standardizing this process grants accounting departments absolute clarity in cash flow forecasting and flawless audit readiness. However, as an educational stipulation, please note that while standardized templates dramatically reduce errors, they must be customized to align with your specific jurisdiction's regulatory boundaries and payroll cycles.

To illustrate, our templates are built to handle complex, concrete variables such as partial-week hourly variances and accrued FUTA/SUTA liabilities. In the following sections, we will break down the mechanics of the wages payable ledger, provide downloadable template frameworks, and outline step-by-step reconciliation strategies to ensure your balance sheet remains impeccable.

Wages Payable General Ledger Sheet

Download: .PDF

Download: .PDF

Payroll Liabilities Ledger Template

Download: .PDF

Download: .PDF

Accrued Wages Payable Account Ledger

Download: .PDF

Download: .PDF

Wages Outstanding Ledger Book

Download: .PDF

Download: .PDF

Employee Wages Payable Record Template

Download: .PDF

Download: .PDF

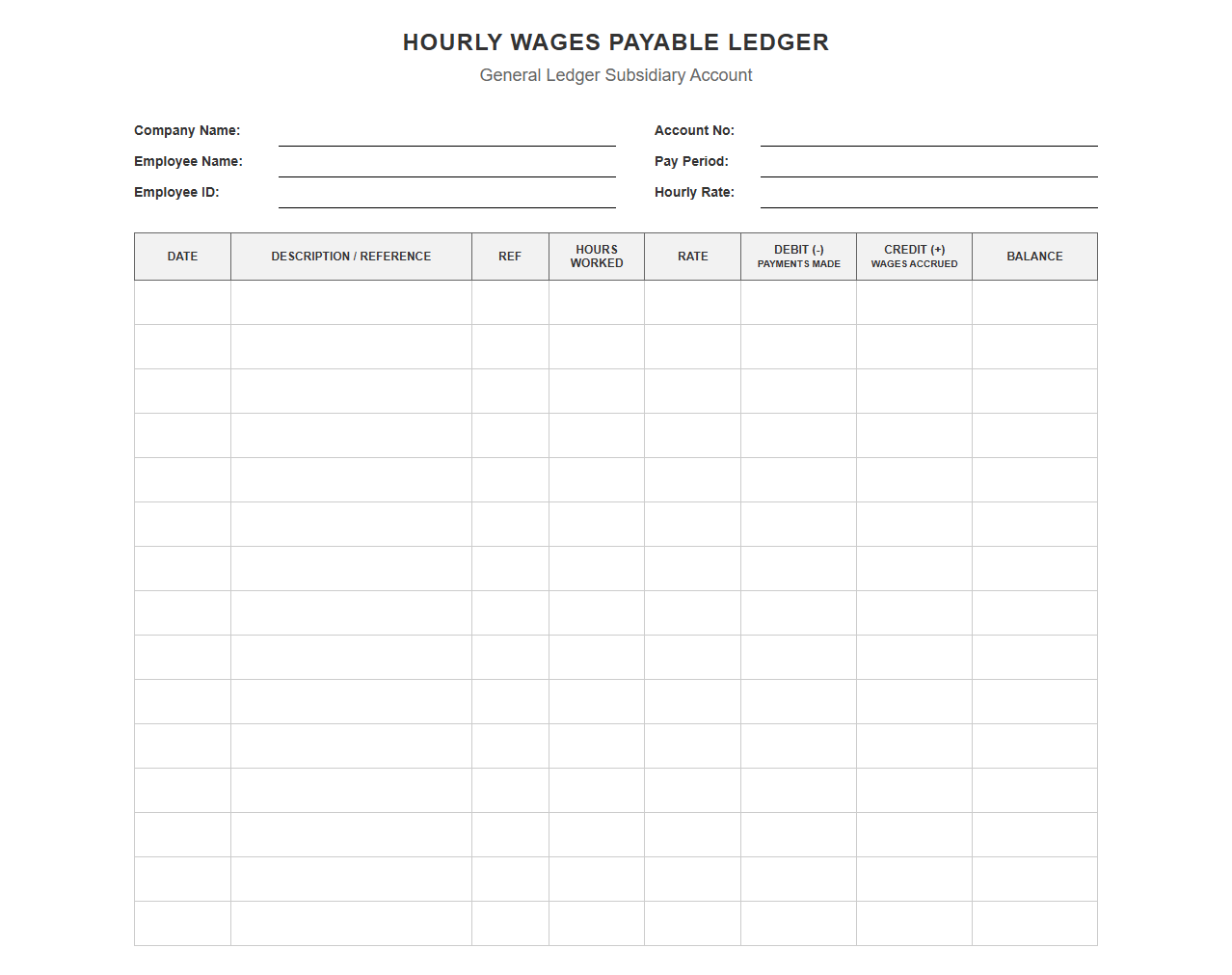

Hourly Wages Payable Accounting Ledger

Download: .PDF

Download: .PDF

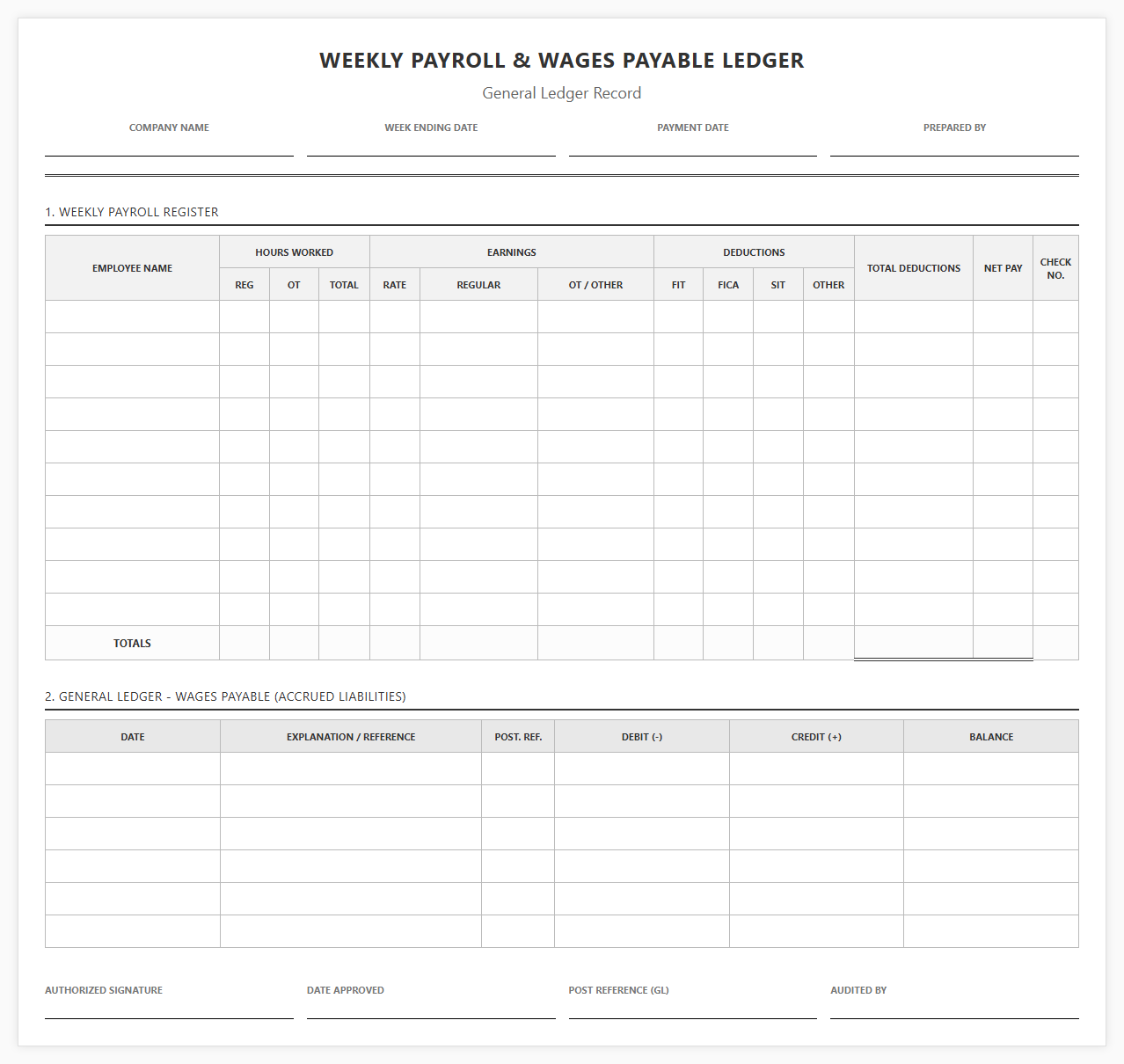

Weekly Payroll and Wages Payable Ledger

Download: .PDF

Download: .PDF

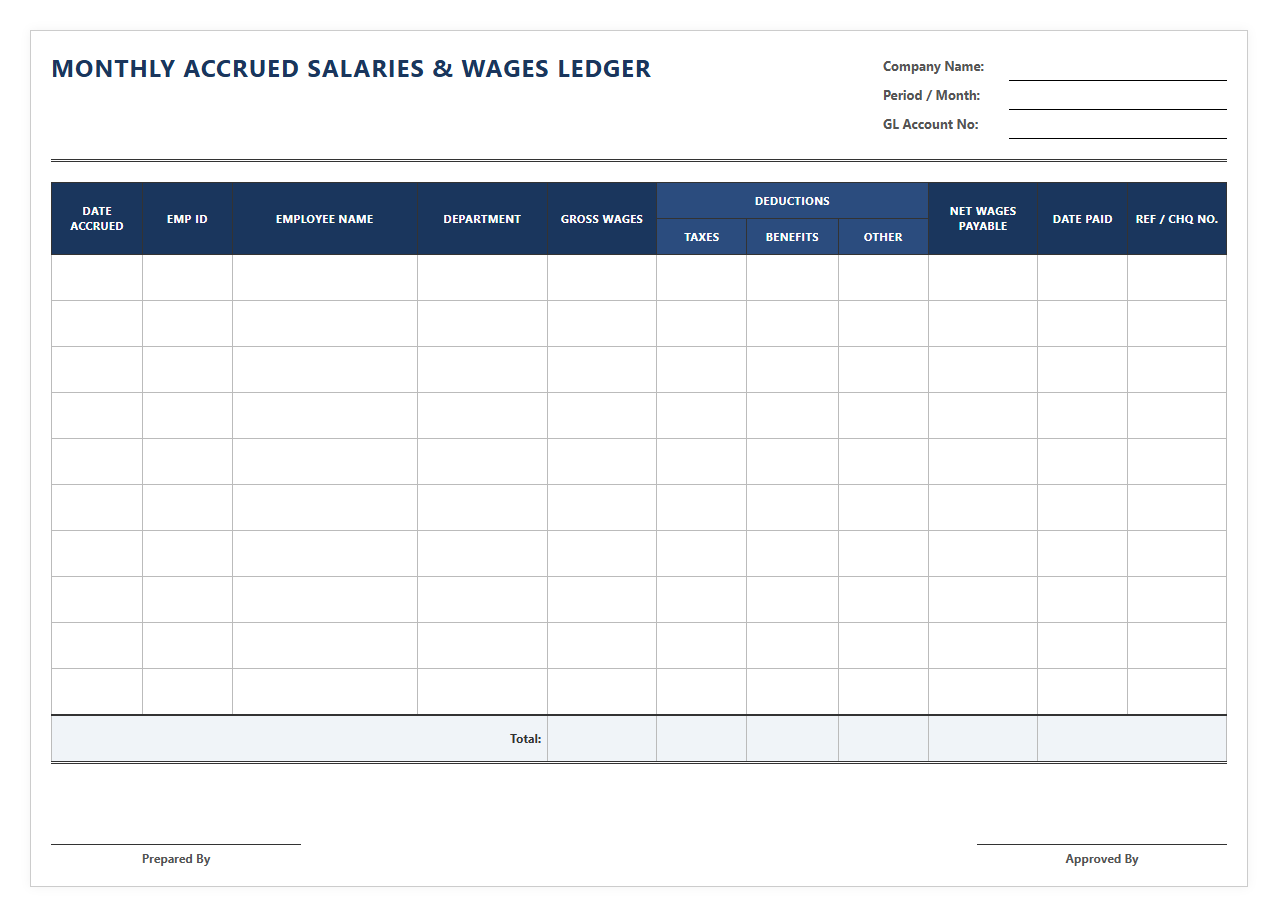

Monthly Accrued Salaries and Wages Ledger

Download: .PDF

Download: .PDF

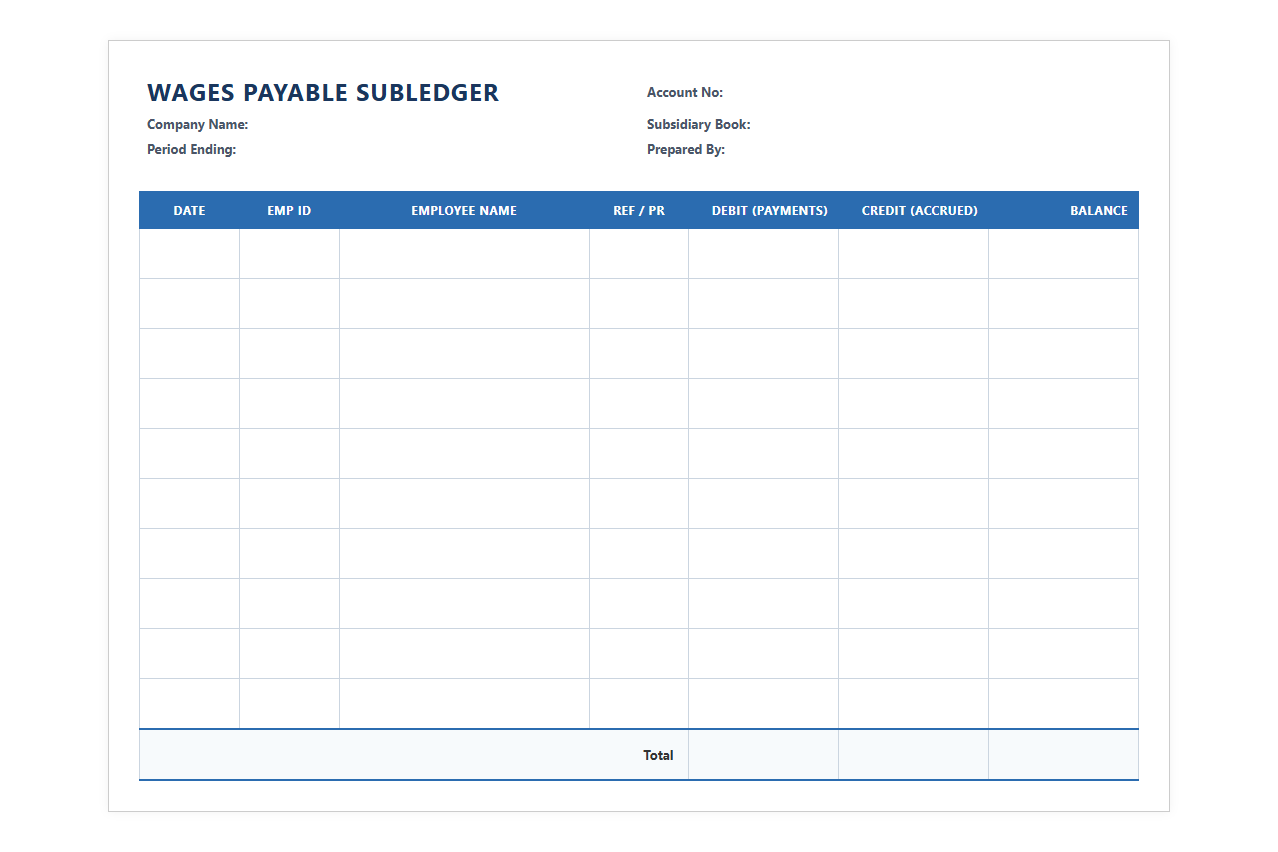

Wages Payable Subledger Template

Download: .PDF

Download: .PDF

Introduction to Accrued Payroll Liabilities

In modern corporate accounting, managing expenses accurately is vital for maintaining a transparent view of a company's financial standing. Accrued payroll liabilities represent the value of wages, salaries, and benefits that employees have earned but have not yet received as payment. This situation typically occurs at the end of a financial period when the payroll cycle does not perfectly align with the final days of the calendar month or fiscal year.

Recording these liabilities is essential for adhering to the accrual basis of accounting, which dictates that expenses must be recognized in the period they are incurred, regardless of when cash changes hands. On the balance sheet, these figures appear as current liabilities under headings such as wages payable or accrued payroll. Properly reporting these obligations ensures a company's financial health is represented accurately, preventing underestimation of expenses and overestimation of net income.

The Role of Standardized Wages Payable Ledgers

To track outstanding wage obligations effectively, finance teams rely heavily on structured record-keeping systems. Standardizing the wages payable ledger ensures that every transaction is documented uniformly. Consistency in record-keeping drastically reduces human error, eliminating discrepancies that arise from manual adjustments or non-standard tracking methods across different departments.

Furthermore, standardized templates act as an essential tool during external and internal financial reviews. They speed up audits by providing auditors with a clear, predictable audit trail. Adhering to a standardized format ensures strict compliance with major accounting standards, such as General Accepted Accounting Principles (GAAP) or International Financial Reporting Standards (IFRS), which mandate clear disclosures of all short-term employee benefits and obligations.

Anatomy of a Standardized Wages Payable Template

A reliable wages payable ledger template must be comprehensive enough to capture all necessary transactional details. Standardizing these columns allows for easy data verification and seamless integration with broader financial reports.

Every functional wages payable template should include the following core fields:

- Employee ID: A unique identifier to map payroll data to specific team members without privacy risks.

- Pay Period Dates: The exact start and end dates of the time frame during which the work was performed.

- Gross Wages: The total amount of compensation earned by the employee before any deductions.

- Tax Withholdings & Deductions: Fields detailing federal, state, and local taxes, alongside voluntary deductions like health insurance or retirement contributions.

- Net Pay: The final amount of cash owed to the employee after all authorized deductions are subtracted.

- Accrual Adjustments: A dedicated section for calculating partial pay period adjustments when the accounting cycle ends mid-week.

Step-by-Step Guide to Calculating and Recording Accruals

To accurately capture payroll obligations at the end of a financial period, accountants must perform specific calculations and journal entries. This ensures the expenses are recorded in the correct month or quarter.

- Identify the number of unpaid days that fall between the end of the last completed payroll cycle and the final day of the accounting period.

- Calculate the daily wage rate for each employee or department by dividing the standard periodic gross wages by the total working days in that cycle.

- Multiply the daily wage rate by the number of unpaid accrual days to determine the total accrued gross wages.

- Draft a journal entry debiting the Wages Expense account to reflect the cost incurred during the period.

- Credit the Wages Payable account to record the current liability on the balance sheet.

- Reverse this entry on the first day of the subsequent accounting period to prevent double-counting when the actual payroll is paid out.

Common Pitfalls in Accrued Payroll Tracking

One of the most frequent errors in tracking payroll liabilities is miscalculating partial pay periods. When a fiscal month ends in the middle of a workweek, teams often fail to prorate daily earnings accurately. This leads to understated liabilities on the balance sheet and skewed profitability metrics on the income statement.

Another major mistake is neglecting tax withholdings and employer-matched contributions during the accrual process. Failing to account for employer FICA taxes, unemployment insurance, and accrued vacation time creates a significant variance between estimated accruals and the actual cash required for disbursement. To avoid these issues, businesses should implement automated calculators within their spreadsheets and double-check calendar cutoffs monthly.

Integrating Ledger Templates with Accounting Software

While spreadsheets are excellent tools for preliminary calculations, manually entering this data into core financial platforms can be tedious. Modern organizations streamline this workflow by importing or syncing standardized ledger templates directly with major accounting software such as QuickBooks, Xero, or enterprise resource planning (ERP) systems. Saving files in standard formats like .CSV or .XLSX allows automated systems to map rows directly to corresponding ledger accounts.

Once mapped, accounting systems can instantly ingest the template data to generate the necessary journal entries automatically. This integration eliminates the risk of manual data entry errors, simplifies complex multi-currency adjustments, and ensures that the financial statements are updated in real-time as the payroll period closes.

Best Practices for Period-End Reconciliation

Reconciliation is the final line of defense against reporting errors. At the close of each month or fiscal year, accountants must verify that the accrued balances residing in the wages payable account match the actual cash disbursements executed during the subsequent payroll run. Any discrepancies, whether due to unexpected overtime or sudden departures, must be thoroughly investigated and corrected through adjusting journal entries.

Leave a comment