Managing the 0.9% Additional Medicare Tax often becomes a compliance minefield for payroll administrators. When high-earner salaries cross IRS thresholds unexpectedly, withholding errors frequently slip through, leaving payroll departments scrambling to resolve discrepancies under tight deadlines.

Navigating these adjustments requires a firm grasp of federal compliance before corrective action can begin. Utilizing standardized payroll document templates grants organizations an immediate operational advantage, transforming a complex audit risk into a structured, repeatable correction process.

Please Note: While these templates streamline administrative workflows, they function as operational guides and should not replace professional tax or legal counsel.

By leveraging specific resources-such as corrected Form W-2c templates, employee notification drafts, and IRS Form 8959 reconciliation sheets-reconciliation becomes highly manageable. In this article, we will examine how to deploy these essential templates, correct active withholding errors, and establish safeguards to prevent future payroll slip-ups.

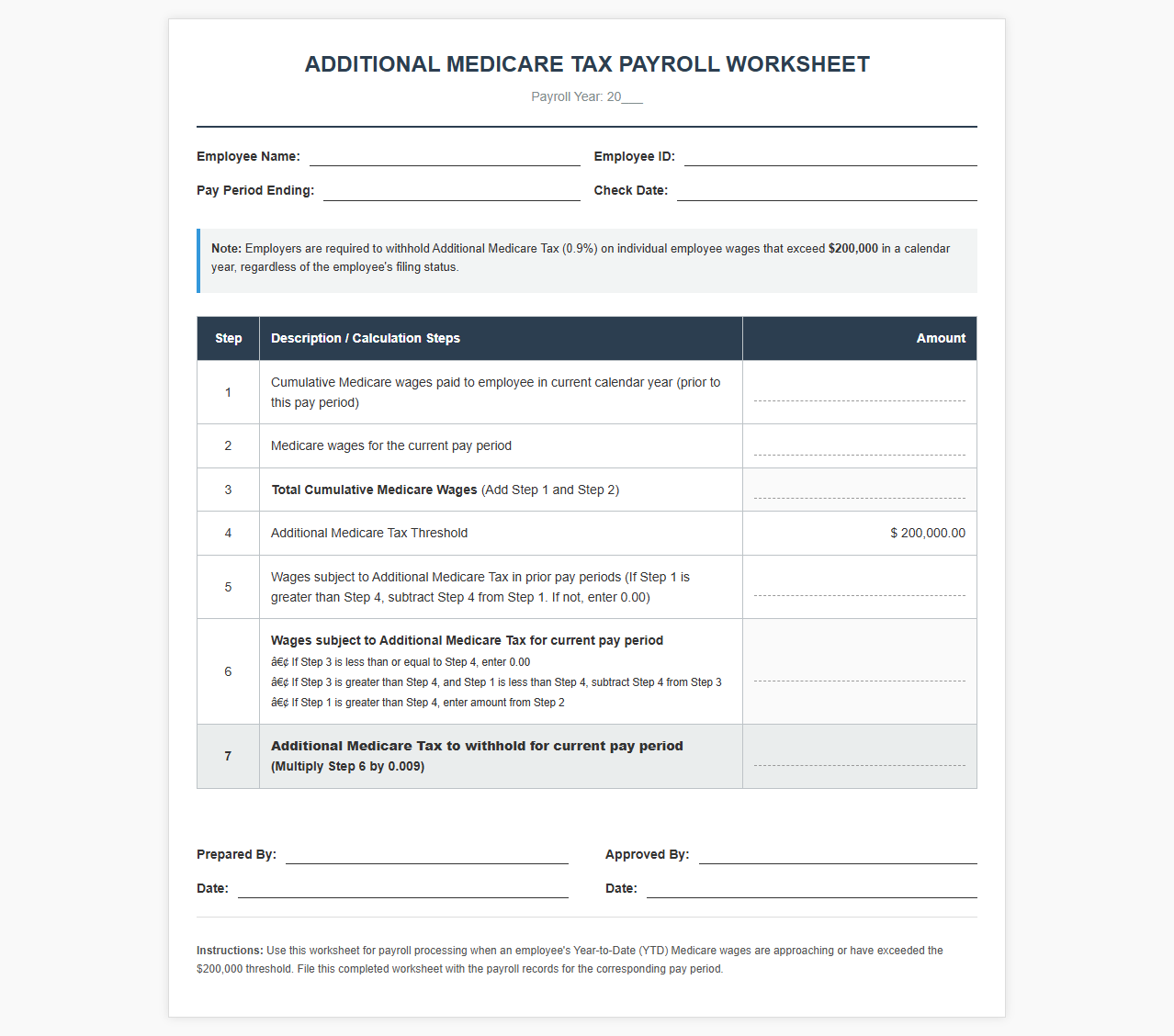

Additional Medicare Tax Payroll Worksheet

Download: .PDF

Download: .PDF

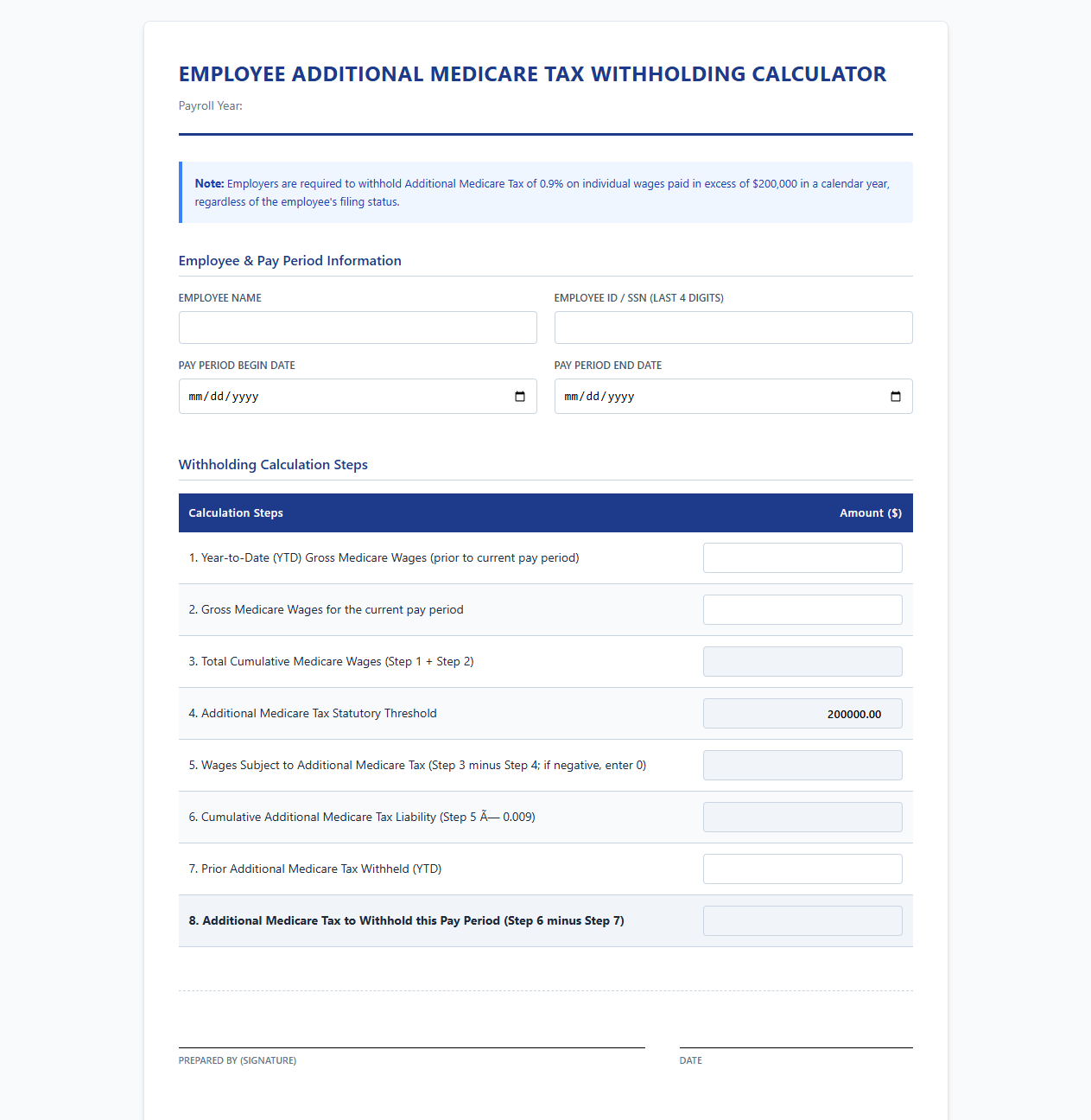

Employee Additional Medicare Tax Withholding Calculator

Download: .PDF

Download: .PDF

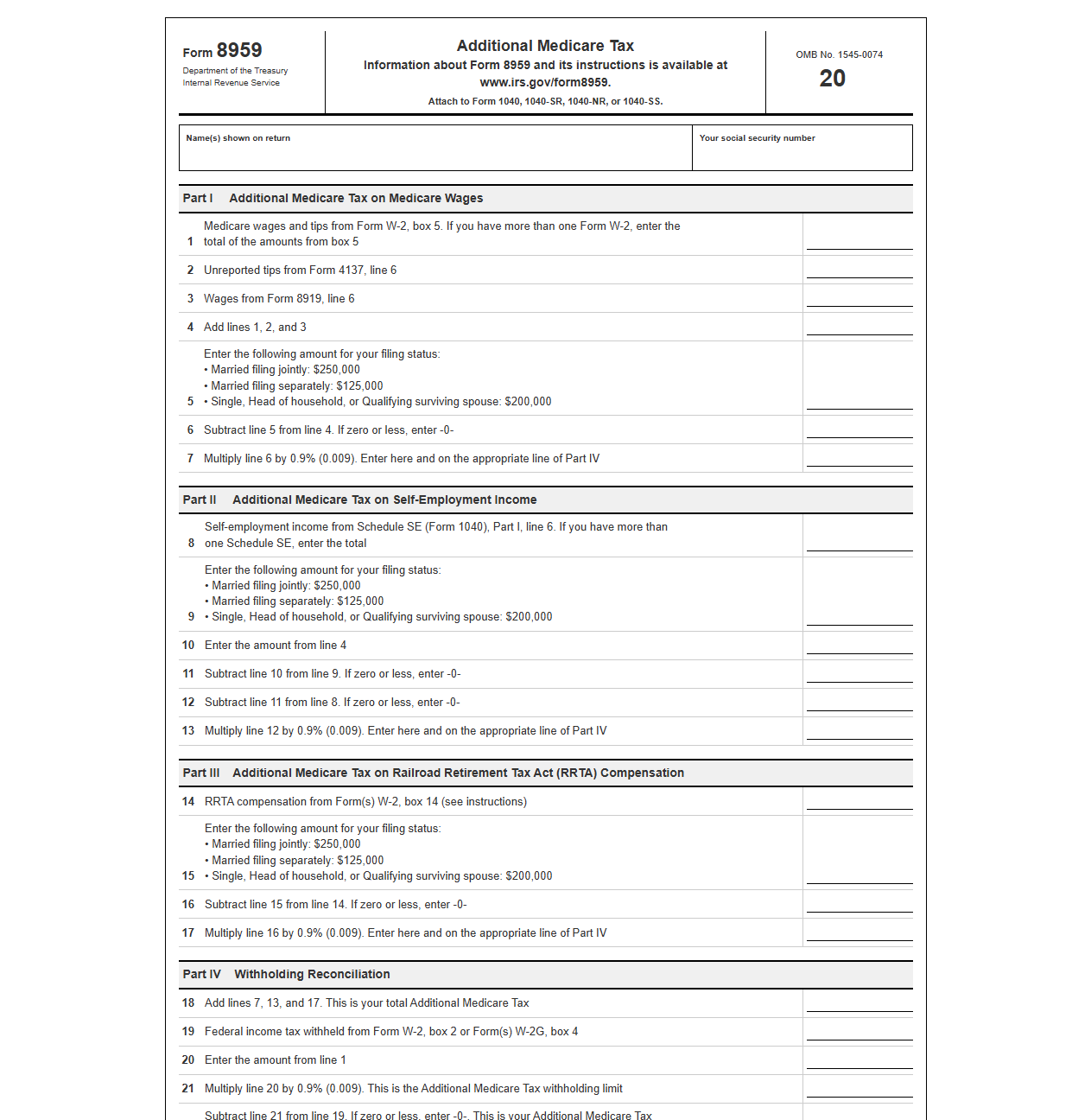

IRS Form 8959 Payroll Withholding Template

Download: .PDF

Download: .PDF

High Earner Medicare Tax Tracking Spreadsheet

![]() Download: .PDF

Download: .PDF

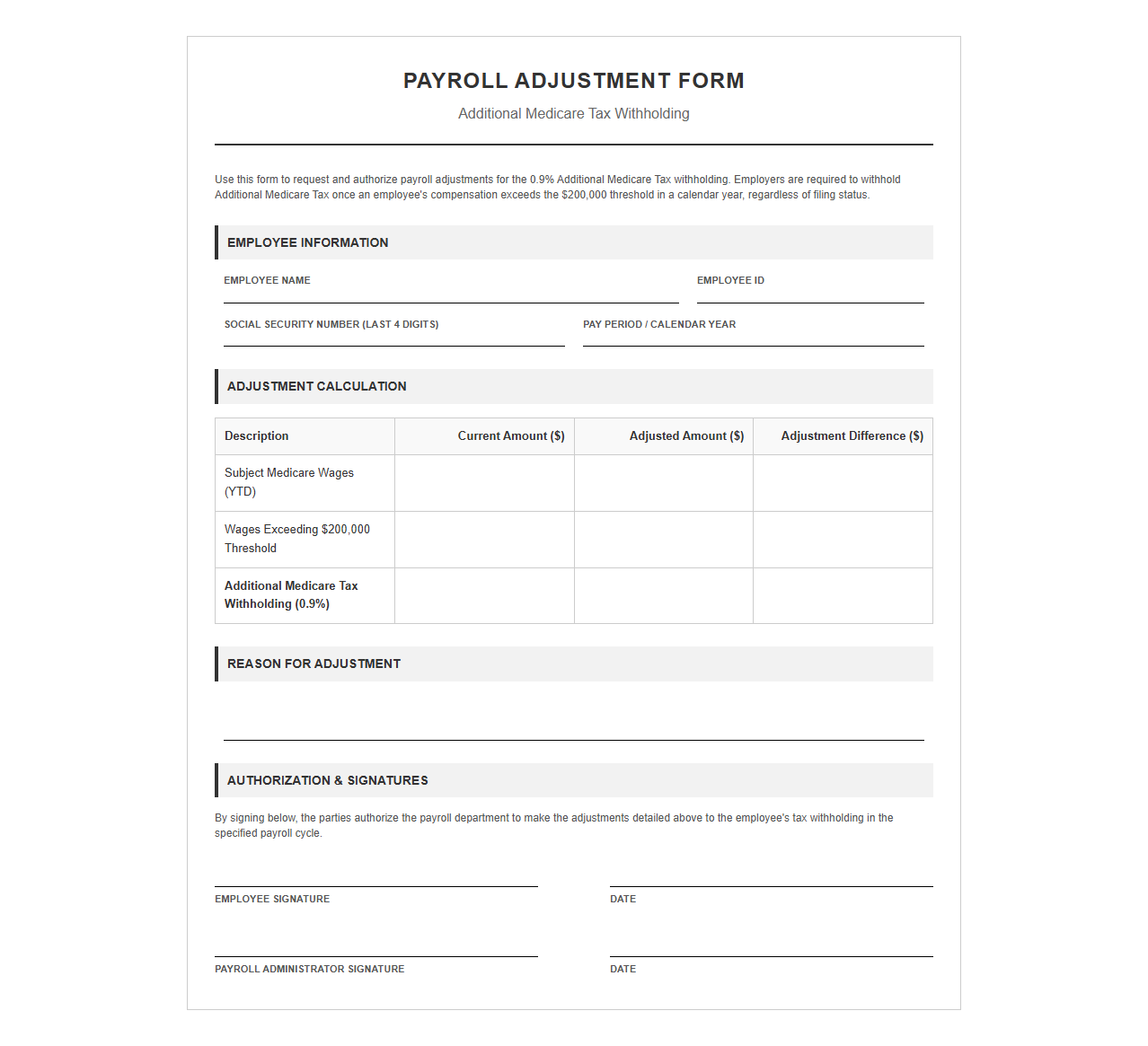

Payroll Adjustment Form for Additional Medicare Tax

Download: .PDF

Download: .PDF

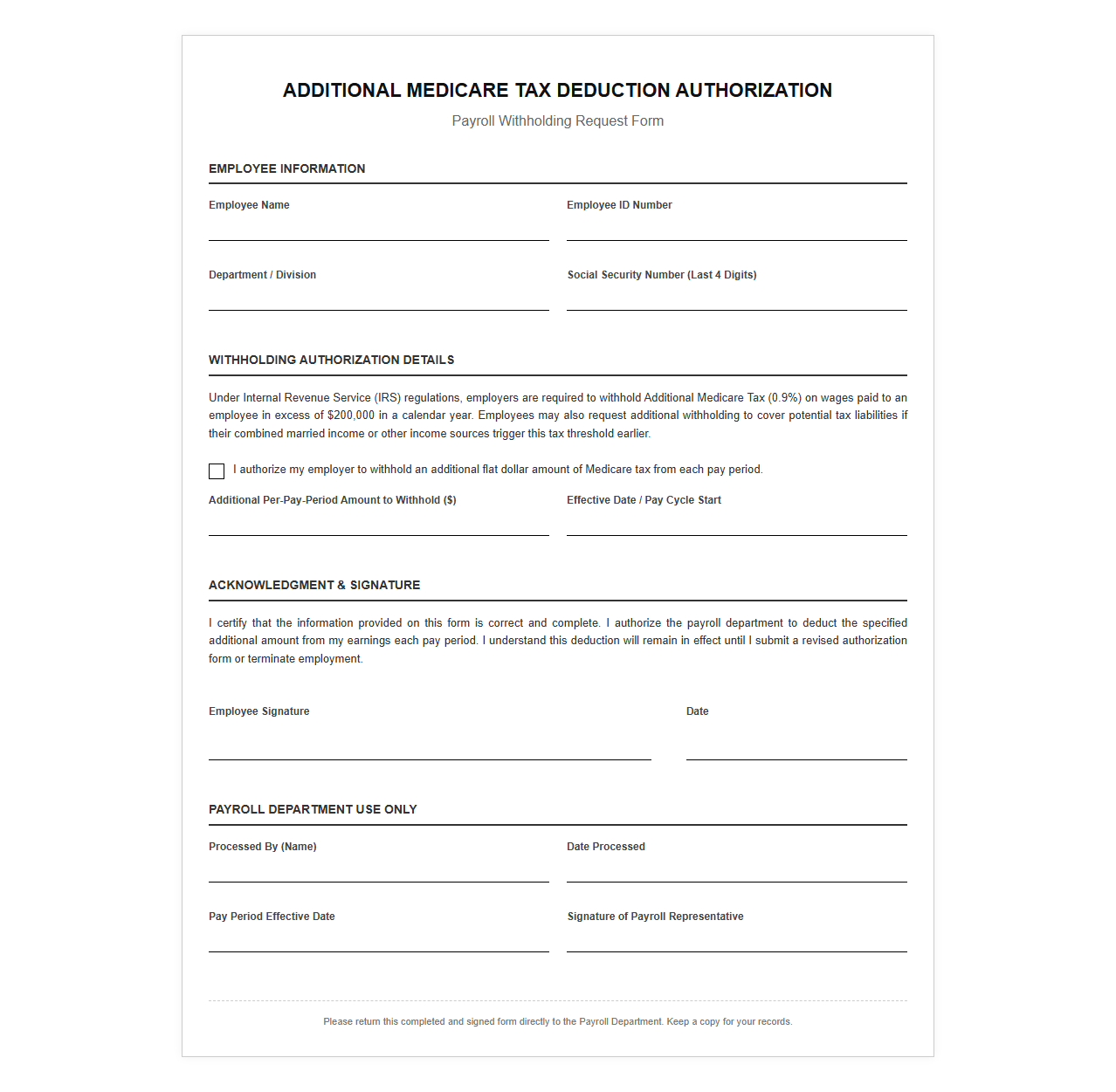

Additional Medicare Tax Deduction Authorization Template

Download: .PDF

Download: .PDF

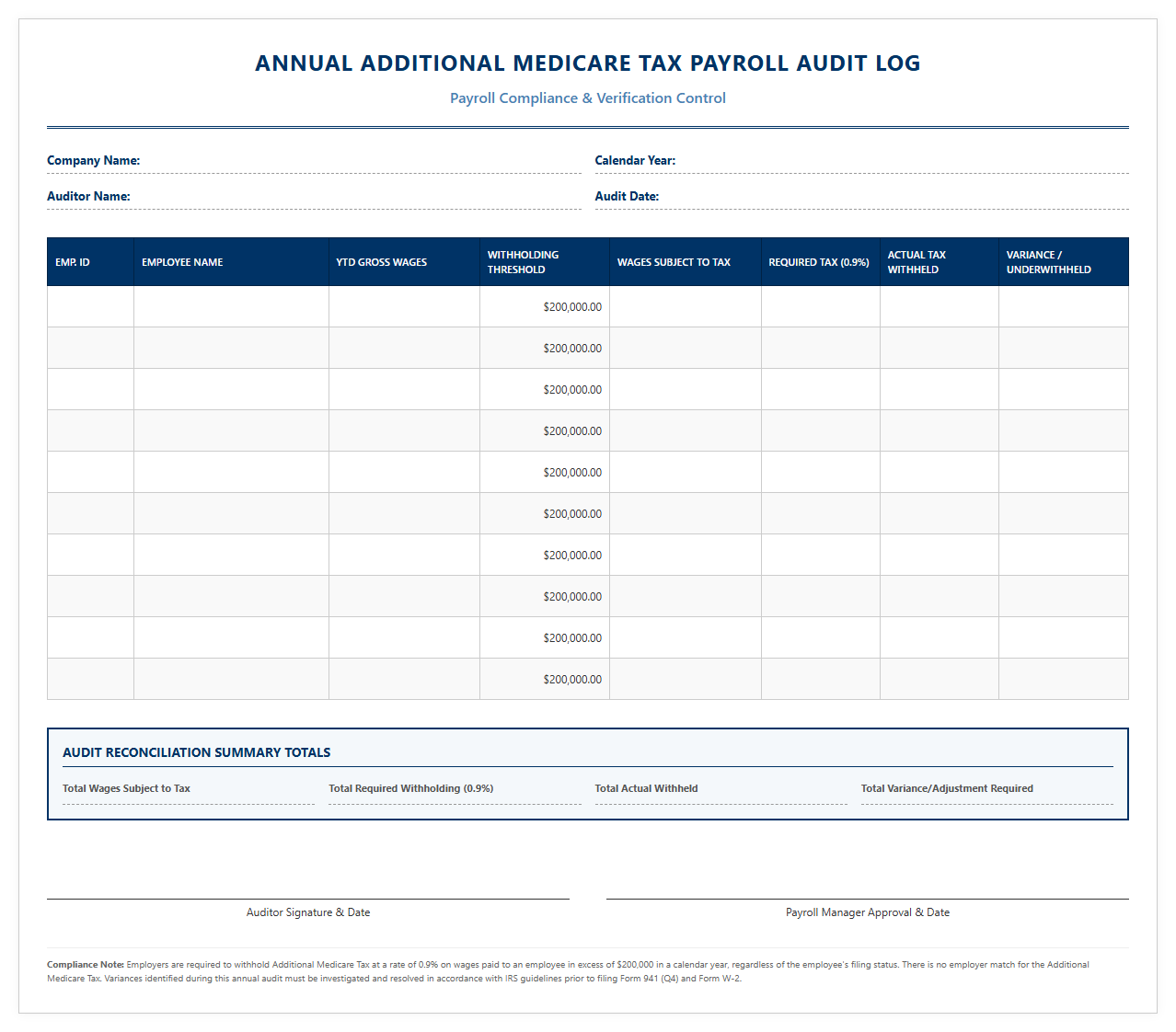

Annual Additional Medicare Tax Payroll Audit Log

Download: .PDF

Download: .PDF

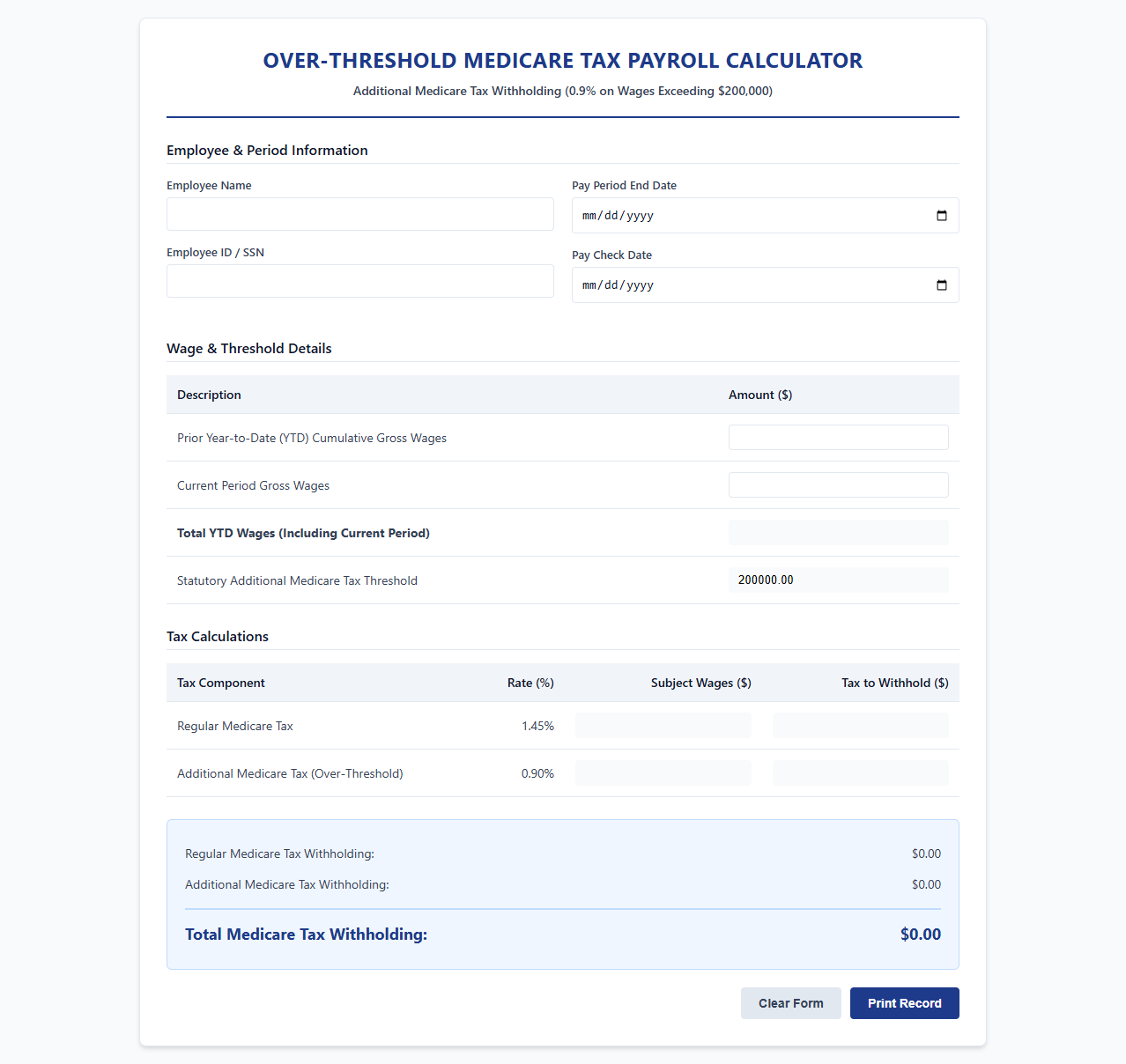

Over-Threshold Medicare Tax Payroll Calculator

Download: .PDF

Download: .PDF

Understanding Additional Medicare Tax and Common Withholding Errors

Managing payroll taxes requires absolute precision, particularly when dealing with the 0.9% Additional Medicare Tax. Under IRS regulations, employers are legally obligated to begin withholding this additional surtax once an individual's wages exceed $200,000 for single filers within a single calendar year, regardless of their marital filing status. Withholding errors frequently occur because of mid-year compensation fluctuations, dual-income households, or localized system overrides. Because employers must track year-to-date earnings per employee dynamically, manual tracking slips or delayed system synchronization can lead to costly compliance gaps.

Identifying Additional Medicare Tax Discrepancies in Your Payroll

To prevent penalties and interest, payroll administrators must actively audit their ledgers to detect under-withholding or over-withholding before the close of the calendar year. Running proactive payroll audits ensures that any discrepancy is identified while the business still has time to make adjustments within the active tax cycle.

- Verify year-to-date gross wages for all employees approaching or exceeding the $200,000 threshold.

- Cross-reference current withholding balances with the required 0.9% rate for earnings above the limit.

- Isolate instances where employees have multiple jobs or mid-year salary adjustments that affected their threshold calculation.

- Reconcile total payroll registers against quarterly federal tax returns to flag systemic calculation variances.

Essential Payroll Templates for Documenting Tax Adjustments

Standardizing the correction process requires structured documentation. Utilizing consistent templates ensures that both internal records and external communications meet compliance standards during a payroll correction.

| Template Name | Primary Purpose | Key Elements Included |

|---|---|---|

| Employee Notification Letter | Informs the employee of the withholding discrepancy and subsequent correction. | Explanation of the 0.9% threshold, amount corrected, and impact on future paychecks. |

| Internal Payroll Adjustment Form | Authorizes and logs manual adjustments in the payroll system. | Employee ID, adjustment period, corrected withholding amounts, and administrative signatures. |

| Prior-Year Correction Log | Tracks historical errors that require retro-active adjustments. | Original filing date, corrected variance amounts, and associated tax amendment dates. |

Step-by-Step Resolution Process for Employer Corrections

Correcting withholding errors requires a structured, chronological approach to comply with IRS guidelines, depending on when the discrepancy is identified.

- Identify the error and verify whether the discovery occurs within the same calendar year or a prior tax year.

- For same-year errors, adjust the withholding on subsequent payroll runs before December 31st to balance the employee's tax obligation.

- Inform the affected employee immediately using the standard notification letter to explain the adjustment.

- For prior-year errors, proceed to prepare retroactive reporting documents without adjusting current-year withholding.

- Document the correction thoroughly in the internal payroll registry for future compliance audits.

Adjusting IRS Form 941 and Correcting Form W-2

When discrepancies bypass the internal calendar year adjustments, employers must utilize specific federal forms to report corrections. If you discover a withholding error after filing your quarterly returns, you must file Form 941-X (Adjusted Employer's Quarterly Federal Tax Return or Claim for Refund) to report the correct Additional Medicare Tax. If the error is discovered after the year-end tax files have been distributed, the employer must also issue Form W-2c (Corrected Wage and Tax Statement) to the employee and the Social Security Administration. Correctly filing these forms prevents compounding interest penalties and updates the taxpayer's federal record accurately.

Implementing Preventive Controls in Payroll Systems

The most effective strategy to manage Additional Medicare Tax issues is preventing them through robust software settings and systematic workflows. Payroll managers should configure automated alerts within their Human Capital Management (HCM) platforms to flag employee accounts as they approach critical wage milestones.

Ensuring Long-Term Payroll Compliance and Accuracy

Maintaining a compliant payroll system is an ongoing responsibility that goes beyond simple calculations. Employers must prioritize routine payroll audits, update standard document templates regularly, and ensure that administrative staff receive continuous training on changing IRS rules. Proactive compliance protects the business from costly audits, penalties, and reputational damage. By treating payroll management as a dynamic operational process, organizations can confidently navigate complex tax codes while safeguarding their workforce's financial accuracy.

Leave a comment