Navigating payroll procedures following the death of an employee is one of the most sensitive and operationally complex challenges an HR or finance department can face. Before resolving outstanding balances, organizations must carefully reconcile federal tax obligations with highly variable state probate laws. Standardizing this delicate transition with structured document templates grants your business administrative efficiency, safeguarding your organization against costly audit penalties and wage disputes.

Please note a vital regulatory stipulation: payroll administrators must always cross-reference templates with local state statutes, as requirements for beneficiary hierarchies vary significantly. For example, correctly determining whether to report unpaid wages on a Form W-2 or a Form 1099-MISC is critical to maintaining IRS compliance.

This guide provides the essential templates, step-by-step settlement workflows, and tax compliance checklists necessary to manage deceased employee payroll with absolute accuracy and professionalism.

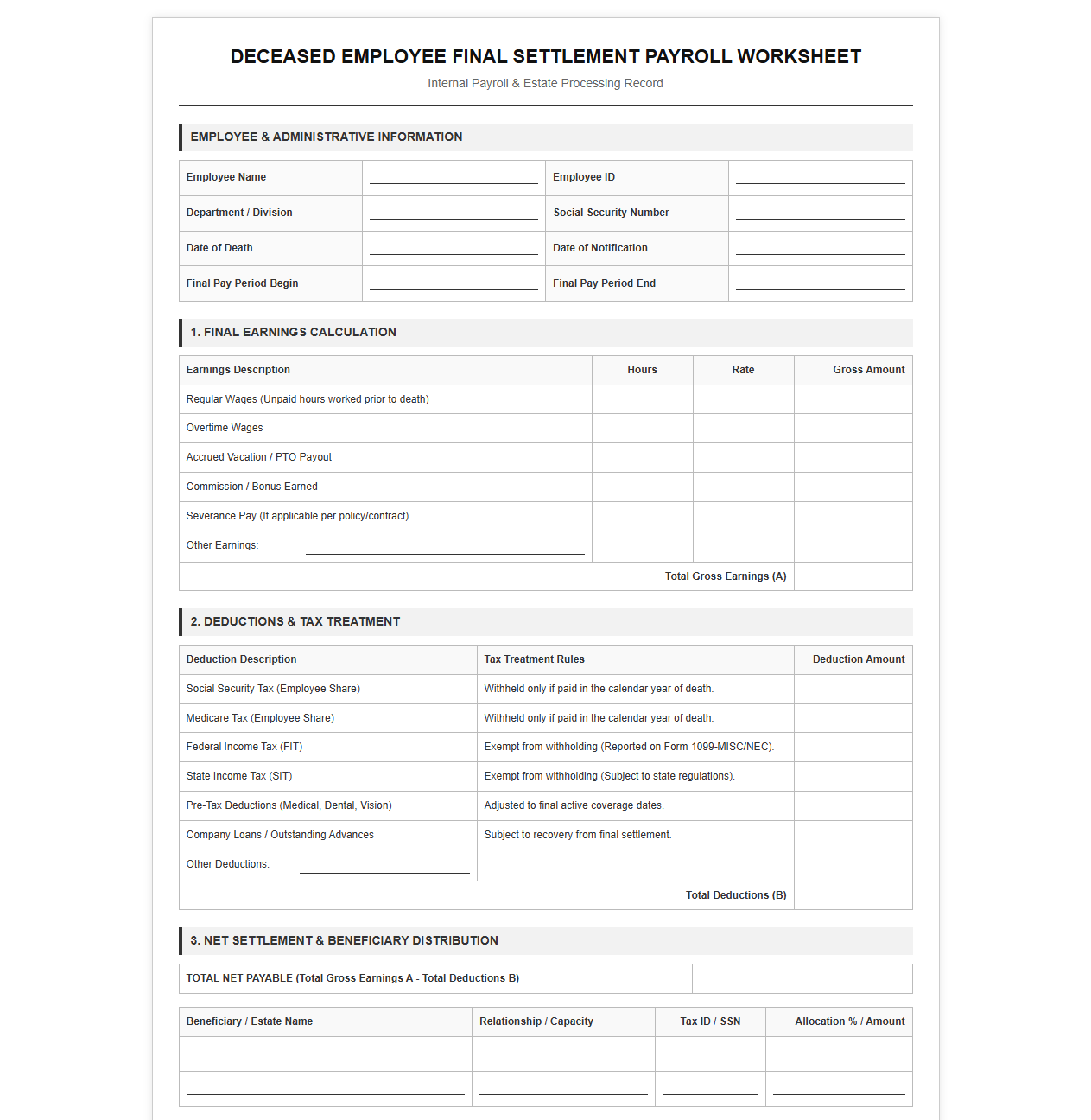

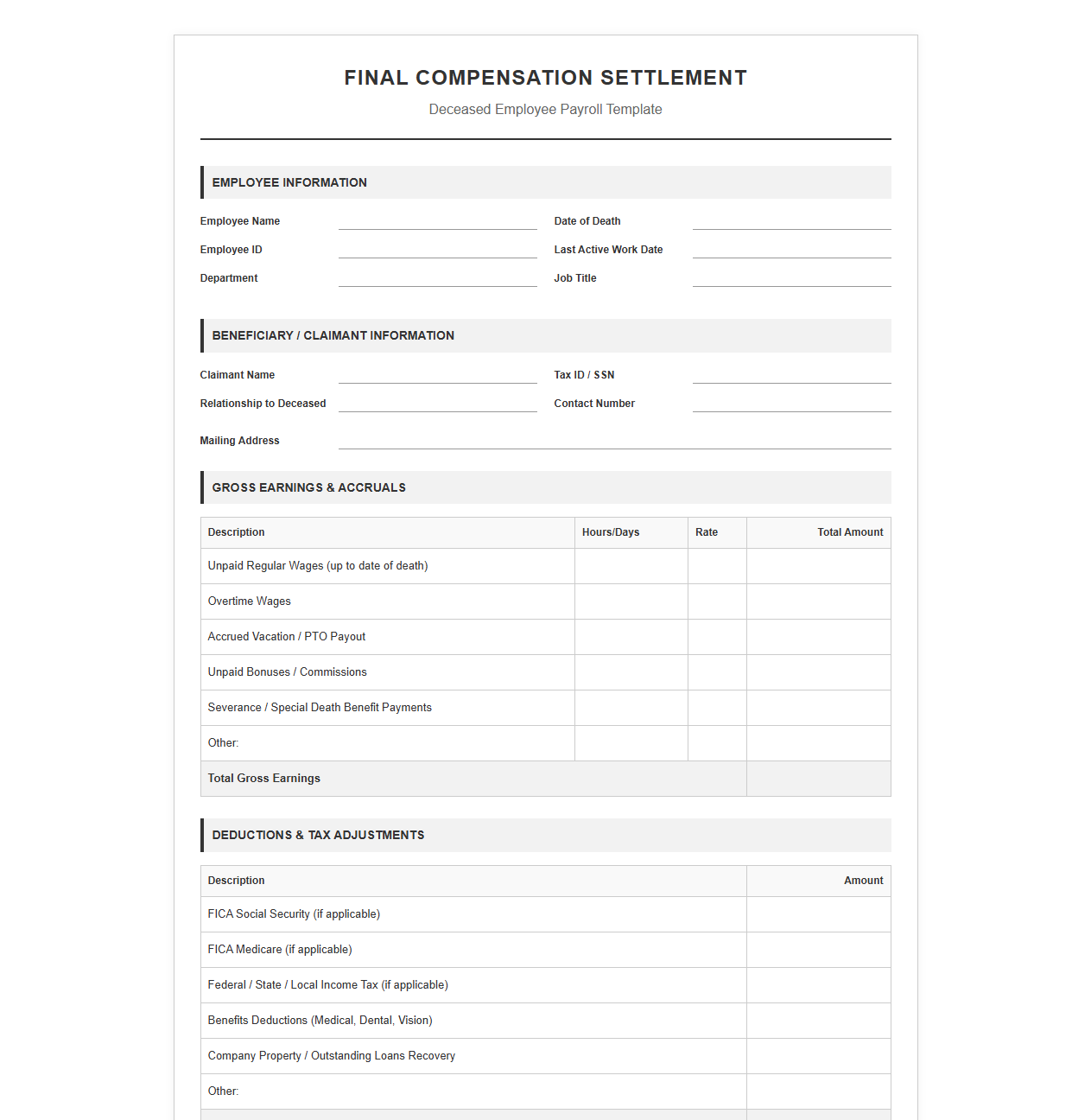

Deceased Employee Final Settlement Payroll Worksheet

Download: .PDF

Download: .PDF

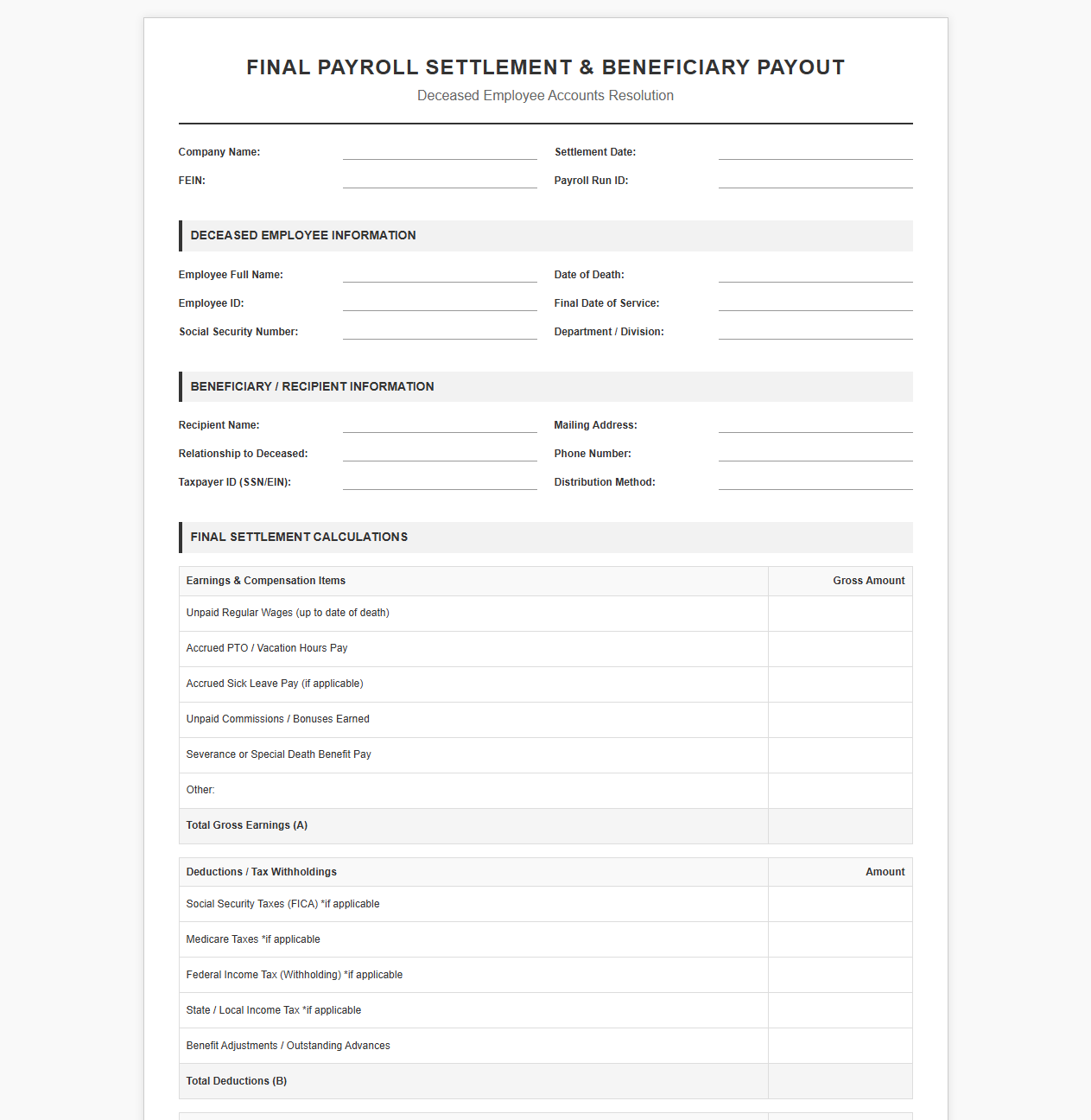

Payroll Template for Final Beneficiary Payouts

Download: .PDF

Download: .PDF

Post-Mortem Employee Payroll Settlement Calculator

Download: .PDF

Download: .PDF

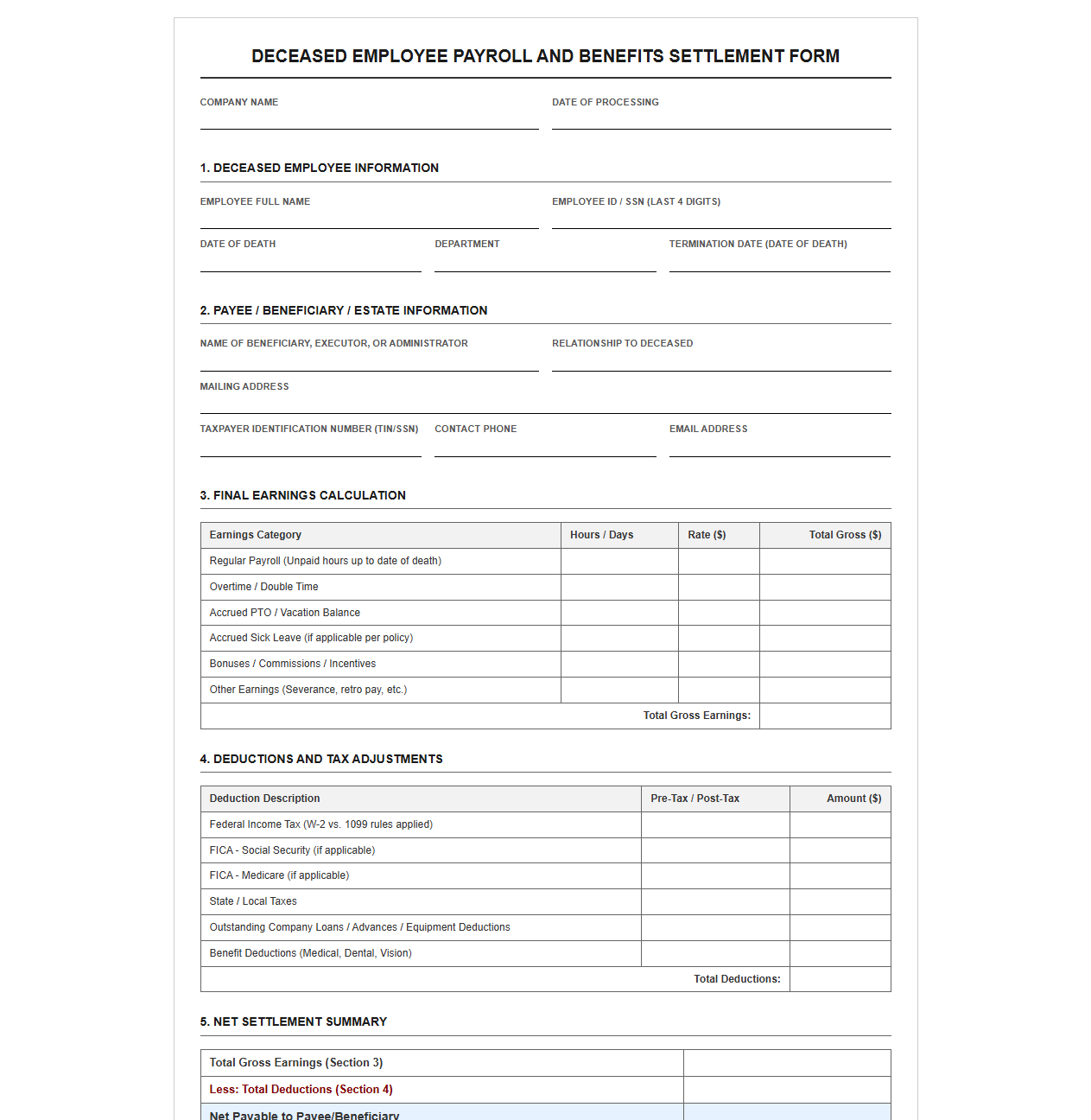

Deceased Employee Payroll and Benefits Settlement Form

Download: .PDF

Download: .PDF

Final Compensation Template for Deceased Staff

Download: .PDF

Download: .PDF

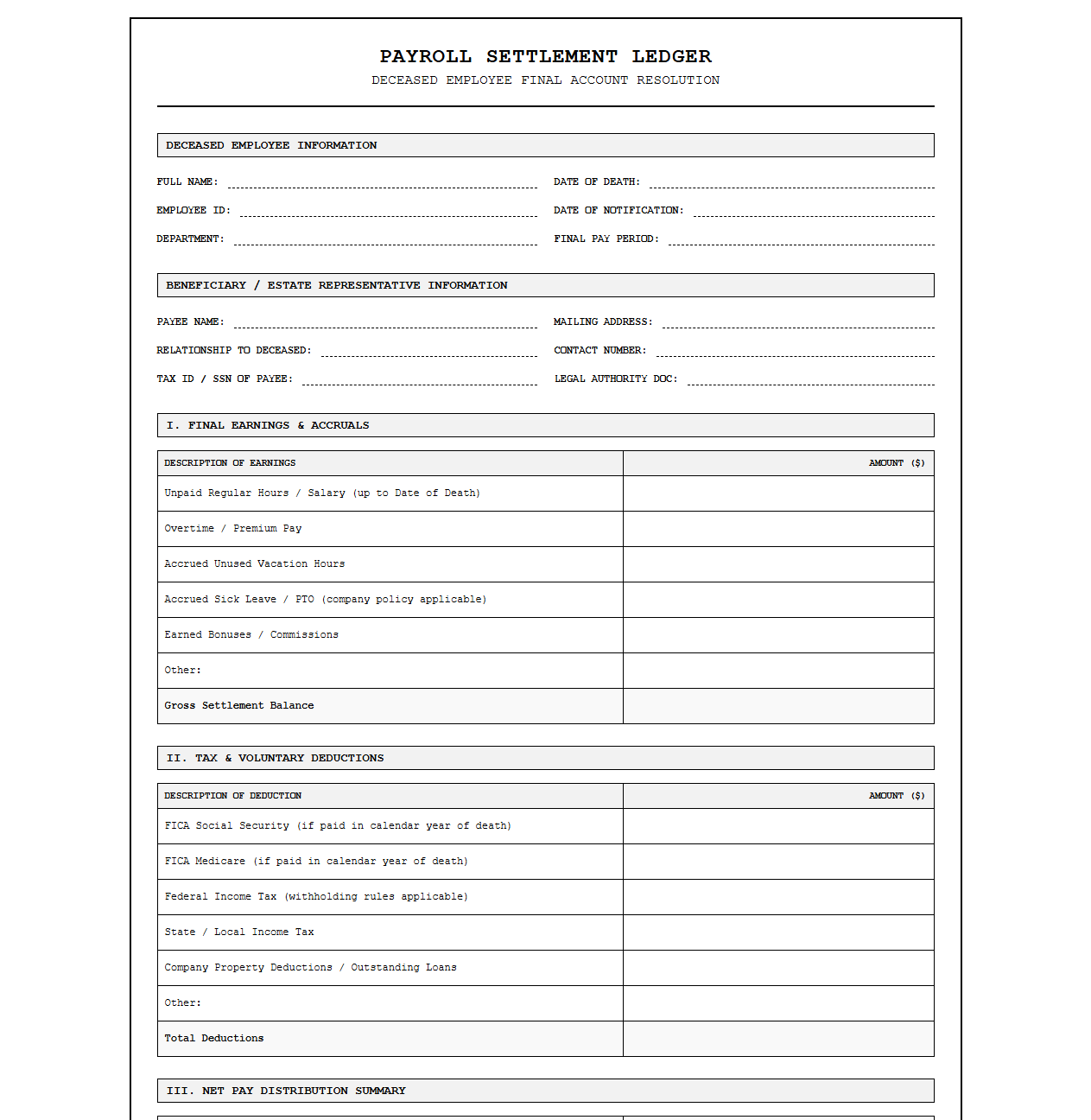

Payroll Settlement Ledger for Deceased Employees

Download: .PDF

Download: .PDF

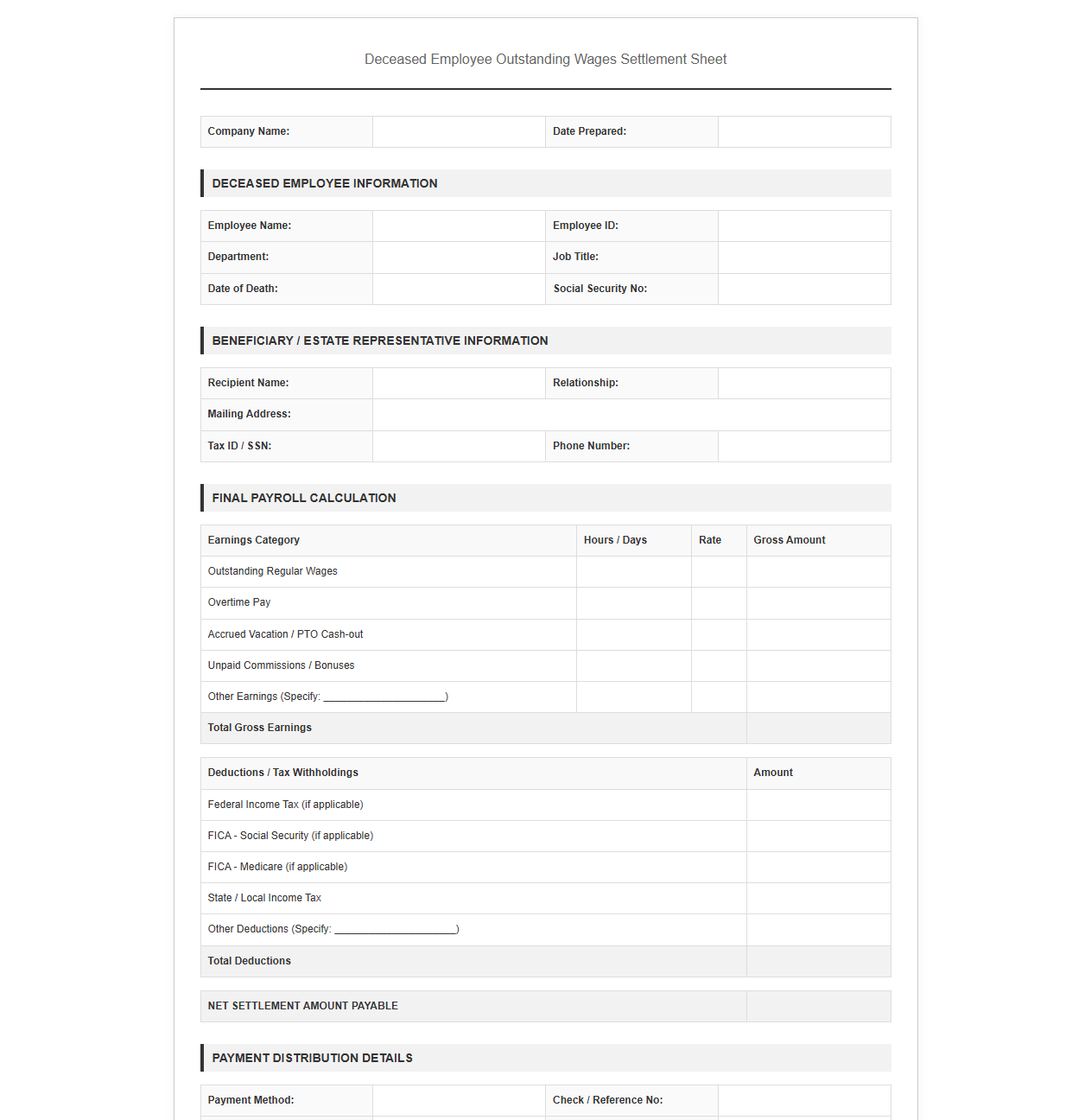

Deceased Employee Outstanding Wages Settlement Sheet

Download: .PDF

Download: .PDF

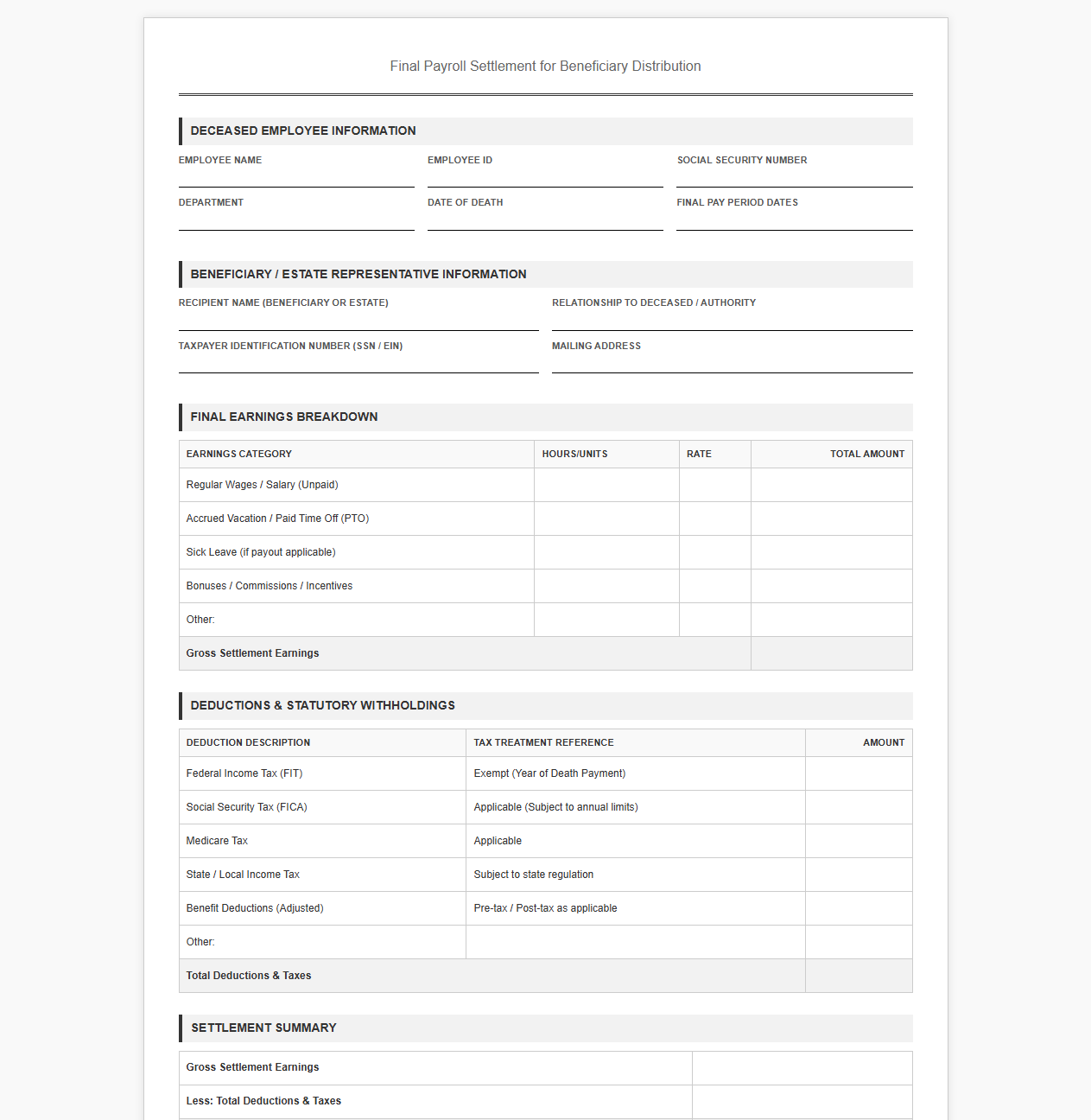

Final Payroll Settlement for Beneficiary Distribution

Download: .PDF

Download: .PDF

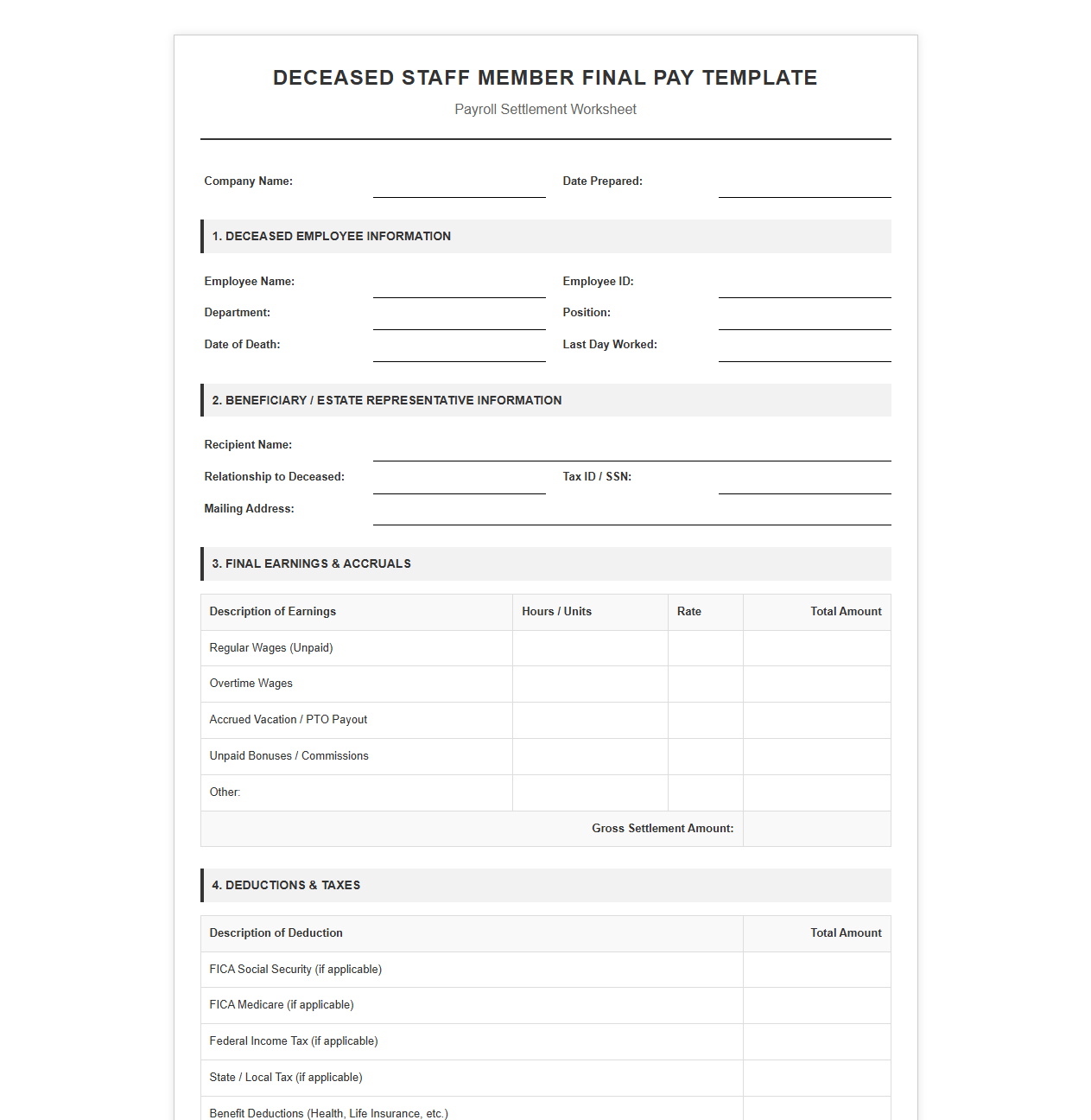

Deceased Staff Member Final Pay Template

Download: .PDF

Download: .PDF

Section 1: Introduction to Deceased Employee Payroll Compliance

Managing the departure of an employee is always a sensitive process, but the passing of a team member introduces a unique set of legal and ethical complexities. HR departments must navigate this difficult period with a balance of profound empathy for the grieving family and strict adherence to federal and state labor laws. Handling the final payroll settlement is not merely an administrative task; it is a critical regulatory requirement that carries significant compliance risks if executed incorrectly.

Failing to process post-mortem payments in accordance with statutory guidelines can lead to severe tax penalties, wage-and-hour violations, and legal disputes with the employee's estate. HR professionals bear the ethical responsibility of ensuring that the deceased worker's hard-earned compensation is accurately calculated and delivered to the rightful beneficiaries. By establishing a structured, compliant, and compassionate protocol, organizations can honor their commitment to their employees while safeguarding the company from regulatory exposure.

Section 2: Establishing the Timeline and Essential Verification Documents

Upon receiving notification of an employee's passing, the HR and payroll departments must immediately pause all active direct deposits and automated payments to prevent unauthorized transactions. Establishing a clear operational timeline is critical to remaining compliant with state laws, which often dictate strict deadlines for releasing final wages. Before any funds can be disbursed, the employer must obtain and verify specific legal documents to ensure payments are legally routed.

The following verification documents must be collected and authenticated before finalizing the payroll settlement:

- An official copy of the employee's death certificate, which confirms the date of passing and provides the legal basis for altering payroll records.

- Letters of Administration or Letters Testamentary, identifying the court-appointed personal representative or executor of the employee's estate.

- The designated beneficiary documentation, if the employer offers specific company-sponsored death benefits or survivor options.

- An IRS Form W-9 completed by the personal representative or beneficiary, which secures the tax identification number required for end-of-year tax reporting.

Section 3: Calculating Final Unpaid Wages and Accrued Benefits

Calculating the final compensation of a deceased employee requires a meticulous audit of all earned but unpaid earnings up to the exact date of death. This calculation must encompass hourly wages for time worked, prorated salaries, earned commissions, and performance bonuses. Accurate tracking of these figures ensures the estate receives the correct amount while preventing overpayment or underpayment errors.

Beyond standard wages, employers must review the company's paid time off (PTO) policy and state regulations regarding accrued benefits. In many jurisdictions, unused vacation days, sick leave, and personal time must be paid out upon separation, regardless of the cause. Additionally, any outstanding expense reimbursements must be compiled, verified against receipts, and integrated into the final calculation to compile a comprehensive, legally compliant payout total.

Section 4: Tax Treatment of Post-Mortem Payments

The tax treatment of payments made after an employee's death depends heavily on the timing of the disbursement relative to the calendar year of passing. Payroll departments must differentiate between payments made in the same calendar year the employee died and payments made in a subsequent calendar year to ensure correct tax withholding.

Section 5: Beneficiary Designation and Release Agreement Template

To protect the organization from conflicting claims over the deceased employee's final wages, HR must utilize a formal, legally binding release agreement. This document confirms the identity of the recipient and legally releases the employer from any further financial liability regarding the outstanding compensation.

The following standardized language serves as a foundational guide for drafting a release form to distribute final payments to the designated beneficiary or estate executor:

I, [Recipient Name], acting in my capacity as the legally authorized [Executor/Administrator/Beneficiary] of the Estate of [Deceased Employee Name], hereby acknowledge receipt of the final payroll settlement totaling $[Amount]. By signing this document, I release [Company Name] from any and all further liabilities, claims, or demands regarding unpaid wages, accrued PTO, or other post-mortem benefits.

Section 6: Annual IRS Reporting and Form Issuance (W-2 and 1099-MISC)

Reporting final payments to the IRS requires utilizing both Form W-2 and Form 1099-MISC. The exact reporting structure depends on when the payment was made relative to the year of death. This process ensures the IRS can track the shift in tax liability from the deceased employee to the receiving entity.

| Payment Timing | Form W-2 Reporting (Deceased Employee) | Form 1099-MISC Reporting (Beneficiary/Estate) |

|---|---|---|

| Paid in Year of Death | Report Social Security and Medicare wages and tax withheld in Boxes 3, 4, 5, and 6. Leave Box 1 blank. | Report the gross payment amount in Box 3 (Other Income) under the name and TIN of the beneficiary or estate. |

| Paid in Subsequent Year | Do not issue a Form W-2 for this payment. No FICA or income tax is reported. | Report the gross payment amount in Box 3 (Other Income) under the name and TIN of the beneficiary or estate. |

Section 7: Final Compliance Checklist and Document Retention Policy

To guarantee that no administrative steps are overlooked during this sensitive process, HR departments should follow a standardized operational checklist. This systematic approach ensures that payroll records are closed cleanly and archived in compliance with federal document retention laws.

Complete the following steps to ensure absolute compliance and proper record preservation:

- Deactivate Payroll Status: Immediately suspend regular direct deposit protocols to prevent automatic, unauthorized pay cycles.

- Obtain Legal Proof: Secure and verify a certified copy of the death certificate alongside estate executor documentation.

- Audit Balances: Calculate all outstanding hourly wages, commissions, accrued PTO, and pending expense reimbursements.

- Apply Correct Taxation: Determine the tax year of the payout and apply FICA and federal income tax withholdings accordingly.

- Execute Release Agreement: Obtain a signed release and beneficiary designation form prior to distributing any physical checks.

- File Year-End Forms: Correctly distribute the wages across Form W-2 for the employee and Form 1099-MISC for the recipient.

- Archive Records: Store all communications, death certificates, tax forms, and signed agreements for a minimum of four years under IRS payroll retention guidelines.

Leave a comment