Navigating high-stakes transactions often exposes parties to significant financial risk and administrative confusion, particularly when verifying escrow deposits. Without clear, written confirmation, disputes over fund disbursement can quickly derail promising deals.

To mitigate these risks, establishing a standardized verification framework is an essential first step. Implementing a standard escrow deposit receipt grants both transacting parties absolute legal clarity, securing the transaction from the outset. However, these templates are only as effective as their specific stipulations, which must clearly define the release conditions and custodian responsibilities. For example, whether managing earnest money for real estate transactions or holding initial deposits for corporate mergers and acquisitions, structured receipts serve as indisputable proof of commitment.

Below, we will explore the essential elements of compliant escrow receipt templates and outline the best practices for securing your next financial transaction.

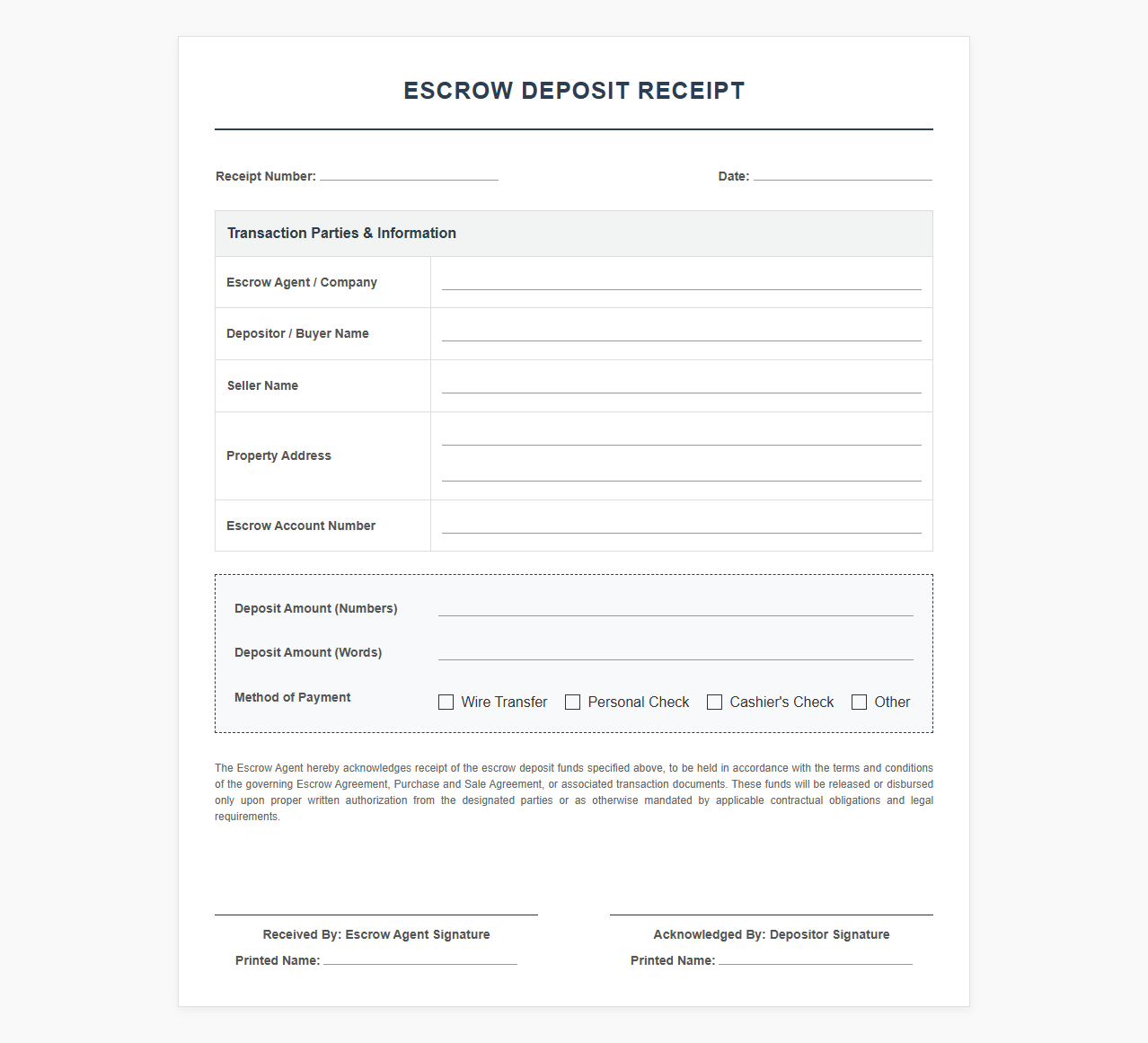

Escrow Deposit Receipt Template

Download: .PDF

Download: .PDF

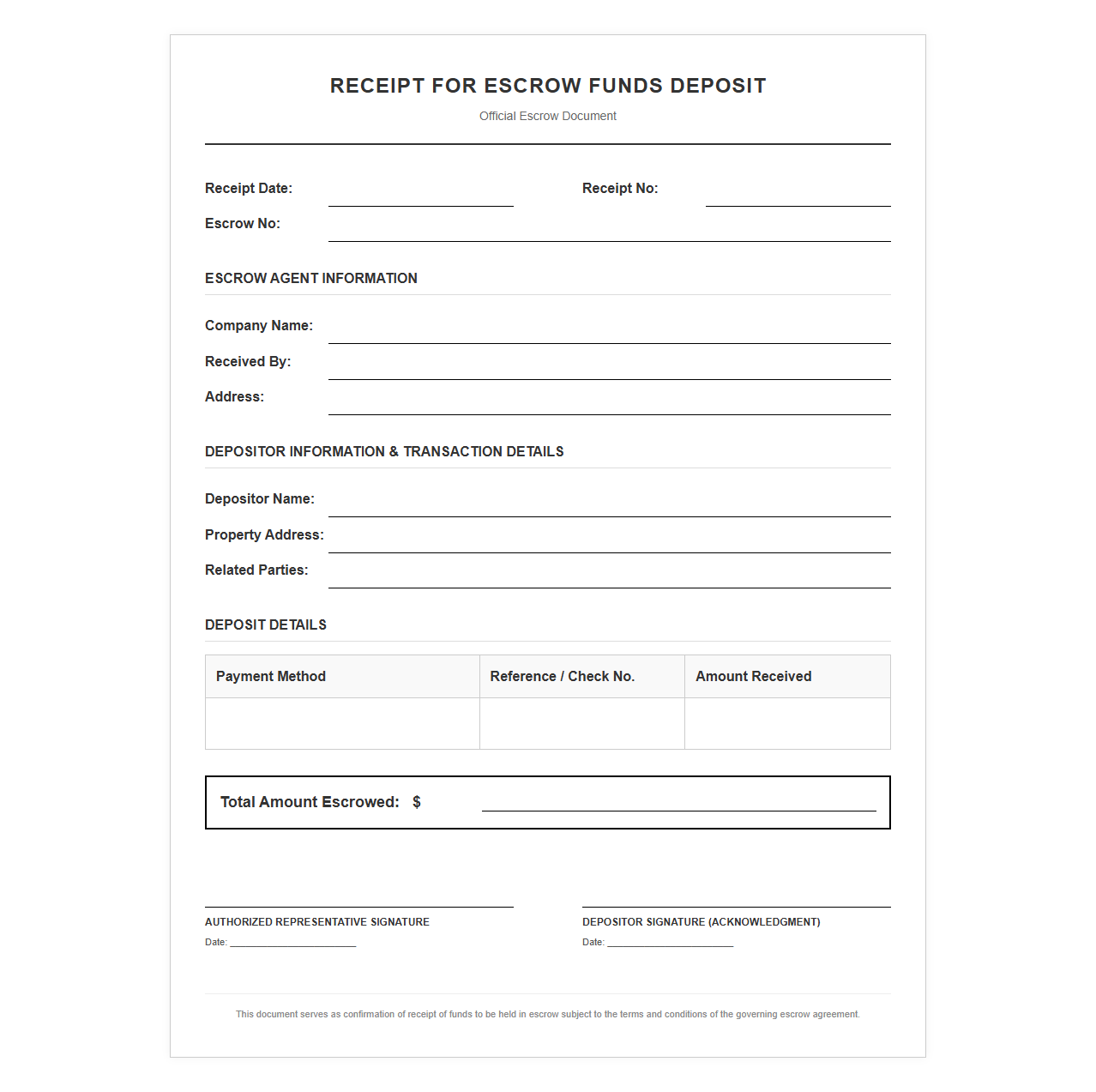

Receipt for Escrow Funds Deposit

Download: .PDF

Download: .PDF

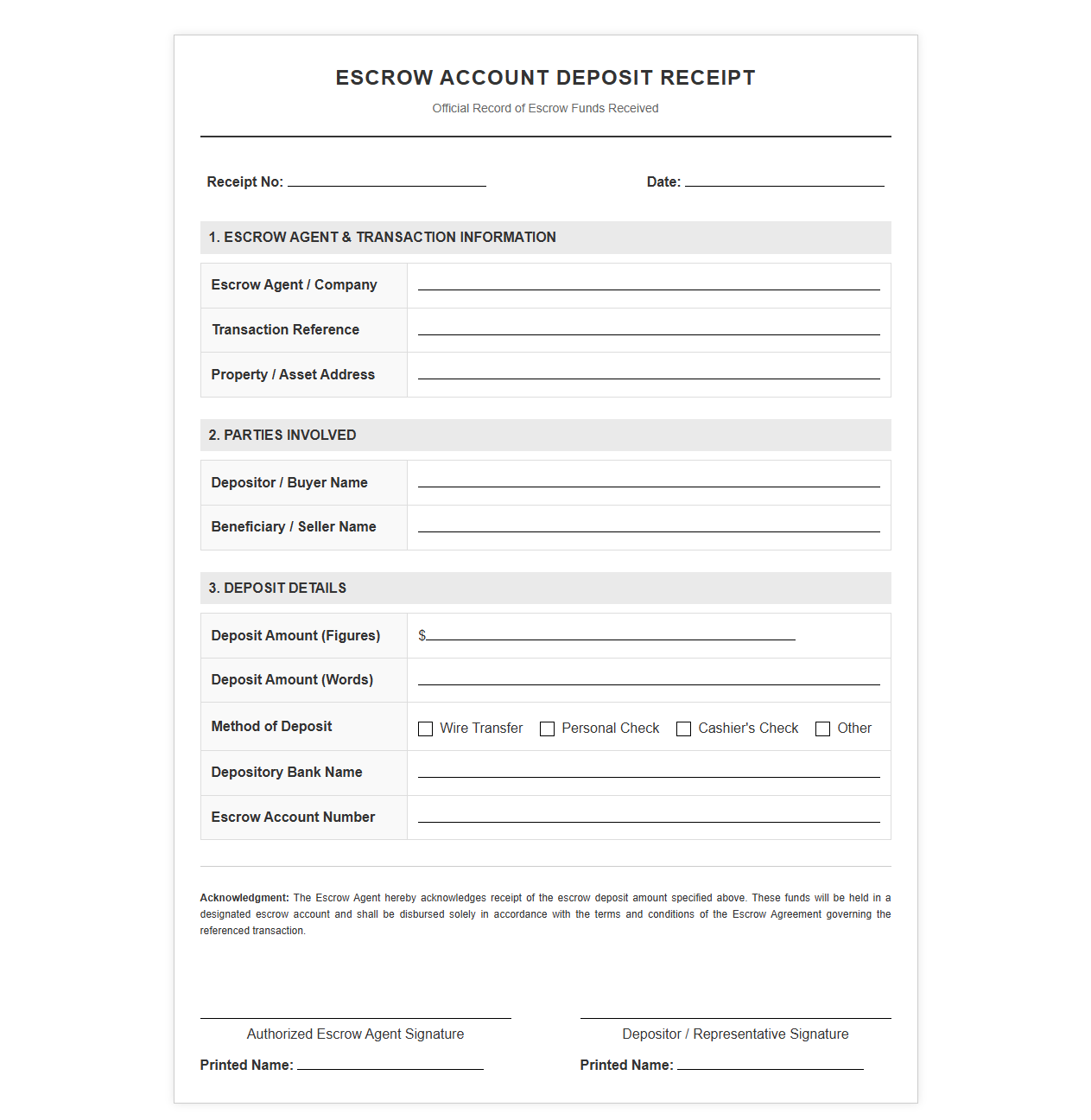

Escrow Account Deposit Receipt Form

Download: .PDF

Download: .PDF

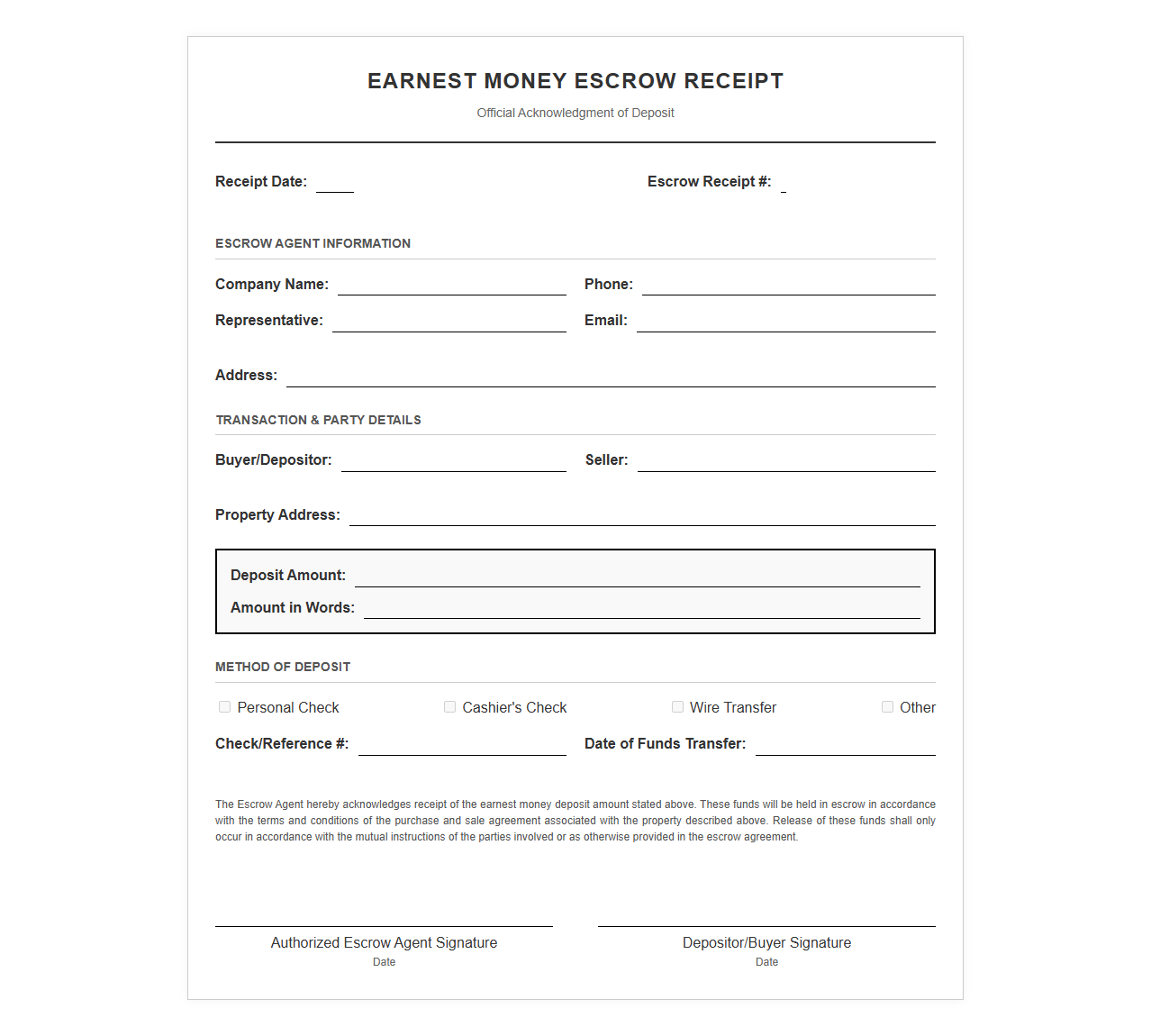

Earnest Money Escrow Receipt Template

Download: .PDF

Download: .PDF

Real Estate Escrow Deposit Receipt

Download: .PDF

Download: .PDF

Escrow Payment Confirmation Receipt Document

Download: .PDF

Download: .PDF

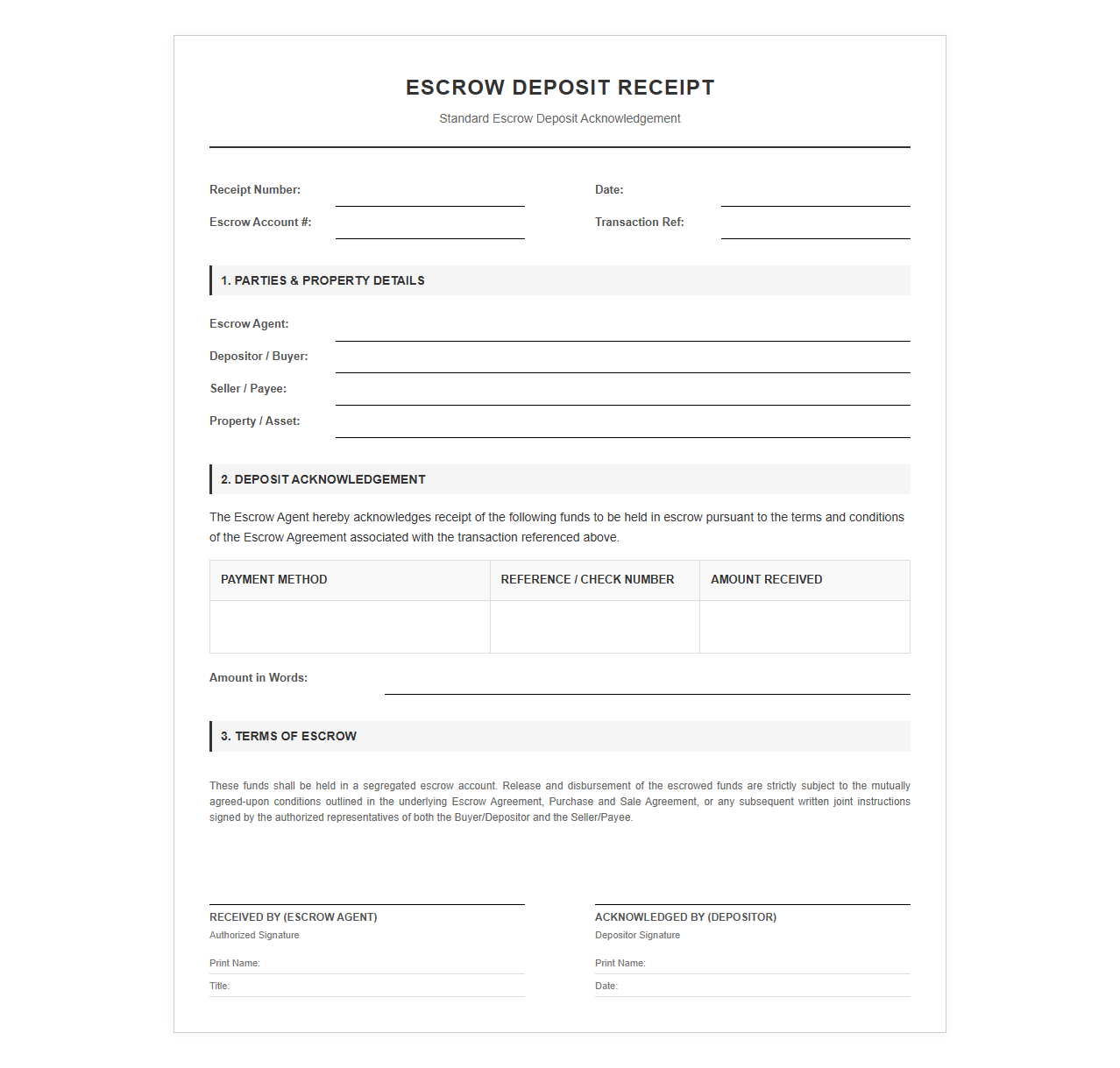

Standard Escrow Deposit Acknowledgement Receipt

Download: .PDF

Download: .PDF

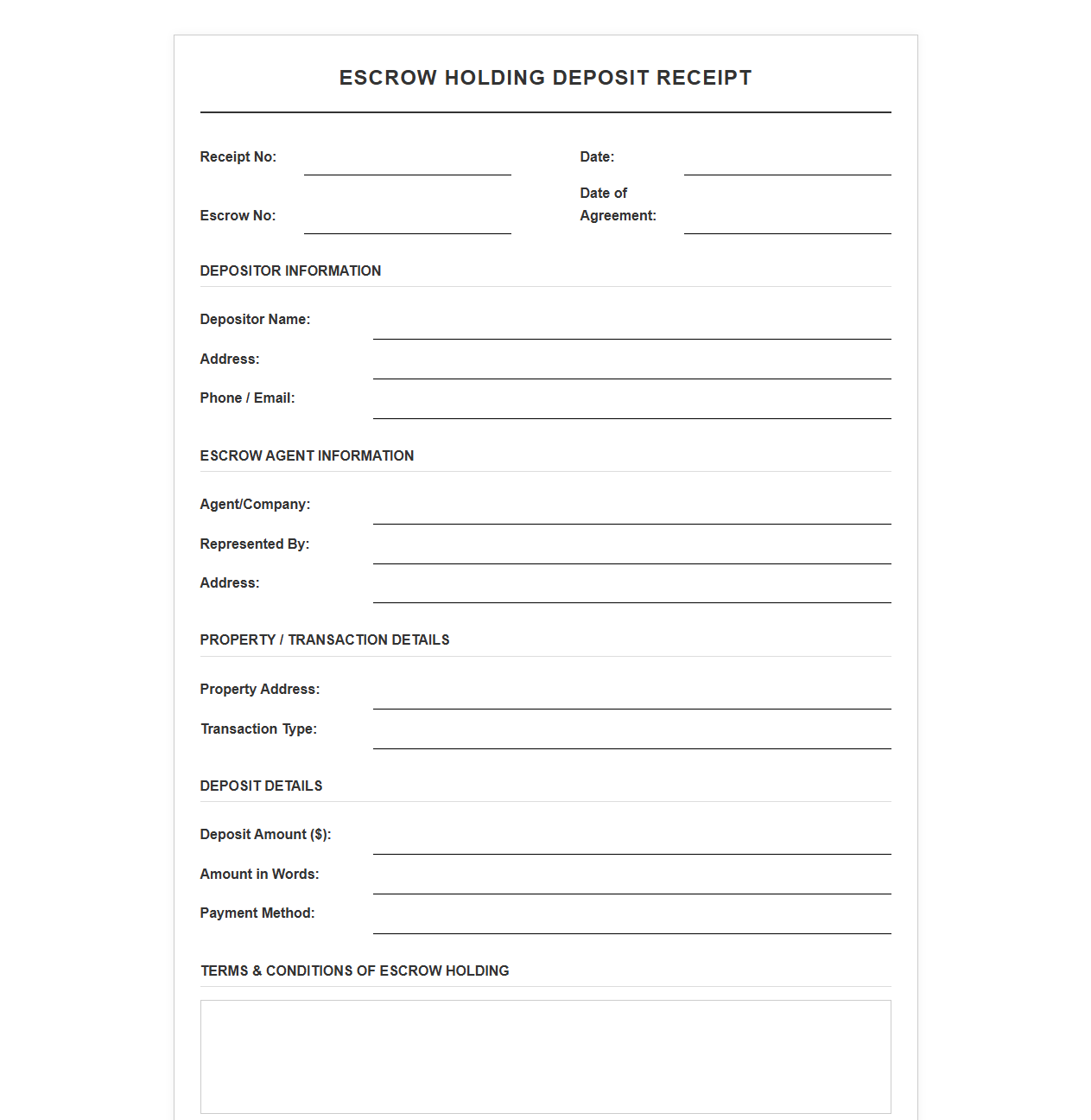

Escrow Holding Deposit Receipt Template

Download: .PDF

Download: .PDF

Introduction to Escrow Deposit Receipts

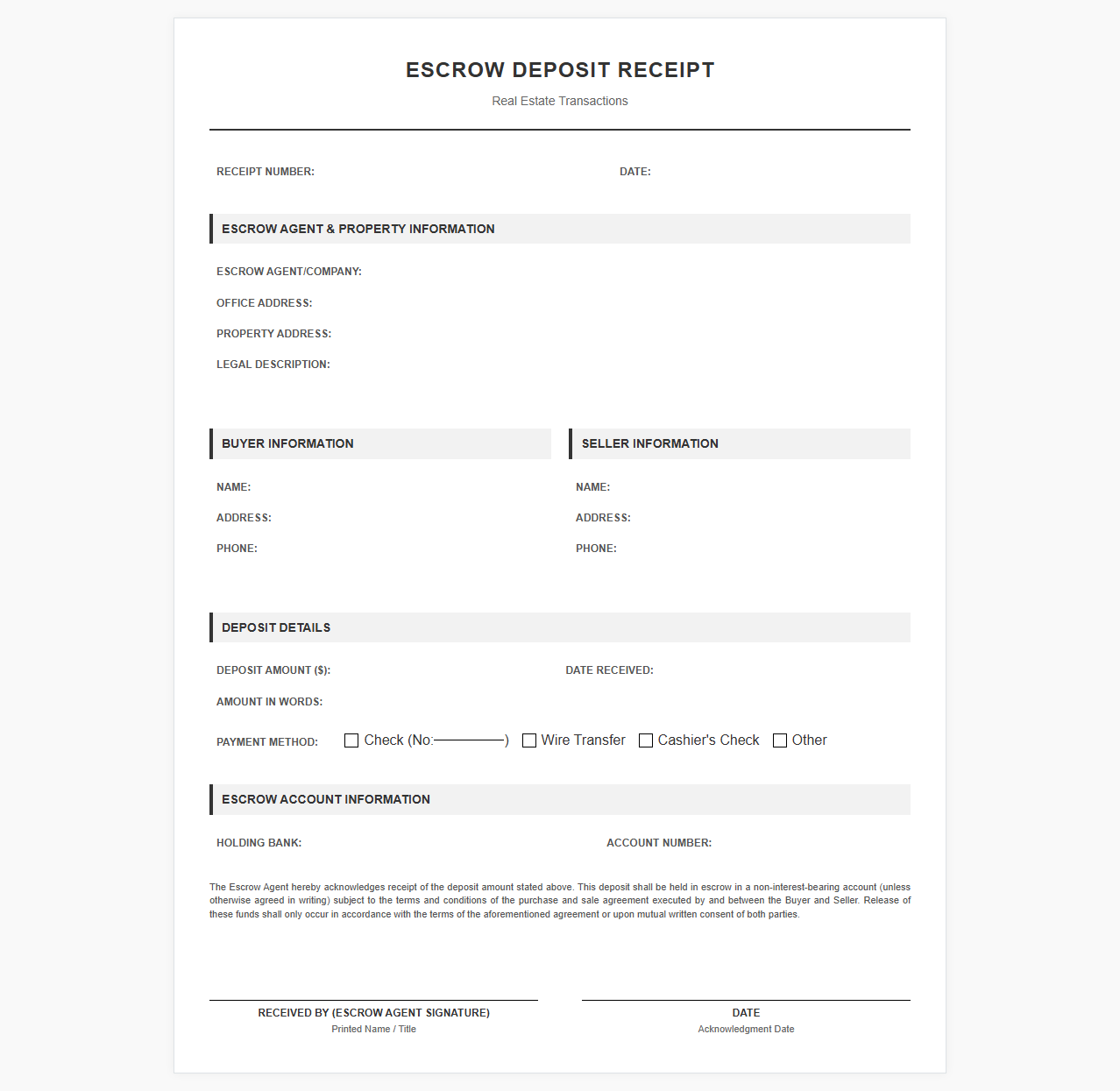

An escrow deposit receipt serves as a fundamental financial instrument designed to mitigate risk in high-value transactions. This document officially acknowledges that a neutral third party has received and is holding funds on behalf of the transacting parties, ensuring that the depositor and the beneficiary can proceed with mutual confidence.

Essential Components of a Standard Template

To ensure validity and clarity, every standard escrow receipt template must contain specific operational details:

- Identities of the Parties: Legal names and contact details of the depositor, beneficiary, and escrow agent.

- Deposit Amount: The exact monetary sum or asset description held in trust.

- Transaction Dates: The precise dates of fund receipt, holding periods, and projected release.

- Escrow Account Details: The designated bank account where the funds are securely held.

Legal Clauses and Compliance Safeguards

Dispute Resolution and Arbitration

Contracts must explicitly state the mechanism for resolving conflicts. An arbitration clause mandates that any disagreements regarding fund disbursement be settled outside of public courts through binding arbitration.

Regulatory Compliance and AML Standards

Escrow agents must adhere to strict regulatory frameworks. This includes satisfying Anti-Money Laundering (AML) and Know Your Customer (KYC) compliance guidelines before releasing any secured deposits.

Tailoring Templates for Specific Industries

- Real Estate Transactions

- Templates focus heavily on property inspections, title searches, and mortgage approval contingencies before the release of earnest money.

- Mergers and Acquisitions (M&A)

- Receipts address indemnity holdbacks, working capital adjustments, and post-closing conditions spanning several months or years.

- Digital Asset Transactions

- Receipts incorporate cryptographic wallet addresses, multi-signature verification protocols, and smart contract execution triggers.

Security, Verification, and Digital Signatures

- Initiate bank-to-bank wire verification to confirm the cleared status of incoming funds.

- Utilize secure, cloud-based platform portals that comply with the ESIGN Act and eIDAS regulations.

- Generate unique cryptographic hashes for each signed document to prevent tampering.

- Distribute automated, system-stamped receipt copies to all certified parties simultaneously.

Common Pitfalls in Escrow Documentation

Implementation and Final Checklist

Before executing any agreement, confirm that your documentation satisfies this final readiness checklist:

- Have all parties verified their banking details via secondary communication channels?

- Are the specific triggering events for fund release clearly defined and mutually agreed upon?

- Is the neutral escrow holder properly licensed to manage the transaction size?

Professional Tip: Always run a test transaction or minor verification transfer prior to moving large capital sums to ensure routing pathways are secure and fully functional.

Leave a comment