Navigating the intricate landscape of nonresident alien tax withholding is a persistent challenge for withholding agents and payroll professionals, who must constantly balance regulatory accuracy with operational efficiency. Before addressing these compliance gaps, organizations must first understand the strict, evolving legal framework governing cross-border transactions. Utilizing standardized return document templates bridges this gap, granting compliance teams the streamlined workflows needed to reduce filing errors and mitigate costly IRS penalties.

It is important to note, however, that while templates for key documents-such as Form 1042-S and Form W-8BEN-provide concrete, actionable frameworks for data collection, they serve as organizational tools rather than substitutes for professional tax advice. In the following sections, we will explore the essential withholding templates every compliance team needs, outline best practices for their implementation, and provide a roadmap for error-free year-end reporting.

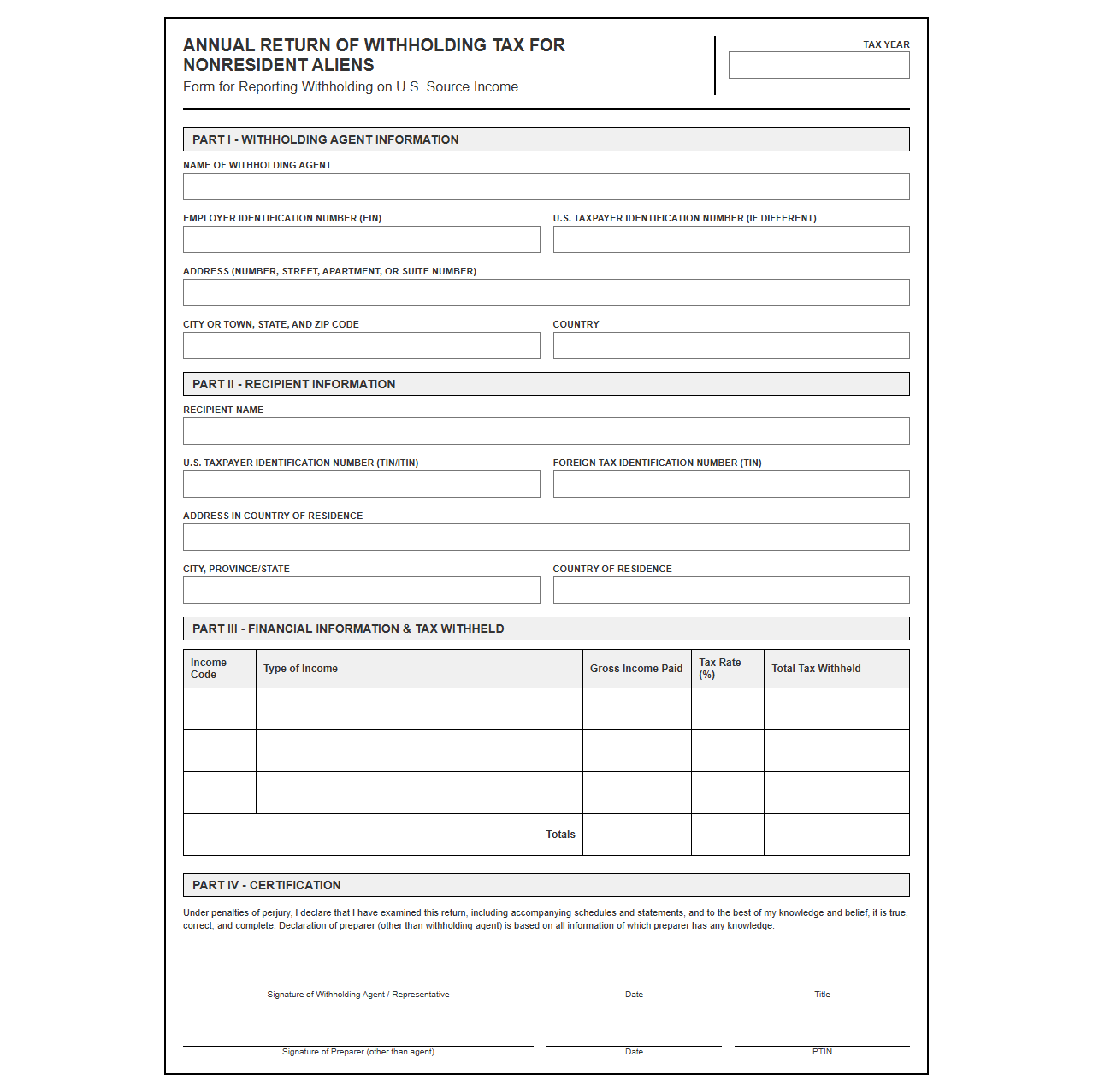

Nonresident Alien Withholding Tax Return Form

Download: .PDF

Download: .PDF

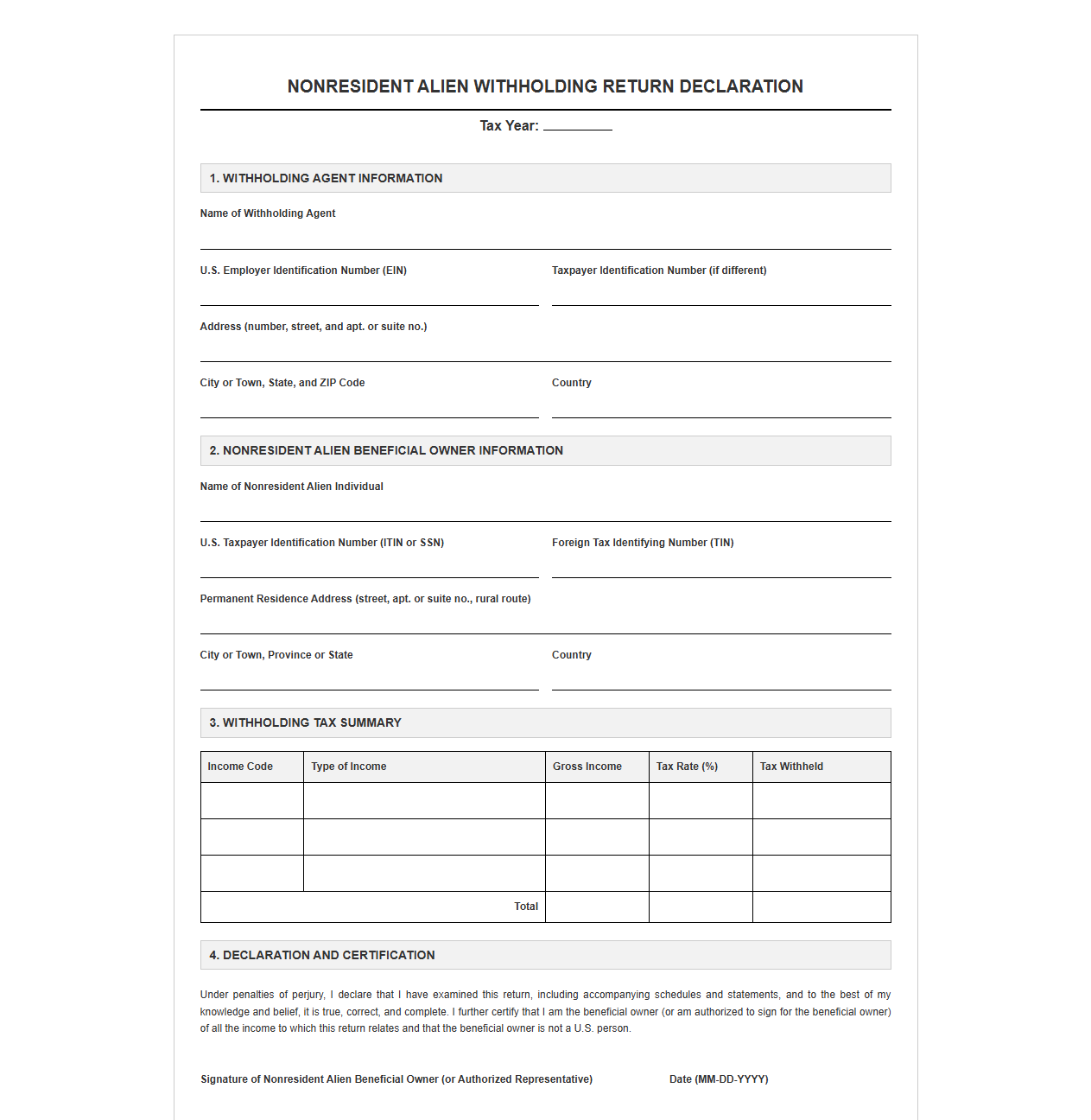

NRA Withholding Return Declaration Template

Download: .PDF

Download: .PDF

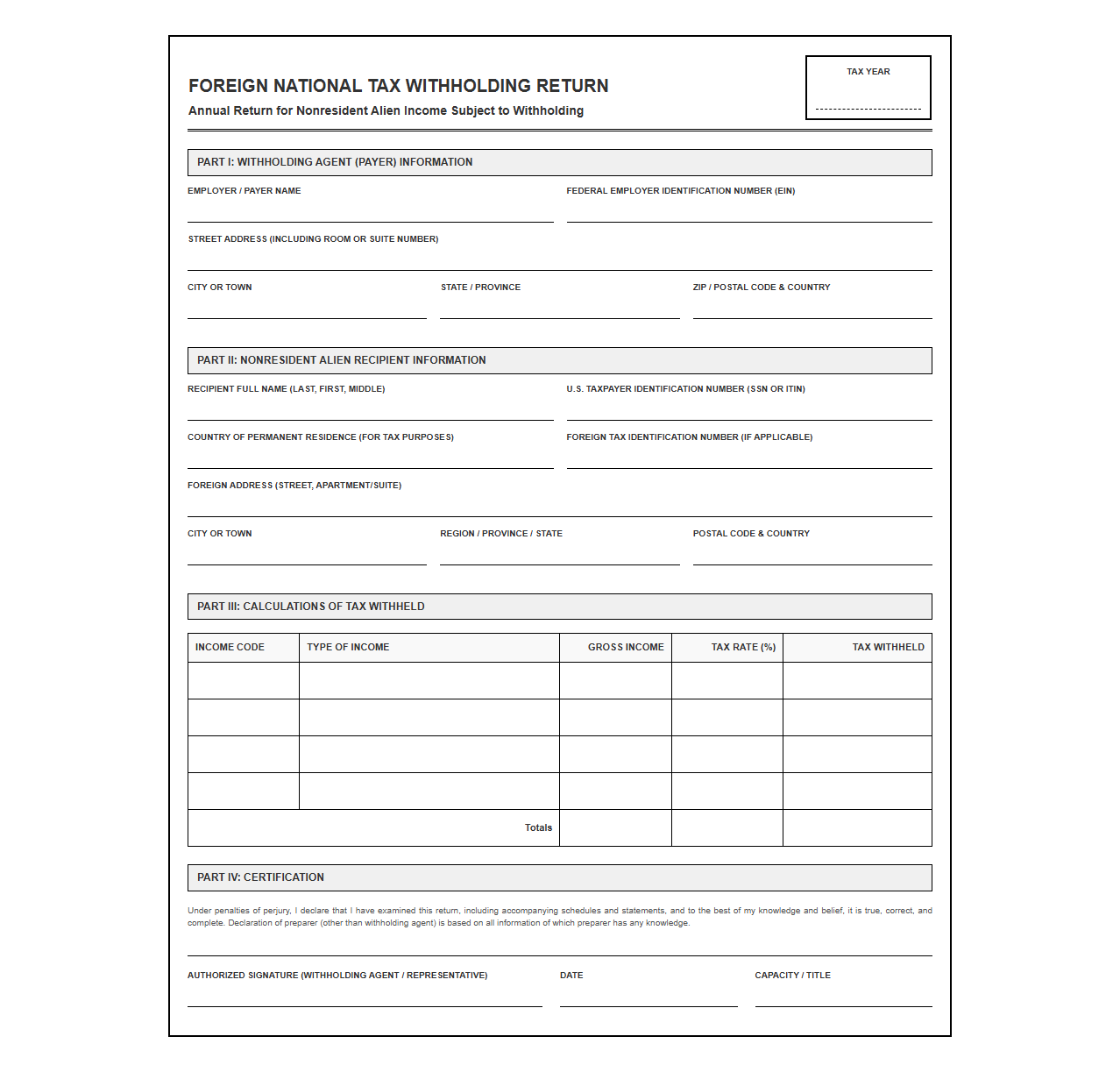

Foreign National Tax Withholding Return Template

Download: .PDF

Download: .PDF

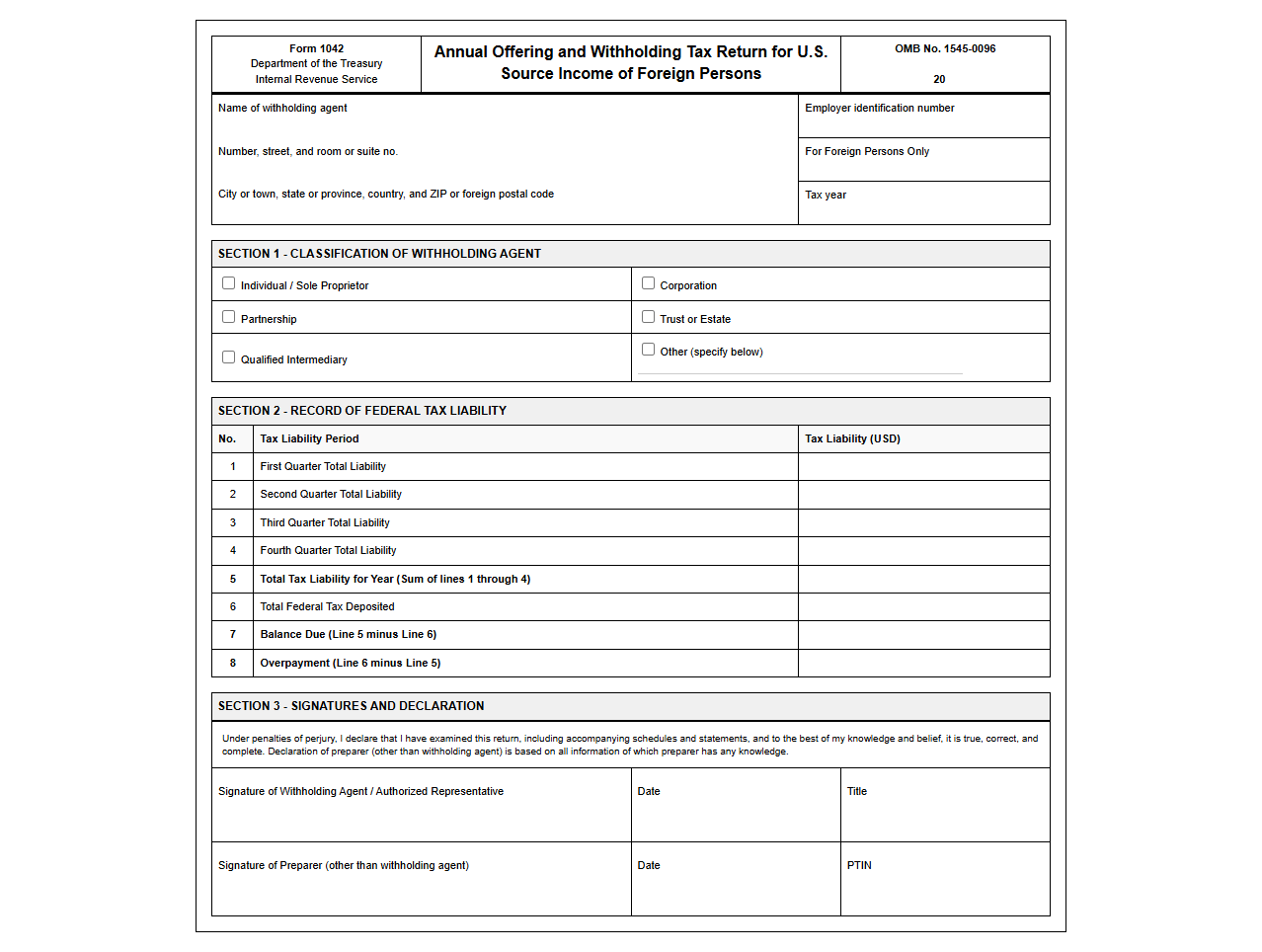

Annual Return for Nonresident Alien Withholding

Download: .PDF

Download: .PDF

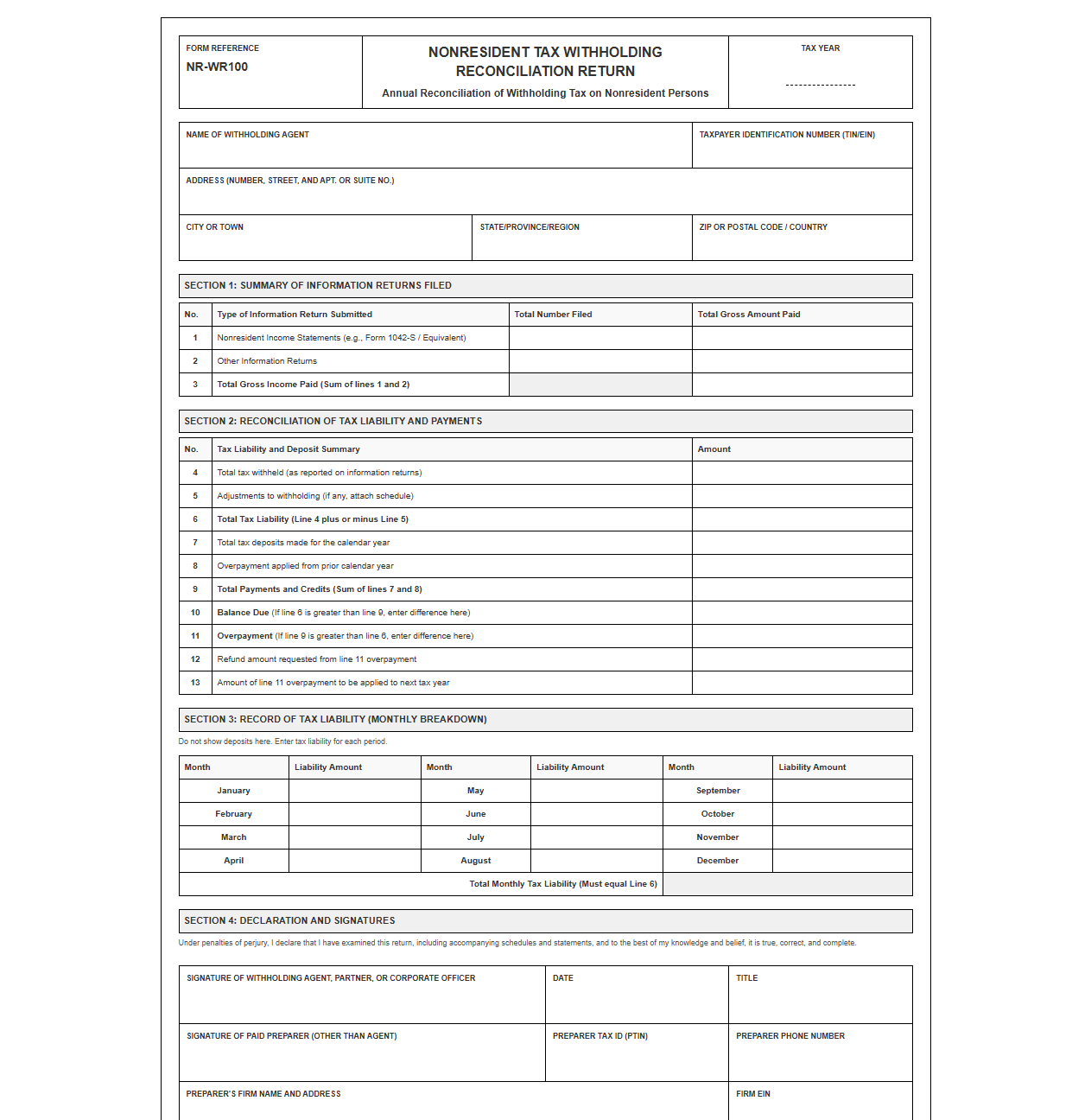

Nonresident Tax Withholding Reconciliation Return

Download: .PDF

Download: .PDF

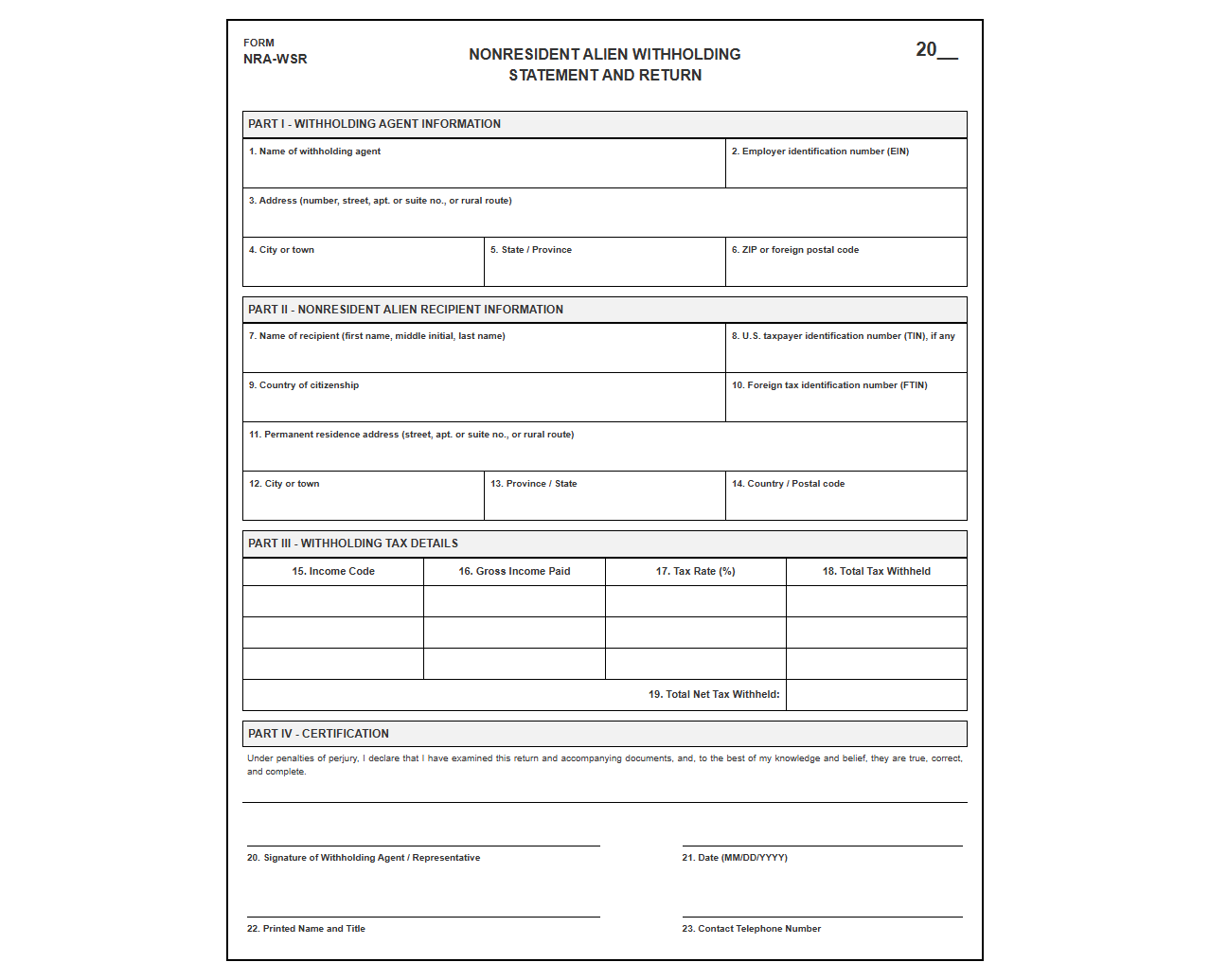

Nonresident Alien Withholding Statement and Return

Download: .PDF

Download: .PDF

Foreign Person Withholding Tax Return Template

Download: .PDF

Download: .PDF

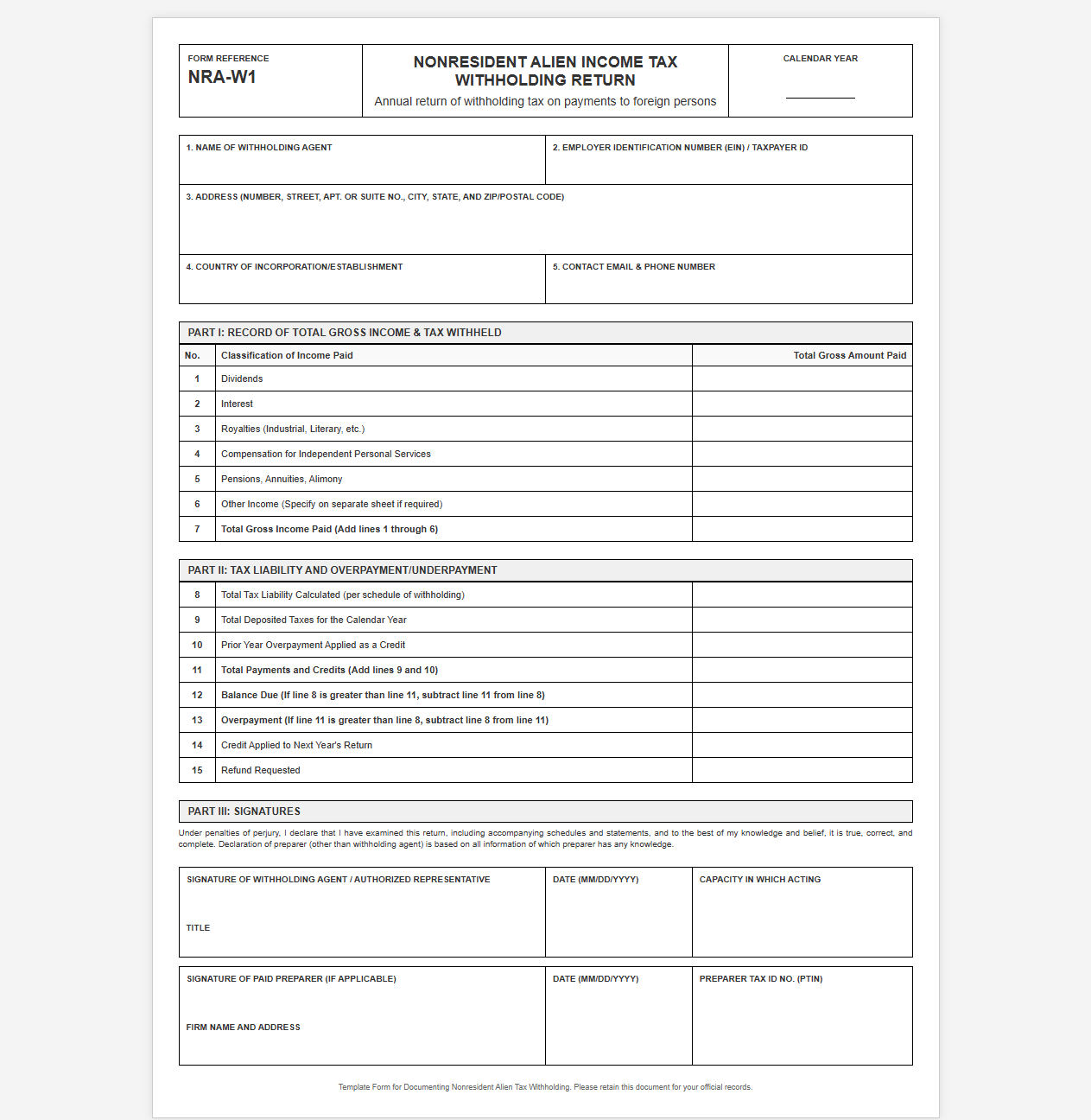

Nonresident Alien Income Tax Withholding Return

Download: .PDF

Download: .PDF

Demystifying Nonresident Alien Withholding Requirements

Navigating the complex landscape of United States tax compliance for foreign entities and individuals requires a deep understanding of Nonresident Alien (NRA) withholding rules. The Internal Revenue Service (IRS) imposes strict regulations on U.S. source income paid to foreign persons, making the role of the withholding agent exceptionally challenging. Managing these diverse requirements manually often leads to administrative friction, costly errors, and potential penalties. Fortunately, utilizing standardized document templates simplifies this intricate process, providing clear, reliable frameworks that help both withholding agents and nonresidents easily fulfill their legal obligations. By structuring complex regulatory requirements into predictable, repeatable formats, organizations can ensure consistent compliance and reduce the burden of cross-border tax administration.

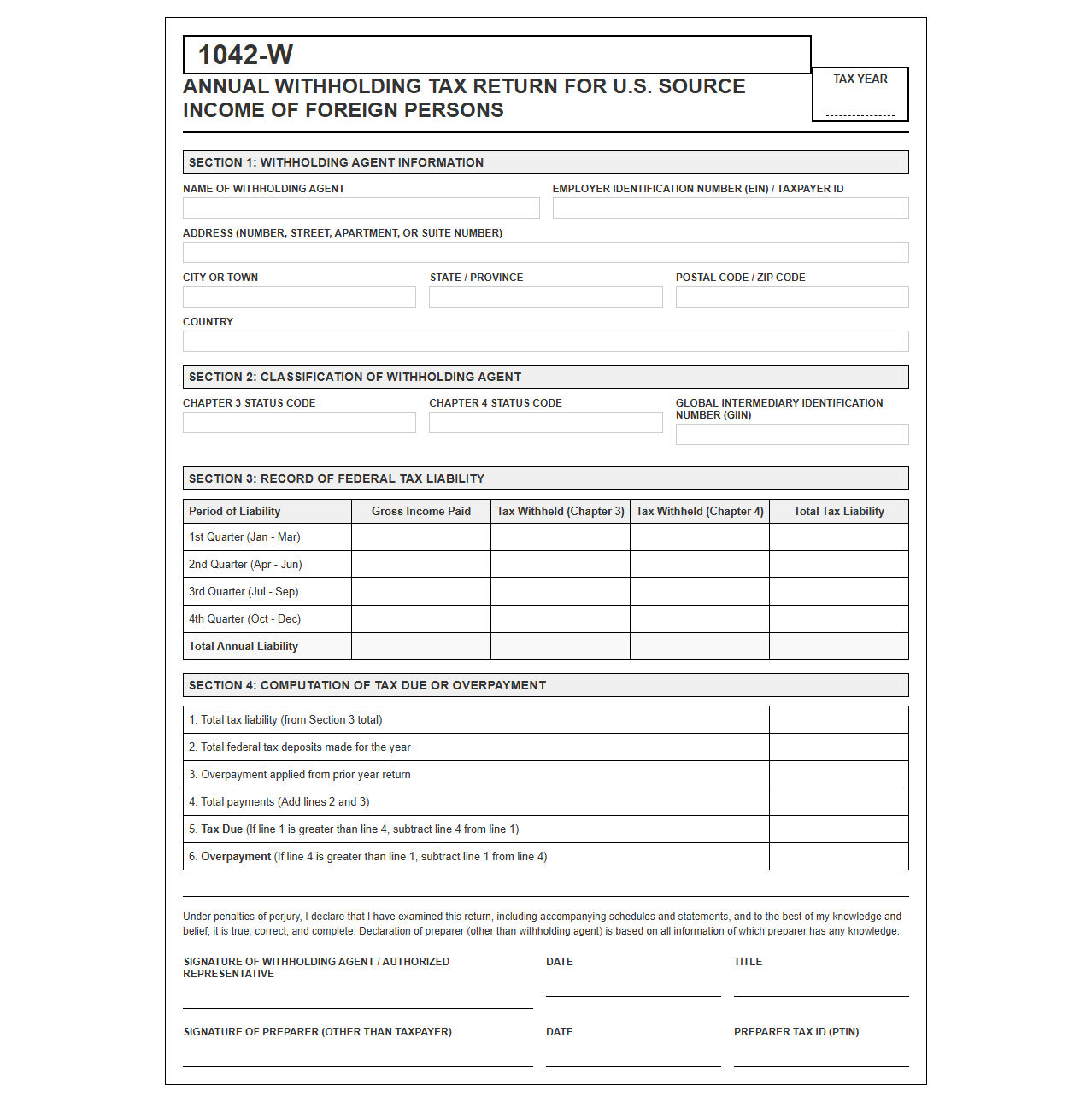

Form 1042-S: The Essential Information Return Template

Form 1042-S, "Foreign Person's U.S. Source Income Subject to Withholding," serves as the cornerstone of NRA tax reporting. Withholding agents must issue this form to report any U.S. source income paid to foreign persons, including dividends, interest, royalties, and compensation for services. A highly structured template makes it easier to compile this data accurately, ensuring that critical details are reported in accordance with IRS standards.

Using a standardized template for Form 1042-S helps organizations manage the following key components:

- Income Codes: Categorizing payments correctly to determine the appropriate tax treatment.

- Withholding Rates: Applying the standard 30% rate or a reduced treaty rate based on the recipient's residency.

- Recipient Information: Documenting names, foreign addresses, and Taxpayer Identification Numbers (TINs) with precision.

Certificate of Foreign Status: Choosing W-8BEN vs. W-8BEN-E

Before any payments are distributed, withholding agents must collect a Certificate of Foreign Status to establish the recipient's tax identity and determine the appropriate tax rate. The IRS provides different versions of the W-8 form based on whether the beneficial owner is an individual or an entity. Utilizing the correct template is vital, as these self-certification forms dictate the specific withholding rate and qualify the recipient for tax treaty benefits.

| Form Name | Target Audience | Primary Purpose |

|---|---|---|

| W-8BEN | Foreign Individuals | To establish foreign status, claim beneficial ownership of income, and claim tax treaty benefits. |

| W-8BEN-E | Foreign Entities | To certify foreign status, claim treaty benefits for corporations or partnerships, and document FATCA classification. |

Form 1040-NR: Streamlining the Annual Income Tax Return

While withholding agents handle reporting at the source, foreign individuals who earn U.S. source income must often file their own annual returns using Form 1040-NR. This comprehensive document template allows nonresidents to report income effectively, calculate their exact tax liabilities, and claim refunds for any excess withholdings. Standardizing the preparation of this form is essential for individuals navigating complex cross-border tax treaties.

Important Note: Form 1040-NR is specifically tailored for nonresidents who do not meet the substantial presence test, allowing them to isolate their U.S.-sourced income from their global assets. It provides the legal mechanism for foreign citizens to claim tax treaty exemptions directly from the IRS.

Creating Standardized Workflows for Document Collection

To minimize compliance risks and accelerate transaction times, organizations must establish a repeatable, secure workflow for collecting and validating tax documentation. Building a centralized, digital repository of current tax templates simplifies compliance for administrative teams.

- Identify and catalog all required IRS templates, including W-8BEN, W-8BEN-E, and Form 1042-S.

- Implement a secure, digital portal where foreign partners and clients can safely upload completed certification forms.

- Automate validation checks to verify that all required fields, including foreign tax identification numbers, are fully populated.

- Integrate digital signing capabilities to streamline authorization and maintain a clear audit trail.

Critical Compliance Pitfalls in NRA Documentation

Even small errors in tax documentation can trigger audit failures, back withholding liabilities, and penalties. Withholding agents must actively monitor incoming documentation to catch common inaccuracies before submission.

One frequent issue is relying on expired W-8 certificates. Generally, W-8 forms remain valid only for the year they are signed plus the three succeeding calendar years. Failing to request updated documentation is a major oversight. Another common mistake involves mismatched Taxpayer Identification Numbers (TINs), where the legal name of the entity or individual does not align perfectly with the number registered with the IRS. Implementing automated sanity checks on names and dates can prevent these issues from escalating into expensive non-compliance penalties.

Checklist for Maintaining Continuous Tax Compliance

To ensure that all nonresident alien documentation remains accurate and ready for audit, withholding agents should conduct structured internal reviews on a quarterly basis. Use the following practical checklist to maintain operational compliance:

- Review all active W-8 forms to identify those approaching their three-year expiration deadline.

- Validate that all withholding rates applied match the current country-specific treaty agreements.

- Reconcile domestic ledger accounts with the figures prepared for the annual Form 1042-S.

- Confirm that every nonresident payee has submitted a validated foreign or U.S. tax identification number where treaty benefits are claimed.

Leave a comment