Multinational tax departments increasingly struggle with the fragmented, highly manual process of preparing transfer pricing disclosure returns across diverse jurisdictions. Before addressing automation, organizations must first view this challenge through the lens of intensifying global audit scrutiny and the complex reporting demands of OECD Pillar Two. Standardizing corporate transfer pricing disclosure templates grants tax teams immediate operational efficiency and robust risk mitigation, transforming a recurring compliance bottleneck into a streamlined workflow.

To manage expectations, it is crucial to stipulate that while standardized templates unify data collection, they do not eliminate the necessity for localized regulatory adjustments. For instance, harmonizing data fields for OECD Local Files alongside specific country schedules-such as Australia's International Dealings Schedule (IDS) or Form 5472 in the United States-demonstrates how a unified framework can satisfy disparate tax authorities.

This article outlines the strategic advantages of template standardization, examines key design principles for global compatibility, and provides a roadmap for implementation.

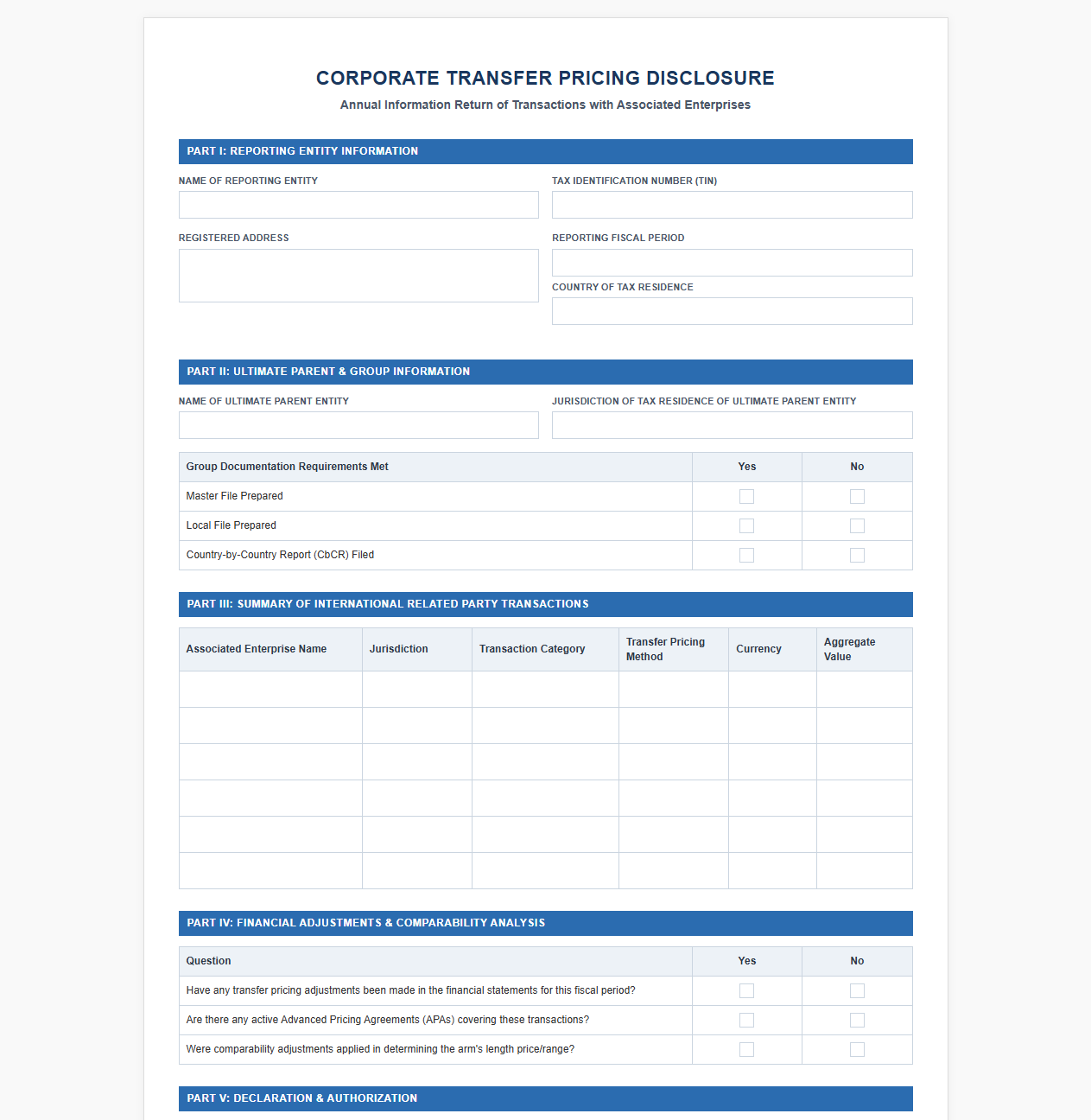

Corporate Transfer Pricing Disclosure Form

Download: .PDF

Download: .PDF

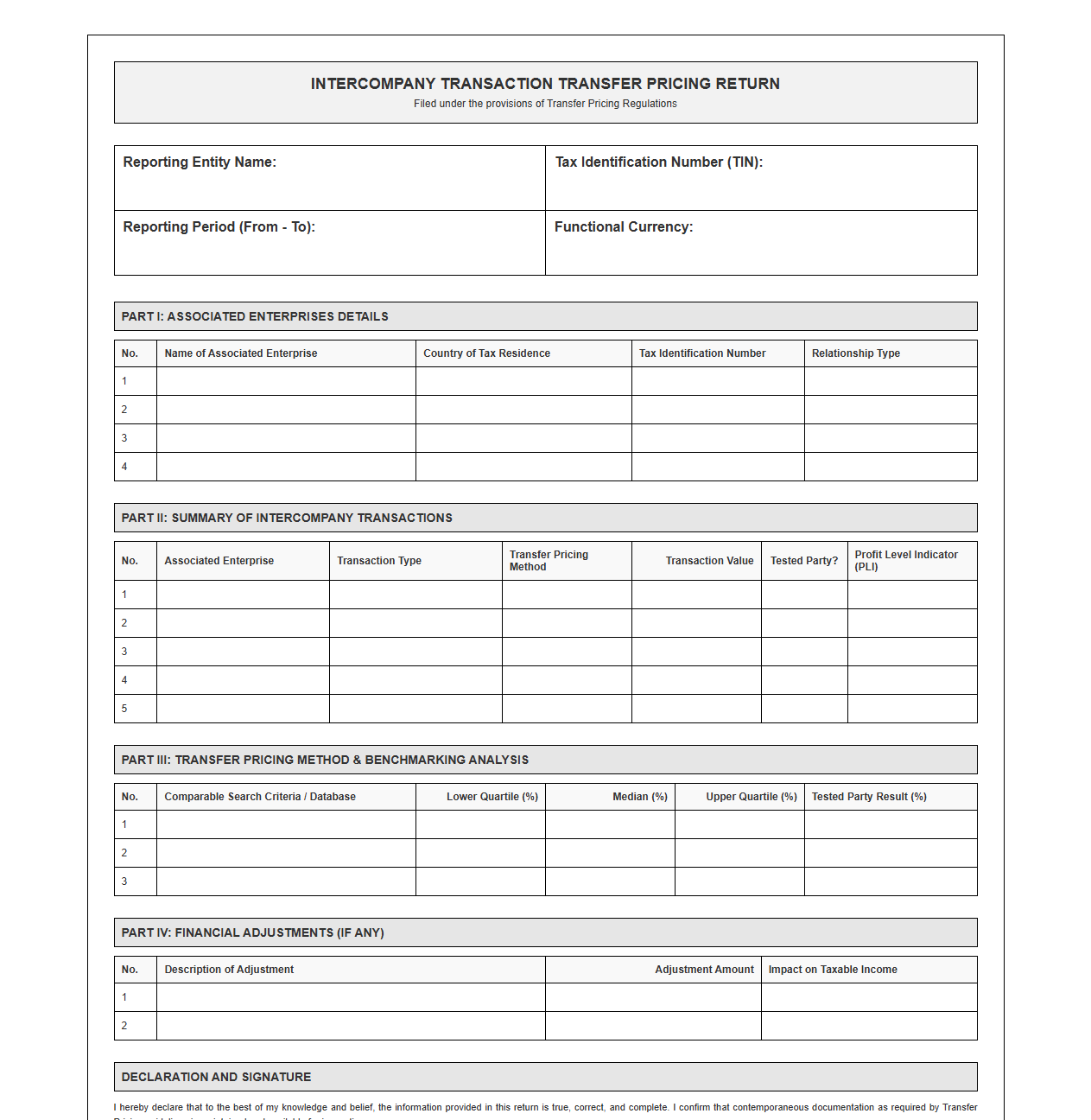

Intercompany Transaction Transfer Pricing Return

Download: .PDF

Download: .PDF

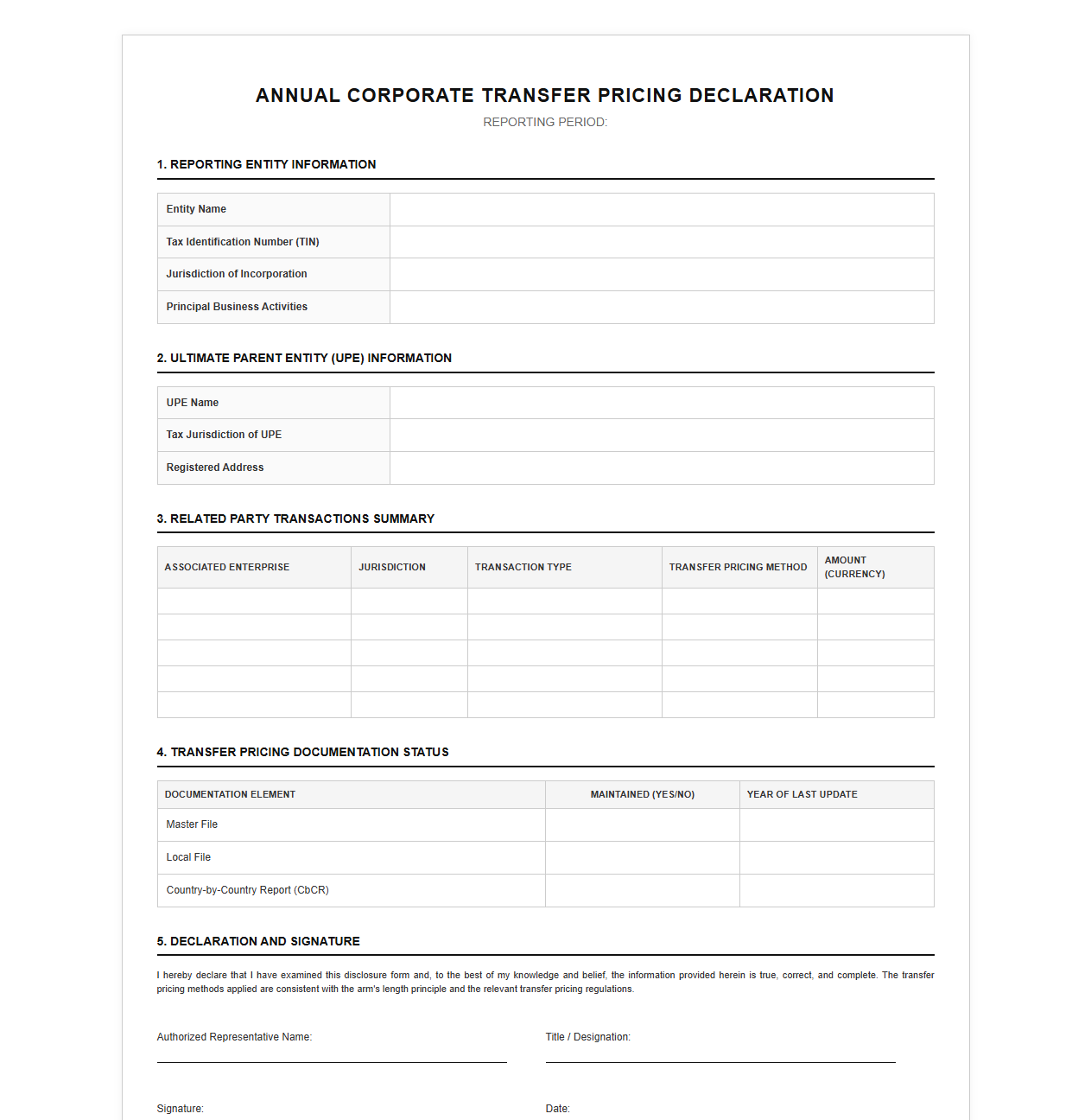

Annual Corporate Transfer Pricing Declaration Template

Download: .PDF

Download: .PDF

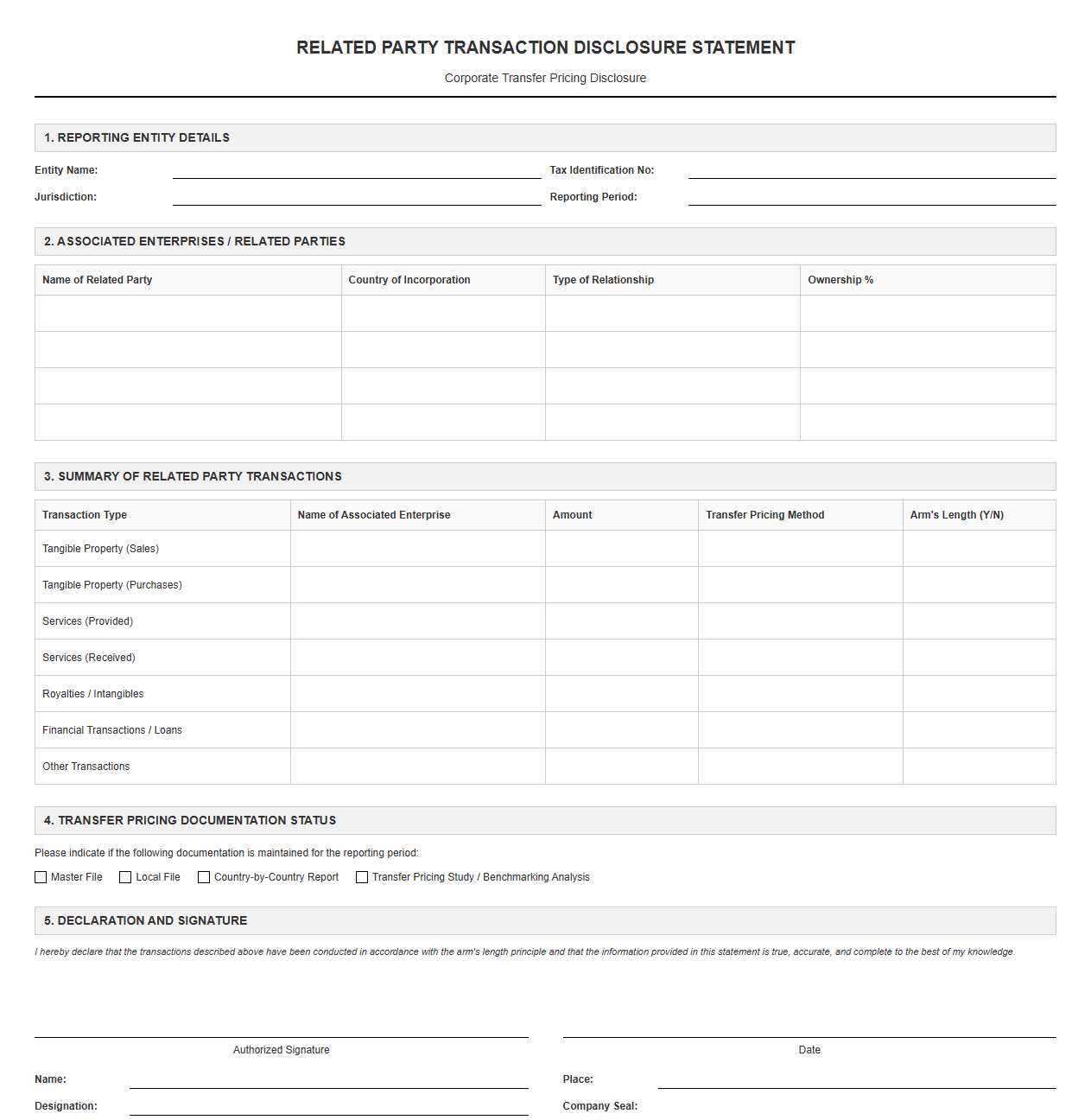

Related Party Transaction Disclosure Statement

Download: .PDF

Download: .PDF

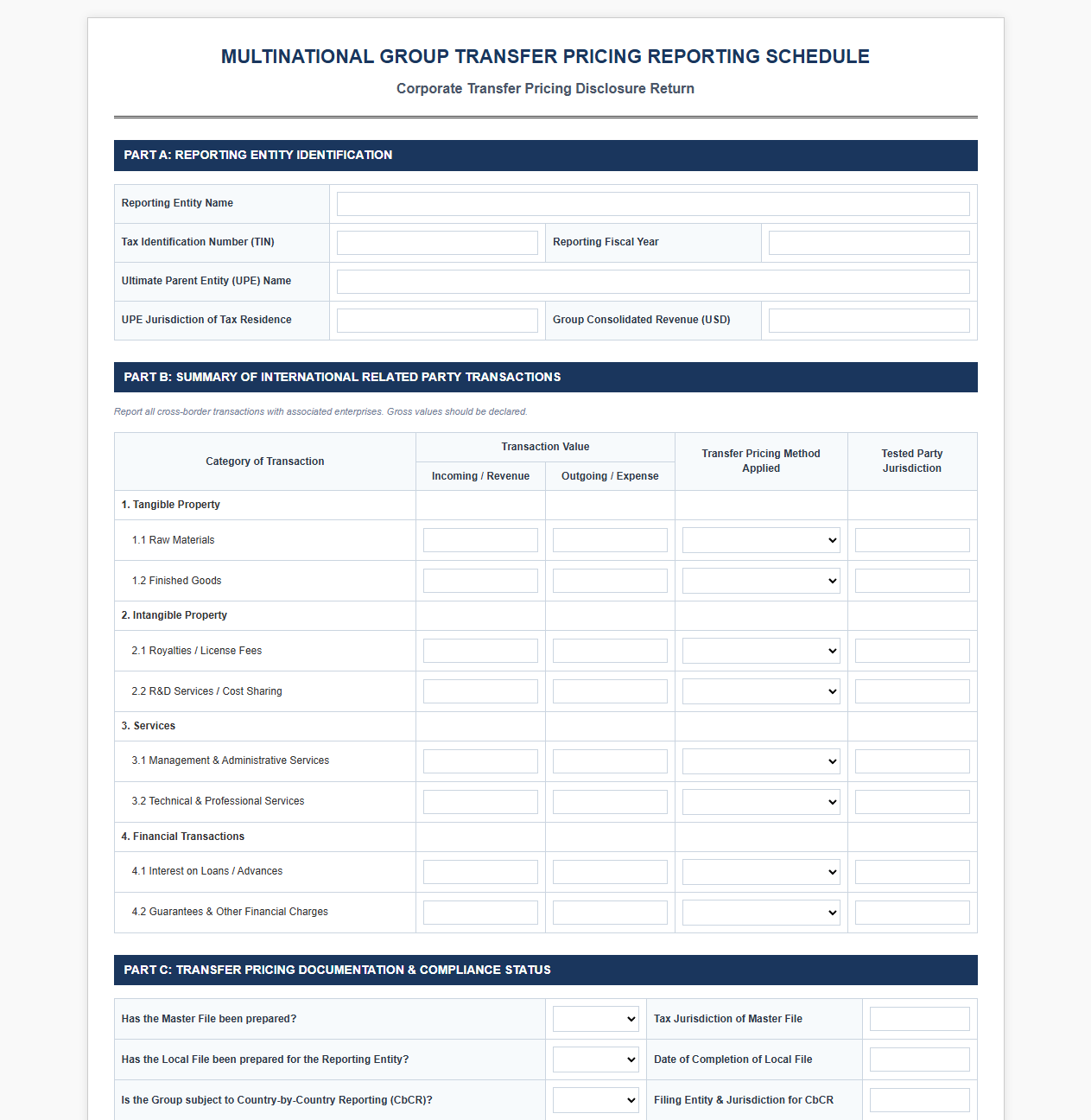

Multinational Group Transfer Pricing Reporting Schedule

Download: .PDF

Download: .PDF

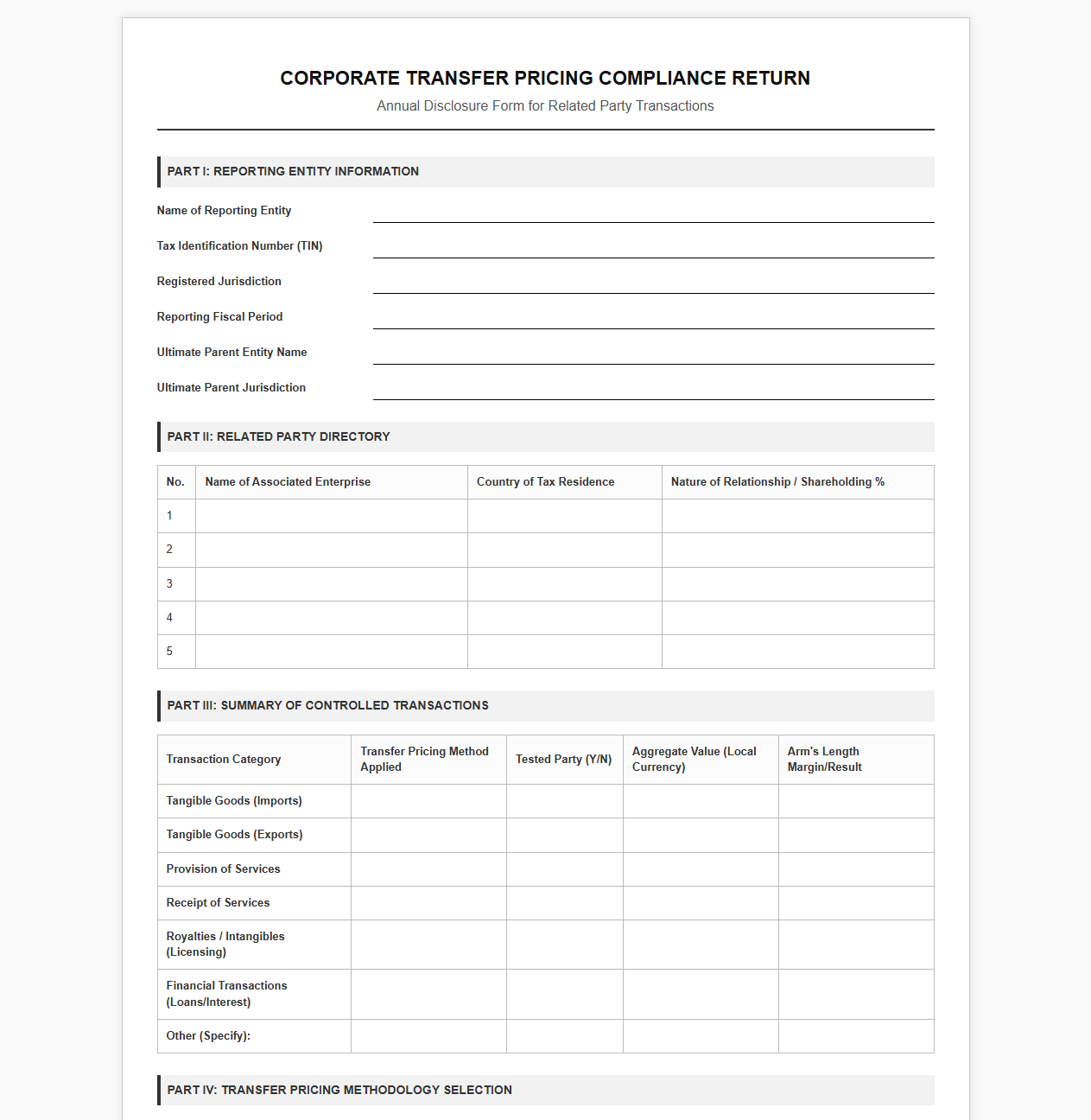

Corporate Transfer Pricing Compliance Return

Download: .PDF

Download: .PDF

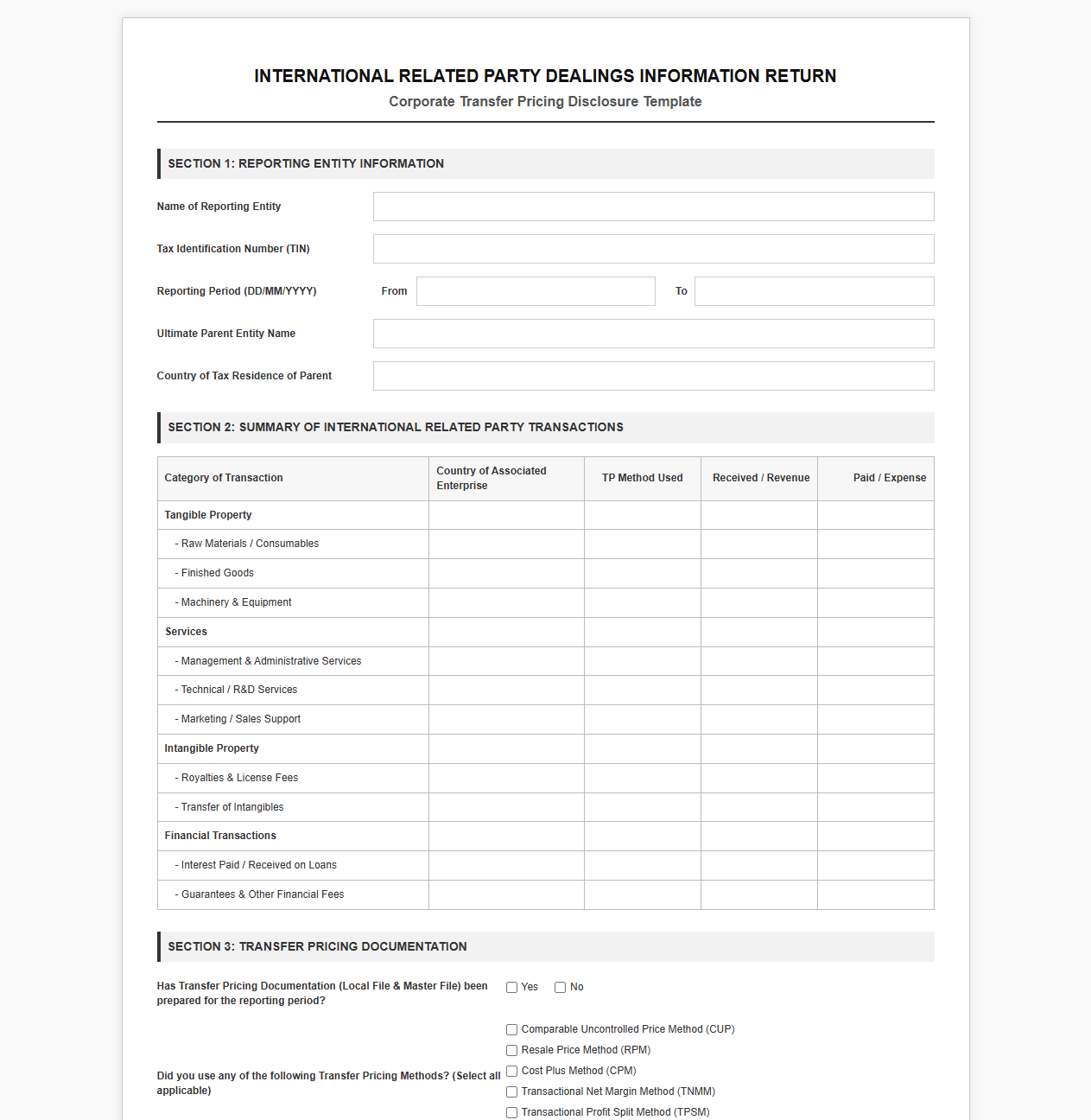

International Related Party Dealings Information Return

Download: .PDF

Download: .PDF

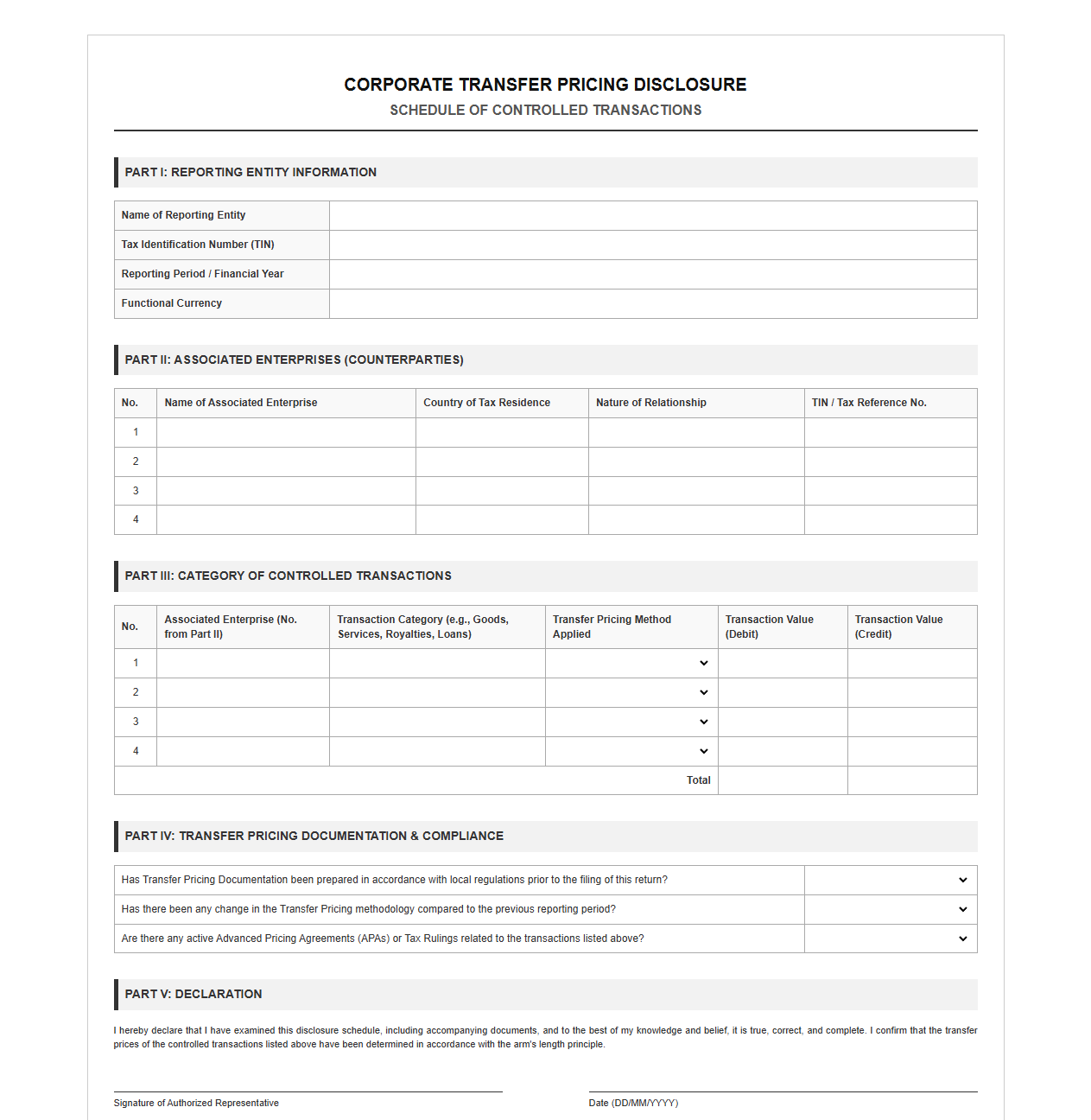

Controlled Transactions Transfer Pricing Disclosure Template

Download: .PDF

Download: .PDF

Group Transfer Pricing Information Return Form

Download: .PDF

Download: .PDF

The Fragmented Landscape of Global Transfer Pricing

Multinational enterprises (MNEs) today operate within an incredibly complex and fragmented global tax environment. Each tax jurisdiction maintains its own distinct transfer pricing disclosure requirements, forcing tax departments to navigate a labyrinth of localized rules, deadlines, and documentation formats. This lack of harmonization creates an extraordinary administrative burden, as tax teams must constantly duplicate efforts to tailor virtually identical financial and transactional data to satisfy minor regional nuances.

The consequences of this fragmentation extend beyond mere operational inefficiencies. The variance in local documentation demands increases the risk of compliance mismatches, leading to inconsistent disclosures across borders. When different tax authorities receive disparate representations of the same intercompany transactions, the probability of double taxation and aggressive transfer pricing audits escalates significantly, placing a severe strain on corporate resources.

The Imperative for Standardized Disclosure Templates

Transitioning toward standardized transfer pricing disclosure templates offers a clear path toward operational excellence. By establishing a uniform baseline for reporting intercompany transactions, multinational corporations can streamline their compliance workflows. Operational efficiency is significantly enhanced when tax departments can gather, process, and validate financial data once, utilizing a single source of truth to meet global obligations.

Furthermore, standardizing these disclosure formats leads to substantial risk reduction. When templates are consistent across jurisdictions, tax authorities receive clean, comparable, and reliable data. This level of transparency fosters a more predictable audit environment, helping enterprises proactively address transfer pricing mismatches and avoid costly bilateral disputes before they manifest.

Core Elements of a Unified Transfer Pricing Return

A globally viable standardized template must capture a comprehensive yet concise dataset to satisfy the core analytical needs of tax administrations. A unified transfer pricing return should structure information systematically across several fundamental categories:

- Transactional Data: Detailed records of intercompany transactions, including tangible goods transfers, service agreements, and intellectual property licensing fees.

- Methodology Selection: A clear justification for the chosen transfer pricing method, along with comparative benchmarking analysis.

- Functional Analysis: An overview of the functions performed, assets employed, and risks assumed (FAR) by each associated enterprise.

- Entity Profiling: Essential organizational data, including ownership structure, legal entity identifiers, and localized business descriptions.

Technical Architecture and XML Schema Integration

To transition standardized templates from conceptual frameworks to functional realities, tax systems must adopt robust technical data standards. Utilizing structured data formats like XML and JSON is critical for automating data exchange between corporate ERP platforms and tax authority portals. By relying on a standardized W3C XML Schema, organizations can ensure that validation rules are embedded directly within the transmission payload.

These structured formats allow for instant validation of data integrity, preventing formatting errors and mismatched currencies before submission. When corporate IT infrastructures can map financial ledgers directly to XBRL or JSON-LD schemas, the manual effort of compliance reporting is minimized, paving the way for frictionless, machine-to-machine tax reporting.

Aligning Templates with OECD BEPS Action 13

Standardized disclosure templates must align with the global consensus established by the Organisation for Economic Co-operation and Development (OECD). Specifically, these templates must map directly to the three-tiered documentation structure defined under Base Erosion and Profit Shifting (BEPS) Action 13.

Ensuring Master File and Local File Consistency

A unified template serves as the connective tissue between the Master File and the Local File. By enforcing strict data alignment, the template ensures that the high-level global business operations described in the Master File are perfectly consistent with the localized transactional details presented in the Local File. This systematic mapping prevents conflicting narratives that could trigger unnecessary corporate tax audits.

Overcoming Barriers to Global Adoption

Despite the clear benefits of standardized reporting, several hurdles impede rapid global implementation. Local legislative resistance remains a formidable challenge, as individual jurisdictions often guard their sovereign taxing rights and demand specialized disclosures tailored to their legacy legal systems.

"The convergence of international tax reporting standards requires not only technical consensus, but also the alignment of sovereign legislative bodies and the modernization of legacy IT frameworks across diverse jurisdictions."

Additionally, strict data privacy regulations, such as GDPR, create hurdles for cross-border data transmission. Corporations are also constrained by legacy ERP systems that struggle to aggregate and export transactional data in standardized, schema-compliant formats without costly custom integrations.

The Future of Real-Time Transfer Pricing Compliance

The adoption of standardized templates represents a major step toward a fully digitalized tax ecosystem. This structural shift lays the necessary groundwork for real-time transfer pricing reporting, moving the industry away from retrospective compliance and toward proactive transaction monitoring.

As structured data becomes the global norm, tax authorities will increasingly leverage AI-driven tax audits to instantaneously detect transfer pricing anomalies across borders. Organizations that integrate standardized schemas into their core financial systems today will enjoy a sustainable competitive advantage, achieving continuous compliance in an era of automated international taxation.

Leave a comment