Discovering a calculation error or an omitted deduction on a previously submitted corporate tax filing can trigger immediate anxiety regarding audits and costly compliance penalties. While regulatory bodies demand absolute accuracy, the tax code inherently accommodates the complexity of corporate accounting by providing a structured rectification process. Utilizing standardized amended income tax return templates grants financial officers the precision needed to correct these oversights swiftly, safeguarding corporate credibility while potentially recovering overpaid assets.

However, successful amendment relies on adherence to strict regulatory windows; for instance, the IRS generally stipulates that corrections must be submitted within three years of the original filing date. Utilizing dedicated templates for frameworks like IRS Form 1120-X ensures that revised liabilities and net income adjustments are documented exactly as auditors require. In this article, we will outline the step-by-step process of deploying these templates, highlight common filing pitfalls to avoid, and establish a clear path to restoring your corporate compliance.

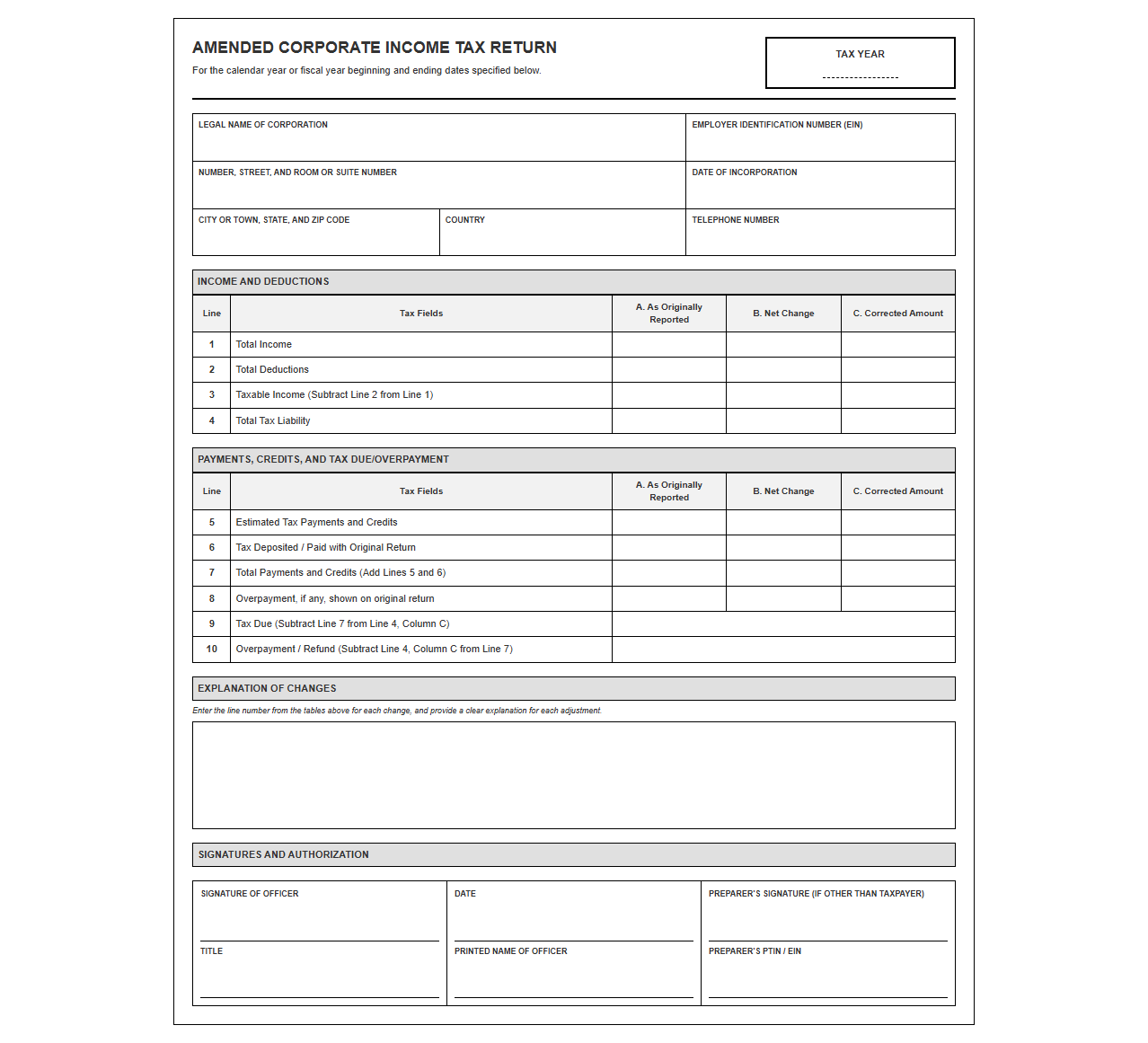

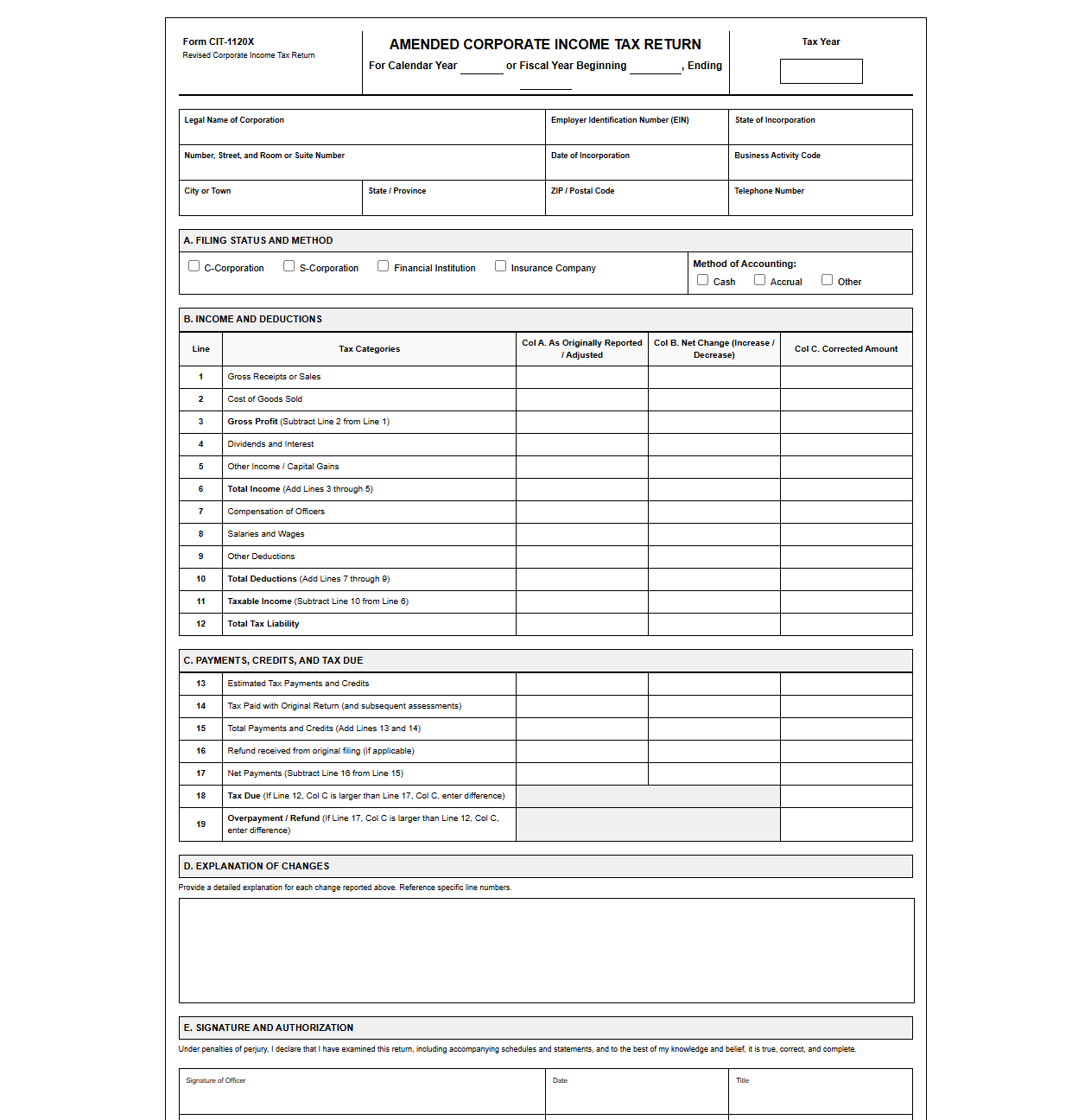

Amended Corporate Income Tax Return Template

Download: .PDF

Download: .PDF

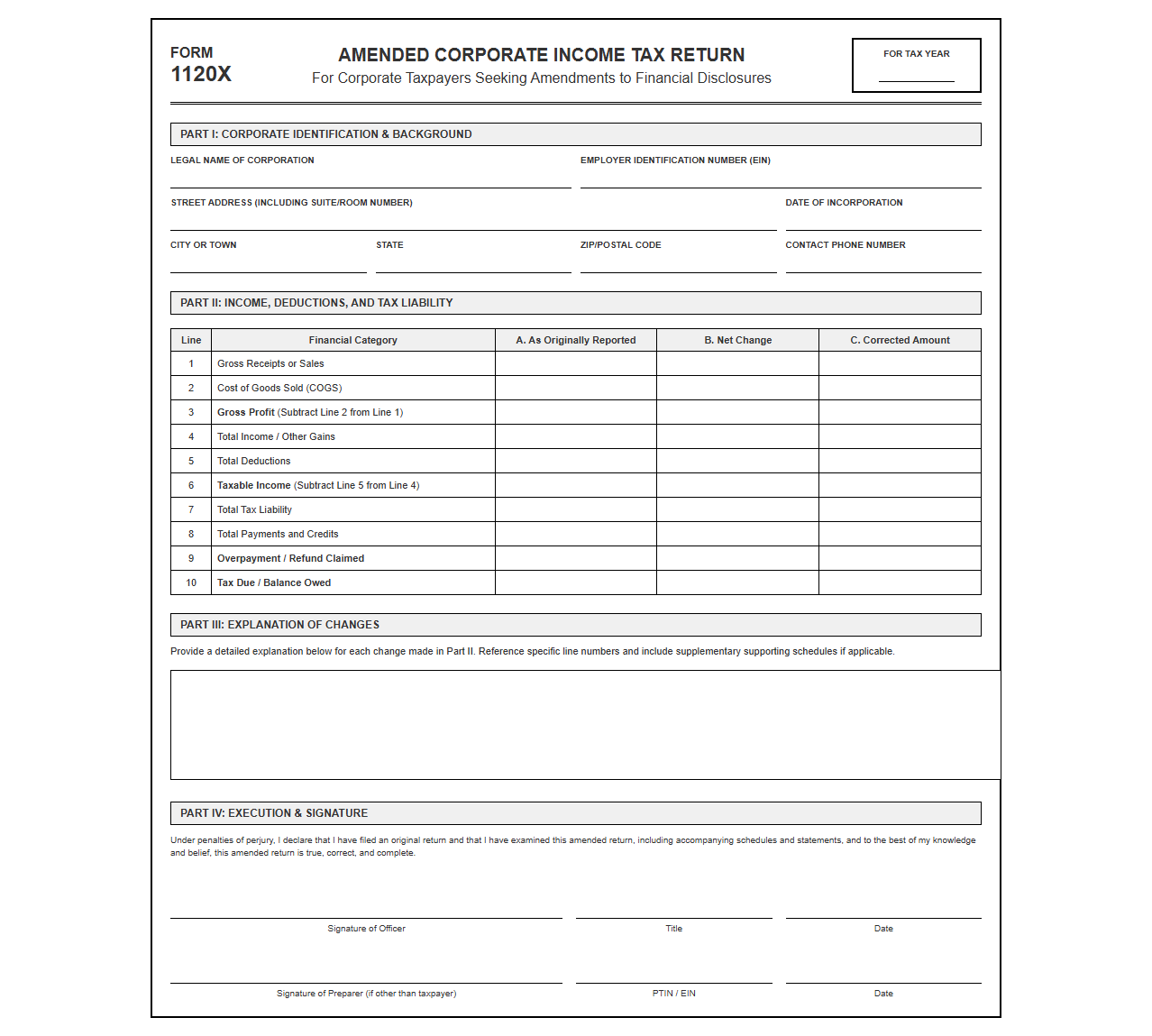

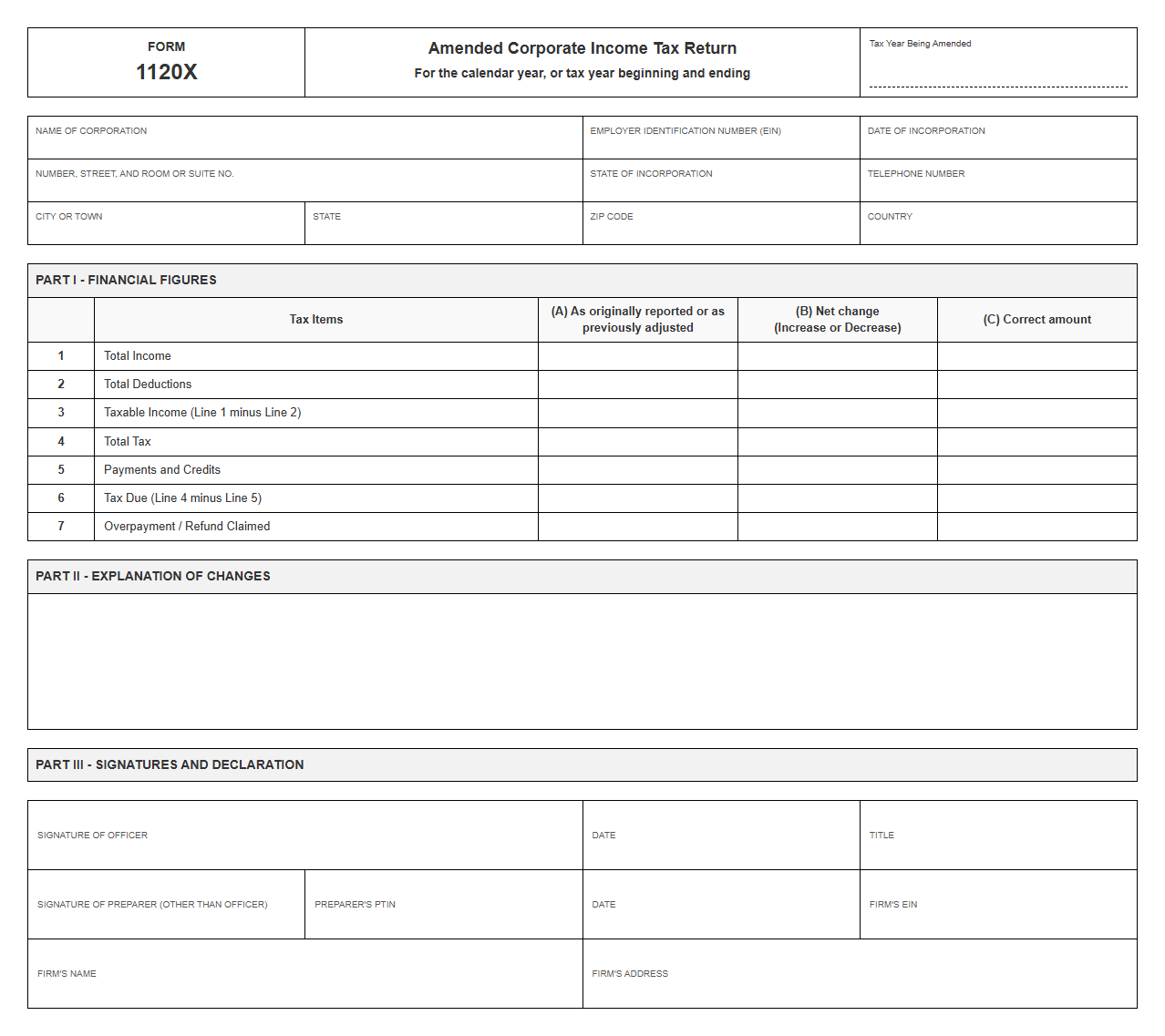

Corporate Income Tax Amendment Return Form

Download: .PDF

Download: .PDF

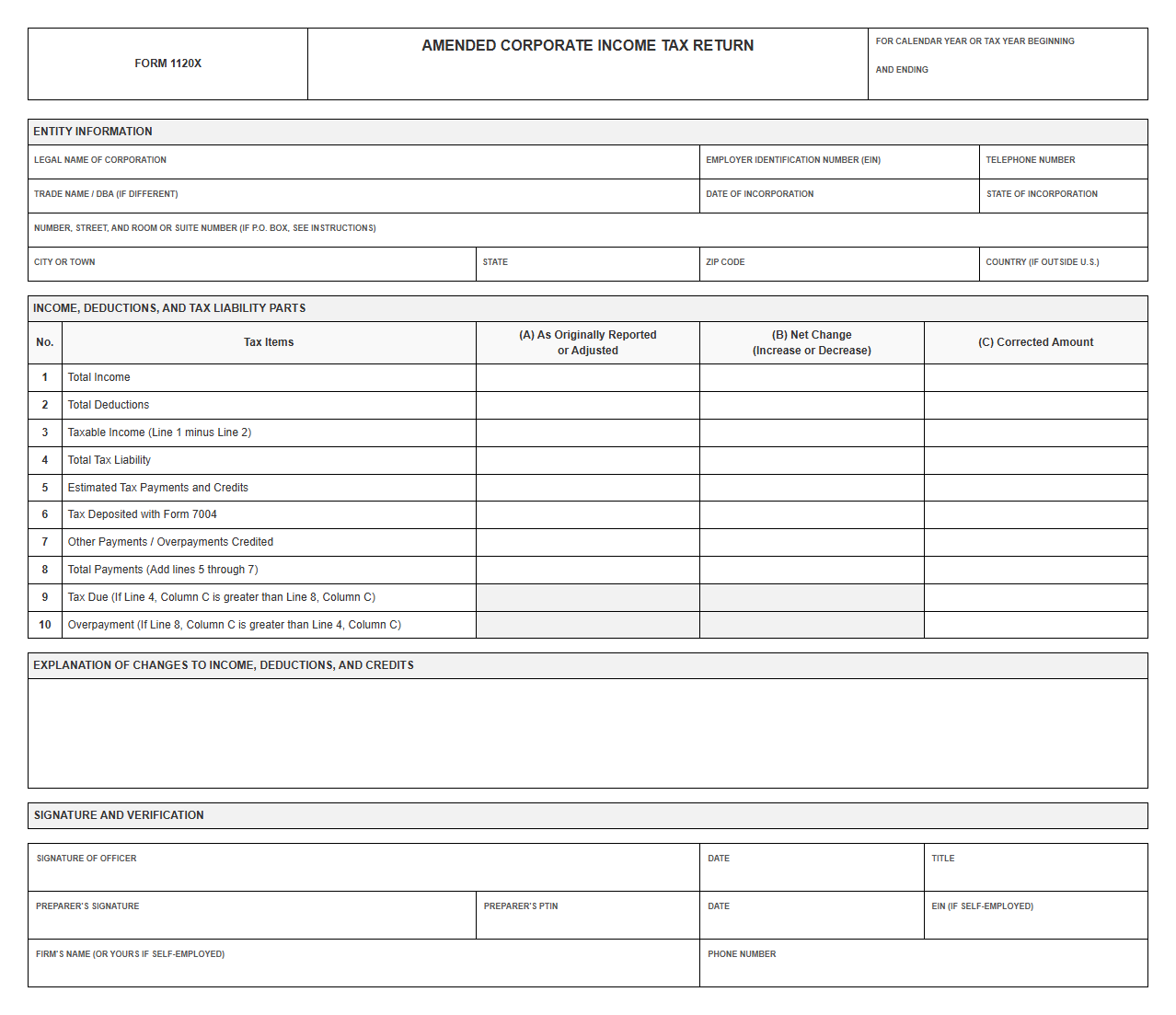

Amended Corporate Tax Return Filing Template

Download: .PDF

Download: .PDF

Revised Corporate Income Tax Return Template

Download: .PDF

Download: .PDF

Corporate Tax Return Amendment Form Template

Download: .PDF

Download: .PDF

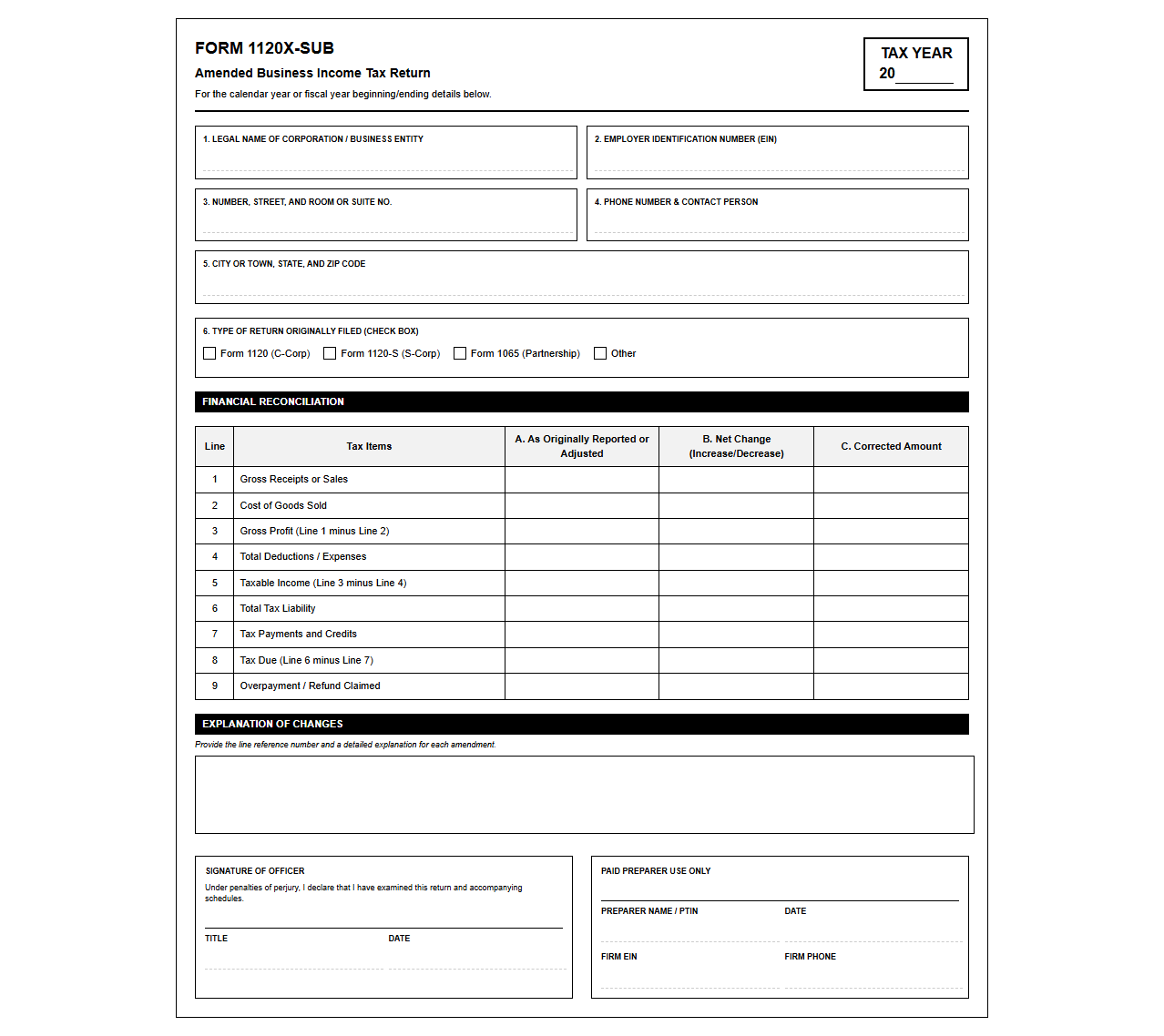

Amended Business Income Tax Return Template

Download: .PDF

Download: .PDF

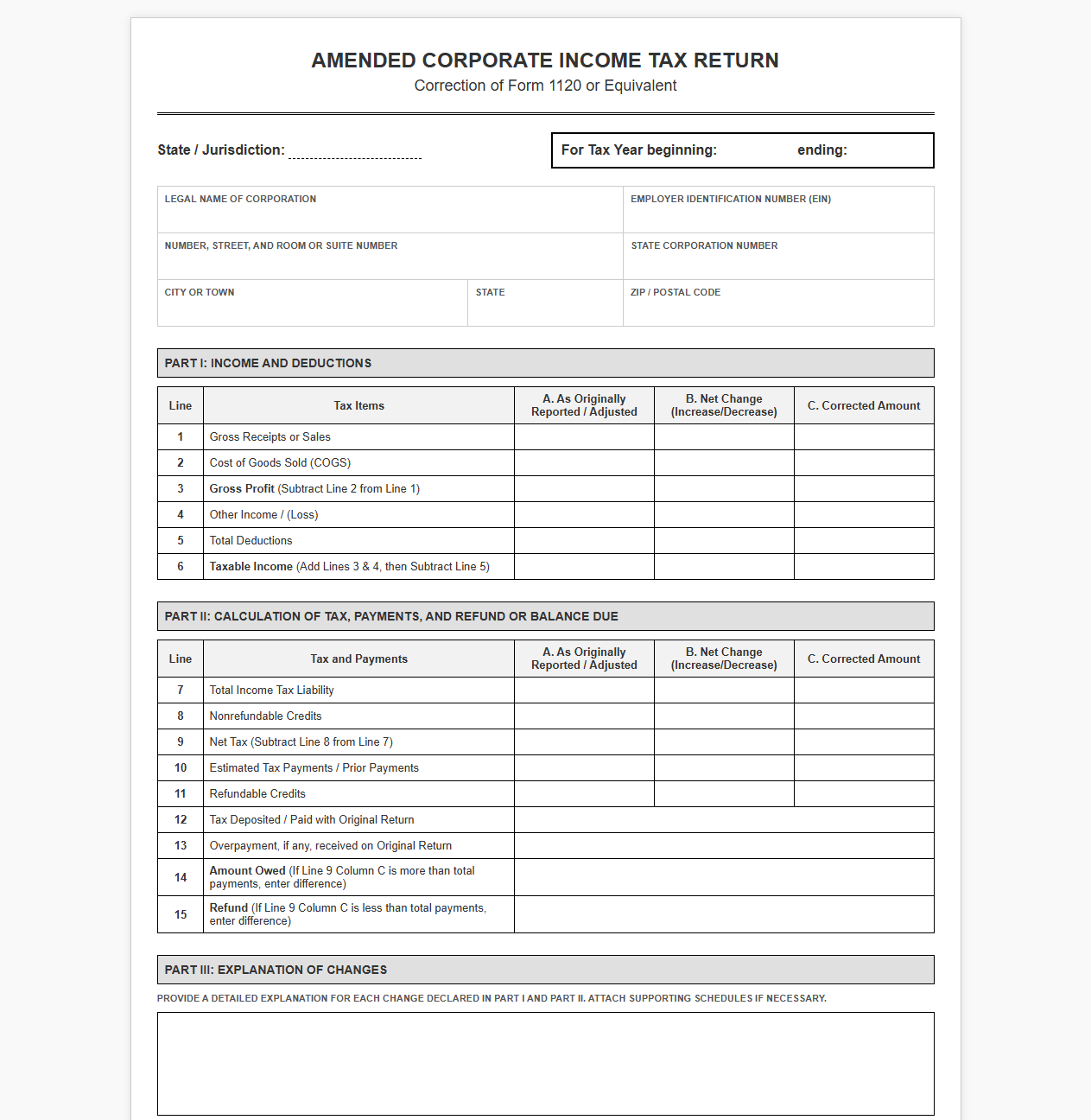

Corporate Income Tax Correction Return Template

Download: .PDF

Download: .PDF

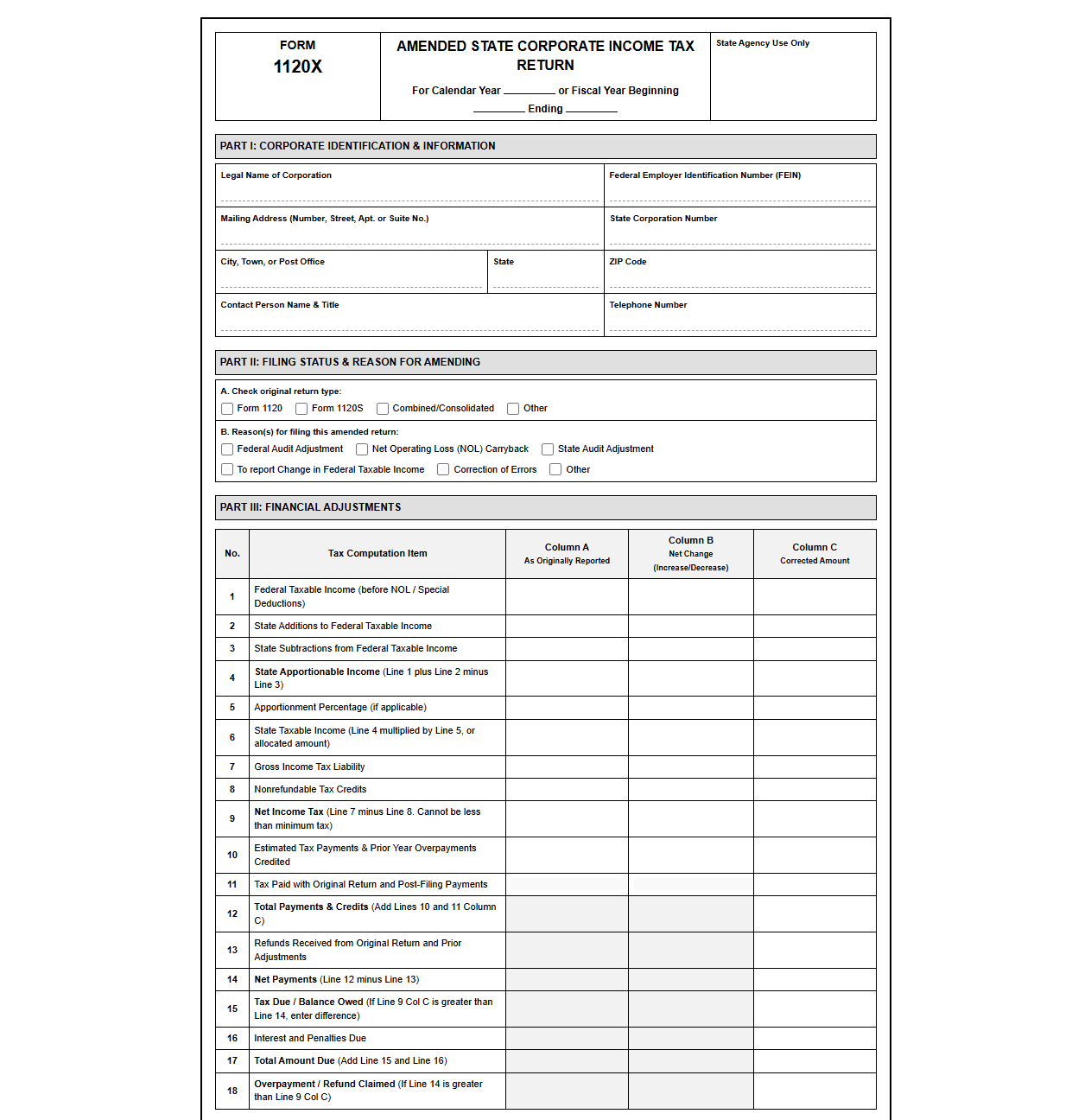

Amended State Corporate Income Tax Return Template

Download: .PDF

Download: .PDF

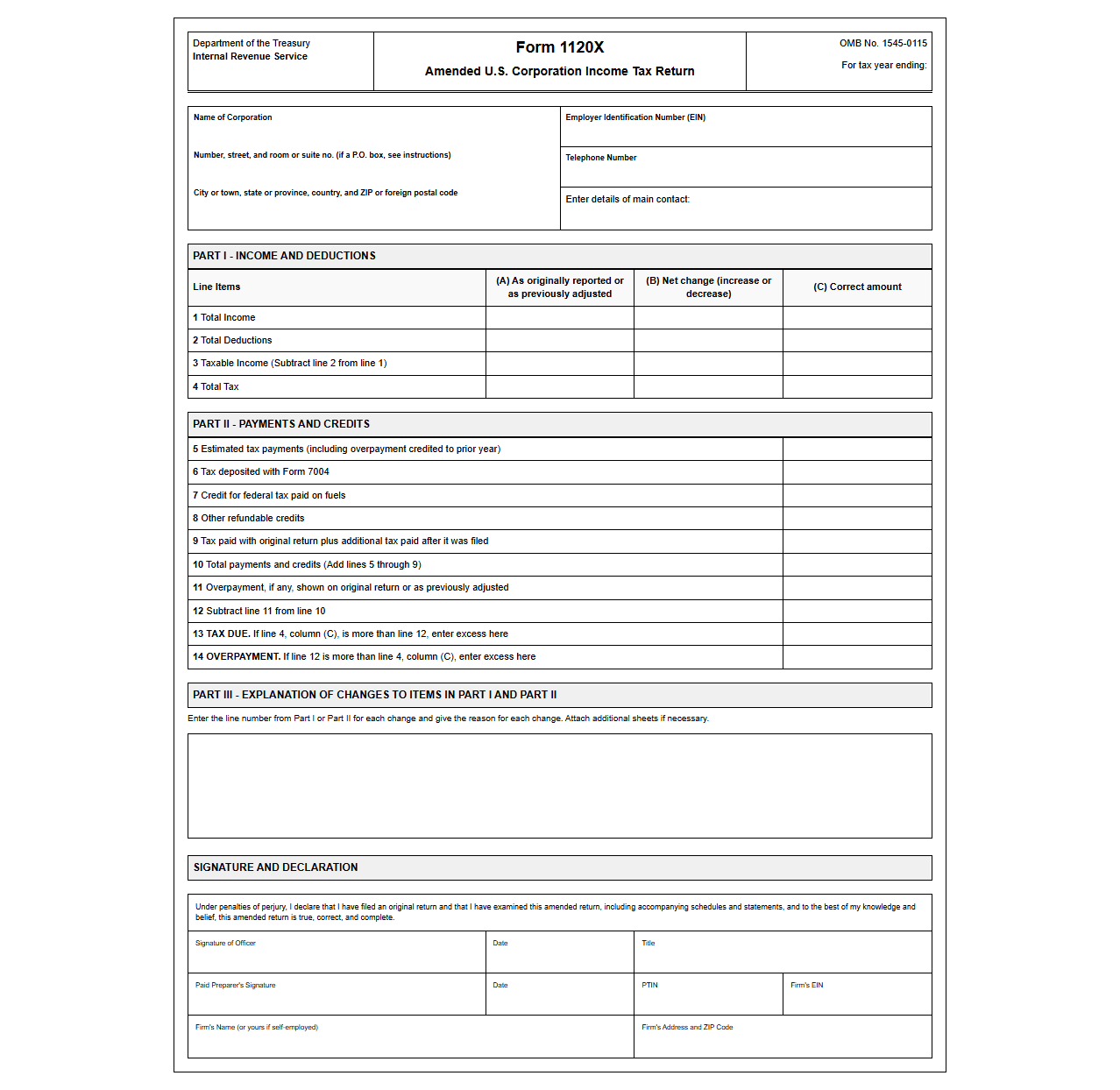

Amended Federal Corporate Income Tax Return Template

Download: .PDF

Download: .PDF

Recognizing Common Corporate Tax Filing Mistakes

Filing corporate taxes is a complex undertaking where even minor oversights can lead to significant financial consequences. Many corporations inadvertently make calculation mistakes, transpose numbers, or overlook valuable industry-specific deductions that could substantially lower their taxable income. Operating in a fast-paced business environment makes it easy to miss these nuances, leaving money on the table or triggering compliance red flags. When these errors occur, they do not have to remain permanent fixtures of your financial record. Accepting that mistakes happen is the first step toward correcting them, which is where the process of amending tax returns becomes an essential tool for corporate treasury and accounting departments.

When is an Amended Corporate Tax Return Required?

Not every error on a corporate tax return demands a formal, complex amendment. The IRS utilizes automated systems that routinely identify and fix simple mathematical miscalculations, sending a notice of correction directly to the business. However, major alterations to your financial data require a proactive filing. You must file an amended corporate tax return under the following circumstances:

- Changes to reported income: Discovering unreported gross receipts or realizing that income was overstated.

- Adjustments to business deductions: Claiming write-offs that were previously overlooked or correcting deductions that were taken in error.

- Claiming tax credits: Retroactively applying research and development (R&D) credits or work opportunity tax credits.

- Net Operating Loss (NOL) carrybacks: Adjusting prior year returns to account for losses that can be carried back to generate immediate refunds.

The Role of Amended Income Tax Return Templates

Navigating the corrective filing process can be daunting, but utilizing standardized corporate tax templates simplifies administrative burdens. These structured digital frameworks guide tax preparers through the intricate process of modifying previously submitted data, ensuring that both federal and state regulations are meticulously satisfied.

"Using a standardized corporate tax amendment template minimizes manual entry errors and significantly reduces compliance overhead by ensuring all state-specific and federal schedules are accounted for."

By relying on pre-configured templates, businesses can establish a repeatable workflow. This reduces the hourly costs typically paid to external accounting firms and helps internal teams verify that every necessary supporting schedule is completely filled out before submission.

Step-by-Step Guide to Amending Your Corporate Return

Correcting your corporate tax filing requires a systematic approach to prevent secondary errors. Follow this chronological process to ensure accuracy:

- Gather original documents: Retrieve a copy of the originally filed corporate return (such as Form

1120or1120-S) along with all supporting schedules and worksheets. - Identify the correct amendment form: Select the appropriate federal amendment form, typically Form

1120-Xfor C-corporations, along with any corresponding state correction forms. - Input corrected figures: Utilize your amendment template to enter the original amounts, the net change (increase or decrease), and the newly calculated correct values.

- Draft the explanation of changes: Complete the mandatory narrative section of the form, clearly stating why the adjustments are being made and referencing the specific lines of the return that are being modified.

Crucial Pitfalls to Avoid When Filing Amendments

Filing an amendment incorrectly can delay your refund or increase your exposure to an audit. To protect your business, keep these common traps in mind:

- Ignoring the statute of limitations: Generally, corporations must file a claim for a refund within three years from the date the original return was filed, or two years from the time the tax was paid, whichever is later.

- Failing to attach supporting documentation: If you are claiming a new deduction or credit, you must attach the modified forms and clear proof of the changes; otherwise, the IRS may reject the amendment.

- Neglecting state-level amendments: Correcting your federal return almost always triggers a requirement to report these changes to your state department of revenue within a strict timeframe.

Submission Methods: Paper vs. Electronic Filing

Corporations have different options for submitting amended returns depending on their entity type and the specific tax year being corrected. Below is a comparison of the primary submission methods:

| Feature | Paper Mailing (Form 1120-X) | Electronic Filing (e-File) |

|---|---|---|

| Processing Speed | Slow (can take several months) | Fast (typically processed within weeks) |

| Tracking Capabilities | Limited (requires certified mail tracking) | Instantaneous confirmation receipt |

| Error Risk | Higher due to manual processing | Lower due to system validation checks |

Establishing Long-Term Corporate Tax Compliance

The most efficient way to handle corporate tax errors is to prevent them from occurring in the first place. By upgrading your internal financial controls, you can significantly lower the frequency of future amendments. Implementing routine internal auditing procedures and migrating to modern, cloud-based digital bookkeeping platforms allows your financial team to track transactions with precision throughout the fiscal year.

Adopting these preventative strategies ensures that your financial statements remain accurate and audit-ready. To protect your organization's bottom line and learn more about navigating corporate tax adjustments, explore our complete library of financial compliance templates to streamline your business workflows.

Leave a comment