Corporate tax departments consistently struggle with the high-stakes complexity of capital gains reporting, where minor calculation errors can trigger costly audits. As regulatory bodies globally tighten reporting standards, tax professionals face the compounding burden of manually reconciling diverse transaction histories across various asset classes.

Utilizing standardized return document templates grants compliance teams immediate operational efficiency and safeguards against reporting discrepancies. Please note that while these templates provide robust structural frameworks, they function as compliance baselines and must be tailored to your specific jurisdictional regulations rather than replacing qualified tax counsel.

By incorporating concrete tools-such as structured asset disposal logs and cost-basis adjustment schedules-your department can establish an audit-ready trail. This article outlines the essential return document templates required for corporate capital gains tax compliance, detailing how to integrate them into your existing financial workflows.

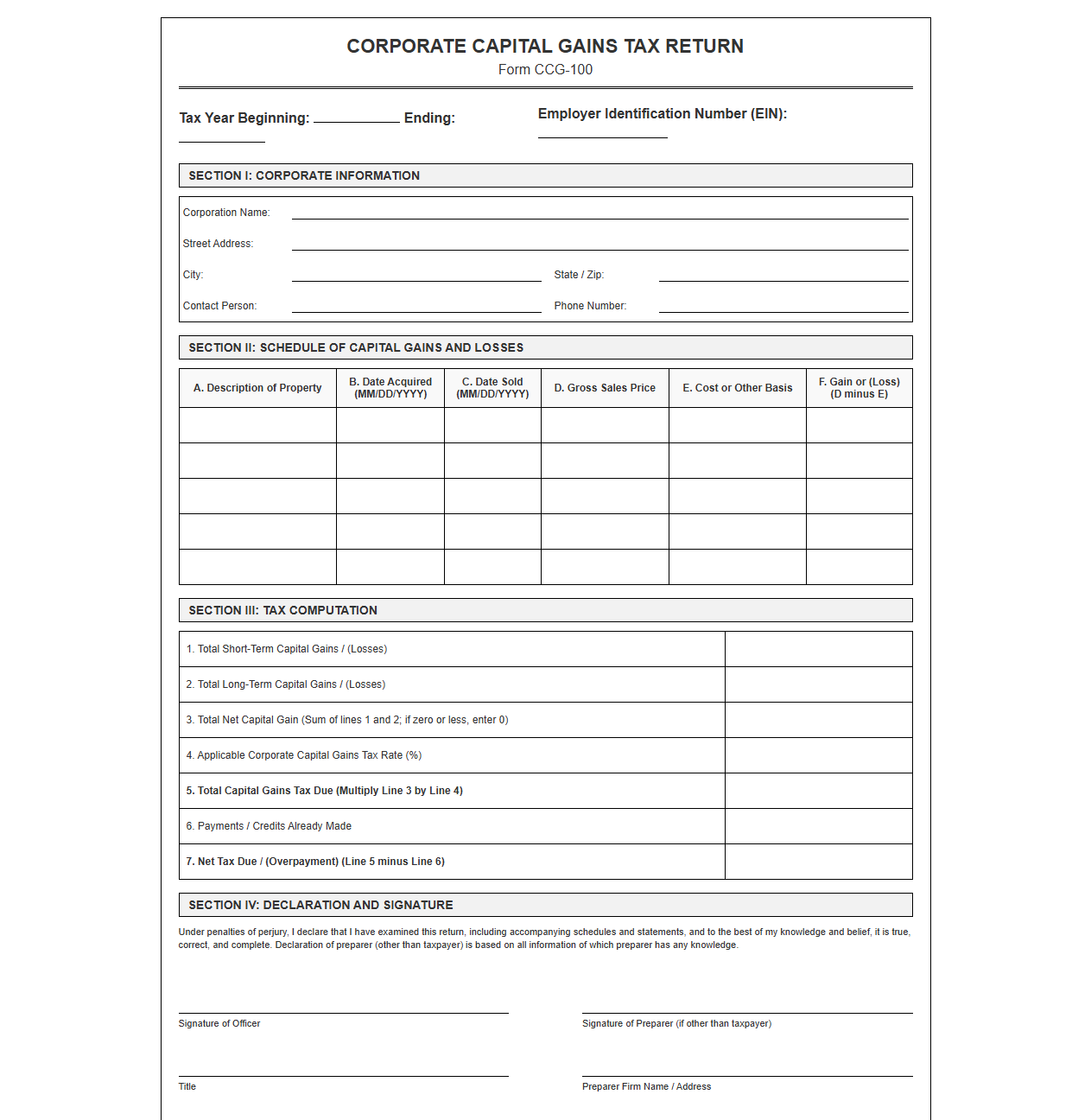

Corporate Capital Gains Tax Return Form

Download: .PDF

Download: .PDF

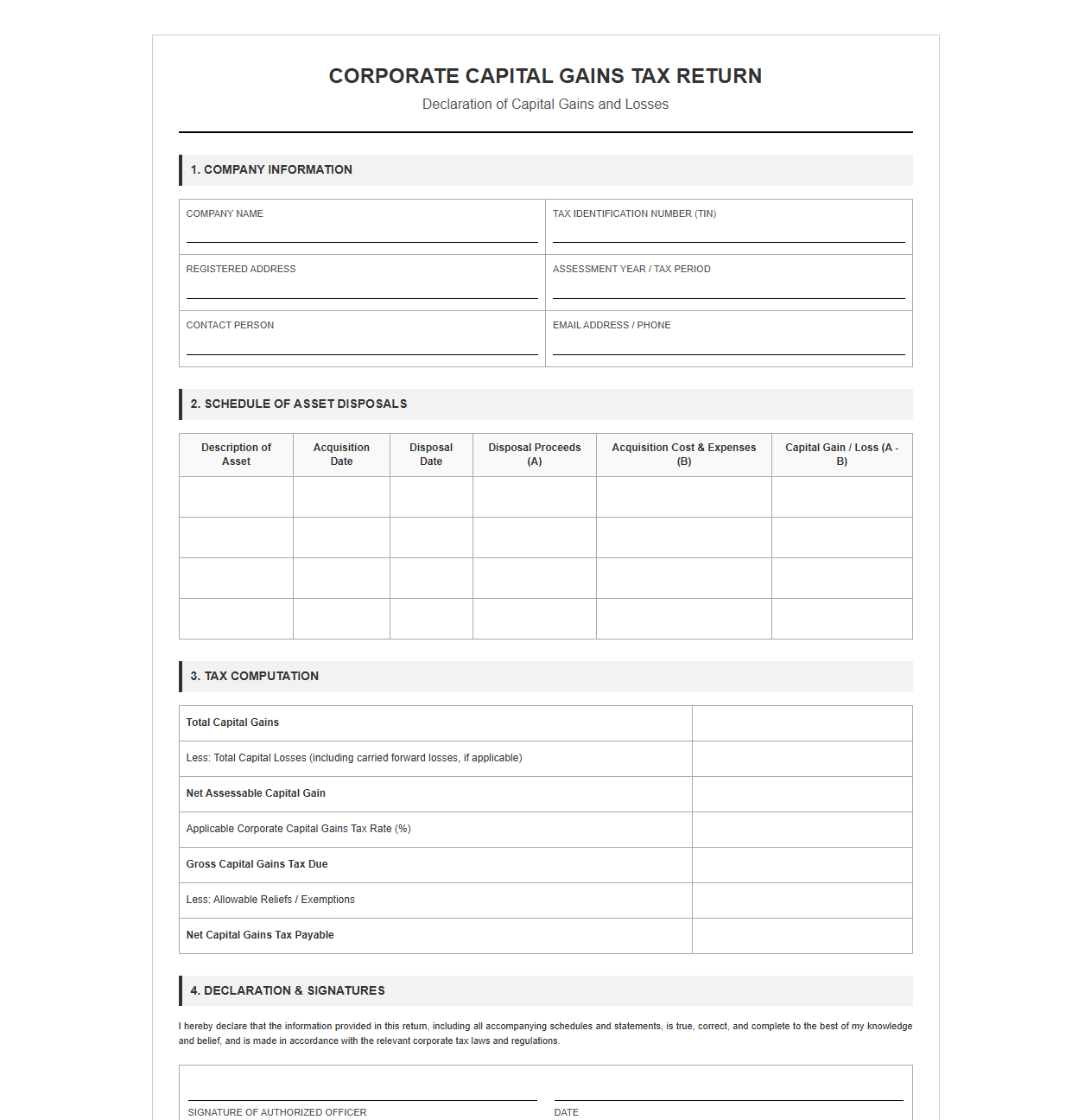

Company Capital Gains Tax Declaration Template

Download: .PDF

Download: .PDF

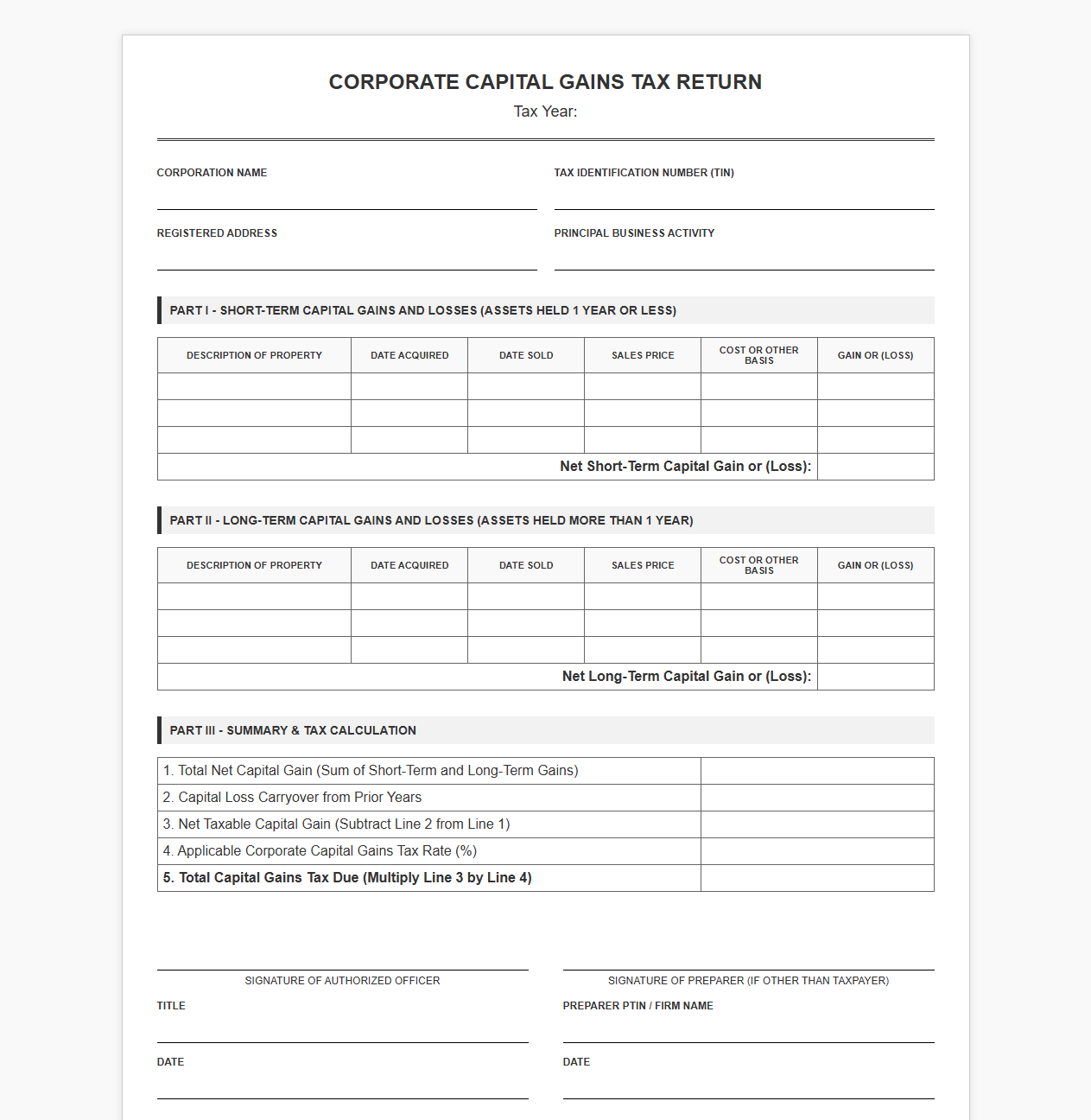

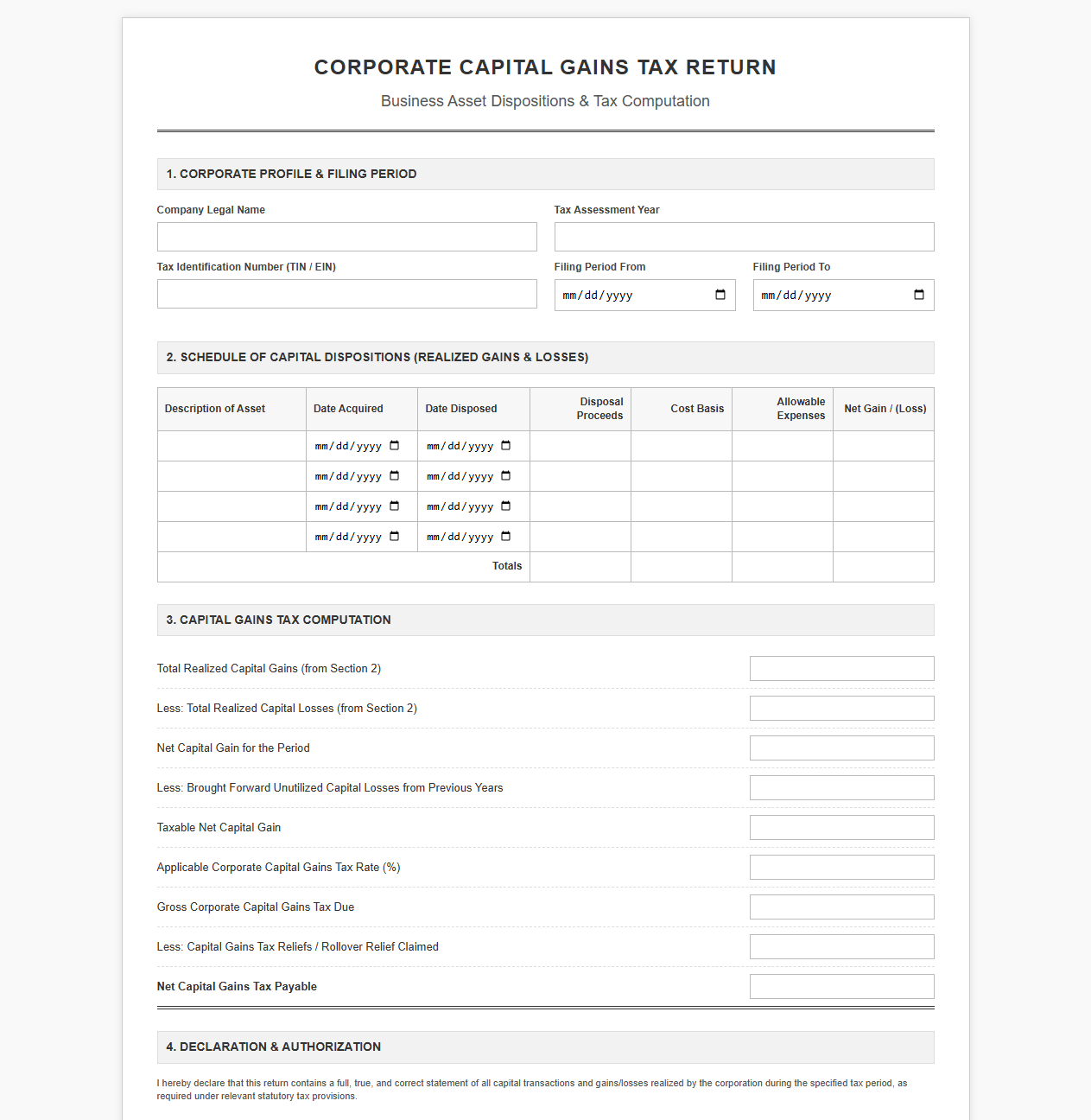

Corporate Capital Gains Tax Filing Template

Download: .PDF

Download: .PDF

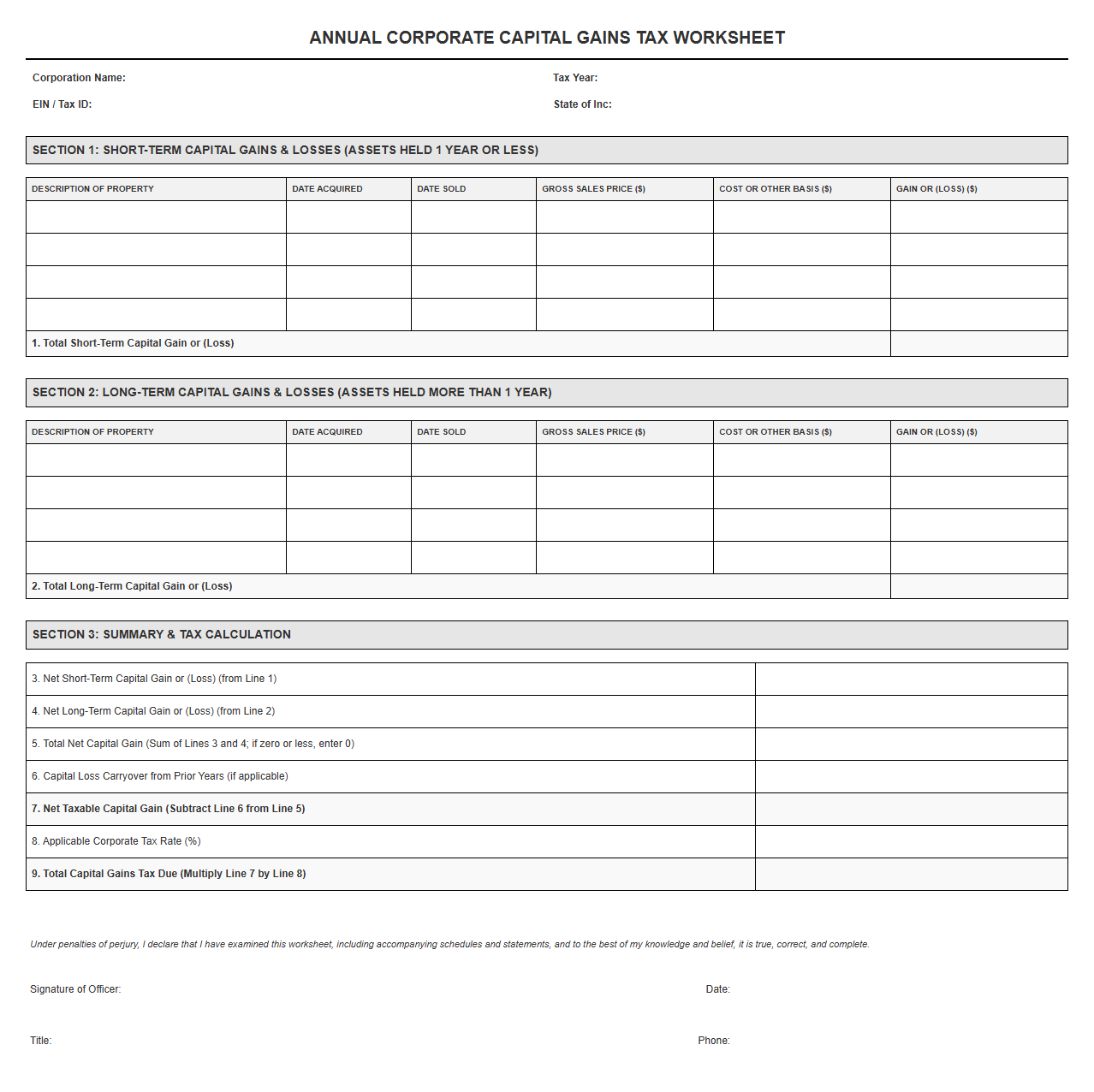

Annual Corporate Capital Gains Tax Worksheet

Download: .PDF

Download: .PDF

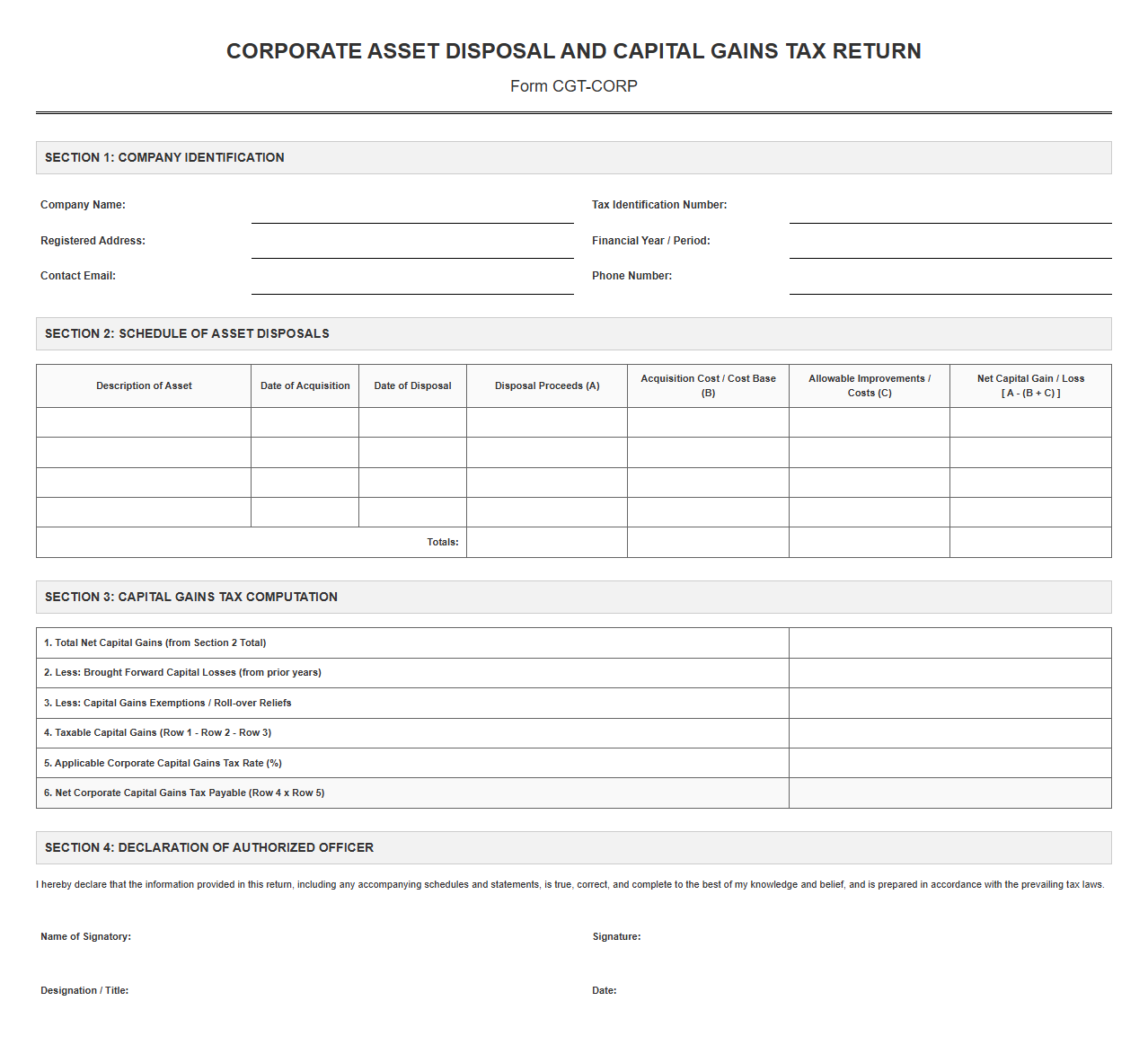

Corporate Asset Disposal and Capital Gains Tax Return

Download: .PDF

Download: .PDF

Business Capital Gains Tax Calculation and Return Template

Download: .PDF

Download: .PDF

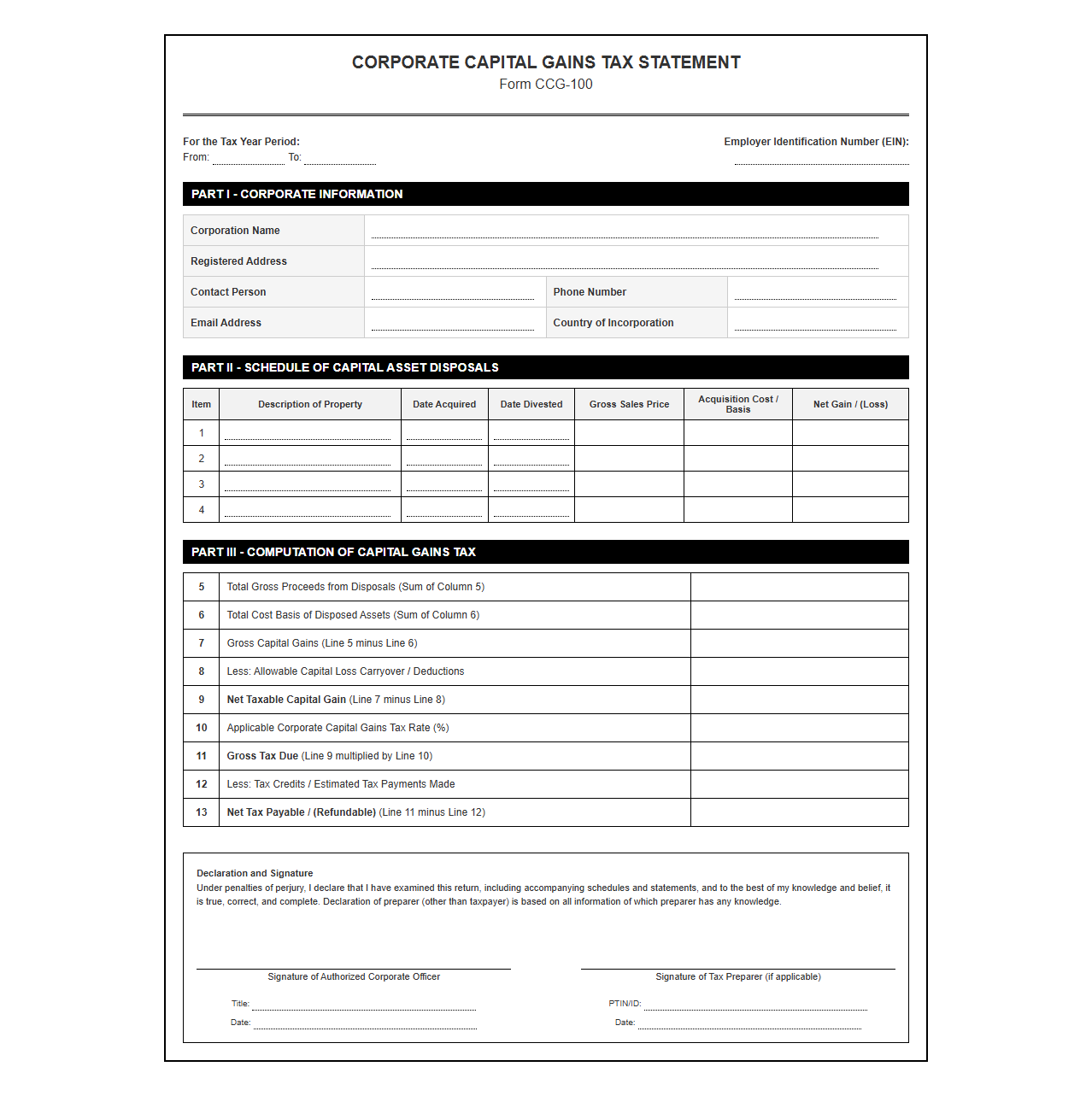

Corporate Capital Gains Tax Statement Form

Download: .PDF

Download: .PDF

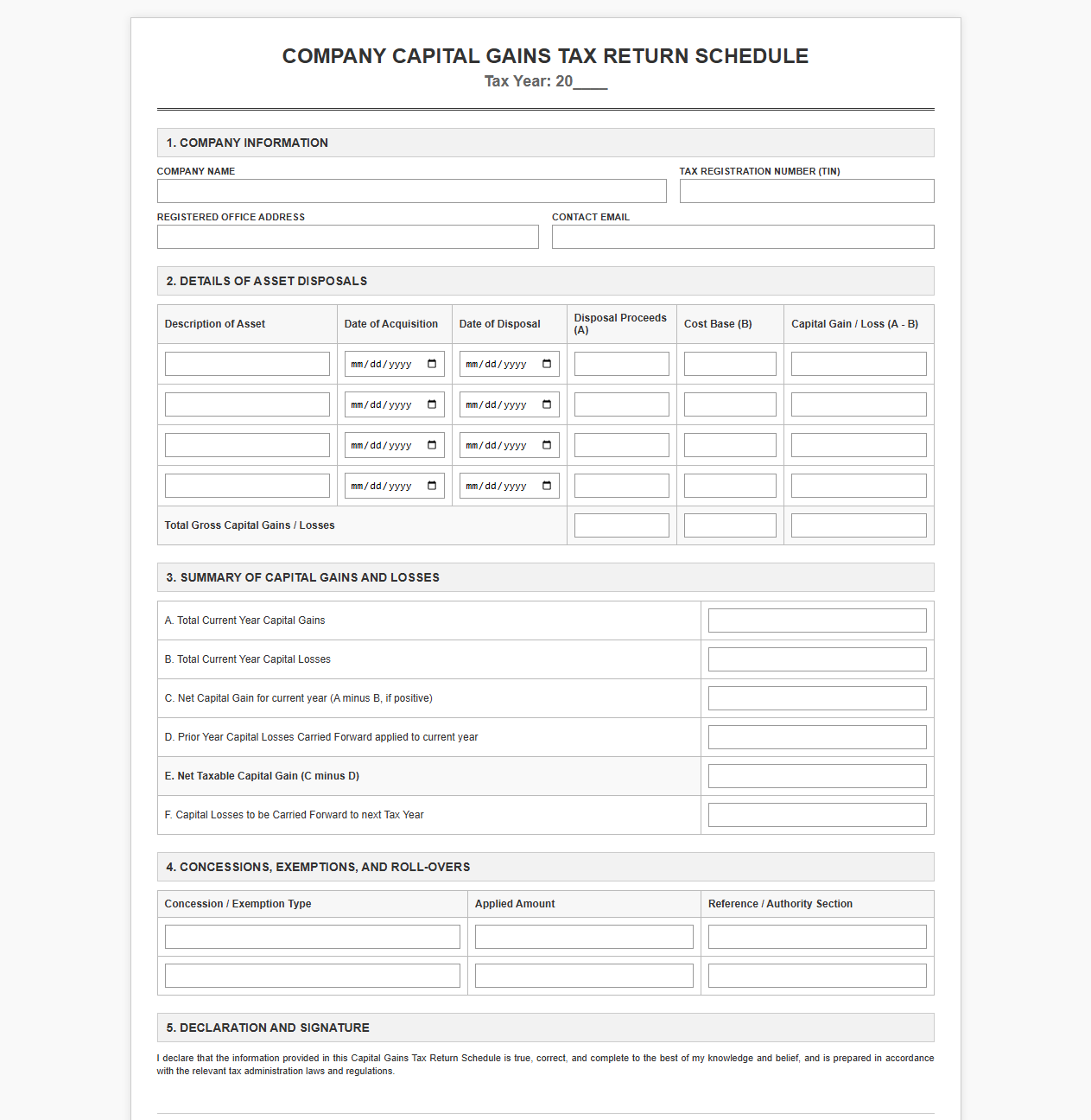

Company Capital Gains Tax Return Schedule

Download: .PDF

Download: .PDF

Section 1: Introduction to Corporate Capital Gains Tax Templates

In the landscape of corporate finance, maintaining tax compliance requires rigorous documentation and standardized reporting structures. Utilizing a structured template for corporate capital gains tax ensures systemic accuracy across all financial quarters. Without standardized tools, corporations risk inconsistencies that can trigger costly audits and financial restructurings.

A robust template framework establishes audit readiness by centralizing transaction records, cost basis adjustments, and tax calculations. By embedding regulatory guidelines directly into corporate tax workflows, organizations can mitigate the risks of underreporting or miscalculating taxable gains, protecting the enterprise from severe penalties.

Section 2: Standardizing the Schedule of Asset Dispositions

A critical component of capital gains reporting is the Schedule of Asset Dispositions. This template tracks every asset sold, exchanged, or retired during the tax year, capturing essential transaction data required by tax authorities.

| Asset Identifier | Description of Property | Acquisition Date | Disposition Date | Gross Sale Proceeds ($) |

|---|---|---|---|---|

| EQ-2023-01 | Corporate Office Server Hardware | 2021-03-15 | 2024-02-10 | 45,000.00 |

| RE-2018-09 | Commercial Warehouse Facility | 2018-06-30 | 2024-05-18 | 1,250,000.00 |

| VEH-2020-04 | Logistics Fleet Delivery Van | 2020-11-12 | 2024-08-01 | 18,500.00 |

Section 3: Cost Basis and Adjustment Calculations

Accurately determining the adjusted cost basis of an asset is vital to calculating the correct taxable capital gain or loss. This process requires systematic tracking of the initial investment and subsequent modifications over the asset's lifecycle. Follow this sequence to establish the adjusted cost basis:

- Identify the original purchase price and direct acquisition costs, such as legal fees, installation, and transfer taxes.

- Add capitalized improvements and capital expenditures that extend the useful life or add value to the asset.

- Subtract accumulated depreciation deductions, amortization, and any depreciation recapture amounts claimed in prior years.

- Add allowable transaction costs incurred during the sale or disposition, such as commissions, brokerage fees, and advertising.

Section 4: Capital Loss Offsets and Carryforward Logs

Corporate capital losses are subject to different rules than individual tax losses. Corporations cannot deduct net capital losses from ordinary income; instead, they must offset them strictly against capital gains. Tracking these offsets requires a dedicated ledger to manage carryback and carryforward schedules.

Under standard corporate tax regulations, net capital losses can be carried back three tax years to offset prior capital gains, and any remaining unused loss can be carried forward for up to five years. Detailed tracking is mandatory to prevent these tax attributes from expiring.

Section 5: Deferral Documentation for Like-Kind Exchanges

Under Section 1031 of the Internal Revenue Code, corporations can defer recognizing capital gains on real property held for productive use in a trade or business by exchanging it for like-kind property. Accurate template documentation is critical to proving compliance with strict statutory timelines and structures.

- Qualified Intermediary (QI) Details: Document the name, address, and escrow account information of the independent third party facilitating the exchange.

- 45-Day Identification Period: Log the exact date the relinquished property was transferred and verify the formal identification of replacement property within 45 calendar days.

- 180-Day Exchange Period: Track the final acquisition date of the replacement property to ensure it is completed before the 180-day regulatory deadline.

- Boot Analysis: Calculate any cash, debt relief, or non-like-kind property received during the exchange, which represents taxable recognized gain.

Section 6: Corporate Reorganizations and Non-Recognition Transactions

Corporate mergers, acquisitions, and restructurings often qualify as tax-free reorganizations under Section 368. These non-recognition transactions allow companies to defer capital gains tax on transferred assets or stock. Tax departments must maintain exhaustive documentation to justify the tax-free status of these transactions to regulatory bodies.

Section 7: Final Reconciliation and Filing Checklist

Before submitting corporate tax returns electronically, tax departments must perform a final reconciliation to ensure all data points align between internal spreadsheets and the actual filing documents. Use the following interactive checklist to verify compliance completeness:

Leave a comment