Corporate tax departments routinely struggle with the fragmented, high-stakes nature of multi-jurisdictional filings, where minor errors in calculating gross receipts trigger severe compliance penalties. Before adopting automated solutions, tax leadership must first navigate a rapidly shifting state-level regulatory landscape where gross receipts levies are increasingly favored for stable revenue generation.

Transitioning to standardized return templates grants corporate tax teams immediate operational relief, drastically reducing filing cycle times and reinforcing audit readiness. However, a key stipulation remains: these templates must be treated as architectural frameworks rather than rigid, one-size-fits-all forms, as they require baseline customization to reflect local tax codes.

For example, accommodating the distinct exclusion rules of the Ohio Commercial Activity Tax (CAT) requires a different data-mapping strategy than managing the margin deductions of the Texas Franchise Tax. Below, we examine how to build these standardized frameworks, integrate state-specific variables, and streamline your end-to-end compliance workflow.

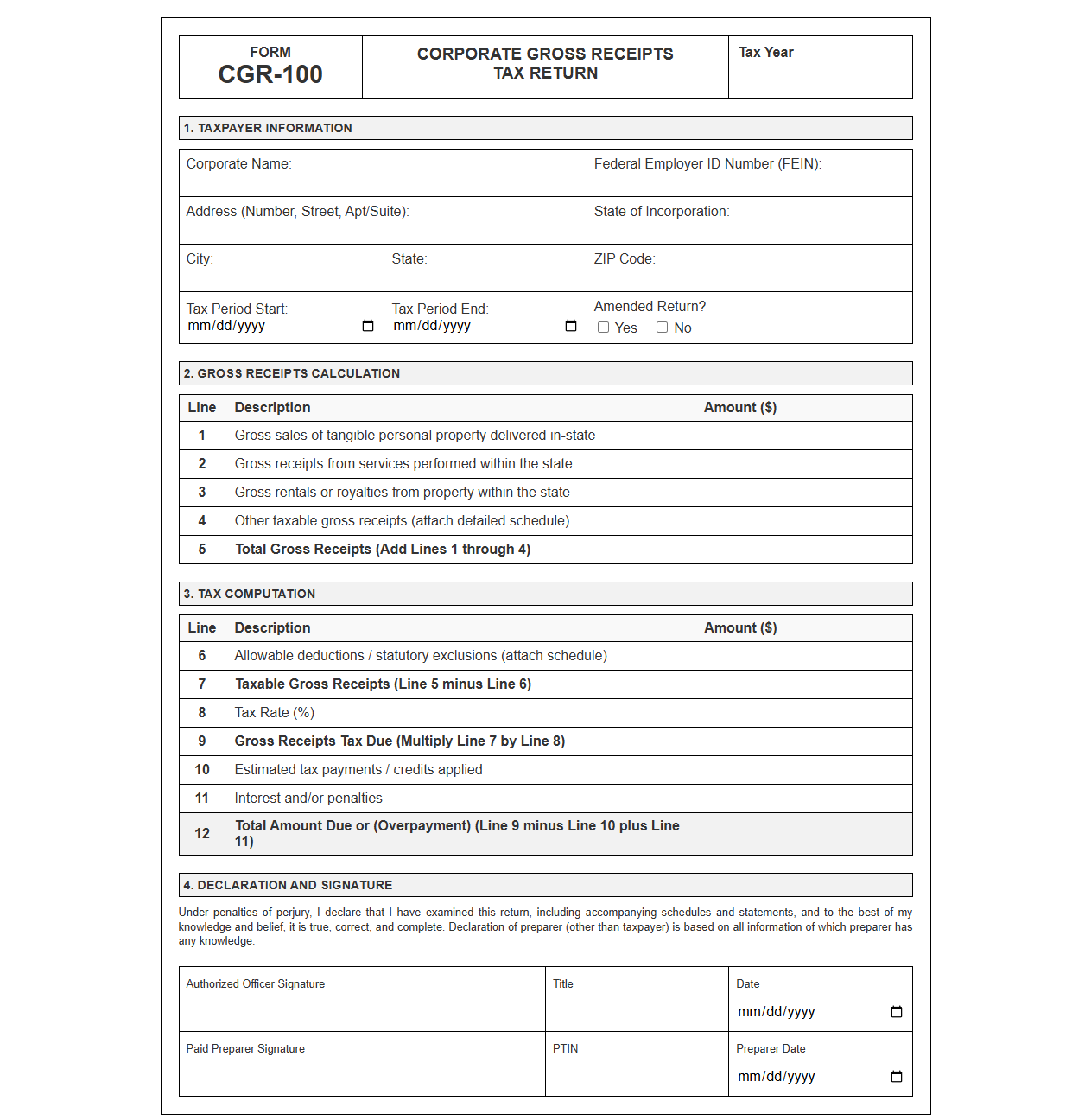

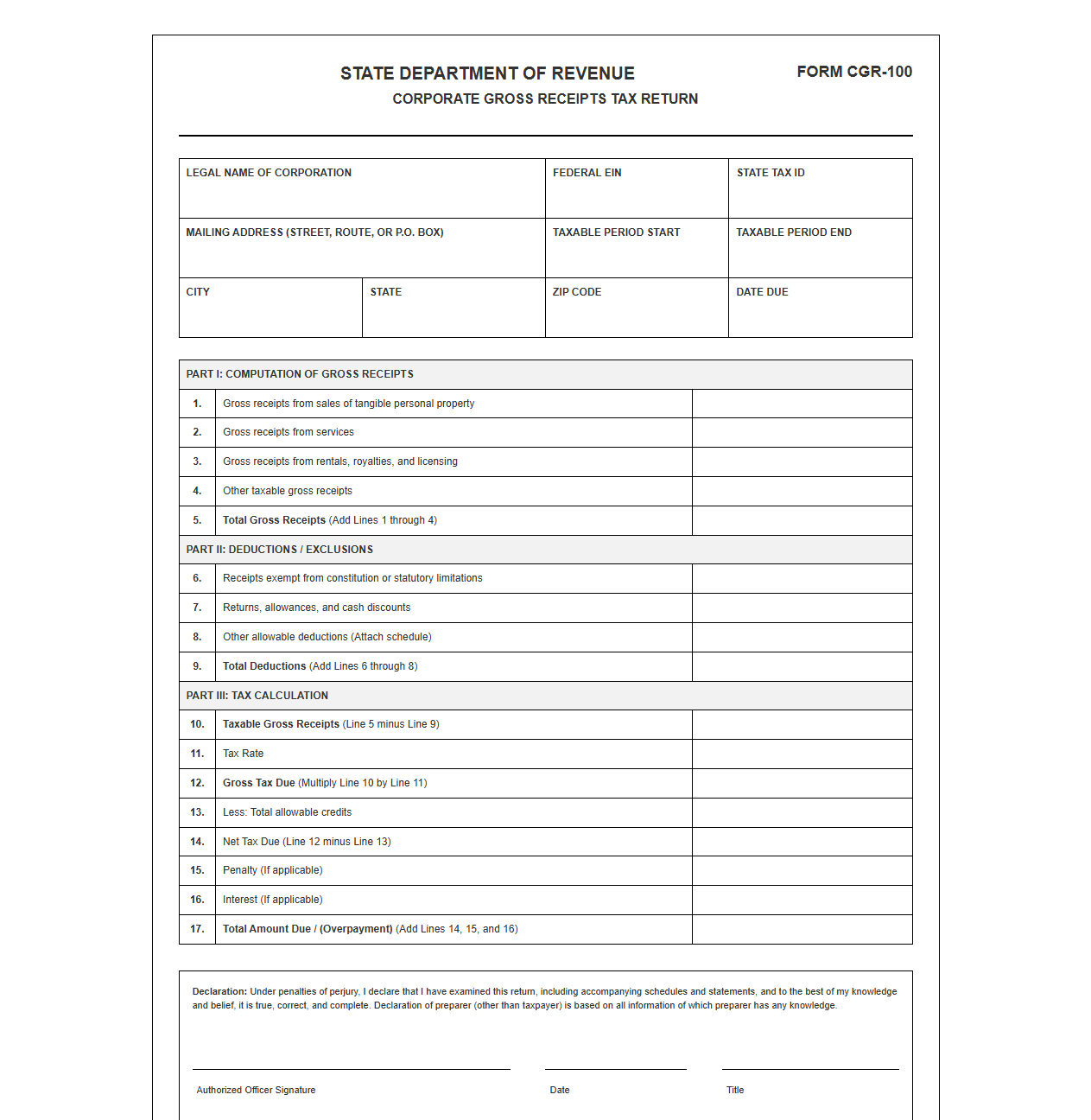

Corporate Gross Receipts Tax Return Form

Download: .PDF

Download: .PDF

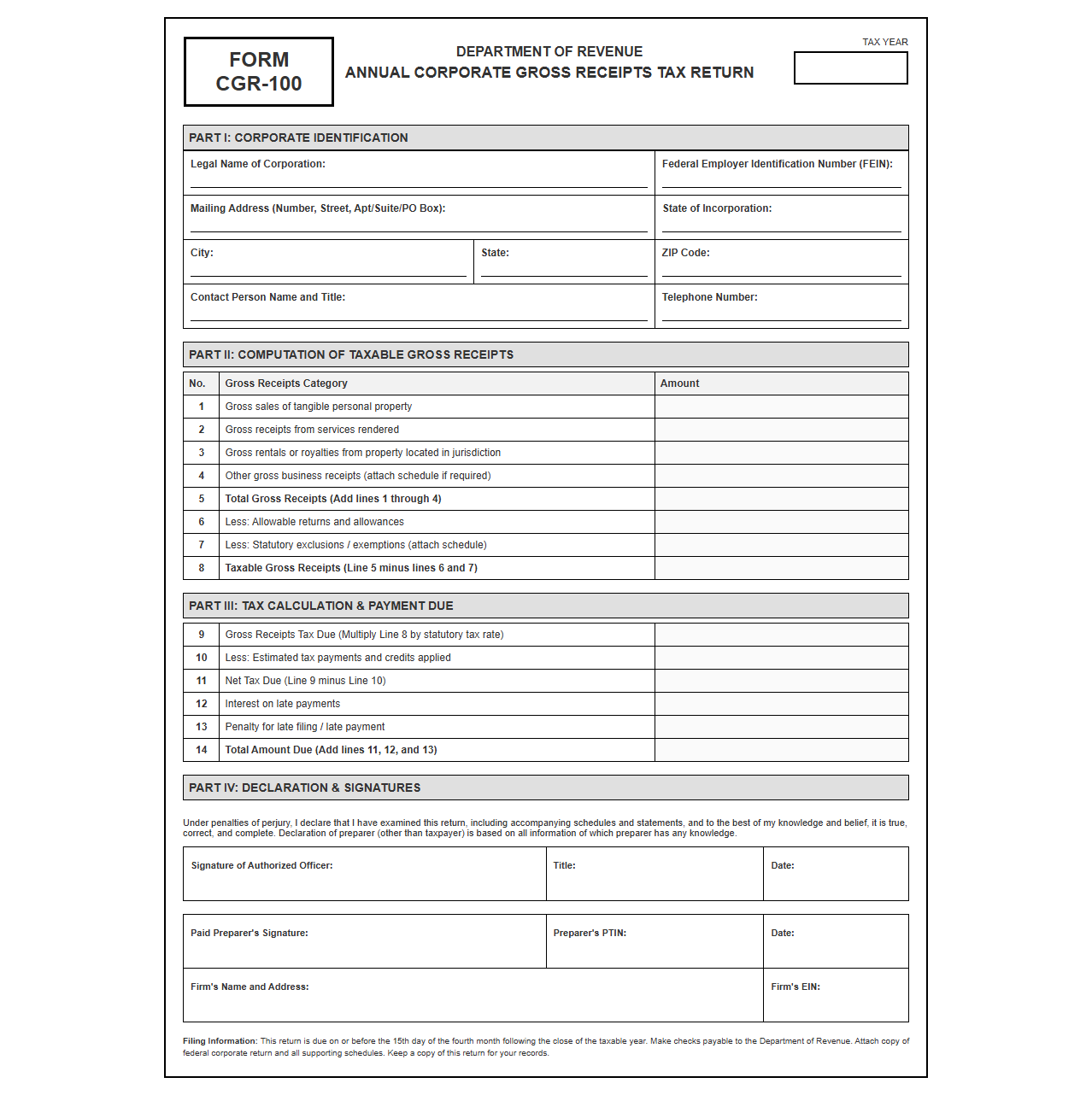

Annual Corporate Gross Receipts Tax Filing Template

Download: .PDF

Download: .PDF

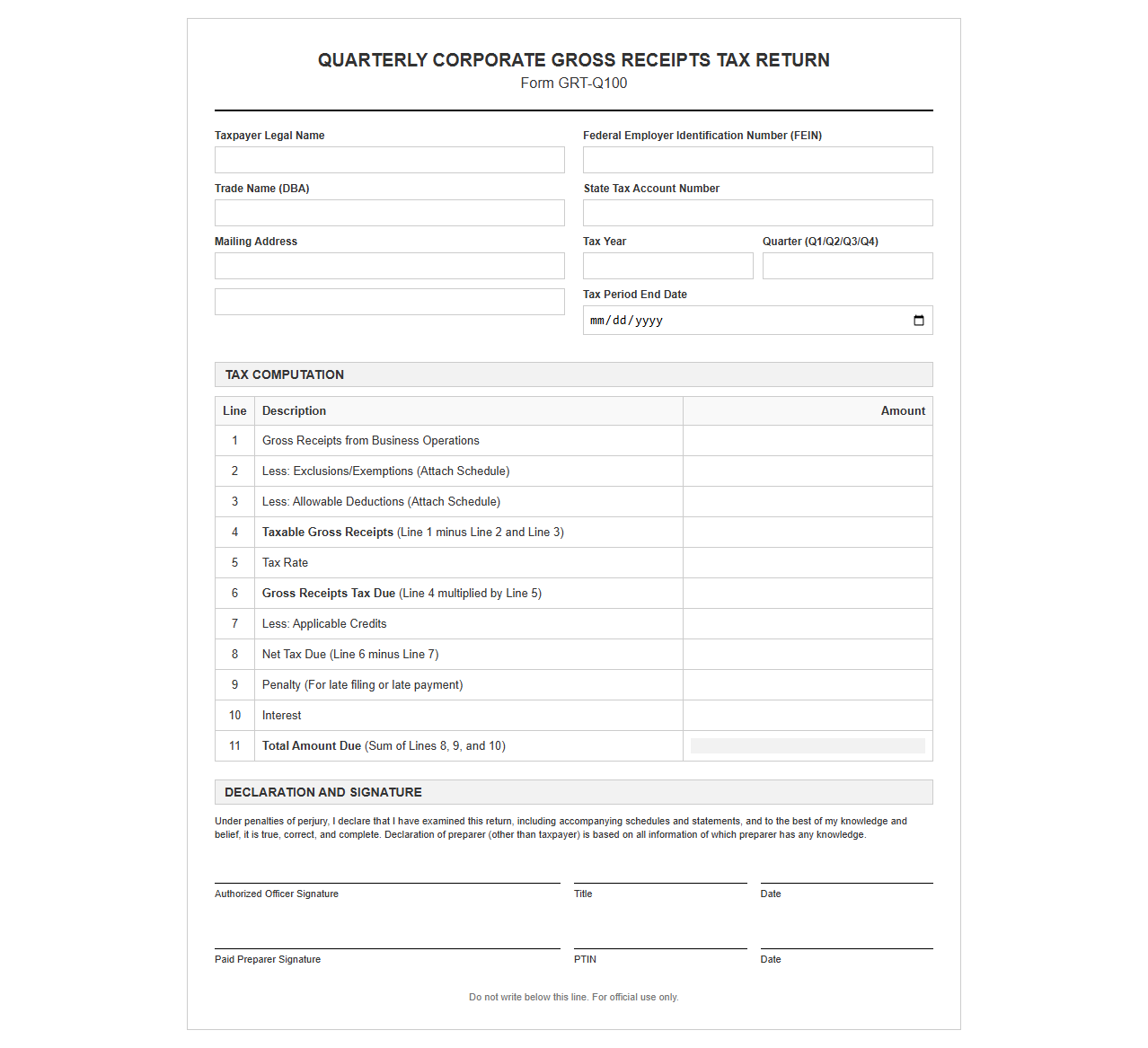

Quarterly Corporate Gross Receipts Tax Return Template

Download: .PDF

Download: .PDF

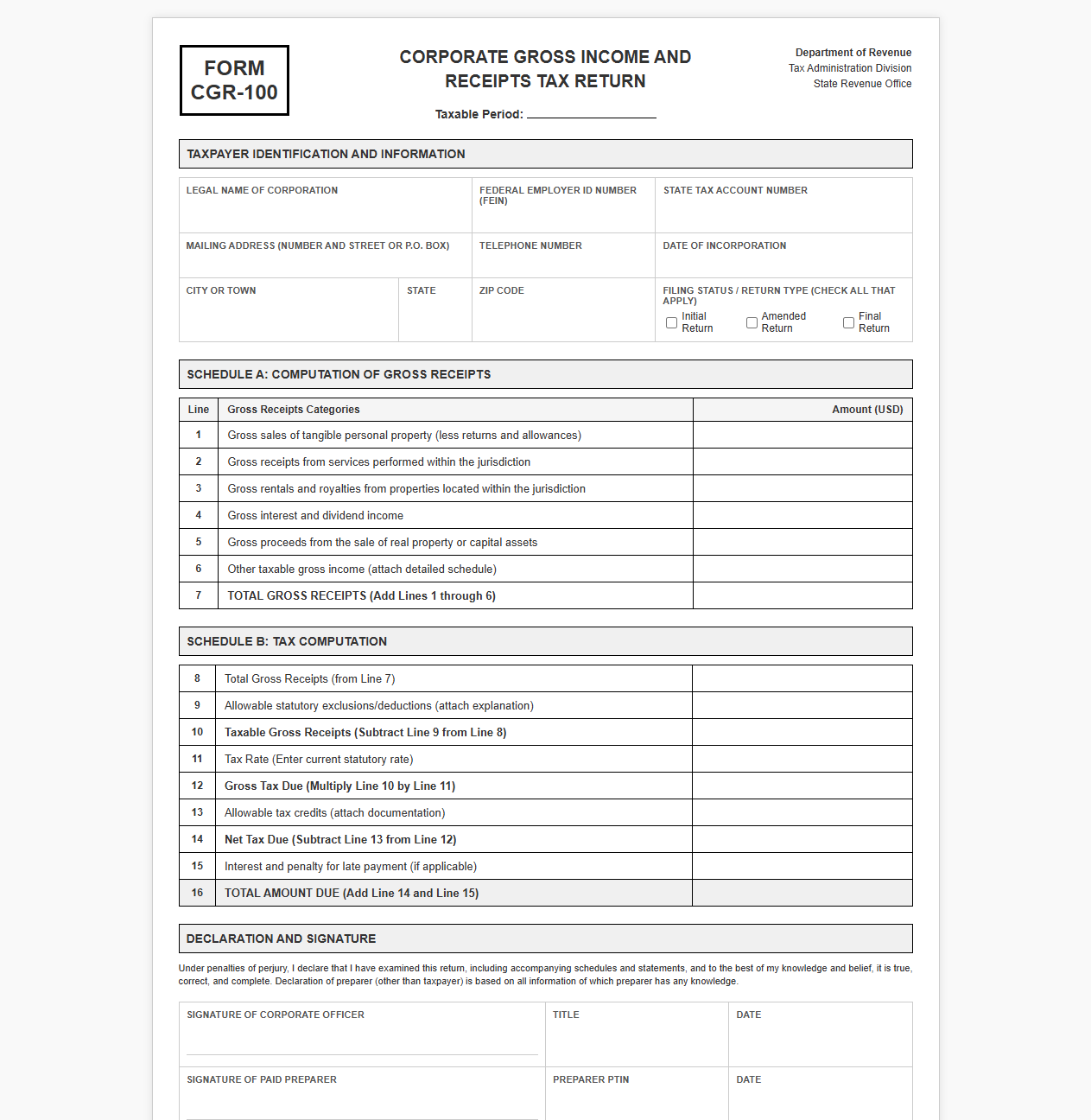

Corporate Gross Income and Receipts Tax Form

Download: .PDF

Download: .PDF

State Corporate Gross Receipts Tax Declaration Template

Download: .PDF

Download: .PDF

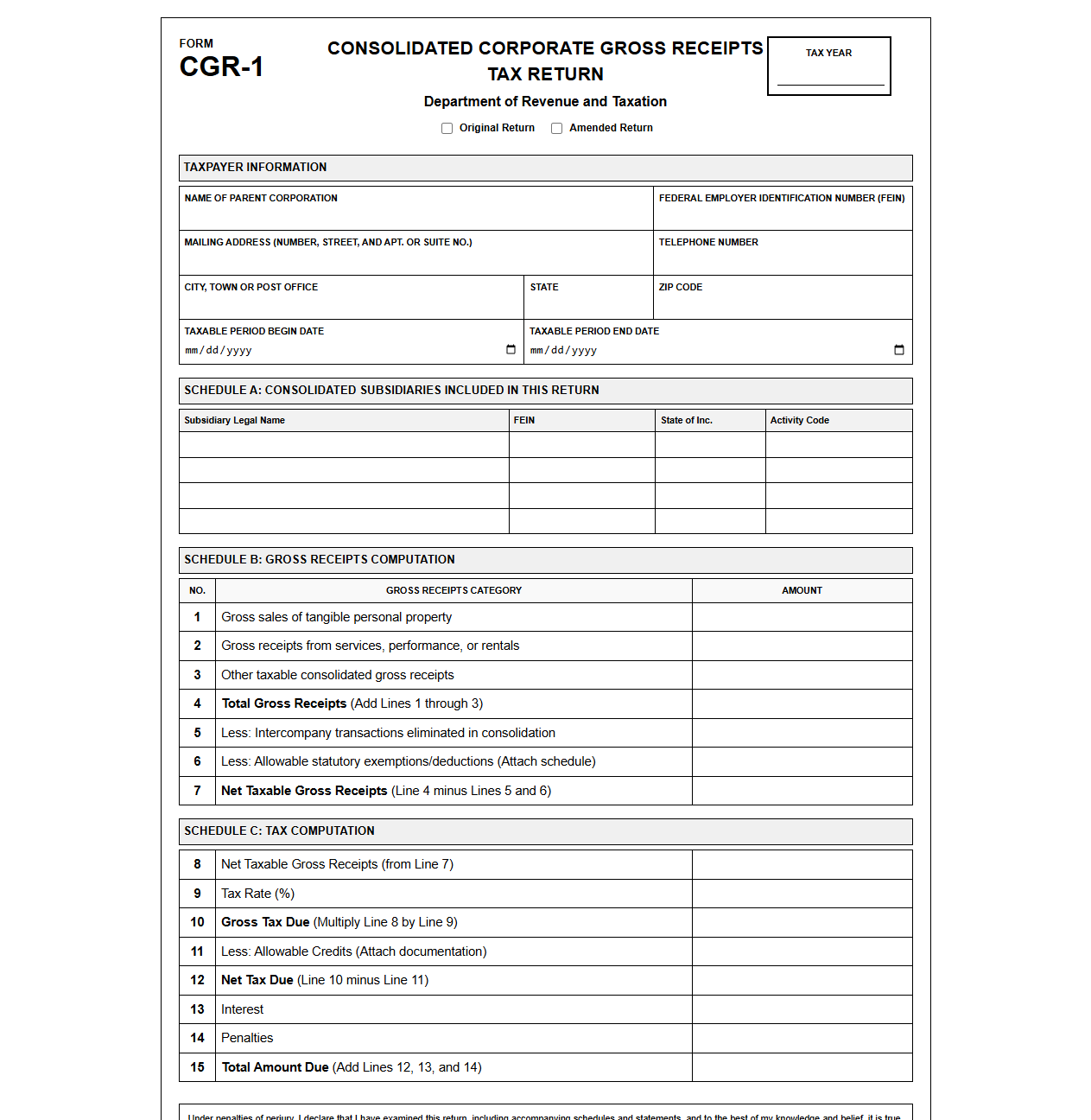

Consolidated Corporate Gross Receipts Tax Return

Download: .PDF

Download: .PDF

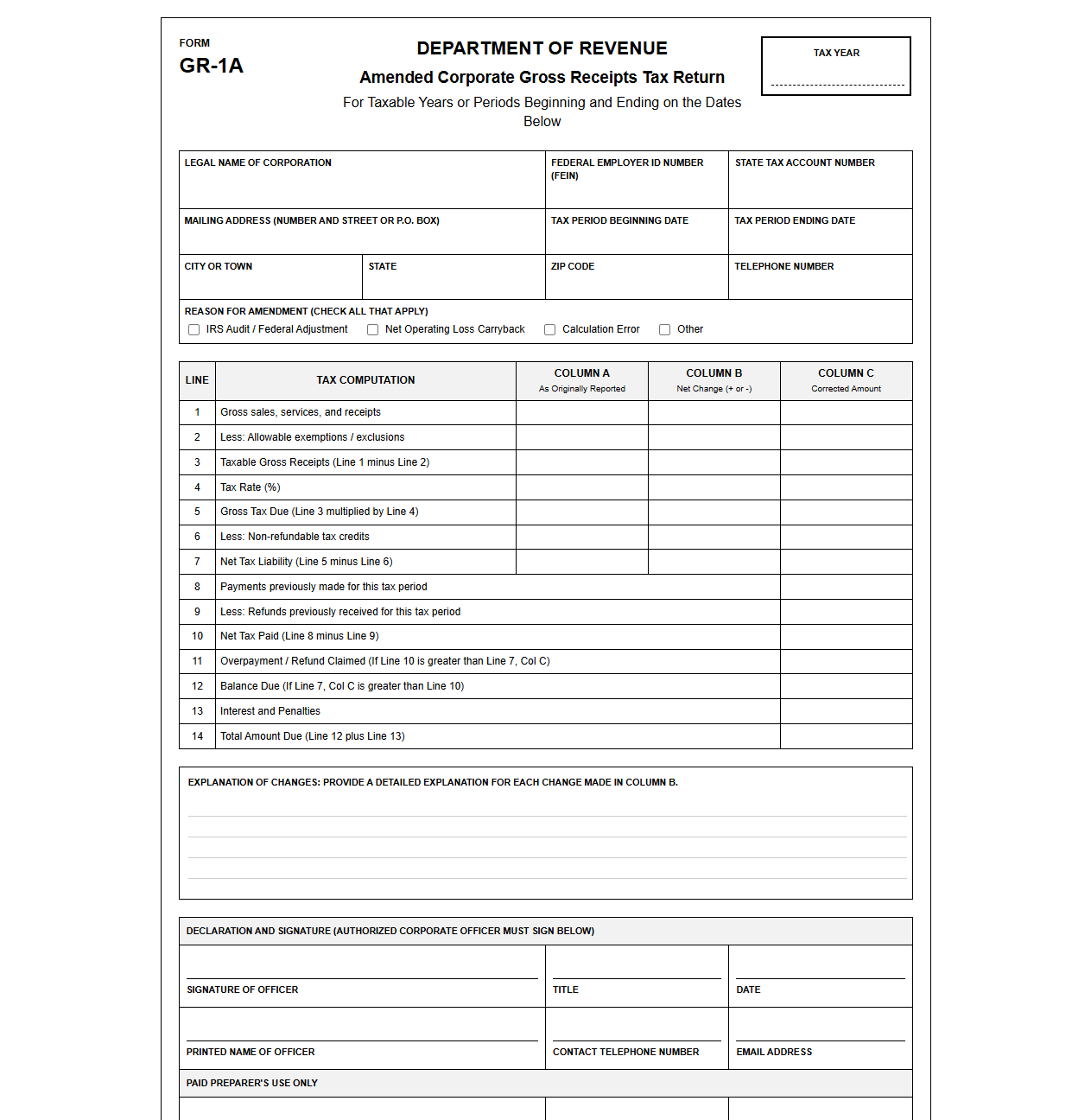

Amended Corporate Gross Receipts Tax Return Template

Download: .PDF

Download: .PDF

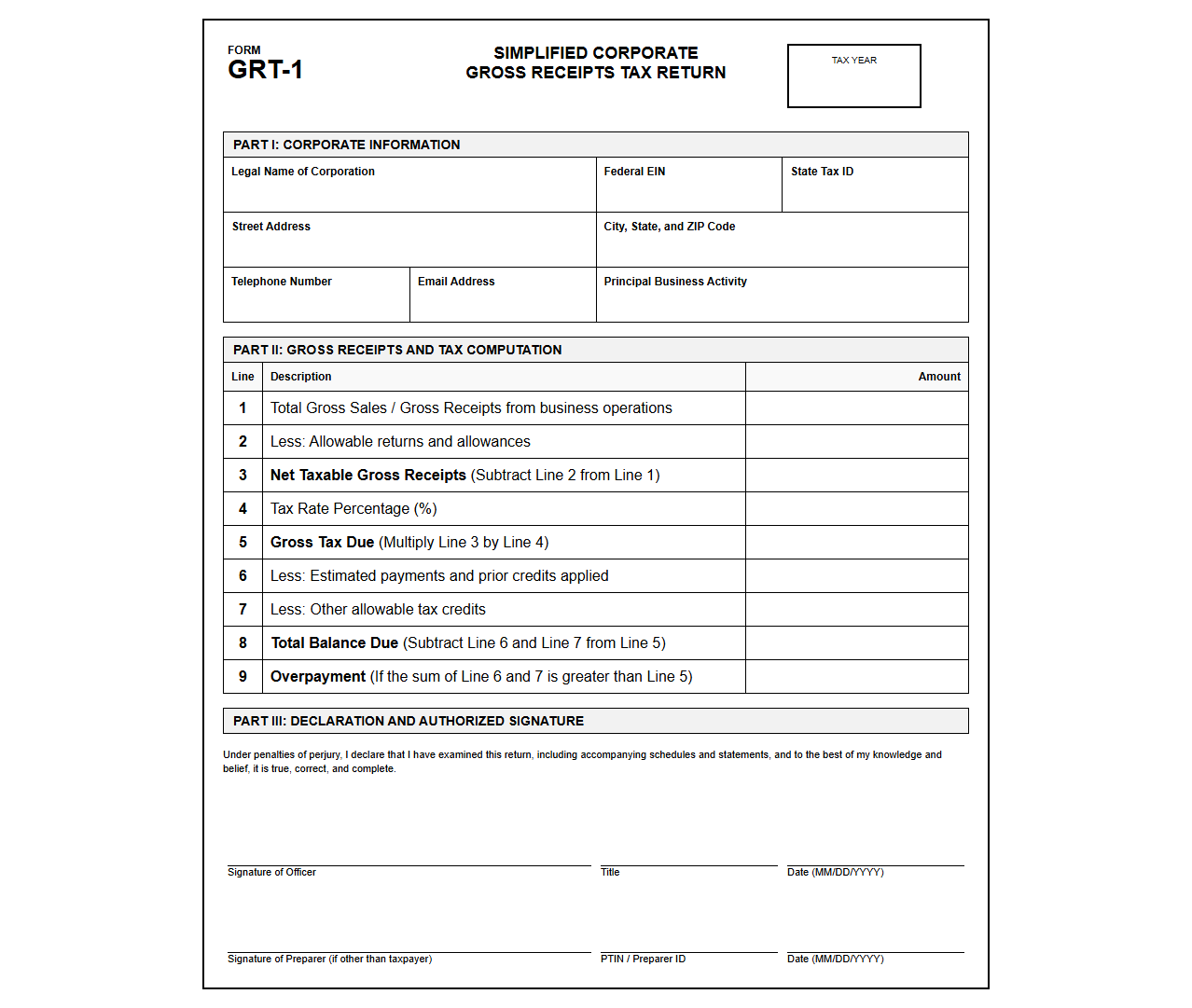

Simplified Corporate Gross Receipts Tax Return Form

Download: .PDF

Download: .PDF

Navigating the Complexity of Corporate Gross Receipts Tax

Managing corporate tax liabilities is an increasingly intricate endeavor for modern enterprises. A major contributor to this complexity is the corporate gross receipts tax (GRT), a tax levied on a company's total gross sales or receipts without deductions for the cost of goods sold or operating expenses.

This differs fundamentally from traditional net income taxes, which only levy taxes on profits after allowable deductions. Because GRT is assessed on top-line revenue, even unprofitable companies can face substantial tax liabilities. To mitigate these administrative hurdles, forward-thinking organizations are adopting standardized templates as a unified solution to streamline modern corporate compliance.

The High Cost of Fragmented Filing Systems

Filing corporate taxes across multiple states and local municipalities often leads to operational inefficiencies. Without a centralized reporting framework, tax departments must navigate a chaotic landscape of disjointed local rules and varying filing formats.

- Manual data entry errors: Manually copying financial data into mismatched state portals often introduces costly administrative mistakes.

- Increased audit vulnerability: Inconsistent calculations across state lines raise red flags for aggressive state tax auditors.

- Missed filing deadlines: Managing unique calendars for dozens of jurisdictions stretches treasury resources thin.

Anatomy of a Standardized Gross Receipts Tax Template

A standardized GRT return template acts as a universal bridge across disparate tax jurisdictions. By establishing a common structural layout, the template standardizes how financial data is compiled and normalized before submission.

The core design groups jurisdictional specifics into modular columns while maintaining a single cohesive framework for gross revenue inputs. This structure allows enterprises to capture total national revenue once and systematically apply localized rules without rebuilding the underlying spreadsheet for every municipal filing.

Essential Data Fields for Streamlined Reporting

To ensure precise reporting across multiple jurisdictions, a standardized GRT template must organize financial information into logical, sequential sections. The following key data fields form the core of an effective reporting template:

- Gross Receipts Categorization: Segmenting total revenue by business activity or product line to match diverse state tax rates.

- Statutory Exemptions: Identifying specific revenue types legally excluded from the local tax base by local statutes.

- Non-Taxable Receipts: Isolating items such as returned merchandise, cash discounts, and intercompany transfers.

- Apportioned Totals: Calculating the exact percentage of corporate economic activity attributable to each taxing jurisdiction.

Transforming Compliance into a Strategic Advantage

Adopting standardized templates shifts the tax department from a reactive cost center to a proactive strategic unit. Standardization drastically reduces the time spent on administrative grunt work, allowing tax professionals to focus on high-value planning and treasury optimization.

"Standardization of tax workflows reduces compliance risks, lowers audit defense costs, and yields unmatched visibility into corporate cash flows." - Corporate Treasury Journal

Step-by-Step Integration with Existing ERP Systems

To maximize the efficiency of your standardized GRT template, financial and IT teams must establish automated connections to the core system of record. Connecting template fields to transaction ledgers minimizes human intervention and ensures data integrity.

- Identify the target revenue ledgers within your ERP software, ensuring all transactional data is tagged with appropriate jurisdictional metadata.

- Map database tables like

GL_BALANCESandAR_TRANSACTIONSdirectly to the input fields of the standardized template. - Create automated staging queries that pull monthly top-line sales figures directly into the template's staging sheet.

- Execute regular verification audits to ensure the mapped ledger totals reconcile perfectly with the consolidated tax template.

The Future of Tax Technology and Automated Reporting

As tax jurisdictions move toward electronic governance, reliance on static documents will fade. The deployment of standardized templates represents the critical first step toward fully automated tax ecosystems. These structured formats prepare corporate financial data for seamless ingestion by real-time reporting APIs and advanced compliance software.

By organizing data into a predictable framework, corporations enable machine learning algorithms to flag audit risks and identify tax savings before filing. Embracing these structured templates today positions tax departments to thrive in a digital-first regulatory environment tomorrow.

Leave a comment