Corporate tax departments constantly struggle with the complex, labor-intensive process of net worth tax compliance, often losing valuable hours to manual data extraction and disjointed filing procedures. As jurisdictions tighten reporting standards and update valuation methodologies annually, tax professionals must establish a reliable framework to bridge the gap between raw financial data and complex regulatory filings.

Standardizing this workflow not only mitigates costly audit risks but also reclaims critical administrative time for strategic planning. Please note that while the return templates discussed herein provide a robust structural foundation, they must be tailored to align with your specific local tax statutes. Incorporating targeted tools, such as dynamic asset valuation worksheets and equity reconciliation trackers, ensures mathematical precision from the outset.

This article outlines the essential templates required for corporate filings, practical deployment strategies, and best practices for seamless integration into your existing compliance workflow.

Corporate Net Worth Tax Return Form

Download: .PDF

Download: .PDF

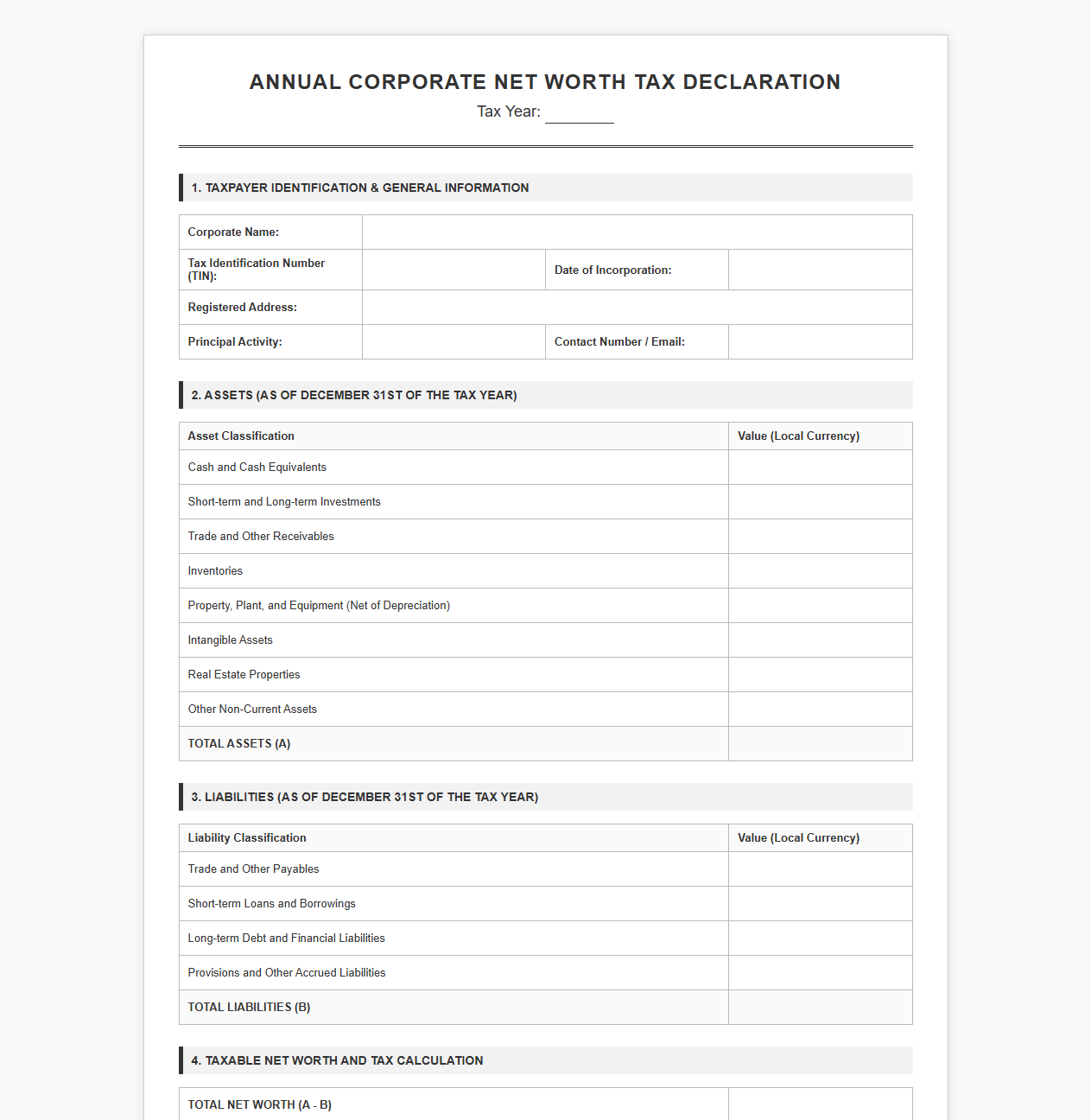

Annual Corporate Net Worth Tax Declaration Template

Download: .PDF

Download: .PDF

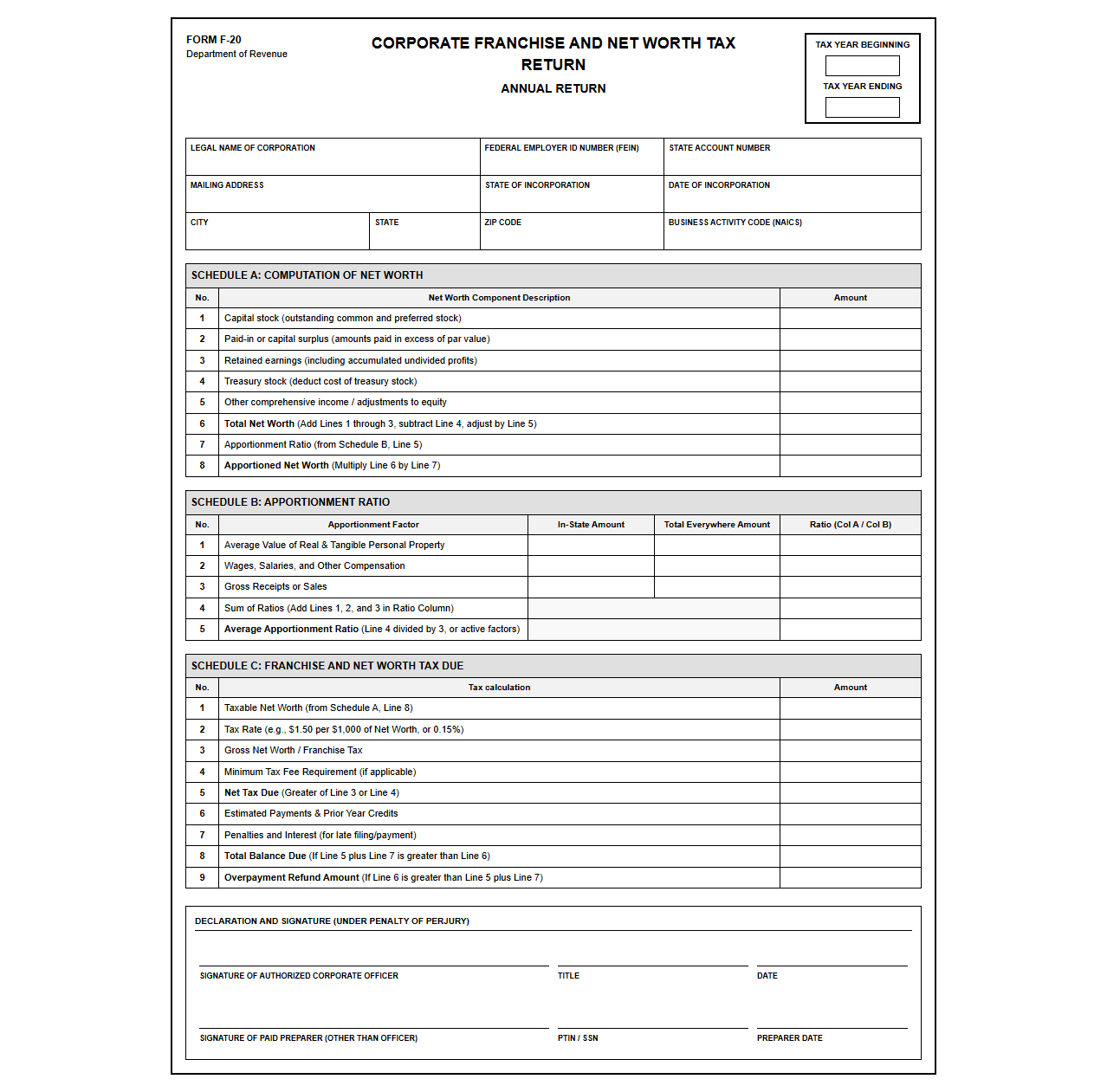

Corporate Franchise and Net Worth Tax Return

Download: .PDF

Download: .PDF

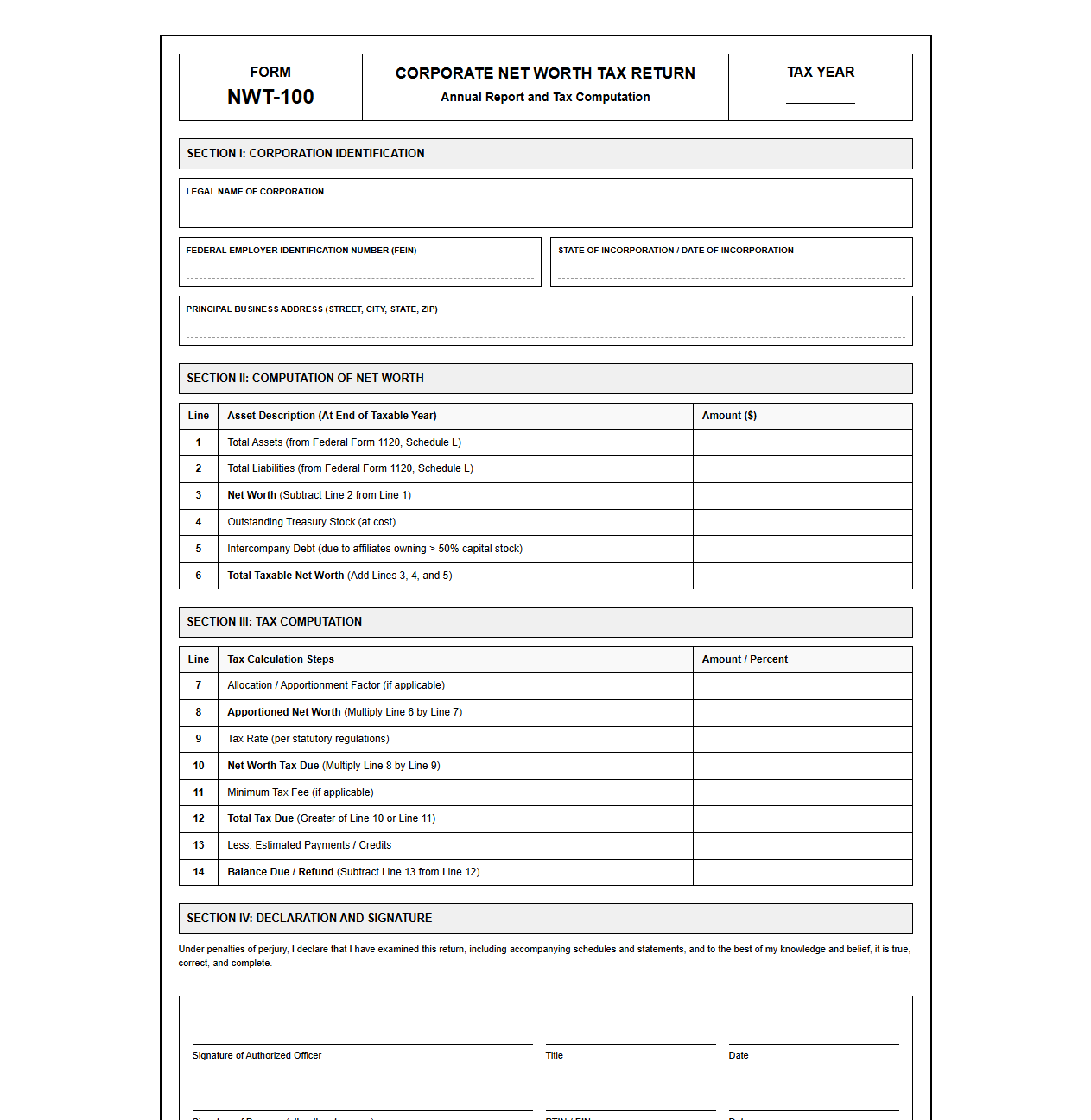

Business Net Worth Tax Reporting Template

Download: .PDF

Download: .PDF

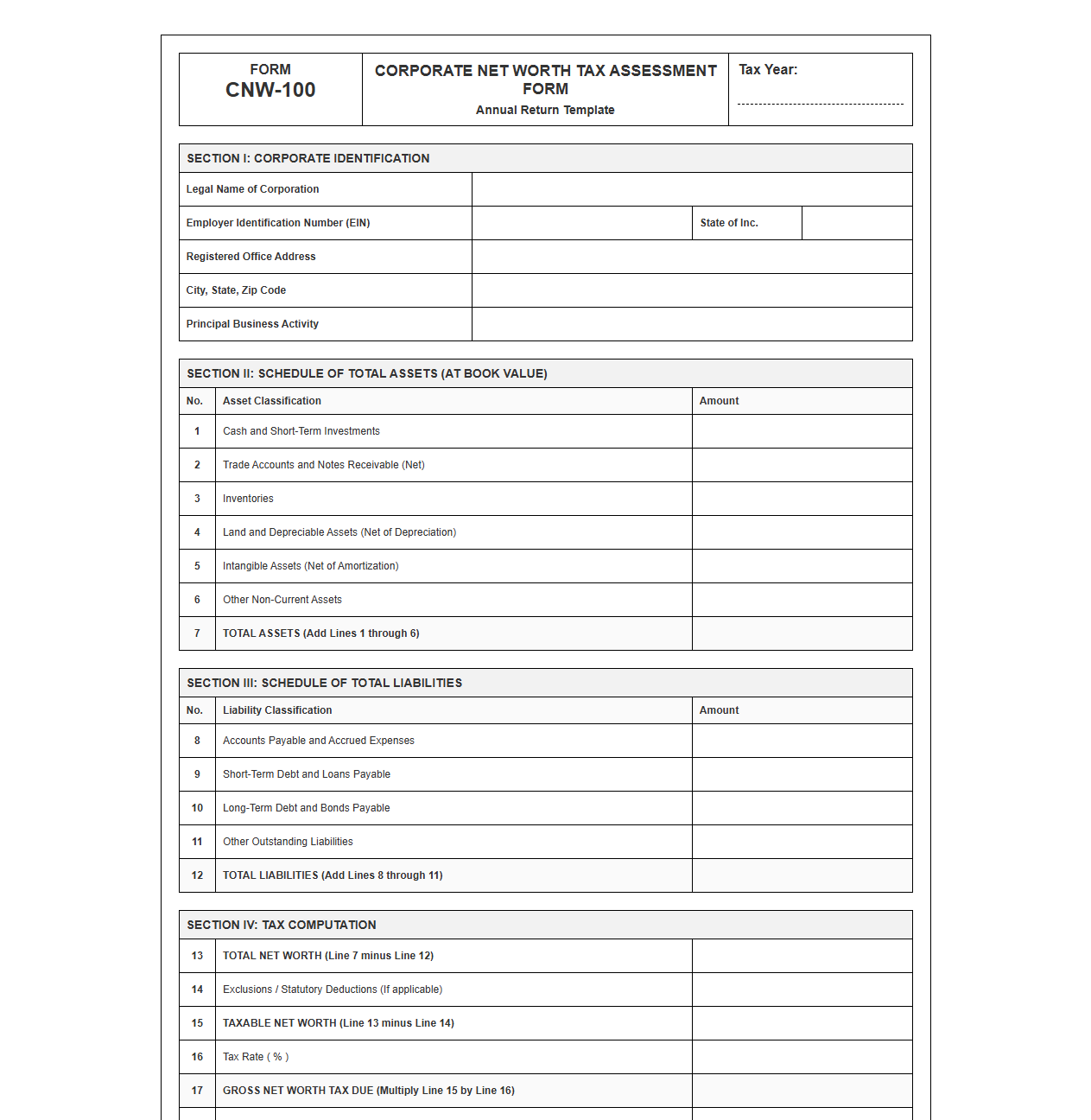

Corporate Net Worth Tax Assessment Form

Download: .PDF

Download: .PDF

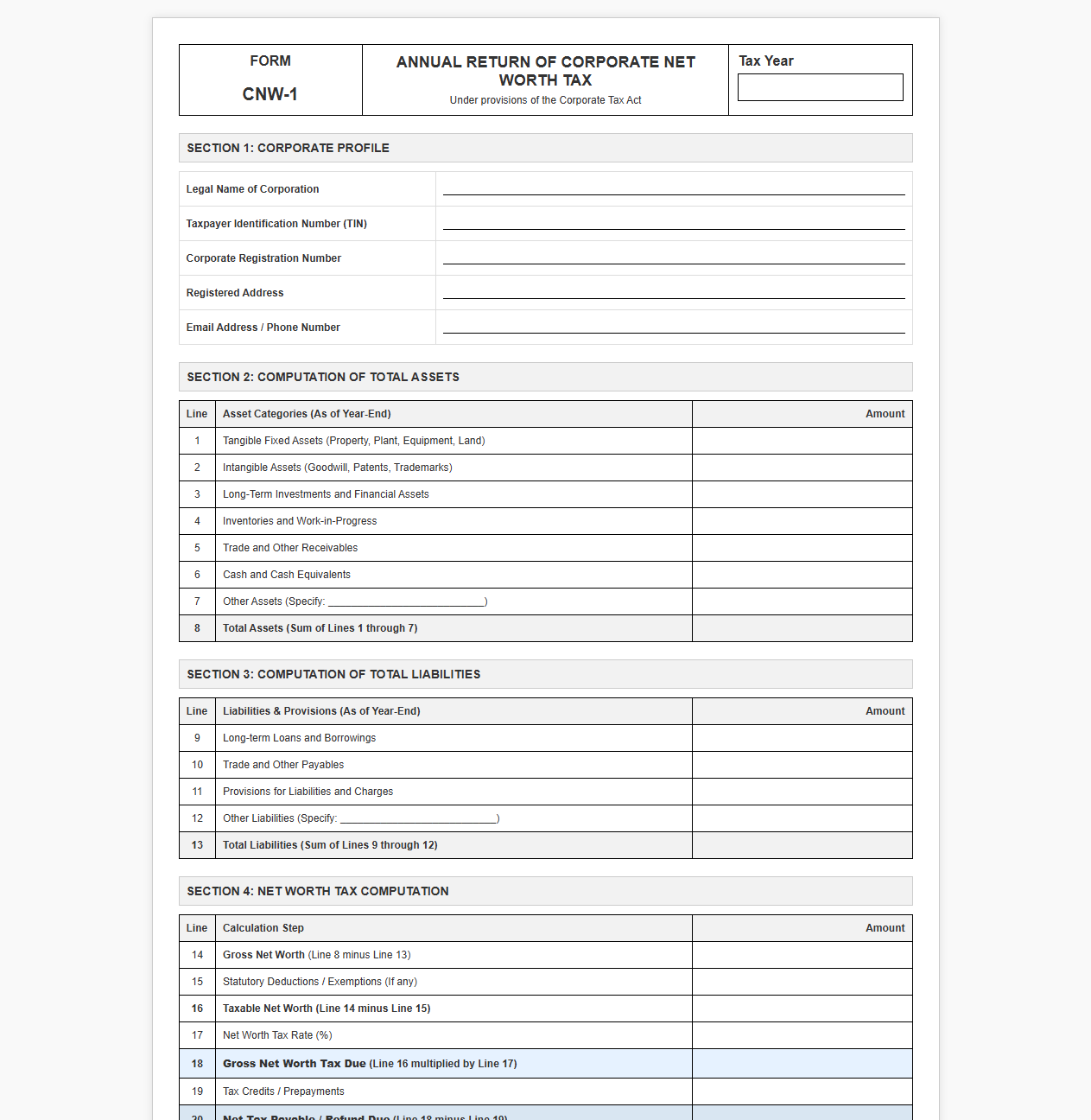

Annual Return of Corporate Net Worth Tax

Download: .PDF

Download: .PDF

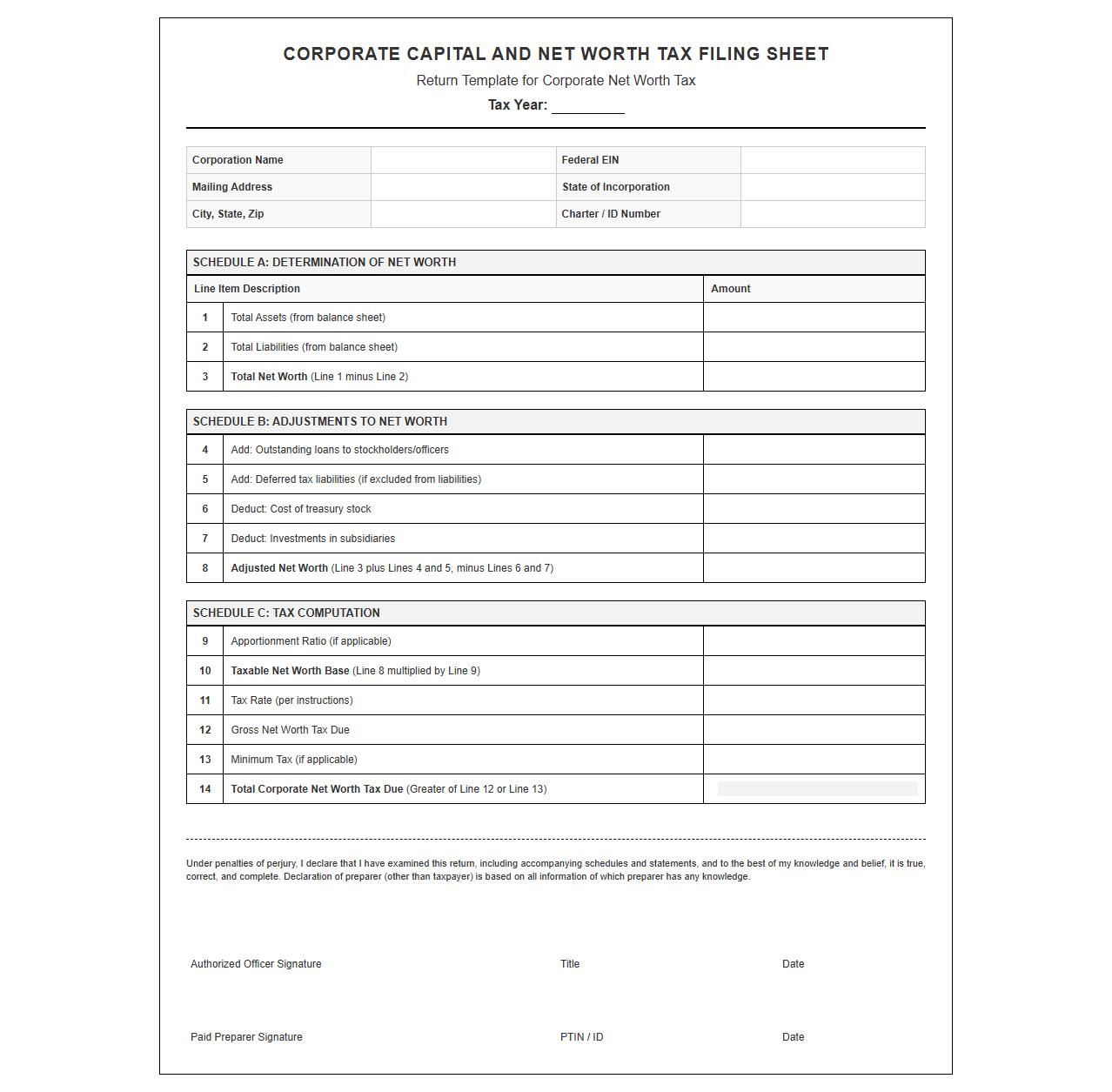

Corporate Capital and Net Worth Tax Filing Sheet

Download: .PDF

Download: .PDF

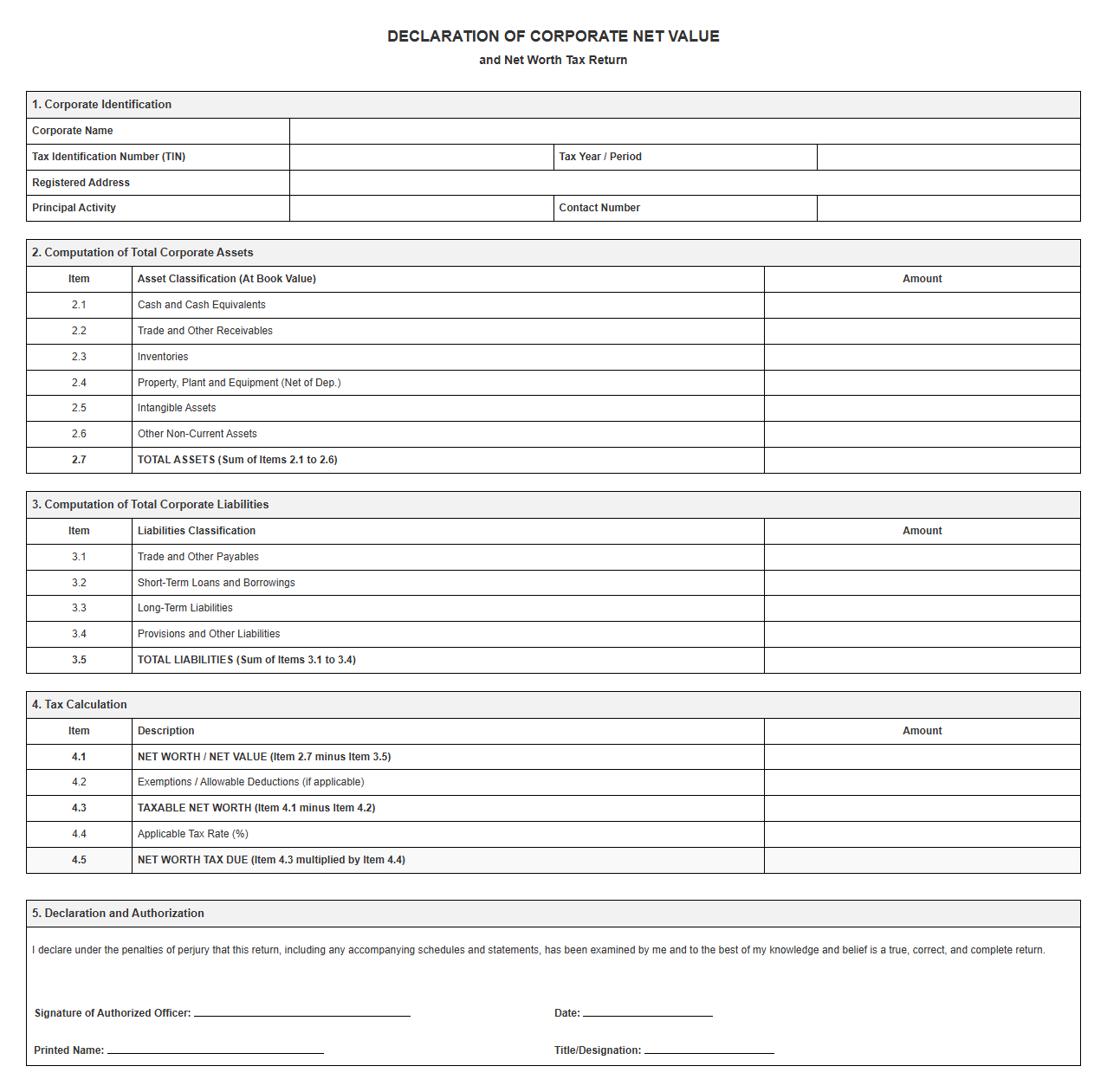

Declaration of Corporate Net Value and Tax Return

Download: .PDF

Download: .PDF

Demystifying Corporate Net Worth Tax: The Role of Standardized Templates

Navigating the complexities of corporate net worth tax compliance presents a significant challenge for modern enterprises. Because net worth tax is levied on the accumulated wealth of a corporation rather than its annual income, companies must accurately determine the fair value of their entire asset portfolio minus allowable liabilities. This process requires meticulous data extraction, cross-departmental alignment, and adherence to specific jurisdictional rules. Without a structured approach, organizations face increased risks of overpaying or triggering costly audits.

Implementing standardized return templates is a highly effective way to streamline this filing process. By establishing a uniform framework, tax departments can automate data aggregation, reduce manual transcription errors, and ensure consistent application of tax rules across all entities. This systematic methodology not only saves valuable hours during the filing season but also provides unprecedented visibility into the underlying financial data that supports the final tax position.

The Foundation: Standardized Balance Sheet Template

Structuring the Asset Framework for Tax Optimization

A standardized balance sheet template serves as the bedrock for calculating a company's net worth tax base. Unlike traditional GAAP or IFRS balance sheets, a tax-optimized balance sheet must isolate specific asset classes that are subject to distinct valuation rules under local tax laws.

To ensure accuracy, the template should clearly segregate assets into well-defined categories. Key asset classifications include:

- Tangible Fixed Assets: Real estate, machinery, and equipment, which often require adjustments for tax-allowed depreciation.

- Intangible Assets: Goodwill, patents, and trademarks, which may have different amortization rules or be exempt in certain jurisdictions.

- Financial Assets: Long-term investments and security holdings that require periodic fair-market value assessments.

- Current Assets: Inventory, accounts receivable, and liquid cash reserves that must be reconciled against short-term liabilities.

Bridging the Gap: Valuation and Depreciation Schedules

Adjusting Book Values to Tax-Compliant Net Worth

Book values recorded under standard accounting principles rarely align perfectly with tax-compliant valuations. To bridge this gap, tax professionals must implement a robust valuation and depreciation schedule template that systematically calculates the required adjustments.

- Identify the historical cost of each asset using the code

ASSET_COSTas the baseline. - Apply the local tax jurisdiction's approved depreciation rate using the standard formula

TAX_DEPR = COST * RATE. - Compare the accumulated tax depreciation against book depreciation to isolate the net adjustment variable

NET_ADJ. - Record the final tax-compliant net worth value in the master ledger.

Liability Tracking: Verifying Deductible Corporate Debt

Reconciling Corporate Liabilities for Tax Reductions

To arrive at an accurate taxable net worth, businesses must subtract qualifying liabilities from their gross asset base. However, not all corporate debts are treated equally by tax authorities. It is critical to use a reconciliation template that categorizes liabilities and ensures only legally deductible debts are applied.

| Liability Type | Deductibility Status | Verification Requirement |

|---|---|---|

| Secured Bank Loans | Fully Deductible | Active loan agreements and bank statements |

| Intercompany Debt | Subject to Limits | Transfer pricing documentation and arm's-length terms |

| Contingent Liabilities | Generally Non-Deductible | Legal risk assessments and accounting provisions |

Consolidation and Equity: Managing Intercompany Holdings

Eliminating Double Taxation in Group Filings

For multinational corporations or groups with complex holding structures, intercompany equity investments pose a significant risk of double taxation. If parent and subsidiary assets are counted independently without adjustments, the same capital may be taxed multiple times within the same group.

Important Compliance Rule: To prevent double taxation, the parent company must systematically eliminate the book value of its equity investments in subsidiaries, ensuring that only the net external capital of the consolidated group is subjected to the corporate net worth tax.

A standardized intercompany consolidation template automates this elimination process, tracking equity ownership percentages and mapping them directly to offsetting liability entries to guarantee an accurate, single-level tax assessment.

The Executive Summary: Creating a Net Worth Tax Cover Sheet

Designing a Sign-Off-Ready Dashboard

A comprehensive net worth tax filing contains dozens of supporting schedules, calculators, and legal references. For executive review and sign-off, this vast amount of data must be synthesized into a clear, high-level cover sheet.

The cover sheet template serves as the executive summary, aggregating figures from all underlying schedules. It highlights the gross assets, total allowable deductions, and the final taxable net worth base. Crucial data points, such as the total tax liability due and the filing deadline, should be highlighted with a visual marker to ensure immediate visibility for corporate officers and external auditors.

Safeguarding the Filing: Audit-Ready Checklist and Documentation Log

Completing the return is only half the battle; ensuring the filing can withstand regulatory scrutiny is equally vital. A standardized checklist and documentation log must accompany every submission to serve as a reliable audit trail.

- Verify that all asset valuations map directly to the general ledger.

- Confirm that all intercompany eliminations are supported by active agreements.

- Validate that deductible liabilities meet local statutory requirements.

- Archive all external appraisal reports used for real estate or intellectual property.

Leave a comment