Chief financial officers and reporting teams consistently struggle with the opaque, volatile nature of Other Comprehensive Income (OCI). Because these fluctuating equity adjustments often obscure core operational performance, presenting them clearly to stakeholders remains a persistent challenge.

Before implementing presentation remedies, however, organizations must position this issue within the context of rapidly evolving international accounting standards. Standardizing OCI reporting is not merely a compliance exercise; it grants corporate treasury and finance leaders the clarity needed to transform reporting noise into strategic foresight.

While this article does not replace formal GAAP or IFRS advisory services, it establishes a practical framework for reducing presentation complexity. By systematically structuring volatile elements-such as foreign currency translation adjustments and unrealized gains on available-for-sale securities-firms can provide much-needed transparency to investors.

Below, we analyze the structural formats, presentation methodologies, and template best practices designed to streamline your OCI disclosures and elevate your financial reporting.

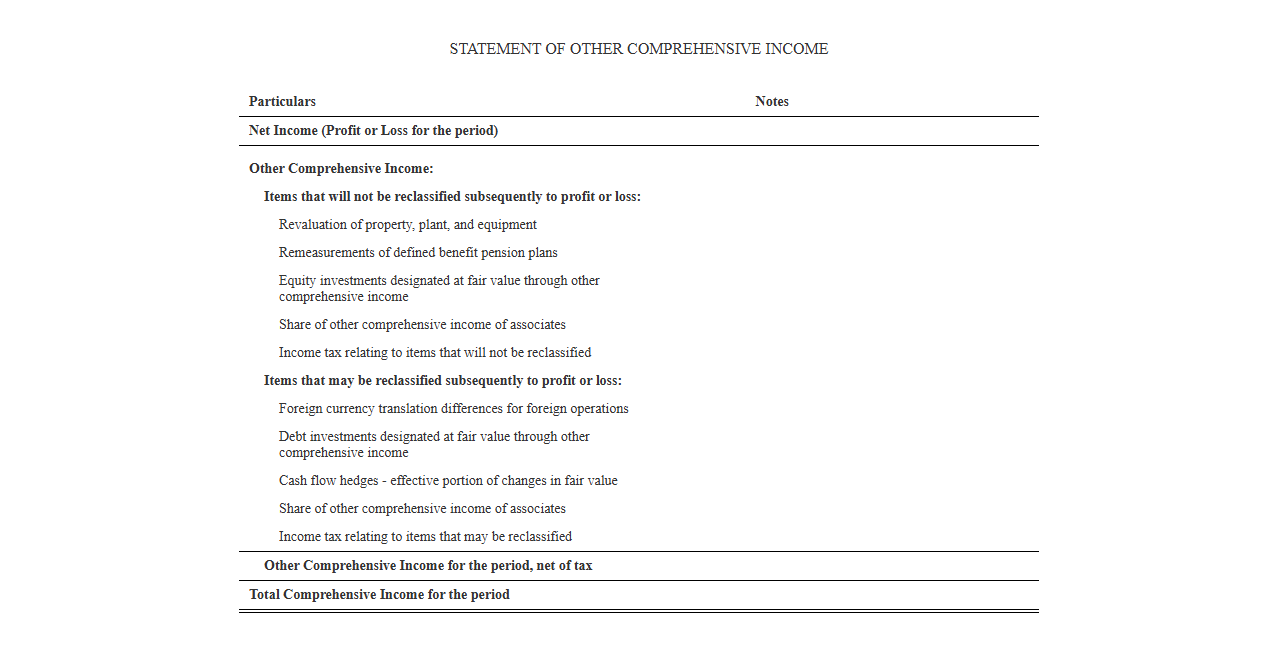

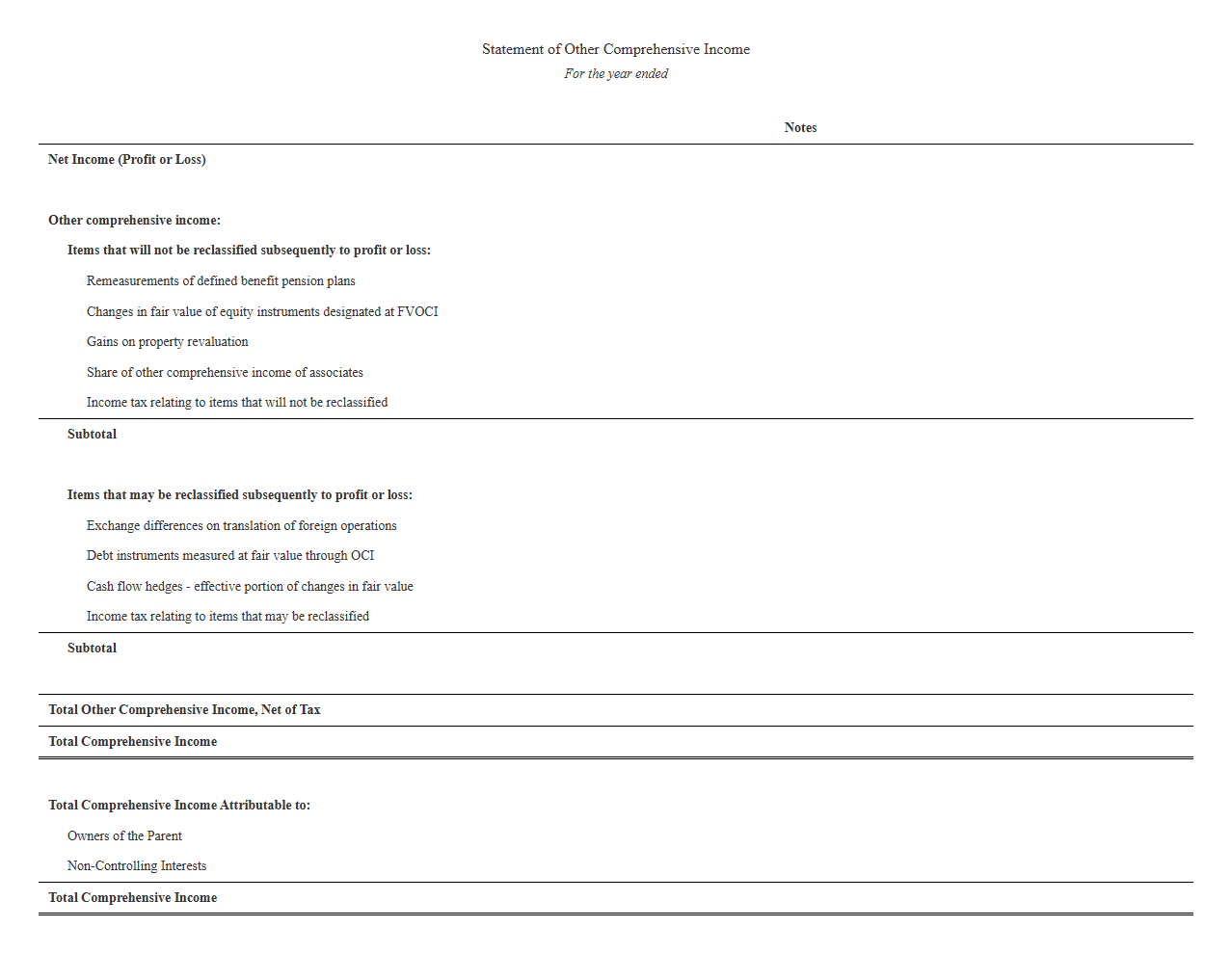

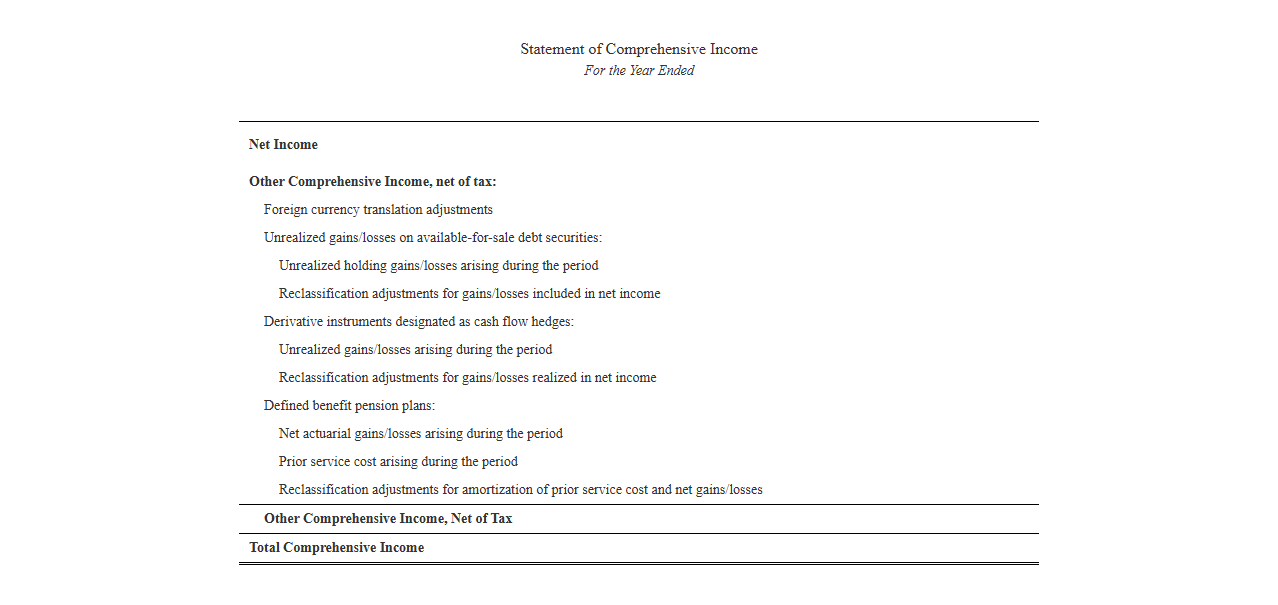

Statement of Other Comprehensive Income Template

Download: .PDF

Download: .PDF

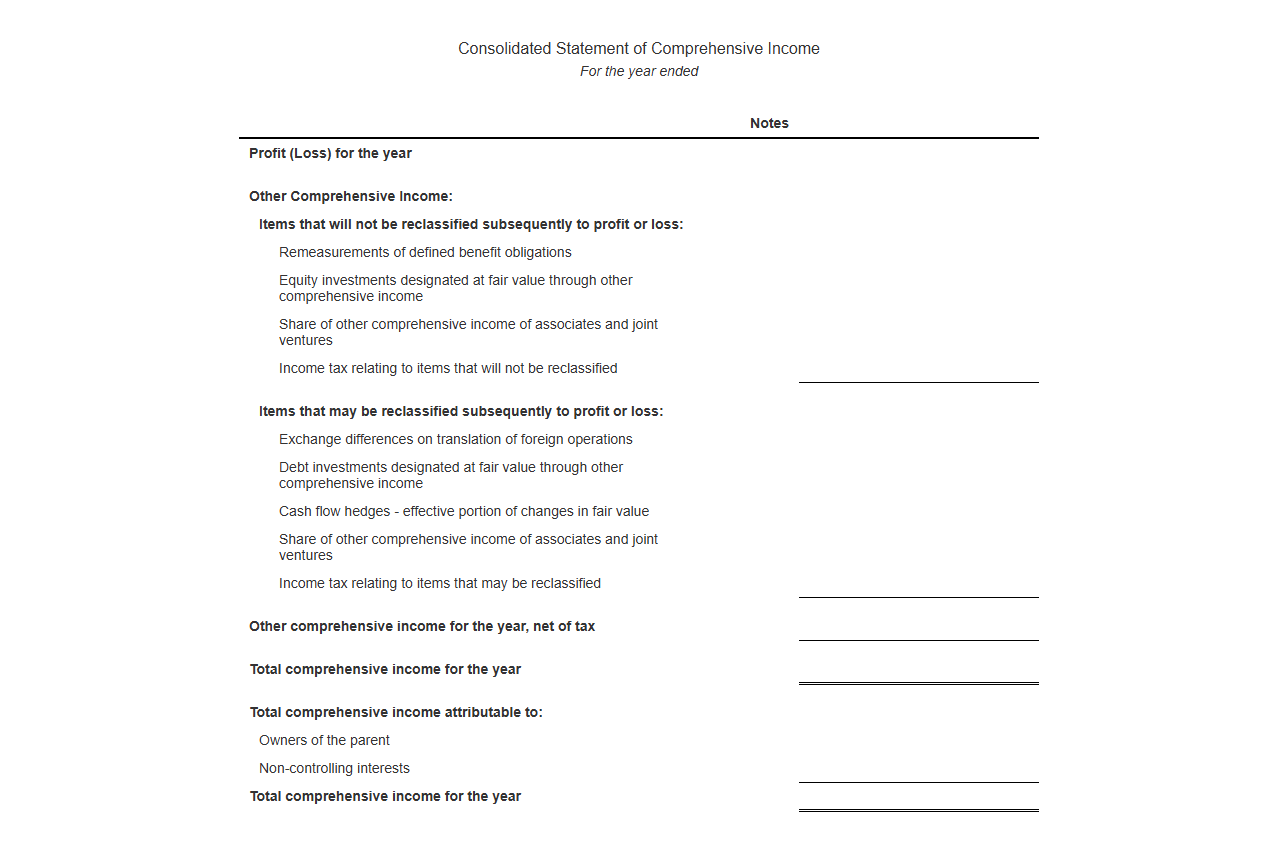

Consolidated Statement of Comprehensive Income Format

Download: .PDF

Download: .PDF

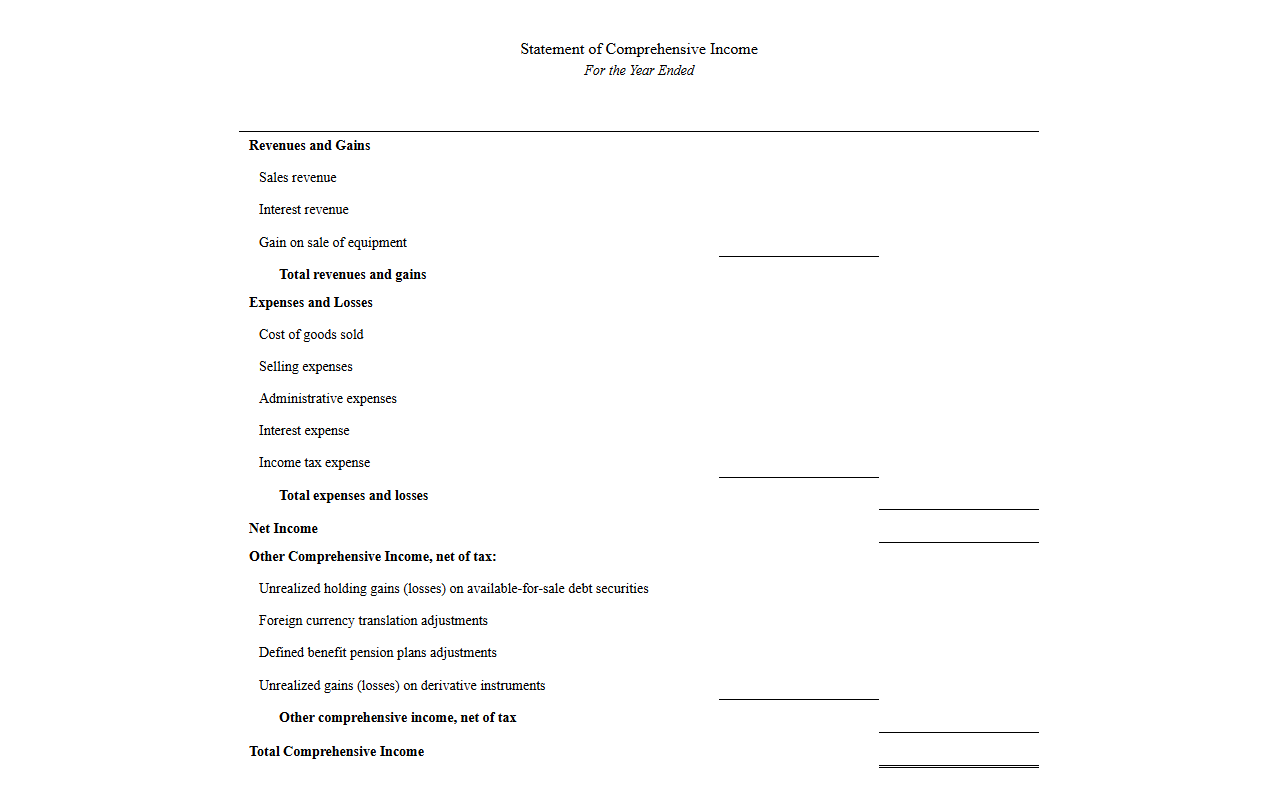

Single-Step Comprehensive Income Statement Template

Download: .PDF

Download: .PDF

Two-Statement Comprehensive Income Report Layout

Download: .PDF

Download: .PDF

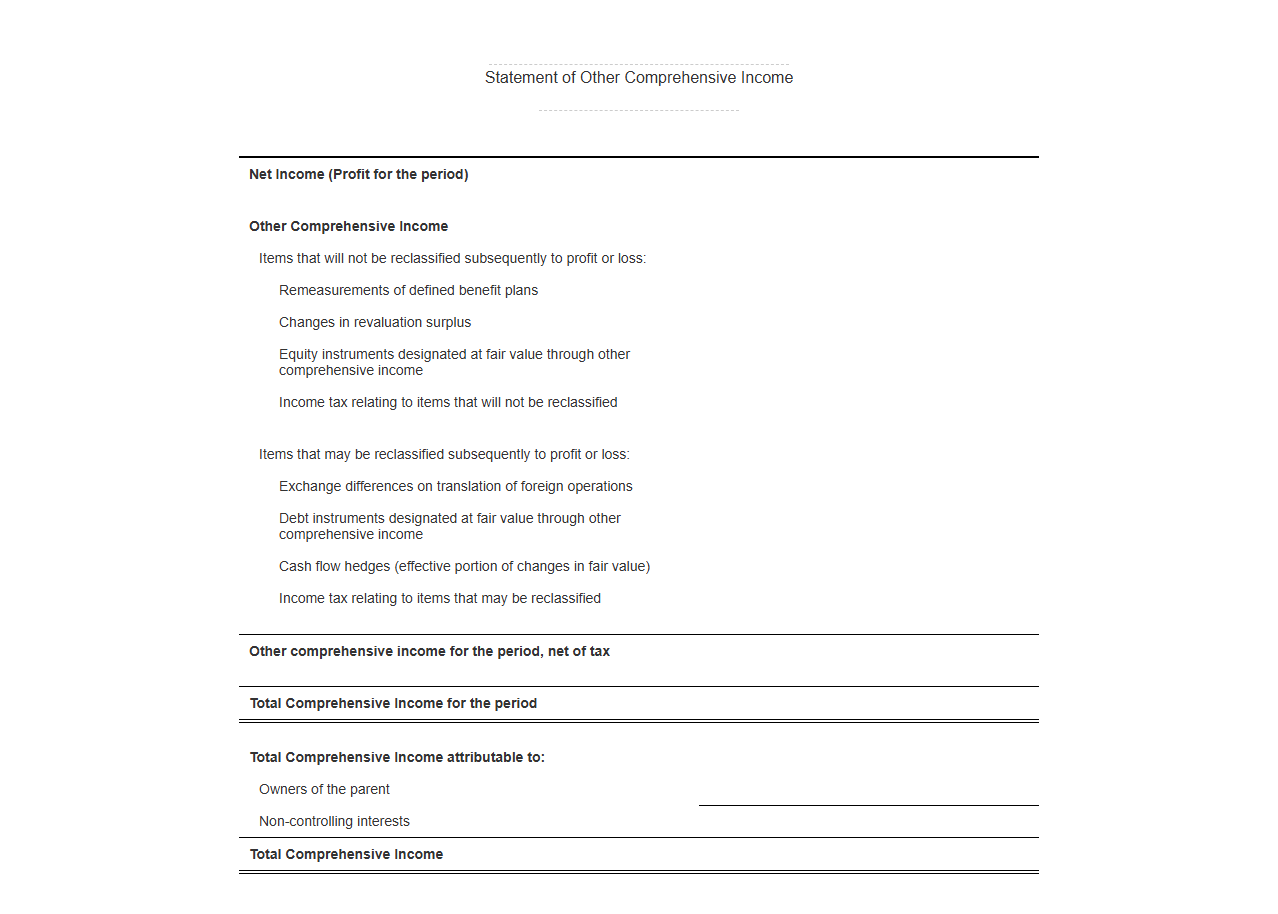

Other Comprehensive Income Disclosure Template

Download: .PDF

Download: .PDF

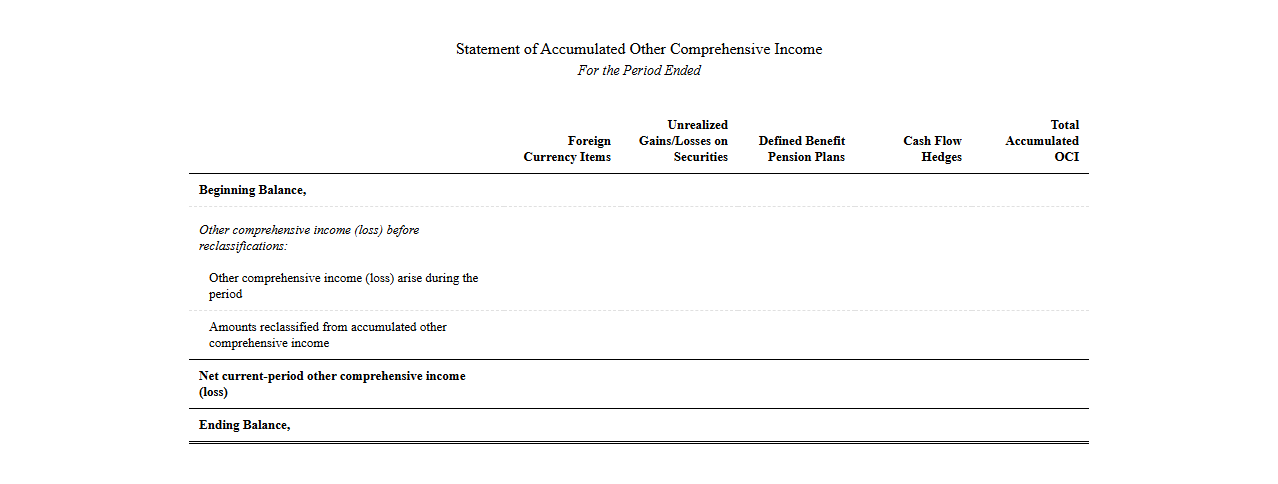

Statement of Accumulated Other Comprehensive Income Template

Download: .PDF

Download: .PDF

Comprehensive Income Reporting Excel Template

Download: .PDF

Download: .PDF

Statement of Changes in Comprehensive Income Format

Download: .PDF

Download: .PDF

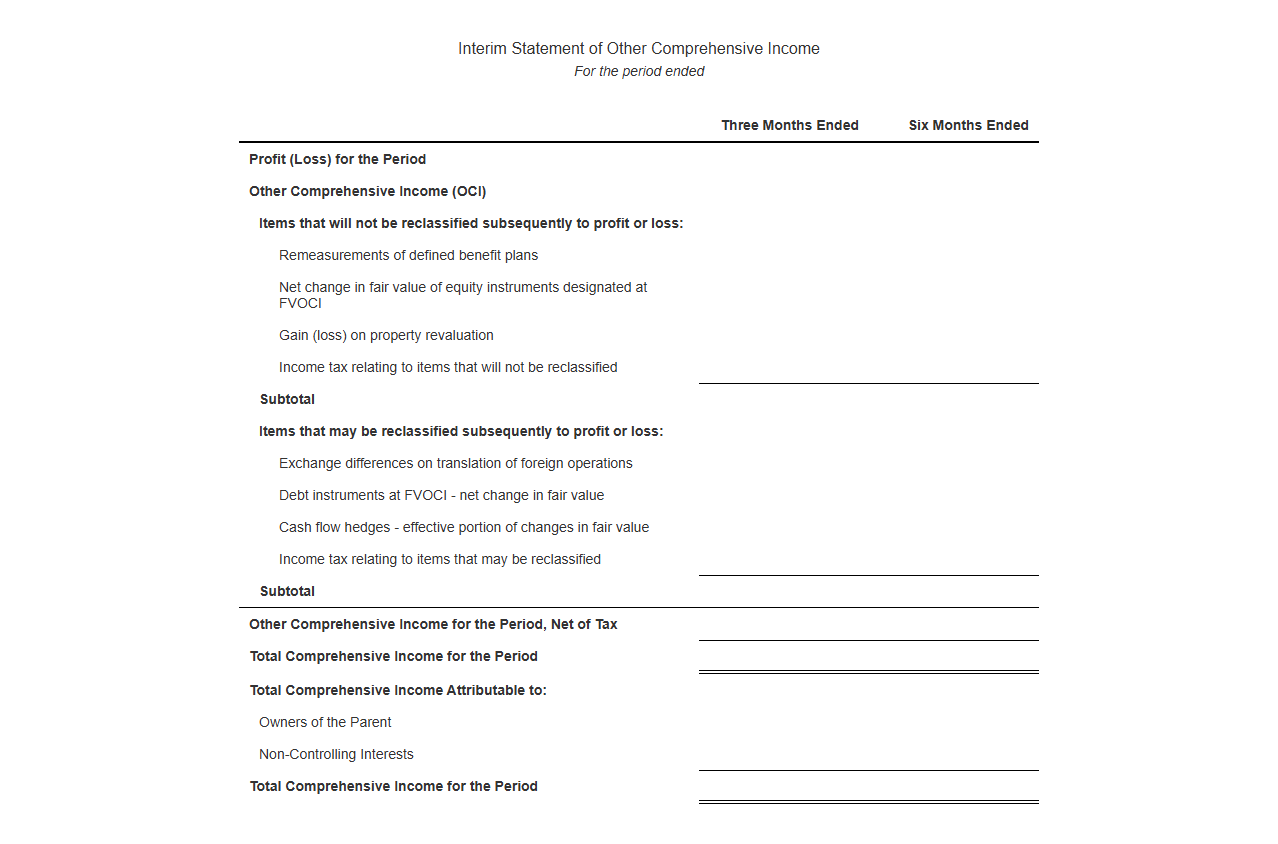

Interim Statement of Other Comprehensive Income Template

Download: .PDF

Download: .PDF

Annual Report Comprehensive Income Statement Template

Download: .PDF

Download: .PDF

Introduction: Decoding the Complexity of Other Comprehensive Income

For many financial professionals and stakeholders, Other Comprehensive Income (OCI) remains one of the most elusive areas of corporate reporting. Traditionally, OCI has been treated as a clearinghouse for complex financial adjustments that do not fit neatly into standard net income. Because these figures bypass the traditional income statement, they often obscure a company's true economic reality, creating a barrier to transparent evaluation.

Modern financial reporting requires a highly structured approach to resolve this legacy opacity. As global markets grow more interconnected and volatile, relying on obscure footnotes to explain significant economic shifts is no longer viable. Implementing a standardized framework for accumulated other comprehensive income (AOCI) and current-period adjustments is essential for presenting a complete, undistorted picture of corporate financial health.

The Core Challenge: Understanding OCI Volatility and its Impact

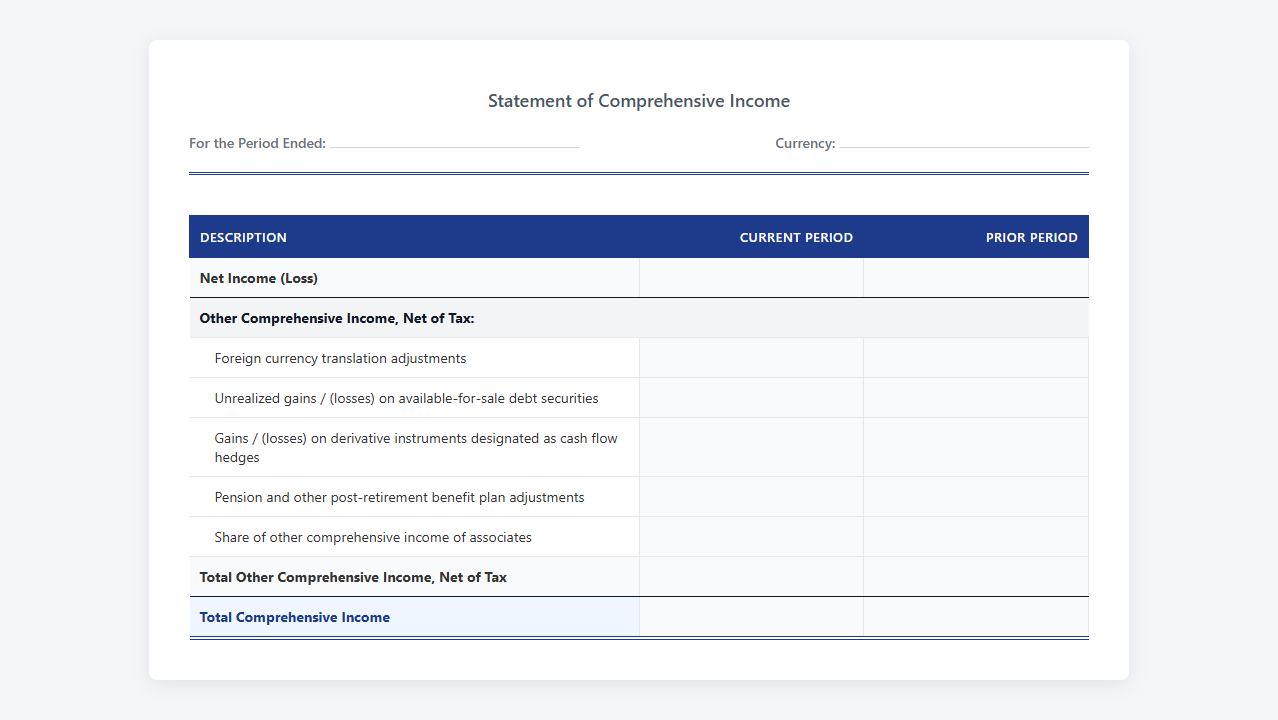

The primary difficulty with OCI lies in its inherent volatility. Unlike standard operational revenues and expenses, OCI is comprised of volatile, market-driven fluctuations. Among the most significant of these elements are unrealized gains and losses on available-for-sale debt securities, which shift constantly with fluctuating interest rates.

Additionally, pension liability adjustments-driven by actuarial assumptions and changing discount rates-can introduce massive, non-operational swings to the balance sheet. When combined with foreign currency translation adjustments arising from global operations, these volatile elements can severely distort traditional net income analysis if not isolated and reported with absolute clarity. Without a dedicated reporting structure, stakeholders may misinterpret these macro-driven fluctuations as fundamental operational failures or successes.

Paradigm Shift: Resolving Confusion through Structured OCI Formats

Transitioning from fragmented disclosure notes to a standardized, structured OCI statement format marks a critical evolution in corporate transparency. By bringing these figures into a cohesive, standardized presentation, organizations dramatically improve data readability and comparability across periods and industries. Analysts no longer need to manually reconstruct financial statements from disparate footnotes; instead, they can seamlessly extract structured data to evaluate long-term performance.

This structural evolution aligns directly with modern accounting directives designed to eliminate reporting ambiguity:

"An entity shall present all items of income and expense recognized in a period either in a single statement of profit or loss and other comprehensive income, or in two statements: a separate statement of profit or loss and a statement of presenting comprehensive income."

Anatomy of a Structured OCI Statement

A well-structured OCI statement systematically categorizes financial adjustments to ensure clarity. The fundamental division within this statement rests on whether specific gains or losses will eventually influence net income, separating items based on their future accounting treatment.

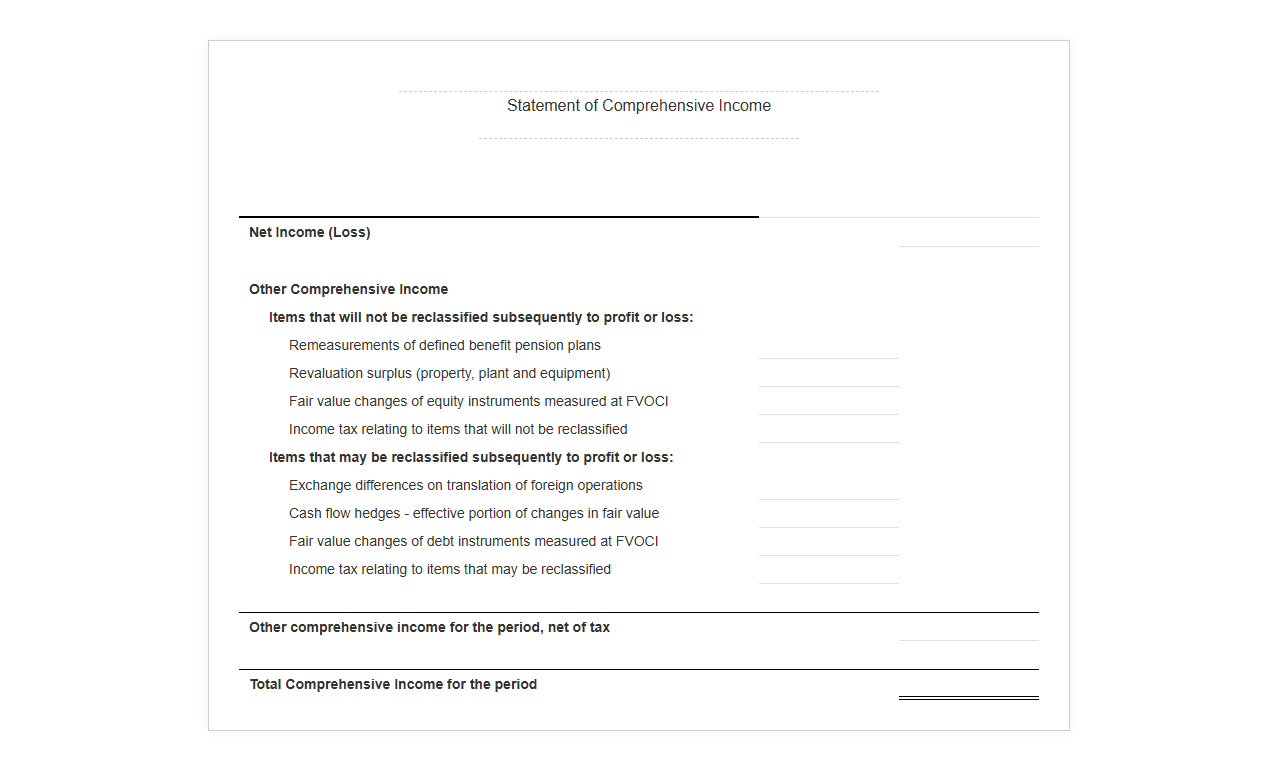

- Items that will not be reclassified subsequently to profit or loss: This category includes changes in revaluation surpluses on property, plant, and equipment, as well as actuarial gains and losses on defined benefit pension plans.

- Items that will be reclassified subsequently to profit or loss: This section captures foreign currency translation differences from foreign operations and unrealized gains or losses on debt instruments measured at fair value through other comprehensive income (FVOCI).

- Tax effects relating to OCI components: Clear disclosure of the tax expenses or benefits allocated individually to each component of OCI.

Strategic Value: How Transparency Benefits Investors and Management

A transparent OCI presentation serves as a powerful strategic tool for both internal and external stakeholders. For internal leadership, isolating market-driven fluctuations allows executives to evaluate core operational profitability without the distorting noise of macro-economic shifts. This operational clarity ensures more accurate capital allocation and strategic planning.

For external investors, structured OCI disclosure provides the necessary visibility to accurately assess risk profiles. Rather than being blindsided by sudden balance sheet adjustments, investors can monitor trends in foreign currency exposure and pension obligations in real time, leading to more confident valuations and a lower cost of capital for compliant corporations.

Technology Integration: Automating the OCI Reporting Process

Achieving accuracy in OCI reporting requires modern technological integration. Advanced ERP systems and specialized financial reporting software streamline the collection of complex data points, such as real-time foreign exchange rates and investment portfolio valuations, drastically reducing the risk of human error during manual consolidation.

To facilitate seamless communication with regulatory bodies and financial markets, these systems embed standardized metadata directly into reports. Utilizing standardized XBRL tags, such as <us-gaap:OtherComprehensiveIncomeLossNetOfTax>, ensures that OCI data is immediately machine-readable. This automation guarantees that complex financial data flows effortlessly from ERP sub-ledgers directly to public-facing financial portals without administrative friction.

Conclusion: The Future of Clear and Compliant Financial Communication

As regulatory scrutiny intensifies and market participants demand greater clarity, the era of treating Other Comprehensive Income as an afterthought is over. Standardized, structured OCI statements have evolved from a preferred accounting method into a regulatory and competitive necessity. By embracing structured presentation formats and modern automation technologies, corporations ensure total compliance while delivering the crystal-clear financial narratives that today's global investment community demands.

Leave a comment