S Corporation owners and tax professionals frequently battle the administrative nightmare of inconsistent financial reporting, which often leads to costly IRS inquiries and amended returns. This friction typically stems from the shifting complexities of basis tracking and disparate bookkeeping methods across entities. Implementing a standardized earnings statement template solves this by granting stakeholders immediate, audit-ready clarity and reducing year-end friction.

However, while these templates streamline data entry, they must be utilized as compliance aids rather than a substitute for professional CPA oversight. For instance, standardizing fields for the Accumulated Adjustments Account (AAA) and shareholder distributions ensures that net income reconciles perfectly with Schedule K-1 reporting. Below, we will explore the common pitfalls of S-Corp reporting, detail how to structure your standardized templates, and outline best practices for maintaining flawless, audit-resilient financial records.

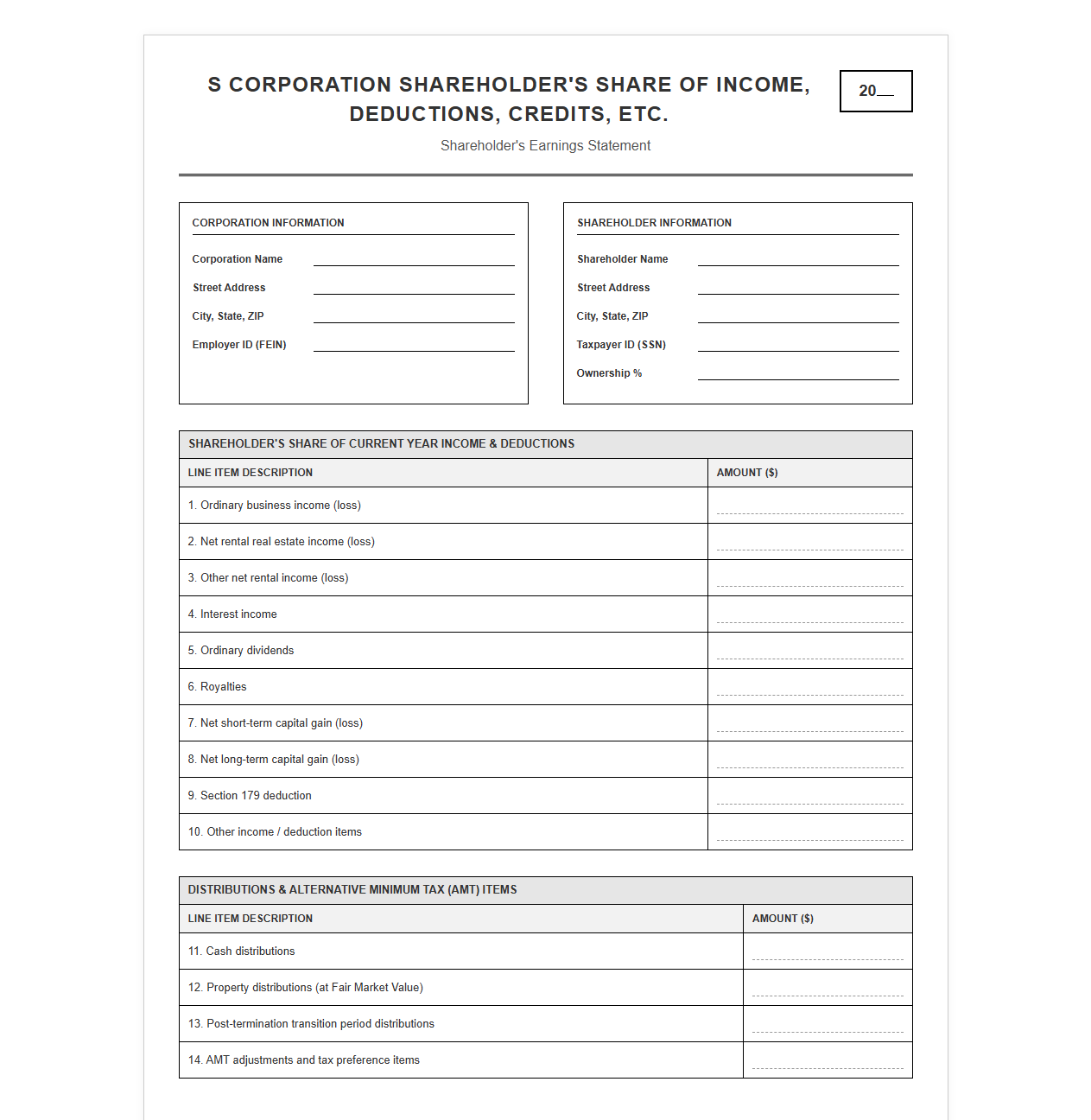

S Corp Shareholder Earnings Statement Template

Download: .PDF

Download: .PDF

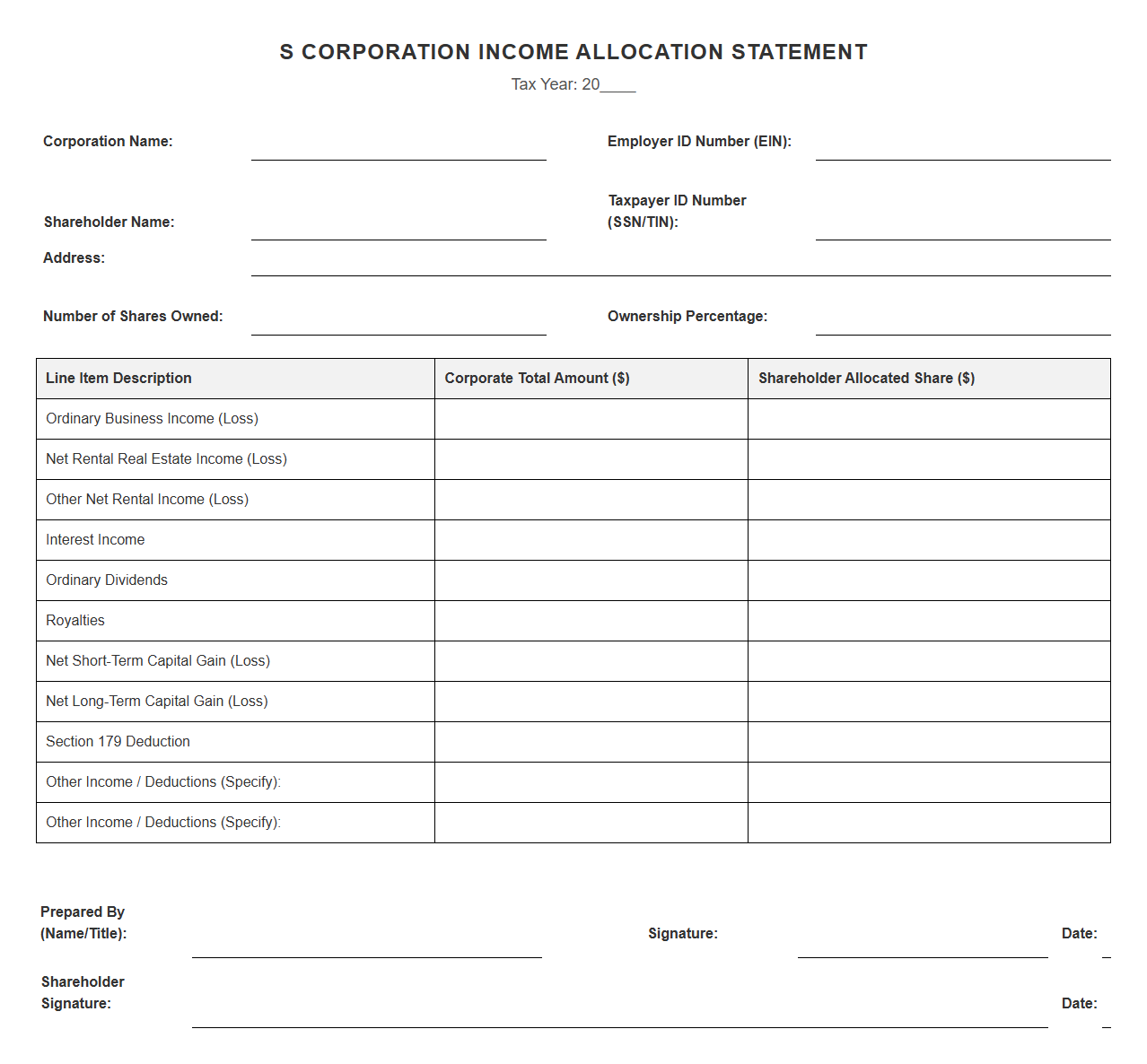

S Corporation Income Allocation Statement Format

Download: .PDF

Download: .PDF

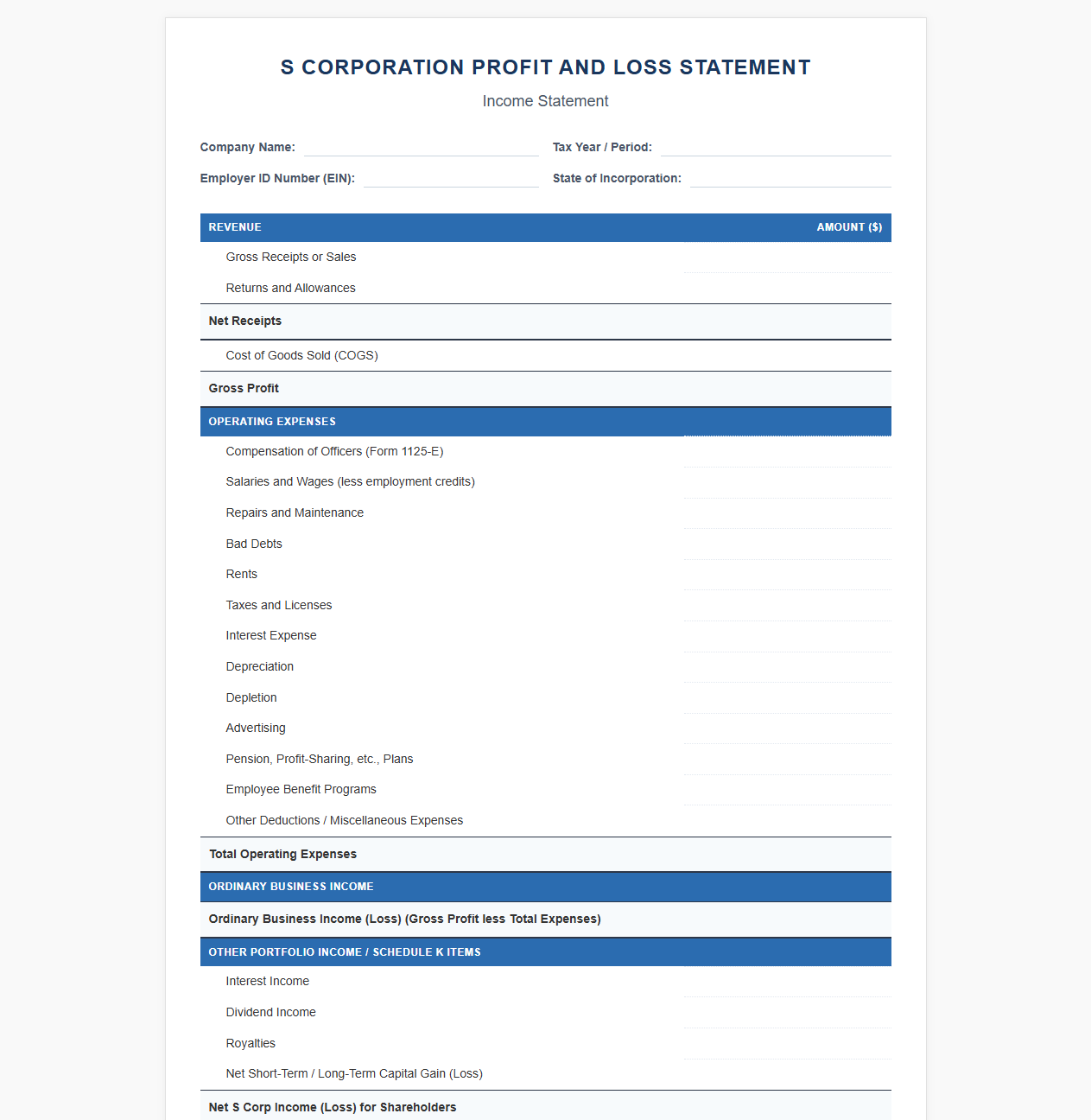

S Corp Profit and Loss Statement Template

Download: .PDF

Download: .PDF

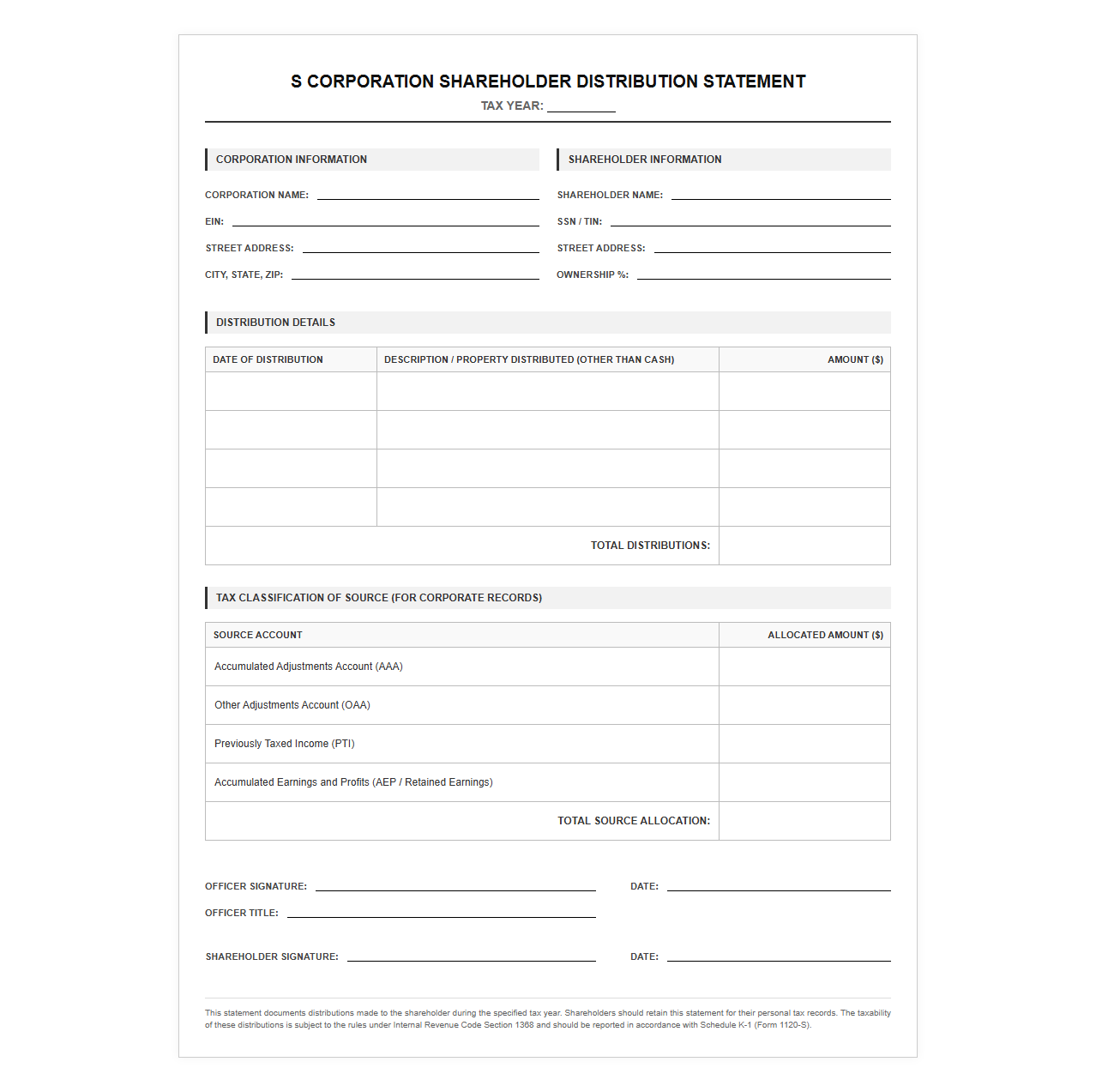

S Corporation Shareholder Distribution Statement

Download: .PDF

Download: .PDF

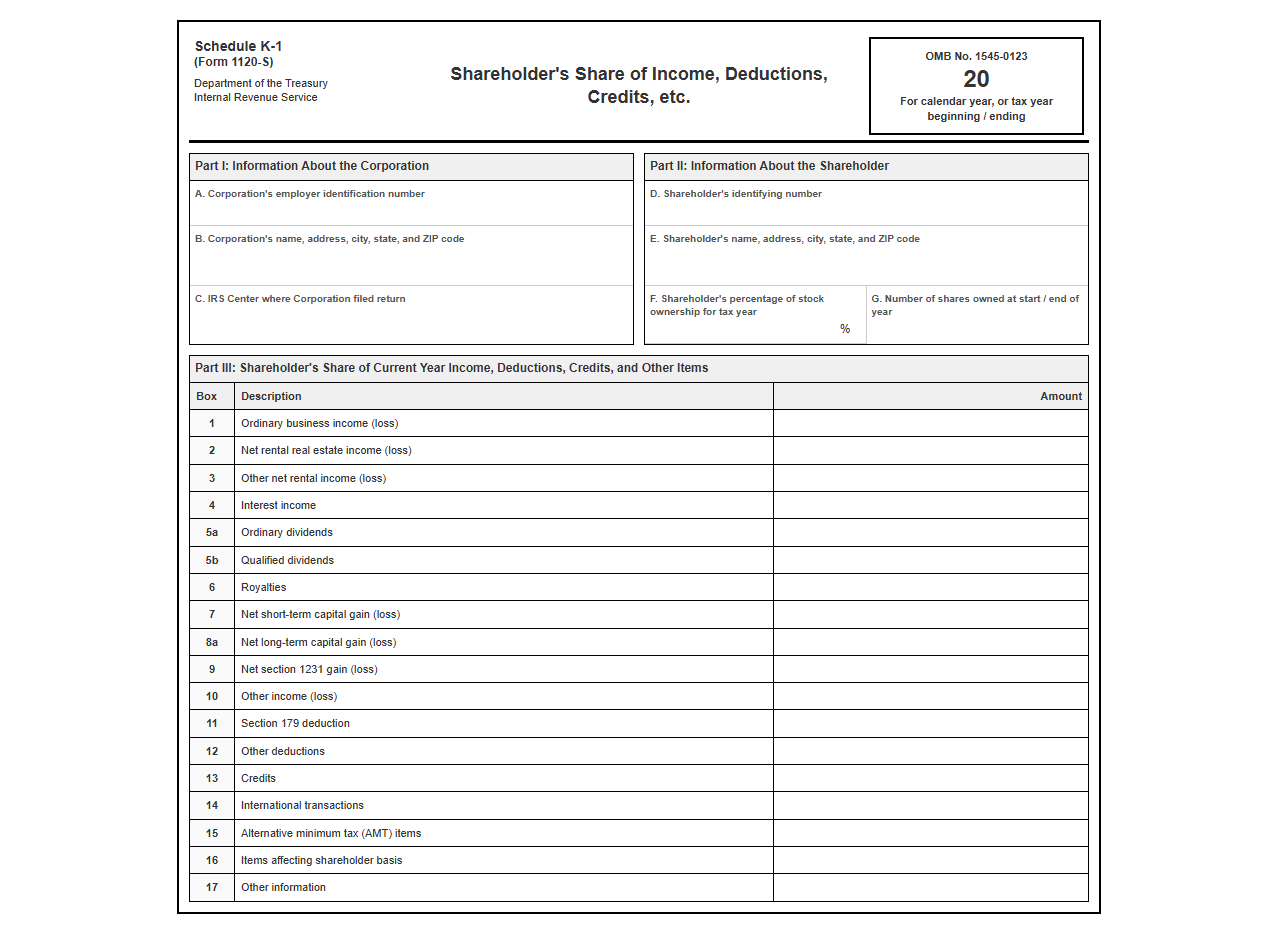

S Corp Schedule K-1 Earnings Statement Template

Download: .PDF

Download: .PDF

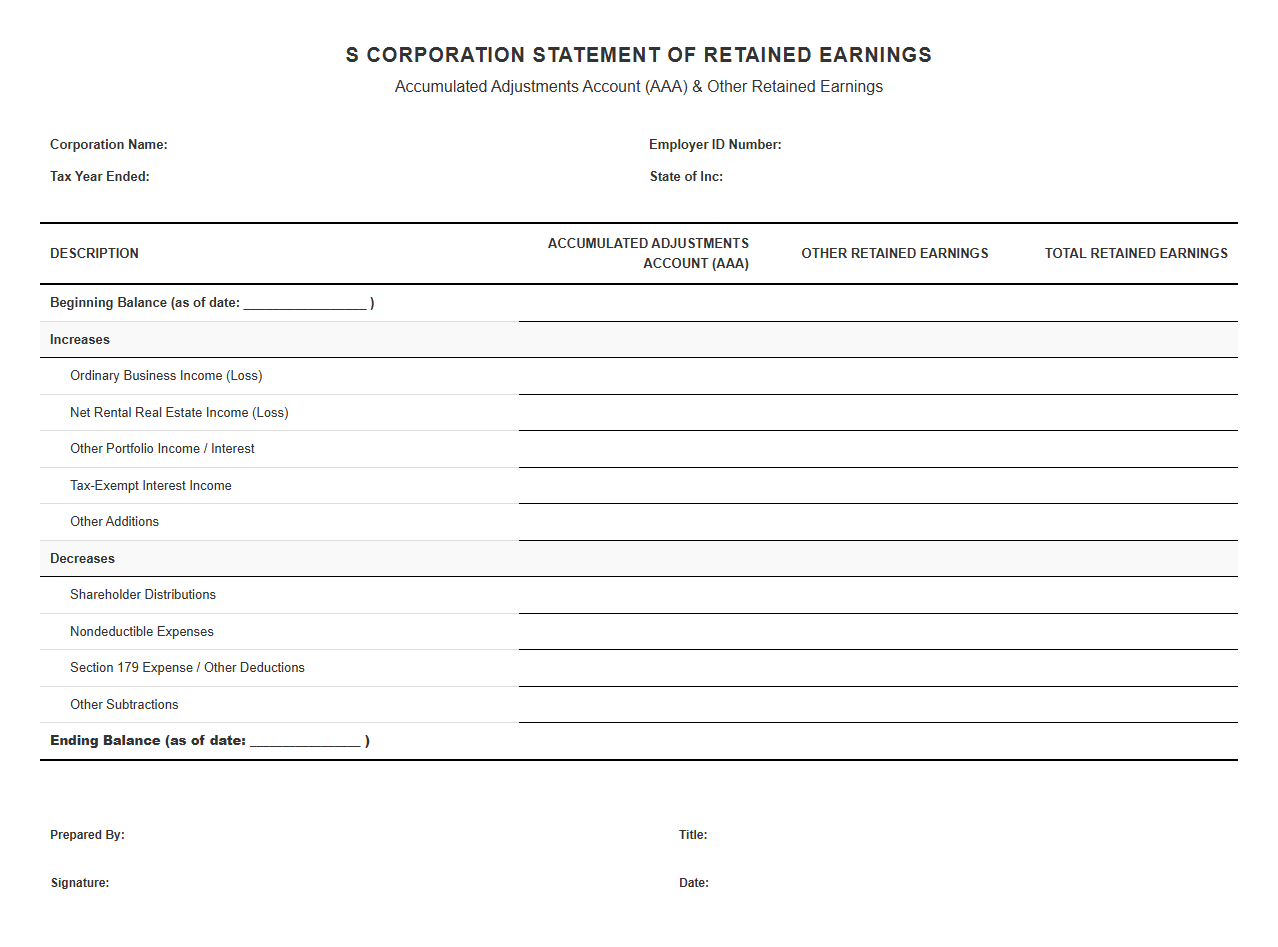

S Corporation Retained Earnings Statement Form

Download: .PDF

Download: .PDF

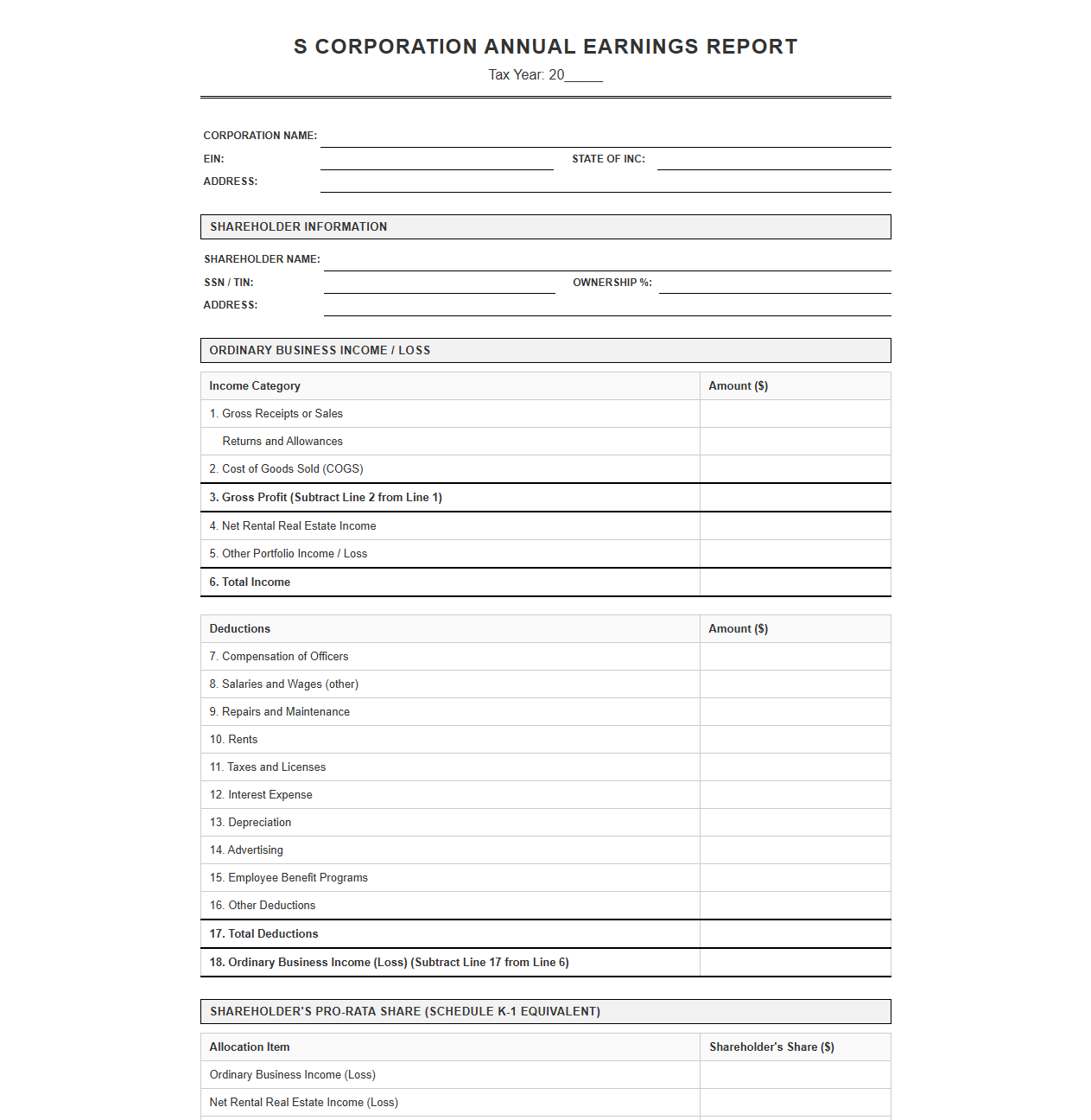

S Corporation Annual Earnings Report Template

Download: .PDF

Download: .PDF

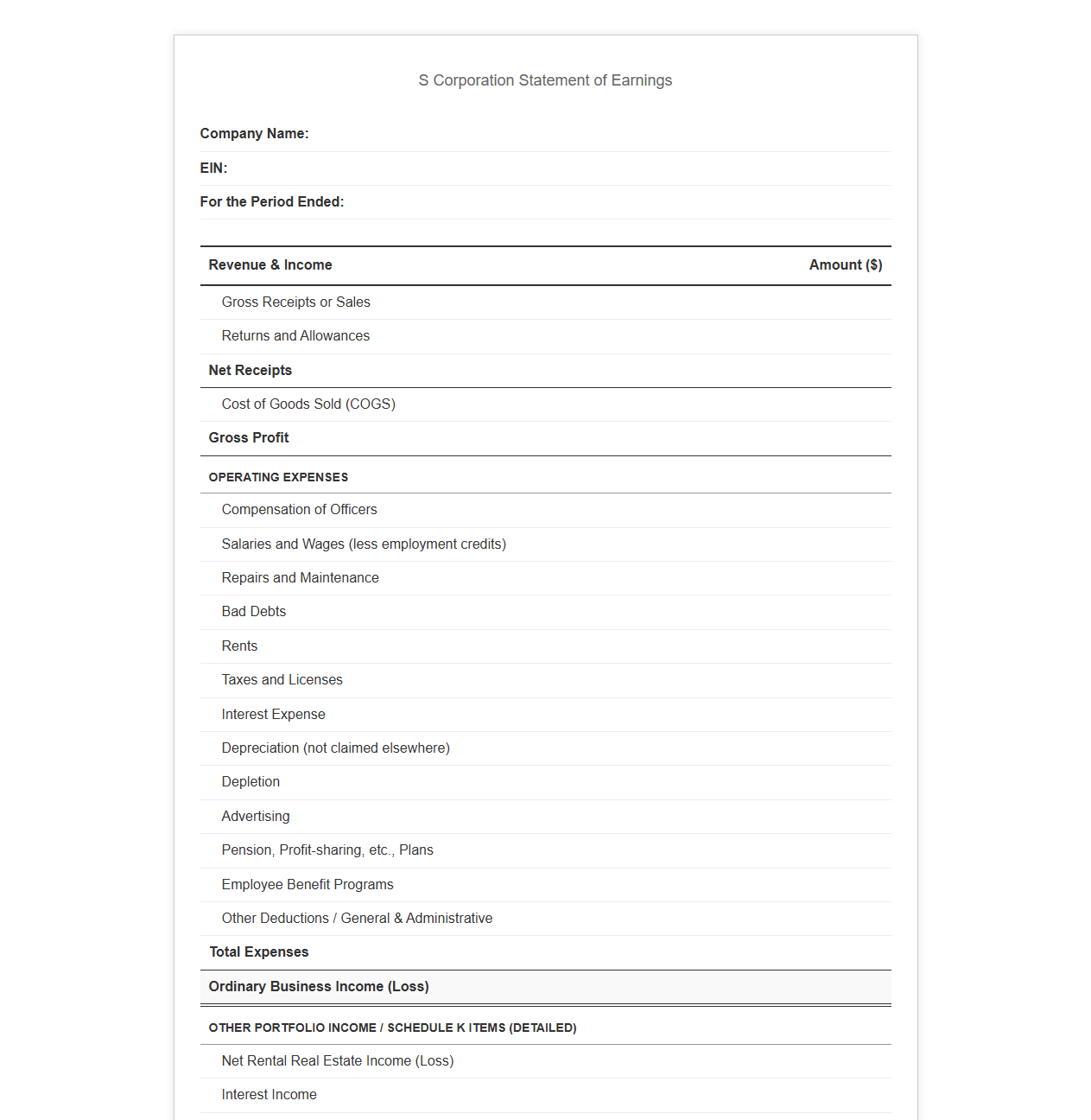

S Corp Net Income Statement Template

Download: .PDF

Download: .PDF

Understanding the S Corporation Reporting Challenge

Operating as an S Corporation offers significant tax advantages, but it also introduces unique regulatory challenges. Unlike traditional corporations or sole proprietorships, S-Corps require a strict separation of shareholder-employee compensation. Compliance errors frequently occur when business owners fail to distinguish between W-2 wages and shareholder distributions. Misunderstanding these definitions often leads to severe penalties during IRS audits.

Why Standardized Earnings Statements are Essential

To maintain clear financial boundaries, S-Corporations must implement standardized earnings statements. These documents serve as a reliable bridge between active payroll processing, annual W-2 reporting, and year-end Schedule K-1 distribution tracking. By maintaining meticulous monthly records, businesses can ensure that wage payments and profit distributions never blur together in the eyes of tax authorities.

Common S-Corp Reporting Pitfalls That Trigger Audits

Failing to adhere to strict IRS guidelines can quickly attract regulatory scrutiny. S-Corporations must remain vigilant against several high-risk reporting mistakes:

- Misclassifying distributions as wages: Attempting to avoid payroll taxes by paying zero or unreasonably low officer compensation.

- Neglecting reasonable compensation rules: Failing to pay shareholder-employees a salary that matches industry standards for their services.

- Improper health insurance reporting: Forgetting to report accident and health insurance premiums paid on behalf of 2% greater shareholders on their W-2 forms.

Anatomy of a Standardized S-Corp Earnings Statement Template

A robust earnings template must clearly delineate different types of income and withholdings. Utilizing a structured format ensures all critical data points are captured consistently during every pay cycle.

Key Structural Sections

- Officer Compensation Details: Clearly labeled gross wages subject to FICA, Medicare, and Federal Income Tax withholding.

- Shareholder Health Insurance Benefits: A dedicated line item reflecting health insurance premiums paid on behalf of 2% shareholders to ensure correct W-2 integration.

- Non-Wage Distributions: A separate category tracking equity distributions, ensuring these amounts are never processed through the payroll mechanism.

Step-by-Step Guide to Implementing the Templates

Transitioning to a standardized reporting system requires a systematic approach to update your accounting workflow successfully.

- Review current payroll software configurations to ensure custom fields can be created for shareholder health premiums.

- Coordinate with your CPA to establish the correct "Reasonable Compensation" figure for all working shareholders.

- Map the fields in your earnings statement template directly to corresponding lines on Form W-2 and Schedule K-1.

- Run a mock payroll reconciliation at the end of the first quarter to verify that wages and distributions remain distinct.

Impact Assessment: Ad-Hoc vs. Standardized Reporting

The difference between manual, ad-hoc tracking and using a standardized template becomes evident during tax season. Below is a comparison of key operational metrics:

| Metric | Ad-Hoc / Manual Reporting | Standardized Templates |

|---|---|---|

| Annual Error Rate | High (frequent misclassifications) | Very Low (systematic validation) |

| Tax Prep Time | Weeks of manual reconciliation | Hours of automated exporting |

| Audit Readiness | Vulnerable to IRS adjustments | Fully documented trail |

Best Practices for Continuous Compliance and Audit Readiness

Maintaining flawless compliance requires consistent effort and proactive management. S-Corp owners should review their earnings templates annually to ensure alignment with changing IRS regulations. It is vital to train internal bookkeeping staff regularly on the nuances of shareholder-employee compensation. By committing to these systematic updates, businesses can protect their tax status and minimize audit exposure. For more detailed guidance, consult the official IRS S Corporation Tax Center to stay informed on the latest federal tax rules.

Leave a comment