Tracking equity and initial investments remains a persistent challenge for business leaders navigating complex corporate structures. Without precise documentation, capturing the nuances of member contributions often leads to compliance risks and accounting discrepancies. Before addressing these reporting challenges, it is vital to recognize that clear equity tracking is the foundation of corporate governance and stakeholder trust.

Leveraging standardized contributed capital statement templates grants financial officers the precision needed to present transparent equity data to investors and regulators. While these templates serve as robust architectural baselines, they must be adapted to your specific regulatory jurisdiction under professional accounting guidance. For instance, a multi-member LLC requires different capital account tracking than a C-Corporation issuing common stock or a partnership managing capital calls.

This guide examines tailored templates for diverse business entities, offering the structural blueprints and best practices necessary to document your organization's equity with absolute confidence.

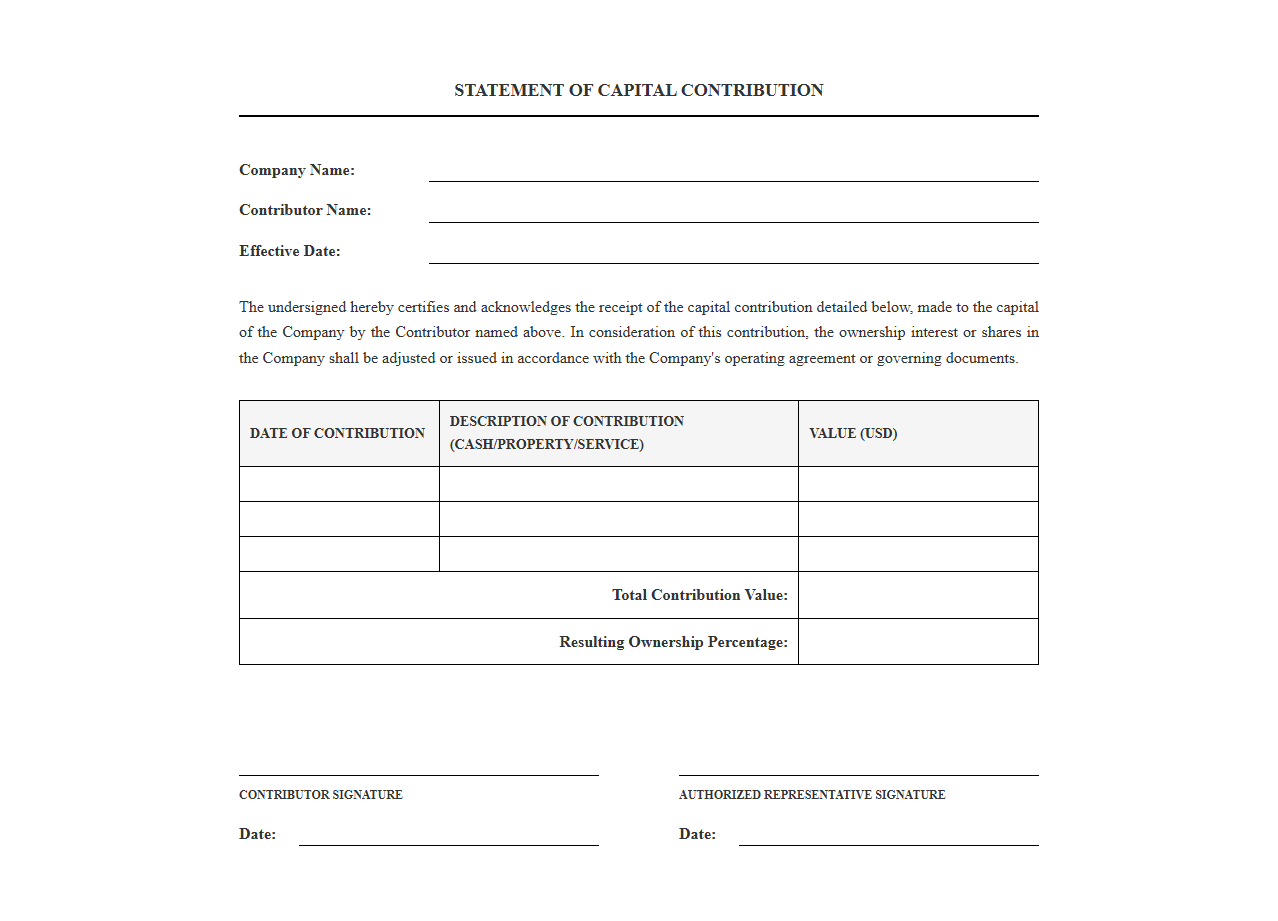

Capital Contribution Statement Template

Download: .PDF

Download: .PDF

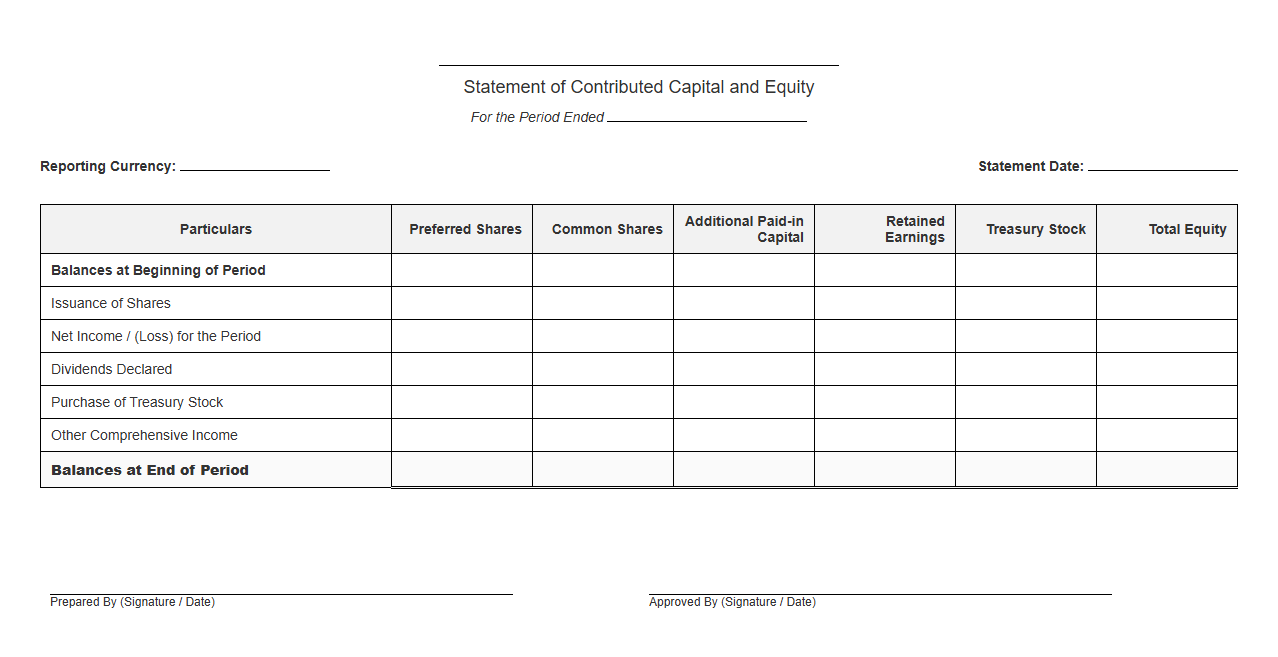

Statement of Contributed Capital and Equity

Download: .PDF

Download: .PDF

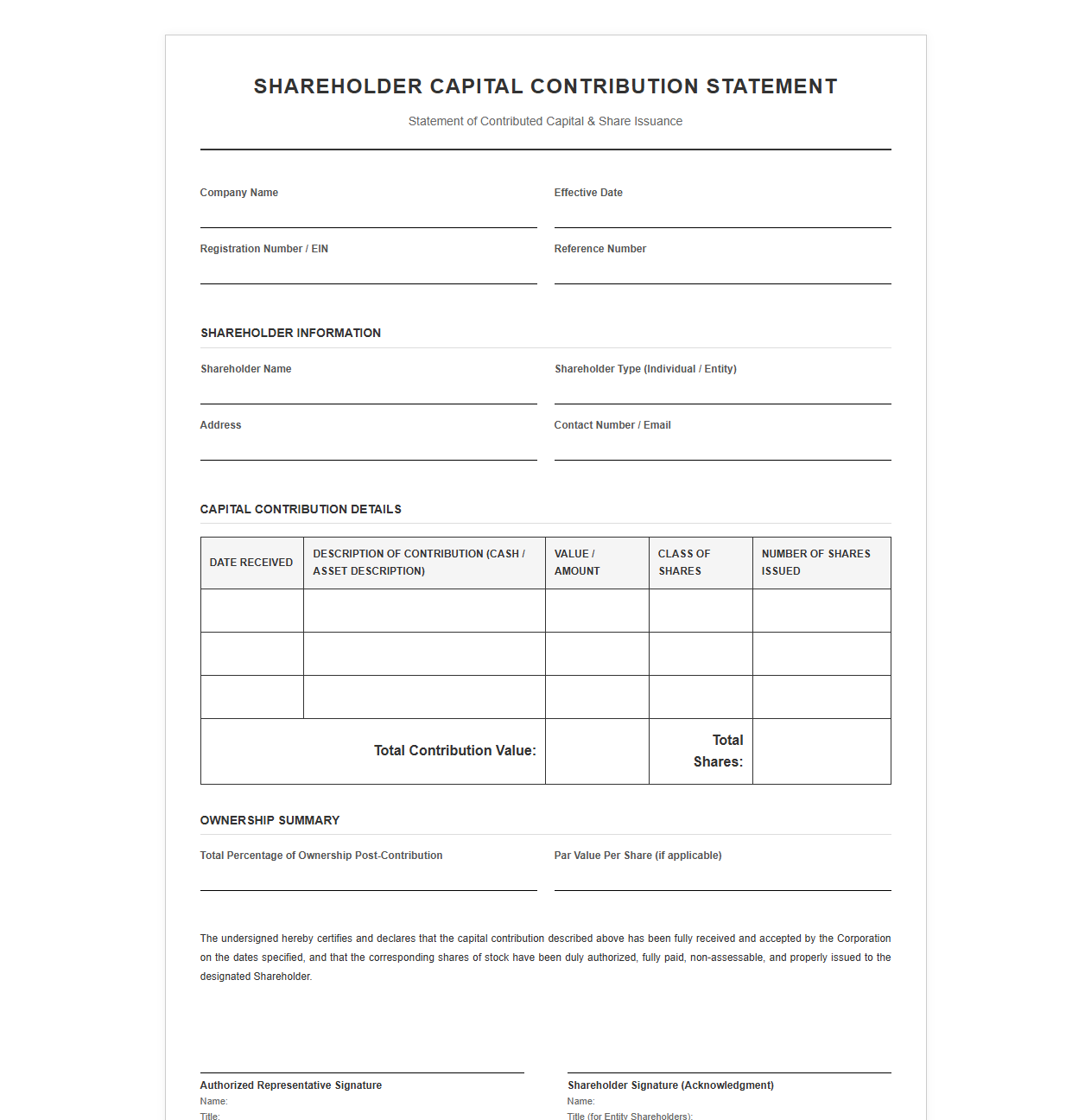

Shareholder Capital Contribution Statement Template

Download: .PDF

Download: .PDF

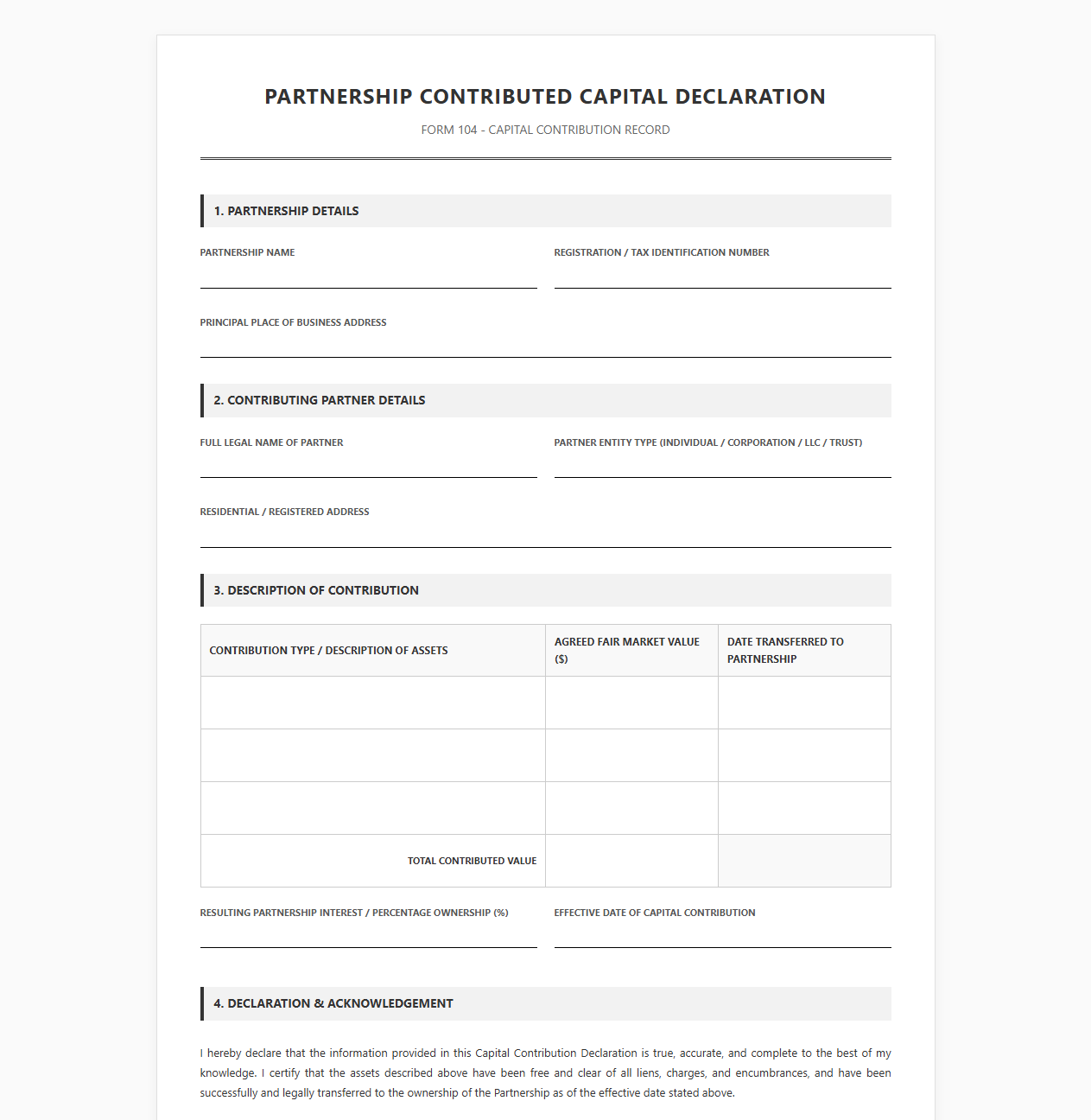

Partnership Contributed Capital Declaration Form

Download: .PDF

Download: .PDF

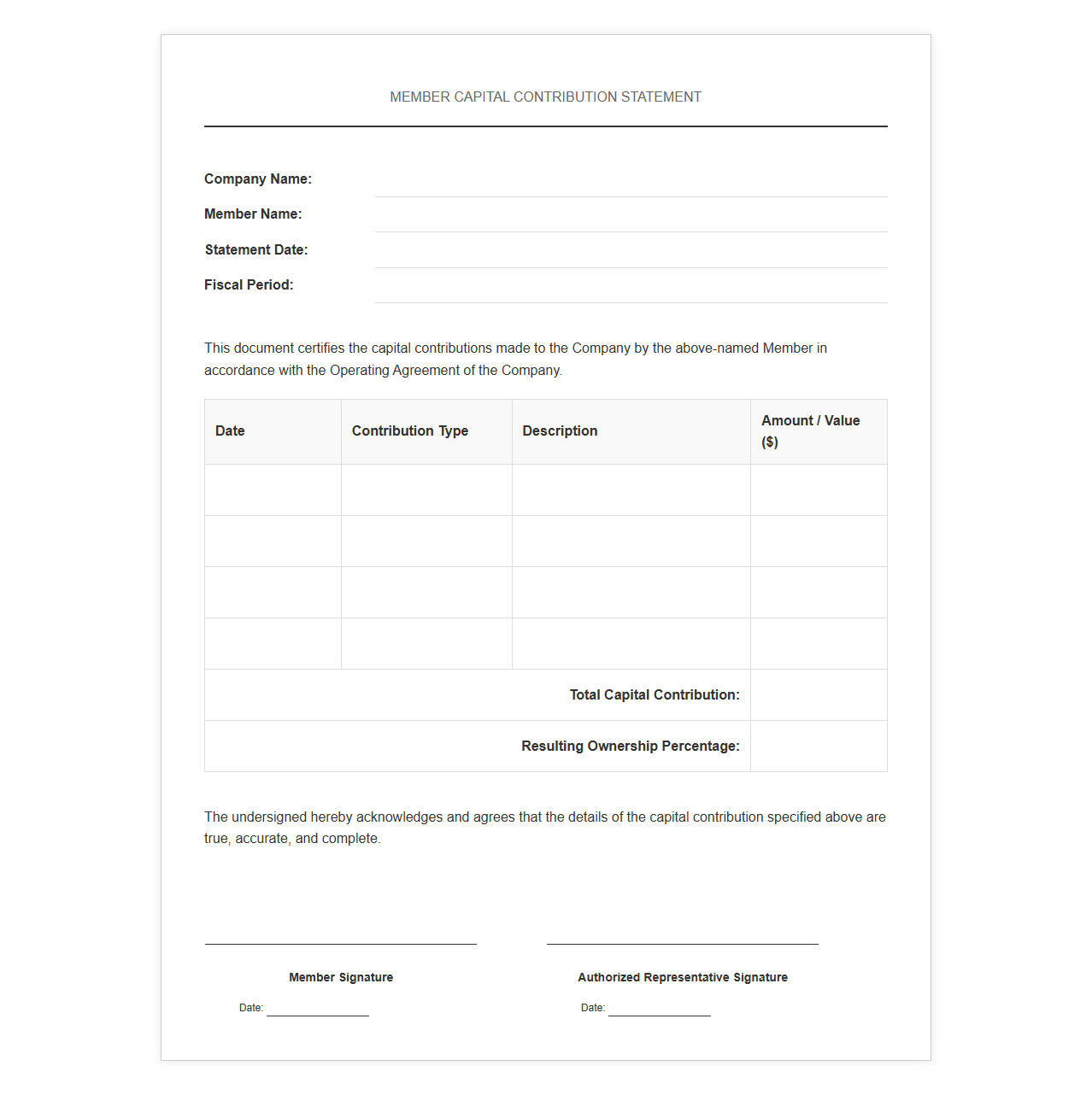

Member Capital Contribution Statement Document

Download: .PDF

Download: .PDF

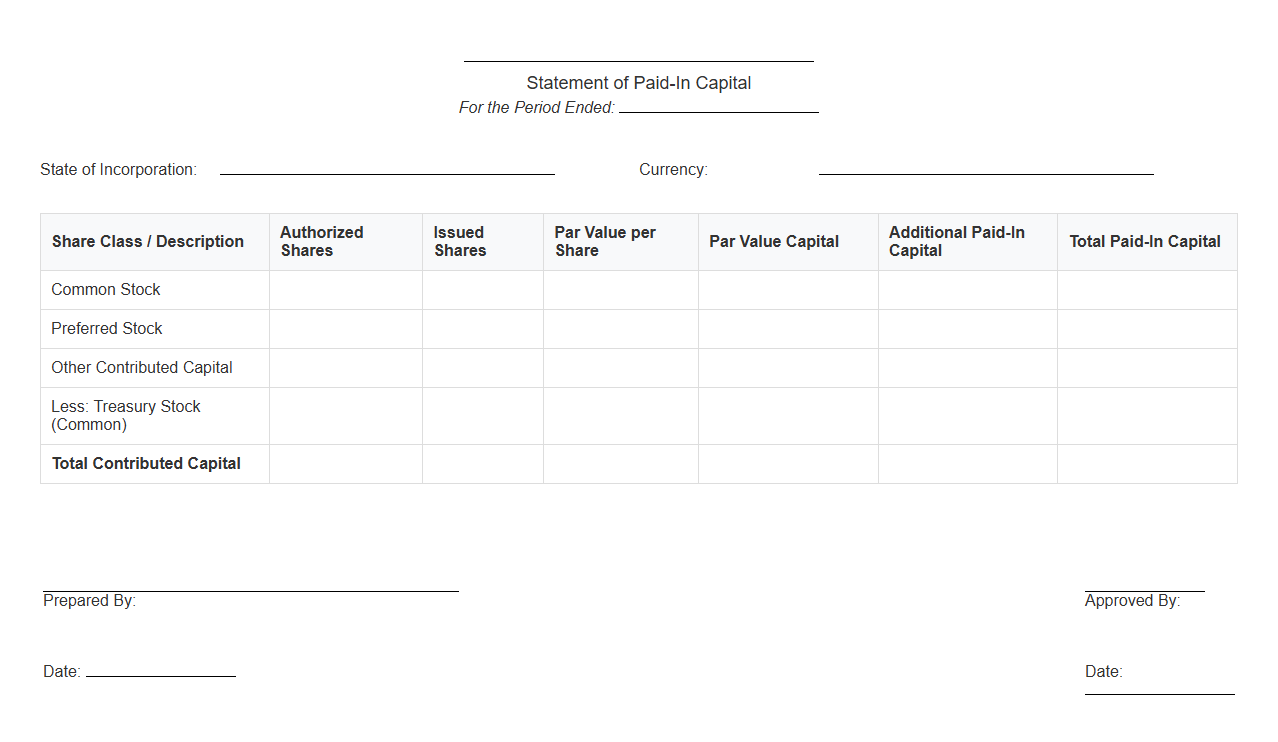

Statement of Paid-In Capital Template

Download: .PDF

Download: .PDF

Certificate of Capital Contribution Template

Download: .PDF

Download: .PDF

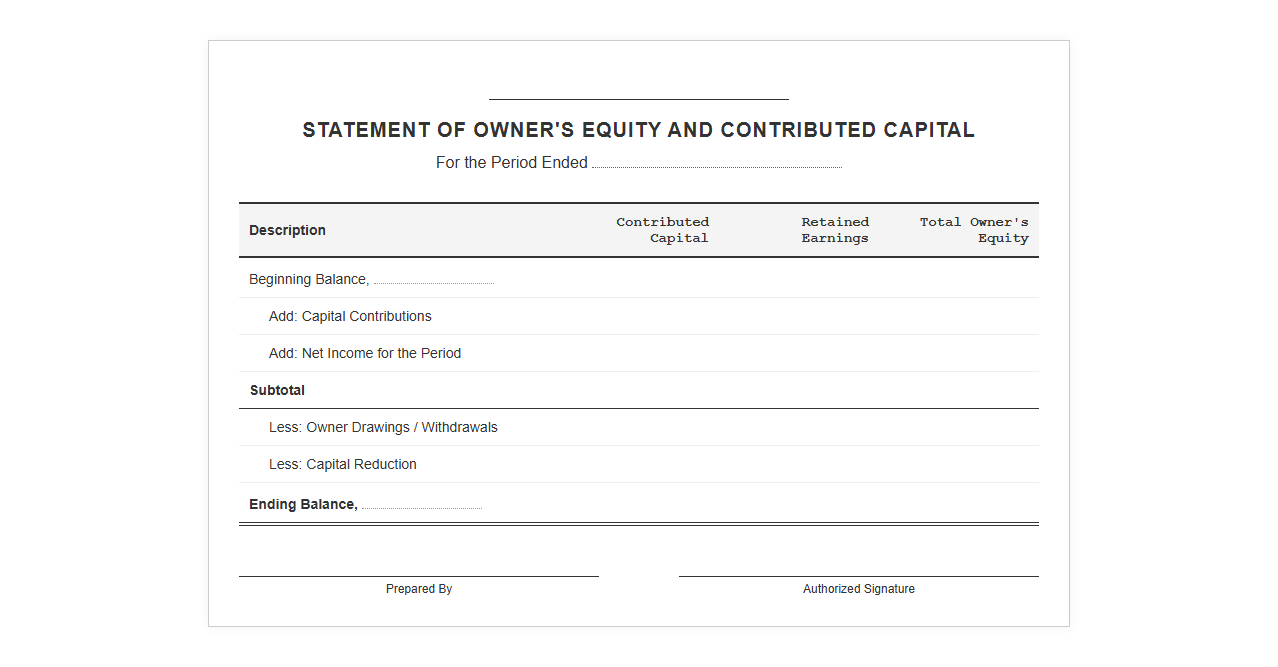

Owner Equity and Contributed Capital Statement

Download: .PDF

Download: .PDF

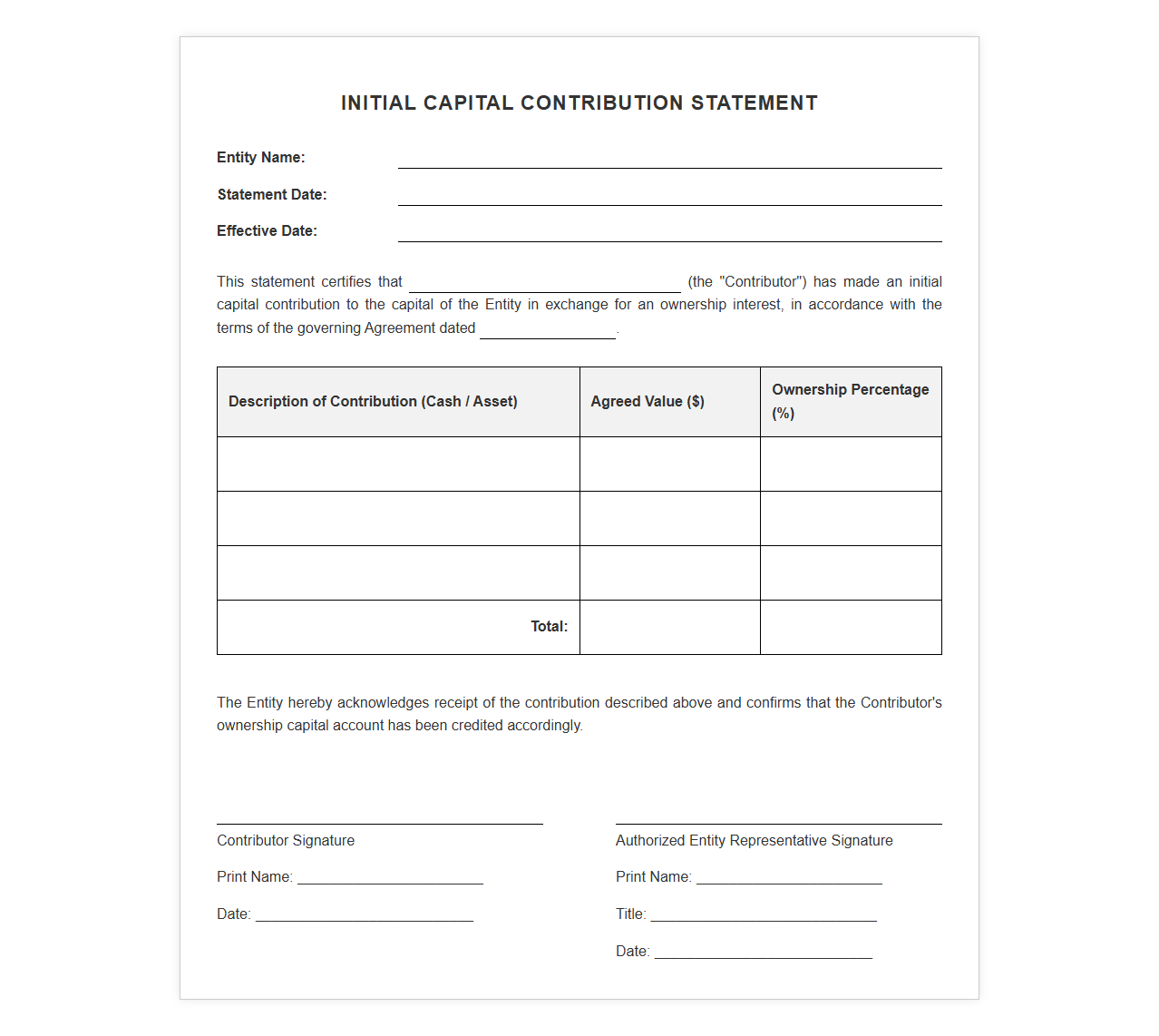

Initial Capital Contribution Statement Template

Download: .PDF

Download: .PDF

Demystifying Contributed Capital: The Foundation of Business Equity

At the core of every financial structure lies contributed capital, the total amount of cash or other assets that shareholders and owners provide to a company in exchange for equity. This initial and ongoing funding represents the primary lifeblood of a starting enterprise, signaling the commitment of its founders and investors. Understanding how this capital behaves is crucial for assessing a business's fundamental financial health, solvency, and operational capacity.

Failing to establish a clean, structured methodology for tracking equity can lead to severe regulatory hurdles and ownership disputes. Transparent equity records ensure that every stakeholder's ownership percentage is accurately preserved and protected. Whether managing a small local venture or positioning a fast-growing startup for venture funding, precise tracking of contributed capital builds the trust necessary to secure external investments and navigate audits successfully.

Equity Dynamics in Sole Proprietorships and Partnerships

In simpler business models, capital tracking behaves differently than in complex corporate structures, reflecting the direct relationship between the owners and the daily operations of the business.

Sole Proprietorship Capital Accounts

For a sole proprietorship, tracking equity is straightforward. All contributed assets are funneled into a single owner's equity account. Because the business and the owner are legally identical, this account fluctuates directly with personal capital injections, net income, and personal withdrawals, often referred to as owner draws.

Partnership Capital and Allocation Agreements

Partnerships introduce collaborative layers that require a more formalized structure to maintain balance among multiple founders.

- Individual Capital Accounts: Each partner has a dedicated capital account recording their unique cash or property contributions.

- Partnership Agreements: Legal documents define the initial valuation of non-cash contributions and dictate how profits, losses, and liquidation assets are distributed.

- Capital Calls: Scheduled or emergency contributions required from partners to sustain operational cash flow during growth phases.

Corporate Structures: Tracking Common and Preferred Stock

Corporations feature highly formalized, regulated methods for managing equity, separating ownership interests into distinct share classes and strict accounting categories.

Understanding Par Value and Additional Paid-In Capital

When a corporation issues shares, the transactions are broken down on the balance sheet to satisfy legal accounting requirements. The par value is the nominal, legal value assigned to each share of stock, which is typically set at a fraction of a cent. Any amount investors pay above this par value is recorded as Additional Paid-In Capital (APIC), reflecting the true market value premium generated during the stock issuance.

Differentiating Common and Preferred Shares

Capital tracking must also distinguish between share classes. Common stock represents basic ownership, granting voting rights and the potential for variable dividends. In contrast, preferred stock acts as a hybrid instrument, offering investors priority claims on dividends and assets during a liquidation event, usually without voting rights. Correctly segregating these pools of capital prevents the dilution of shareholder rights and ensures accurate financial reporting.

LLC Capital Accounts: Managing Member Contributions

Limited Liability Companies combine the flexibility of partnerships with the liability protections of corporations, resulting in a unique framework for tracking equity.

Documenting Initial and Subsequent Capital Contributions

LLC owners, known as members, contribute capital to establish their initial membership interest. These contributions do not rely on share prices but are instead credited directly to individual member capital accounts. If the business requires additional funding later, the operating agreement dictates whether members must contribute more capital or if the LLC will seek external debt.

"The operating agreement serves as the ultimate source of truth for an LLC, clearly outlining how capital contributions correspond to voting percentages and profit distributions, ensuring members cannot arbitrarily change ownership terms."

Template: Standard Statement of Contributed Capital

| Equity Class | Beginning Balance | New Issuances | Ending Balance |

|---|---|---|---|

| Preferred Stock (Par) | $10,000 | $5,000 | $15,000 |

| Common Stock (Par) | $1,000 | $250 | $1,250 |

| Additional Paid-In Capital | $450,000 | $120,000 | $570,000 |

| Total Contributed Capital | $461,000 | $125,250 | $586,250 |

Crucial Pitfalls to Avoid in Equity Accounting

Accurate equity tracking is straightforward in theory but often complicated in practice. Businesses regularly stumble over standard transactions, creating balance sheet errors that can take weeks of forensic accounting to correct.

- Misclassifying Owner Loans as Equity: When an owner injects emergency cash into a business, they must formally document whether the funds are a loan to be repaid or a permanent capital contribution. Mixing these up distorts debt-to-equity ratios and creates tax headaches.

- Neglecting Non-Cash Valuations: Contributing physical assets, intellectual property, or services in exchange for equity requires documented, fair-market valuations. Recording these arbitrarily can lead to immediate audit red flags.

- Failing to Maintain the Stock Ledger: Financial balance sheets and physical stock ledgers must match perfectly. Forgetting to record share transfers or option exercises results in discrepancies that can halt future funding rounds or acquisitions.

Finalizing Your Equity Framework for Long-Term Growth

Establishing a flawless equity framework is an ongoing process that directly impacts your business's valuation, fundraising capabilities, and compliance profile. Regular internal equity audits and systematic reviews of your ledger ensure that your records reflect reality. Consistently maintaining these metrics prepares your organization for the next level of institutional investment or operational scale.

To ensure your corporate documentation aligns with modern accounting standards, consider partnering with certified public accountants and corporate attorneys. For deeper insights on managing corporate structures and regulatory compliance, review our comprehensive guides on financial modeling and business entity management at the Equity Management Hub.

Leave a comment