Valuing intangible assets remains one of the most complex hurdles in modern corporate finance, often leading to protracted audit disputes and balance sheet volatility. Before attempting to quantify these elusive holdings, organizations must first establish a rigorous, standardized reporting framework to ground their assumptions. Utilizing structured valuation statement templates grants finance teams immediate analytical defensibility and reporting precision when presenting figures to auditors and stakeholders.

However, as an educational stipulation, these templates must be viewed as adaptable baselines rather than rigid, universal formulas. For example, documenting the fair value of proprietary software codebases requires entirely different impairment parameters than evaluating acquired brand trademarks. This article outlines specialized statement templates designed for diverse intangible accounts, providing a structural roadmap to streamline your compliance workflows and resolve your toughest valuation challenges.

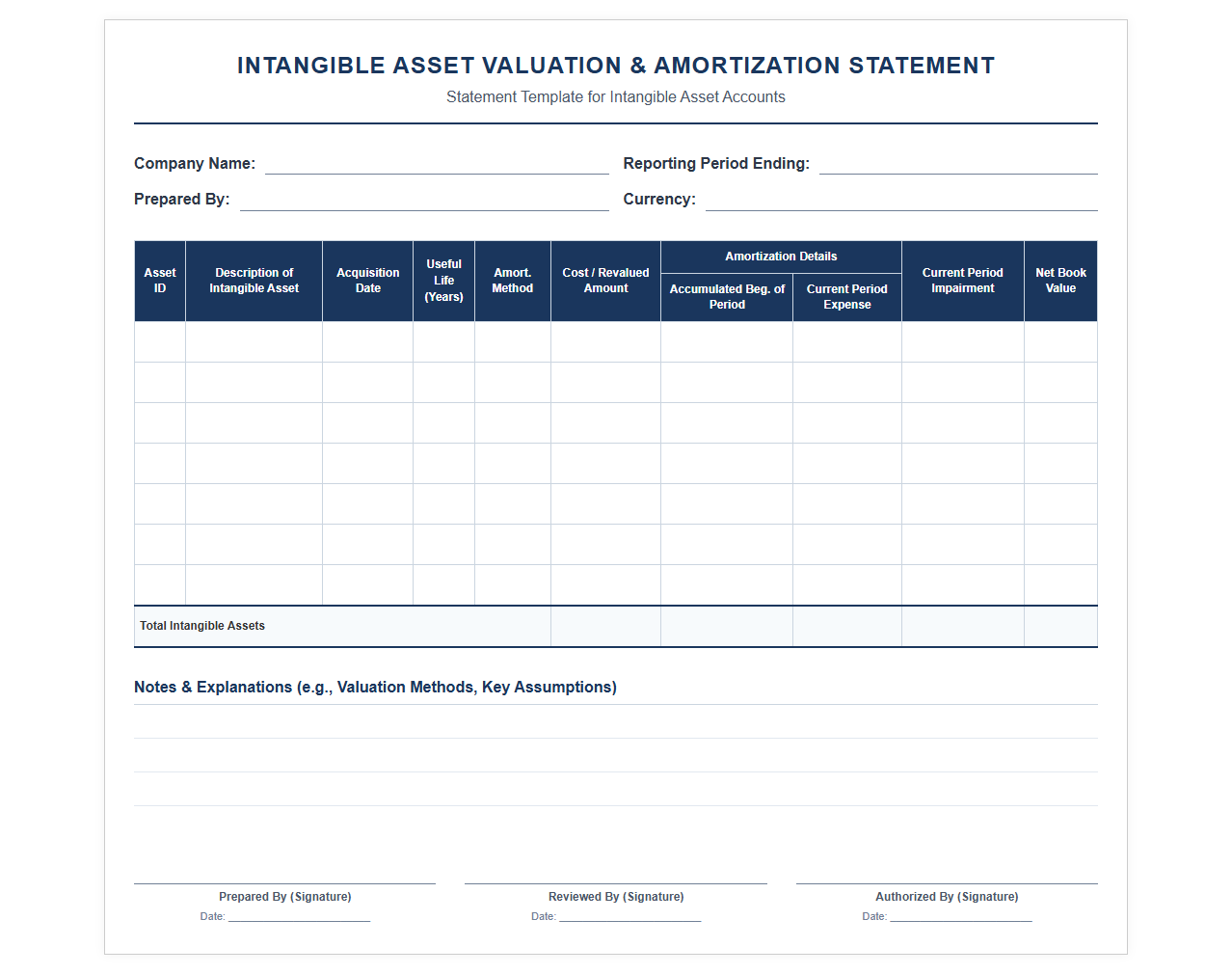

Intangible Asset Valuation and Amortization Statement Template

Download: .PDF

Download: .PDF

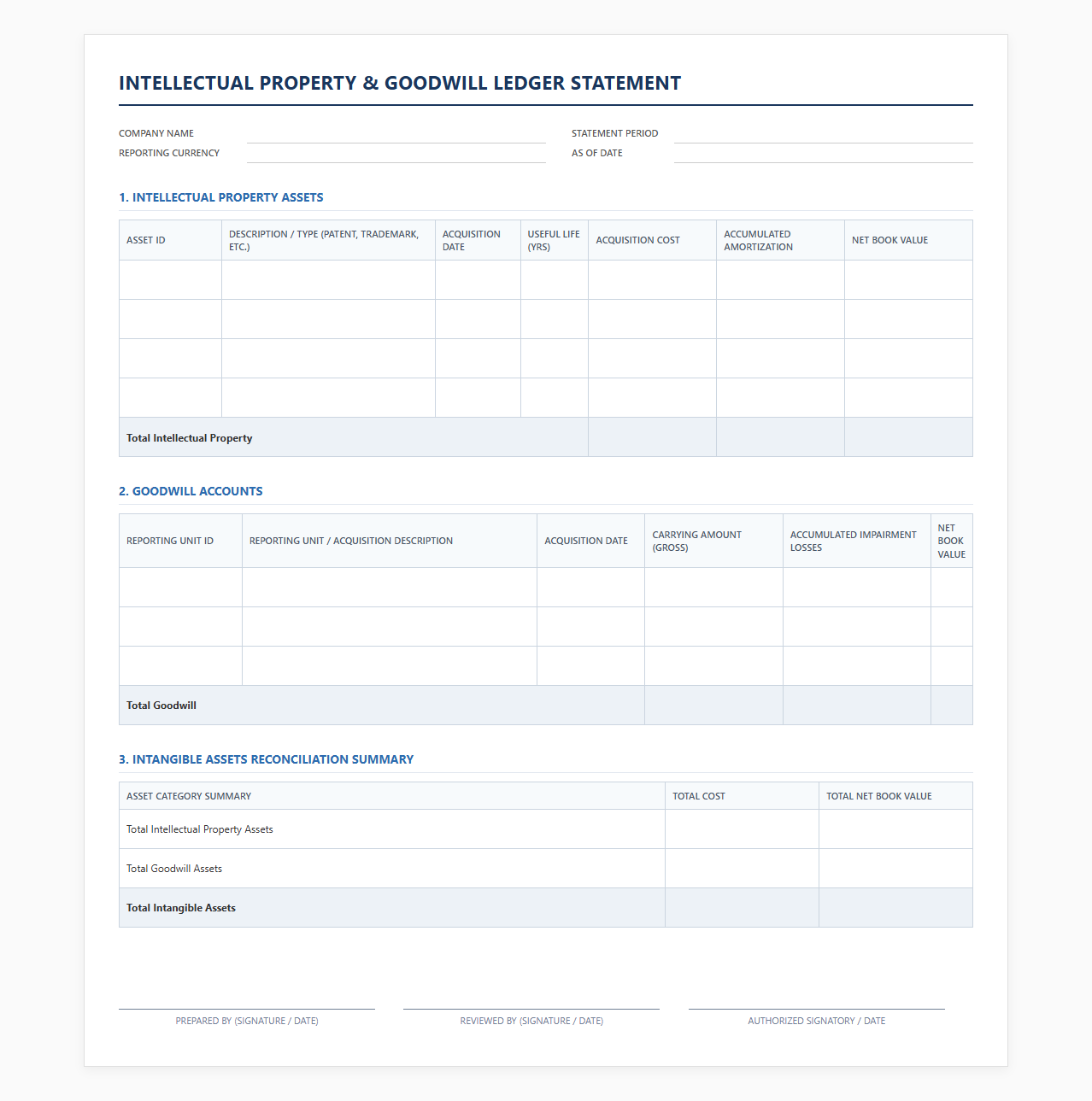

Intellectual Property and Goodwill Ledger Statement Template

Download: .PDF

Download: .PDF

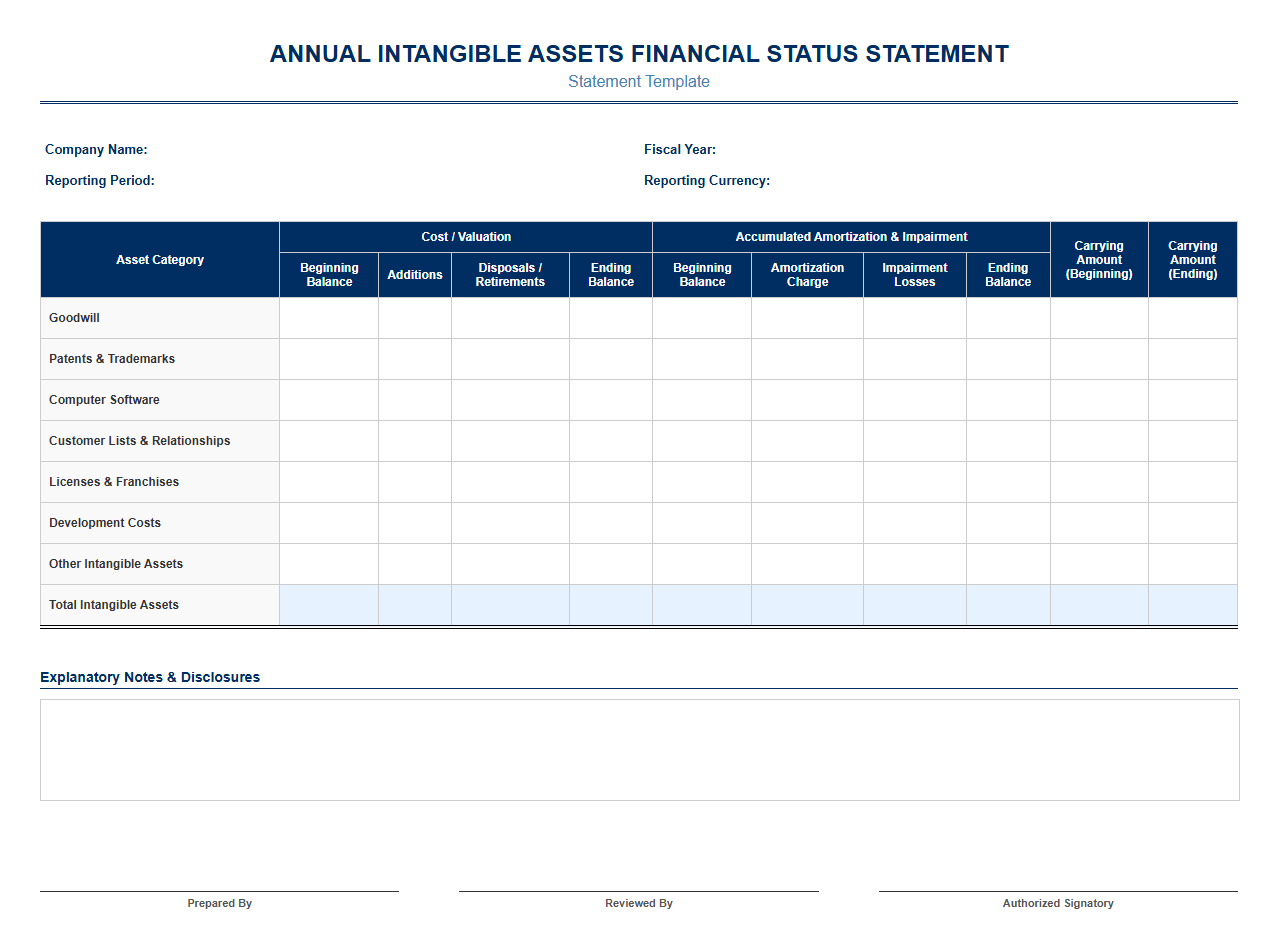

Annual Intangible Assets Financial Status Statement Template

Download: .PDF

Download: .PDF

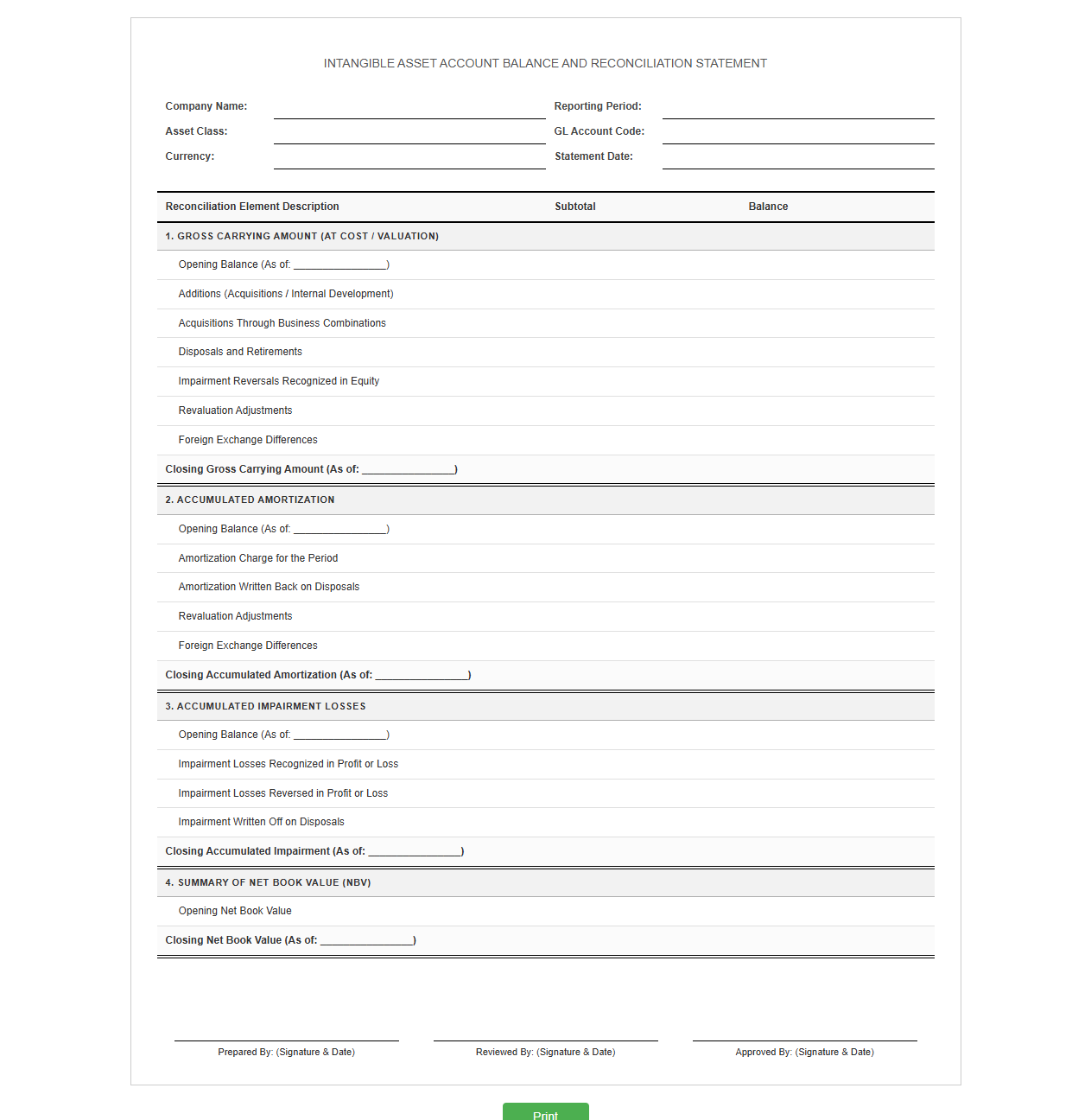

Intangible Asset Account Balance and Reconciliation Statement

Download: .PDF

Download: .PDF

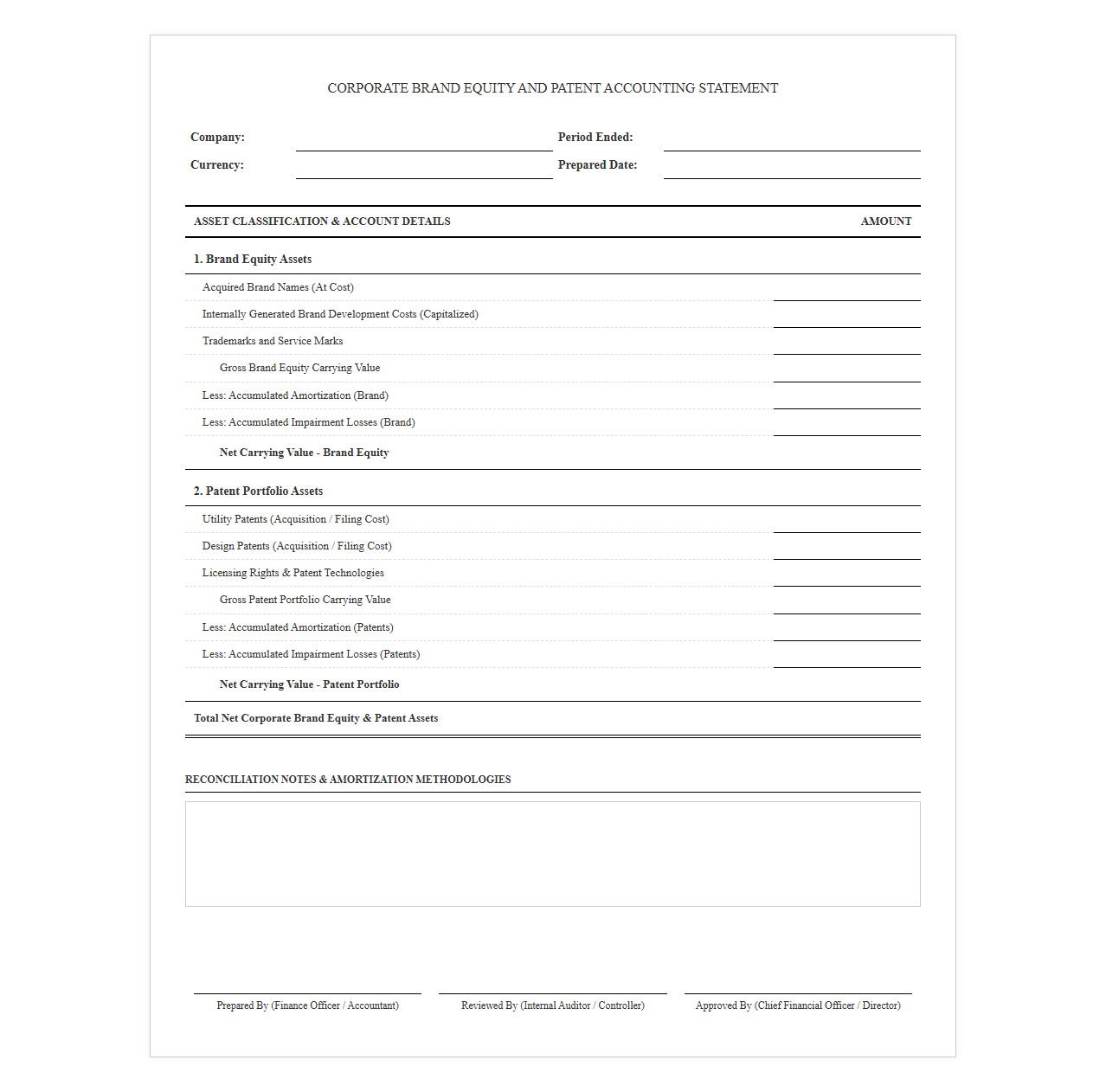

Corporate Brand Equity and Patent Accounting Statement Template

Download: .PDF

Download: .PDF

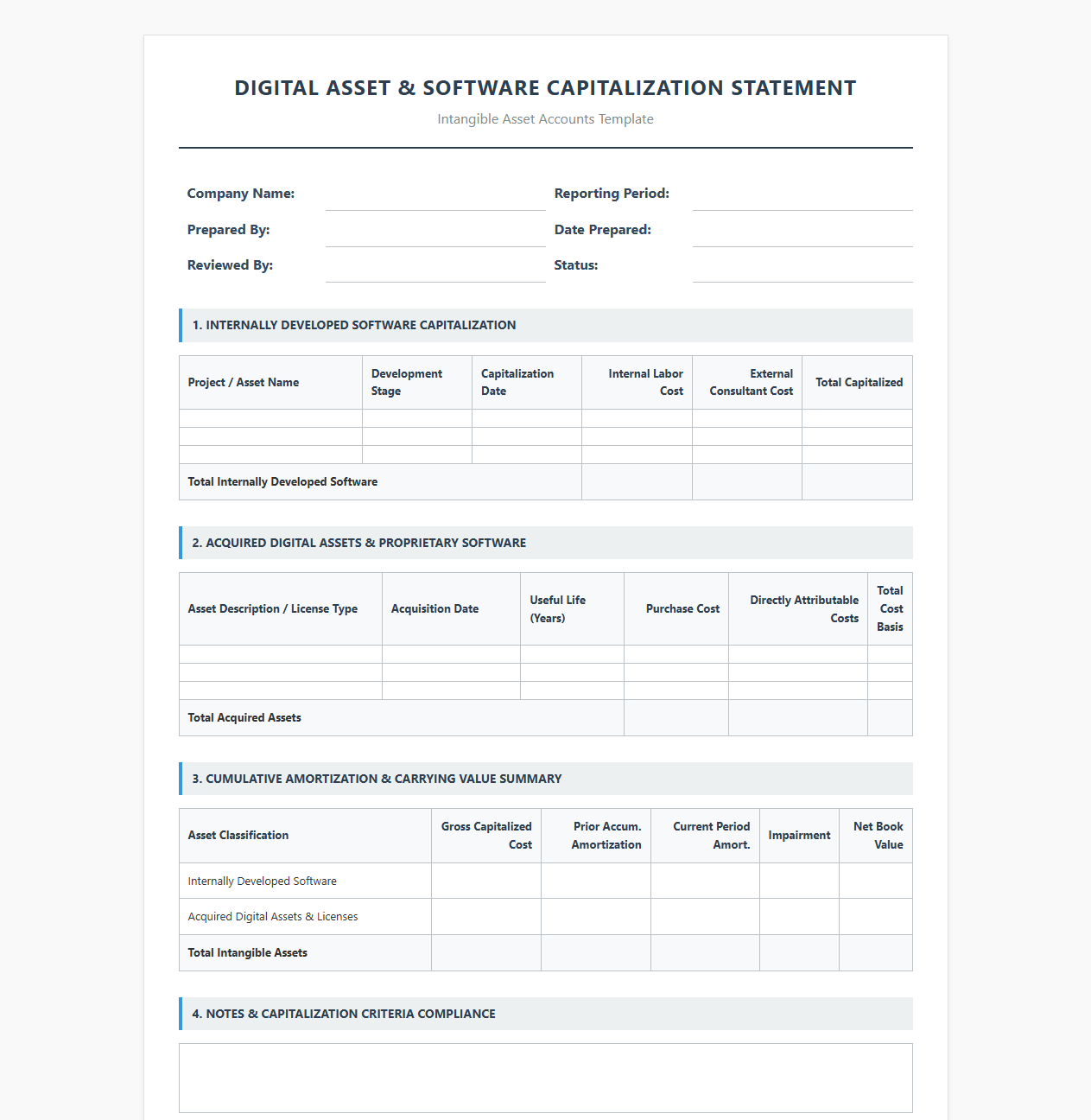

Digital Asset and Software Capitalization Statement Template

Download: .PDF

Download: .PDF

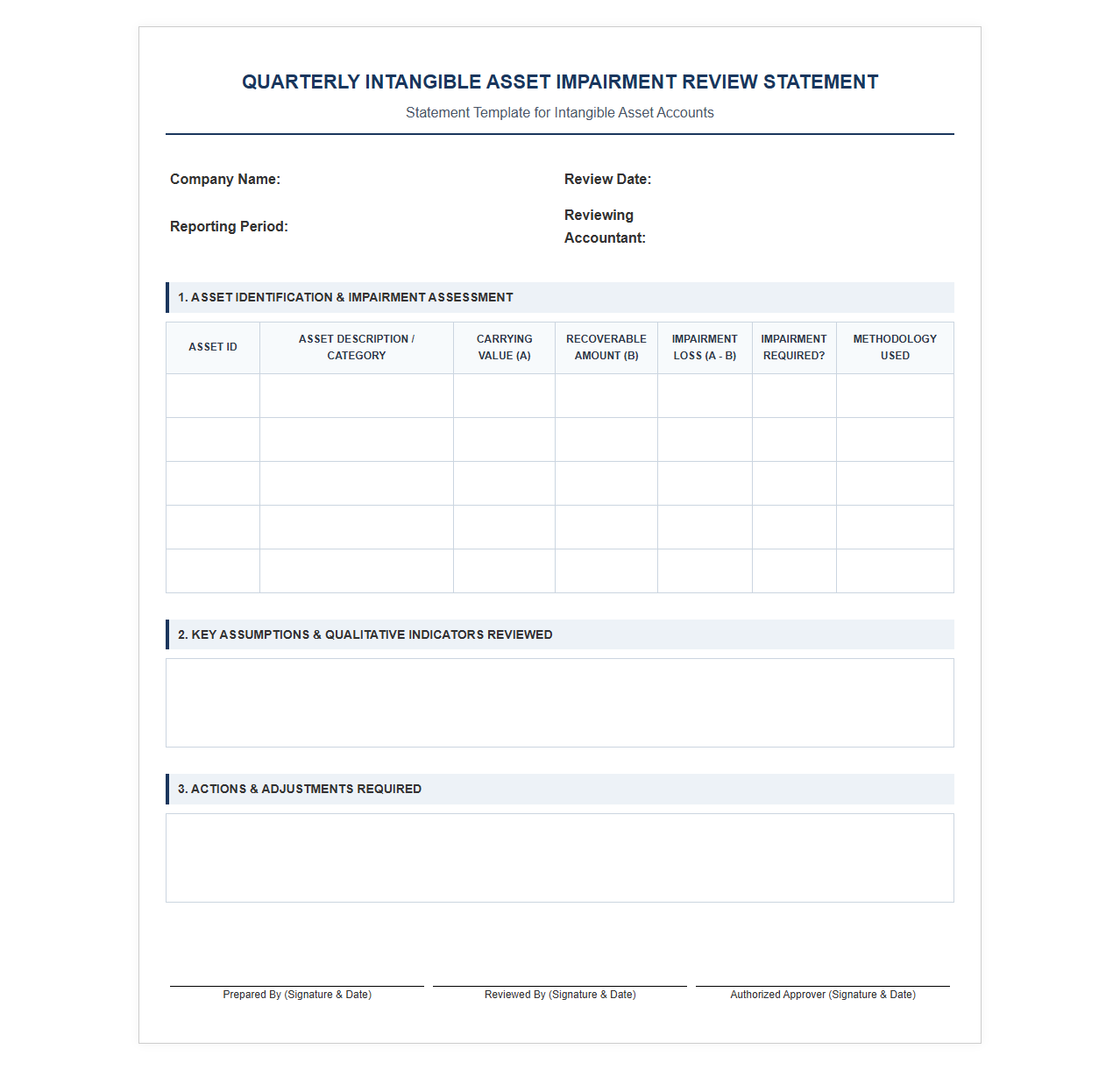

Quarterly Intangible Asset Impairment Review Statement Template

Download: .PDF

Download: .PDF

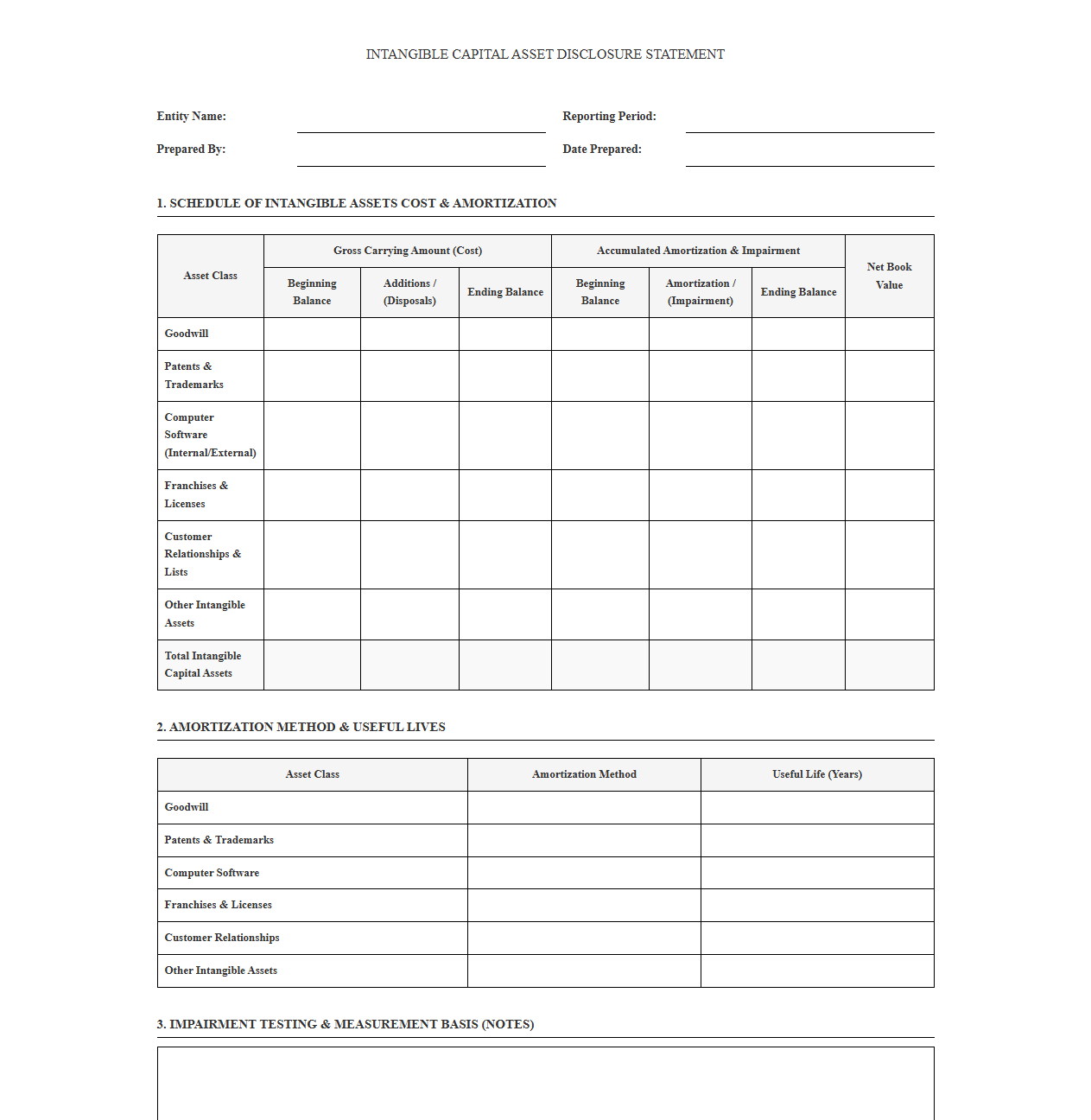

Intangible Capital Asset Disclosure Statement Template

Download: .PDF

Download: .PDF

Introduction to Intangible Asset Valuation Challenges

Valuing intangible assets presents a unique set of challenges for corporate accountants, as these non-physical assets lack active public markets and clear pricing benchmarks. To maintain financial accuracy during major corporate transitions, organizations must rely on standardized statement templates that ground subjective projections in verifiable methodologies. Adhering to rigorous frameworks established under ASC 350 and IAS 38 ensures that valuations are consistent, defensible, and reflective of true economic realities.

Intellectual Property and Patent Valuations

Template for Intellectual Property and Patent Accounts

During mergers and acquisitions, resolving disputes over the valuation of active patents and proprietary technology requires a structured, contractually binding framework. The following template establishes a clear resolution pathway based on independent expert determination and defined valuation parameters.

[Patent Valuation Dispute Resolution Template]

1. Disputing Parties: [Acquiring Entity] & [Target Entity]

2. Subject Asset: Patent Registration No. [Number] / [Proprietary Technology Name]

3. Agreed Valuation Methodology: Income Approach (Relief-from-Royalty Method)

4. Escalation Protocol: If internal valuation teams diverge by more than [X]%, an independent third-party valuator certified by the ASA shall be appointed.

5. Binding Verdict: The third-party valuation will serve as the final fair value for the closing balance sheet.

Brand Equity and Trademark Adjustments

Statement Frameworks for Brand Equity and Trademarks

Sudden market shifts, such as reputational crises or technological disruptions, can severely depress the fair value of recognized brand names. The statement template below is designed to record and justify adjustments to brand equity carrying values to ensure compliance with periodic reporting standards.

====================================================================

TRADEMARK FAIR VALUE ADJUSTMENT DISCLOSURE TEMPLATE

====================================================================

Reporting Period: [Quarter/Year]

Asset Description: [Trademark Portfolio / Brand Name]

Original Carrying Value: $[Amount]

Adjusted Fair Value: $[Amount]

Impairment Loss Recognized: $[Amount]

Triggering Event Analysis:

[Insert brief narrative detailing the specific market shift or economic

event that necessitated the reassessment of the brand's cash flows.]

Valuation Inputs:

- Selected Discount Rate: [X]%

- Long-term Growth Rate Adjustment: [X]%

====================================================================

Goodwill Impairment Methodology

Addressing Goodwill Impairment Testing Discrepancies

When annual impairment testing reveals conflicting valuation inputs between internal management and external auditors, a standardized disclosure framework is necessary to reconcile the differences. This methodology ensures all critical assumptions are transparently documented and weighted.

- Reporting Unit Identification: Specification of the cash-generating unit (CGU) under review.

- Discount Rate Discrepancy Margin: Documentation of the variance between the weighted average cost of capital (WACC) inputs.

- Long-term Growth Assumptions: Comparative analysis of management's terminal growth rates versus market indicators.

- Reconciliation Settlement: The final agreed-upon impairment charge based on a weighted sensitivity analysis matrix.

Customer-Related Intangibles

Valuing Customer Relationships and Contractual Agreements

During a business combination, customer lists and contractual relationships must be capitalized based on their projected economic life. This template provides a structured table format to reconcile valuation adjustments driven by changes in historical customer churn rates.

| Asset Description | Initial Value ($) | Original Churn Rate (%) | Adjusted Churn Rate (%) | Adjusted Fair Value ($) |

|---|---|---|---|---|

| Enterprise Contract Portfolio | 5,000,000 | 8.0% | 12.5% | 4,100,000 |

| Direct Consumer Database | 1,200,000 | 15.0% | 18.0% | 950,000 |

Software and Digital Asset Valuation

Capitalized Software and Digital Asset Adjustments

Internal-use software platforms require frequent re-evaluation of their remaining useful life due to rapid technological obsolescence. This guidelines framework helps accounting departments adjust amortization schedules to match actual operational utility.

Regulatory Compliance Reminder: Under GAAP and IFRS, any significant reduction in the expected useful life of capitalized software must trigger an immediate review for impairment before updating the prospective amortization schedule.

Implementation Best Practices for Valuation Compliance

Integrating these standardized templates into corporate accounting workflows ensures that the organization remains prepared for rigorous external audits. Consistent application of these frameworks reduces the risk of material misstatements and regulatory non-compliance.

- Embed the templates directly into the enterprise resource planning (ERP) system to automate standard inputs.

- Conduct bi-annual training sessions for finance personnel on the application of the impairment methodologies.

- Archive all supporting market data and third-party appraisal reports alongside the completed templates.

- Perform pre-audit reviews of all adjusted intangible asset schedules with the internal audit committee.

Leave a comment