Accounting departments frequently struggle to accurately isolate and report cash flows from investing activities, where minor classification errors can quickly distort a company's true liquidity profile. Before addressing this complexity, it is critical to understand how these transactions interface with non-current asset reconciliations under GAAP and IFRS standards. Utilizing structured templates to organize these movements offers an immediate advantage: it dramatically reduces year-end audit risks while accelerating monthly close cycles.

However, while standardized frameworks streamline the reporting process, users must recognize that templates serve as a foundation rather than a substitute for professional accounting judgment. For example, distinguishing cash paid for property, plant, and equipment (PP&E) from proceeds generated by the mature sale of debt securities requires precise transactional mapping.

In this guide, we will break down the essential components of the investing activities section, provide customizable templates for immediate deployment, and explore best practices for error-free financial reporting.

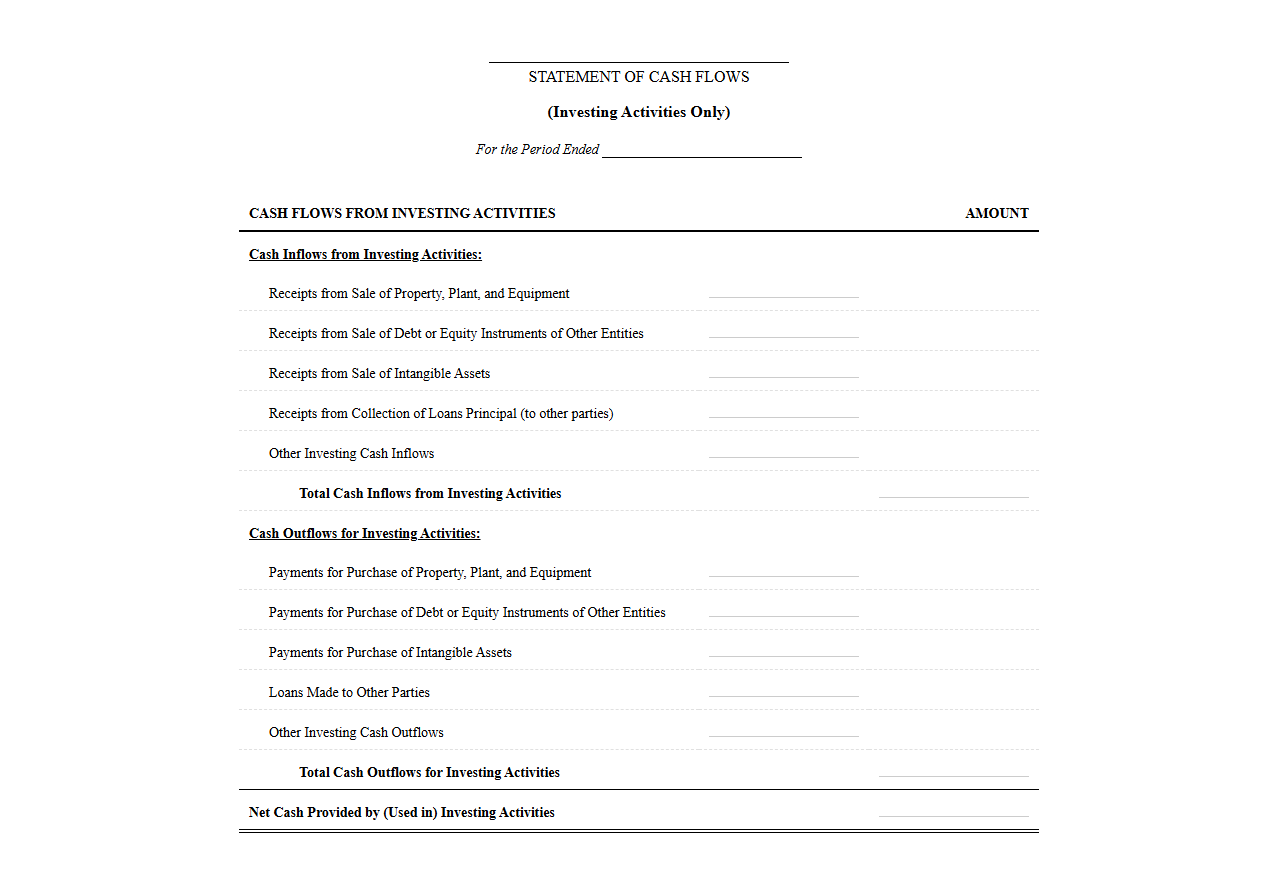

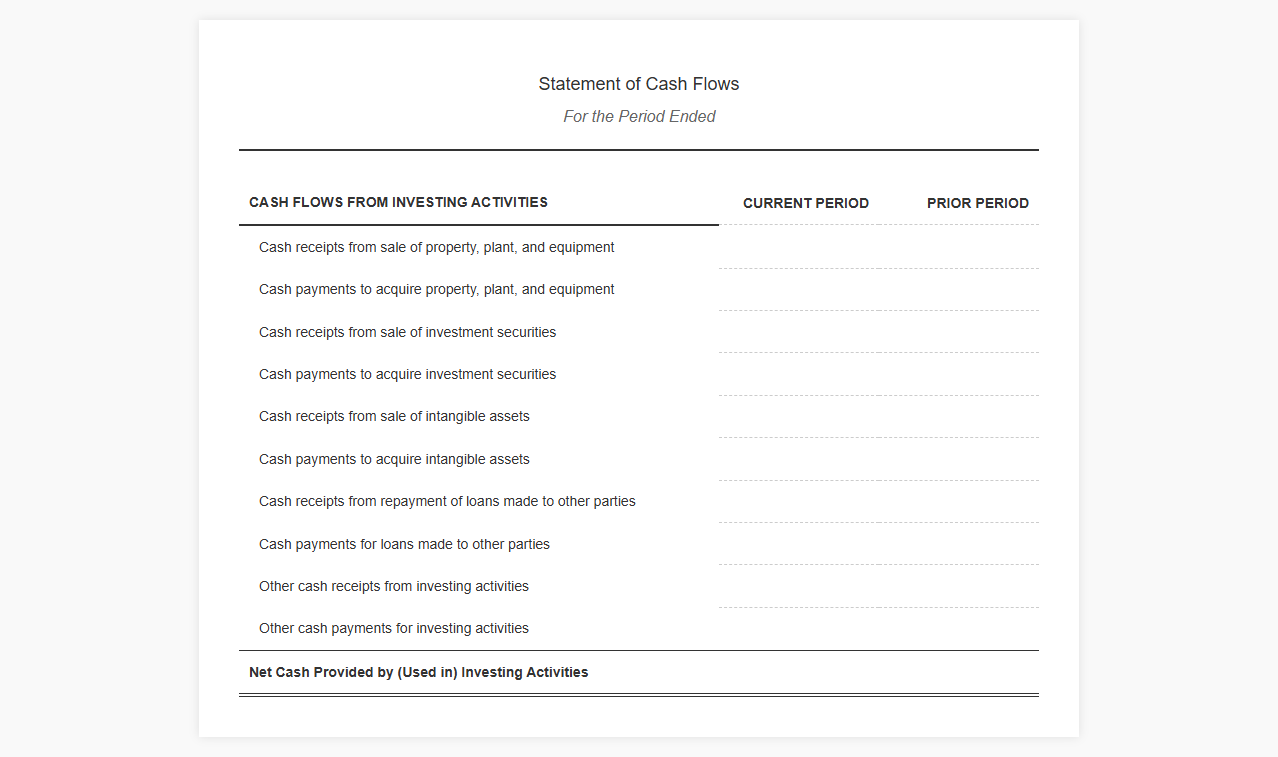

Investing Activities Cash Flow Statement Template

Download: .PDF

Download: .PDF

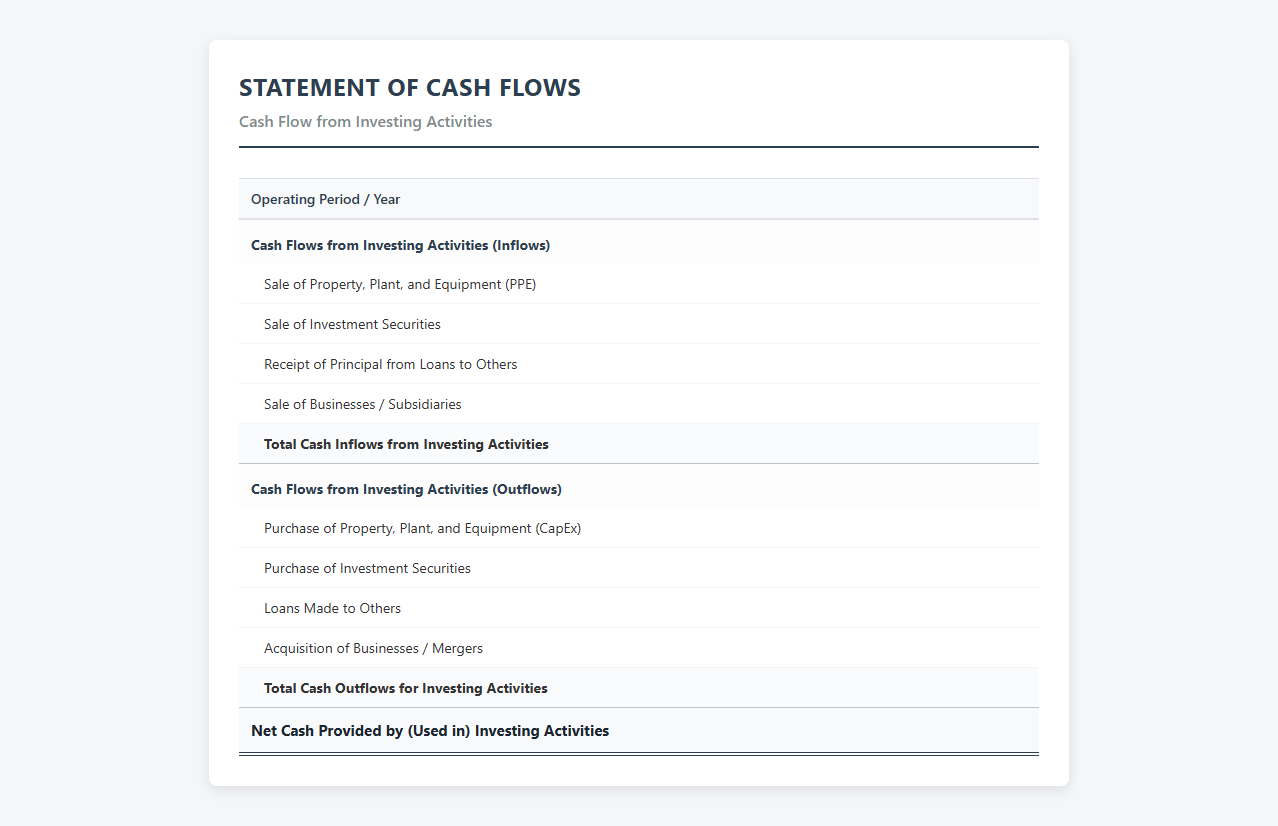

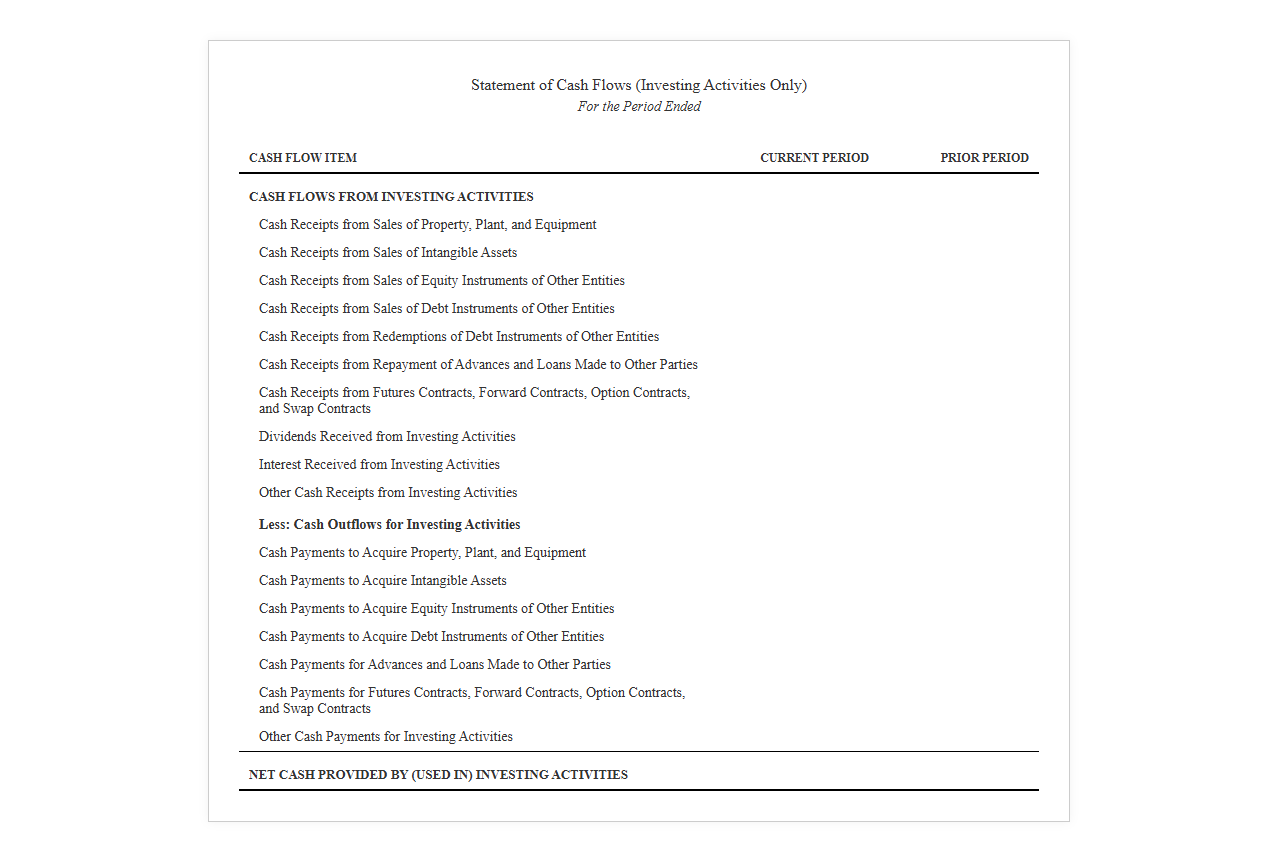

Cash Flow from Investing Activities Spreadsheet Template

Download: .PDF

Download: .PDF

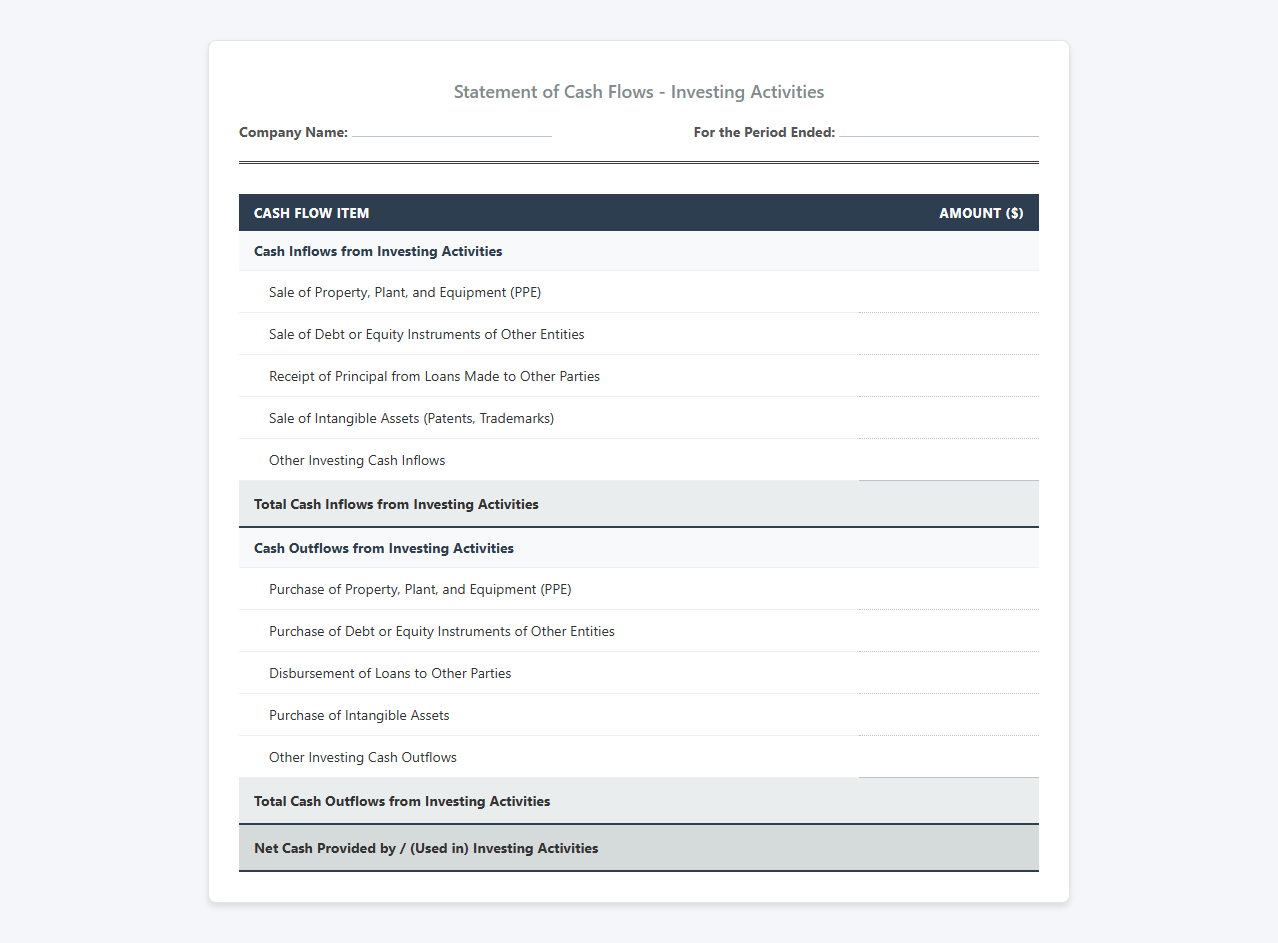

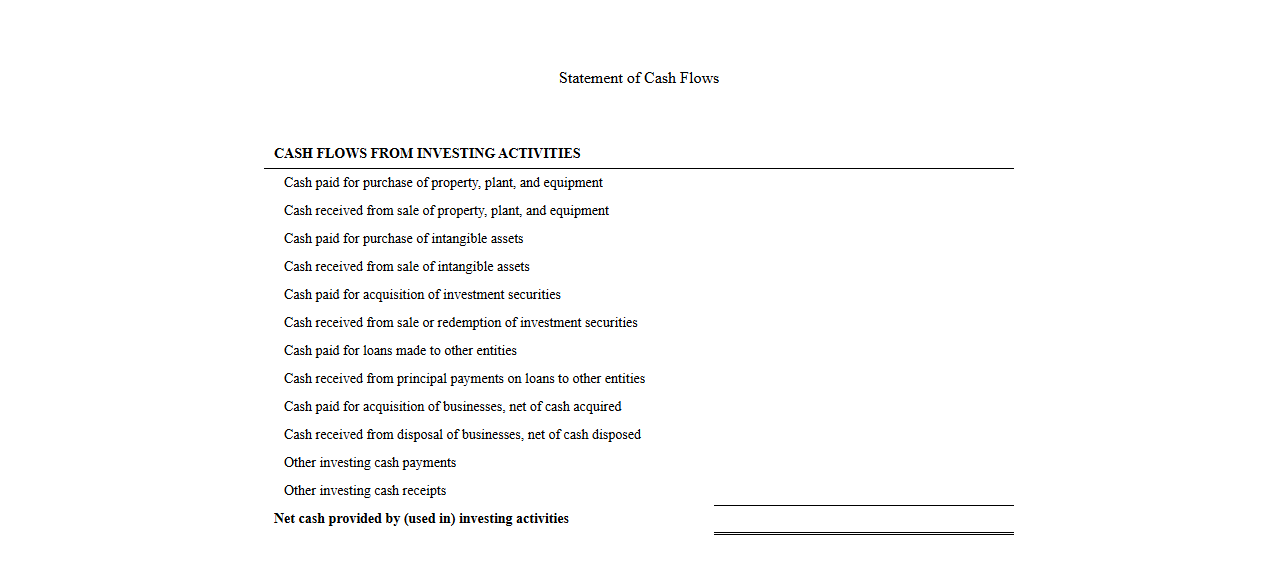

Investment Cash Flow Statement Excel Template

Download: .PDF

Download: .PDF

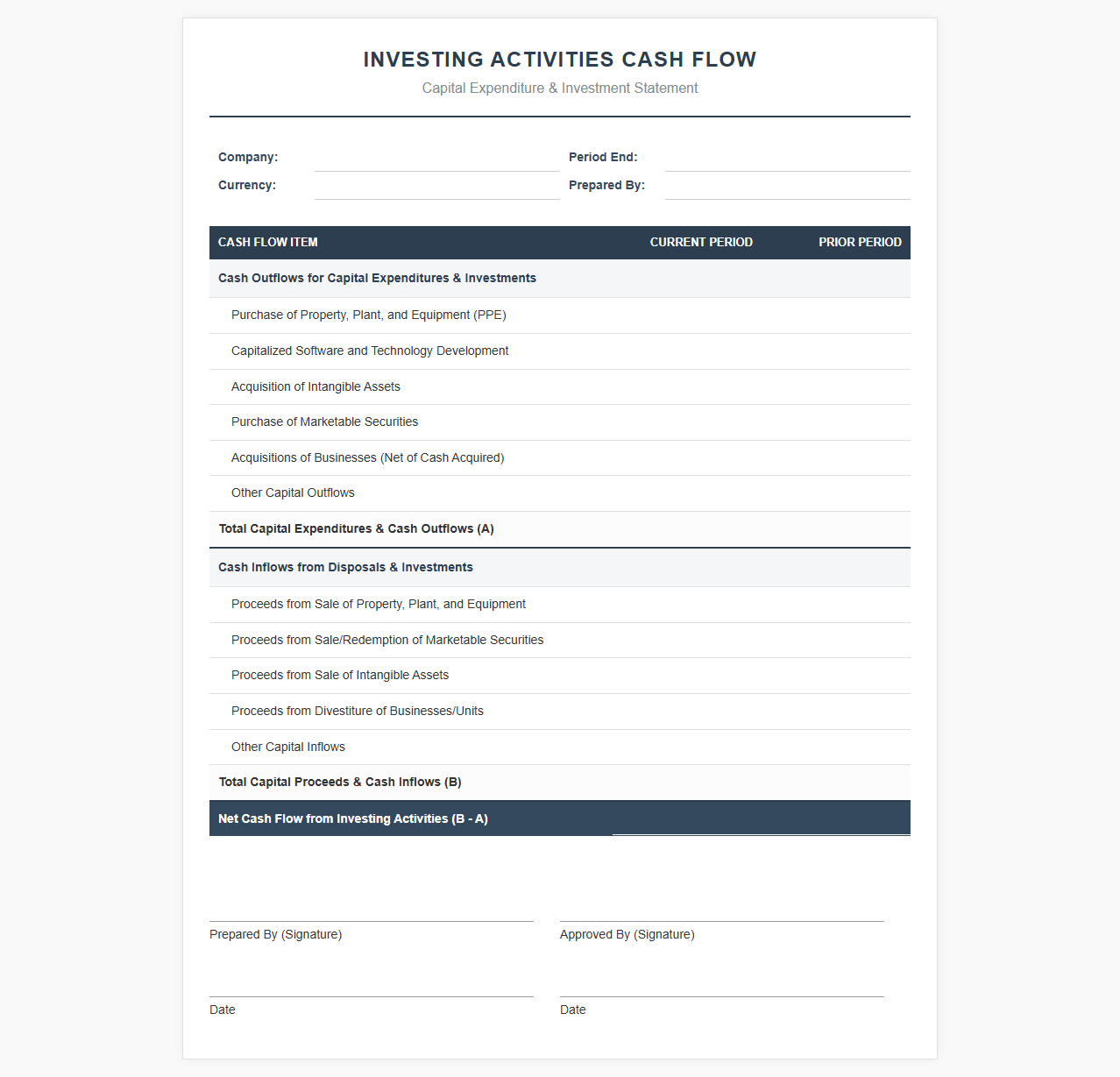

Capital Expenditure and Investment Cash Flow Template

Download: .PDF

Download: .PDF

Cash Flows from Investing Activities Reporting Template

Download: .PDF

Download: .PDF

Investing Cash Flow Statement Format

Download: .PDF

Download: .PDF

Statement of Cash Flows Investing Activities Template

Download: .PDF

Download: .PDF

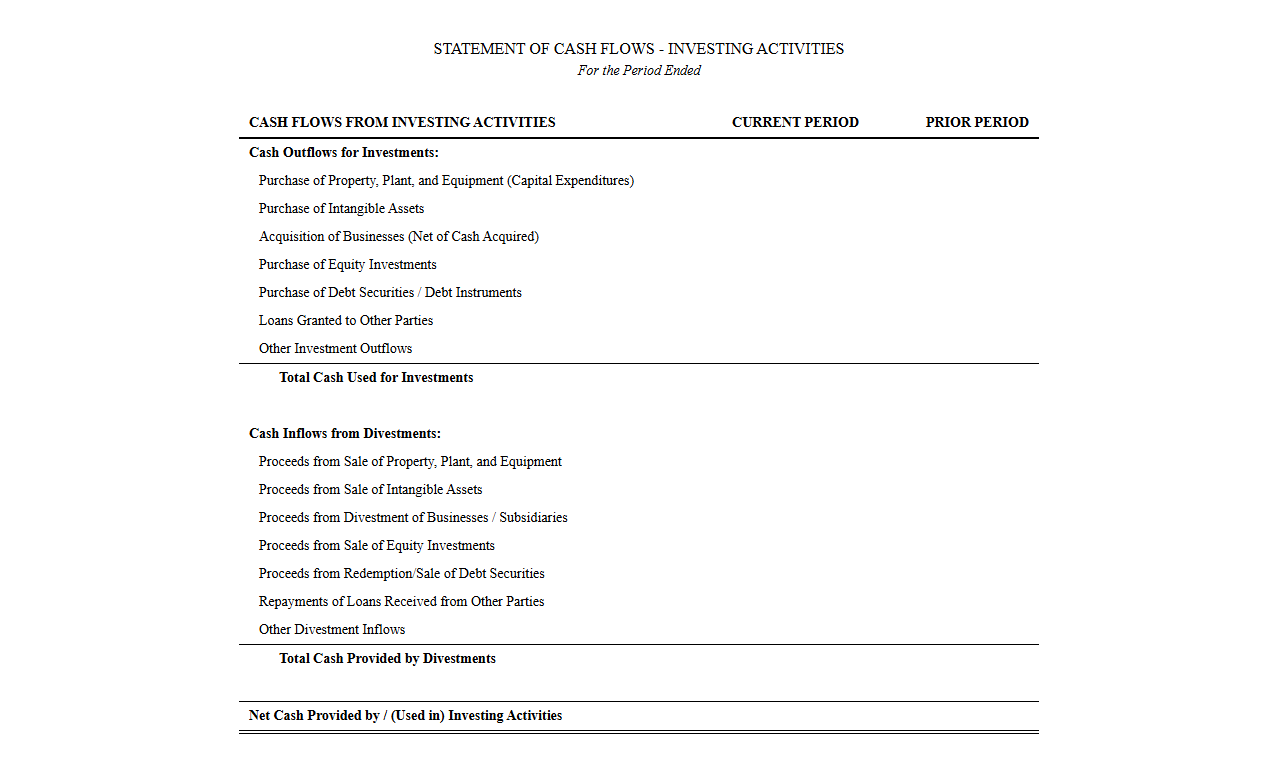

Investment and Divestment Cash Flow Template

Download: .PDF

Download: .PDF

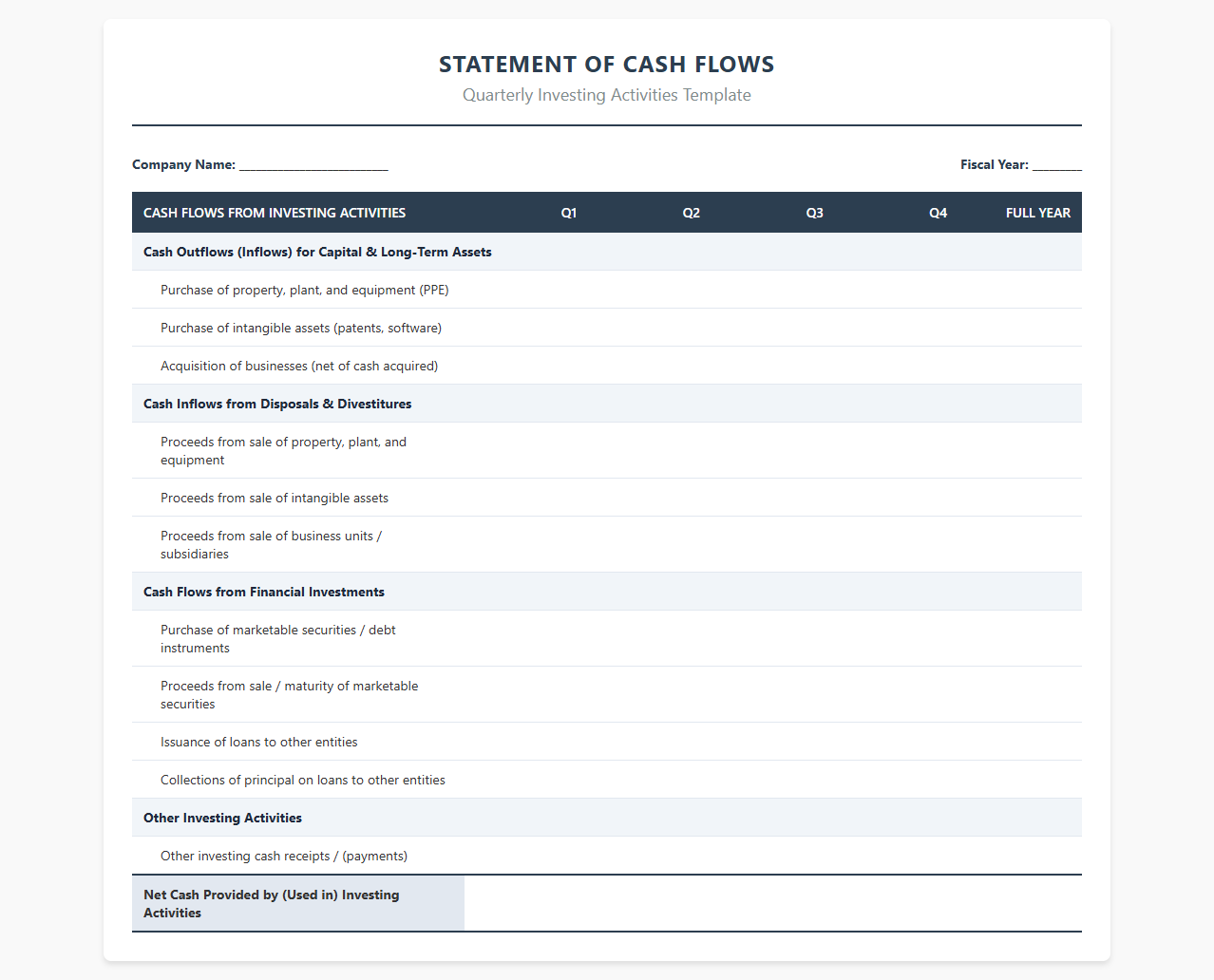

Quarterly Investing Activities Cash Flow Template

Download: .PDF

Download: .PDF

Introduction to Cash Flow from Investing Activities

The cash flow statement is a critical financial document that provides a transparent view of an organization's liquidity and cash management. Among its core divisions, the investing activities section serves as a key indicator of a company's long-term growth strategy. This section details the acquisition and disposal of long-term assets and other investments, reflecting how much capital is being allocated to sustain and expand operations.

For investors, analysts, and internal stakeholders, monitoring these transactions is vital. It reveals whether a business is actively investing in its future through capital expenditures, or conversely, if it is downsizing by liquidating assets to maintain short-term solvency. Proper reporting within this category ensures a realistic valuation of corporate health and strategic direction.

Core Components of Investing Cash Flows

Investing activities primarily encompass transactions involving long-term assets. These transactions directly influence the productive capacity of the business and are generally categorized into three primary areas:

- Capital Expenditures (CapEx): Funds used by a company to acquire, upgrade, and maintain physical assets such as property, plants, buildings, technology, or equipment.

- Acquisitions and Mergers: Cash spent to acquire other businesses, joint ventures, or equity stakes in external entities to foster strategic expansion.

- Sale of Long-Term Assets: Cash inflows generated from disposing of property, plant, and equipment (PP&E), or selling off investment securities.

Cash Inflows vs. Cash Outflows Comparison

| Transaction Type | Cash Inflow (Source of Cash) | Cash Outflow (Use of Cash) |

|---|---|---|

| Property, Plant & Equipment (PP&E) | Cash received from selling old machinery or real estate. | Cash paid to purchase new manufacturing equipment or land. |

| Marketable Securities | Cash received from redemption or sale of debt/equity instruments. | Cash spent buying stocks, bonds, or mutual funds. |

| Business Divestitures / Acquisitions | Cash proceeds from selling a subsidiary or business unit. | Cash outflow for acquiring another company or business line. |

| Loans Made to Other Entities | Principal payments received from borrowers. | Capital advanced to third parties as loans. |

Step-by-Step Reporting Template

To calculate and present the net cash provided by or used in investing activities, accountants follow a structured chronological process. Below is the standard reporting template:

- Identify all cash inflows from the sale of non-current assets and investment securities during the accounting period.

- Identify all cash outflows dedicated to purchasing property, plant, equipment, and intangible assets.

- Record cash outflows related to corporate acquisitions, purchase of debt, or equity instruments of other entities.

- Aggregate all cash inflows from investing activities to establish total cash generated.

- Aggregate all cash outflows from investing activities to establish total cash spent.

- Subtract total outflows from total inflows to calculate the "Net Cash Provided by (Used in) Investing Activities."

Crucial Distinctions: Non-Cash Investing Activities

A common error in financial preparation is the inclusion of non-cash transactions directly in the cash flow statement. Because the statement of cash flows is strictly designed to track the physical movement of currency, transactions that do not involve actual cash exchanges must be excluded from this section.

Best Practices for Financial Accuracy

- Balance Sheet Reconciliation

- Verify that changes in non-current asset accounts on the comparative balance sheets align exactly with the transactions reported in the investing section.

- General Ledger Cross-Referencing

- Audit the general ledger accounts for equipment, land, and marketable securities to confirm that non-cash adjustments, like depreciation or asset write-offs, are isolated from pure cash transactions.

- Capital Expenditures Tracking

- Cross-verify purchase invoices and bank statements against Capital Expenditures ledgers to ensure capitalized interest and unpaid liabilities are adjusted out of the cash total.

Finalizing and Integrating the Statement

Once the investing activities section is reconciled, it must be integrated with the operating and financing sections to construct the complete cash flow statement. The combined net cash flows from these three categories, when added to the beginning cash balance, must match the ending cash and cash equivalents reported on the balance sheet.

Before publishing the financial reports, ensure that the following final compliance steps are complete: Verify that all non-cash disclosures are appended as footnotes, cross-check the net investing cash flow against the statement of changes in equity, and confirm that net totals align seamlessly with the general ledger balances. This systematic alignment ensures regulatory compliance and provides stakeholders with a dependable view of the company's financial state.

Leave a comment