Corporate finance teams frequently struggle with the complex, manual process of reporting non-controlling interests, where even minor disclosure errors can trigger regulatory scrutiny and delay audits. Before addressing how to streamline this reporting, we must consider the evolving landscape of modern GAAP and IFRS equity disclosure mandates, which demand unprecedented transparency from parent entities.

Implementing standardized statement templates grants reporting teams both rigorous audit-readiness and significant time savings. Please note, however, that while these templates establish a robust baseline, they must be tailored to your firm's specific jurisdictional and organizational requirements.

By utilizing concrete examples-such as detailed equity attribution tables and non-controlling interest (NCI) roll-forward schedules-this article demonstrates how to standardize complex disclosures. Below, we will explore the core challenges of minority interest reporting, deliver customizable templates, and outline best practices for seamless integration into your financial statements.

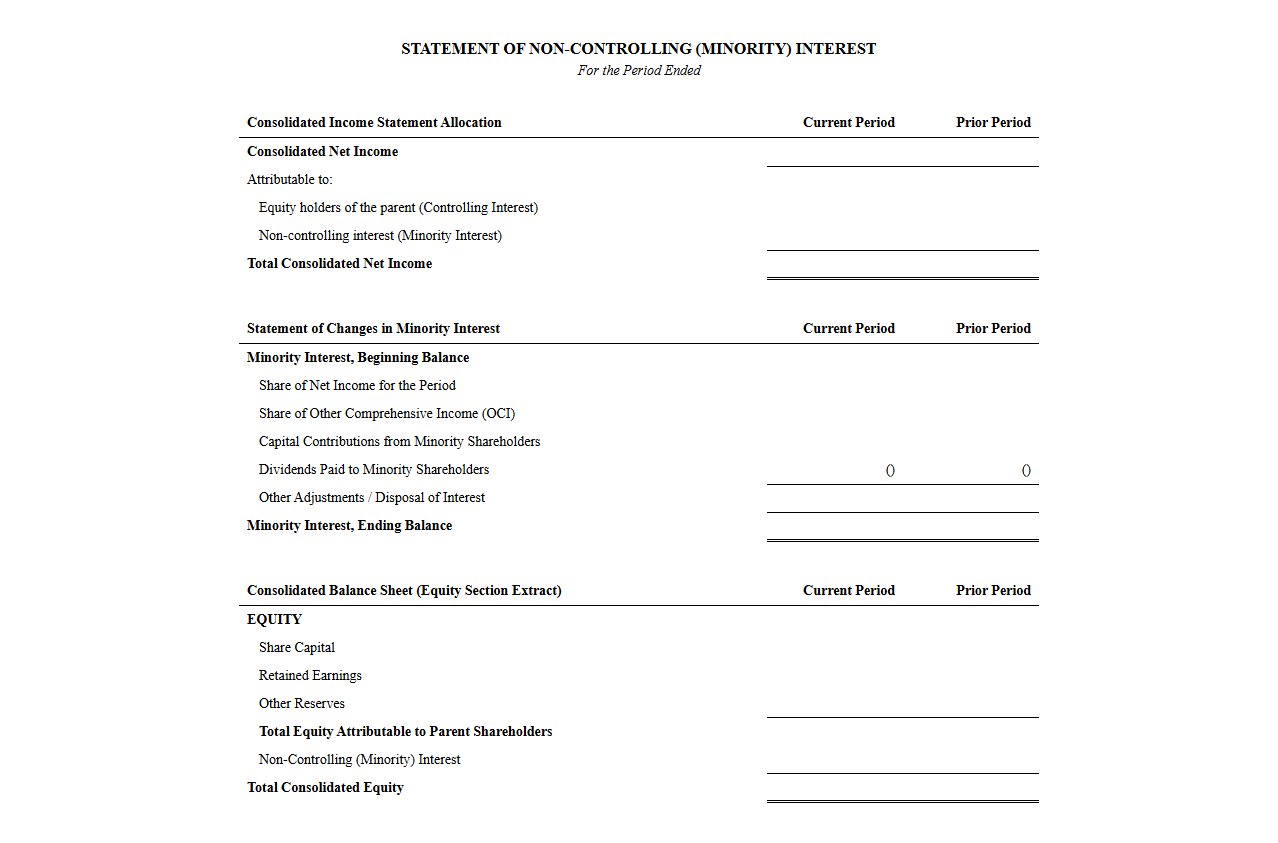

Minority Interest Financial Statement Template

Download: .PDF

Download: .PDF

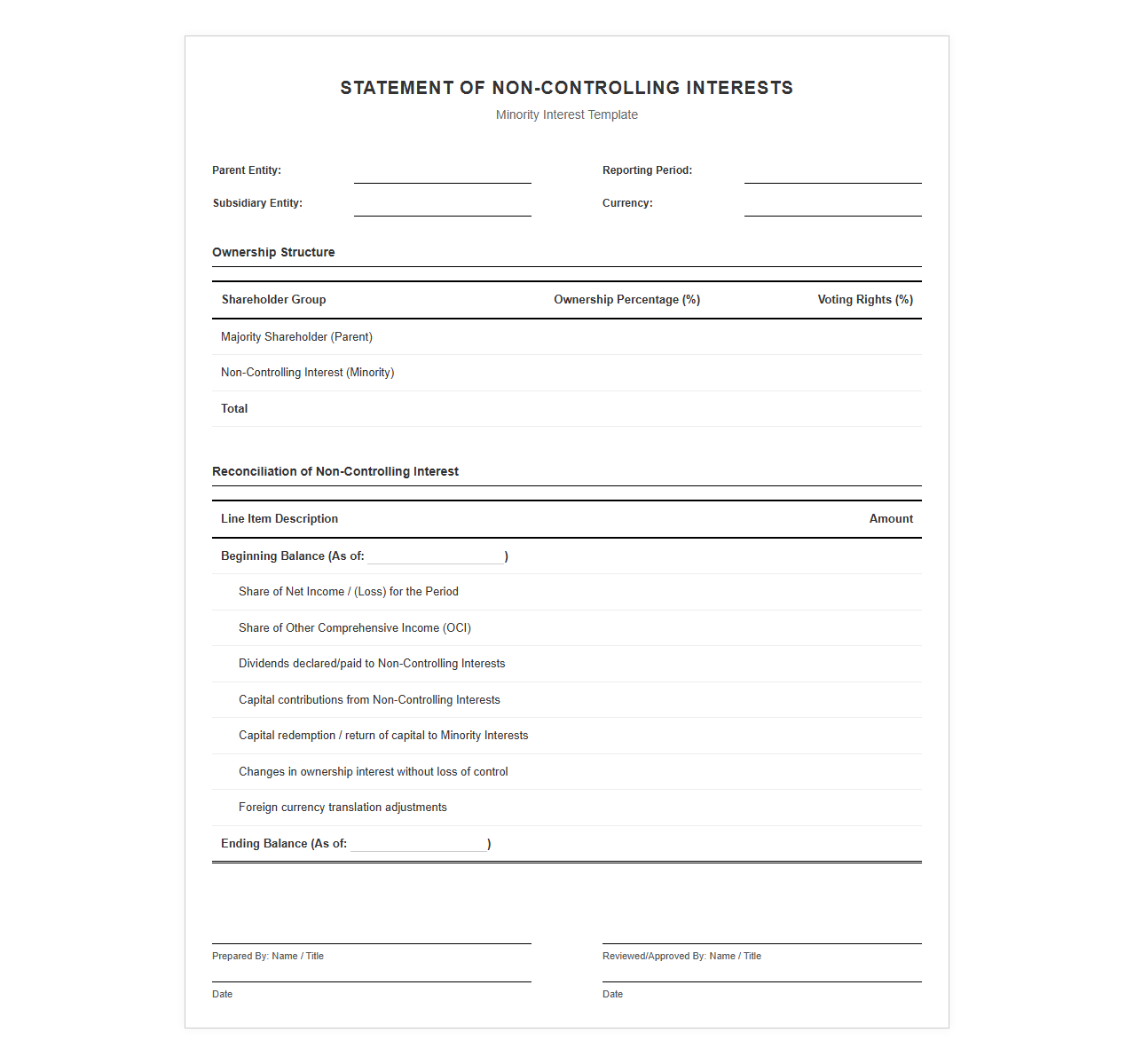

Non-Controlling Interest Statement Form

Download: .PDF

Download: .PDF

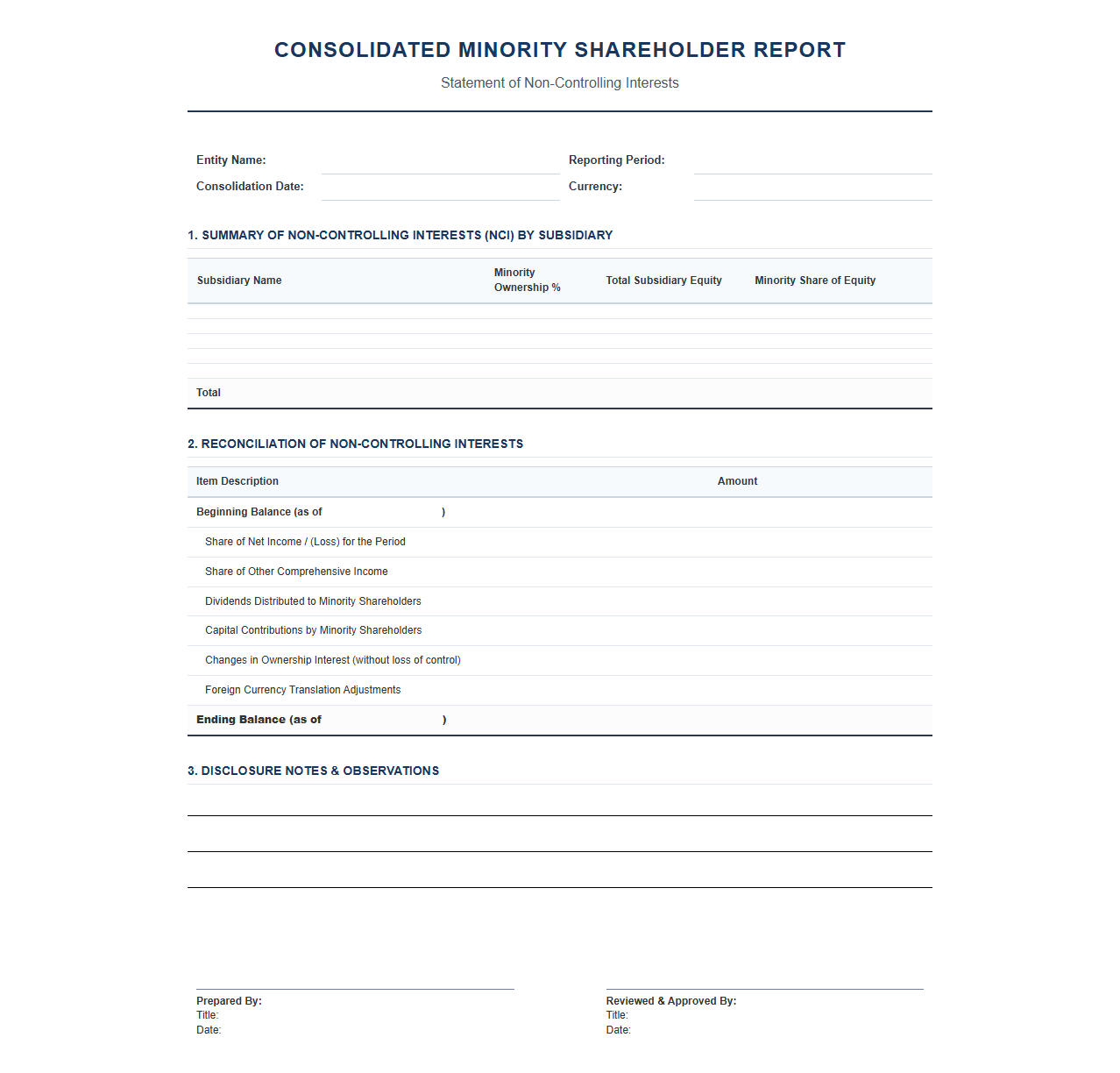

Consolidated Minority Shareholder Report Template

Download: .PDF

Download: .PDF

Equity Valuation Statement for Minority Interests

Download: .PDF

Download: .PDF

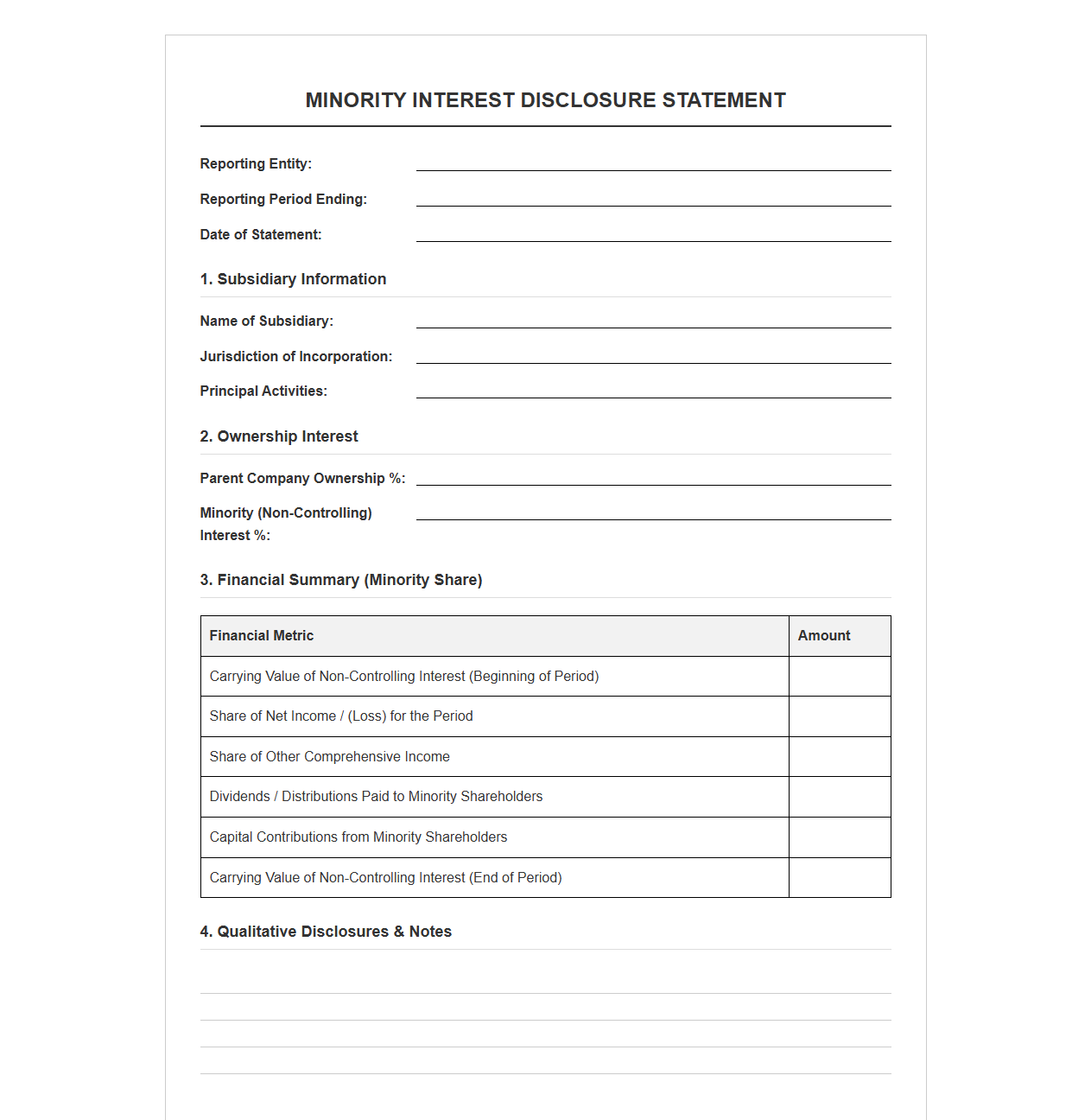

Minority Interest Disclosure Statement Template

Download: .PDF

Download: .PDF

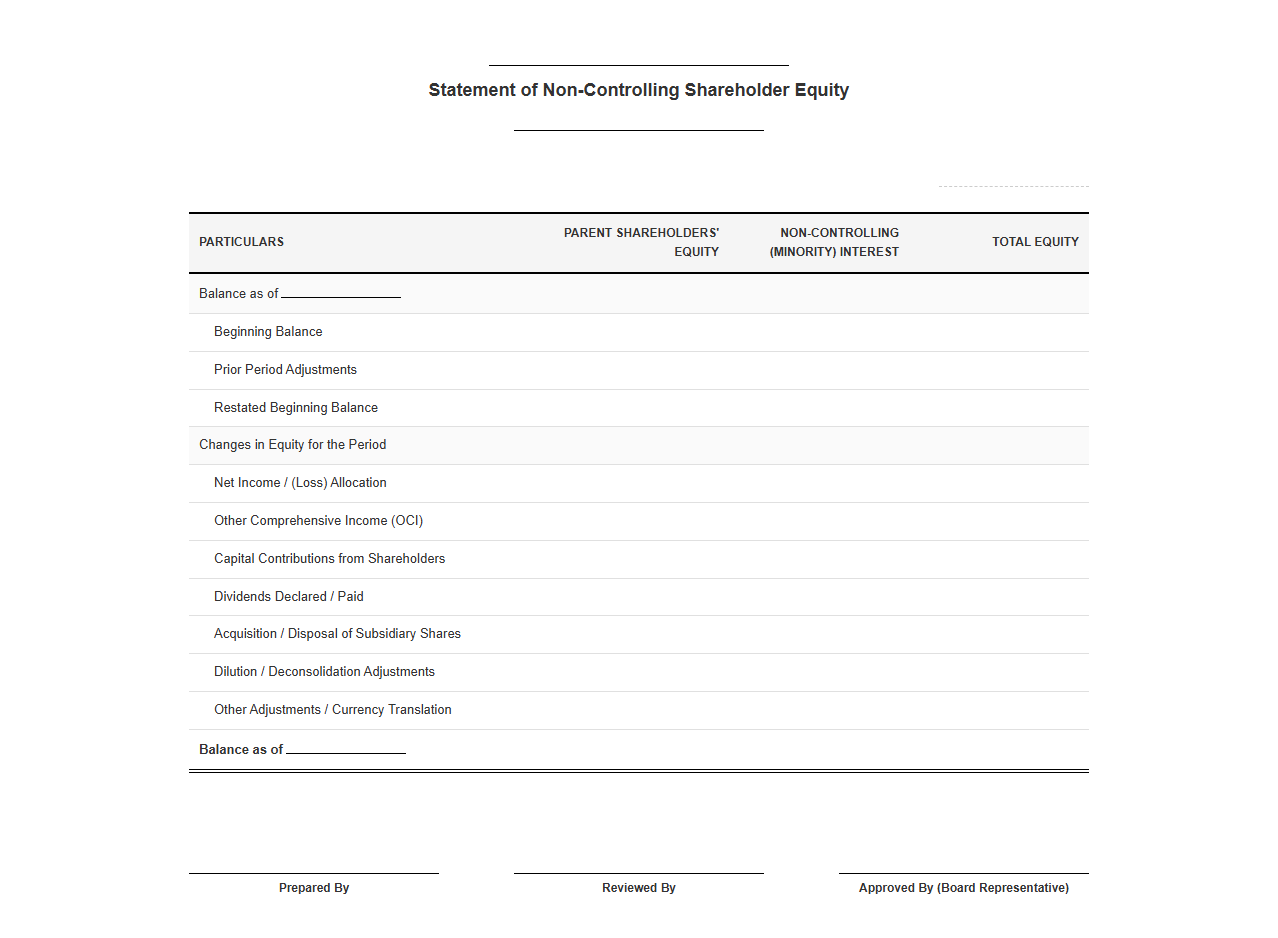

Non-Controlling Shareholder Equity Statement

Download: .PDF

Download: .PDF

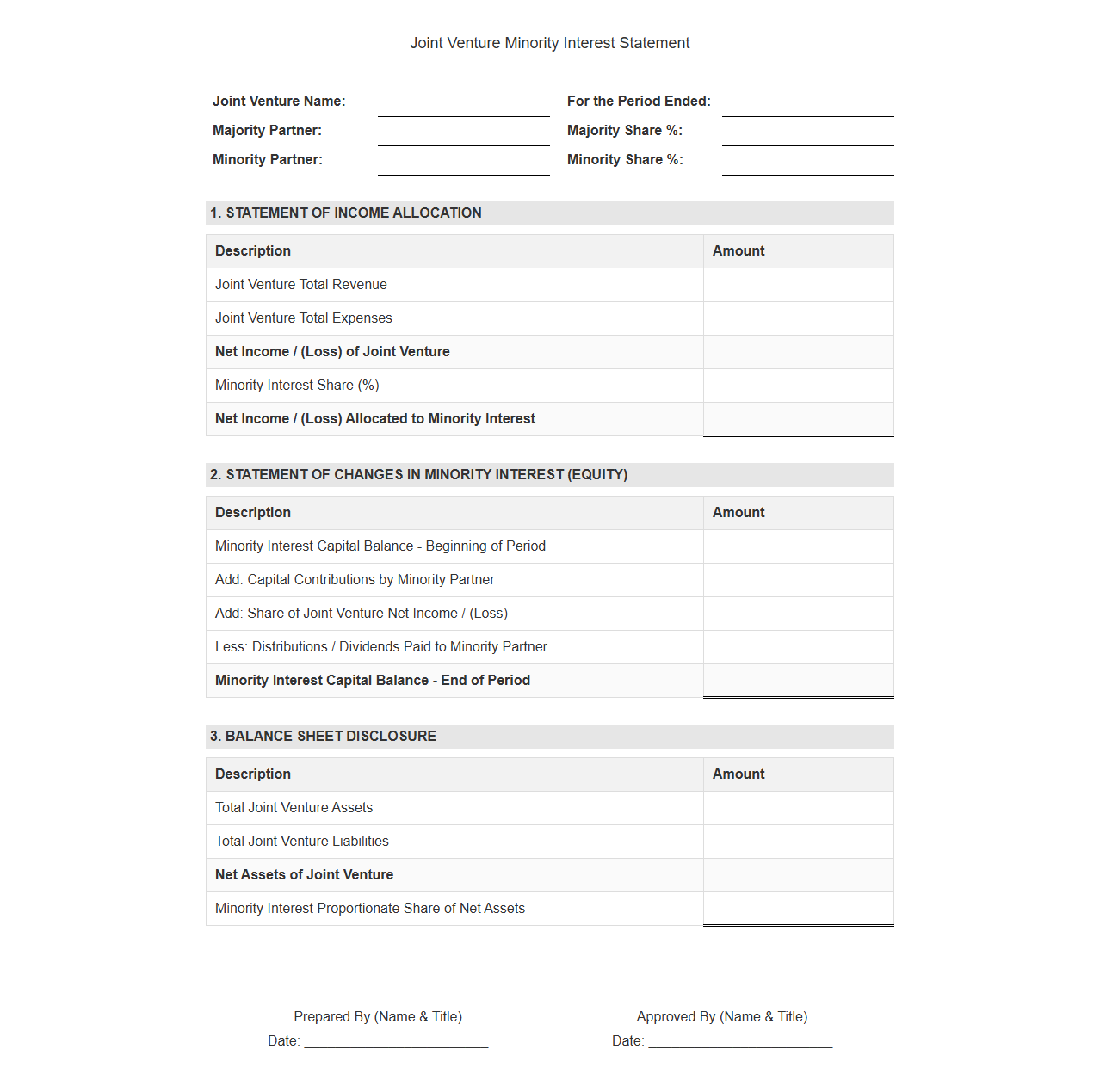

Joint Venture Minority Interest Statement Format

Download: .PDF

Download: .PDF

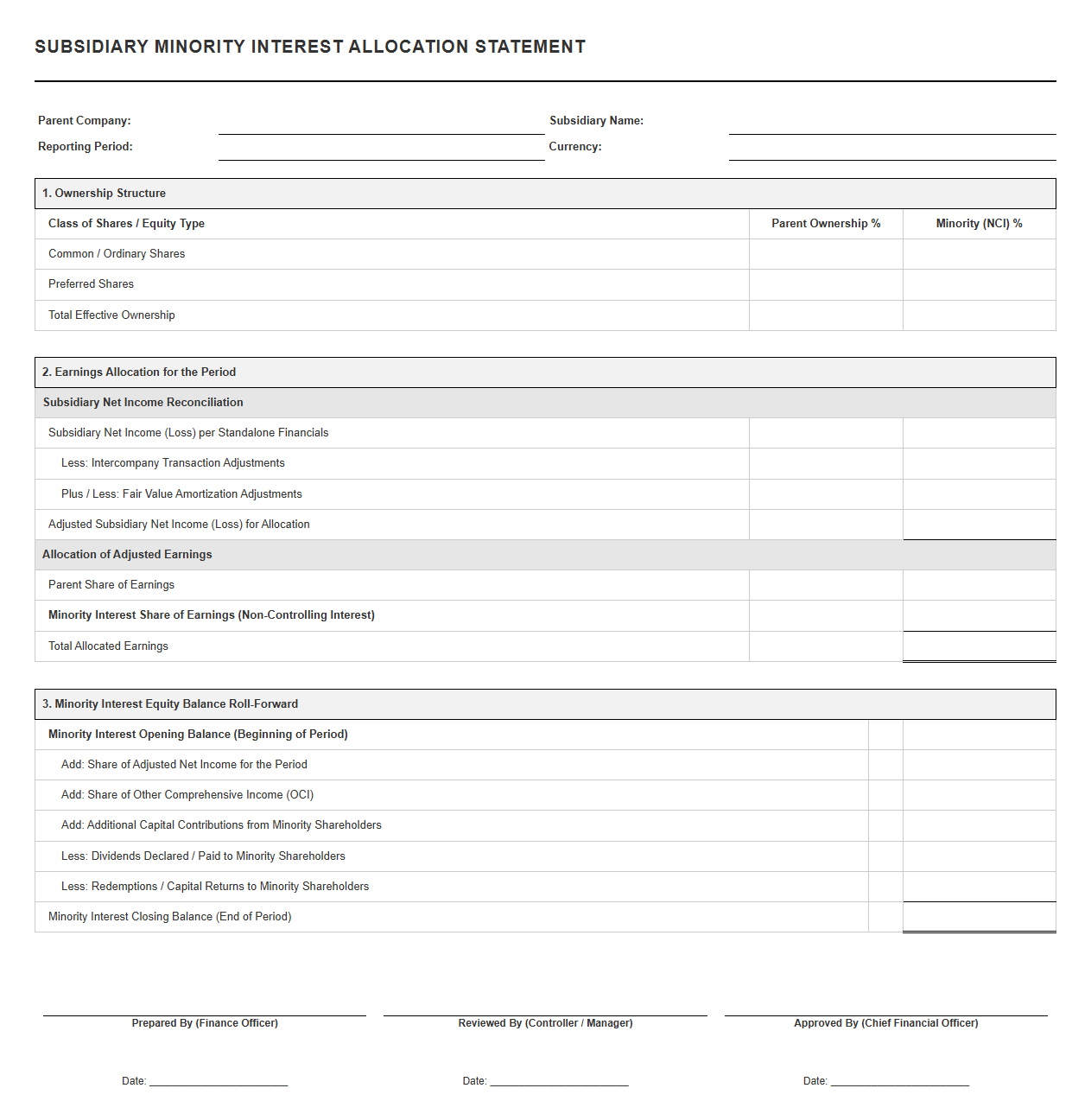

Subsidiary Minority Interest Allocation Template

Download: .PDF

Download: .PDF

Introduction to Minority Interest Disclosure Complexity

Disclosing minority interests, or non-controlling interests (NCI), under both IFRS and US GAAP creates persistent reporting friction and compliance challenges for public companies. Financial consolidations require meticulous tracking of equity ownership boundaries, often leading to technical friction when reconciling parent and subsidiary ledgers across diverse jurisdictions.

Core Challenges in Equity Valuation and Reporting

Accounting departments regularly encounter structural obstacles when attempting to align subsidiary financials with parent reporting frameworks. The three primary hurdles include:

- Measurement Inconsistency: Divergent fair value measurement rules between GAAP and IFRS for initial NCI recognition.

- Consolidation Boundaries: Difficulty in determining control versus significant influence under changing ownership structures.

- Presentation Variations: Inconsistent classification of NCI transaction costs and comprehensive income items.

The Strategic Value of Standardized Statement Templates

Utilizing standardized reporting templates dramatically simplifies the financial consolidation process. By embedding structured formats directly into reporting workflows, companies significantly lower the likelihood of manual calculation errors.

"Standardized disclosures not only mitigate compliance risks and accelerate audit readiness, but they also enhance overall financial transparency, providing global stakeholders with clear, comparable, and reliable equity data."

Template A: Consolidated Balance Sheet Equity Presentation

| Equity Component | Parent Shareholders | Non-Controlling Interest | Total Equity |

|---|---|---|---|

| Common Stock | $1,000,000 | - | $1,000,000 |

| Retained Earnings | $4,500,000 | - | $4,500,000 |

| Accumulated Other Comprehensive Income | $150,000 | $15,000 | $165,000 |

| Non-Controlling Interest Equity Balance | - | $650,000 | $650,000 |

| Total Equity | $5,650,000 | $665,000 | $6,315,000 |

Template B: Consolidated Income Allocation Statement

| Consolidated Net Income | $850,000 |

| Net Income Attributable to Parent Shareholders | $730,000 |

| Net Income Attributable to Non-Controlling Interest | $120,000 |

| Consolidated Comprehensive Income | $900,000 |

| Comprehensive Income Attributable to Parent Shareholders | $770,000 |

| Comprehensive Income Attributable to Non-Controlling Interest | $130,000 |

Best Practices for Accompanying Footnote Disclosures

To ensure full compliance with global financial reporting standards, teams must supplement consolidated templates with rich, qualitative narrative footnotes.

- Detailed breakdown of the subsidiary's assets and liabilities prior to consolidation adjustments.

- The explicit valuation techniques and inputs used to measure non-controlling interest at fair value.

- A reconciliation of the carrying amount of NCI at the beginning and the end of the reporting period.

- Significant restrictions on the parent company's ability to access or use the subsidiary's assets.

Action Plan for Integrating Disclosure Templates

Successfully embedding standardized templates requires a coordinated approach from the corporate controller's group.

Leave a comment