Consolidating equity, specifically tracking Non-Controlling Interests (NCI), is a notorious bottleneck for corporate finance teams, often leading to reporting delays and reconciliation errors. Before jumping into complex software integrations, establishing a robust accounting framework that aligns with IFRS 10 and ASC 810 standards is a critical prerequisite.

By adopting standardized, comprehensive statement templates, organizations gain immediate reporting accuracy, drastically reducing audit preparation times and ensuring flawless equity roll-forwards. However, for these templates to be truly effective, users must adapt them to their specific subsidiary ownership shifts and multi-currency environments.

For example, integrating automated roll-forward schedules for pre-acquisition equity and post-acquisition profit allocation provides the empirical proof needed to satisfy rigorous audit standards. Below, we will dissect the anatomy of an effective NCI template, explore step-by-step implementation strategies, and provide downloadable models to elevate your financial reporting.

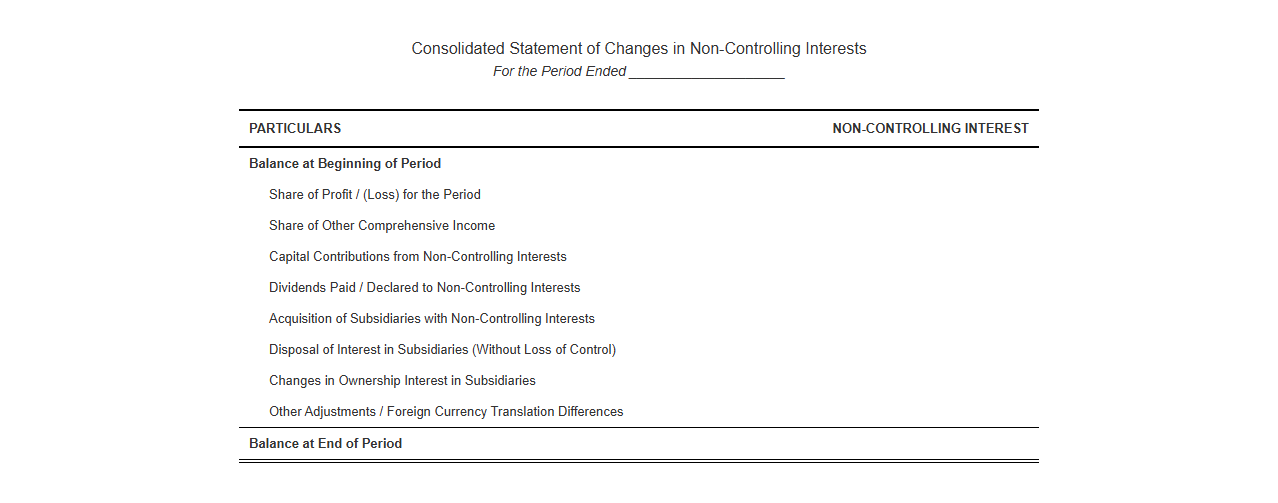

Consolidated Statement of Non-Controlling Interest Changes

Download: .PDF

Download: .PDF

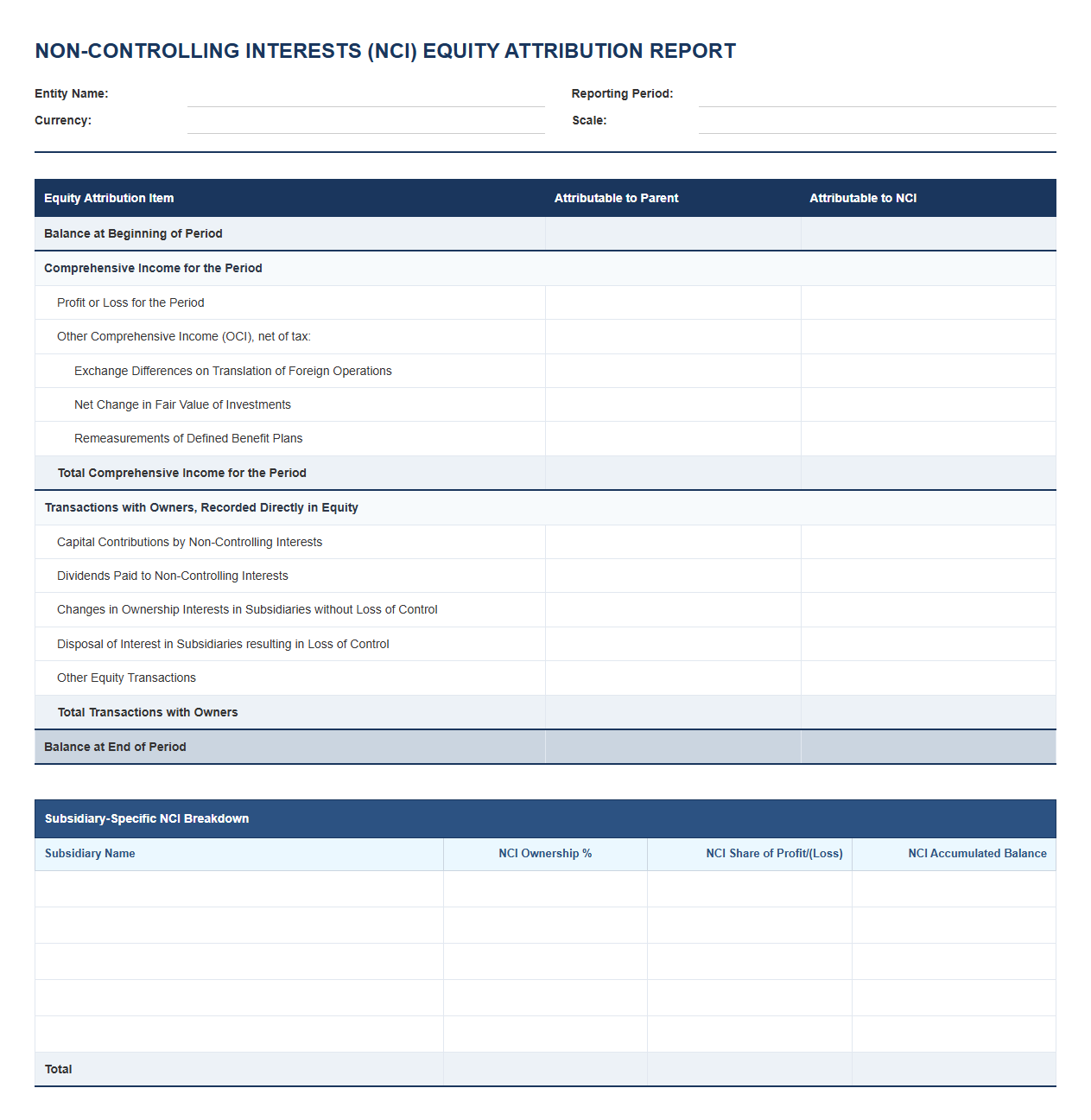

NCI Equity Attribution Report Template

Download: .PDF

Download: .PDF

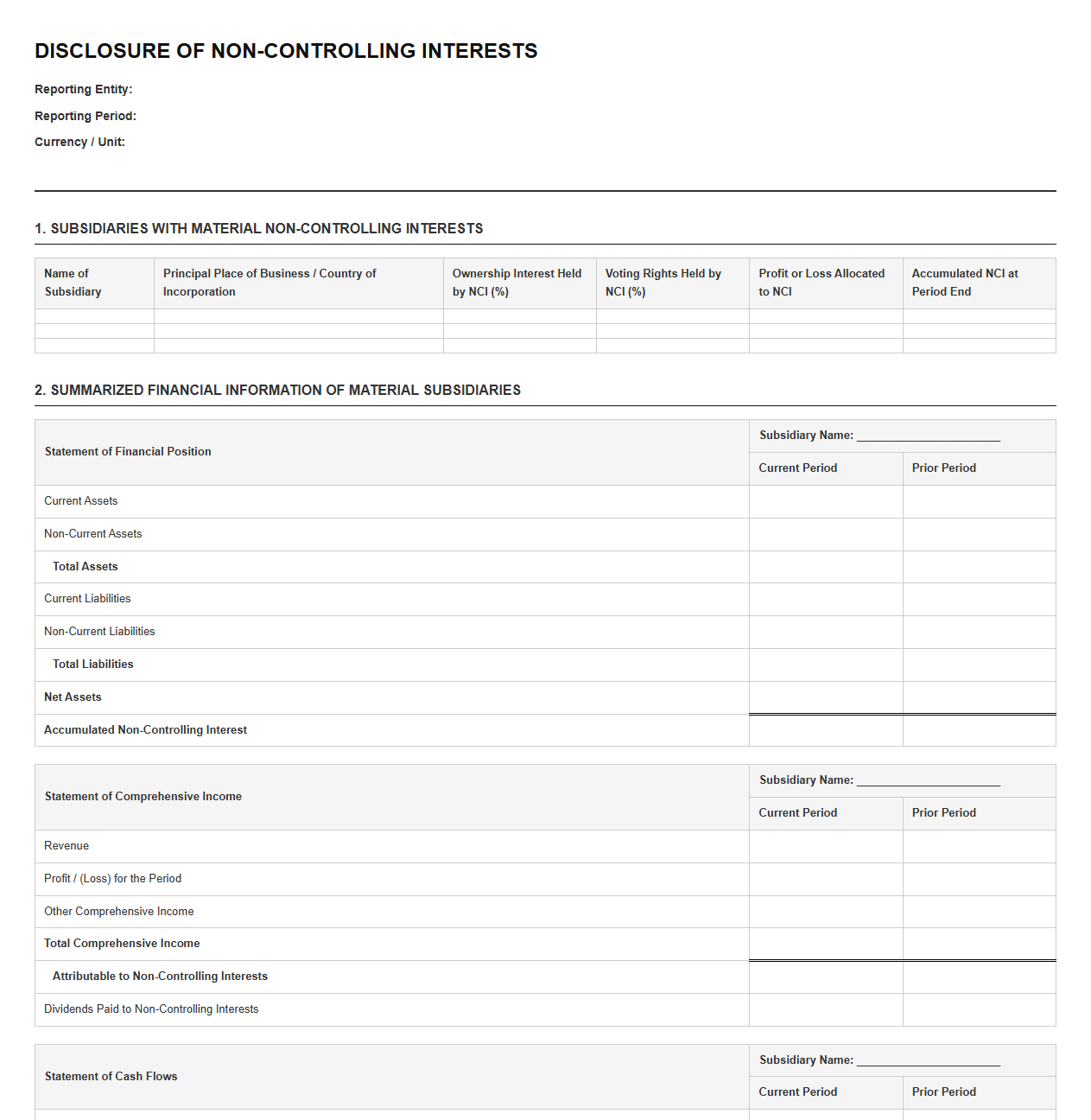

Non-Controlling Interest Disclosure Statement Format

Download: .PDF

Download: .PDF

Minority Interest Shareholder Equity Statement

Download: .PDF

Download: .PDF

Consolidated Equity Schedule for Non-Controlling Interests

Download: .PDF

Download: .PDF

NCI Balance Sheet Reconciliation Template

Download: .PDF

Download: .PDF

Schedule of Non-Controlling Interest Allocation

Download: .PDF

Download: .PDF

NCI Earnings and Dividends Statement Template

Download: .PDF

Download: .PDF

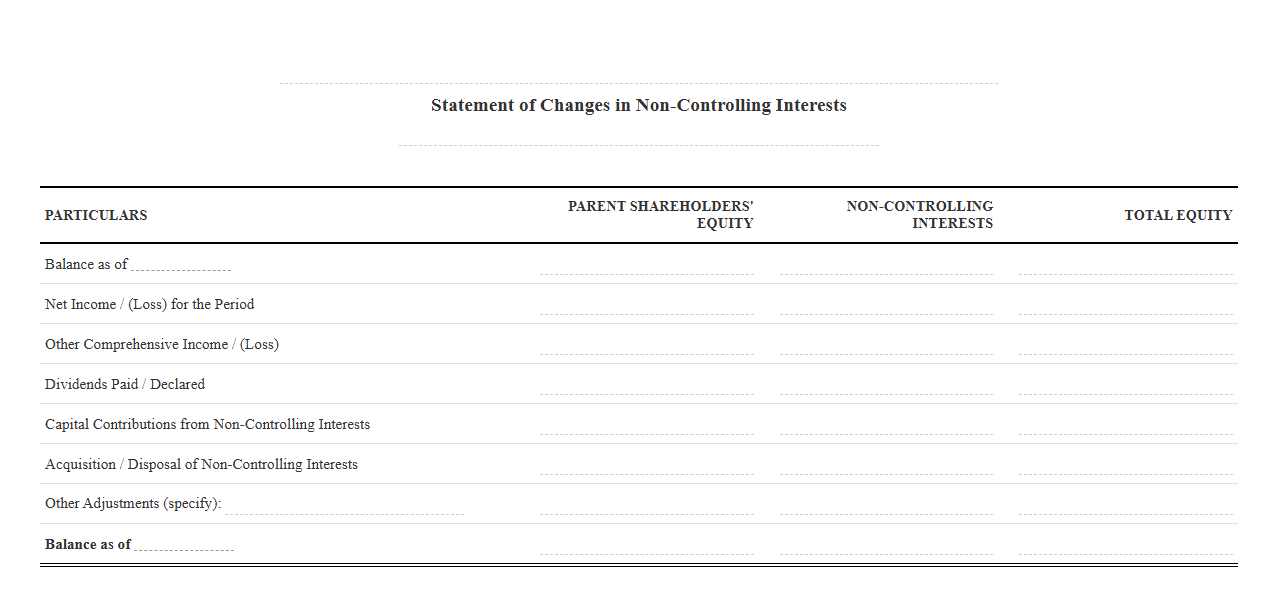

Statement of Changes in Minority Interest Equity

Download: .PDF

Download: .PDF

Demystifying Consolidated Equity and Non-Controlling Interests

In corporate financial reporting, presenting a clear picture of a parent company and its subsidiaries requires a deep understanding of consolidated equity. When a parent company holds a controlling stake in a subsidiary but owns less than 100% of its shares, Non-Controlling Interests (NCI)-historically referred to as minority interests-must be recognized. NCI represents the portion of equity in a subsidiary not attributable, directly or indirectly, to the parent company.

Accurately representing NCI is not merely a compliance requirement; it is a critical aspect of transparent financial reporting. For financial professionals, masterfully reporting NCI ensures that investors and stakeholders can easily distinguish between the equity attributable to the parent's shareholders and that which belongs to external, non-controlling owners. This distinction is vital for analyzing true corporate value, earnings per share metrics, and overall return on equity.

The Financial Complexity of Tracking NCI

Accounting for NCI introduces substantial complexity into consolidated financial statements, particularly when dealing with complex corporate hierarchies. When parent-subsidiary ownership structures change over time, accounting teams must make precise adjustments under the equity method to reflect these shifts without losing historical accuracy.

"Fluctuating ownership stakes-such as partial acquisitions, step acquisitions, or the sale of a portion of a subsidiary's shares-directly impact the balance of both parent equity and NCI, demanding continuous and meticulous calculation."

These dynamic equity balances require continuous monitoring to ensure that changes in ownership control that do not result in a loss of control are accounted for as equity transactions, rather than gain-or-loss events on the income statement.

Key Components of the Consolidated Statement of Equity

A standardized consolidated statement of changes in equity must present a transparent breakdown of all equity elements, carefully separating the amounts allocable to the parent company from those allocable to the NCI. To ensure compliance and clarity, the template must include several essential components:

- Common Stock and Paid-in Capital: The par value and additional capital contributed by the parent's shareholders.

- Retained Earnings: Cumulative consolidated net income retained in the business, excluding the portion allocated to NCI.

- Accumulated Other Comprehensive Income (AOCI): Unrealized gains and losses, such as foreign currency translation adjustments, split proportionally between the parent and NCI.

- Non-Controlling Interest Balance: The total book value of the subsidiary's equity belonging to external minority shareholders, presented within the consolidated equity section but separate from the parent's equity.

A Step-by-Step Template for NCI Calculations

To accurately track and report NCI balances across financial periods, organizations should implement a structured roll-forward template. Below is an example of a calculation model that tracks the life cycle of NCI balances from the beginning of the fiscal period to its close.

| Calculation Step | Description | Sample Amount ($) |

|---|---|---|

| Beginning NCI Balance | The carrying value of NCI at the start of the reporting period. | 150,000 |

| Allocation of Subsidiary Net Income | NCI share of the subsidiary's net income for the current period. | 25,000 |

| Allocation of Subsidiary OCI | NCI share of other comprehensive income (e.g., translation adjustments). | 5,000 |

| Less: Dividends Distributed | Dividends paid out by the subsidiary directly to the non-controlling shareholders. | (10,000) |

| Ending NCI Balance | The finalized carrying value of NCI to be reported on the consolidated balance sheet. | 170,000 |

Strategies for Streamlining the Equity Reconciliation Process

Reconciling parent and NCI balances during the financial close process can lead to significant delays if managed manually. To simplify consolidation and improve data integrity, finance departments should adopt proactive reconciliation strategies.

- Establish clear intercompany transaction policies to eliminate errors at the source before consolidation begins.

- Implement standardized equity roll-forward schedules that dynamically update as journal entries are posted.

- Automate the tracking of historical exchange rates for foreign subsidiaries to prevent manual calculation discrepancies during consolidation.

- Conduct regular intermediate closes to identify and resolve equity imbalances prior to the final year-end reporting cycle.

Critical Reporting Errors and How to Mitigate Them

Errors in calculating and presenting NCI can result in restatements, compliance issues, and damaged investor trust. Recognizing where these mistakes frequently happen is the first step toward prevention.

Incorrect Exchange Rate Applications

When consolidations involve foreign subsidiaries, finance teams often apply incorrect exchange rates to equity balances. While income statement items are translated using average rates, equity balances must be translated using historical rates. Misapplying these rates distorts both the consolidated equity and the NCI balances.

Misallocated Subsidiary Dividends

Another common pitfall is the incorrect treatment of dividends. Dividends paid by a subsidiary to its non-controlling interest holders must reduce the NCI balance on the consolidated balance sheet. Under no circumstances should these dividends be recorded as dividend income on the parent's income statement, as they represent a return of capital to external owners.

Modernizing Equity Reporting Through Technology

The manual preparation of consolidated equity statements using disconnected spreadsheets is rapidly becoming obsolete. Modern Enterprise Resource Planning (ERP) systems and dedicated automated consolidation software allow organizations to generate real-time, audit-ready NCI reports. These systems enforce rigorous accounting rules, handle complex multi-tier currency conversions automatically, and maintain a clear digital audit trail.

By shifting to digital consolidation platforms, finance teams drastically reduce manual errors and free up valuable time for strategic analysis. Embracing standardized reporting frameworks alongside automated technology ensures your organization remains agile, compliant, and highly precise in its financial disclosures. Financial leaders who leverage these advanced systems position their businesses to navigate future regulatory shifts and evolving global structures with complete confidence. Investing in modern financial technology is the most effective way to secure error-free equity reporting.

Leave a comment