For many finance leaders and corporate accountants, tracking secondary revenue streams remains a fragmented and frustratingly manual process. While robust ERP systems excel at capturing core operational transactions, they often fail to cleanly accommodate the unique reporting nuances of peripheral cash flows.

Bridging this gap with standardized, professional statement templates grants organizations immediate visibility and precision, empowering strategic treasury management. However, optimization requires recognizing that not all secondary revenue is equal; distinct accounting rules apply whether you are documenting interest yield, real estate leasing dividends, or intellectual property licensing royalties.

In this guide, we will analyze specialized template structures designed for diverse non-operating income sources, demonstrating how to streamline your reporting, minimize reconciliation errors, and ensure audit-ready financial statements.

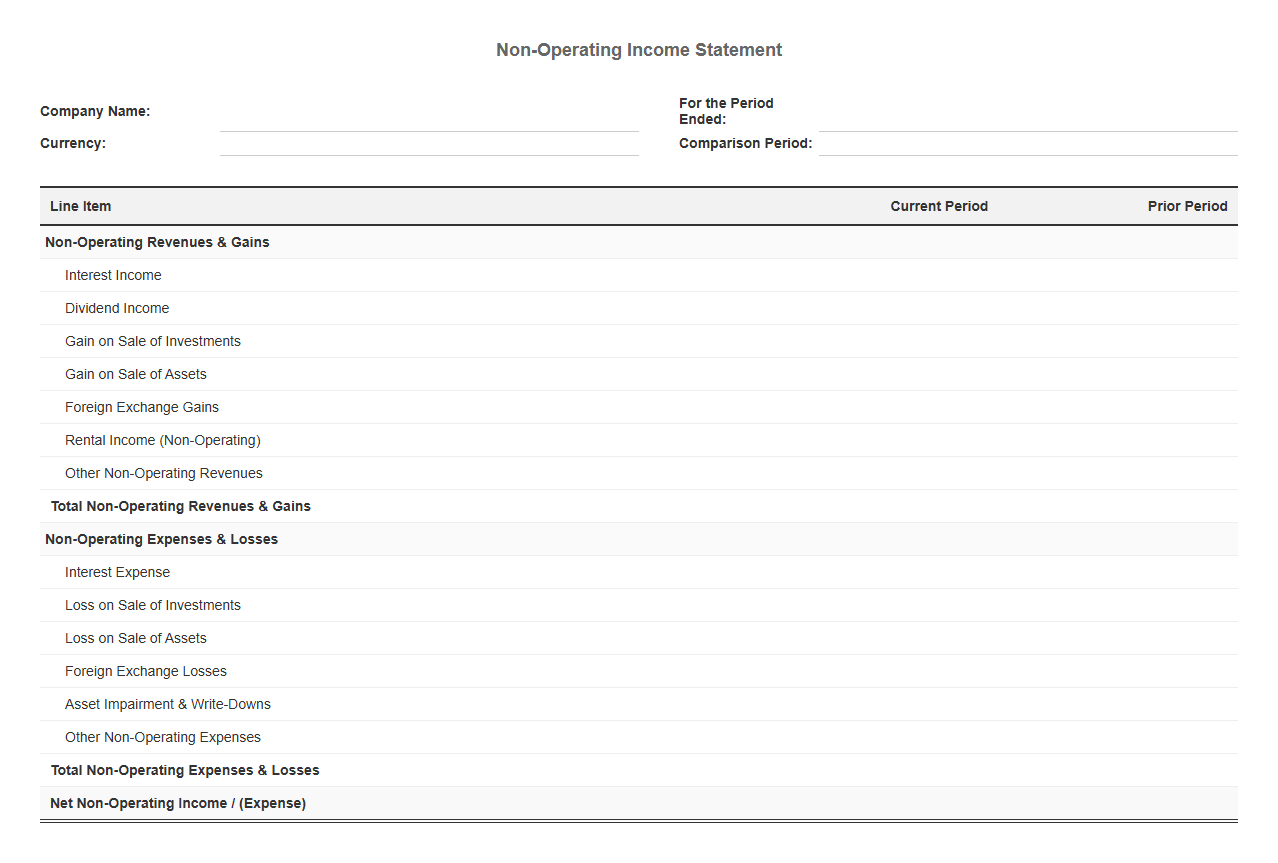

Non-Operating Income Statement Template

Download: .PDF

Download: .PDF

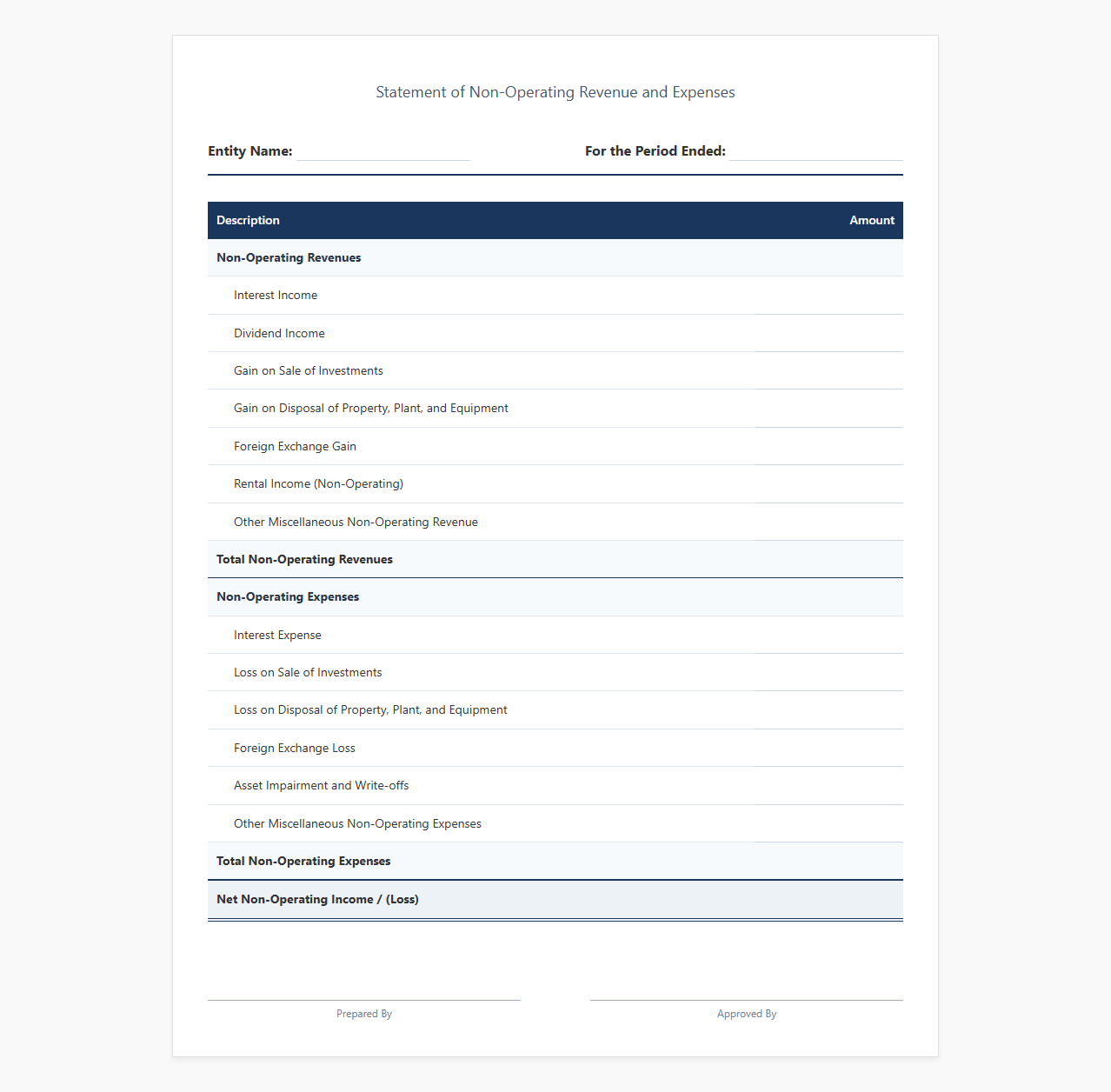

Non-Operating Revenue and Expense Statement Template

Download: .PDF

Download: .PDF

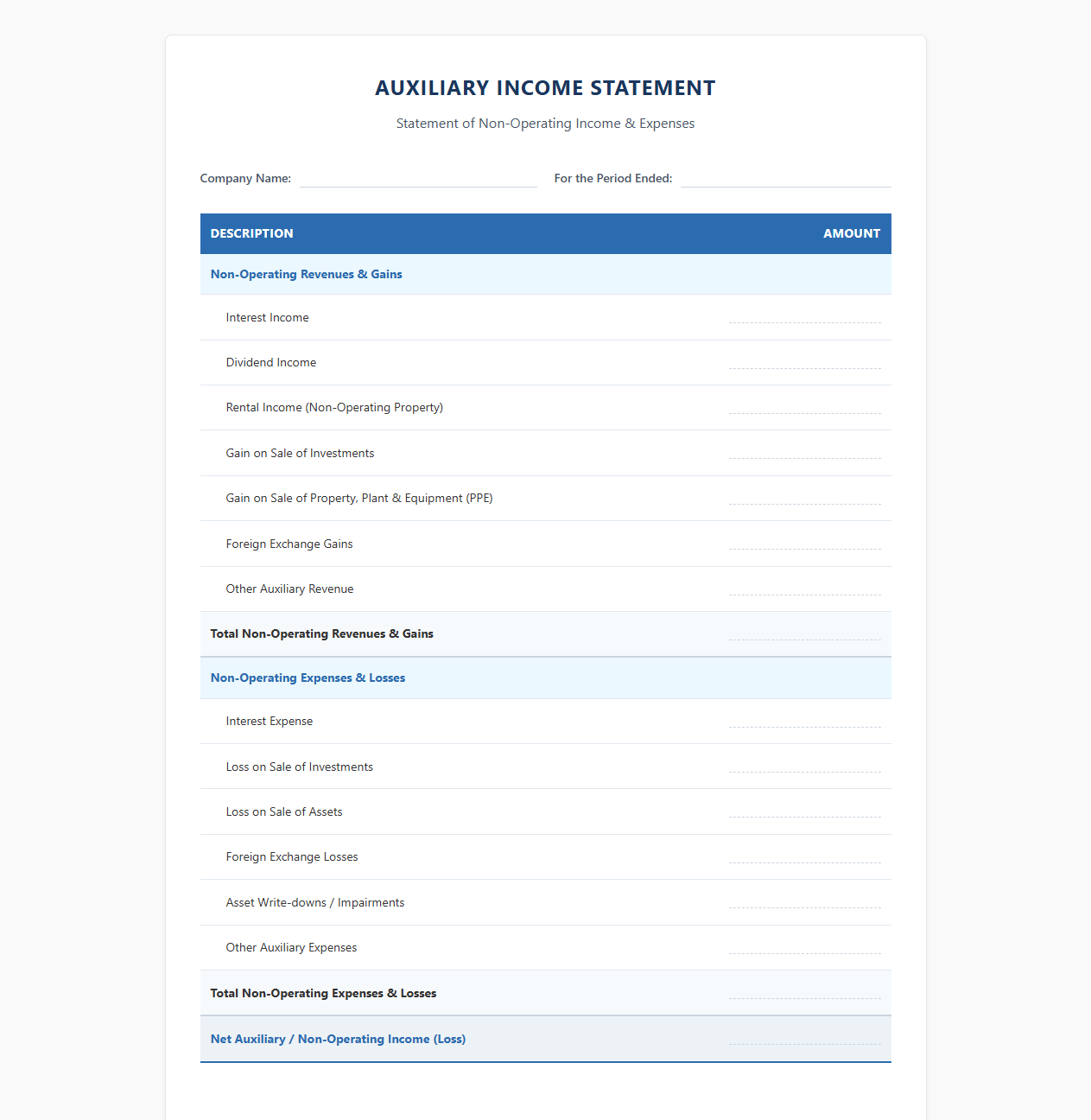

Auxiliary Income Statement Template

Download: .PDF

Download: .PDF

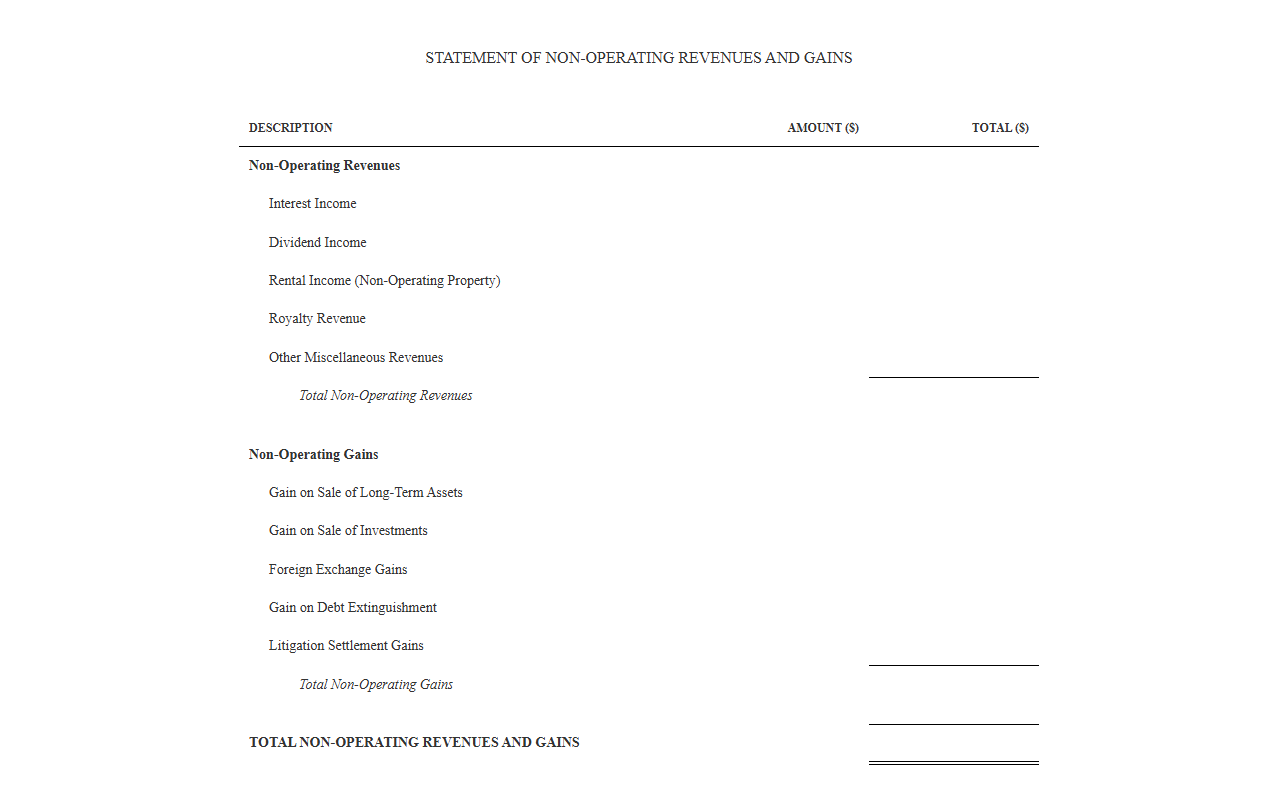

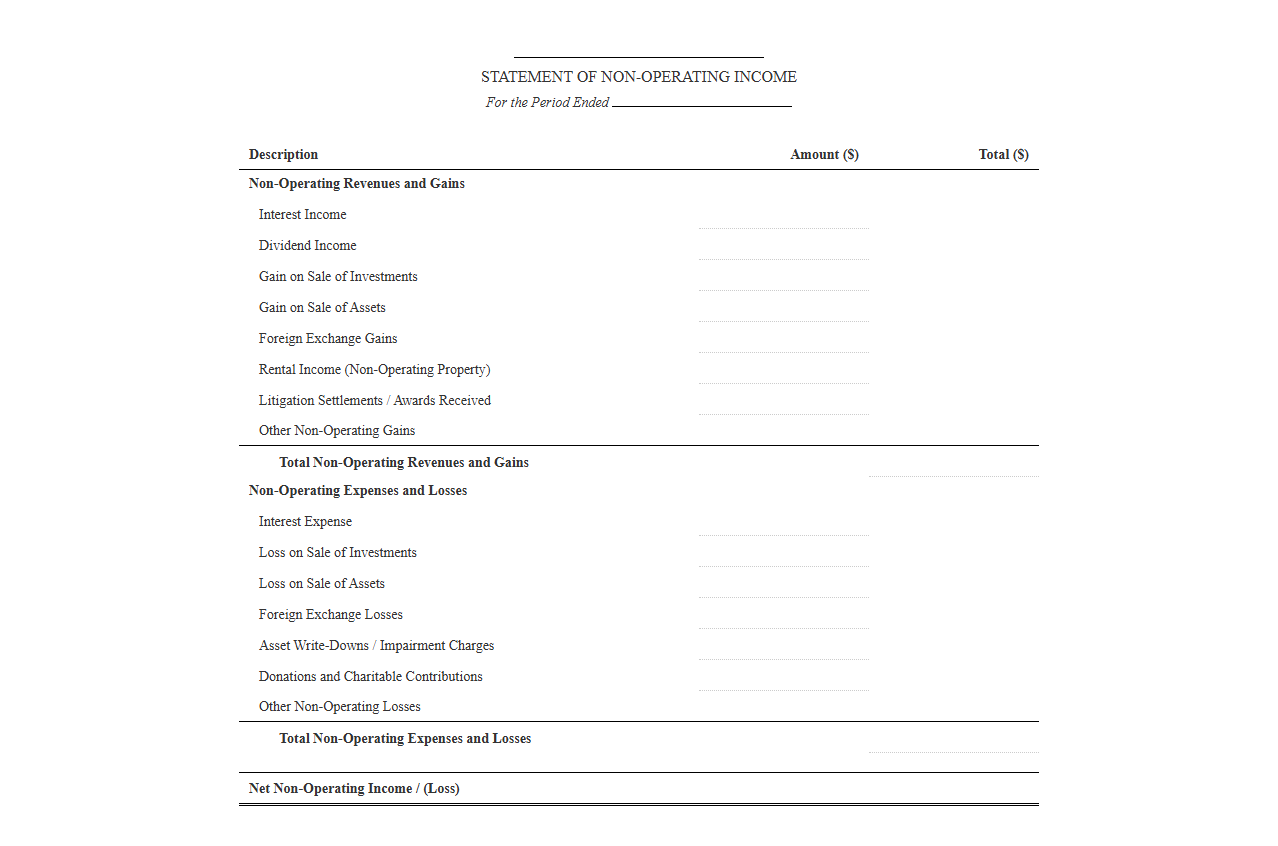

Statement of Non-Operating Revenues and Gains

Download: .PDF

Download: .PDF

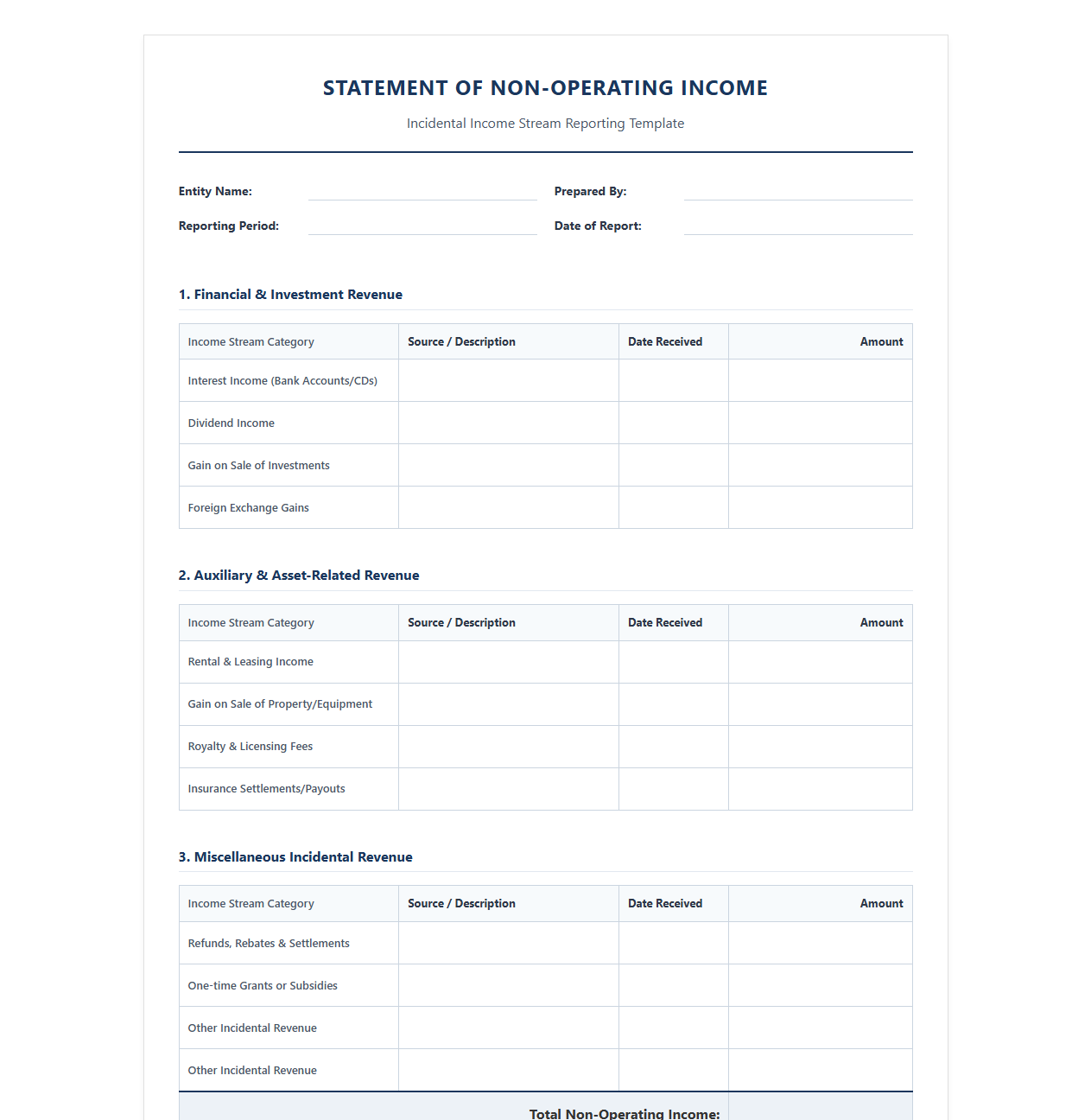

Incidental Income Stream Reporting Template

Download: .PDF

Download: .PDF

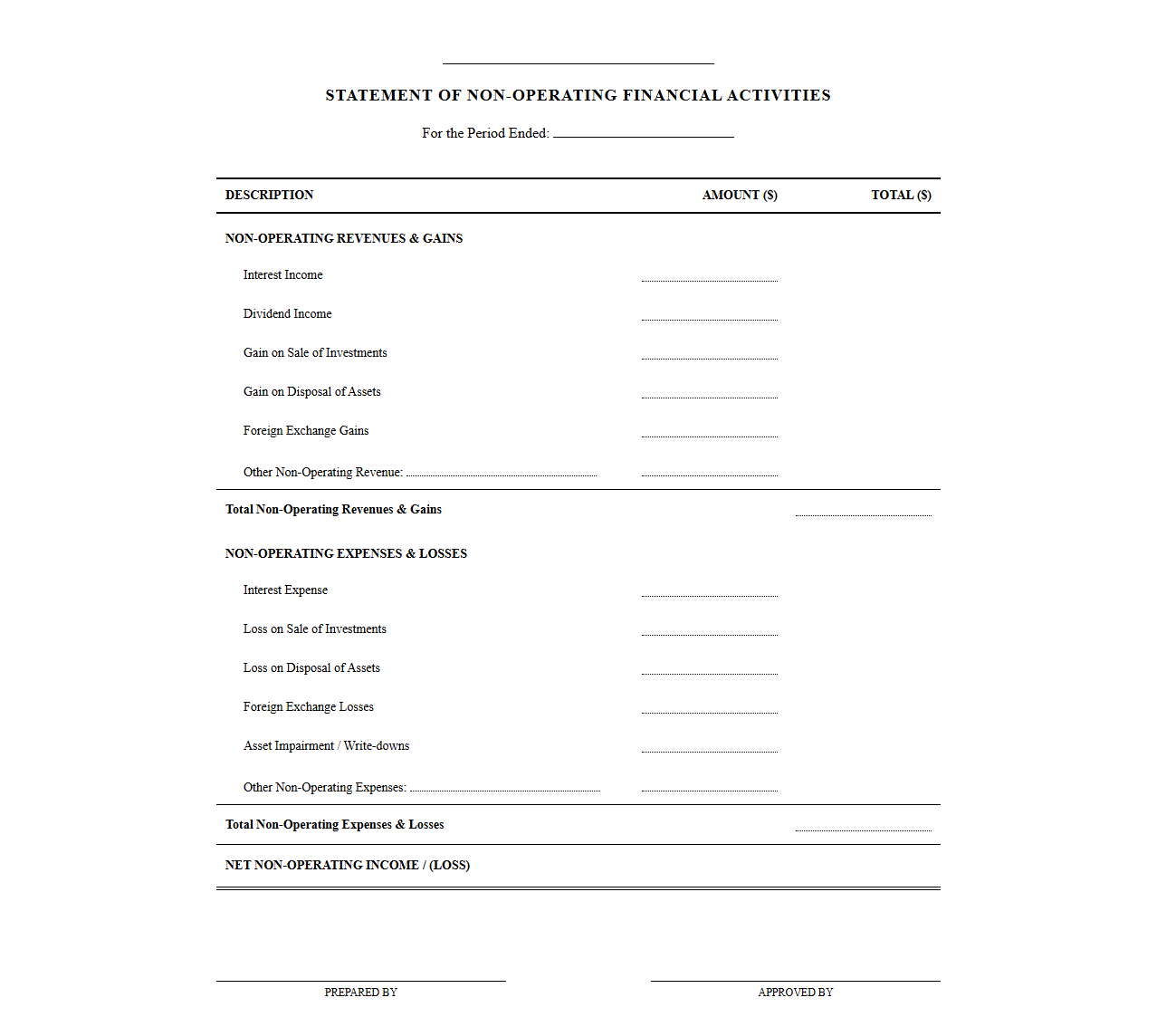

Non-Operating Financial Activities Statement

Download: .PDF

Download: .PDF

Secondary Income Statement Template

Download: .PDF

Download: .PDF

Non-Operating Gains and Losses Template

Download: .PDF

Download: .PDF

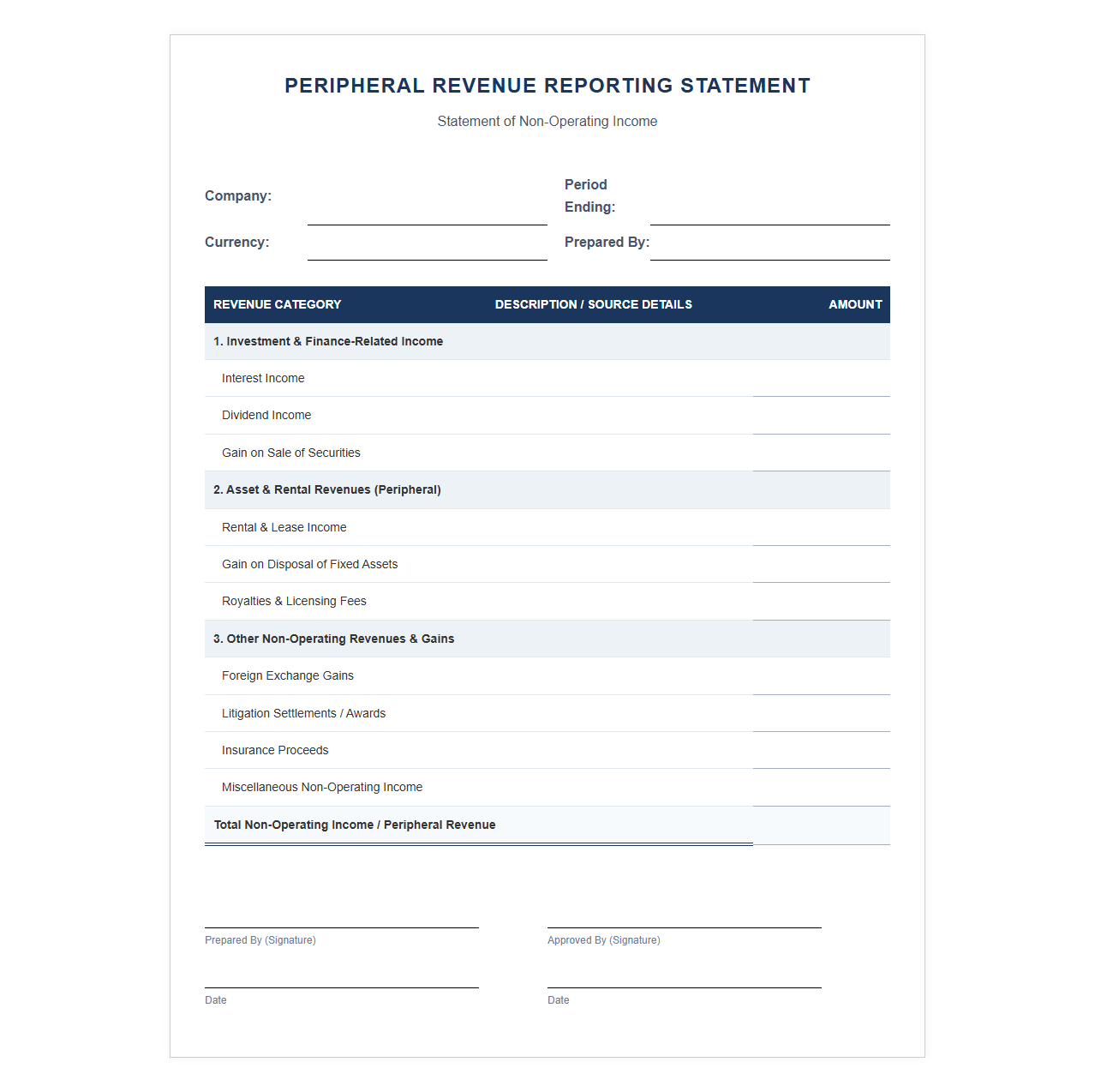

Peripheral Revenue Reporting Statement Template

Download: .PDF

Download: .PDF

Executive Summary: The Strategic Value of Non-Operating Income Tracking

To acquire an accurate view of a company's financial performance, decision-makers must distinguish between core operational achievements and peripheral financial activities. Operating income reflects the core business model's viability, efficiency, and market demand. Conversely, non-operating income represents revenues and expenses derived from activities outside the company's daily operations, such as investment yields, asset sales, and foreign currency fluctuations.

Failing to isolate non-operating items can distort key financial metrics, leading to misinformed strategic decisions. For instance, a one-off windfall from a property sale could mask declining sales in core product lines, creating an illusion of healthy operational growth. By tracking non-operating income on a dedicated, separate basis, finance teams ensure stakeholders receive transparent, reliable data that facilitates accurate valuations, forecasting, and resource allocation.

Categorizing Diverse Revenue Streams: From Investments to FX Gains

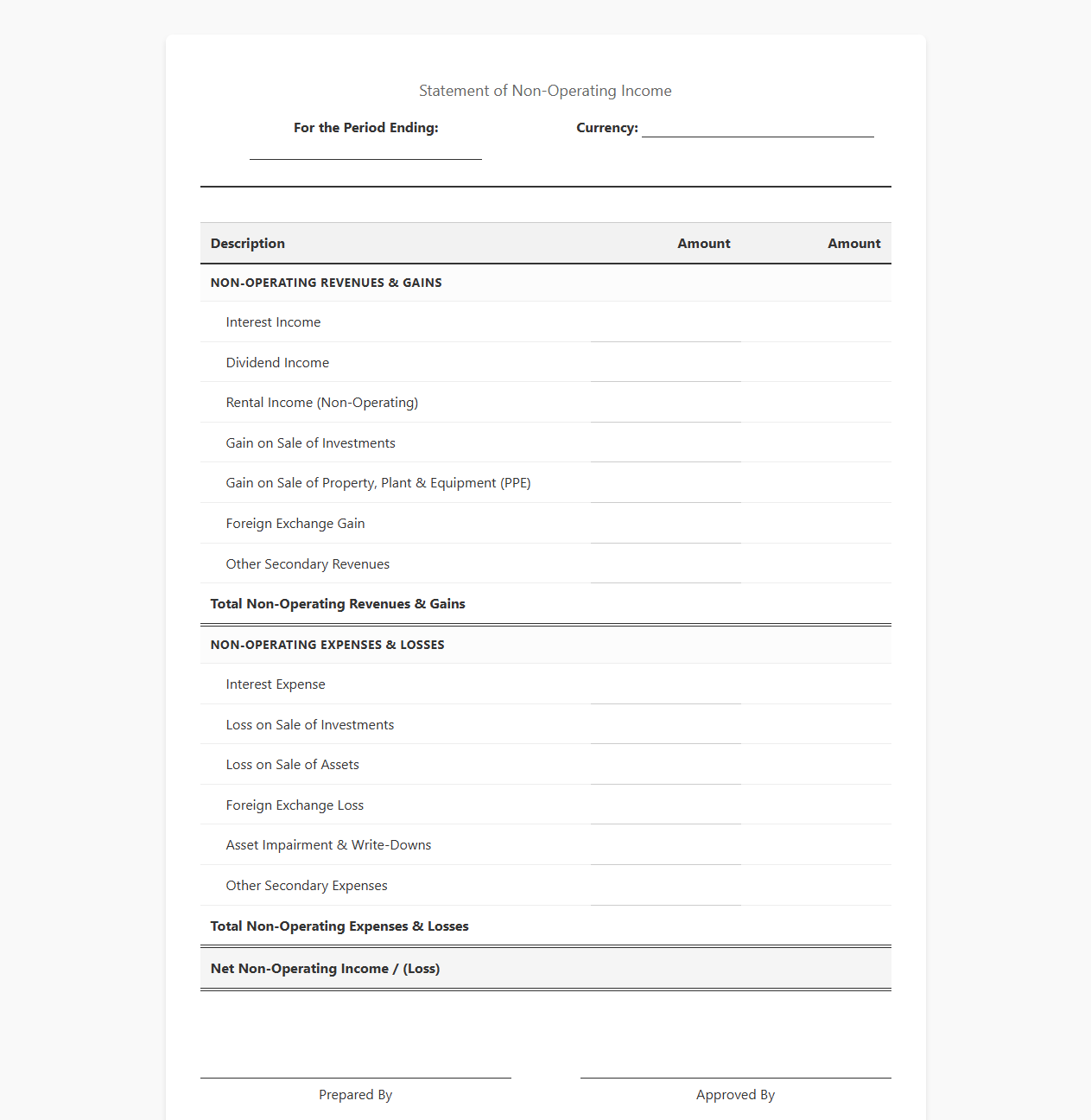

Non-operating revenue consists of diverse financial elements that require careful classification. Identifying and segmenting these streams ensures that they are treated correctly under standard tax and accounting frameworks. Below are the primary categories of non-operating revenue that organizations encounter:

- Dividend Income: Revenues received from equity investments held in other corporations, representing a share of those entities' profits.

- Interest Income: Earnings generated from cash reserves held in high-yield savings accounts, certificates of deposit (CDs), or yields from corporate and government bonds.

- Foreign Currency Exchange (FX) Gains: Financial gains realized from fluctuations in exchange rates when transactions or foreign assets are converted back into the parent company's functional currency.

- Auxiliary Rental Income: Revenue generated from renting out unused corporate real estate, equipment, or land that is not part of the primary business offering.

Designing the Statement Template: Key Architectural Elements

A functional non-operating income statement template requires a logical layout to ensure readability and integrity of the underlying data. It must seamlessly transition from the operating profit line to net income, clearly presenting the non-operating inputs without cluttering the core operating calculations. Key layout considerations include consistent column headers for periods (monthly, quarterly, or annually), clear categorizations of inflows versus outflows, and specific reconciliation rows that tie these figures directly back to the general ledger.

Step-by-Step Guide: Tracking Recurring Investment and Dividend Income

Accurately tracking recurring non-operating income streams prevents accounting mismatches and ensures that passive cash flows are recognized in the correct reporting periods. Finance teams should establish a structured workflow to monitor, calculate, and report these yields regularly.

- Identify the investment instrument and locate the payout schedule, noting the ex-dividend and payment dates.

- Reconcile the received cash distributions against bank statements to confirm the exact amounts deposited.

- Calculate accrued interest for bond yields that have been earned but not yet paid during the reporting period.

- Record the entry in the ledger, debiting cash (or interest receivable) and crediting dividend/interest income.

- Verify the consolidated figures in the non-operating template during month-end closing procedures.

Accounting for One-Time Gains and Asset Disposals

Irregular, high-value transactions-such as selling real estate, machinery, or intellectual property-require precise accounting because they involve removing the asset's book value, accounting for accumulated depreciation, and recognizing the net gain or loss on the transaction. The net gain is calculated by subtracting the asset's carrying value (historical cost minus accumulated depreciation) from the net proceeds received from the sale. This net gain is recorded under non-operating income rather than operational revenue.

| Asset Description | Historical Cost | Accumulated Depreciation | Net Book Value | Sale Proceeds | Recognized Gain (Loss) |

|---|---|---|---|---|---|

| Headquarters Office Lot B | $1,200,000 | $300,000 | $900,000 | $1,450,000 | $550,000 |

| Manufacturing Line 4 Equipment | $450,000 | $350,000 | $100,000 | $120,000 | $20,000 |

| Legacy Patent Portfolio | $150,000 | $150,000 | $0 | $75,000 | $75,000 |

System Integration: Automating Data Flows from Treasury to Ledger

Manual entry of non-operating data increases the risk of transcription errors and delays month-end closing. Modern enterprise architectures integrate treasury management systems directly with the main ERP system. Utilizing secure banking APIs, automated data pipelines fetch real-time transaction data from investment accounts, currency desks, and external property management tools, feeding this data directly into the non-operating ledger templates.

"Automating the transfer of non-operating financial transactions from corporate custody accounts directly to the ERP system reduces human error by over ninety percent and ensures that currency adjustments are calculated and applied with daily spot rates."

Audit Readiness and Compliance Standards for Non-Operating Revenue

Because non-operating income often contains highly variable, one-time transactions, it frequently draws scrutiny from internal and external auditors. To ensure audit readiness, businesses must maintain robust audit trails that link every recorded transaction to its source documentation. This includes preserving purchase contracts, valuation reports, bank confirmations, and foreign exchange conversion receipts.

Compliance requires strict adherence to international and local accounting frameworks. Under GAAP and IFRS standards, non-operating items must be clearly segregated on the income statement or comprehensively explained within the accompanying financial notes. Entities must consistently apply recognition criteria, ensuring that gains are only recognized when they are realized or realizable, and that any associated asset write-downs are taken immediately to provide a fair and balanced view of the organization's overall financial position.

Leave a comment