Reconciling cash flow discrepancies during the month-end close is a persistent headache for corporate finance teams, often leading to delayed reporting and strategic friction. Before rushing to patch these balance errors, it is vital to recognize that mismatches usually stem from systemic misclassifications within increasingly complex transactional workflows. Transitioning to a standardized operating cash flow template grants organizations immediate reporting precision, turning chaotic ledger data into an audit-ready financial narrative.

However, a template is only as reliable as its baseline inputs; accurate reporting stipulates a strict adherence to standardized GAAP or IFRS classification rules. For example, consistently isolating non-cash transactions like depreciation or correctly adjusting for net accounts receivable fluctuations is critical to balancing the indirect method. In this article, we will examine the standard template formats utilized by industry leaders, outline step-by-step reconciliation protocols, and provide actionable strategies to eliminate reporting discrepancies permanently.

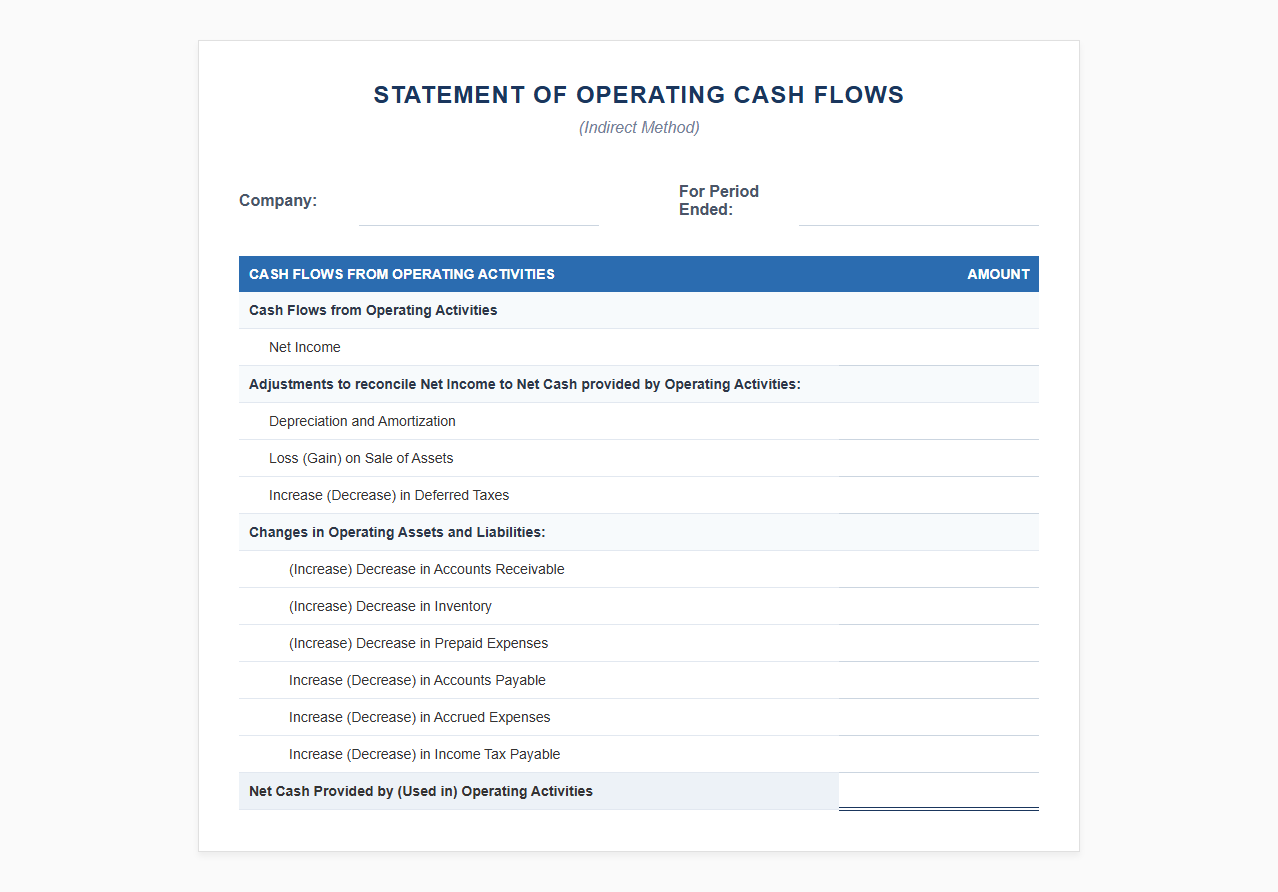

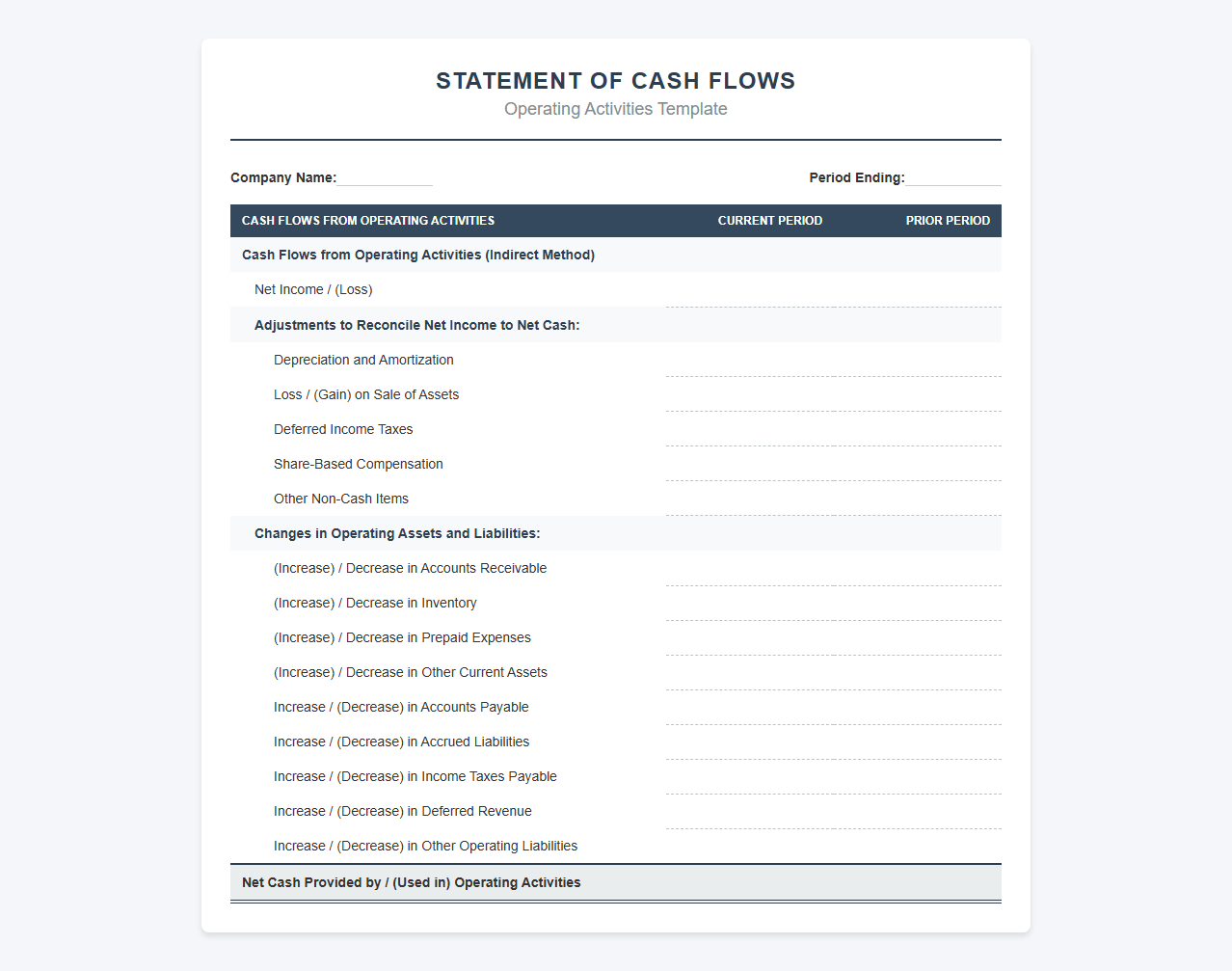

Operating Cash Flow Statement Template

Download: .PDF

Download: .PDF

Cash Flow from Operations Reporting Template

Download: .PDF

Download: .PDF

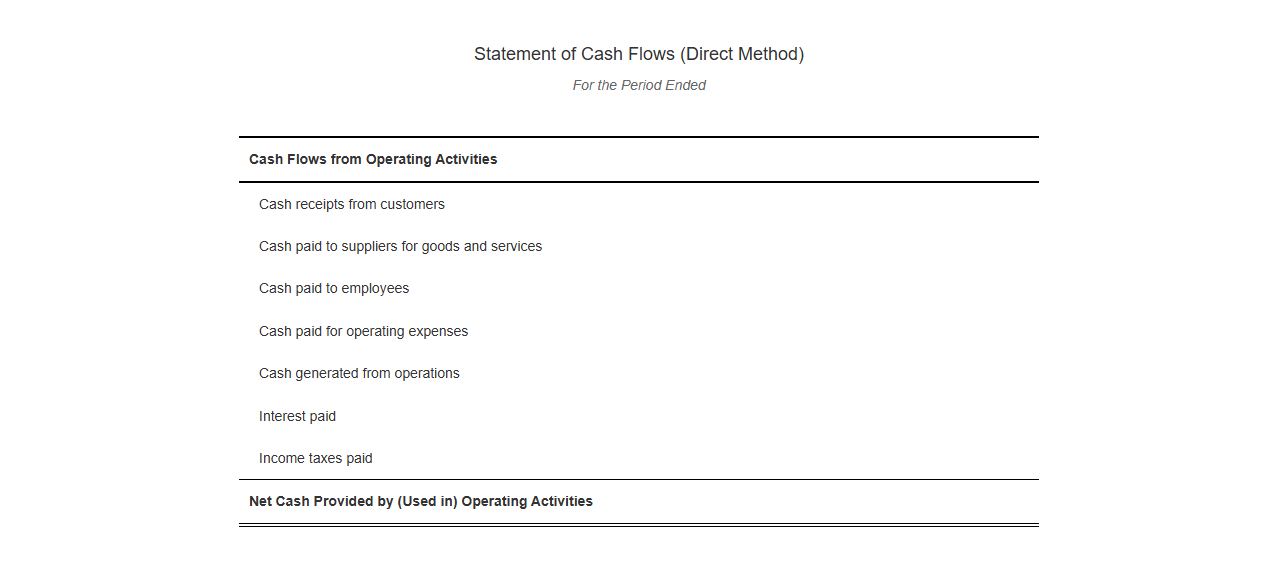

Direct Method Operating Cash Flow Template

Download: .PDF

Download: .PDF

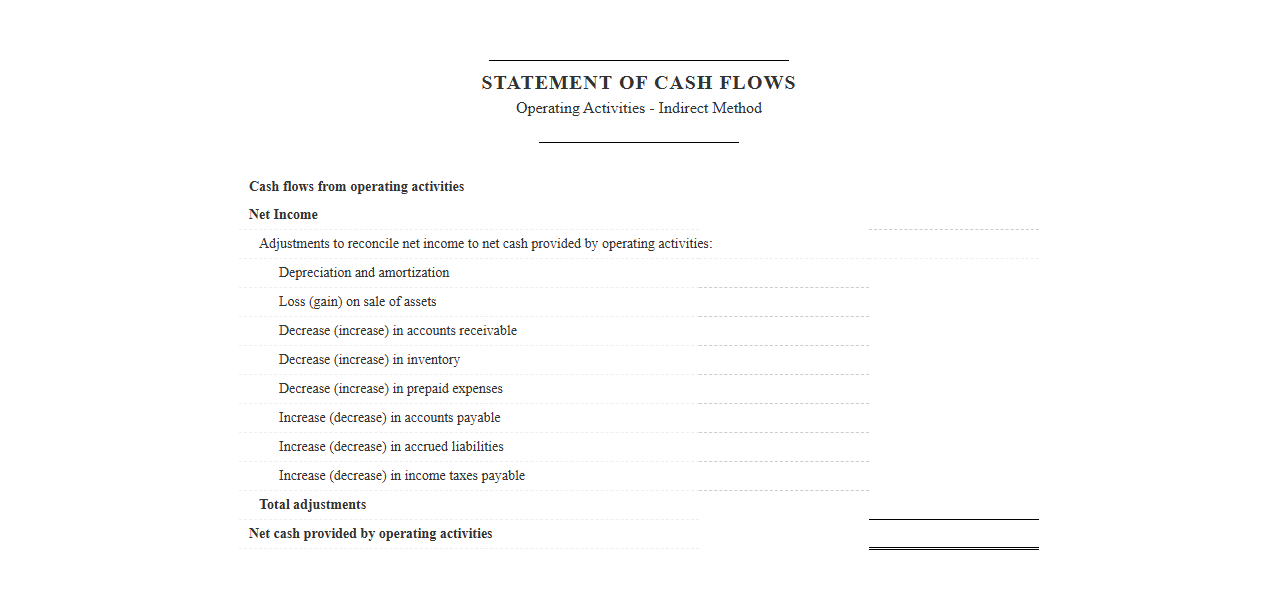

Indirect Method Operating Cash Flow Statement

Download: .PDF

Download: .PDF

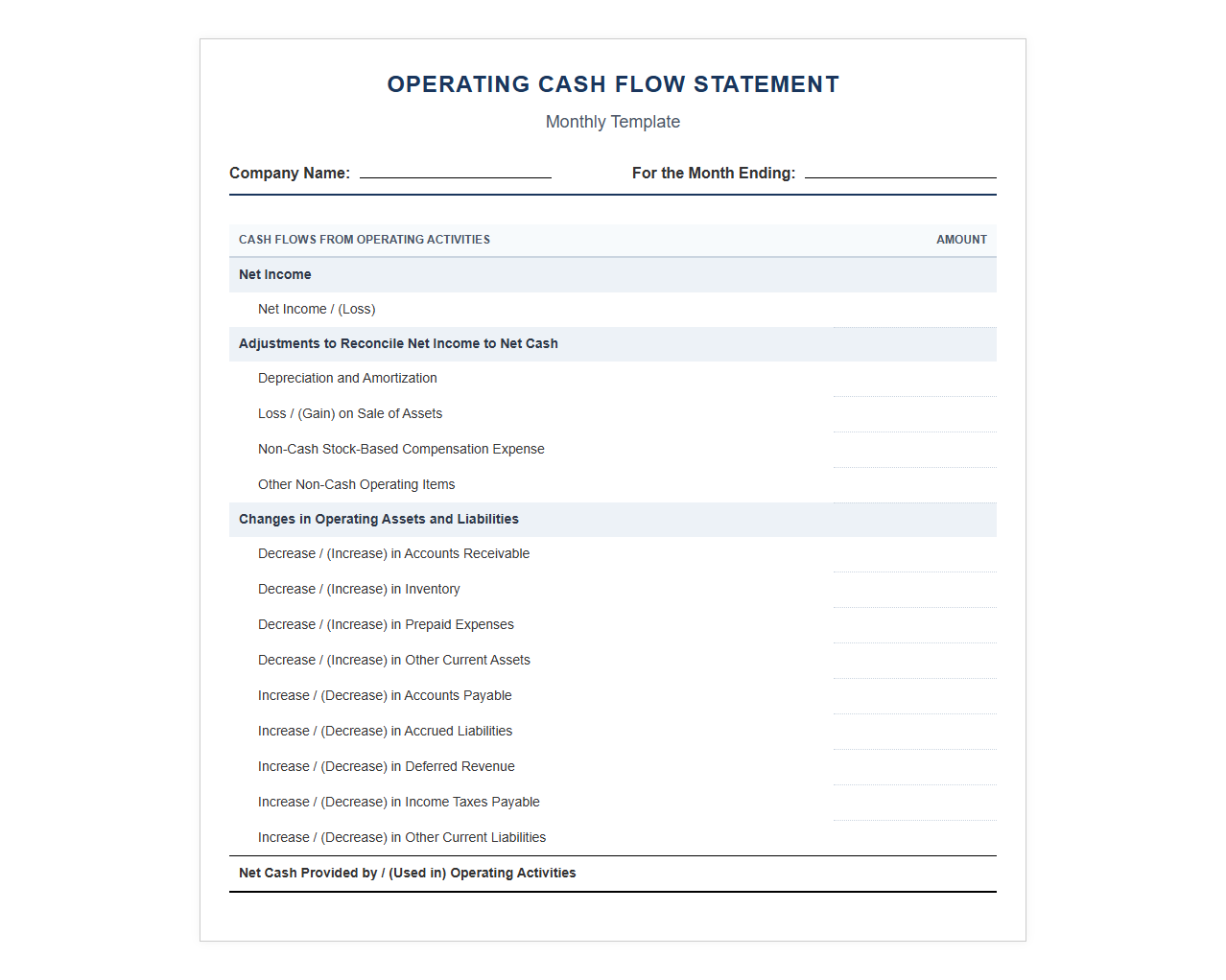

Monthly Operating Cash Flow Statement Template

Download: .PDF

Download: .PDF

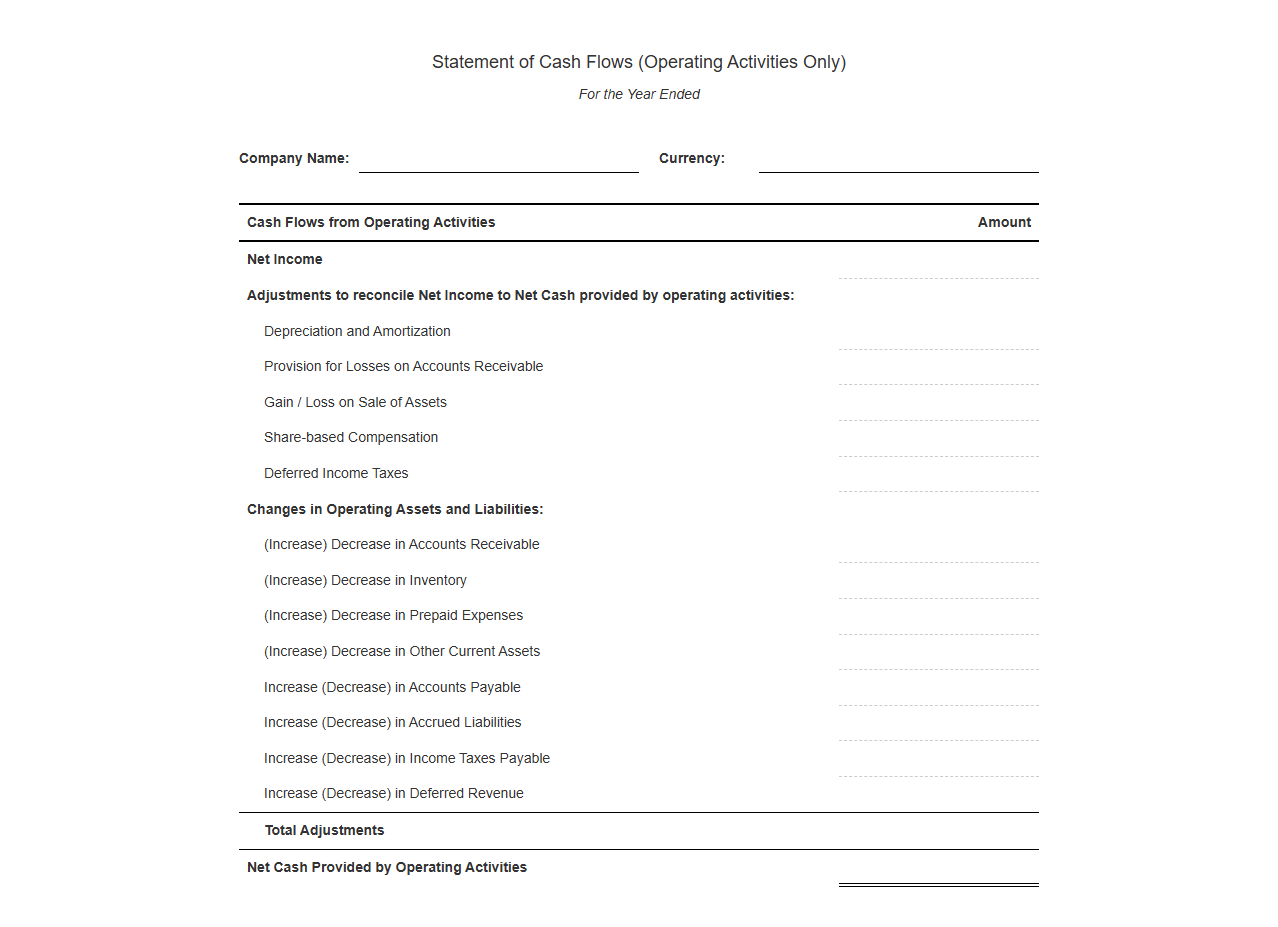

Annual Cash Flow from Operations Statement

Download: .PDF

Download: .PDF

Small Business Operating Cash Flow Template

Download: .PDF

Download: .PDF

Operational Cash Flow Tracker and Statement

![]() Download: .PDF

Download: .PDF

Understanding Cash Flow Discrepancies and Their Impact

Cash flow discrepancies within operating activities frequently arise from timing differences between revenue recognition and actual cash collection, as well as errors in tracking non-cash transactions. When these mismatches go unresolved, they distort a company's true liquidity position, leading to flawed strategic decisions and compromised financial reporting accuracy. Unresolved discrepancies undermine investor confidence, risk regulatory non-compliance, and mask operational inefficiencies. To mitigate these risks, implementing a standardized template serves as the first line of defense, establishing a structured framework that ensures consistency, simplifies error detection, and guarantees that book cash aligns perfectly with bank realities.

Core Components of the Operating Cash Flow Statement

To construct an accurate cash flow statement, financial teams must understand the foundational elements that bridge accrual accounting with cash-basis reality.

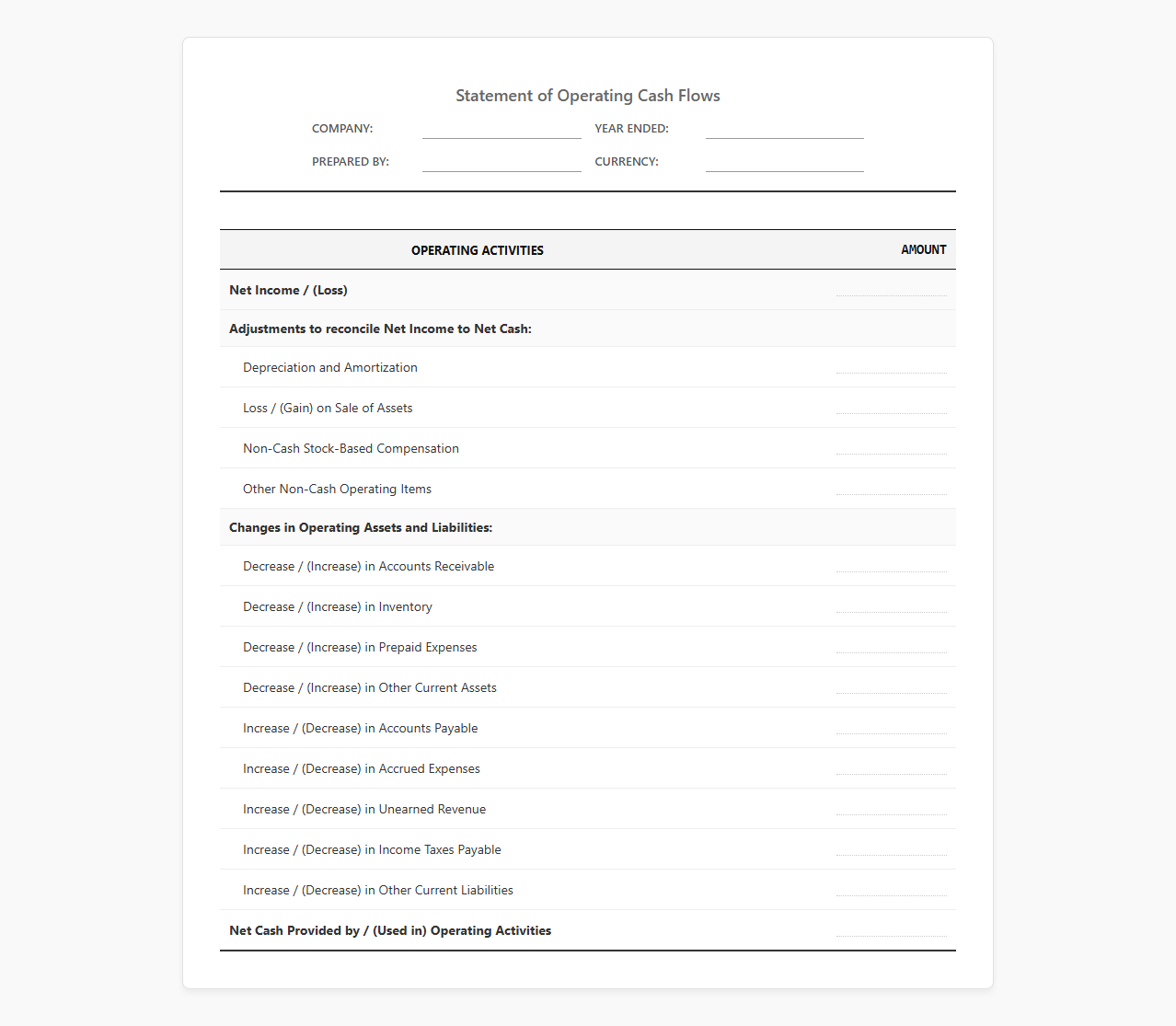

Net Income

This serves as the starting point for the indirect cash flow method, representing the total net earnings derived from the income statement before any cash-flow adjustments are made.

Non-Cash Adjustments

These entries add back expenses that reduced net income but did not involve an actual outflow of cash during the period.

- Depreciation of physical assets

- Amortization of intangible assets

- Deferred tax adjustments

- Stock-based compensation

Working Capital Changes

These adjustments reflect the cash impact of short-term asset and liability balance fluctuations on the balance sheet.

- Changes in Accounts Receivable (decreases increase cash)

- Changes in Inventory (decreases increase cash)

- Changes in Accounts Payable (increases increase cash)

The Indirect Method Template Format

The indirect method template reconciles accrual-based net income to the actual cash generated by operations. This reconciliation is essential for stakeholders to understand why net earnings rarely equal net cash inflows.

- Start with Net Income sourced directly from the current period's Income Statement.

- Add back all non-cash expenses, such as depreciation and amortization, since no cash left the business for these accounting write-offs.

- Subtract increases in current operating assets (like Accounts Receivable and Inventory), as this represents revenue recognized for which cash has not yet been collected.

- Add decreases in current operating assets, reflecting the conversion of those assets into realized cash.

- Add increases in current operating liabilities (such as Accounts Payable and Accrued Expenses), which show that cash has been preserved by delaying payments.

- Subtract decreases in current operating liabilities, representing the cash outflow to settle outstanding obligations.

The Direct Method Template Format

The direct method presents actual cash inflows and outflows directly from operating activities, eliminating accrual concepts from the presentation. This format resolves discrepancies at the source by tracking the literal movement of cash.

| Operating Cash Flow Line Item | Description / Calculation Source |

|---|---|

| Cash Received from Customers | Sales Revenue adjusted for changes in Accounts Receivable balance |

| Cash Paid to Suppliers | Cost of Goods Sold adjusted for changes in Inventory and Accounts Payable |

| Cash Paid to Employees | Salaries and Wages Expense adjusted for changes in Accrued Payroll |

| Cash Paid for Operating Expenses | Selling, General, and Administrative expenses adjusted for Prepaid Expenses |

| Interest and Taxes Paid | Actual cash outflows for financial charges and government levies |

Pinpointing and Resolving Template Discrepancies

Even with structured templates, discrepancies can occur due to data entry mistakes or systemic accounting misalignments. Recognizing these issues early prevents larger reconciliation errors at year-end.

Another frequent issue is the failure to adjust for non-cash transactions, such as the direct conversion of debt to equity or asset write-downs. If your cash flow statement does not reconcile with the cash balance on your balance sheet, check for misclassified non-operating items such as capital expenditure outflows hiding in operational accounts payable.

Step-by-Step Reconciliation Workflow

Accountants can systematic identify and resolve variances by executing a structured reconciliation workflow comparing the key financial statements.

- Verify that the beginning cash balance on the cash flow statement matches the ending cash balance from the prior period's balance sheet.

- Tie the Net Income figure directly to the final line of the current period's Income Statement.

- Cross-reference each working capital change on the cash flow statement with the net change of the corresponding line items on the comparative Balance Sheet.

- Confirm that the total depreciation and amortization added back matches the accumulated depreciation change, adjusted for any asset disposals during the period.

- Isolate any remaining variance and audit the general ledger for unusual journal entries that bypass the standard cash flow accounts.

- Document the resolution of the variance within the template for audit-trail transparency.

Maintaining Financial Integrity Through Standardized Reporting

Standardizing the cash flow template is not a one-time task but an ongoing commitment to financial hygiene. To ensure long-term accuracy, organizations must regularly update template automation formulas to reflect changes in the chart of accounts. Furthermore, integrating internal control audits ensures that cash reconciliation is subjected to independent reviews. Continuous training for accounting staff on both the "why" and "how" of cash flow classification completes this system, safeguarding the organization's financial reporting from errors and ensuring stakeholder reporting remains robust and reliable.

Leave a comment