Managing partnership distributions often becomes a logistical nightmare, especially when navigating disparate capital accounts and shifting profit-sharing ratios. Before addressing modern reporting solutions, we must recognize that traditional, ad-hoc spreadsheet models frequently fail to capture the nuanced legal terms embedded in complex partnership agreements.

Implementing standardized statement templates grants stakeholders absolute transparency, drastically reducing partner disputes and administrative overhead. However, as an educational stipulation, these templates are not magic fixes; their success relies on clean baseline financial data and a rigorous understanding of your specific distribution waterfall. For instance, accurately calculating preferred returns, hurdle rates, or clawback provisions requires structured input fields to prevent compounding formula errors.

This article explores how to deploy these standardized templates to streamline your allocations, outlines best practices for data integration, and provides a step-by-step framework for flawless financial reporting.

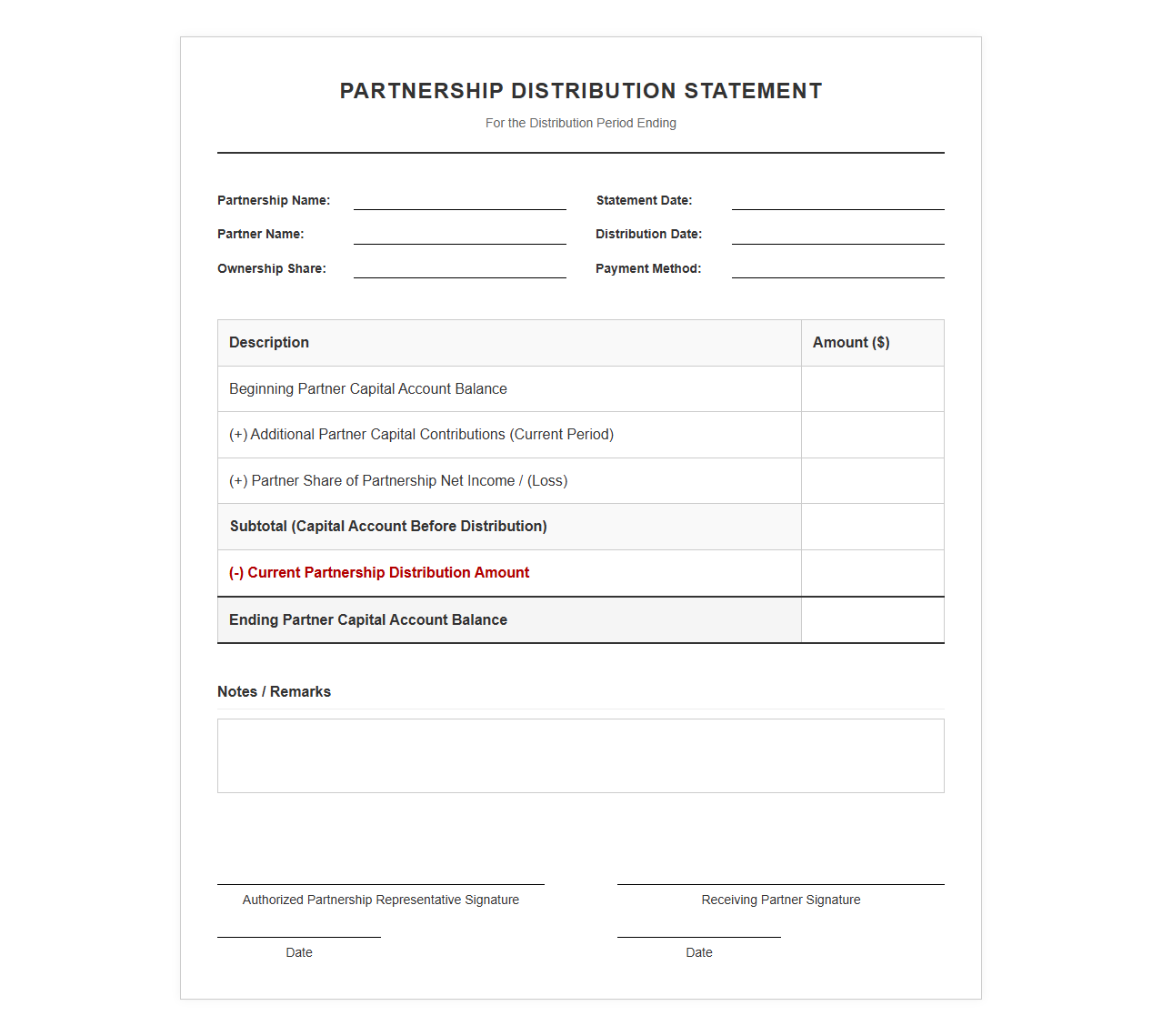

Partnership Distribution Statement Template

Download: .PDF

Download: .PDF

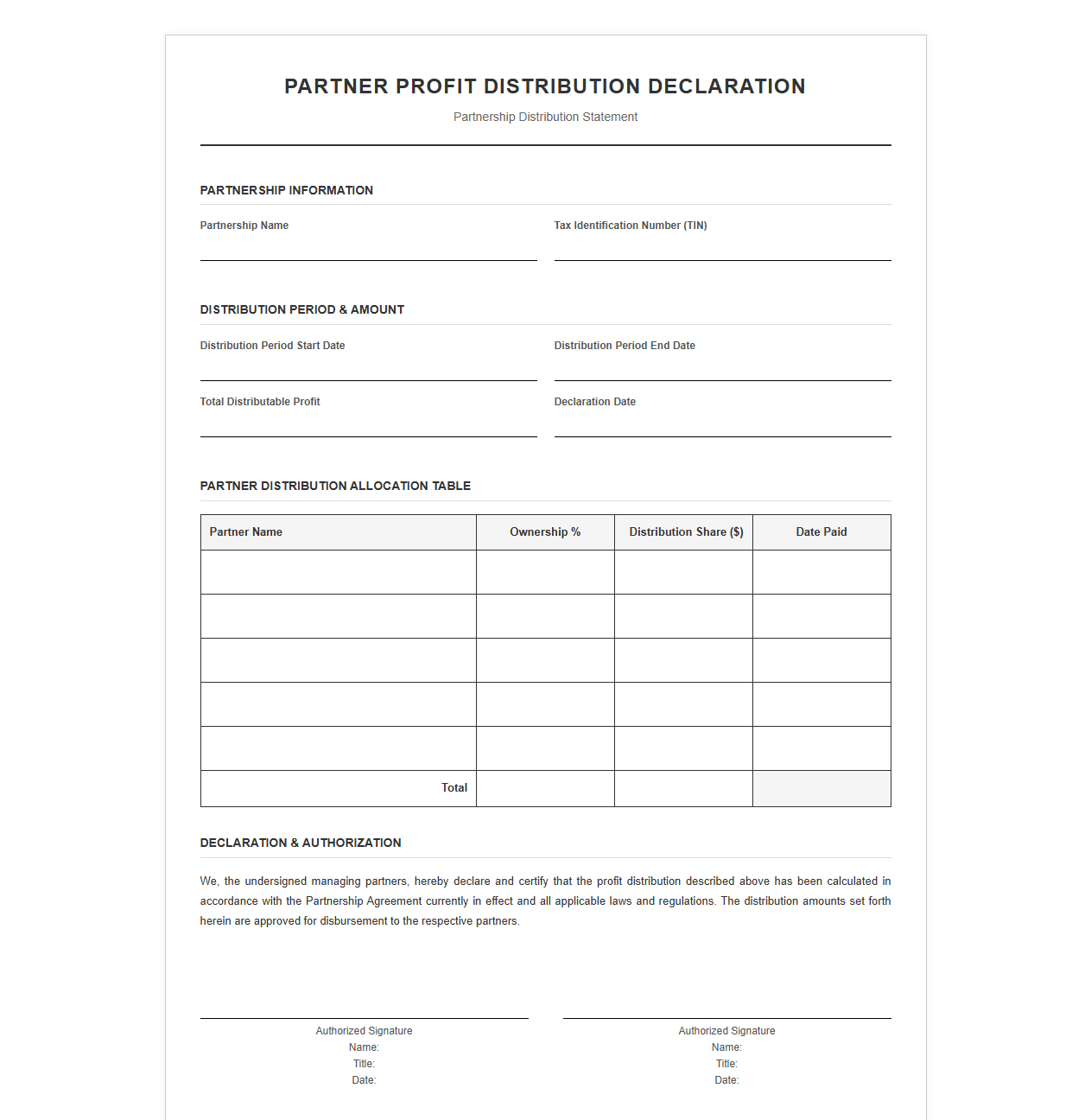

Partner Profit Distribution Declaration Form

Download: .PDF

Download: .PDF

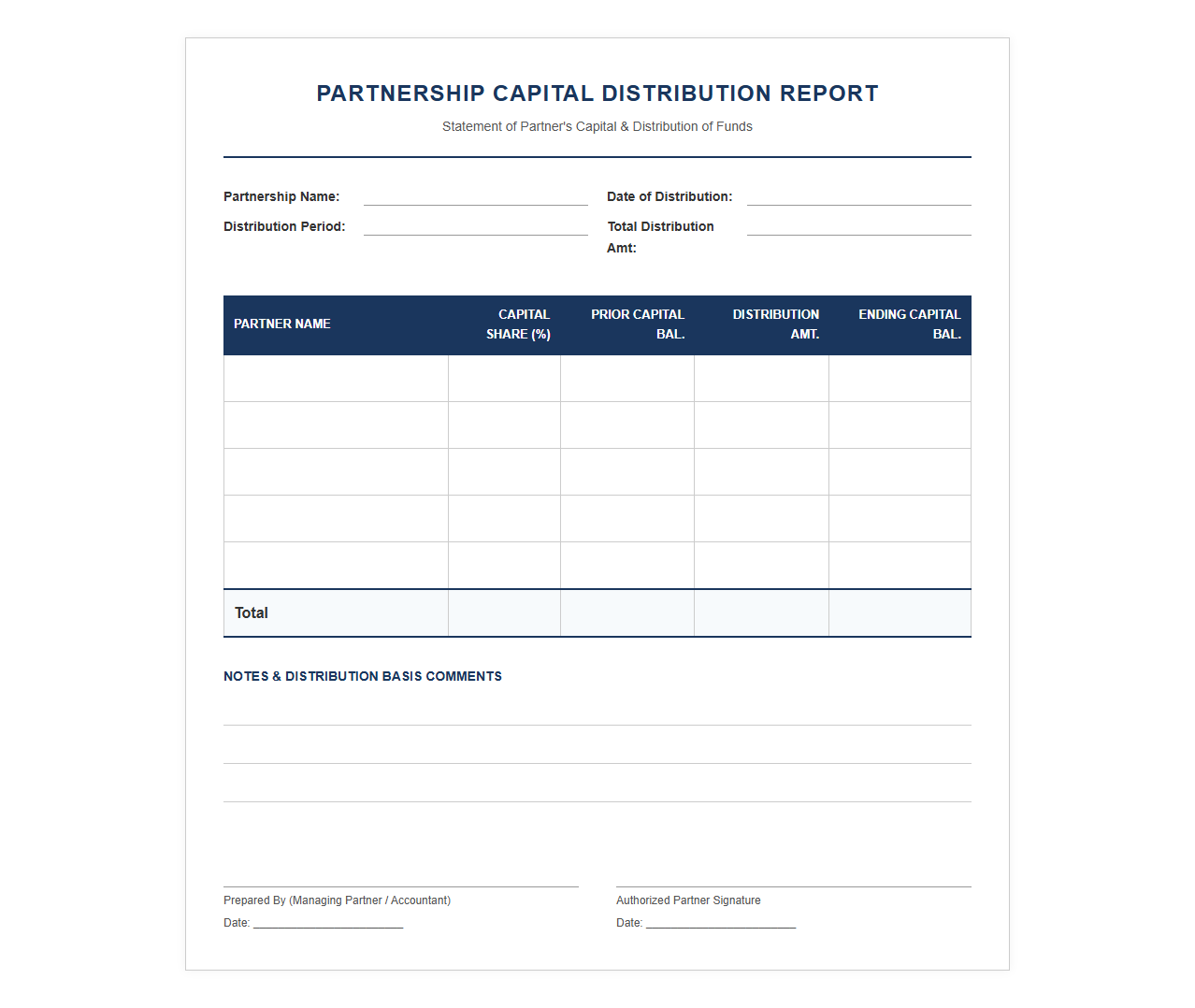

Partnership Capital Distribution Report Template

Download: .PDF

Download: .PDF

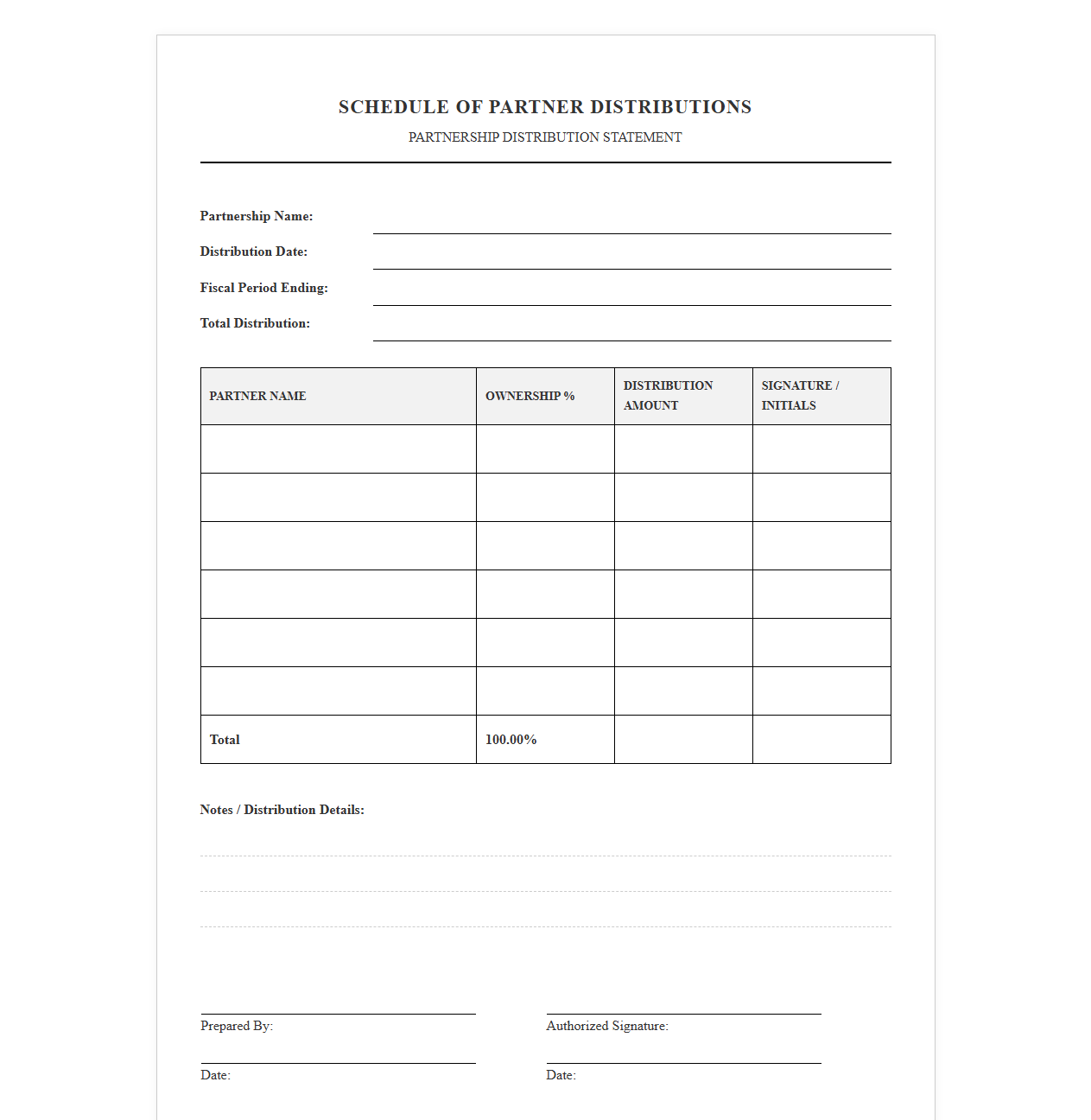

Schedule of Partner Distributions Document

Download: .PDF

Download: .PDF

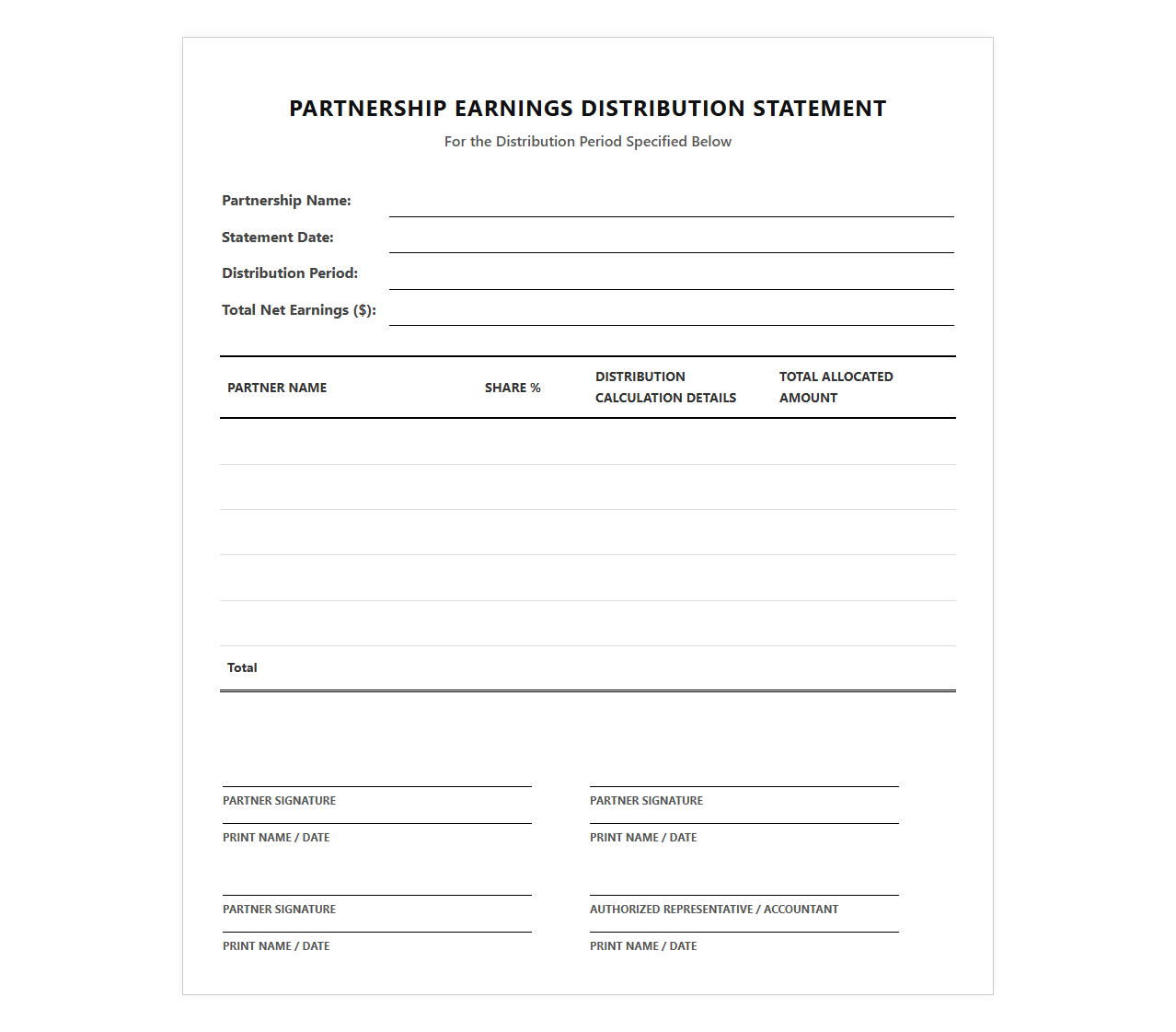

Partnership Earnings Distribution Statement

Download: .PDF

Download: .PDF

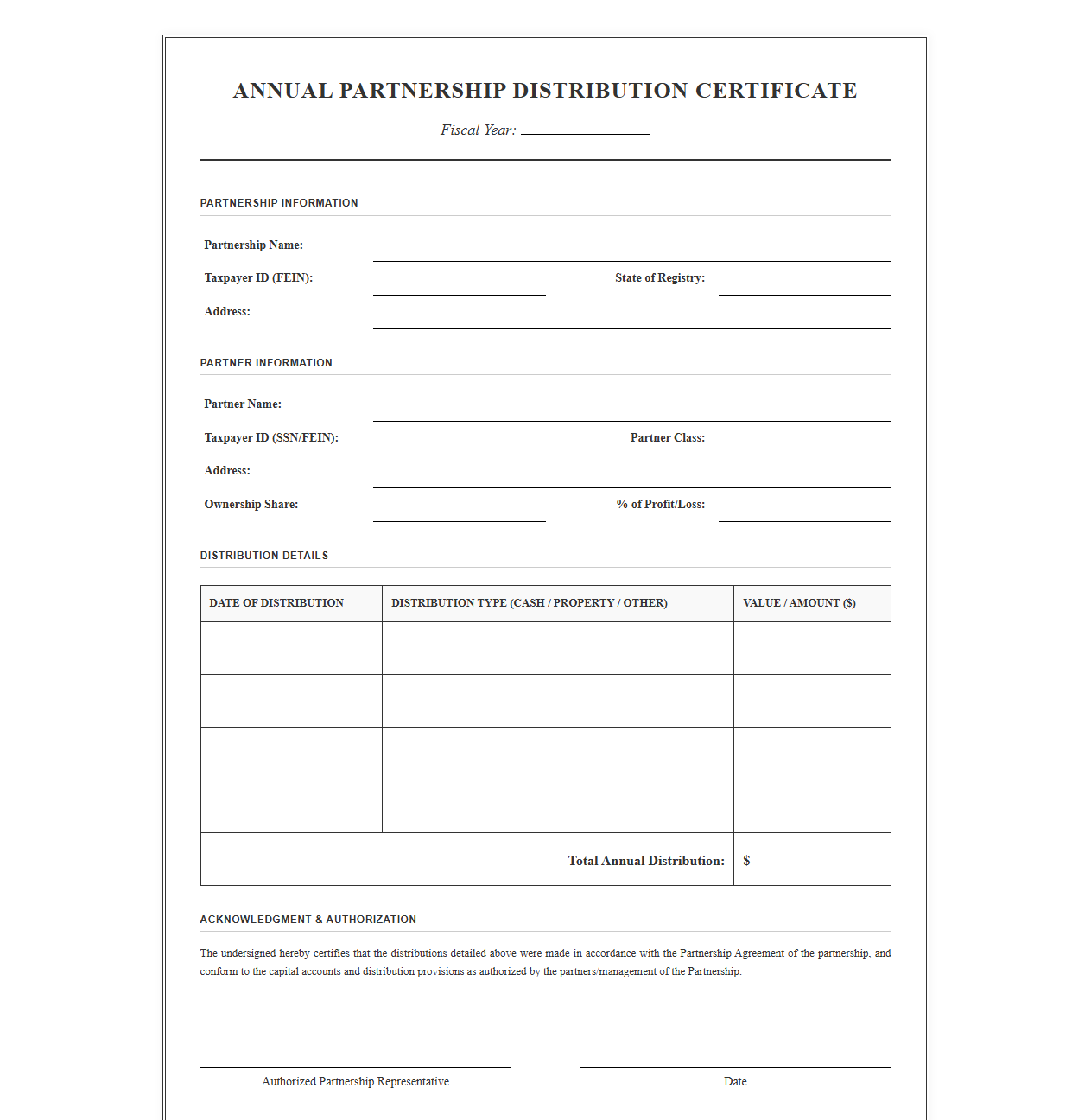

Annual Partnership Distribution Certificate

Download: .PDF

Download: .PDF

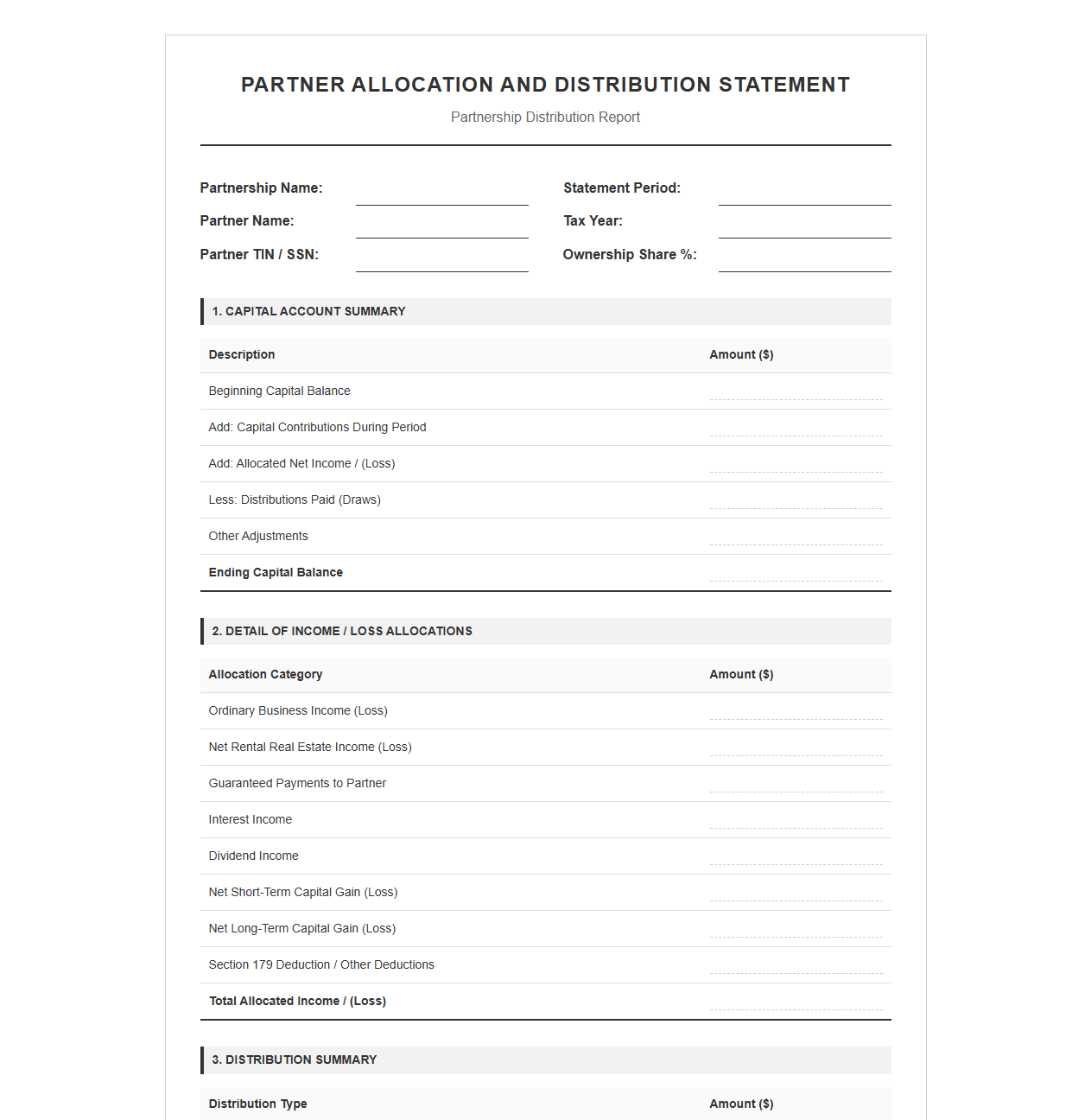

Partner Allocation and Distribution Statement

Download: .PDF

Download: .PDF

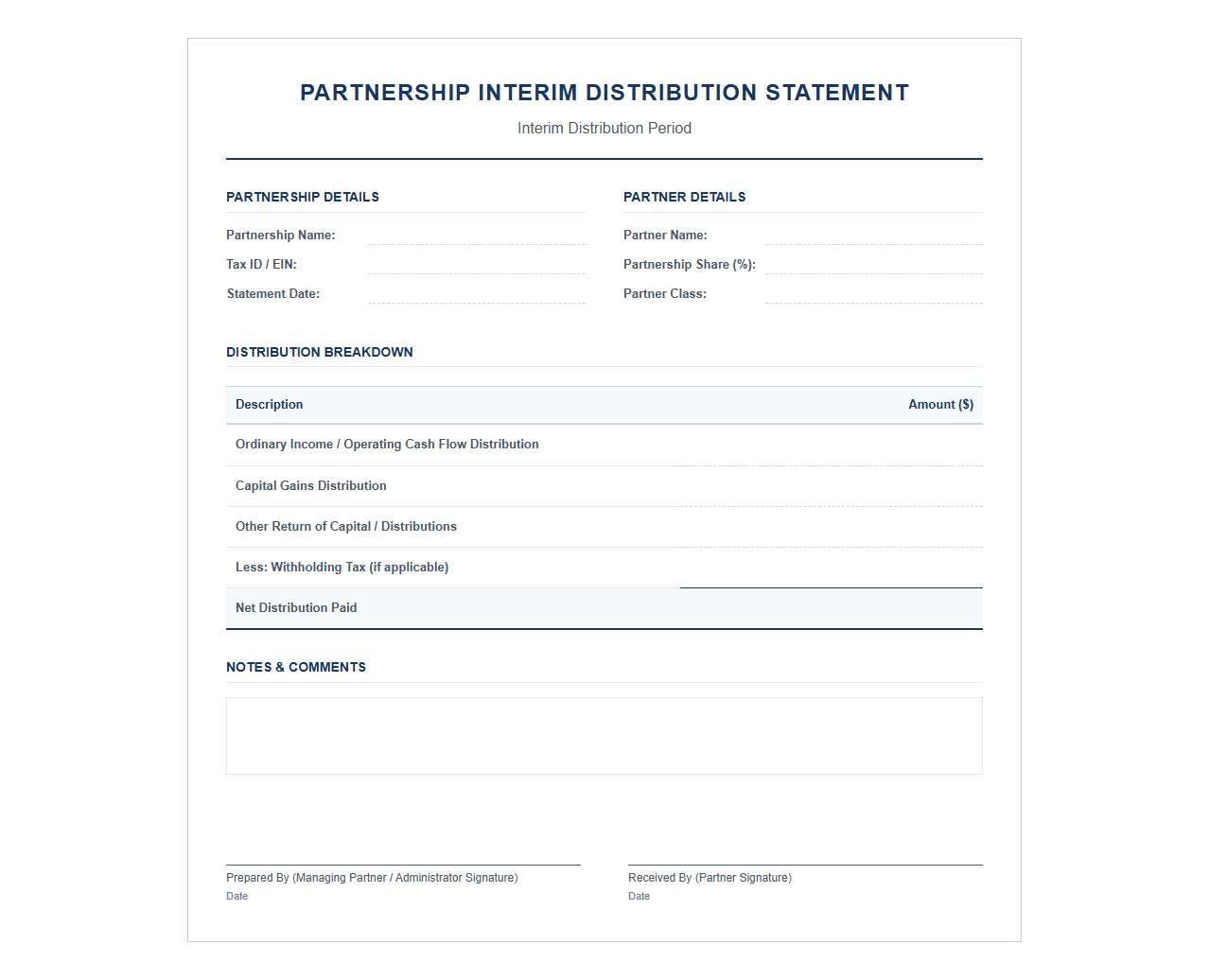

Partnership Interim Distribution Statement Template

Download: .PDF

Download: .PDF

Demystifying Partnership Distributions and Financial Complexity

Navigating the financial architecture of a multi-partner business often reveals significant friction points, particularly when calculating partnership distributions. Because partners may contribute varying levels of capital, intellectual property, or sweat equity, their financial returns rarely follow a simple, flat-rate division. This natural complexity is compounded when partners use disparate accounting methods-such as cash-basis versus accrual-basis accounting-leading to misaligned expectations, administrative bottlenecks, and potential disputes. To resolve these friction points, firms must adopt standardized statements that serve as a single source of truth, aligning all parties under a unified, transparent financial framework.

The Imperative for Standardized Distribution Statements

Relying on ad-hoc spreadsheet reports to calculate and communicate distributions introduces severe operational risks. When financial managers use non-standardized methods, the risk of experiencing unreconciled capital account discrepancies increases exponentially. These errors can lead to the misallocation of profits, which severely damages partner relations and erodes institutional trust.

Without a consistent, repeatable template, verifying the accuracy of historical calculations becomes nearly impossible. Standardizing these reports ensures that every stakeholder can clearly trace how cash flows from the partnership's net income directly into their individual accounts, eliminating ambiguity and fostering an environment of absolute transparency.

Core Elements of an Effective Distribution Template

To establish a reliable framework, a standardized partnership distribution statement must systematically track capital movements. An effective template provides a comprehensive snapshot of each partner's equity positioning over a specific period.

- Beginning Capital Balance: The starting equity position of the partner at the beginning of the financial period.

- Capital Contributions: Any additional cash or asset injections made by the partner during the period.

- Net Income/Loss Allocations: The partner's share of the partnership's earnings or losses, calculated based on the partnership agreement.

- Distributions: The actual cash or assets disbursed to the partner during the period.

- Ending Capital Balance: The finalized equity balance carried forward into the next accounting cycle.

Navigating Complex Allocation Waterfalls and Preferred Returns

Standardized templates must be robust enough to handle sophisticated equity arrangements. Multi-tiered distribution waterfalls, hurdle rates, and preferred returns often govern how cash is disbursed, requiring a highly structured, sequential approach to prevent calculation errors.

- First Tier (Preferred Return): Partners receive distributions up to a specified percentage of their contributed capital before any other allocations occur.

- Second Tier (Capital Return): Outstanding principal contributions are returned to the initial investors to reduce their capital risk.

- Third Tier (The Catch-Up): The general partners receive a disproportionate allocation until a specific GP/LP split ratio is satisfied.

- Fourth Tier (Residual Split): Remaining profits are distributed according to a predetermined percentage split among all partners.

Implementing Templates Within Existing Accounting Workflows

Integrating standardized templates into your current operational architecture requires a deliberate, step-by-step approach to avoid disrupting daily business activities.

First, evaluate your existing Enterprise Resource Planning (ERP) or accounting software to determine its capability to export clean, structured capital account data. During the data migration phase, carefully map historical partner transactions into the new standardized format to ensure continuity and balance accuracy.

Second, prioritize comprehensive staff training. Financial personnel must be fully educated on the mechanics of the new templates, ensuring they understand the underlying formulas and data entry protocols. This safeguards the system against manual input errors and maintains report integrity over time.

Ensuring Regulatory Compliance and Audit Readiness

Standardized financial reporting does more than resolve internal queries; it is a critical defense mechanism against regulatory scrutiny. Clear distribution records directly streamline the preparation of Schedule K-1 forms, reducing the risk of costly tax filing errors and processing delays.

"Inconsistent capital account reporting is one of the primary triggers for regulatory audits. Partnerships must maintain clear, standardized trails of all distributions and capital allocations to demonstrate compliance with internal revenue codes."

By keeping standardized, auditable records of all transactions, the partnership protects itself and its individual partners from the complications of internal disputes or external tax audits.

Achieving Long-Term Partnership Harmony Through Clarity

Clear, consistent, and structured financial reporting is the foundation of any enduring business alliance. When partners receive transparent, easily understood distribution statements, speculation is replaced by trust, and the potential for costly legal disputes is virtually eliminated.

Providing partners with unambiguous insights into how their capital is managed ensures that everyone remains aligned with the firm's broader strategic goals, paving the way for sustainable growth and long-term financial stability.

Leave a comment