Managing shareholder reporting for complex equity structures often introduces severe administrative bottlenecks. Finance teams routinely struggle to accurately calculate cumulative dividends, track liquidation preferences, and report conversion ratios under tight regulatory deadlines. Before streamlining these workflows, organizations must first align their internal data with the increasingly rigorous demands of modern accounting standards. By establishing a standardized reporting framework, issuers grant stakeholders immediate, transparent clarity into their equity value, reinforcing institutional trust.

Please note that while these resources provide robust analytical frameworks, they must be customized to align with your specific corporate charter. To demonstrate their practical application, this article examines concrete templates modeled for complex scenarios, including participating preferred distributions and weighted-average anti-dilution adjustments.

In the following sections, we will break down these essential statement templates and outline step-by-step methodologies to simplify your reporting cycle, mitigate compliance risks, and elevate your investor relations.

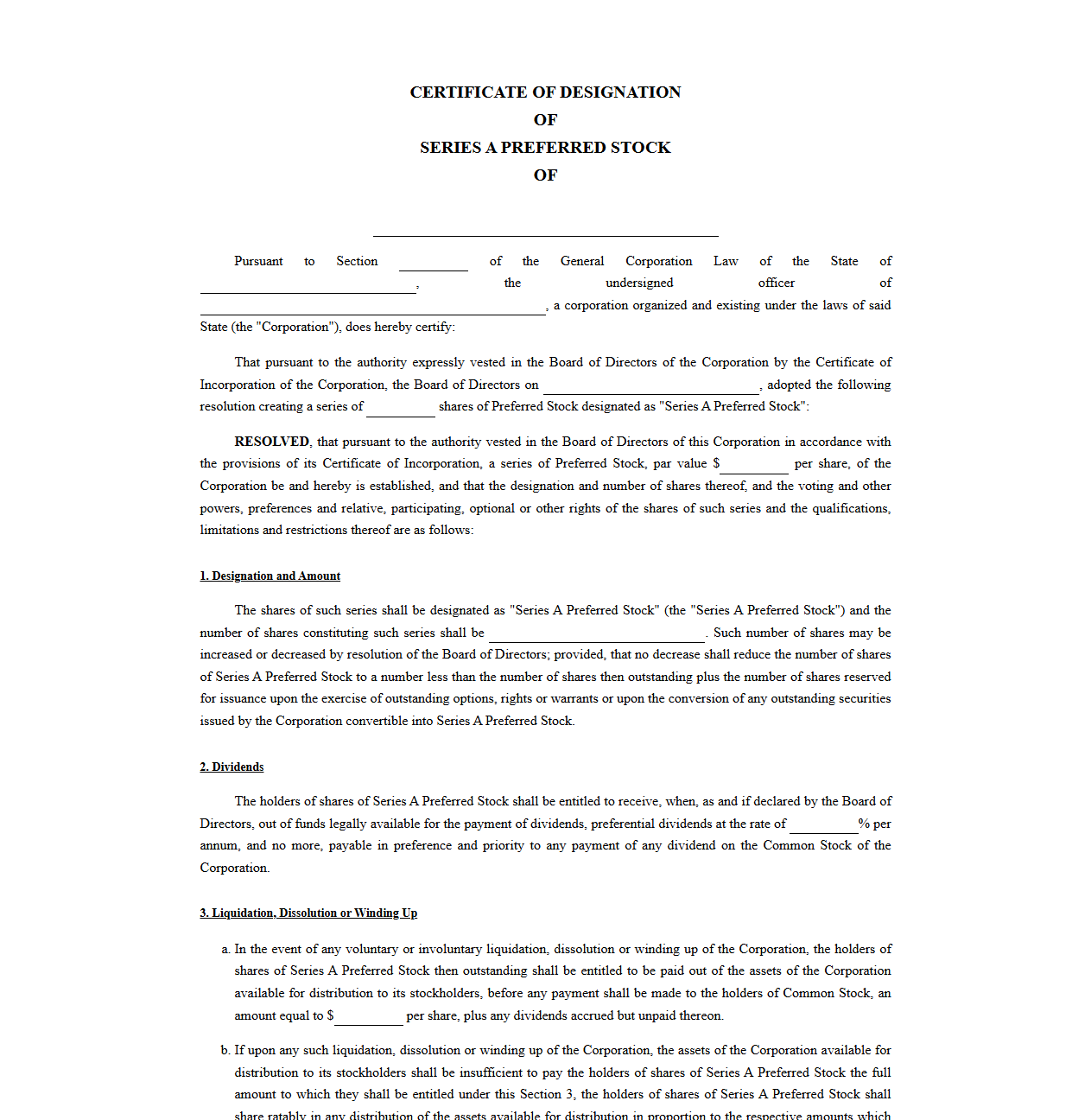

Series A Preferred Stock Certificate of Designation Template

Download: .PDF

Download: .PDF

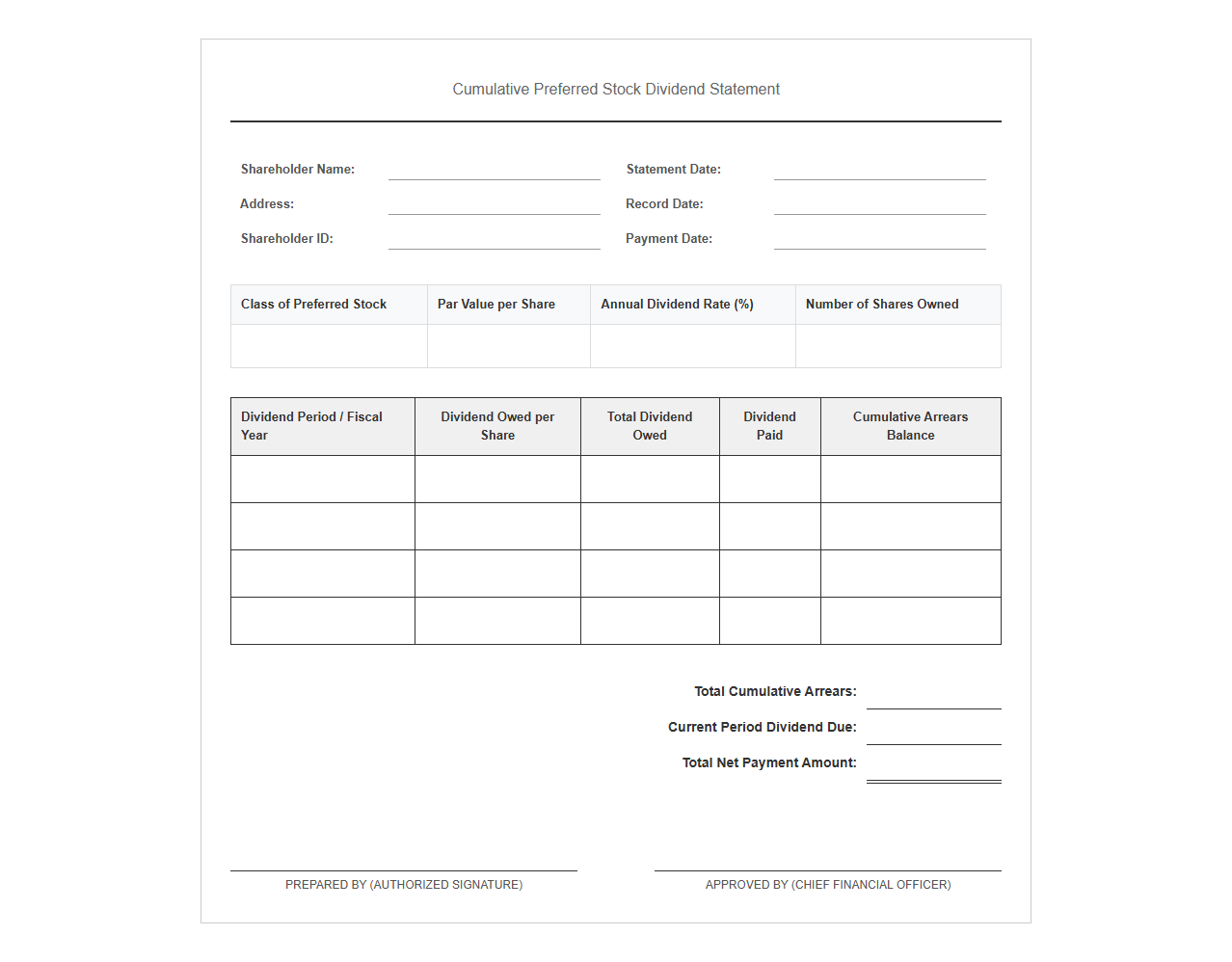

Cumulative Preferred Stock Dividend Statement Template

Download: .PDF

Download: .PDF

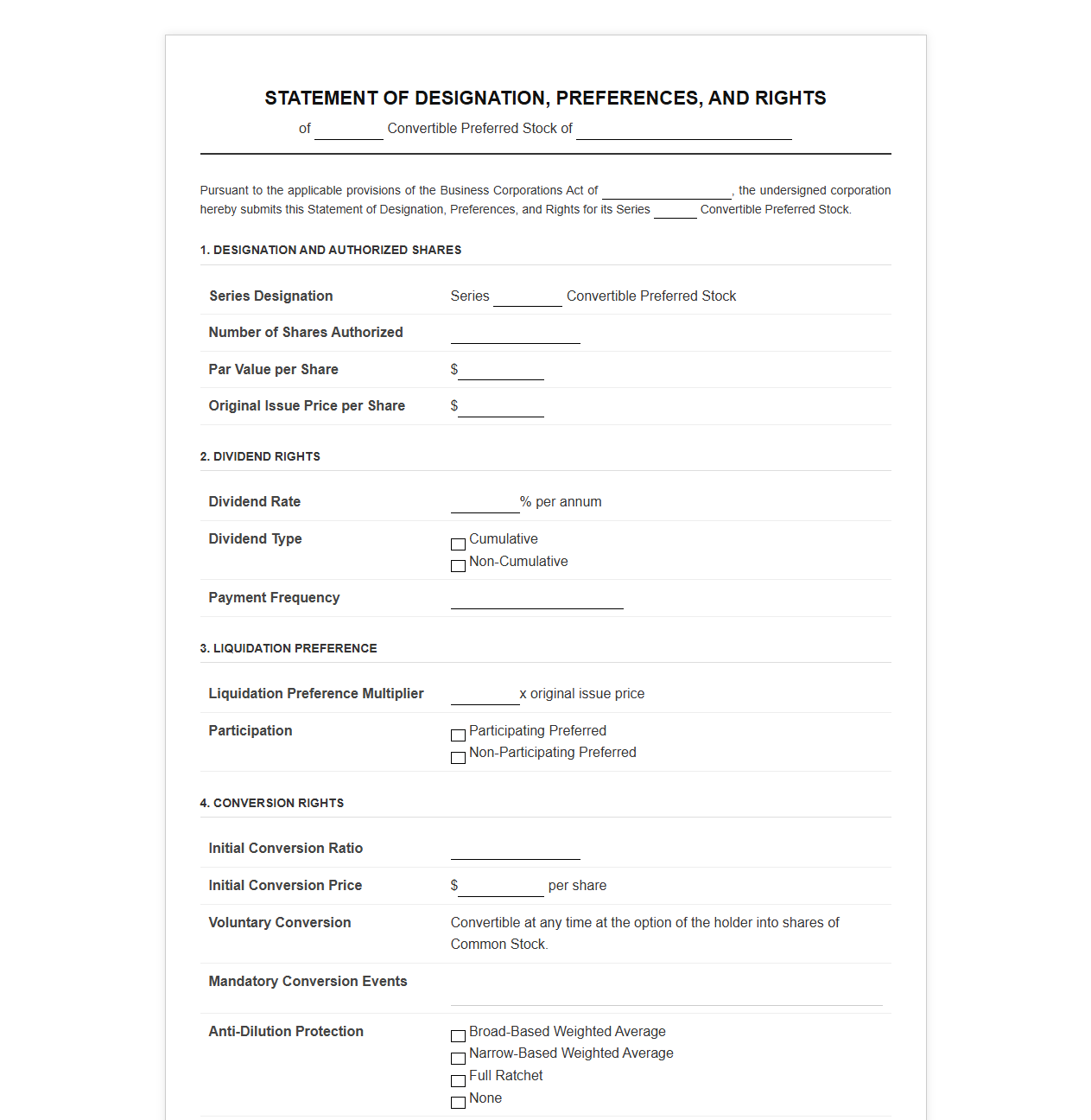

Convertible Preferred Stock Terms Statement Template

Download: .PDF

Download: .PDF

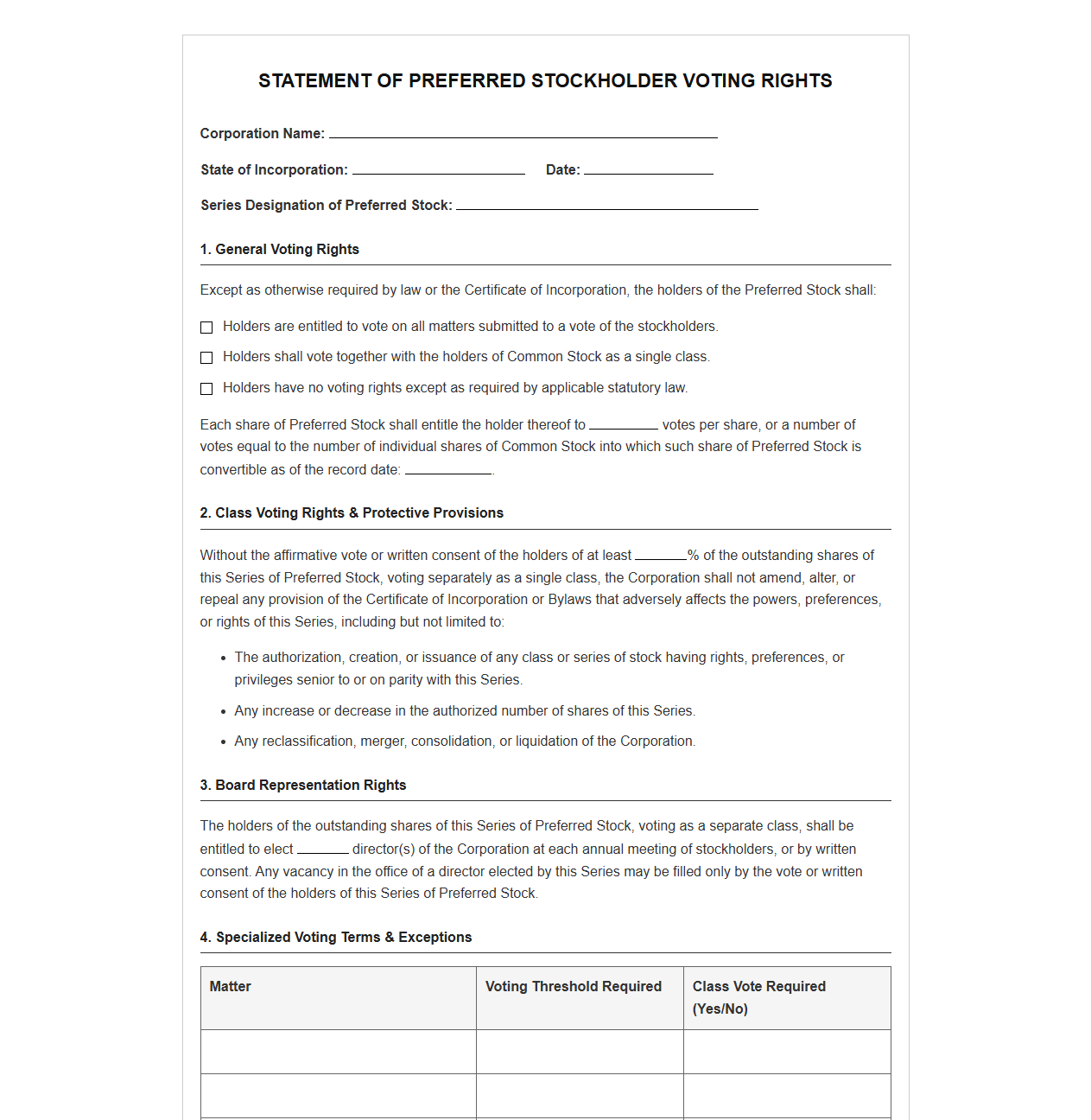

Preferred Stockholder Voting Rights Statement Template

Download: .PDF

Download: .PDF

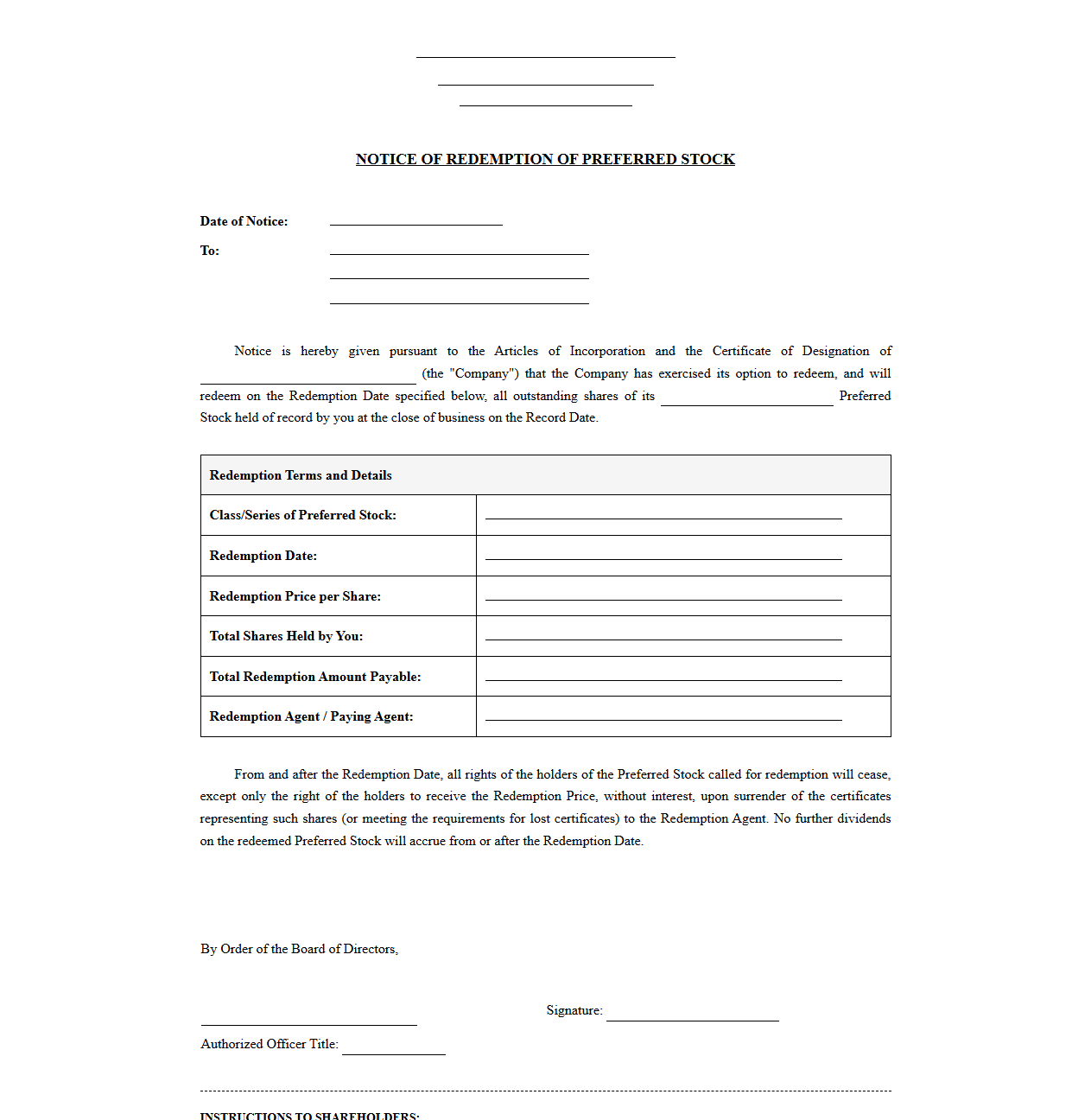

Preferred Stock Redemption Notice Statement Template

Download: .PDF

Download: .PDF

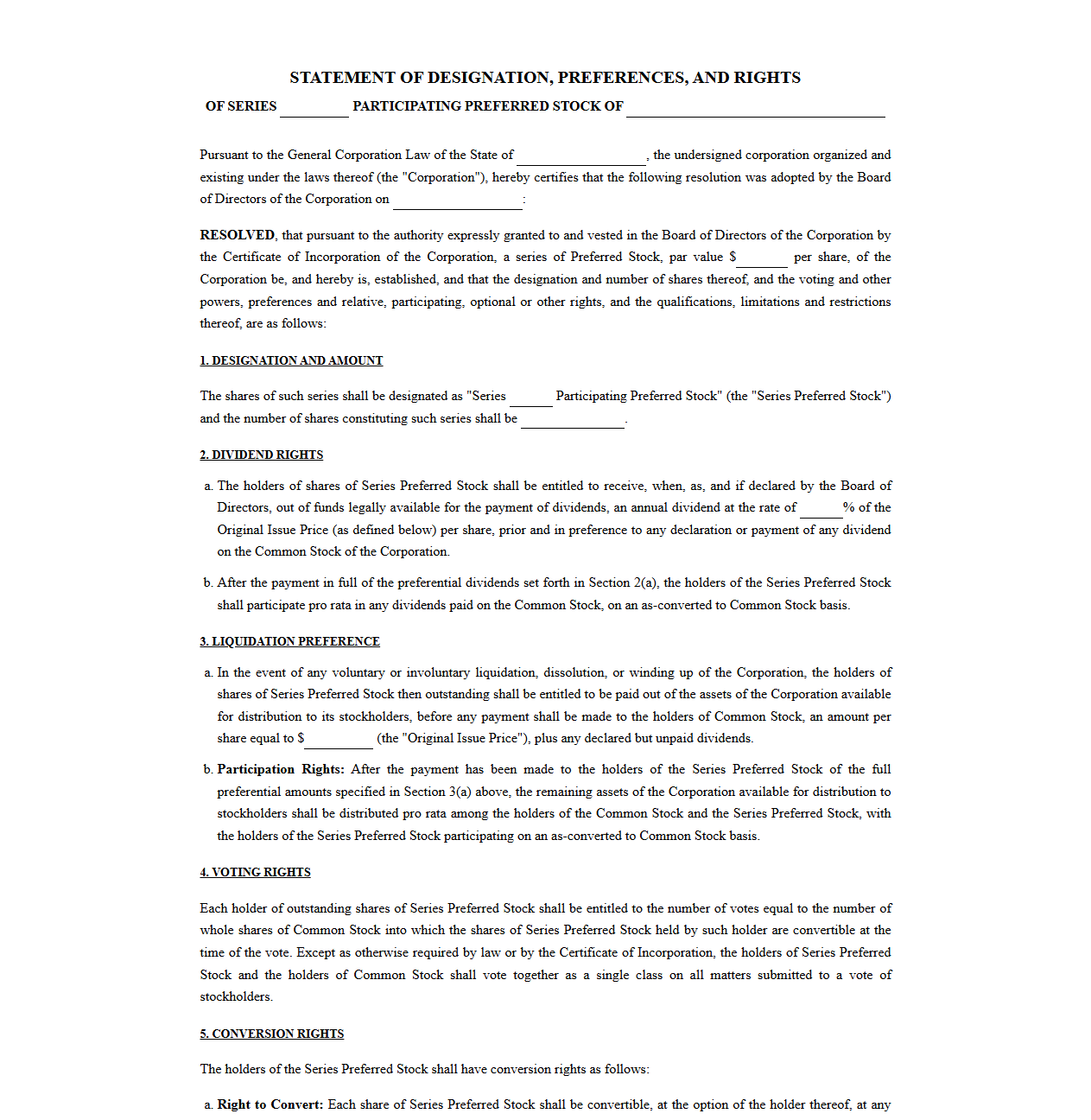

Participating Preferred Stock Agreement Statement Template

Download: .PDF

Download: .PDF

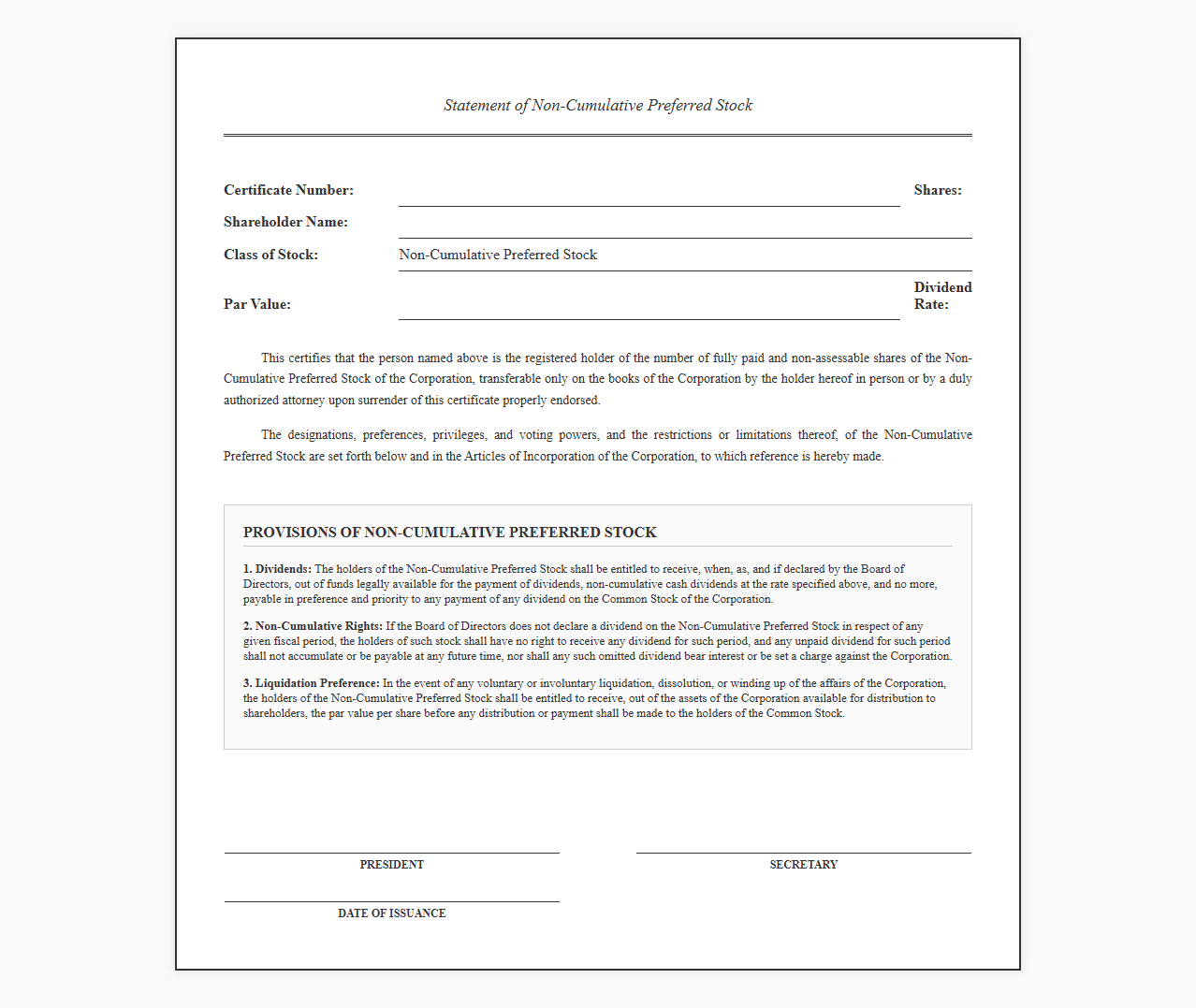

Non Cumulative Preferred Stock Statement Template

Download: .PDF

Download: .PDF

Preferred Stock Certificate of Designation Statement Template

Download: .PDF

Download: .PDF

Understanding Preferred Stock Complexity in Shareholder Reporting

Preferred stock occupies a unique, transitional space in corporate finance. It represents a hybrid financial instrument that blends the steady income characteristics of debt with the ownership and equity upside typical of common stock. Consequently, this dual nature introduces significant accounting and reporting challenges when preparing annual shareholder equity statements.

For financial reporters, classifying these instruments requires navigating complex accounting standards. Certain redemption features can trigger a reclassification from equity to liabilities under both GAAP and IFRS. Accurate reporting demands a deep understanding of how these shares impact the statement of changes in stockholders' equity, dilution calculations, and earnings-per-share (EPS) metrics.

Cumulative vs. Non-Cumulative Dividend Allocation Statement

To ensure transparent reporting of distributions, corporations must carefully track whether preferred shares carry cumulative or non-cumulative rights. Cumulative features require that any unpaid dividends from prior periods accumulate as dividends in arrears, which must be fully satisfied before any distributions can be made to common shareholders. The template below outlines the reporting mechanism for allocating current-period distributions and tracking outstanding arrearages.

| Share Class Name | Cumulative Status | Prior Arrearages ($) | Current Period Allocation ($) | Total Paid Out ($) | Remaining Arrearages ($) |

|---|---|---|---|---|---|

| Class A Preferred | Cumulative | 150,000 | 50,000 | 200,000 | 0 |

| Class B Preferred | Non-Cumulative | 0 | 75,000 | 50,000 | 0 |

| Class C Preferred | Cumulative | 80,000 | 40,000 | 30,000 | 90,000 |

Liquidation Preference and Waterfall Distribution Template

During a liquidation event, preferred shareholders hold priority over common shareholders regarding the distribution of assets. This liquidation preference is often expressed as a multiple of the original issuance price. Furthermore, participating features may allow preferred holders to share in remaining assets alongside common holders after receiving their preference payout. The following template demonstrates the payment waterfall sequence under standard liquidation terms.

| Tranche Priority | Equity Class | Liquidation Preference Multiple | Participating Feature | Maximum Cap Amount ($) |

|---|---|---|---|---|

| Senior Priority 1 | Series A Preferred | 1.0x | Non-Participating | 15,000,000 |

| Junior Priority 2 | Series B Preferred | 2.0x | Fully Participating | Unlimited |

| Residual Priority 3 | Common Stock | N/A | N/A | Residual Assets |

Conversion and Redemption Feature Disclosures

Preferred stock terms frequently incorporate options that allow either the issuer or the holder to convert or redeem the shares. Disclosing these conditions clearly in the financial notes prevents misinterpretation of potential dilutive events and cash outflow commitments.

- Conversion Ratio and Adjustment Formulas: Series A shares are convertible into common stock at an initial ratio of 1:1, subject to broad-based weighted-average anti-dilution adjustments in the event of down-round financing.

- Optional Redemption Clauses: The issuer retains the right to redeem Class B preferred shares at any point after the fifth anniversary of issuance at a premium price of 105% of par value.

- Mandatory Redemption Schedules: Class C preferred shares require mandatory redemption on December 31, 2029, requiring a cash outflow of par value plus all unpaid accrued dividends.

Voting Rights and Class-Specific Governance Reporting

Although preferred stock typically does not carry broad voting rights, certain classes hold protective provisions and specific governance influence. These provisions ensure that key corporate changes cannot occur without explicit approval from a designated majority of the preferred share classes.

- Class-specific voting rights: Preferred holders vote on an as-converted basis alongside common shareholders on general corporate matters, except where class voting is legally required.

- Protective provisions: The company cannot issue senior debt, modify the articles of incorporation, or authorize a class of stock with senior rights without the approval of at least 66% of the Series A holders.

- Special board representation rights: Series B preferred shareholders, voting as a separate class, hold the exclusive right to elect two directors to the corporate board of directors at each annual meeting.

Balance Sheet Presentation and Footnote Disclosures

Preferred Stock Footnote Presentation

Financial reporting guidelines dictate that companies disclose the key characteristics of their preferred equity directly on the face of the balance sheet or within the accompanying footnotes. This standardizes how institutional investors evaluate corporate capital structures.

Note 8: Preferred Stock Capital Structure - As of December 31, 2023, the Company has authorized 10,000,000 shares of preferred stock, par value $0.001 per share. Of the authorized amount, 2,500,000 shares are designated as Series A Cumulative Convertible Preferred Stock, with a liquidation preference of $10.00 per share. As of the reporting date, 1,200,000 shares of Series A are issued and outstanding, carrying a total carrying value of $12,000,000.

Streamlining Shareholder Communication and Audit Readiness

Establishing a repeatable framework for preferred stock reporting minimizes friction during year-end reconciliation. To build audit readiness and ensure alignment with both GAAP and IFRS, accounting teams should implement structured control checklists. This proactive preparation ensures that complex calculations regarding dividend allocations, conversion pricing, and redemption liabilities are easily verified by external auditors.

Maintaining clear historical documentation of original stock purchase agreements remains the most effective method to avoid disputes with institutional shareholders. By formalizing these tracking procedures, companies can confidently present their capital structure to the public while ensuring compliance with complex regulatory standards.

Read More

Leave a comment