Finance teams frequently grapple with the anxiety of unpredictable cash crunches, spending exhausting hours manually consolidating disparate spreadsheets only to find that historical data offers little guidance for future solvency. Before resolving this complexity, organizations must first recognize that a resilient forecasting model relies on linking operational drivers directly to liquidity. Embracing structured projected cash flow statement templates grants decision-makers the immediate foresight required to navigate capital constraints and fund growth initiatives confidently.

However, these models are not self-sustaining solutions; their predictive power is strictly conditional upon the accuracy of your baseline inputs. For instance, factoring in precise client payment lag times or seasonal inventory build-ups is essential to prevent misleading surpluses. In this guide, we will analyze the core architecture of high-performing cash flow templates, outline customization strategies for various business models, and demonstrate how to turn raw projections into actionable strategic directives.

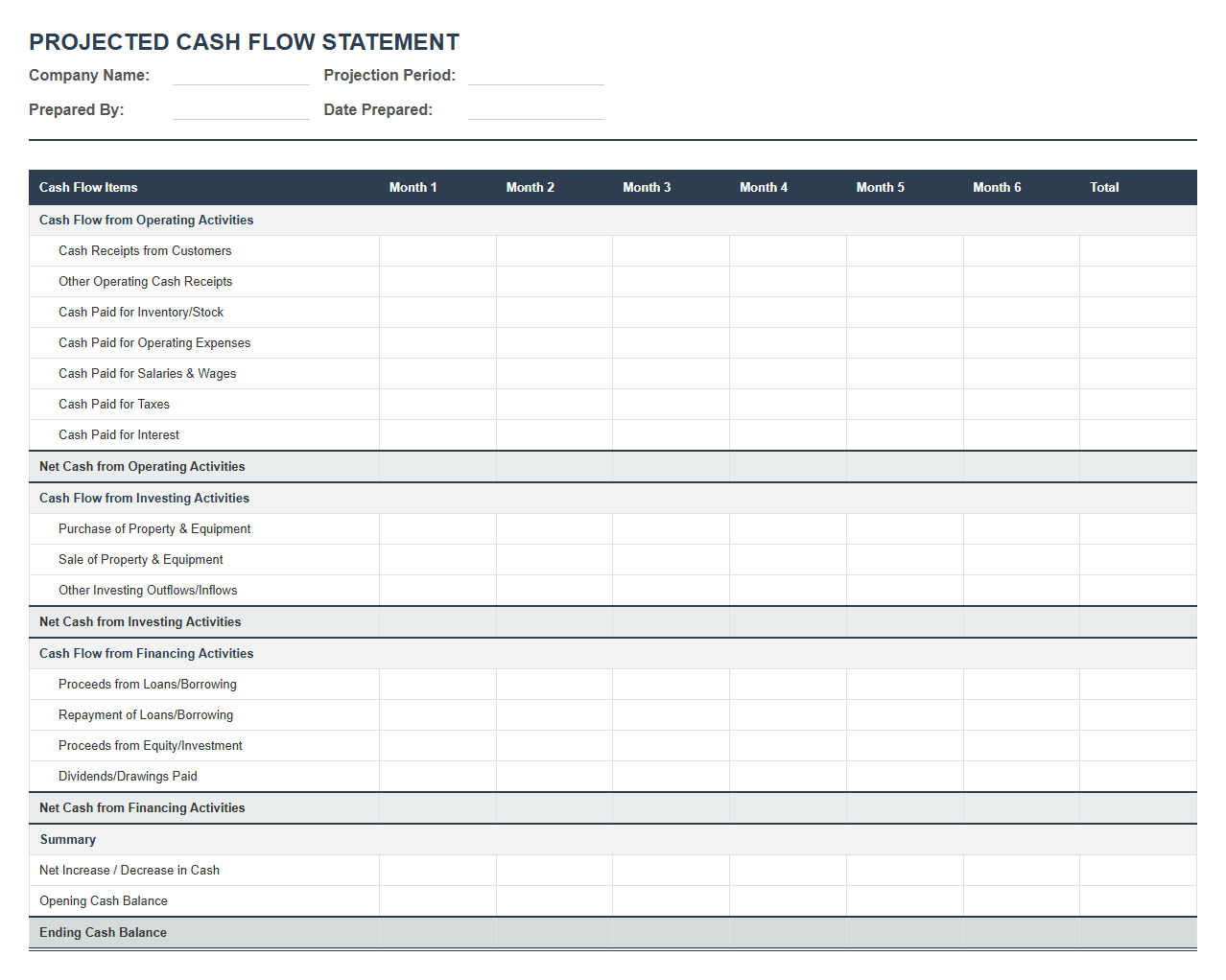

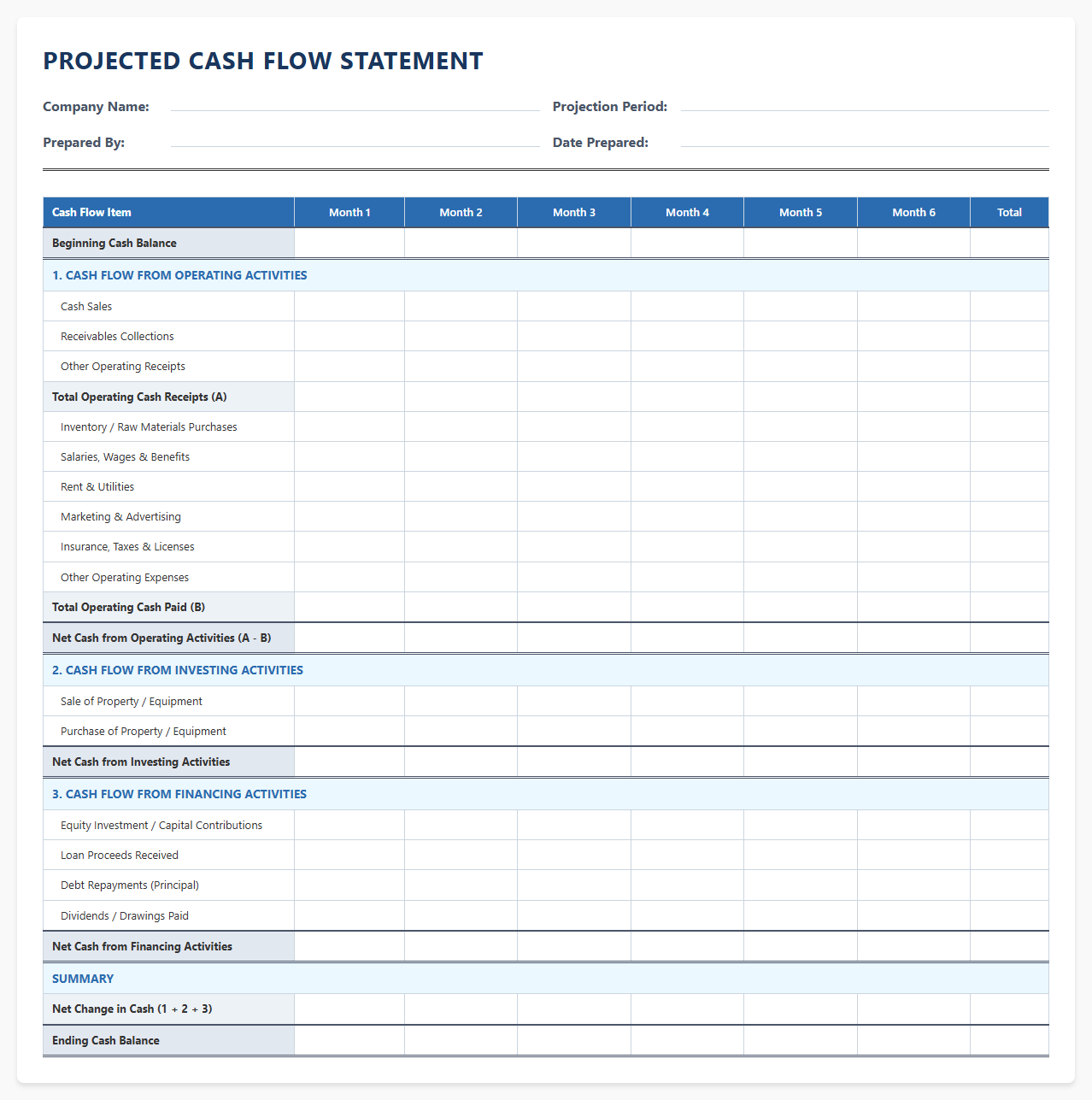

Projected Cash Flow Statement Template

Download: .PDF

Download: .PDF

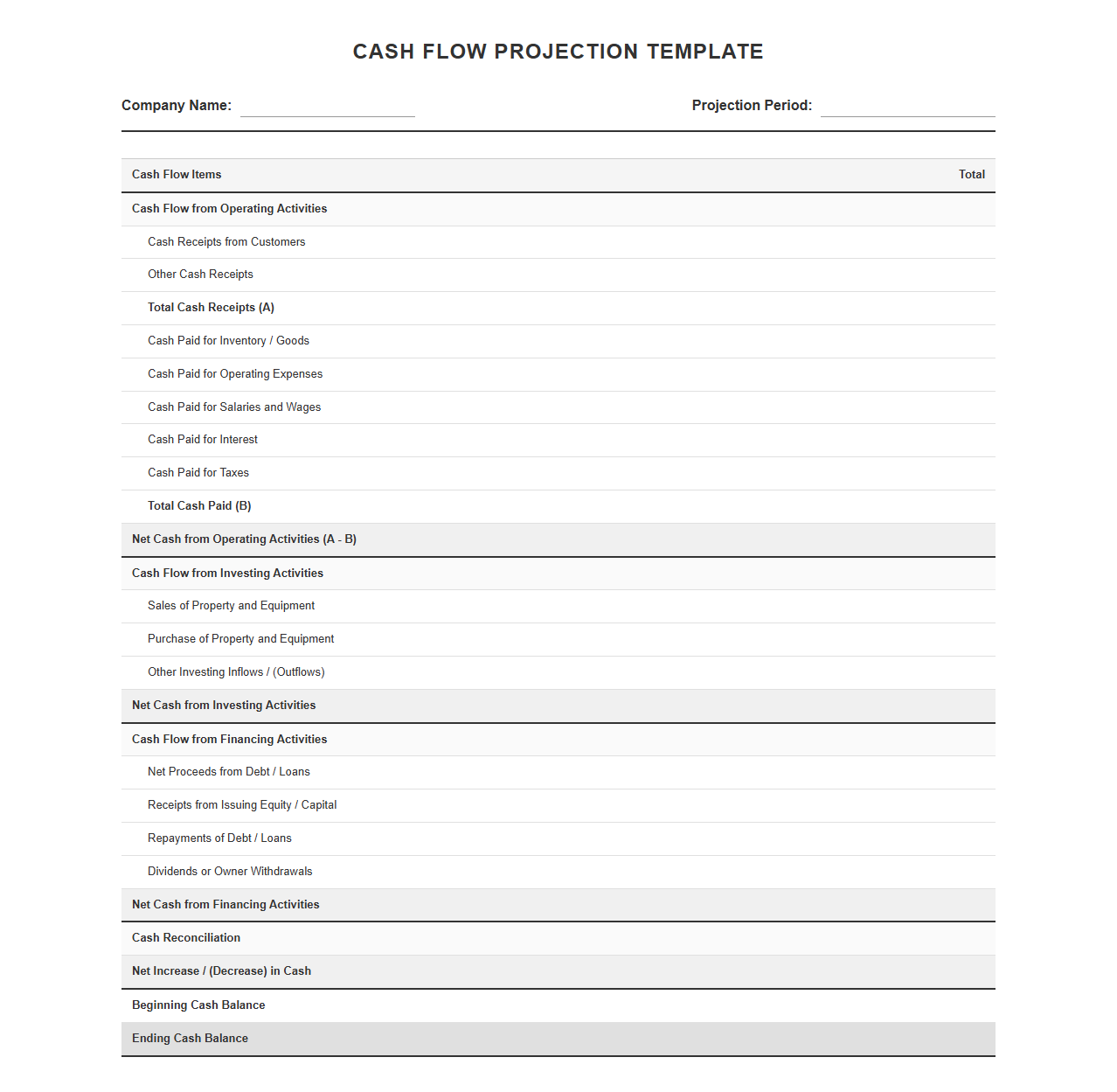

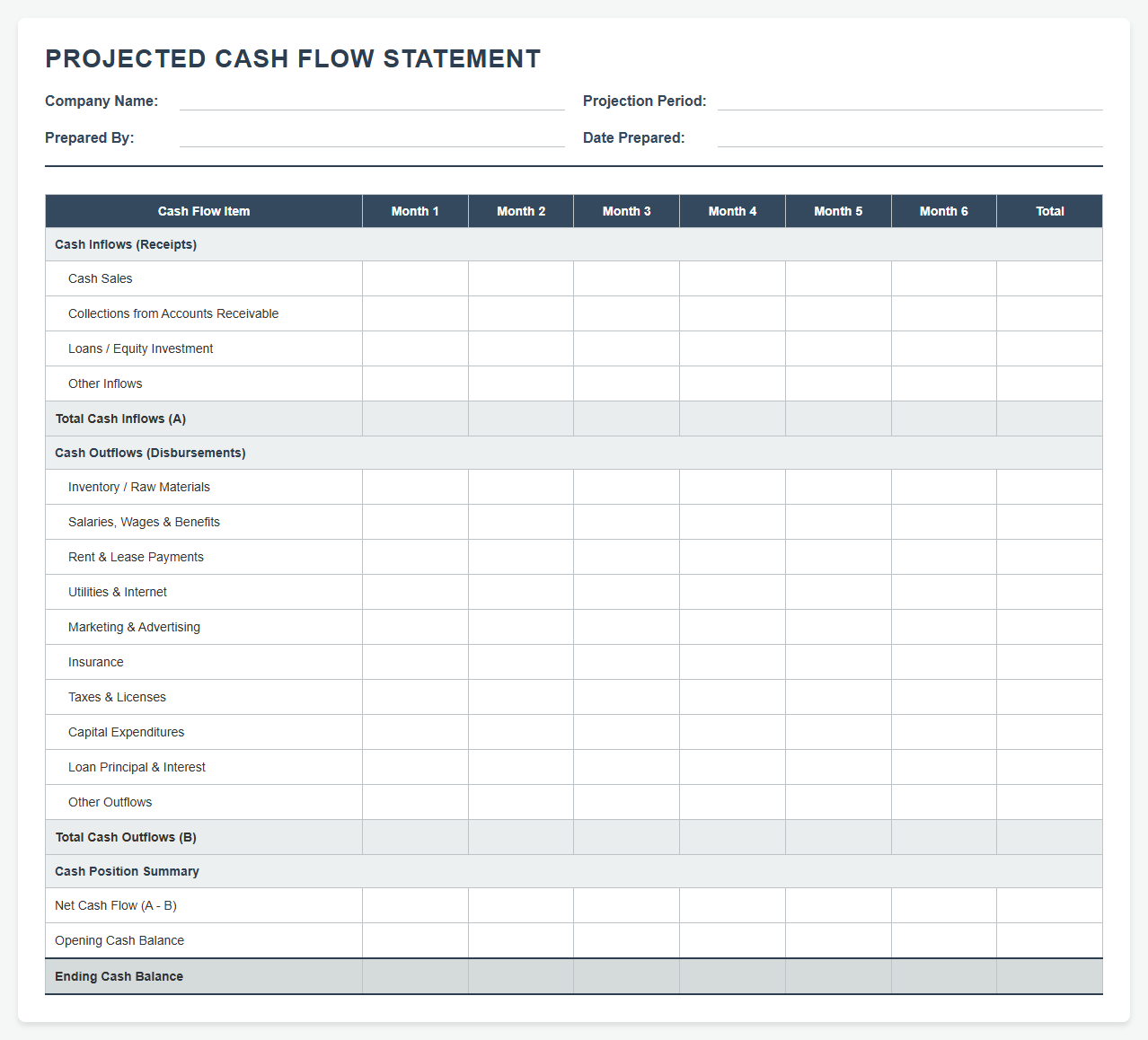

Cash Flow Projection Statement Template

Download: .PDF

Download: .PDF

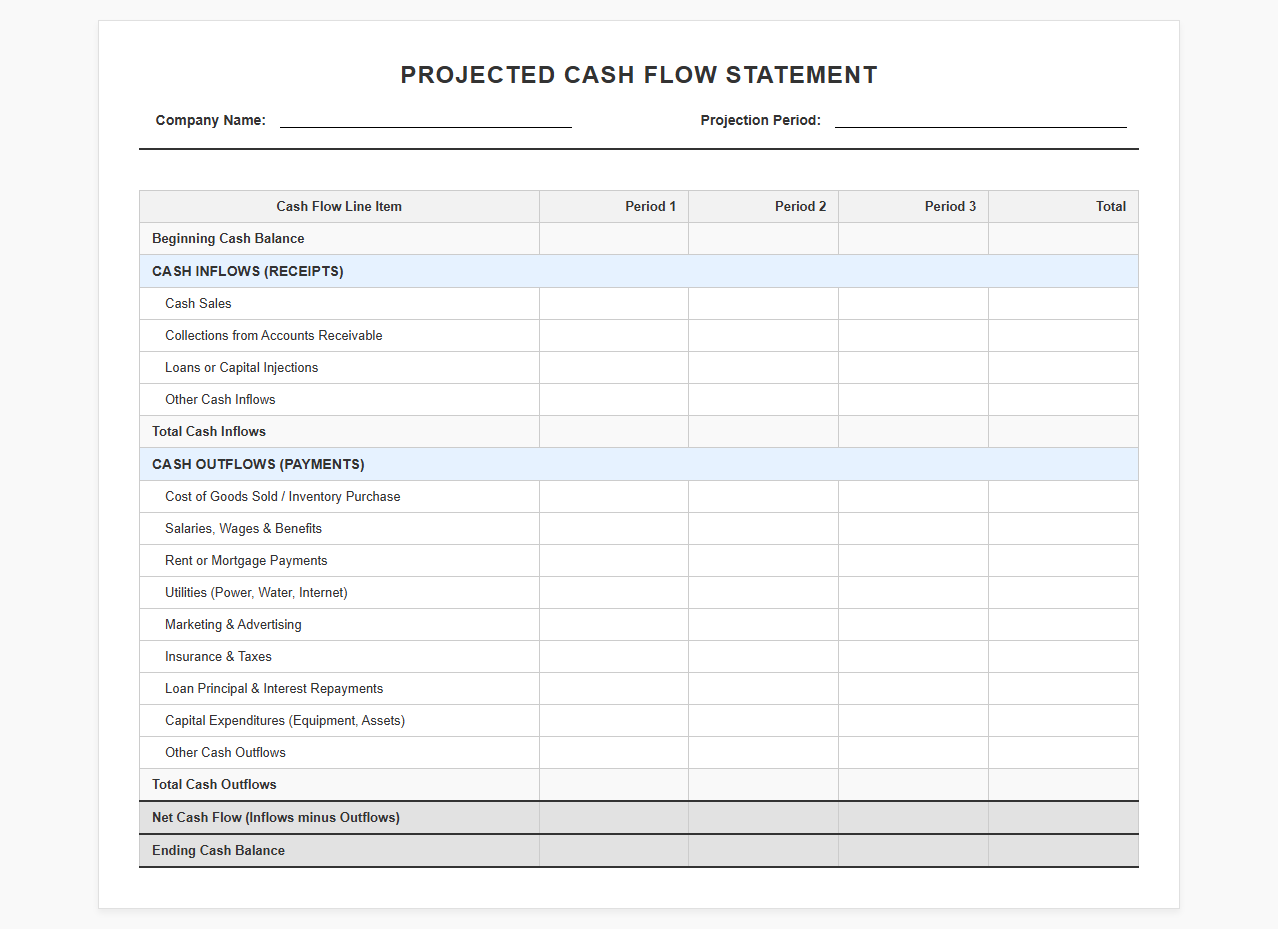

Forecasted Cash Flow Statement Template

Download: .PDF

Download: .PDF

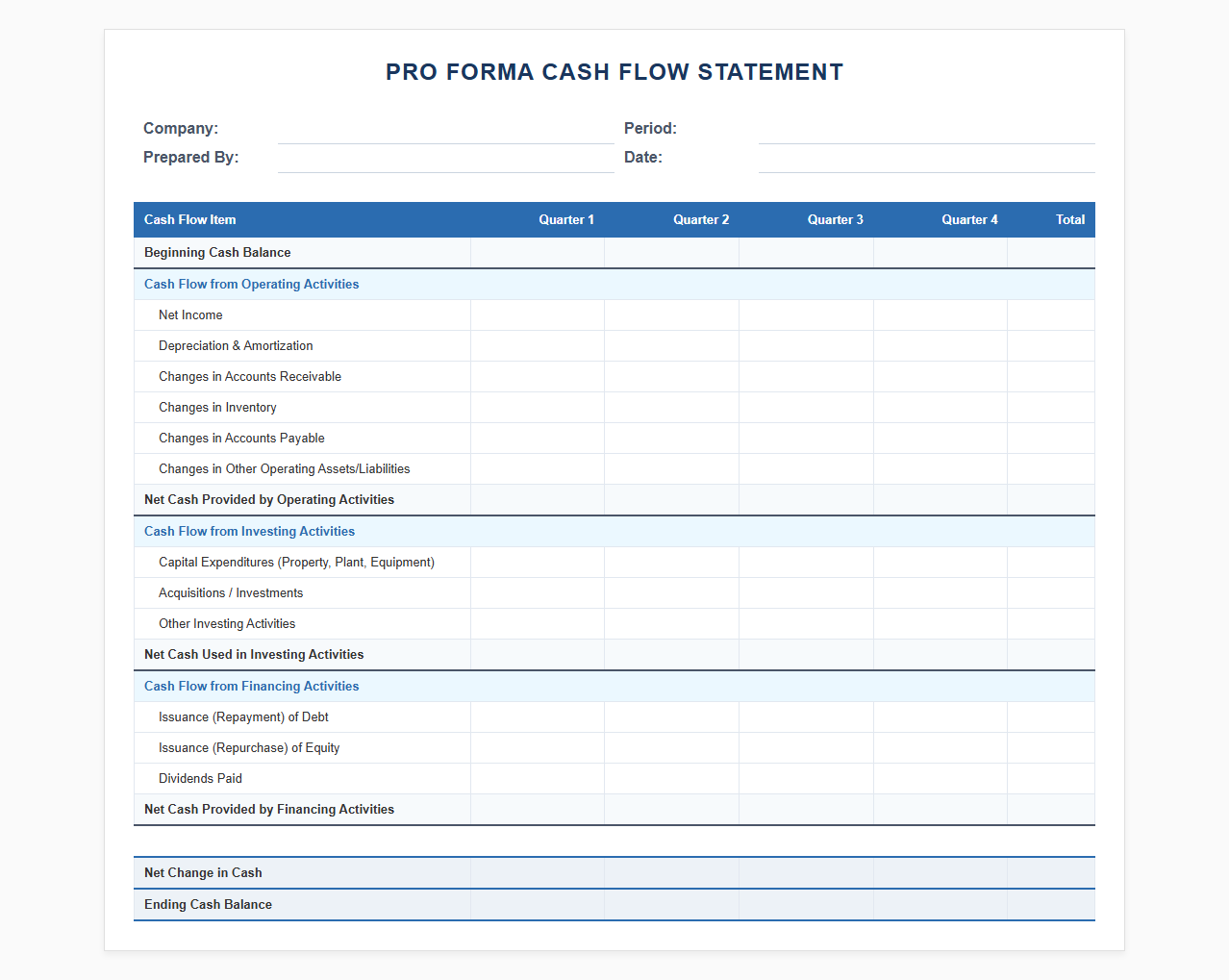

Pro Forma Cash Flow Statement Template

Download: .PDF

Download: .PDF

Cash Flow Forecasting Statement Template

Download: .PDF

Download: .PDF

Future Cash Flow Statement Template

Download: .PDF

Download: .PDF

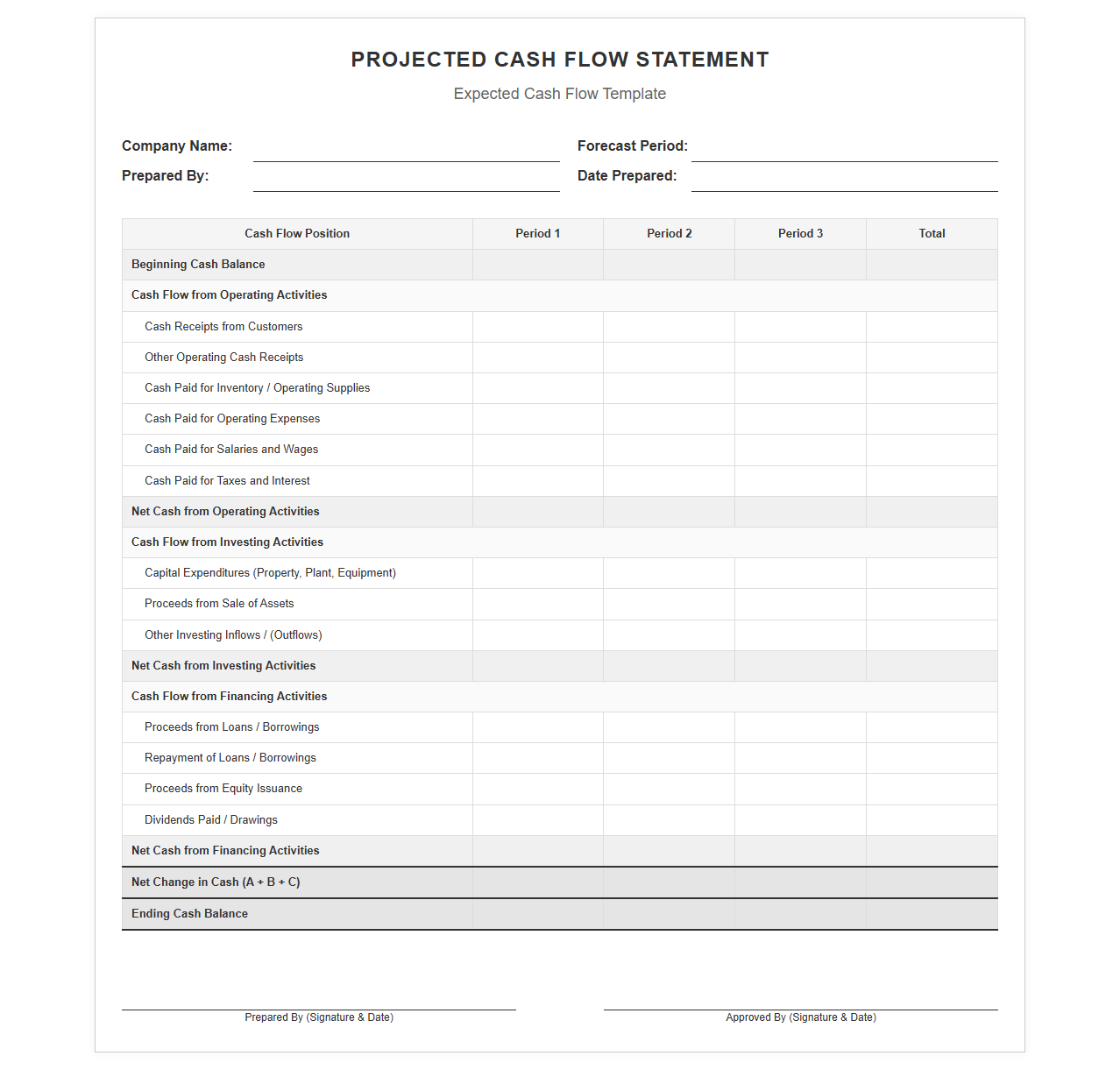

Expected Cash Flow Statement Template

Download: .PDF

Download: .PDF

Cash Flow Outlook Statement Template

Download: .PDF

Download: .PDF

Demystifying Projected Cash Flow Statements

For any growing business, cash is the fundamental fuel that keeps operations running. While an income statement measures theoretical profitability by matching revenues with expenses, it does not show when actual money enters or leaves your bank account. A business can appear highly profitable on paper but still fail due to a sudden lack of liquidity. A projected cash flow statement is a vital survival tool because it maps out your future cash position, ensuring you can anticipate shortfalls, plan major purchases, and maintain solvency before critical challenges arise.

Operating Activities: The Core Engine of Cash Flow

Operating activities represent the primary source of cash generation for an ongoing enterprise. When building your projection template, you must carefully forecast the day-to-day cycles of your business to understand how day-to-day transactions impact your liquid capital.

To accurately project this section, you must detail several key components:

- Customer Collections: Do not assume sales translate immediately to cash. Factor in payment terms, accounts receivable delays, and potential bad debts to map out when cash actually lands in your accounts.

- Payments to Suppliers: Balance your inventory needs with vendor credit terms. Projecting these payments helps you maintain healthy relationships with critical suppliers.

- Recurring Operational Expenses: Map out regular outflows such as payroll, rent, utilities, marketing, and software subscriptions that keep the daily business running smoothly.

Investing Activities: Planning for Future Growth

Investing activities capture the cash spent on acquiring or selling long-term assets that will fuel your company's future expansion. Unlike operating expenses, these transactions represent significant, often non-recurring, cash movements that must be carefully timed.

Your projections must account for major capital expenditures (CapEx), such as purchasing manufacturing equipment, vehicles, or upgrading technological infrastructure. Additionally, you should forecast any planned asset purchases or cash inflows generated from the liquidation of long-term investments. Accurately mapping these transactions ensures you do not trigger a cash crisis while trying to fund long-term growth initiatives.

Financing Activities: Managing Debt and Equity

Financing activities reflect how your business funds its operations and capital investments through external sources. This section details the flow of cash between your company, its lenders, and its investors.

To build a comprehensive cash flow forecast, your financing section must track:

- Cash inflows from new bank loans, lines of credit, or venture capital equity investments.

- Cash outflows for scheduled debt servicing, including loan principal repayments.

- Cash outflows dedicated to dividend payments or equity buybacks for company owners and investors.

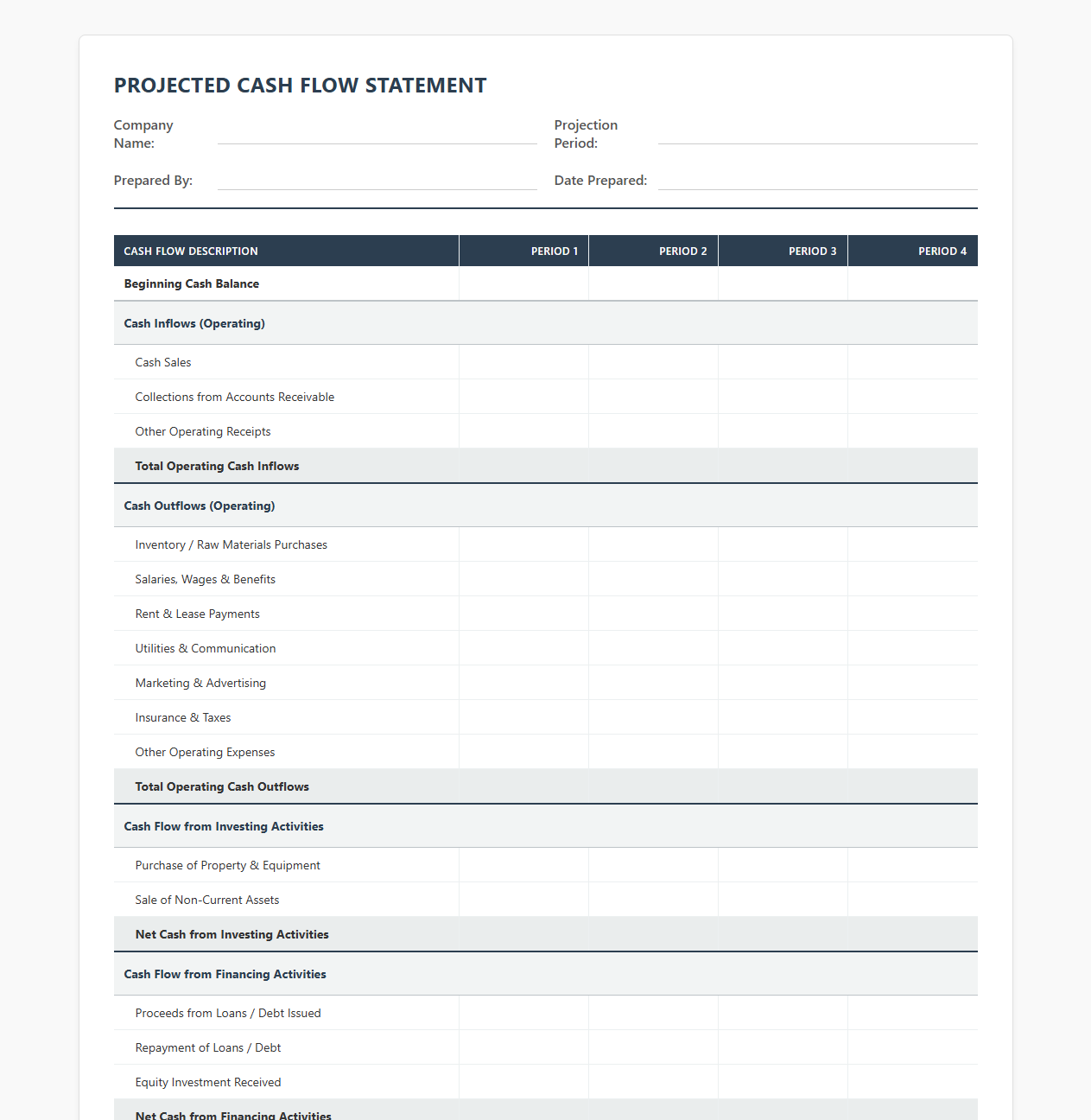

Structuring the Perfect Projected Cash Flow Template

A functional cash flow template must be organized chronologically to allow for easy monthly updates and comparisons. Below is a structural outline for a standard 12-month outlook, demonstrating how to organize your rows and columns.

| Cash Flow Category | Month 1 | Month 2 | Month 3 | ... Month 12 |

|---|---|---|---|---|

| Starting Cash Balance | $50,000 | $55,000 | $48,000 | $120,000 |

| Operating Cash Inflows | $30,000 | $35,000 | $40,000 | $65,000 |

| Operating Cash Outflows | ($20,000) | ($22,000) | ($25,000) | ($30,000) |

| Investing Cash Flow | $0 | ($15,000) | $0 | ($10,000) |

| Financing Cash Flow | ($5,000) | ($5,000) | $50,000 | ($5,000) |

| Net Cash Flow Change | $5,000 | ($7,000) | $65,000 | $20,000 |

| Ending Cash Balance | $55,000 | $48,000 | $113,000 | $140,000 |

Pitfalls to Avoid in Cash Flow Forecasting

Creating a model is only useful if it reflects reality. Many businesses construct overly optimistic forecasts that lead to poor operational decisions and unexpected liquidity crunches.

Overestimating Sales Velocity

Assuming that closed deals translate immediately into cash is a dangerous mistake. Always account for collections lag, as customers often take 30, 60, or even 90 days to settle accounts receivable invoices.

Ignoring Seasonality

Very few businesses experience perfectly flat monthly sales. Failing to adjust for seasonal downturns can lead to severe cash shortages during slow months when fixed operating expenses remain constant.

Neglecting Emergency Cash Buffers

Unforeseen market shifts, sudden supply chain disruptions, or emergency repairs can quickly drain your reserves. Maintaining a dedicated cash reserve within your model ensures you can absorb unexpected shocks without disrupting daily business operations.

Best Practices for Continuous Forecast Optimization

A projected cash flow statement is not a static document to be filed away after creation. To maximize its value, you must treat your forecast as a living tool that evolves alongside your operational reality. Make it a routine to regularly update your models at the close of every month, replacing forecasted assumptions with your actual financial performance data.

Additionally, you must stress-test your forecasts under various negative scenarios, such as a major customer departure or a sudden increase in supplier costs. By continuously reconciling your projected cash flow against actual bank balances, you can identify variance patterns, refine your prediction models, and build a highly resilient financial framework for long-term business success.

Leave a comment