For sole proprietors, tracking equity isn't just a matter of checking bank balances; it is a continuous struggle to untangle personal draws from business reinvestments without the rigid guardrails of a corporate structure. Before implementing automated software, establishing a manual, logically sound accounting framework is essential for maintaining clean, compliant books.

Mastering this structure grants business owners absolute financial clarity, reducing tax-season friction and ensuring investor-ready records. Naturally, these templates require a baseline commitment to accurate daily ledger entry to remain reliable. For example, explicitly separating "Owner's Drawings" from "Net Income Reinvestment" provides an immediate, auditable trail of equity flow that prevents costly balance sheet discrepancies.

Below, we will explore essential statement templates, break down core equity formulas, and outline a step-by-step framework to help you structure your proprietorship capital with absolute precision.

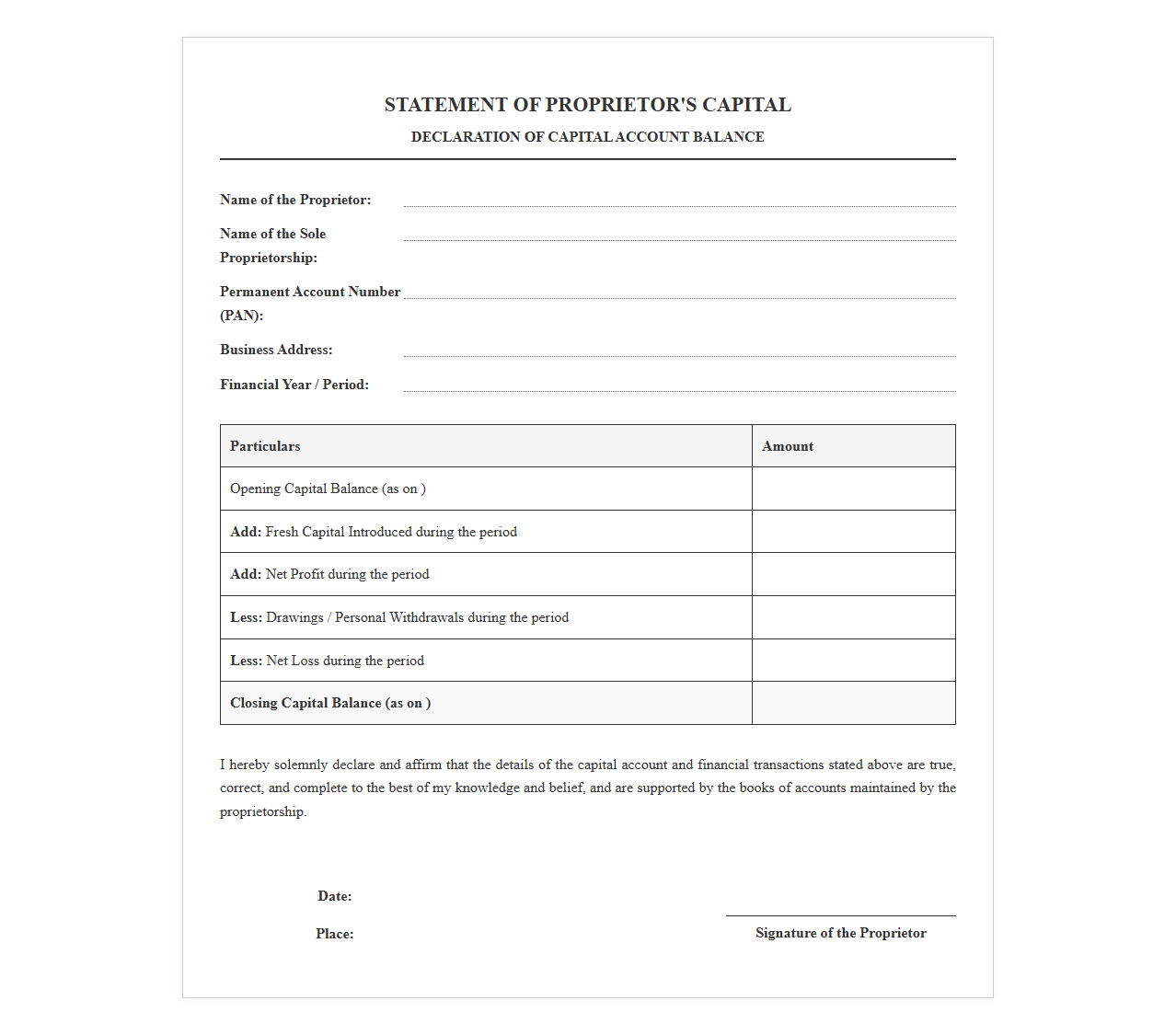

Sole Proprietorship Capital Statement Template

Download: .PDF

Download: .PDF

Proprietor Capital Account Statement Template

Download: .PDF

Download: .PDF

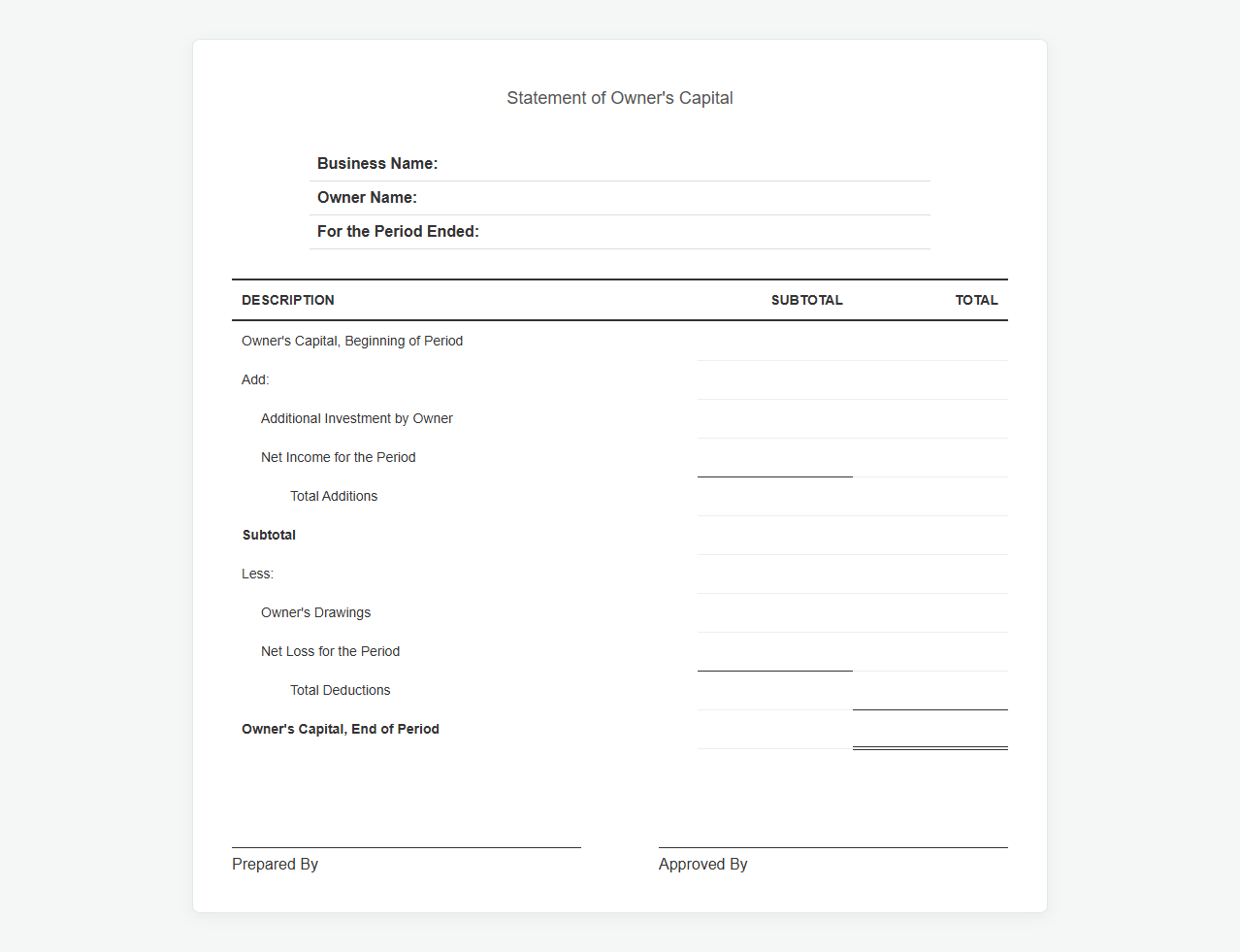

Statement of Owner Equity for Sole Proprietorship

Download: .PDF

Download: .PDF

Sole Proprietor Capital Declaration Template

Download: .PDF

Download: .PDF

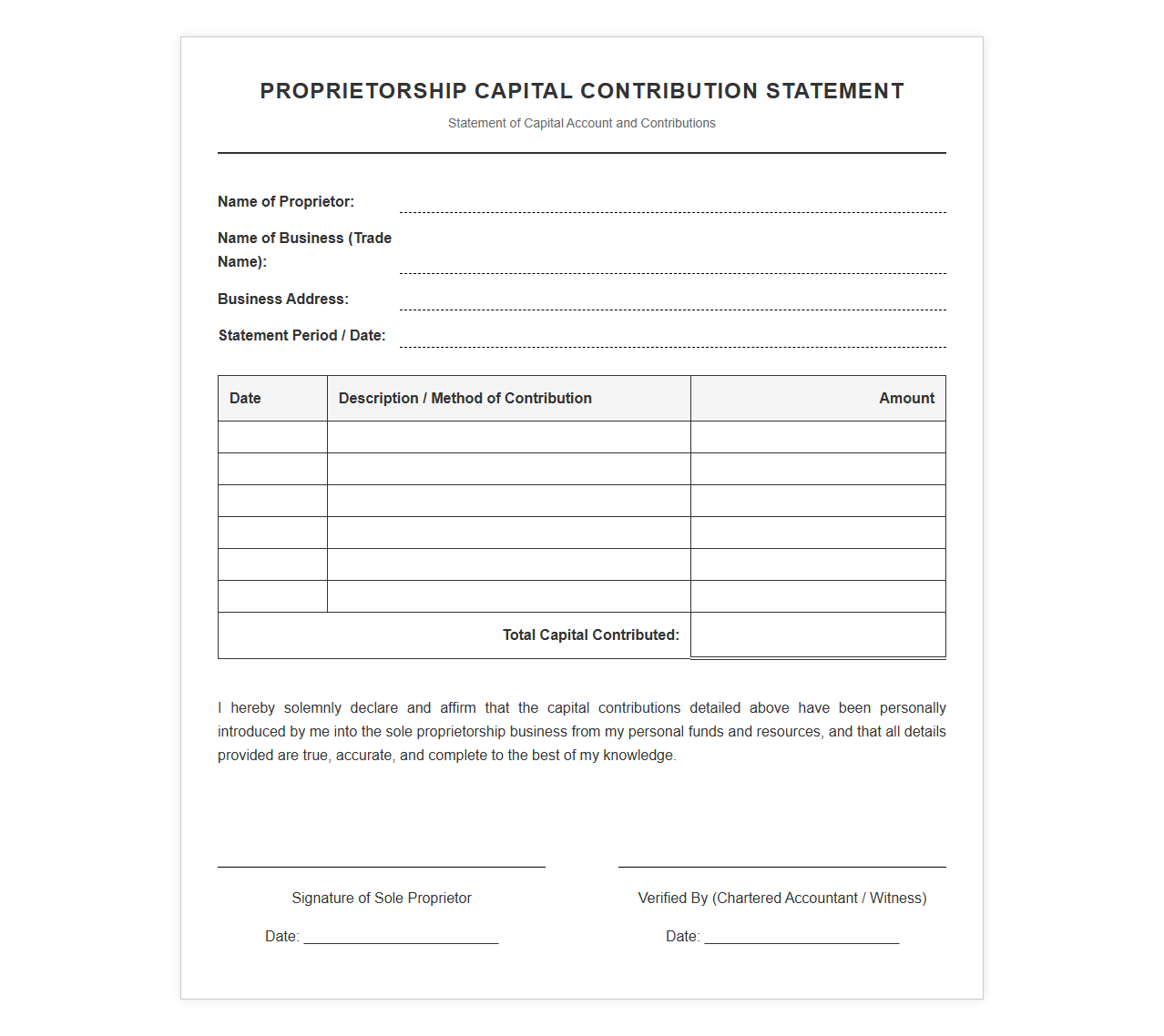

Proprietorship Capital Contribution Statement

Download: .PDF

Download: .PDF

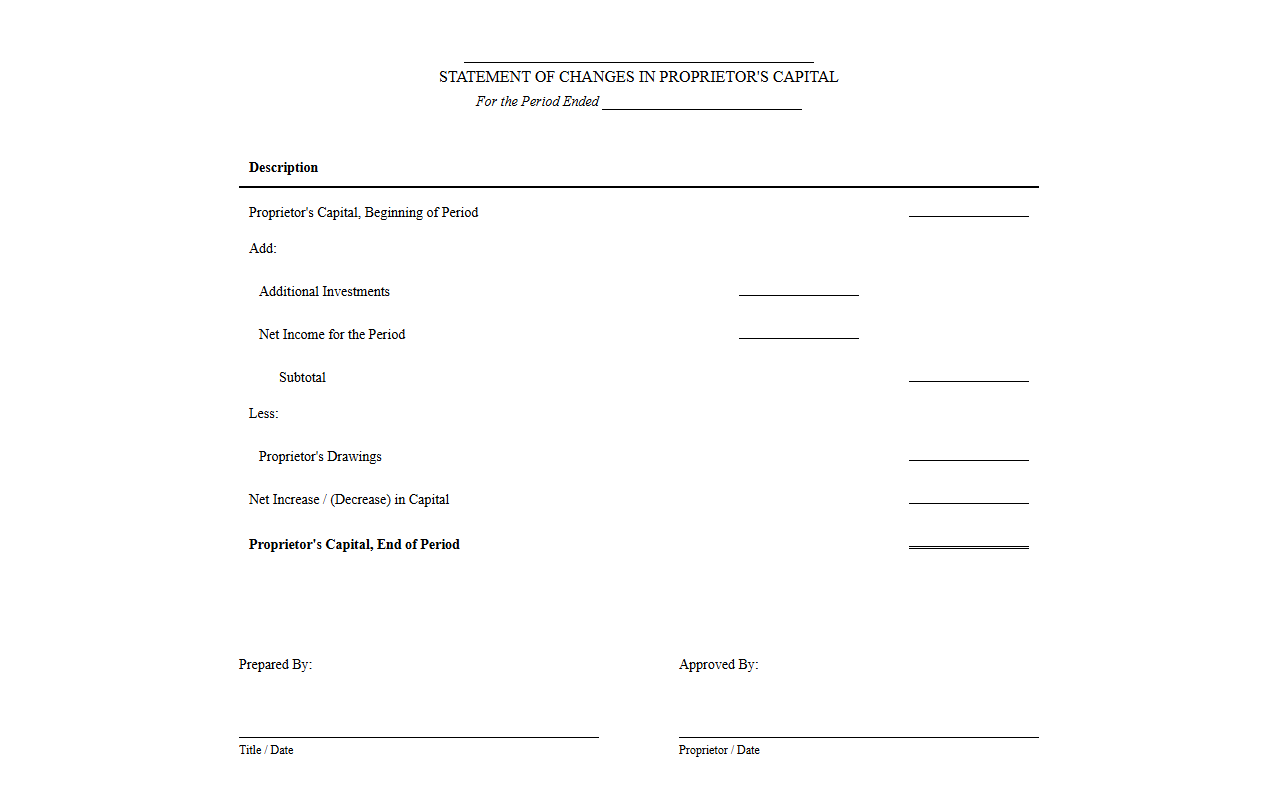

Statement of Changes in Proprietor Capital

Download: .PDF

Download: .PDF

Sole Trader Capital Statement Template

Download: .PDF

Download: .PDF

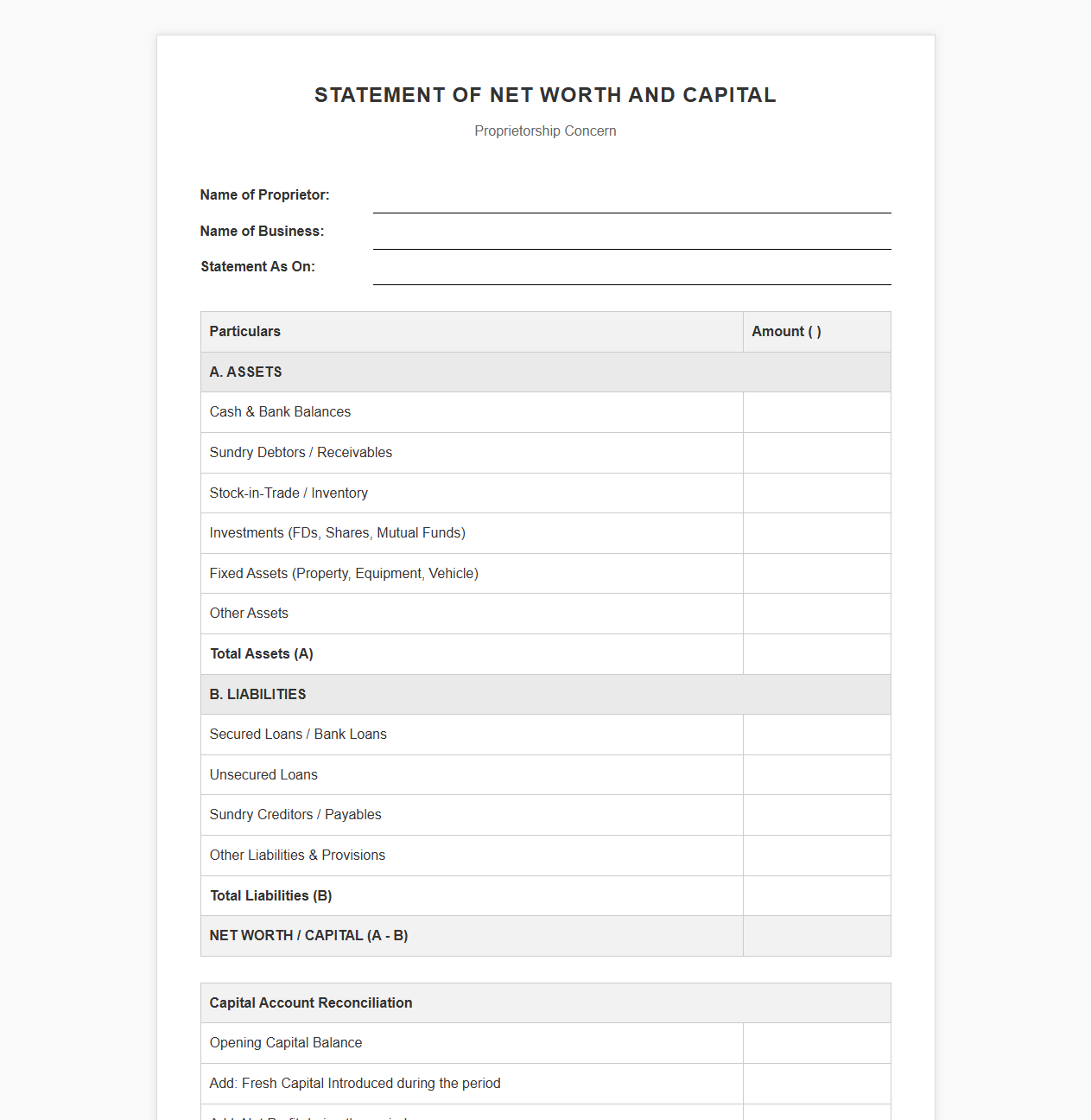

Proprietorship Net Worth and Capital Statement

Download: .PDF

Download: .PDF

Demystifying Sole Proprietorship Equity Structure

For a sole proprietor, tracking owner's equity is not just a bookkeeping chore; it is the financial backbone of your business. Because a sole proprietorship is not a separate legal entity from its owner, it is incredibly easy for personal and business finances to blur. Maintaining a clear line of demarcation between these assets is vital. Owner's equity represents your true financial stake in the business-the remaining value of assets after all liabilities have been deducted. By carefully monitoring this balance, you gain clear insights into profitability, safeguard personal assets, and ensure your business remains financially viable over the long term.

Core Components of the Proprietorship Capital Statement

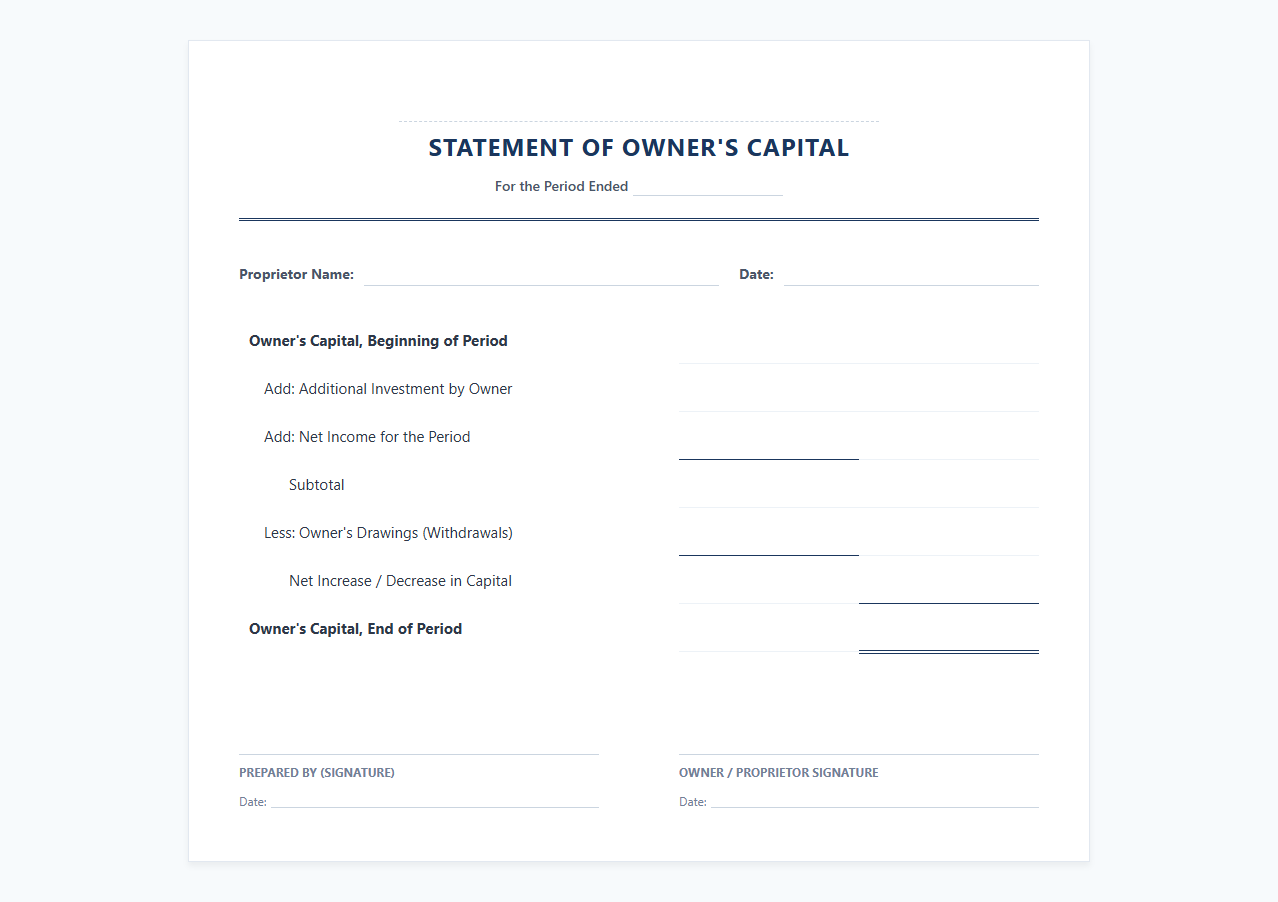

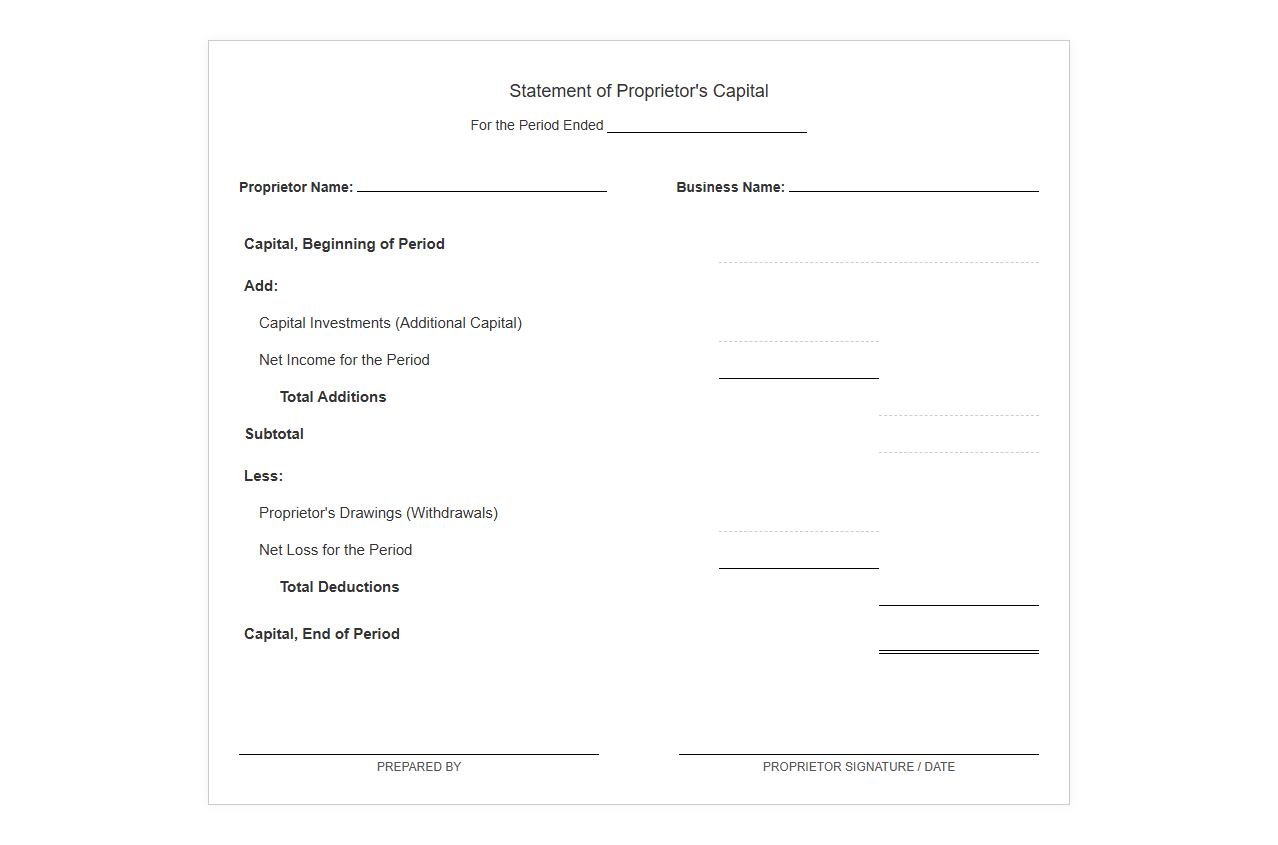

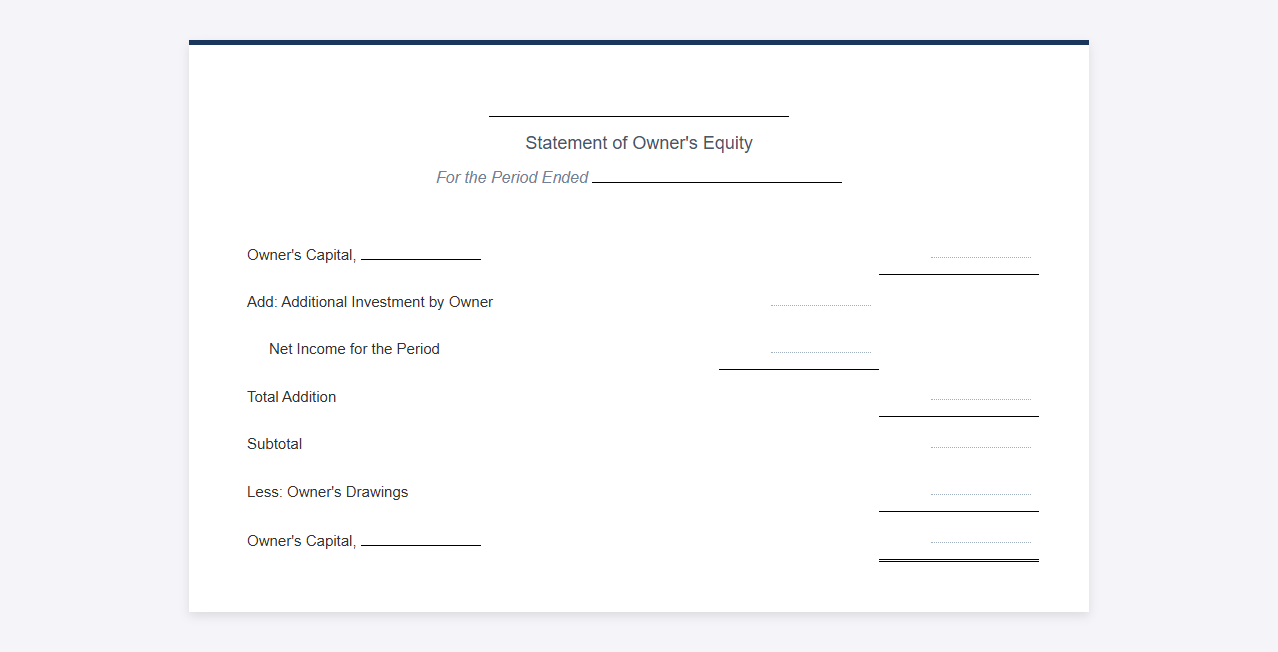

As an accountant, I view the Statement of Owner's Equity as a vital financial bridge. It explains exactly how your business's net worth changed from the beginning of the fiscal period to the end. The ledger balances rely on four fundamental pillars:

- Opening Capital: The valuation of the business owner's investment at the very start of the accounting period.

- Additional Investments: Any personal funds or assets injected into the business during the year to support operations or expansion.

- Net Income: The total revenues earned minus expenses incurred, representing the net profit (or loss) generated.

- Drawings: The withdrawal of business cash or other assets by the owner for personal use, which directly reduces overall equity.

Standard Template Structure for Equity Tracking

To keep your financial tracking seamless, use this clean, structured layout to calculate your ending capital balance for any given fiscal period.

| Line Item | Description | Amount ($) |

|---|---|---|

| Beginning Capital | Balance at start of period | 10,000.00 |

| Add: Additional Investments | Personal cash or assets injected | 2,500.00 |

| Add: Net Income (or Loss) | Net profit from Income Statement | 8,200.00 |

| Less: Owner Drawings | Cash or assets withdrawn for personal use | (3,000.00) |

| Ending Capital Balance | Final equity balance for the period | 17,700.00 |

Documenting Initial and Ongoing Capital Contributions

Accurately recording how and when you inject capital into your sole proprietorship prevents valuation errors and keeps your books audit-ready. Follow these steps to log both cash and non-cash contributions:

- Identify the Asset Type: Determine whether the contribution is cash or a non-cash physical asset, such as a vehicle, computer, or office equipment.

- Determine Fair Market Value: For non-cash contributions, establish the current fair market value of the asset at the exact time of contribution rather than its original purchase price.

- Journalize the Entry: Debit the appropriate asset account (e.g., Cash or Equipment) and credit the Owner's Capital account to reflect the increase in business equity.

- Archive Supporting Documentation: Keep bank transfer receipts, invoices, or appraisal documents to substantiate the transaction.

Managing and Recording Owner Drawings

Owner's drawings represent the withdrawal of business assets for personal use. It is crucial to understand that drawings are not business expenses; they do not impact your company's net income and are not tax-deductible.

Crucial Rule: Because drawings are a distribution of equity, they must bypass the income statement entirely and be debited directly to a temporary equity account called "Owner's Drawings" or "Owner's Withdrawals."

To keep your records clean, avoid paying for personal living expenses directly from the business account. Instead, transfer a round sum from your business account to your personal account, logging that transaction as a drawing. This practice preserves the integrity of your financial reporting.

Linking Net Income from the Income Statement

At the end of an accounting cycle, the net profit or loss calculated on your income statement must flow directly into your capital statement. This is achieved through the closing process. By running a closing entry, the system transfers the balance of the temporary revenue and expense accounts into a summary account, and then directly to the permanent capital ledger using the Capital account.

If your business generated a profit, you will credit the capital account to increase your total equity. Conversely, if the business suffered a net loss, you will debit the capital account, reflecting a reduction in your overall business net worth. This architectural linkage ensures your balance sheet remains perfectly in balance.

Best Practices for Maintaining Equity Ledger Accuracy

Regular reviews prevent minor bookkeeping oversights from turning into costly errors at tax time. Incorporate these habits into your regular routine:

- Reconcile Accounts Monthly: Match your business bank statements with your ledger entries to ensure every dollar is accounted for.

- Separate Personal Finances: Maintain entirely separate bank accounts and credit cards for your business operations.

- Review Drawings Regularly: Check the drawings account monthly to confirm no business expenses were accidentally misclassified.

- Audit Capital Injections: Ensure every personal fund transfer into the business has a corresponding documented source and purpose.

Read More

Leave a comment