For corporate finance teams, the annual reconciliation of retained equity often becomes a high-stakes bottleneck, fraught with manual data-entry errors and complex calculations. As accounting standards grow more stringent, maintaining a precise ledger of reinvested earnings is no longer just a best practice-it is a critical regulatory necessity. Streamlining this process with standardized reporting templates grants finance departments both organizational peace of mind and significant time savings during audit season.

It is important to note, however, that while professional templates offer a highly structured framework, they are not a substitute for certified CPA oversight and must be adapted to your firm's specific accounting policies. For example, capturing nuanced transactions such as prior-period adjustments or stock-based compensation roll-forwards requires careful calibration to preserve balance sheet integrity.

In this guide, we will explore the core components of professional equity statements, provide customizable templates, and outline best practices for seamless integration into your financial workflow.

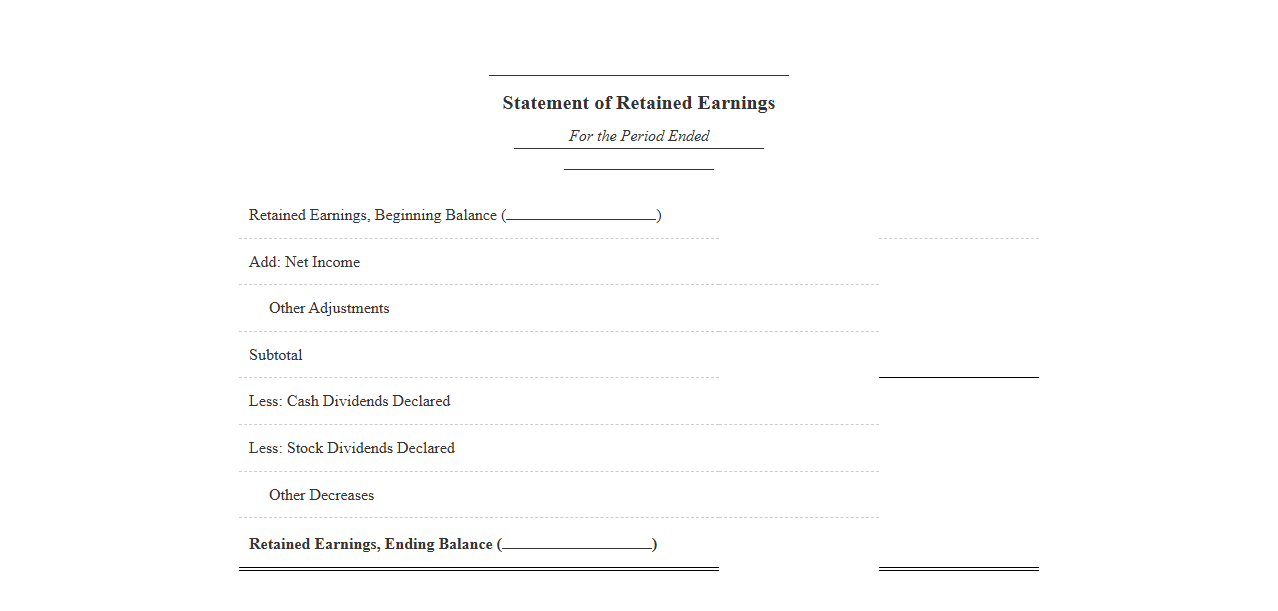

Statement of Retained Earnings Template

Download: .PDF

Download: .PDF

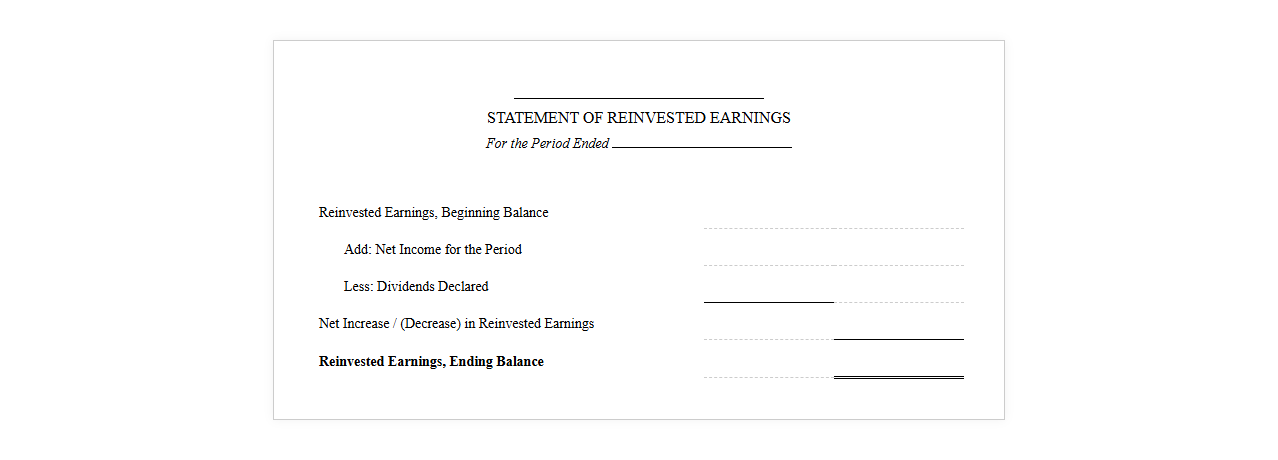

Reinvested Earnings Statement Format

Download: .PDF

Download: .PDF

Retained Earnings Report Template

Download: .PDF

Download: .PDF

Statement of Reinvested Capital Template

Download: .PDF

Download: .PDF

Accumulated Earnings Statement Template

Download: .PDF

Download: .PDF

Schedule of Retained Earnings Template

Download: .PDF

Download: .PDF

Reinvested Profits Statement Template

Download: .PDF

Download: .PDF

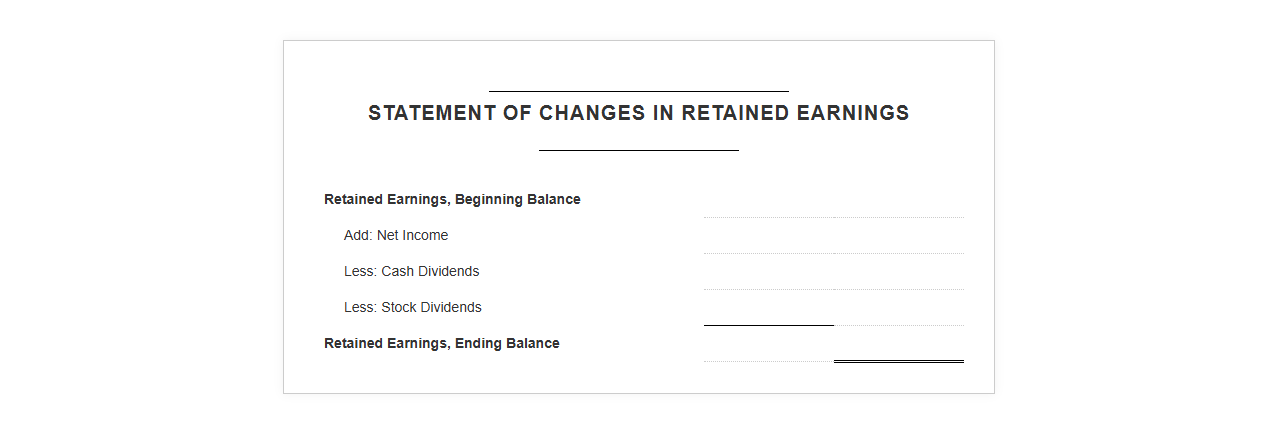

Statement of Changes in Retained Earnings Template

Download: .PDF

Download: .PDF

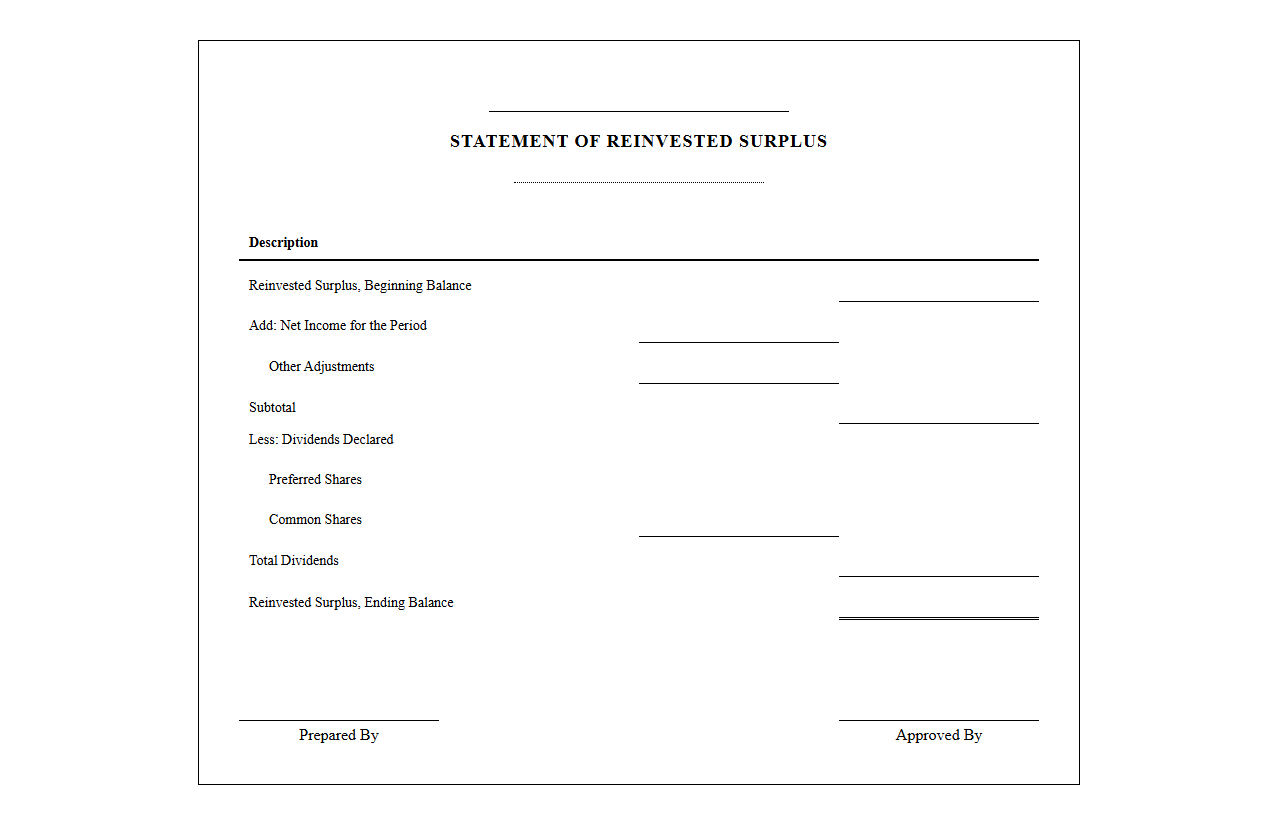

Reinvested Surplus Statement Template

Download: .PDF

Download: .PDF

Demystifying Retained Equity and Reinvested Earnings

In corporate finance, retained equity represents the cumulative portion of a business's net income that is kept within the company rather than distributed to shareholders as dividends. Often referred to as reinvested earnings, this capital serves as a vital engine for organic growth, debt reduction, and strategic research and development. While these metrics are fundamental to assessing a organization's long-term financial health, they are frequently buried under complex accounting jargon. Establishing simplified, transparent reporting methods is crucial for stakeholders, enabling investors, board members, and internal teams to quickly grasp how efficiently a company is allocating its capital for future expansion.

Common Obstacles in Traditional Equity Reporting

Traditional equity reporting often alienates the very stakeholders it is meant to inform. By relying on overly dense financial disclosures, companies risk obscuring critical performance indicators. Several persistent challenges include:

- Excessive Technical Jargon: Using overly complex accounting terminology where simpler phrasing would convey the message more effectively.

- Fragmented Data Layouts: Spreading equity adjustments across multiple sections of a financial report, making it difficult to trace the flow of funds.

- Lack of Visual Hierarchy: Presenting dense walls of numbers without clear distinctions between starting balances, mid-year adjustments, and final balances.

- Manual Calculation Errors: Relying on static spreadsheets that increase the risk of rounding discrepancies and input mistakes.

Essential Elements of a Modern Retained Earnings Statement

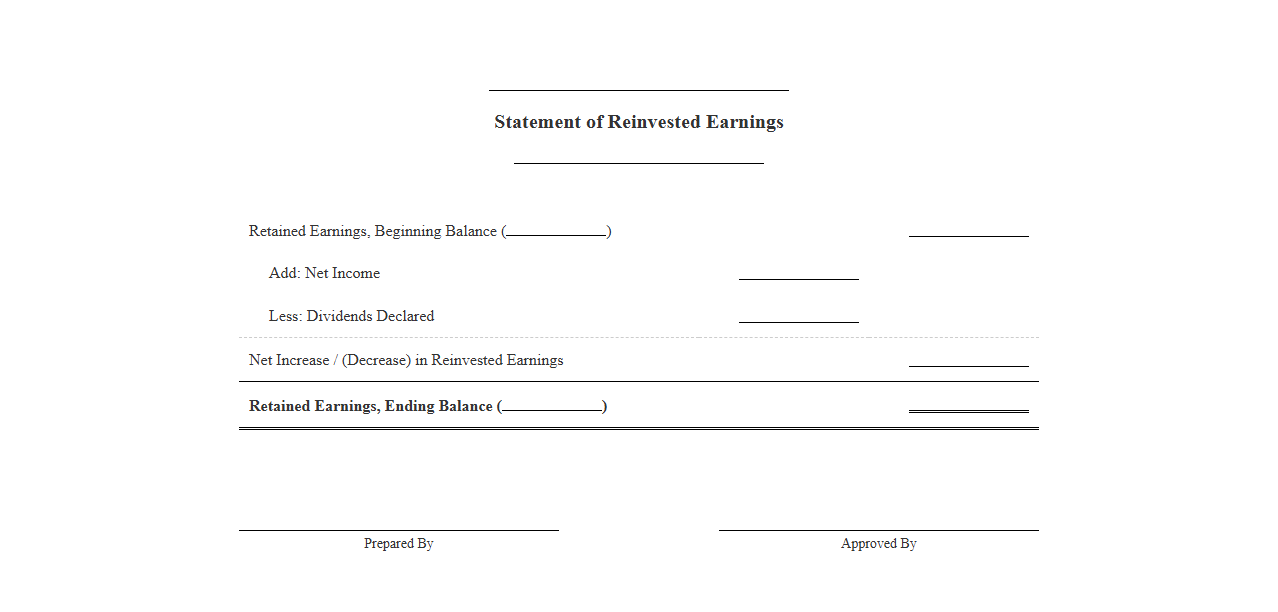

To deliver maximum clarity, a modern retained earnings statement should strip away unnecessary noise and focus on a logical, chronological flow of core financial metrics. Calculating the final balance involves a straightforward, sequential progression:

- Beginning Balance: Establish the starting point by carrying over the retained earnings from the end of the previous fiscal period.

- Add Net Income: Incorporate the net profit generated during the current reporting period, which represents the total pool of earnings available for allocation.

- Subtract Dividends Paid: Deduct any cash or stock distributions promised to shareholders, as this capital leaves the corporate equity pool.

- Ending Retained Earnings: Calculate the final sum, which is carried forward to the balance sheet as the new baseline for the next period.

Standardized Professional Statement Template

The table below provides a clean, highly structured template designed for reporting reinvested earnings clearly over a standard fiscal year.

| Line Item Description | Fiscal Year 2024 (USD) | Fiscal Year 2023 (USD) |

|---|---|---|

| Retained Earnings (Beginning Balance) | $1,250,000 | $950,000 |

| Add: Net Income for the Period | $450,000 | $400,000 |

| Less: Cash Dividends Declared | ($120,000) | ($100,000) |

| Retained Earnings (Ending Balance) | $1,580,000 | $1,250,000 |

Best Practices for Presenting Reinvested Earnings

When presenting reinvestment strategies to non-financial stakeholders, focus on the narrative behind the numbers. Explain exactly how retained capital is being deployed-whether it is funding a new product line, expanding into geographical markets, or paying down high-interest liabilities. Using plain language helps bridge the gap between complex accounting rules and real-world business objectives.

"True financial transparency is not just about making data public; it is about making that data instantly comprehensible to those who rely on it to make decisions."

Streamlining the Reporting Process with Technology

Relying on legacy spreadsheets for equity tracking often introduces human error and slows down closing cycles. Modern cloud-based ERP platforms and specialized accounting software automate the entire flow of financial data, pulling information directly from the general ledger to construct equity statements dynamically. This automated approach ensures real-time accuracy and frees up finance professionals to focus on strategic analysis rather than manual data entry. To learn more about modern tools, you can review our guide on integrating financial reporting systems.

Driving Transparency Through Simplified Reporting

Adopting clean, straightforward templates for retained equity statements benefits the entire corporate ecosystem. Clear reports reduce review times, build deeper trust with external investors, and empower internal executives to make faster, data-backed strategic choices. Finance teams must prioritize reporting clarity as a core professional standard, transforming dense financial disclosures into valuable communication assets.

Leave a comment