Accurately reconciling retained profits remains a persistent challenge for corporate accountants, often leading to compliance risks and misaligned balance sheets. Before selecting a reporting format, however, organizations must first establish how these figures interface with broader equity transactions and tax obligations. Utilizing standardized templates grants financial teams the precision needed to streamline calculations and safeguard reporting integrity. Yet, it is critical to note that these tools must be customized to meet specific jurisdictional standards; a generic template cannot substitute for professional oversight. For example, incorporating dedicated line items for prior-period adjustments and stock dividends provides concrete proof of rigorous, audit-ready documentation. Below, we break down the essential structural components of the statement of undistributed earnings, review professional templates, and outline best practices for flawless financial disclosure.

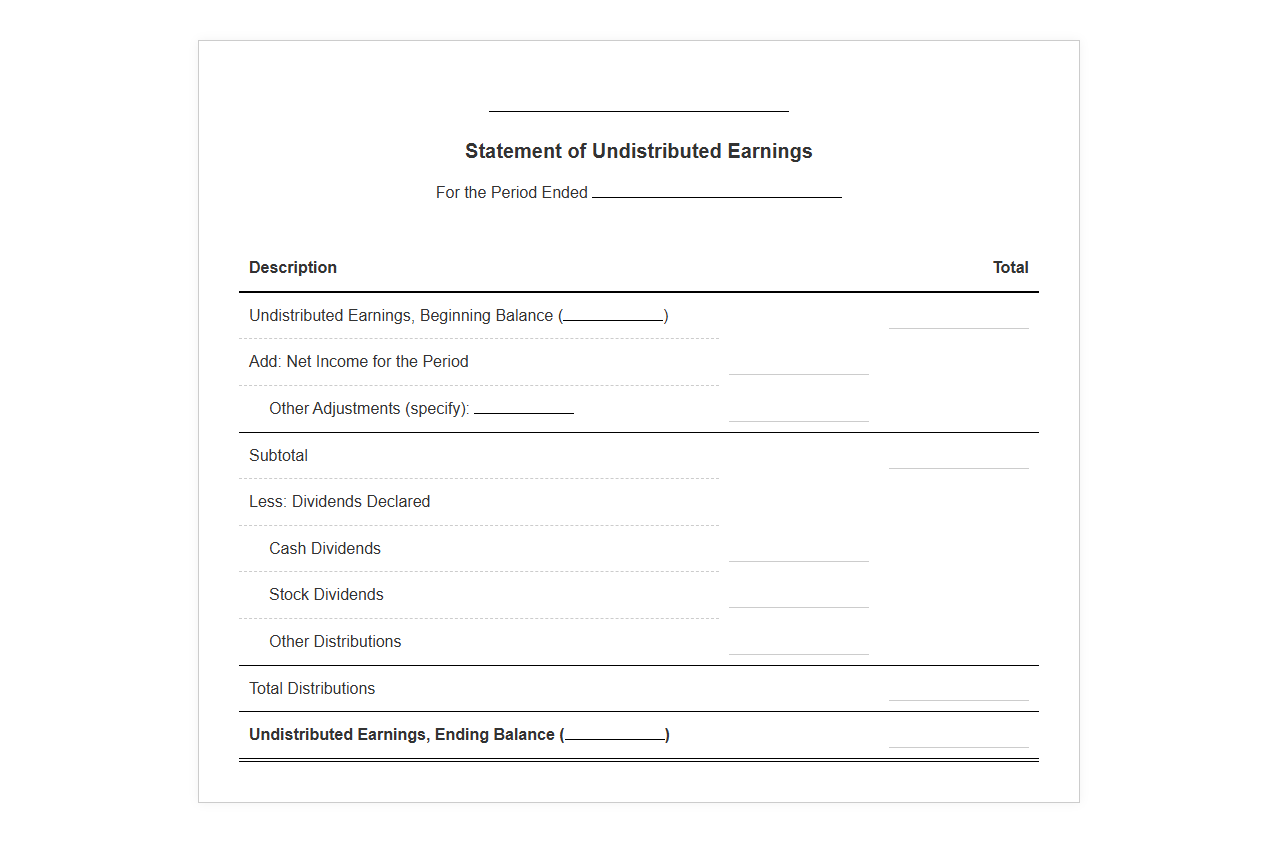

Retained Earnings Statement Template

Download: .PDF

Download: .PDF

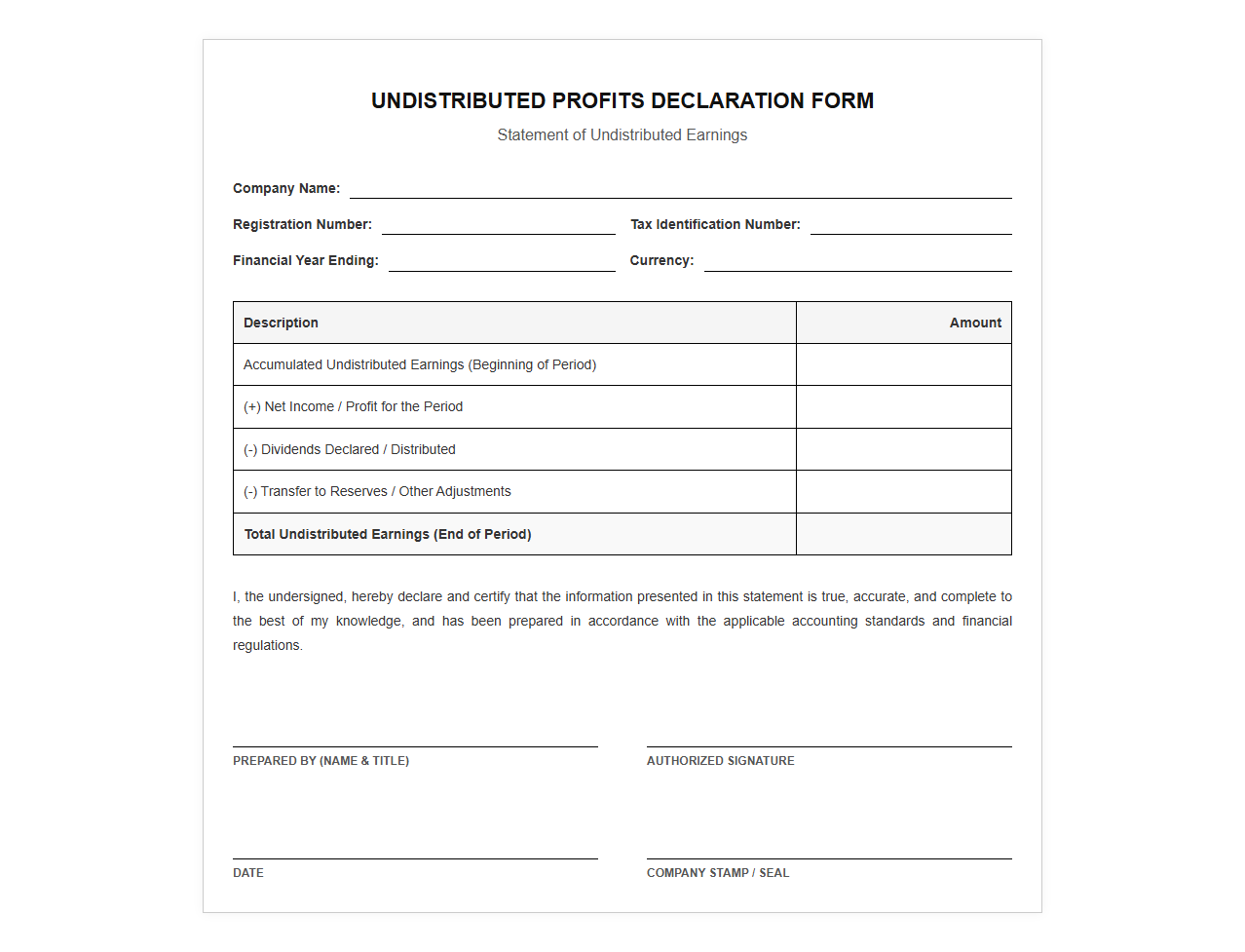

Undistributed Profits Declaration Form

Download: .PDF

Download: .PDF

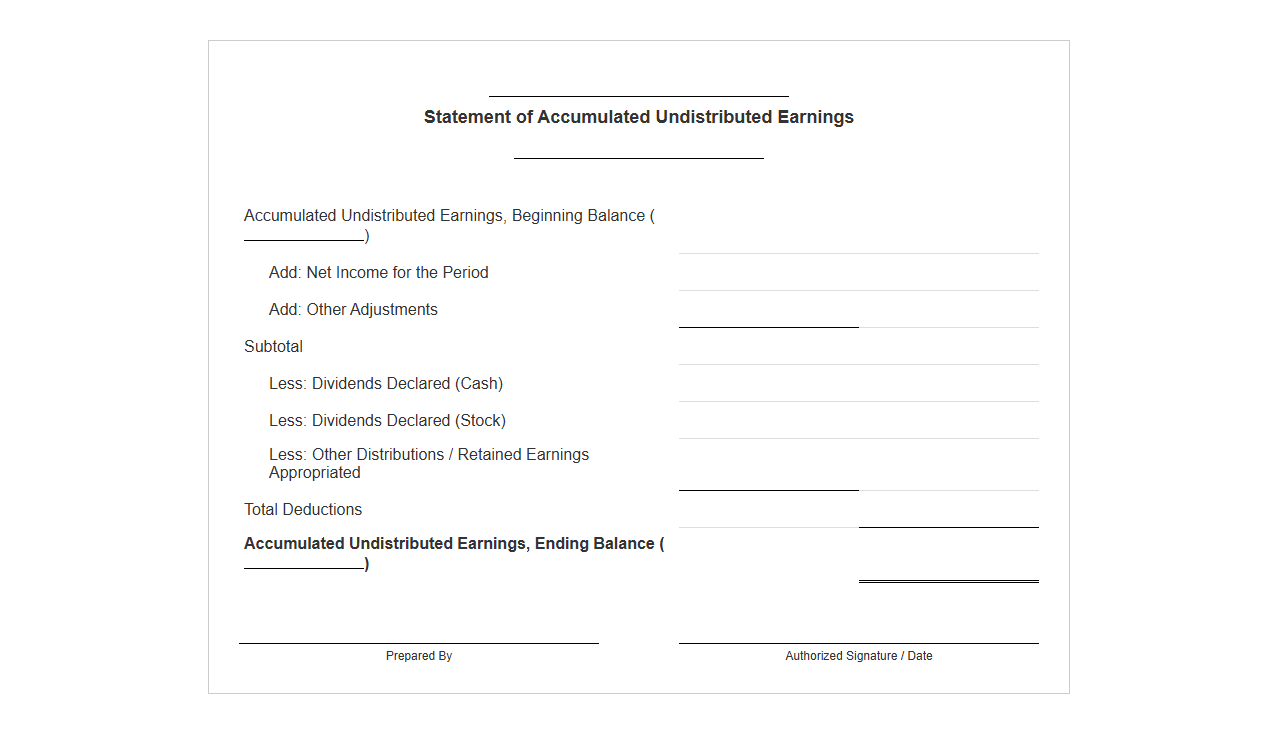

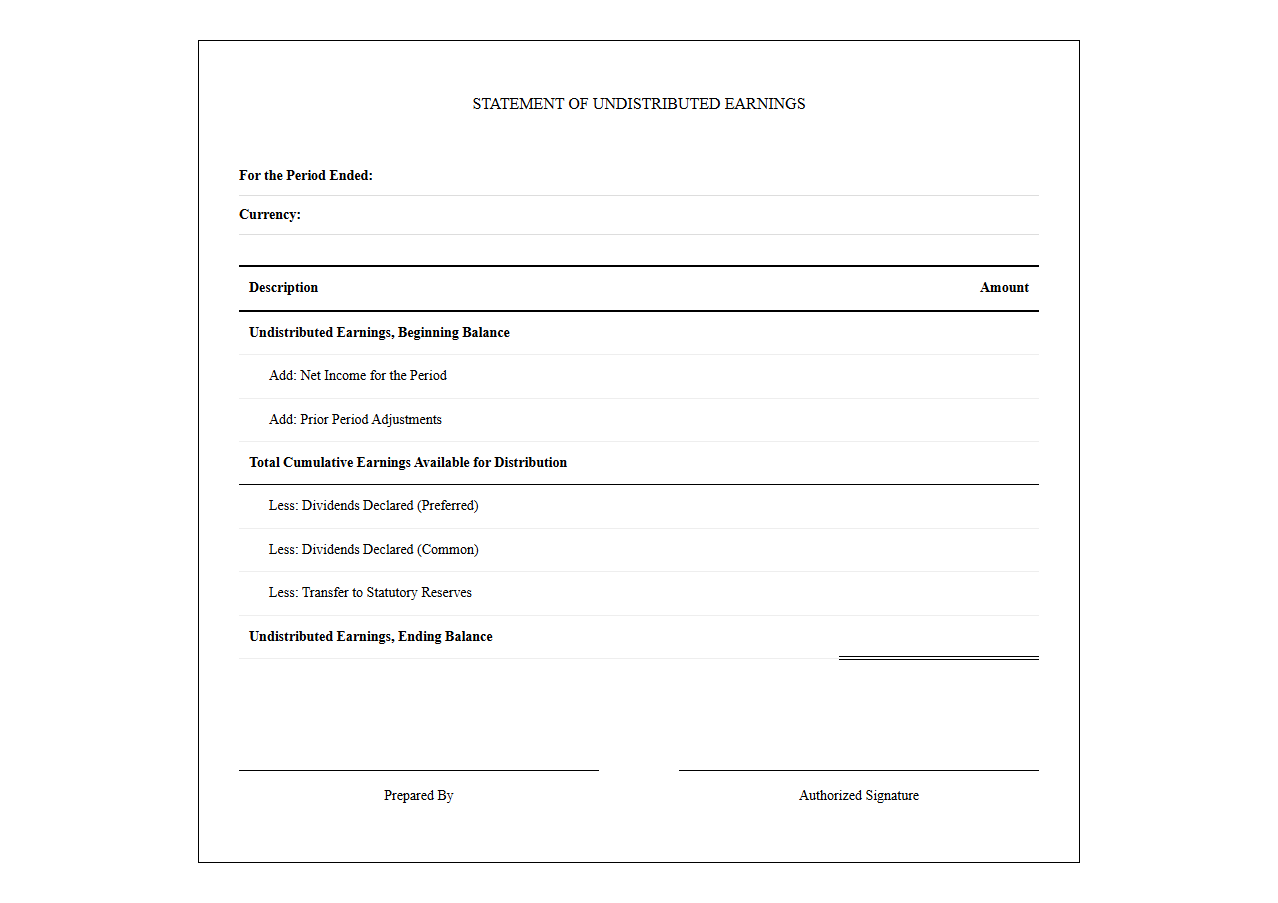

Statement of Accumulated Undistributed Earnings

Download: .PDF

Download: .PDF

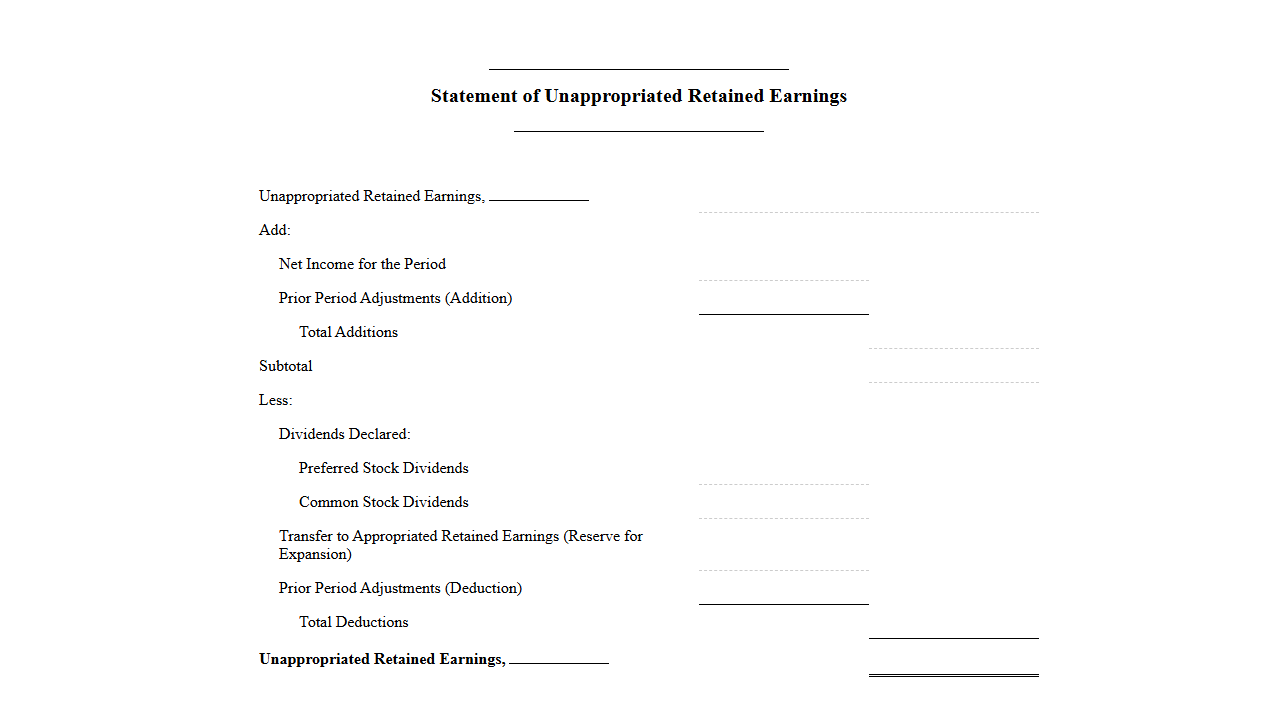

Unappropriated Retained Earnings Statement

Download: .PDF

Download: .PDF

Undistributed Earnings Report Template

Download: .PDF

Download: .PDF

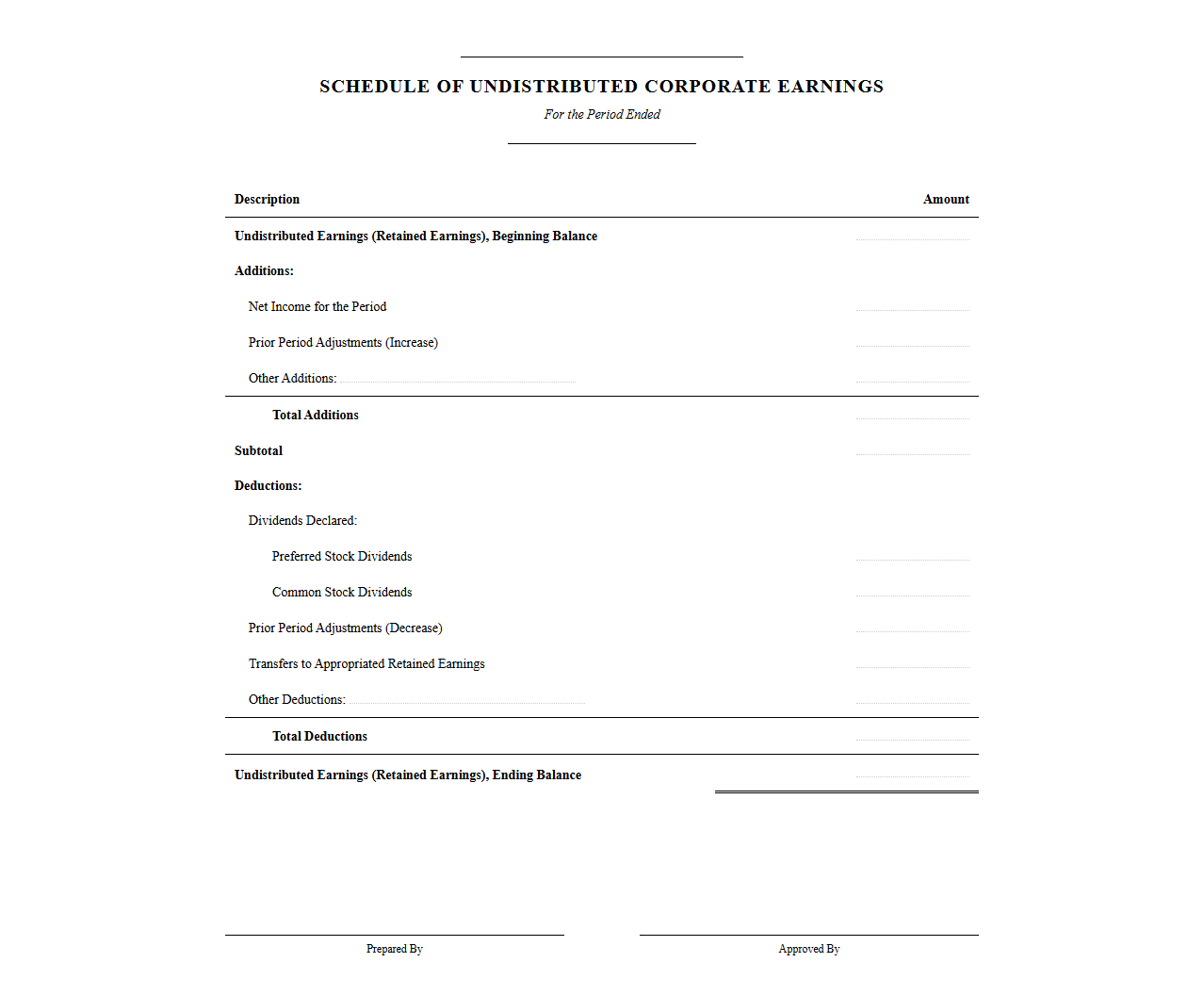

Schedule of Undistributed Corporate Earnings

Download: .PDF

Download: .PDF

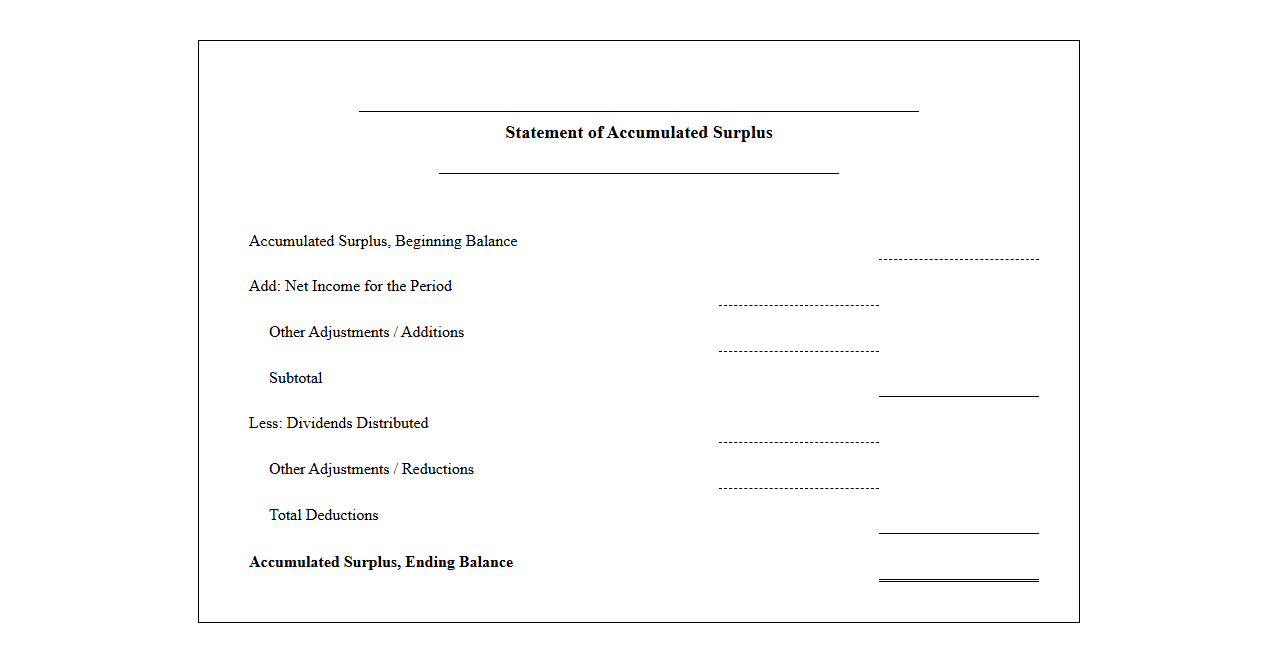

Accumulated Surplus Statement Template

Download: .PDF

Download: .PDF

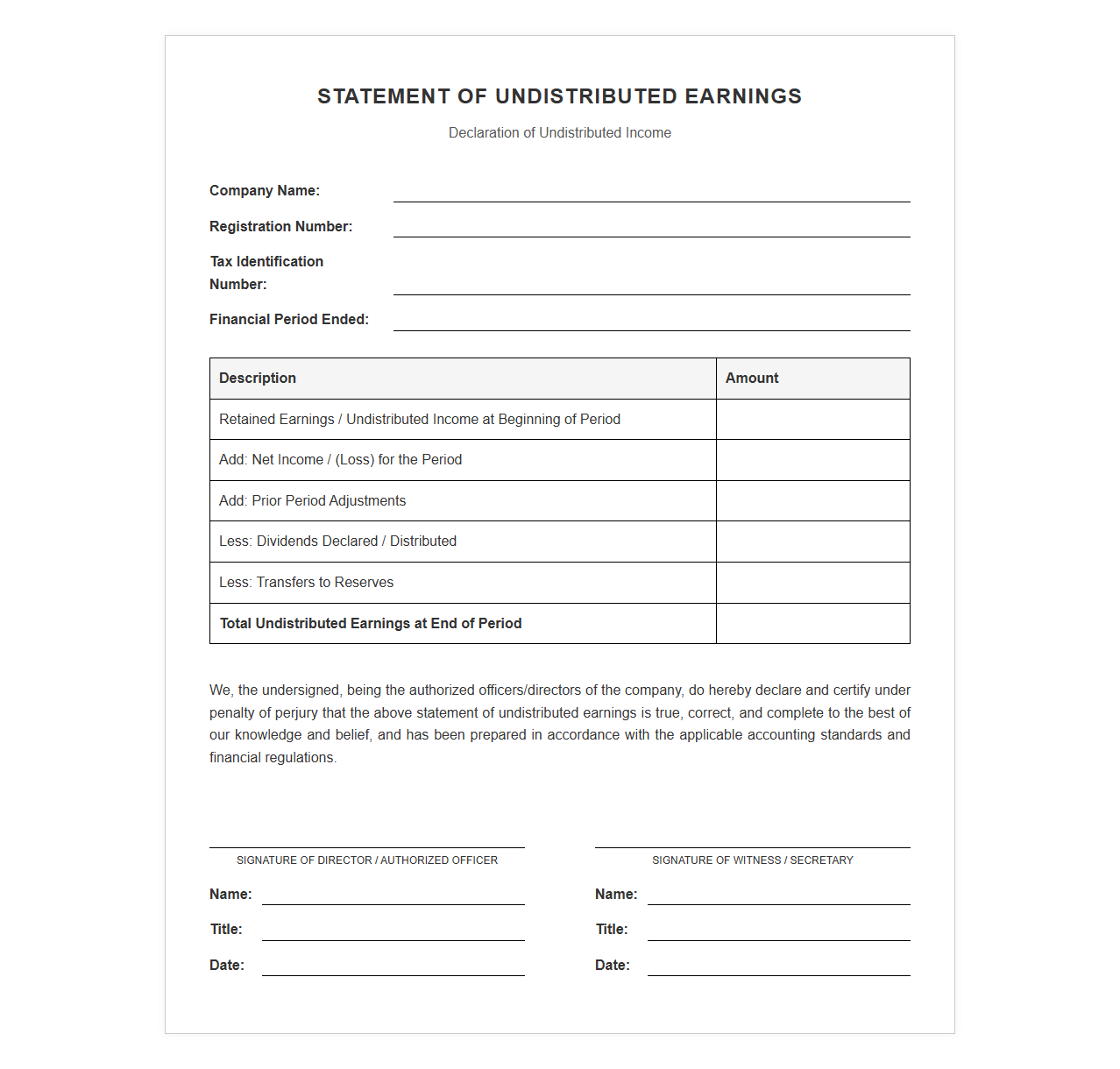

Declaration of Undistributed Income Template

Download: .PDF

Download: .PDF

Introduction to Undistributed Earnings in Financial Reporting

In corporate finance, tracking where profits flow is essential for assessing a company's financial health. Undistributed earnings represent the portion of a corporation's net income that is retained within the business rather than paid out to shareholders as dividends. Understanding these accumulated profits is highly significant, as they serve as a primary source of internal funding for reinvestment, debt reduction, and strategic expansion. By presenting these figures in a structured statement, businesses offer stakeholders an unfiltered view of capital allocation strategies and long-term viability.

Core Components of the Statement of Undistributed Earnings

A standard statement of undistributed earnings relies on key financial components to paint a complete picture of equity movements over a specific reporting period. These elements include:

- Beginning Balance: The accumulated undistributed earnings brought forward from the end of the previous fiscal period.

- Net Income Additions: The net profit earned during the current period, which increases the total pool of retainable earnings.

- Dividend Deductions: Cash or stock dividends distributed to shareholders, which reduce the remaining balance of retained wealth.

- Ending Balance: The finalized total of undistributed earnings at the close of the period, carried forward to the next cycle.

Step-by-Step Mathematical Formulation

Calculating the final ending balance of undistributed earnings is a straightforward mathematical process. Follow these systematic steps to compute the correct figures:

- Identify the starting point of the period using the

Beginning Balance. - Add the current period's total profitable output, represented as

Net Income. - Subtract any declared cash or stock distribution, known as

Dividends Declared. - Calculate the final result to determine the

Ending Balance of Undistributed Earnings.

The core accounting formula is represented as: Ending Undistributed Earnings = Beginning Undistributed Earnings + Net Income - Dividends Declared.

Standardized Template and Layout Representation

The following table presents a standardized layout for presenting the Statement of Undistributed Earnings for a typical fiscal year, assisting accountants in maintaining uniform reporting standards.

| Line Item Description | Amount (USD) |

|---|---|

| Beginning Balance (As of January 1) | $500,000 |

| Add: Net Income for the Year | $150,000 |

| Subtotal | $650,000 |

| Less: Dividends Declared | ($50,000) |

| Ending Balance (As of December 31) | $600,000 |

Distinguishing Undistributed Earnings from Retained Earnings

While the terms "undistributed earnings" and "retained earnings" are frequently used interchangeably in casual financial conversation, they possess distinct technical and legal profiles.

Accounting Definitions

Retained earnings serve as the broad, cumulative accounting category on the balance sheet representing all profits kept since the inception of the company. In contrast, undistributed earnings often refer specifically to profits that are legally or contractually unrestricted and available for distribution, or are designated for a specific current period before formal capitalization actions occur.

Legal and Contractual Limits

In certain jurisdictions, some portion of retained earnings may be legally restricted from distribution due to debt covenants or local capital preservation laws. Thus, the actual pool of undistributed earnings representing freely payable dividends might be smaller than the total retained earnings balance recorded in the equity section.

Regulatory Compliance and GAAP/IFRS Standards

Reporting undistributed earnings requires strict adherence to international and domestic accounting frameworks to maintain transparency and comparability across markets.

"The presentation of changes in equity, including undistributed balances, must clearly delineate transactions with owners in their capacity as owners from other comprehensive income changes." International Financial Reporting Standards (IFRS) - IAS 1

Under US Generally Accepted Accounting Principles (GAAP), companies must fully disclose any restrictions placed on undistributed balances, such as requirements stemming from loan agreements or preferred stock provisions, to ensure investors understand the true liquidity available for future dividend payouts.

Best Practices for Error-Free Financial Reconciliation

Maintaining precision in your financial reconciliation process prevents compliance issues and ensures reporting accuracy. Implementing robust controls protects against systematic reporting errors.

- Regular Trial Balance Matching: Always reconcile the net income figures used in the statement directly to the finalized income statement before posting equity updates.

- Track Prior-Period Adjustments: Ensure that any restatements due to error corrections from previous years are applied directly to the beginning balance rather than current-year activity.

- Separate Dividend Tracking: Maintain distinct ledger accounts for stock dividends, cash dividends, and liquidating dividends to prevent incorrect deductions.

- Implement Dual-Signoff Controls: Require secondary reviews of all ledger entries affecting the equity accounts to eliminate manual entry mistakes.

Leave a comment