Managing disjointed receipts for annual bar dues, medical certifications, and local board fees often leaves finance departments and busy professionals buried in administrative chaos. This recurring friction points to a deeper operational challenge that goes beyond mere paperwork.

Before adopting new software, organizations must first establish a unified policy framework to categorize these diverse professional costs. Standardizing this process grants leadership unprecedented visibility into overhead expenses, ultimately unlocking significant tax advantages and enabling more accurate annual budget forecasting.

However, a successful standardization framework stipulates that eligible expenses must directly align with active job requirements and regional regulatory mandates. For instance, while a structural engineer's state licensing fee is a clear reimbursable necessity, general civic club memberships require stricter scrutiny to prevent budget leakage.

Below, we outline the step-by-step methodology for establishing clear compliance parameters, configuring your ledger accounts, and streamlining the approval workflow for all professional dues.

Professional Membership and Licensing Fee Tracker

![]() Download: .PDF

Download: .PDF

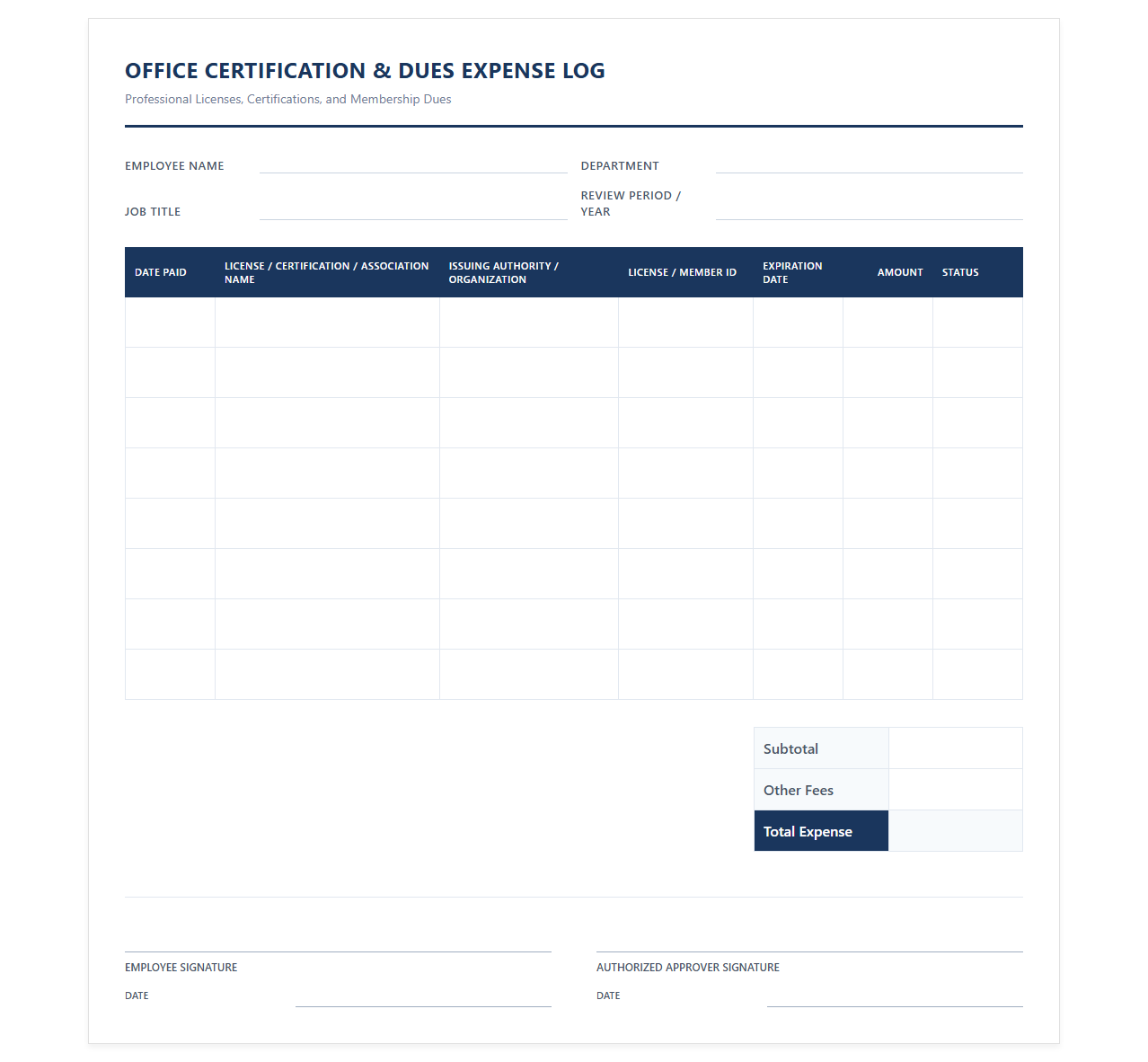

Office Certification and Dues Expense Log

Download: .PDF

Download: .PDF

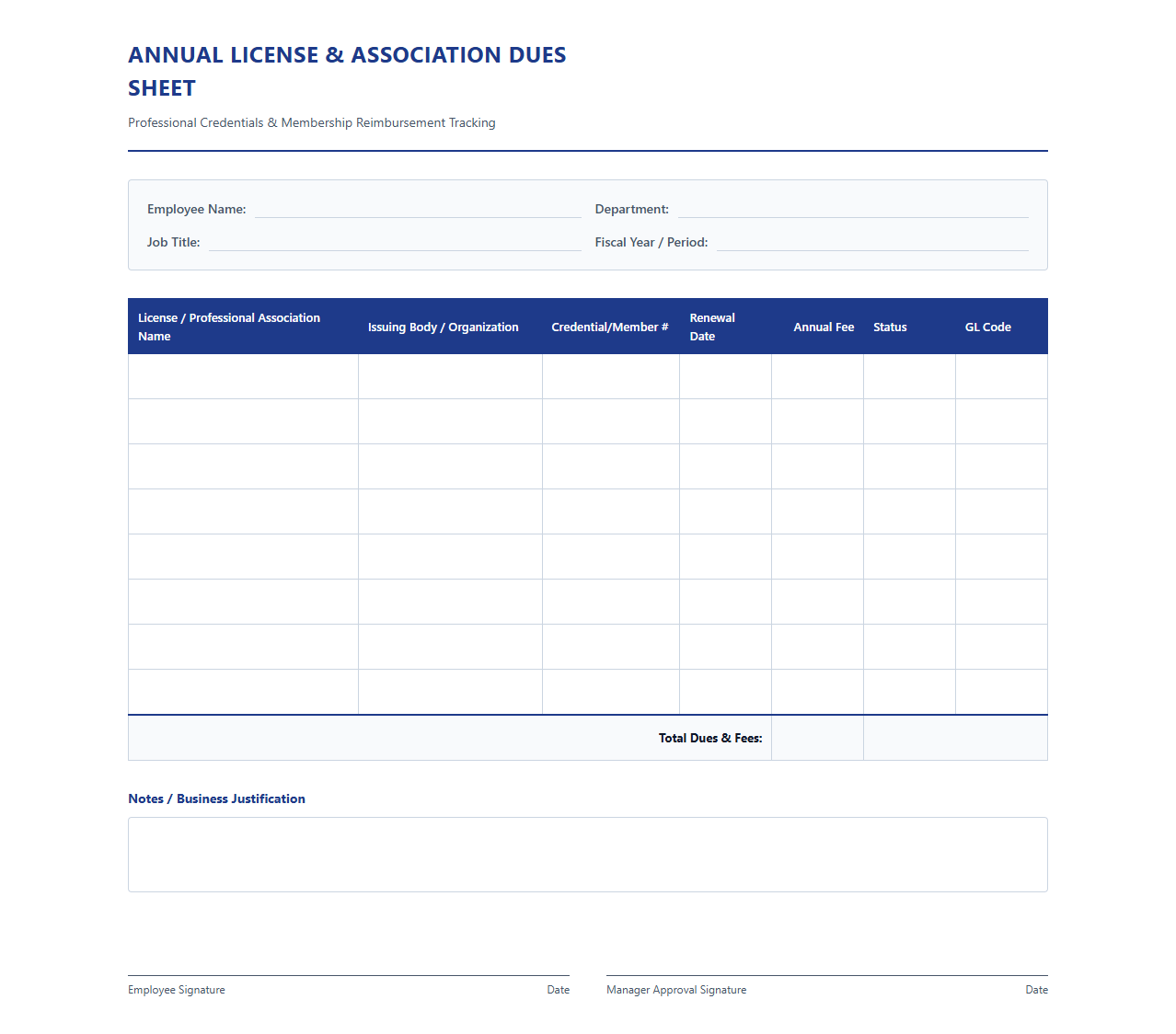

Annual License and Association Dues Sheet

Download: .PDF

Download: .PDF

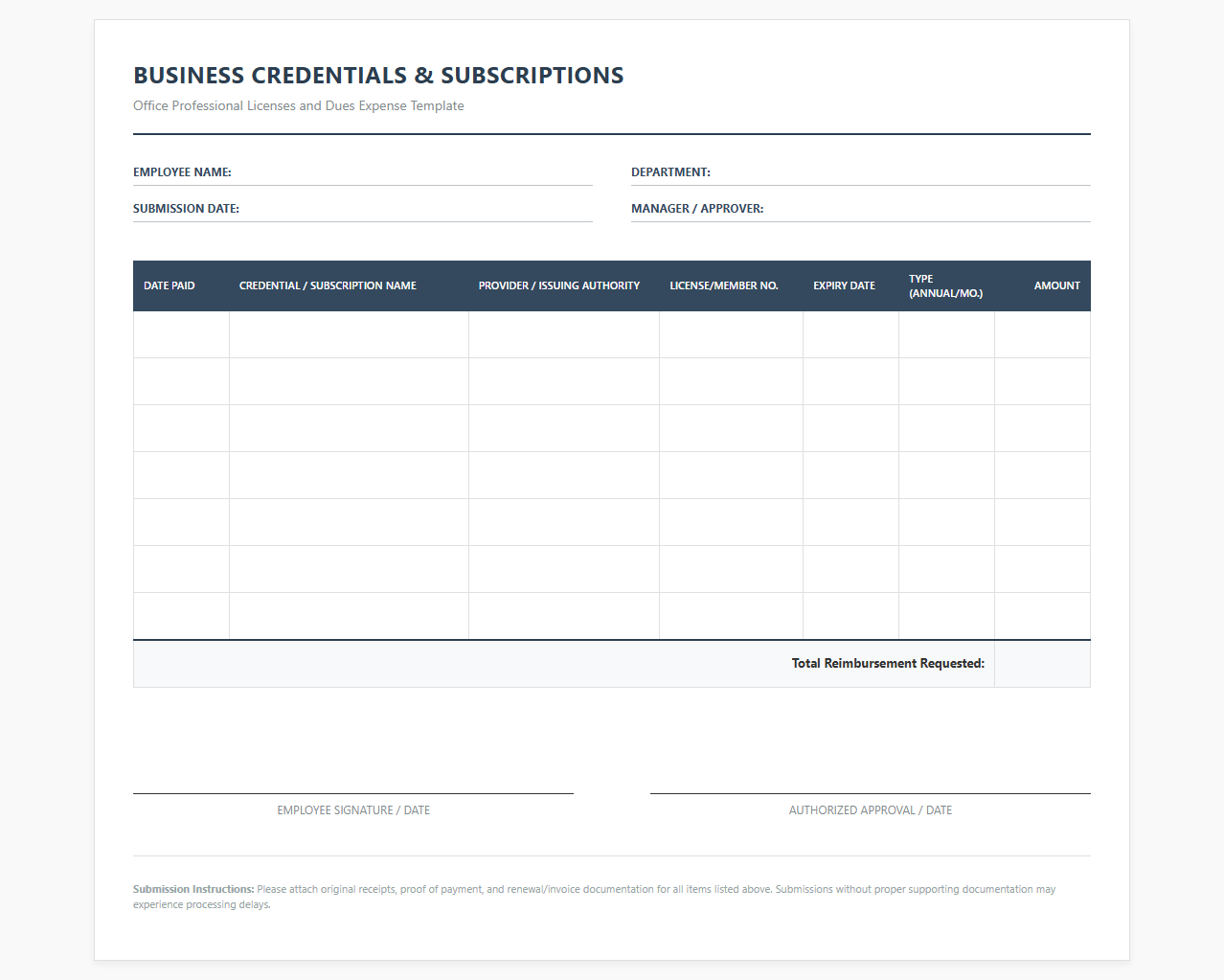

Business Credentials and Subscriptions Expense Template

Download: .PDF

Download: .PDF

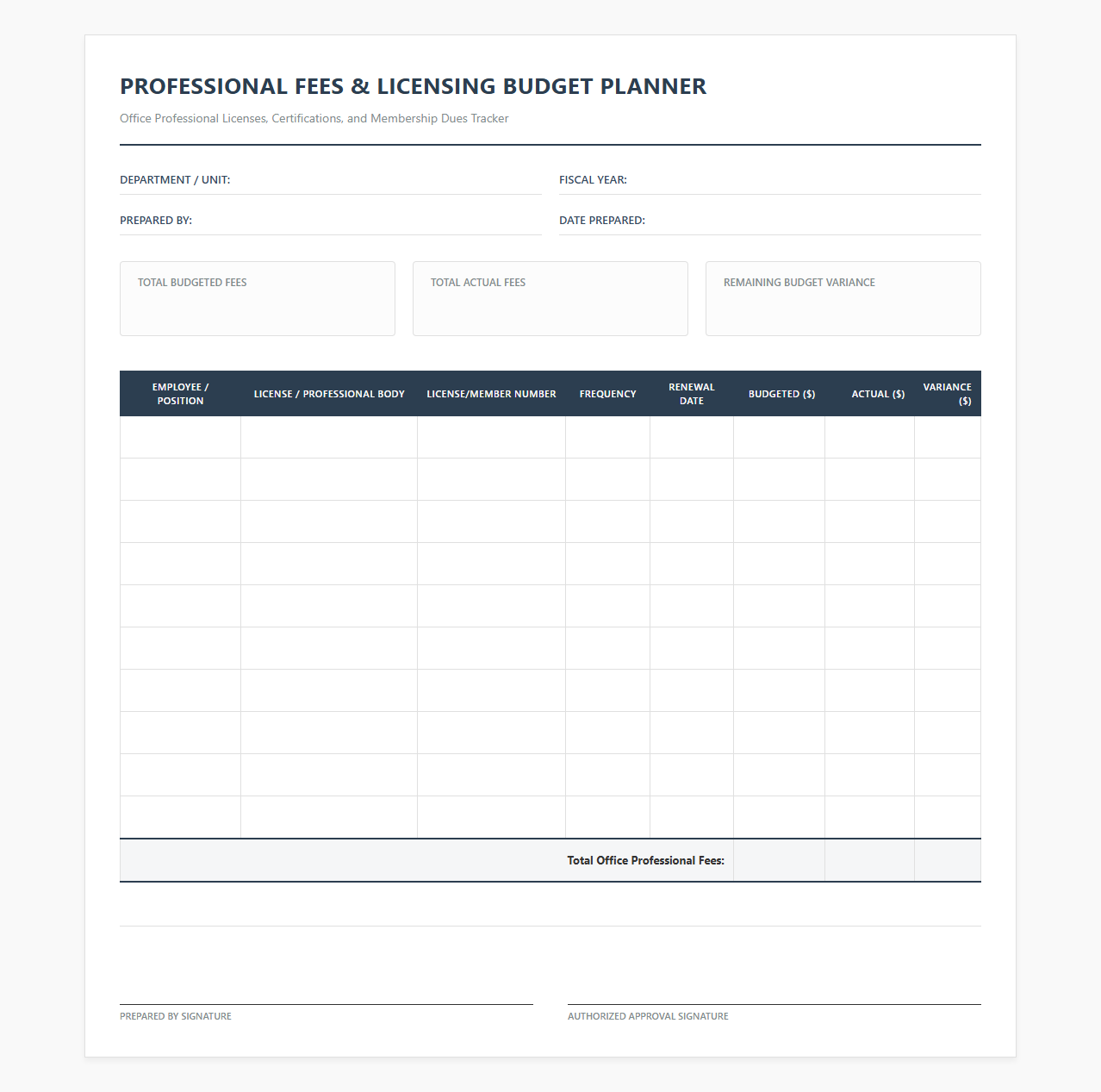

Professional Fees and Licensing Budget Planner

Download: .PDF

Download: .PDF

Corporate Membership and Licensing Expense Record

Download: .PDF

Download: .PDF

Office Professional Dues Reimbursement Form

Download: .PDF

Download: .PDF

Certifications and Professional Dues Cost Tracker

![]() Download: .PDF

Download: .PDF

Introduction to Expense Standardization for Licenses and Dues

In modern corporate environments, tracking professional licenses, certifications, and organizational dues can quickly become an administrative challenge. Establishing a standardized system for these expenses is vital for maintaining tight financial control and robust regulatory compliance. By unifying how these costs are recorded, organizations can prevent duplicate payments, forecast annual recurring costs with high precision, and ensure that all team members maintain the active credentials required to perform their duties safely and legally.

Defining and Categorizing Licenses versus Dues

To avoid misallocation in the general ledger, it is essential to distinguish between different types of professional and operational fees. Clear categorization ensures accurate tax reporting and better budget oversight.

Professional Credentials

These are individual-specific certifications required for an employee to legally practice their profession within the organization. Examples include Certified Public Accountant (CPA) licenses, state bar associations, or medical board certifications.

Regulatory Licenses

These are corporate or facility-level permits required by local, state, or federal agencies to operate the business legally. This includes health department permits, environmental licenses, and municipal operating certificates.

Office and Association Dues

These are voluntary or industry-recommended memberships in professional organizations, local chambers of commerce, or trade associations that benefit the organization's network and industry standing rather than fulfilling a strict legal requirement.

Implementing a Unified Submission Workflow

A structured, digital submission workflow minimizes processing delays and ensures all transactions are logged uniformly across the organization.

- The employee logs into the centralized expense management portal and selects the "Licenses and Dues" category.

- The employee enters key metadata, including the renewal frequency, expiration date, and the specific certifying body.

- The employee attaches the required digital invoice and proof of payment to the electronic submission form.

- The system automatically routes the request to the department manager for validation of business necessity.

- Once approved, the transaction is forwarded to the finance department for final reconciliation and reimbursement.

Documentation and Receipt Retention Requirements

The accounting department requires specific documentation to substantiate reimbursement claims and satisfy internal and external audit standards. Incomplete submissions will be returned to the employee for correction.

- The official renewal notice or invoice clearly showing the vendor name, billing period, and itemized cost breakdown.

- A valid proof of payment, such as a credit card receipt, bank statement transaction, or cancelled check.

- A copy of the renewed certificate, card, or license showing the updated expiration date.

- A written justification if the expense represents an off-cycle renewal or an unexpected rate increase.

Establishing Approval Hierarchies and Validation Rules

To maintain fiscal responsibility, expense claims must follow a structured approval hierarchy based on the type and cost of the credential. The Department Manager acts as the first line of defense, validating that the license or membership is directly relevant to the employee's current job description. For expenses exceeding established thresholds, the Division VP must provide secondary authorization to confirm budget availability. Finally, the Compliance Officer or internal auditor periodically reviews high-cost regulatory licenses to ensure the organization remains in lockstep with industry laws and standards without overspending on redundant memberships.

Integration with Accounting Software and Tax General Ledgers

By mapping these expenses to specific general ledger accounts, organizations can seamlessly feed data into Enterprise Resource Planning (ERP) systems. Professional credentials are mapped directly to GL-6120 (Employee Professional Development), while corporate regulatory licenses are routed to GL-6840 (Taxes, Licenses, and Permits). Voluntary memberships and networking fees are directed to GL-6910 (Dues and Subscriptions). This systematic categorization allows tax software to automatically isolate fully deductible business expenses from those that are subject to tax limitations, simplifying year-end filings and shielding the company during audit cycles.

Periodic Audits and Continuous Policy Review

To maintain policy compliance and identify opportunities for cost savings, the finance team must conduct internal audits on a recurring basis. Quarterly reviews help identify inactive licenses held by former employees, while annual audits evaluate corporate memberships to negotiate bulk organizational discounts. This active oversight keeps internal controls sharp, prevents spend leakage, and ensures that the expense policy adapts to changing regulatory environments and organizational needs.

Leave a comment