Managing grant receivables is a notoriously complex endeavor. Nonprofits and research entities frequently struggle with fragmented tracking, mismatched allocation periods, and the administrative burden of delayed disbursements. To bridge this operational gap, organizations must first establish robust internal financial controls. Because grants represent critical funding that directly fuels long-term community impact, maintaining precise, real-time oversight is essential for securing donor trust and ongoing organizational viability.

However, effective management stipulates that finance teams clearly distinguish between conditional awards and unconditional promises to give. Utilizing standardized ledger templates to track key parameters-such as Federal Award Identification Numbers (FAIN), matching-fund ratios, and milestone-based drawdowns-provides the concrete proof required for clean regulatory audits.

Below, we outline the essential ledger template formats designed to streamline your receivables process, ensure compliance, and optimize your organization's cash flow management.

Grant Receivable Ledger Spreadsheet

Download: .PDF

Download: .PDF

Grant Funding Accounts Receivable Ledger

Download: .PDF

Download: .PDF

Nonprofit Grant Revenue Ledger Template

Download: .PDF

Download: .PDF

Grant Award Receivables Tracking Ledger

![]() Download: .PDF

Download: .PDF

Donor and Grant Receivable Ledger Book

Download: .PDF

Download: .PDF

Grant Income and Receivable Reconciliation Ledger

Download: .PDF

Download: .PDF

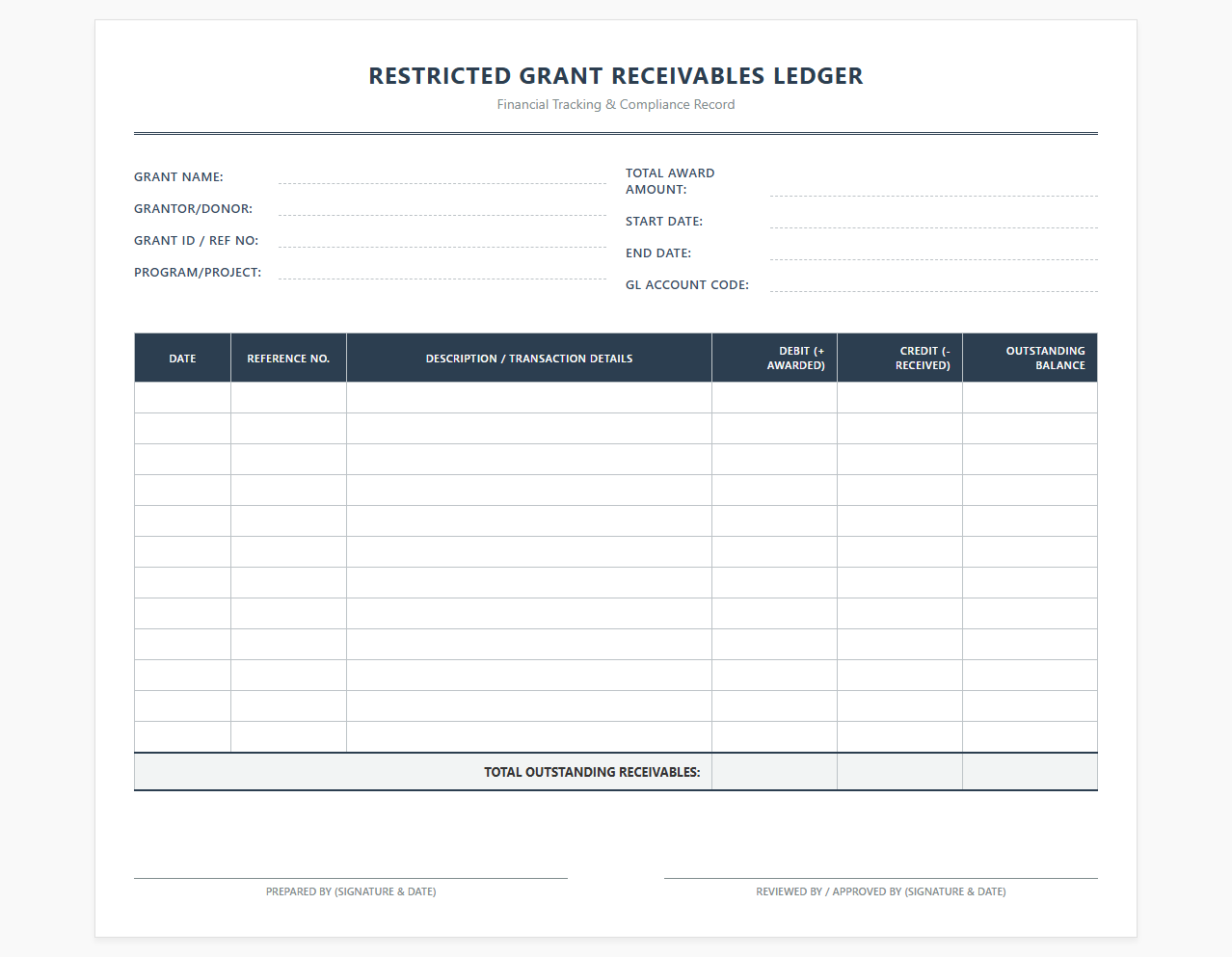

Restricted Grant Receivables Ledger Template

Download: .PDF

Download: .PDF

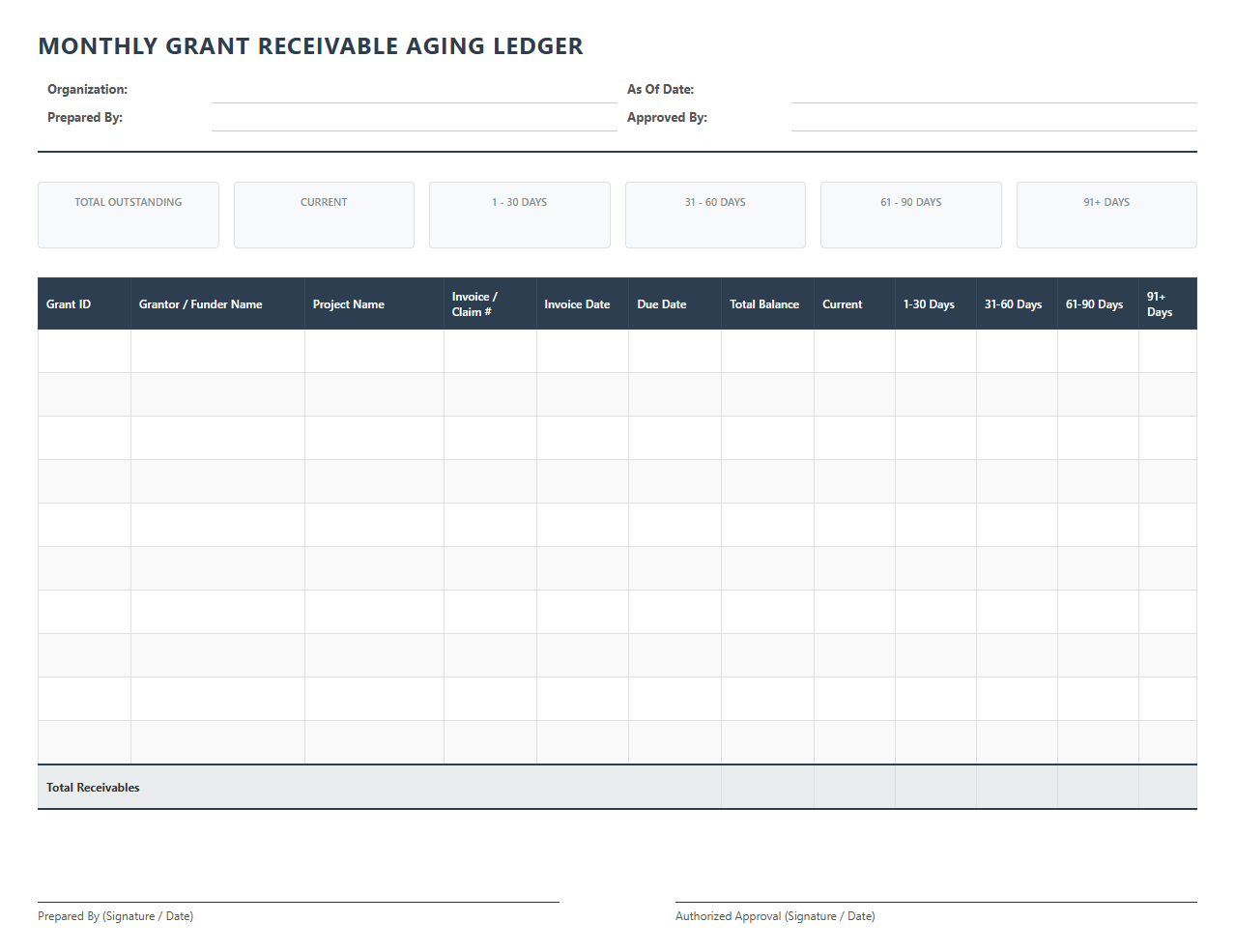

Monthly Grant Receivable Aging Ledger

Download: .PDF

Download: .PDF

Setting the Standard: The Role of Ledger Templates in Grant Tracking

For non-profit organizations and research institutions, securing funding is only the first step in a complex lifecycle of financial stewardship. Managing grant receivables requires meticulous precision to satisfy stringent donor requirements and maintain public trust. Structured ledger templates serve as the foundation of this process, providing a standardized framework to monitor incoming funds, track expenditures, and prevent compliance failures. By establishing a clear, repeatable system, organizations can ensure that every dollar is accounted for, safeguarding their operational integrity and securing future funding opportunities.

Anatomical Essentials: Key Columns Every Grant Ledger Must Include

An effective grant ledger must capture granular details to provide a comprehensive financial narrative. To maintain audit-ready records, templates must incorporate standardized columns that track unique identifiers and timing. The following fields form the absolute backbone of a compliant grant tracking sheet:

Award_ID: A unique alphanumeric identifier assigned to each specific grant.Disbursement_Date: The exact calendar date when funds are scheduled for release or actually received.Restriction_Status: A classification indicating whether funds are temporarily restricted, permanently restricted, or unrestricted.Funding_Source: The name of the government agency, foundation, or private donor providing the capital.

The Accrual Model: Tracking Committed vs. Realized Revenue

Understanding Accrual Accounting in Grant Management

Accrual-based ledger templates allow institutions to recognize revenue when it is earned, rather than when the cash physically enters the bank account. This model provides a more accurate reflection of fiscal health by matching committed revenue against the periods in which the corresponding research or service is performed.

"Recognizing grant revenue upon meeting performance obligations, rather than receipt, prevents artificial inflation of cash balances."

Milestone-Based Formats: Aligning Ledger Entries with Project Deliverables

Structuring Performance-Based Milestones

Performance-based grants release funds only when specific project deliverables are met. Ledgers tracking these awards must explicitly link financial records to project timelines, ensuring that revenue recognition aligns with verified achievements.

Multi-Funder Segregation: Preventing Co-mingling of Restricted Funds

Designing Segregated Ledger Structures

Co-mingling restricted funds is one of the quickest paths to a failed financial audit. When managing multiple funding sources simultaneously, templates must use strict classification boundaries to keep each fund's activities completely independent.

| Funder Name | Allocated Amount | Compliance Restriction |

|---|---|---|

| National Science Foundation | $150,000 | Equipment Purchase Only |

| Gates Foundation | $200,000 | Direct Fieldwork Expenses |

Reconciliation Frameworks: Ensuring Accuracy and Audit Readiness

Regular reconciliation safeguards the integrity of your grant ledger. Following a structured verification routine prevents discrepancies from compounding over time:

- Compare ledger entry balances with monthly bank statement transactions.

- Verify that all recognized receivables match official donor award letters.

- Cross-reference ledger totals against the central institutional financial report.

Digital Transition: Moving from Static Spreadsheets to Dynamic Systems

While manual templates are excellent for establishing initial workflows, scaling institutions must transition to automated accounting software. Moving your ledger formats into dynamic systems allows for real-time tracking, automatic bank feeds, and instant compliance reporting. This evolution minimizes human error and frees up valuable administrative resources to focus on programmatic success rather than manual data entry.

Leave a comment