Reconciling quarterly state unemployment insurance (SUI) tax filings is a notoriously stressful task for payroll professionals. Minor variance discrepancies often trigger painful state audits, costly penalties, and endless hours of manual data tracing. Before rushing to file amended returns, however, organizations must first establish a standardized framework to isolate where these systemic reporting mismatches occur.

Deploying a structured State Unemployment Tax Ledger Template grants your finance team immediate operational clarity, turning chaotic historical data into audit-ready insights. While these templates significantly streamline reconciliation, users must keep in mind that their efficacy relies on inputting accurate state-specific taxable wage caps-such as California's $7,000 threshold versus Washington's much higher limit.

This article will guide you through mapping payroll register outputs to your ledger, isolating common reporting anomalies, and implementing a repeatable compliance workflow.

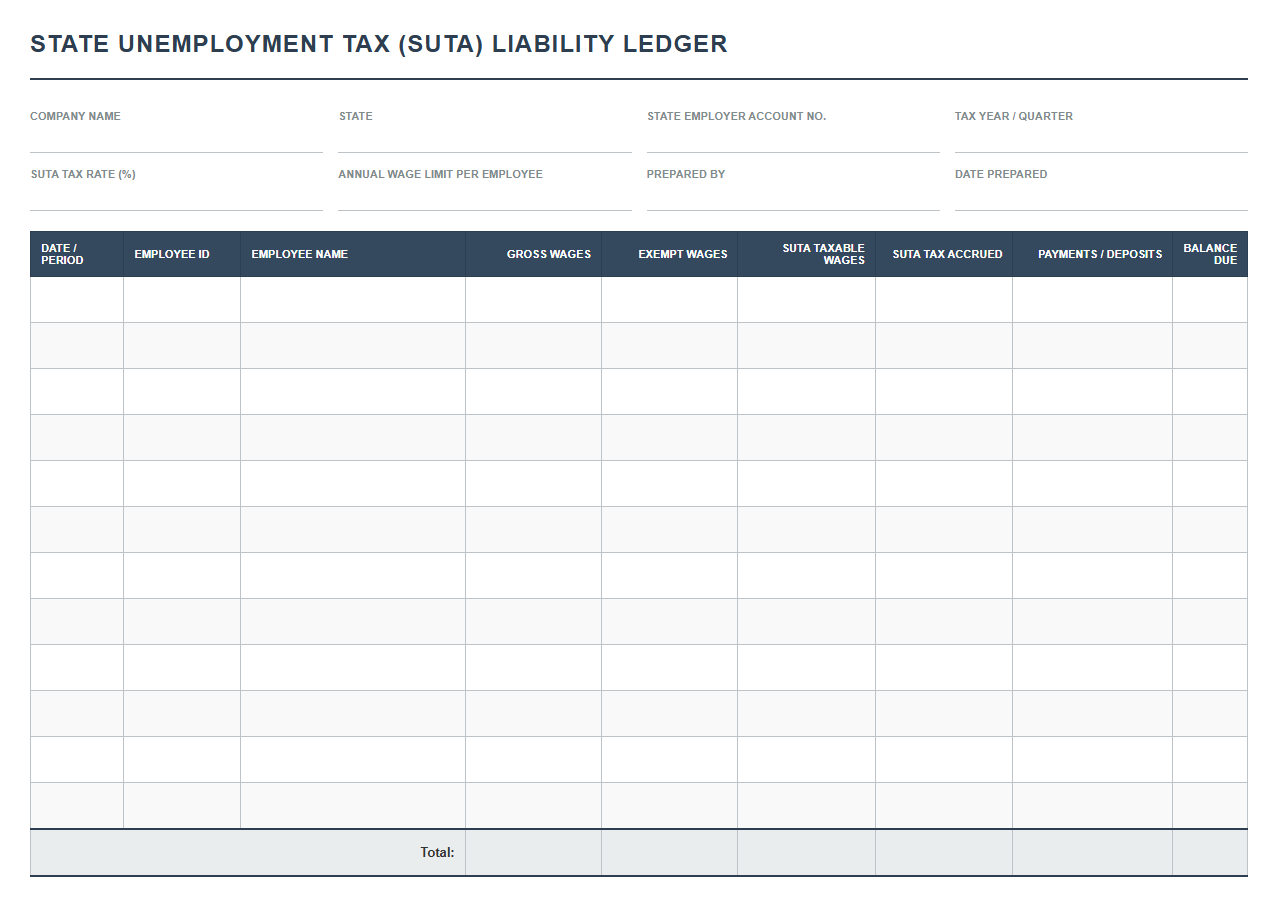

State Unemployment Tax Liability Ledger

Download: .PDF

Download: .PDF

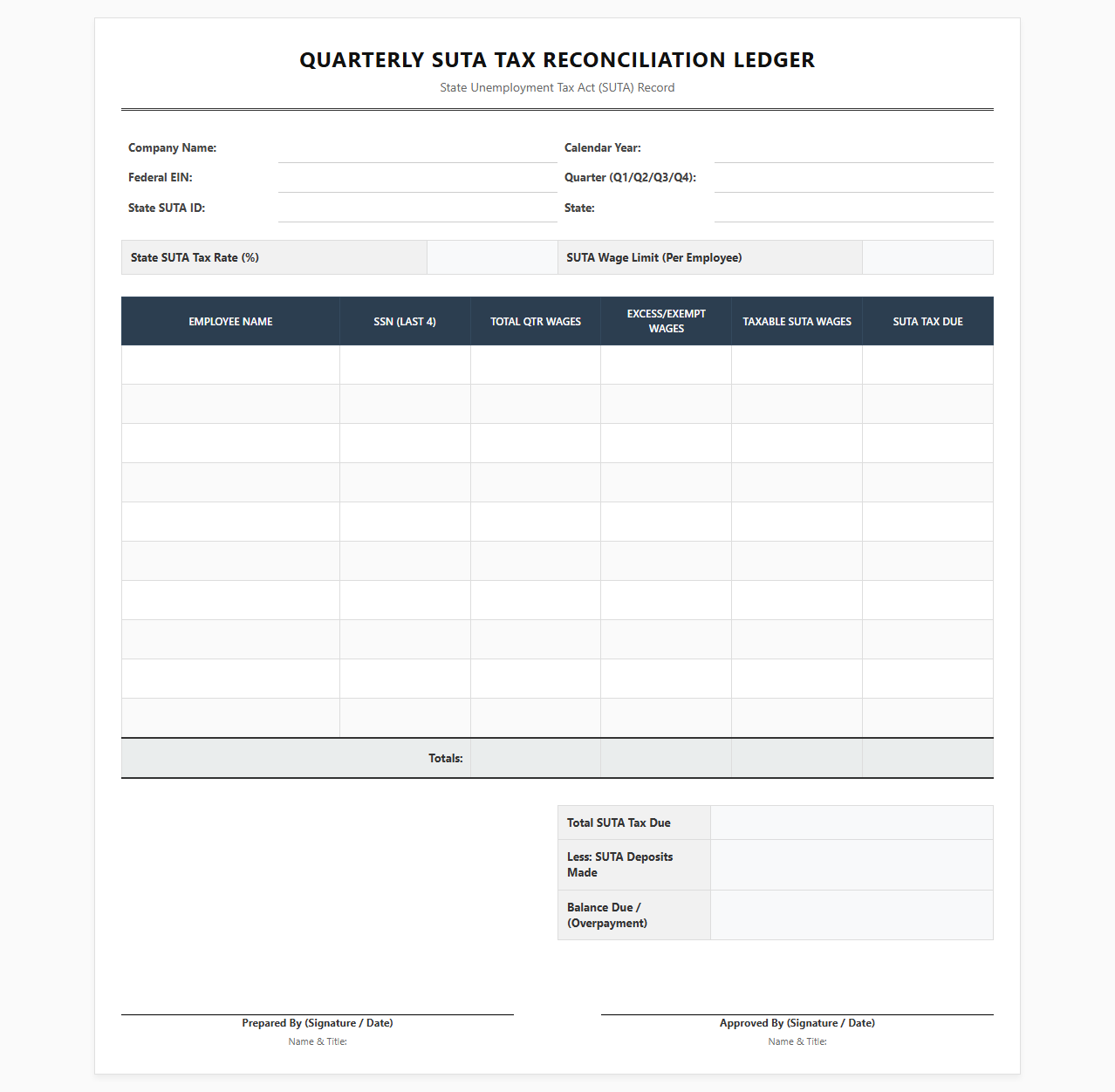

Quarterly SUTA Tax Reconciliation Ledger

Download: .PDF

Download: .PDF

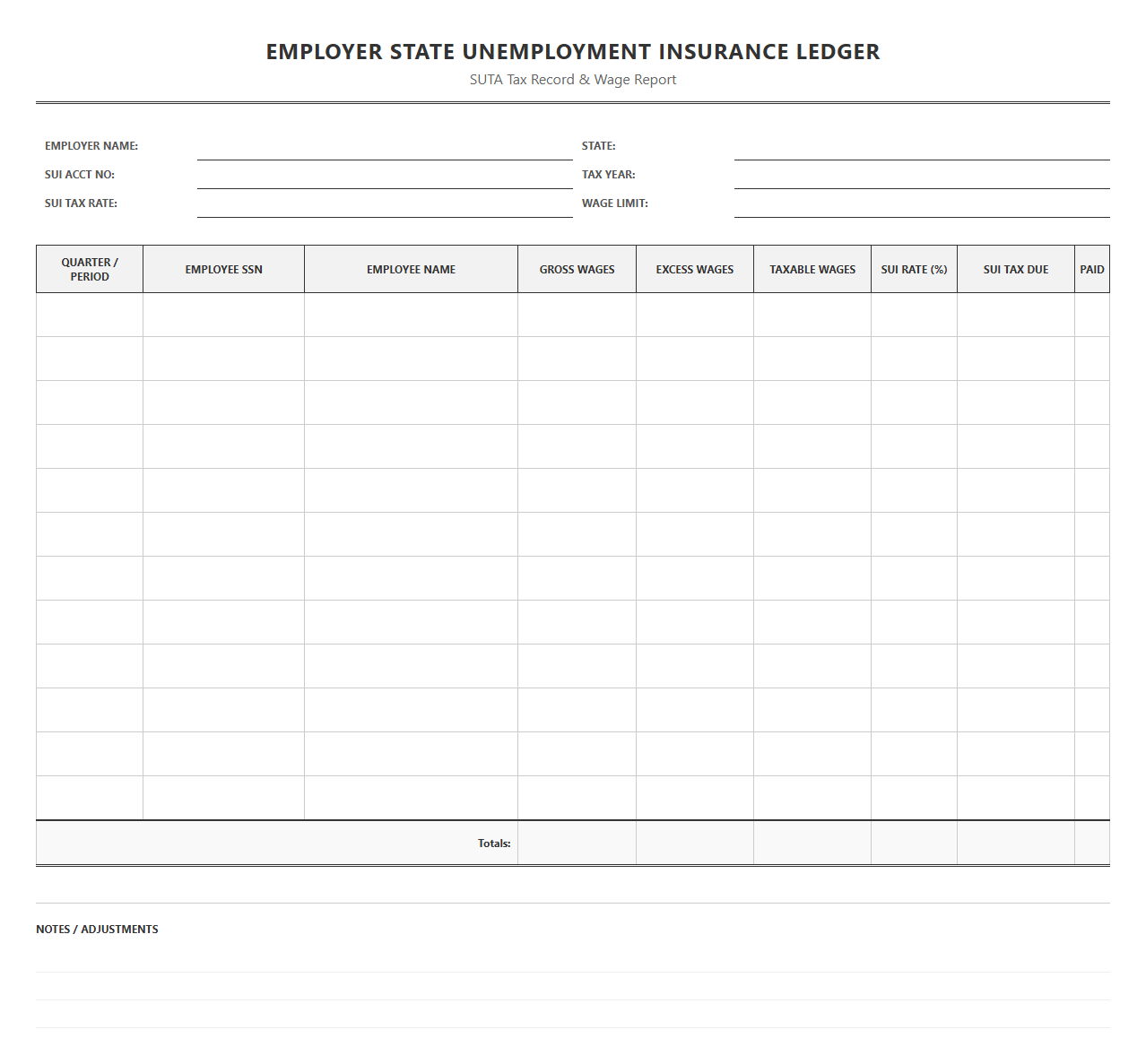

Employer State Unemployment Insurance Ledger

Download: .PDF

Download: .PDF

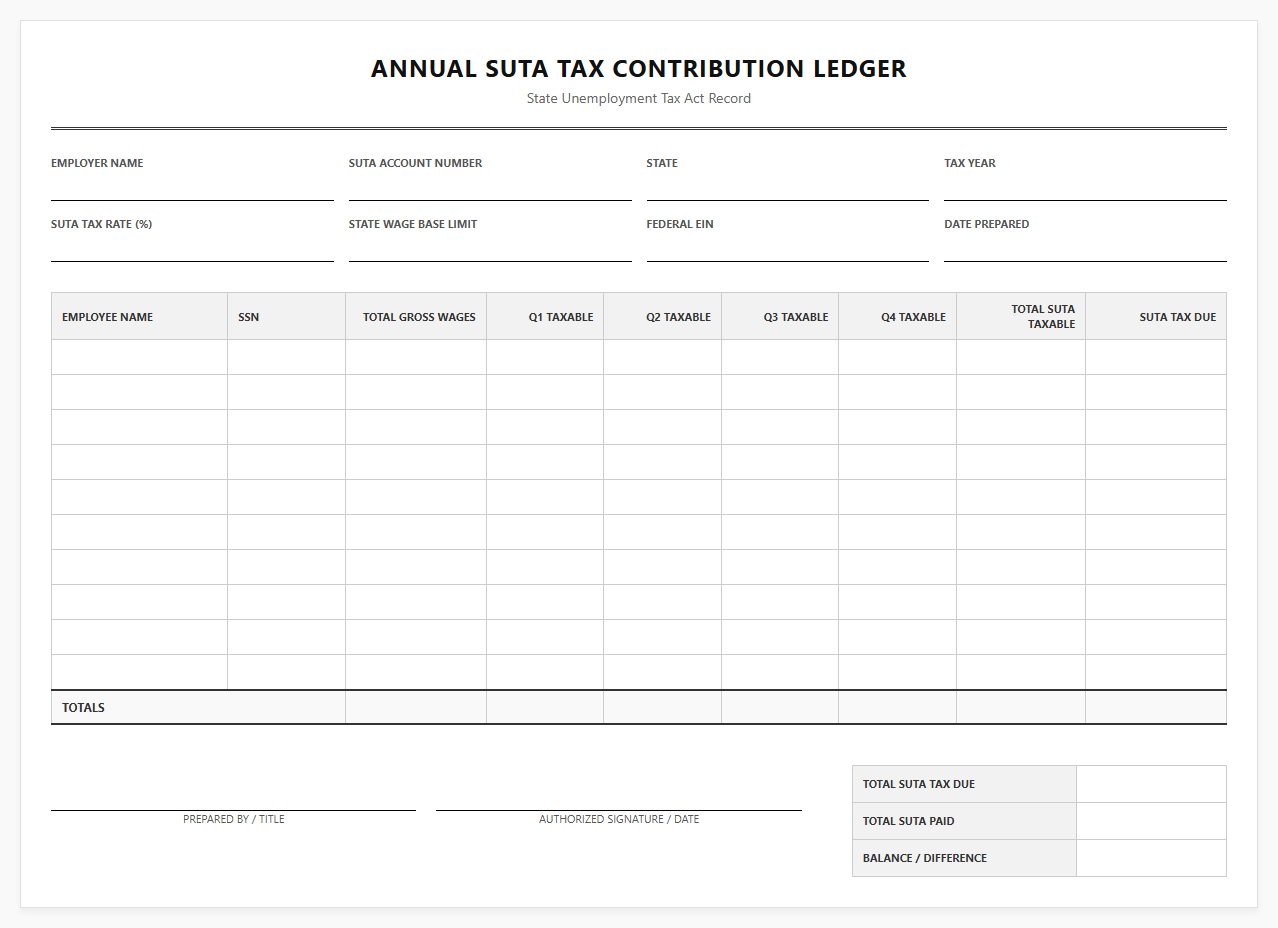

Annual SUTA Tax Contribution Ledger

Download: .PDF

Download: .PDF

State Unemployment Tax Payroll Deduction Ledger

Download: .PDF

Download: .PDF

Multi-State Unemployment Tax Allocation Ledger

Download: .PDF

Download: .PDF

SUI Tax Liability Ledger Template

Download: .PDF

Download: .PDF

Historical State Unemployment Tax Ledger Sheet

Download: .PDF

Download: .PDF

Understanding SUTA and the Challenge of Payroll Discrepancies

Navigating the complexities of the State Unemployment Tax Act (SUTA) is a critical responsibility for modern businesses. Because SUTA tax rates and taxable wage bases vary significantly by state, maintaining perfect compliance is highly challenging. Minor payroll reporting discrepancies-such as mismatched wage totals or miscalculated tax liabilities-can quickly capture the attention of state departments of labor, triggering costly, time-consuming state audits and severe financial penalties.

What is a SUTA Ledger Template?

A SUTA ledger template is a structured data tool that aggregates state-specific unemployment wage data across all employees. By serving as a single source of truth, it helps payroll teams track, calculate, and verify tax obligations before filing. Key columns within a SUTA ledger include:

Gross Wages: The total compensation paid to an employee during the reporting period.Exempt Wages: Earnings that are legally excluded from SUTA tax calculations, such as certain retirement contributions or specific fringe benefits depending on the state.Taxable Wage Limits: The maximum amount of employee earnings subject to SUTA tax, which varies widely by state and resets annually.SUTA Taxable Wages: The calculated portion of gross wages (up to the state limit) that is actually subject to the tax rate.

Common Sources of Payroll Reporting Discrepancies

Payroll errors rarely stem from deliberate non-compliance; instead, they are usually the result of structural gaps or human oversight in tracking dynamic workforces. The most common causes of SUTA reporting discrepancies include:

- Out-of-State Remote Employees: Assigning employee SUTA liability to the company's headquarters state instead of the physical state where the remote worker performs their duties.

- Misclassified Workers: Improperly labeling employees as independent contractors, which leads to unreported wages and potential retroactive tax audits.

- Incorrect State-Specific Wage Caps: Failing to update payroll systems when states change their annual taxable wage limits, resulting in overpayments or underpayments.

Step-by-Step Reconciliation Using Your Ledger

To ensure total accuracy, payroll administrators must perform systematic reconciliations by comparing quarterly Form 941 filings, SUTA state returns, and individual employee payroll registers against the ledger template. Use the following structured cross-reference guide to identify variances:

| Reconciliation Step | Data Source A | Data Source B | Target Variance |

|---|---|---|---|

| Verify Gross Wages | Quarterly Form 941 (Line 2) | Sum of all State SUTA Gross Wages | $0.00 (Must align fully) |

| Check Wage Cap Exemptions | SUTA Ledger (Exempt Wages Column) | Individual Employee Payroll Registers | $0.00 (Exemptions must match state laws) |

| Validate Taxable Wages | State Unemployment Return | SUTA Ledger (Taxable Wages Column) | $0.00 (Prevents filing overruns) |

Resolving Discrepancies with State Agencies

When a mismatch is identified after submission, taking immediate action is vital to minimize interest charges. Employers must follow a clear protocol to correct prior-quarter wage reports and adjust filed returns with the appropriate state tax authorities.

Always submit an amended SUTA return (often marked as Form UI-3/4 or equivalent depending on the state) alongside a detailed explanation of the correction to resolve discrepancies before an audit is initiated.

Proactive Best Practices for Payroll Maintenance

Waiting until the end of the year to address payroll data is a recipe for compliance failure. Organizations should adopt continuous monitoring practices to identify and fix errors long before quarterly filing deadlines arrive:

- Conduct monthly internal audits by cross-referencing ledger reports with general ledger payroll accounts.

- Utilize automated ledger updates that integrate directly with your human resources information system (HRIS) to capture employee address changes in real-time.

- Establish a regular training schedule for payroll staff to keep them updated on changing state-by-state wage bases and UI tax rates.

Streamlining Compliance for Future Growth

Establishing a reliable SUTA ledger system is not just about avoiding immediate penalties; it is a foundational step toward sustainable business scaling. By maintaining a single, clean source of truth, organizations build audit readiness directly into their operational workflows. This systematic approach reduces the heavy administrative burden on HR and finance teams, ensures long-term financial accuracy, and allows leadership to focus on expansion without the lingering threat of unexpected regulatory costs.

Leave a comment