Managing employee expense reimbursements through payroll often leaves finance departments walking a regulatory tightrope, fearing costly tax penalties and internal audit failures. Before streamlining these workflows, organizations must recognize that the tax-exempt status of these payments relies entirely on precise accounting categorization rather than simple payroll entry.

Deploying the correct payroll document formats grants your business seamless audit protection while preserving the highly advantageous tax-free status of these payouts. Crucially, this benefit is stipulated on the strict adherence to IRS Accountable Plan rules, requiring robust employee substantiation. For instance, utilizing dedicated, non-taxable earning codes on pay stubs or isolating reimbursements on Form W-2 (such as Box 12 codes) serves as concrete proof of compliance.

This guide will detail the essential payroll document formats, compliance pitfalls to avoid, and step-by-step methods to optimize your reimbursement architecture for maximum tax efficiency.

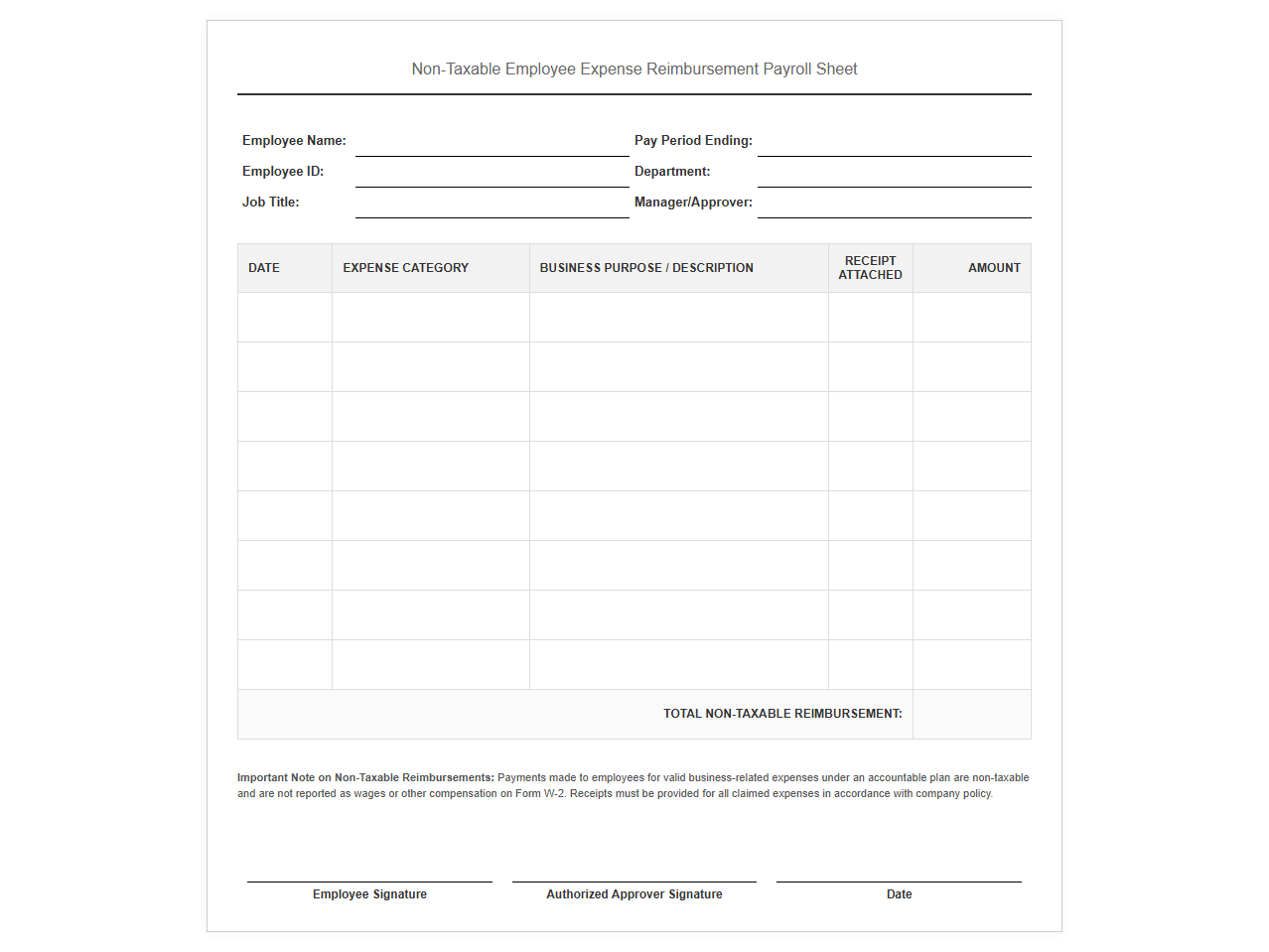

Non-Taxable Employee Expense Reimbursement Payroll Sheet

Download: .PDF

Download: .PDF

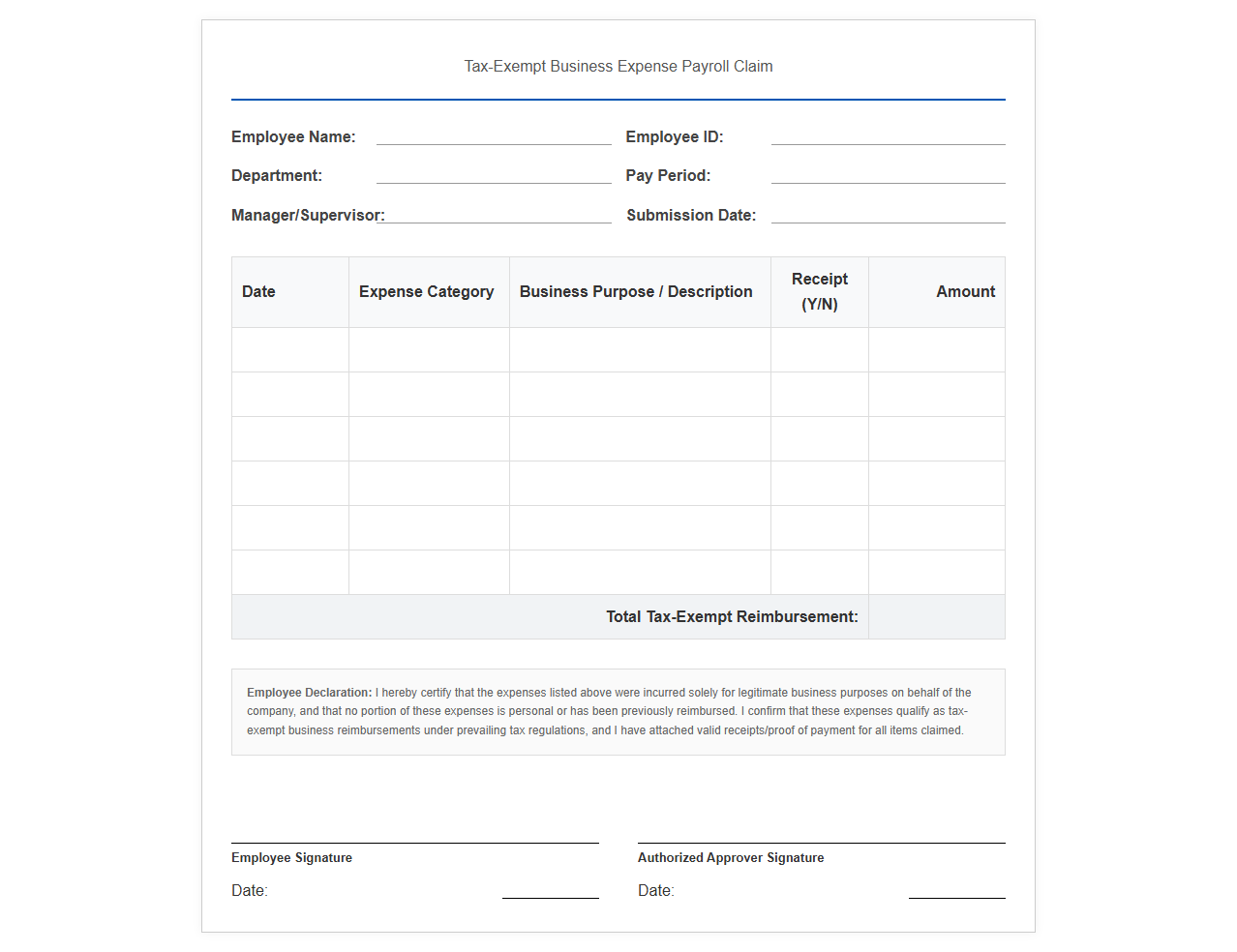

Tax-Exempt Business Expense Payroll Claim Template

Download: .PDF

Download: .PDF

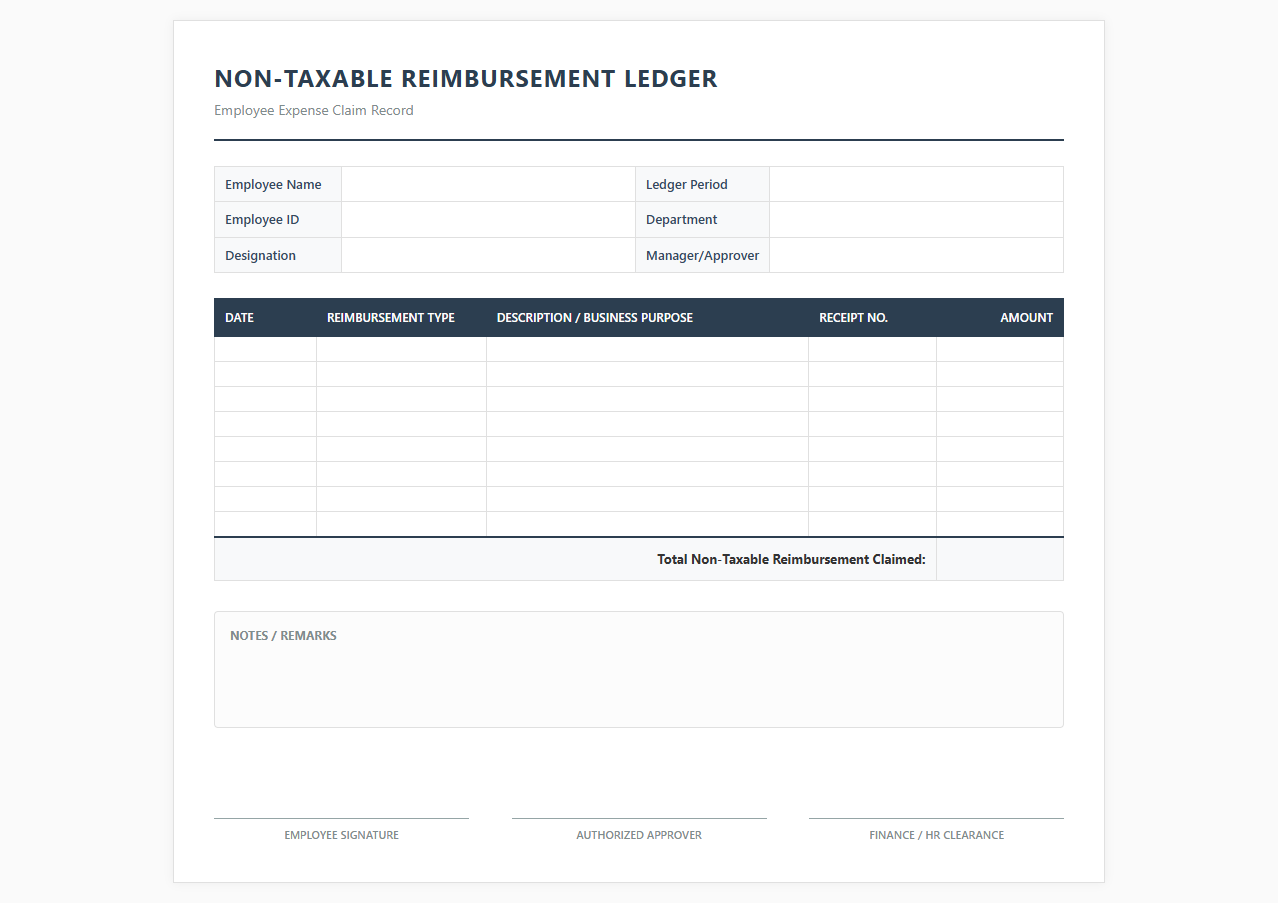

Employee Non-Taxable Reimbursement Ledger Document

Download: .PDF

Download: .PDF

Monthly Non-Taxable Payroll Reimbursement Tracker

![]() Download: .PDF

Download: .PDF

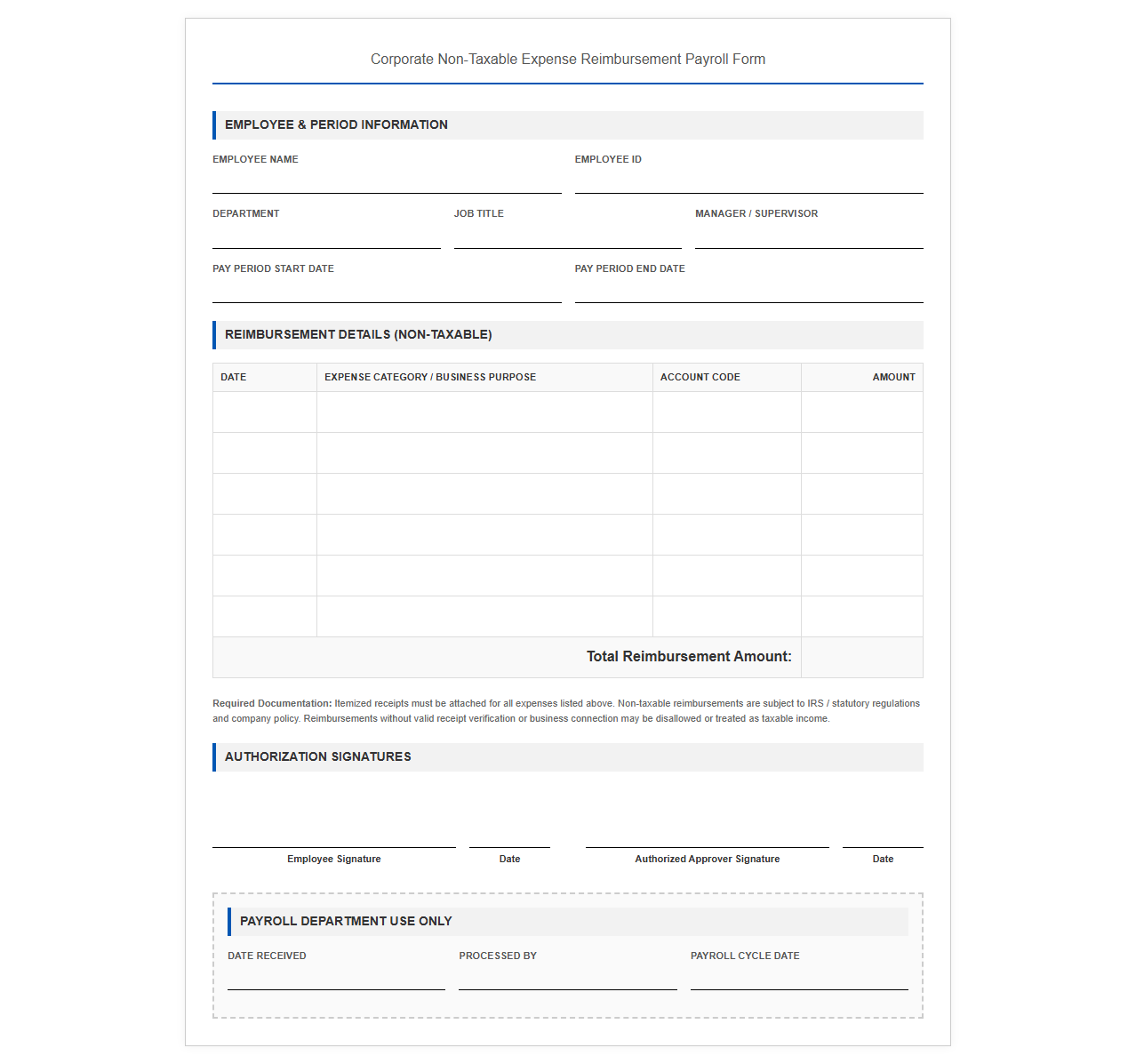

Corporate Non-Taxable Expense Reimbursement Payroll Form

Download: .PDF

Download: .PDF

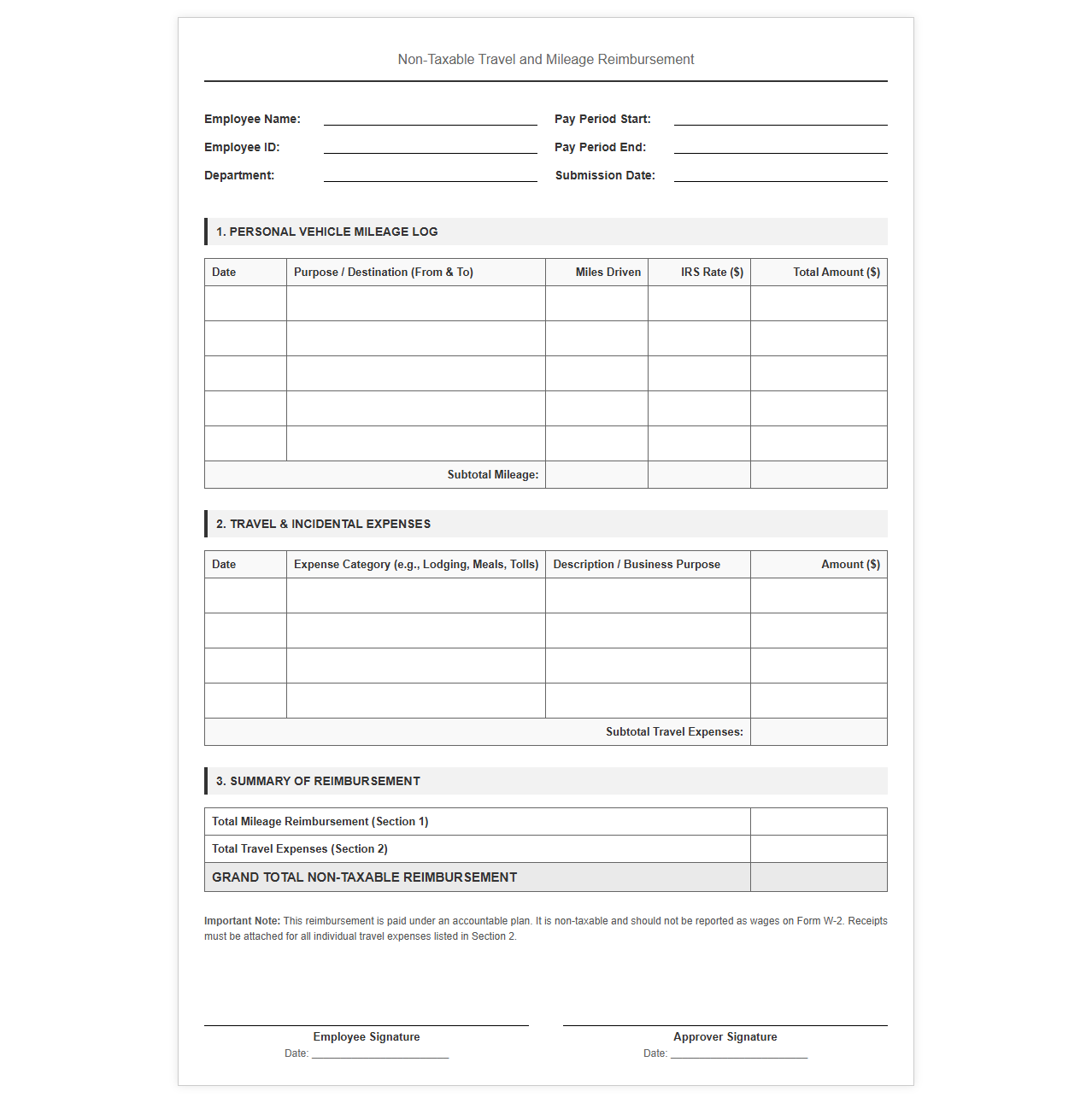

Non-Taxable Travel and Mileage Reimbursement Payroll Template

Download: .PDF

Download: .PDF

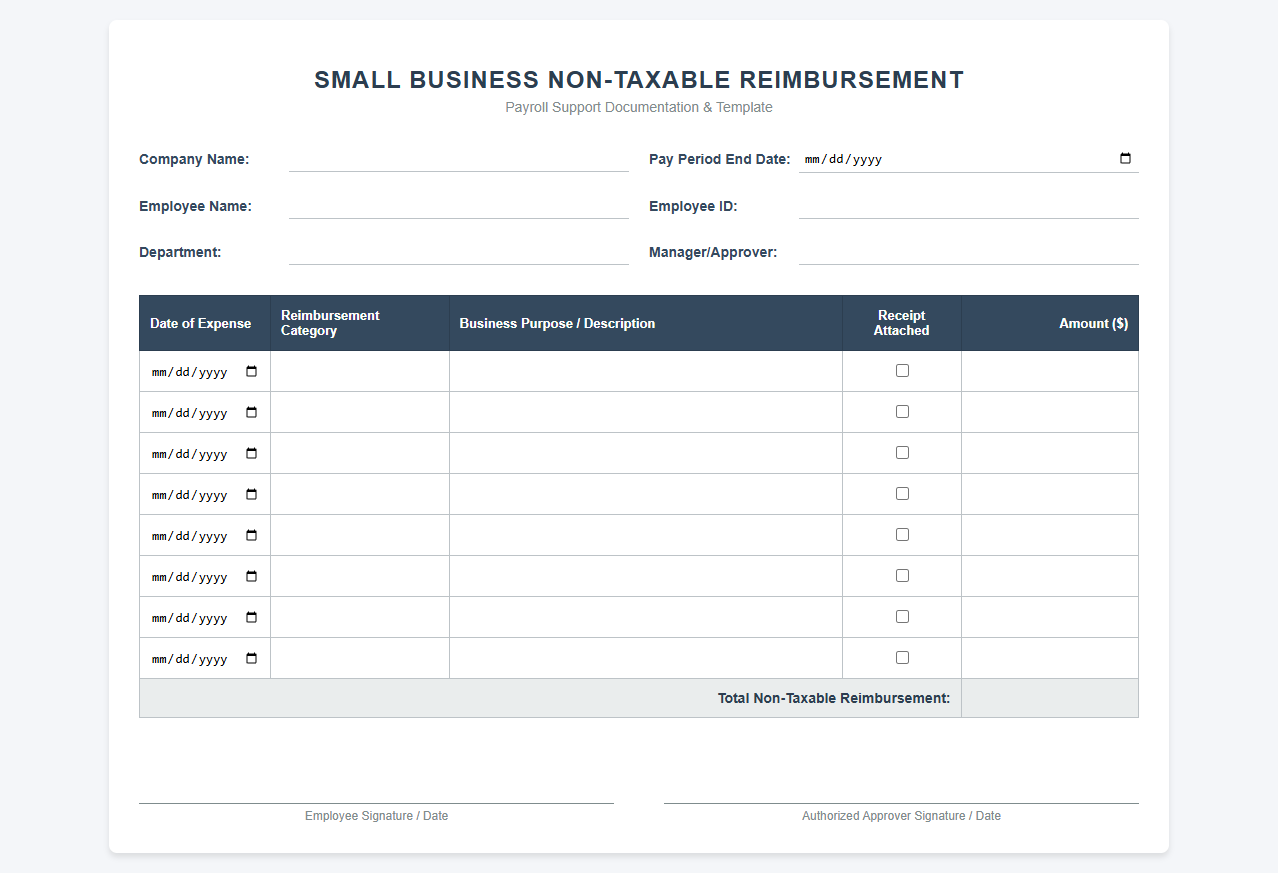

Small Business Non-Taxable Reimbursement Payroll Spreadsheet

Download: .PDF

Download: .PDF

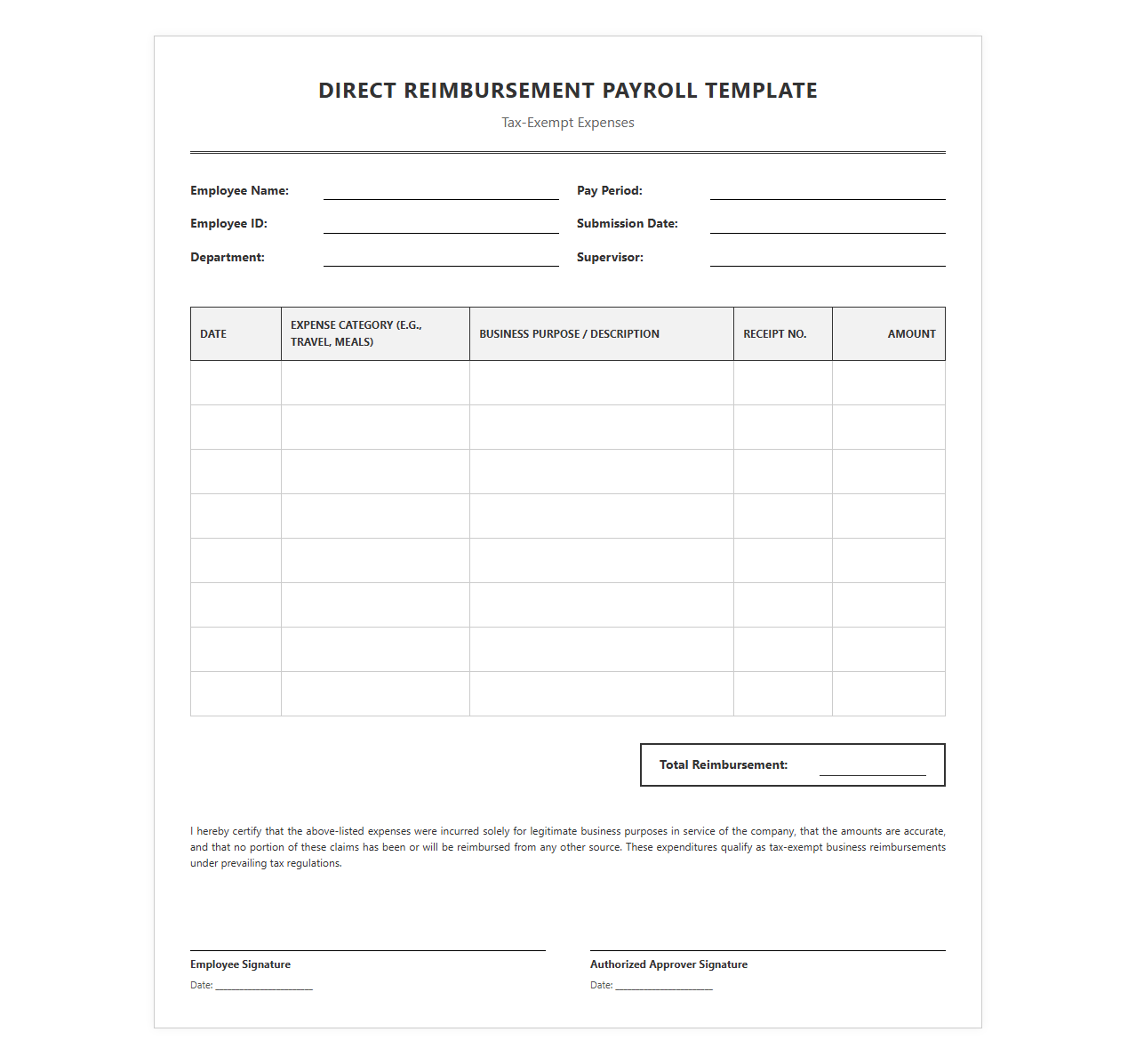

Direct Reimbursement Payroll Template for Tax-Exempt Expenses

Download: .PDF

Download: .PDF

Establishing the Foundation: Non-Taxable Reimbursement Compliance

Separating taxable wages from non-taxable expense reimbursements is a critical financial strategy for modern enterprises. By properly categorizing these payments, businesses can significantly minimize their payroll tax liabilities while ensuring strict compliance with IRS regulations. Failing to distinguish between regular income and business-related expense repayments can result in costly tax penalties and unnecessary audits. Establishing a clear boundary between these two payment structures protects both the employer and the employee, optimizing overall tax efficiency.

The Core Framework: IRS Accountable Plan Requirements

To guarantee that expense reimbursements remain non-taxable, employers must establish and maintain an Accountable Plan. The IRS enforces three distinct criteria that every business must meet to justify this tax-exempt status:

- Business Connection: The expenses must have been incurred while performing services as an employee of the company.

- Substantiation: Employees must provide adequate proof of the expenses, including dates, locations, and amounts, within a reasonable timeframe.

- Returning Excess Amounts: Any excess reimbursement or allowance must be returned to the employer within a designated period.

Standardizing Payroll Document Formats for Reimbursements

Choosing the right format for reporting and documenting non-taxable payments is essential for system compatibility and administrative efficiency. The table below compares the most common payroll document formats used in business today.

| Format | Primary Use Case | Audit Suitability |

|---|---|---|

| PDF Receipts | Visual proof of purchase and vendor verification | High |

| CSV Logs | Bulk data transfer and simple internal audits | Medium |

| Structured Digital Ledgers | Automated compliance tracking and software integration | Very High |

Critical Data Fields for Compliant Expense Documentation

To satisfy regulatory scrutiny, payroll files must contain specific information linked to each reimbursement. Missing even one of these fields can invalidate the non-taxable status of a payment. Your documentation system should mandate the following inputs:

- Transaction Date: The exact date the expense was incurred, ensuring it aligns with the business activity period.

- Business Purpose Description: A detailed explanation of how the expense directly benefits company operations.

- Original Receipt Cross-Reference: A unique identifier linking the digital transaction entry directly to the original supporting document.

Integrating Expense Management with Modern Payroll Systems

Manual data entry is one of the most common points of failure in expense management. By utilizing automated API integrations, organizations can seamlessly sync expense software directly with their payroll ledgers. This connection ensures that approved reimbursements flow automatically into the payment pipeline without human intervention, eliminating discrepancies.

Bulletproofing Your Payroll for Regulatory Audits

Defending your organization's reimbursement tax exemptions during a regulatory audit requires an organized and accessible digital archive. Tax authorities prioritize historical accuracy and structured audit trails over self-reported ledgers.

An organization's audit defense is only as strong as its weakest record. Continuous digital archiving remains the most reliable method to verify compliant expense processing.

Internal Revenue Manual Guidelines

Continuous Optimization: Policy Reviews and Training

Tax regulations and operational structures are constantly evolving. Implementing annual policy reviews ensures your accountable plan remains aligned with the latest IRS guidelines. Regular evaluations of your internal guidelines prevent compliance drift and identify potential structural vulnerabilities before they escalate.

Equally critical is the implementation of regular employee training programs. Educating staff on proper documentation practices ensures higher data accuracy at the source, reducing the burden on payroll administrators. By combining regular policy updates with structured training, your organization sustains high compliance standards and protects its non-taxable status over the long term.

Leave a comment