Managing payroll deductions for employee retirement accounts is a recurring headache for HR and finance professionals. A single manual data entry error can easily trigger compliance penalties, skew employee tax liabilities, and damage organizational trust.

Before implementing a solution, it is critical to position this challenge within the context of changing state-mandated retirement programs and shifting IRS contribution limits. Standardizing these complex workflows through structured payroll templates grants administrators absolute processing consistency and audit-ready accuracy, transforming a high-risk monthly chore into a seamless operation.

Note on Scope: While these standardized templates drastically reduce human error, they are designed as operational frameworks and should not replace certified tax or legal counsel.

For instance, a robust template must cleanly differentiate between pre-tax formulas for Traditional IRAs and post-tax withholding rules for Roth IRAs. In this article, we will examine how to build these templates, integrate automatic validation checks, and establish a foolproof withholding workflow.

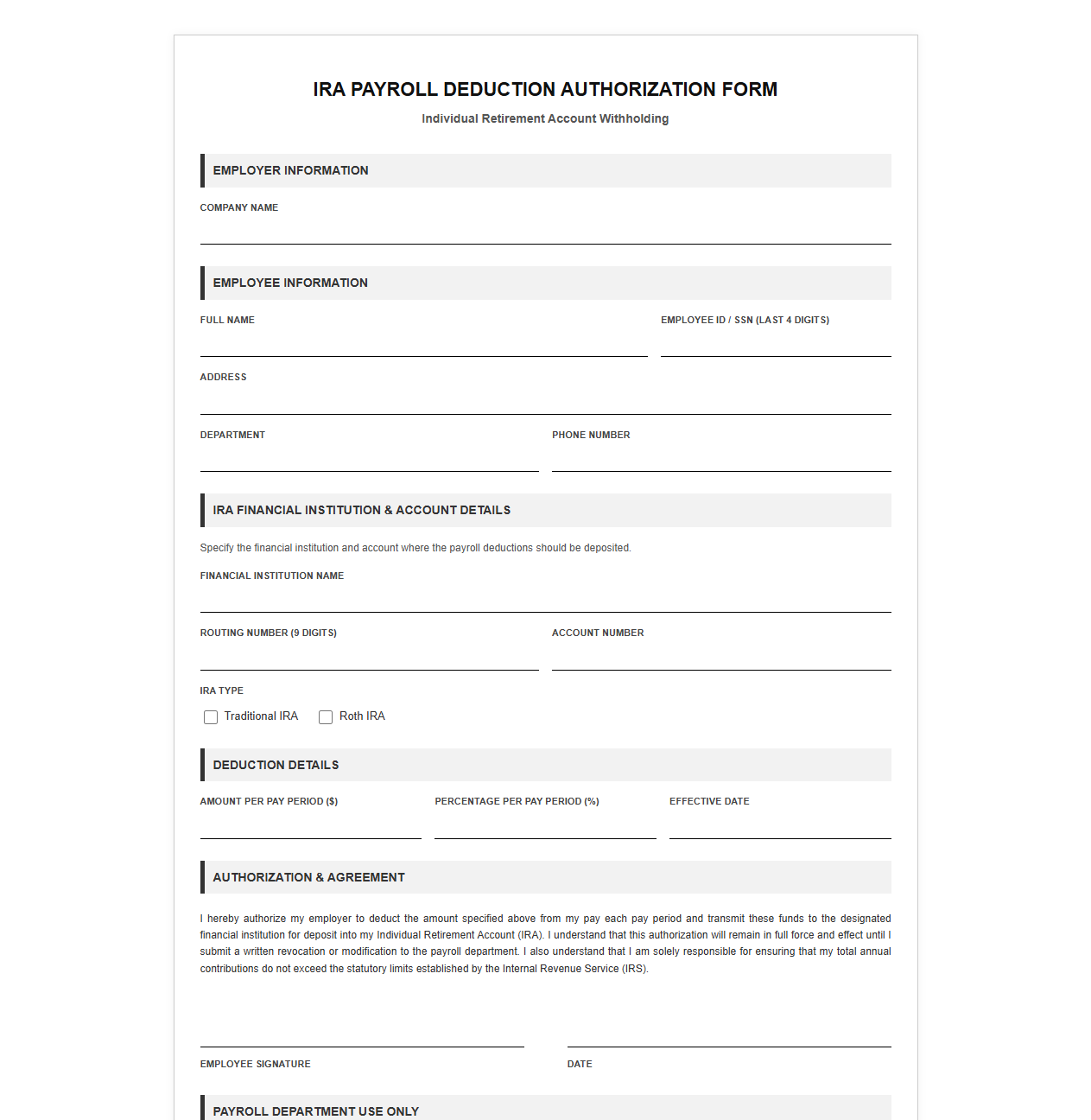

IRA Payroll Deduction Authorization Form

Download: .PDF

Download: .PDF

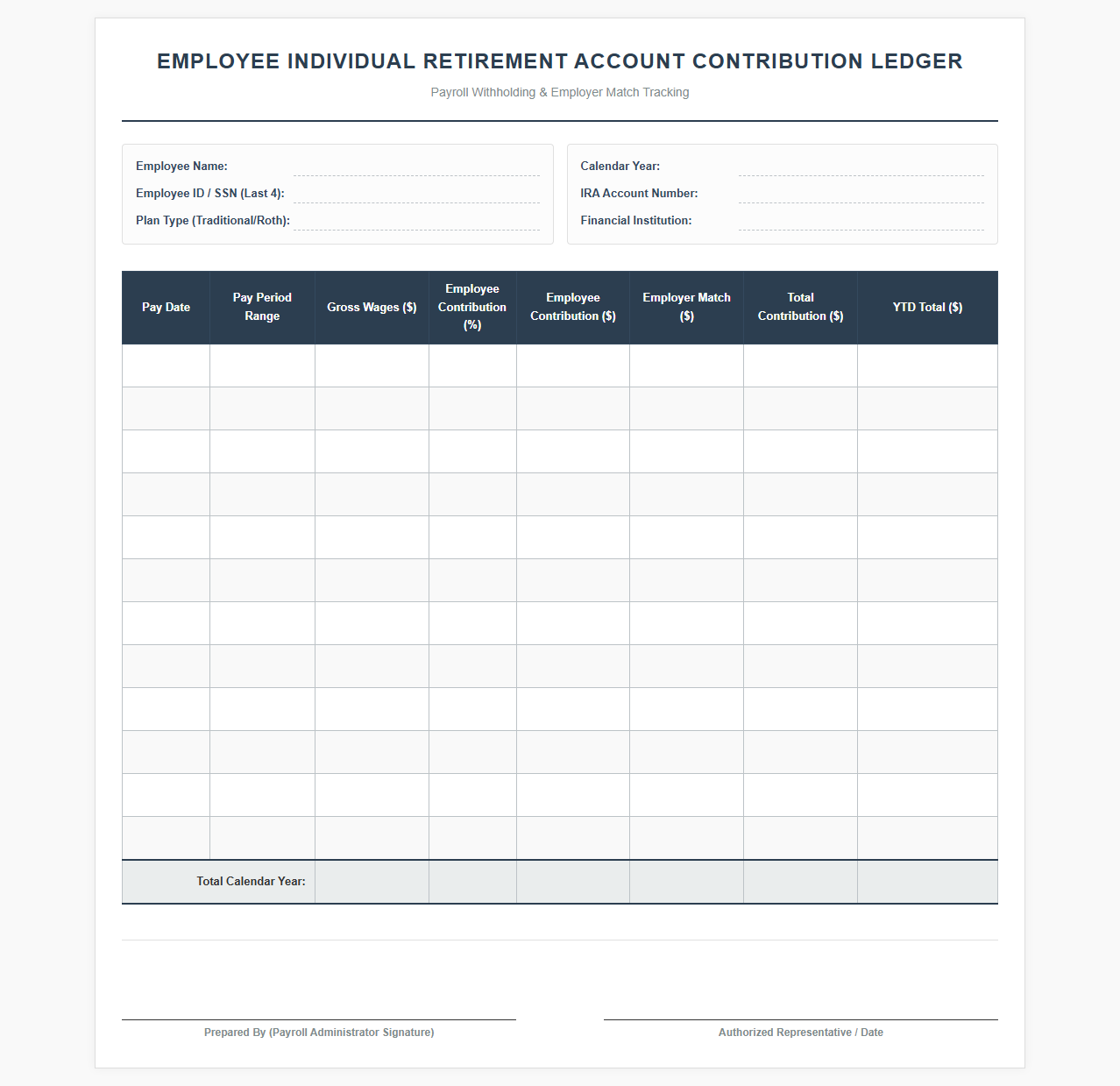

Employee Individual Retirement Account Contribution Ledger

Download: .PDF

Download: .PDF

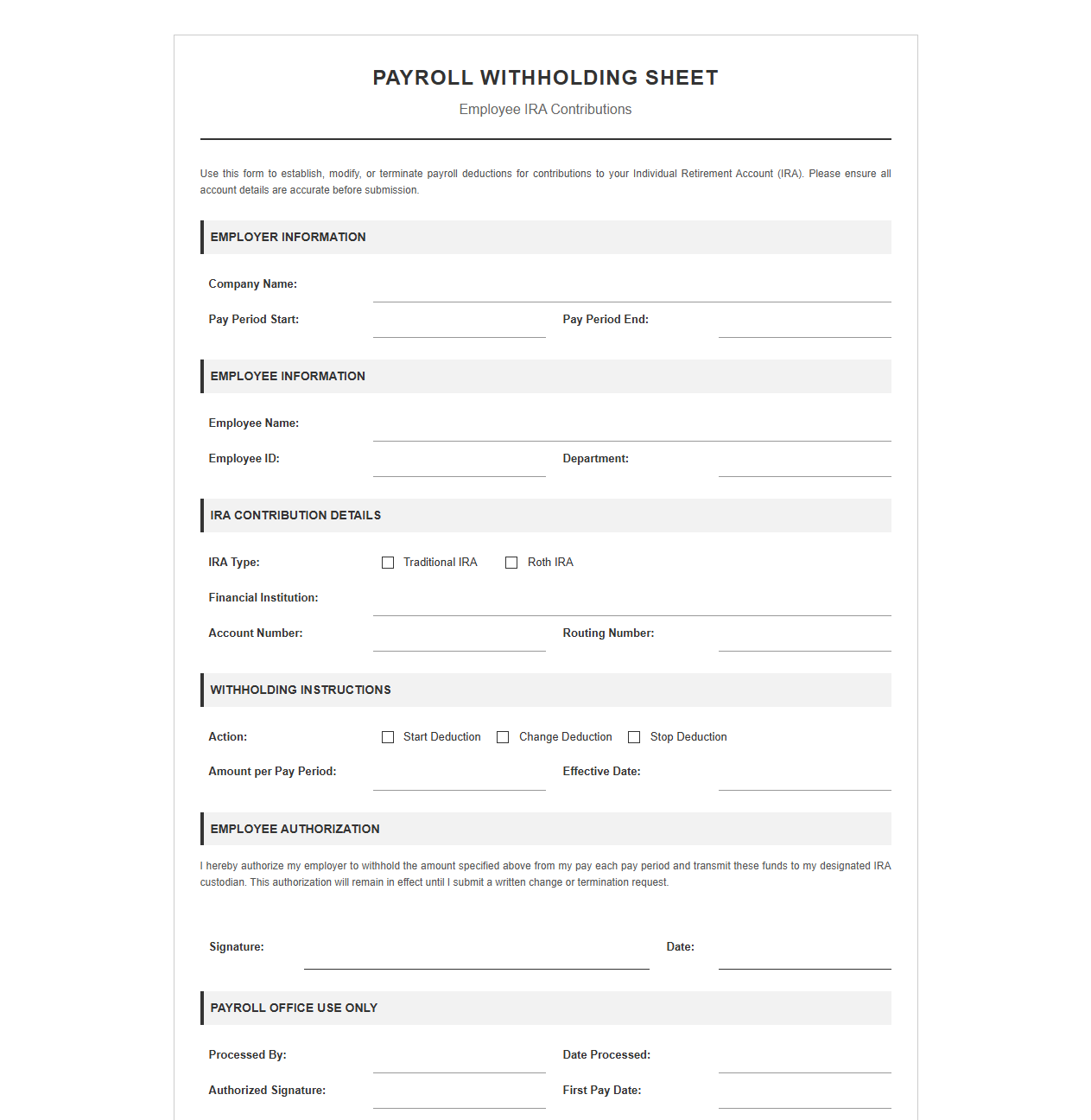

Payroll Withholding Sheet for Employee IRA Contributions

Download: .PDF

Download: .PDF

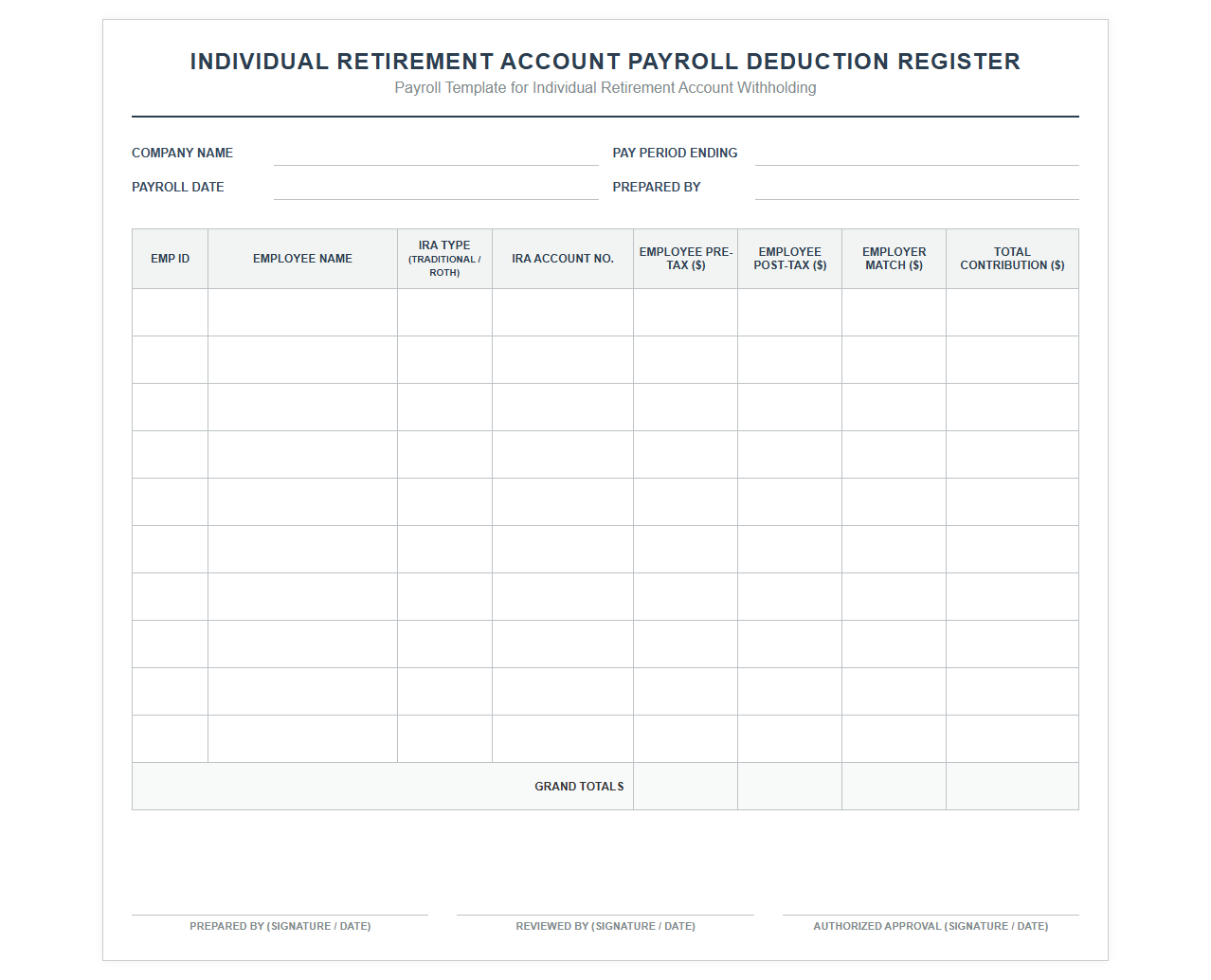

Individual Retirement Account Payroll Deduction Register

Download: .PDF

Download: .PDF

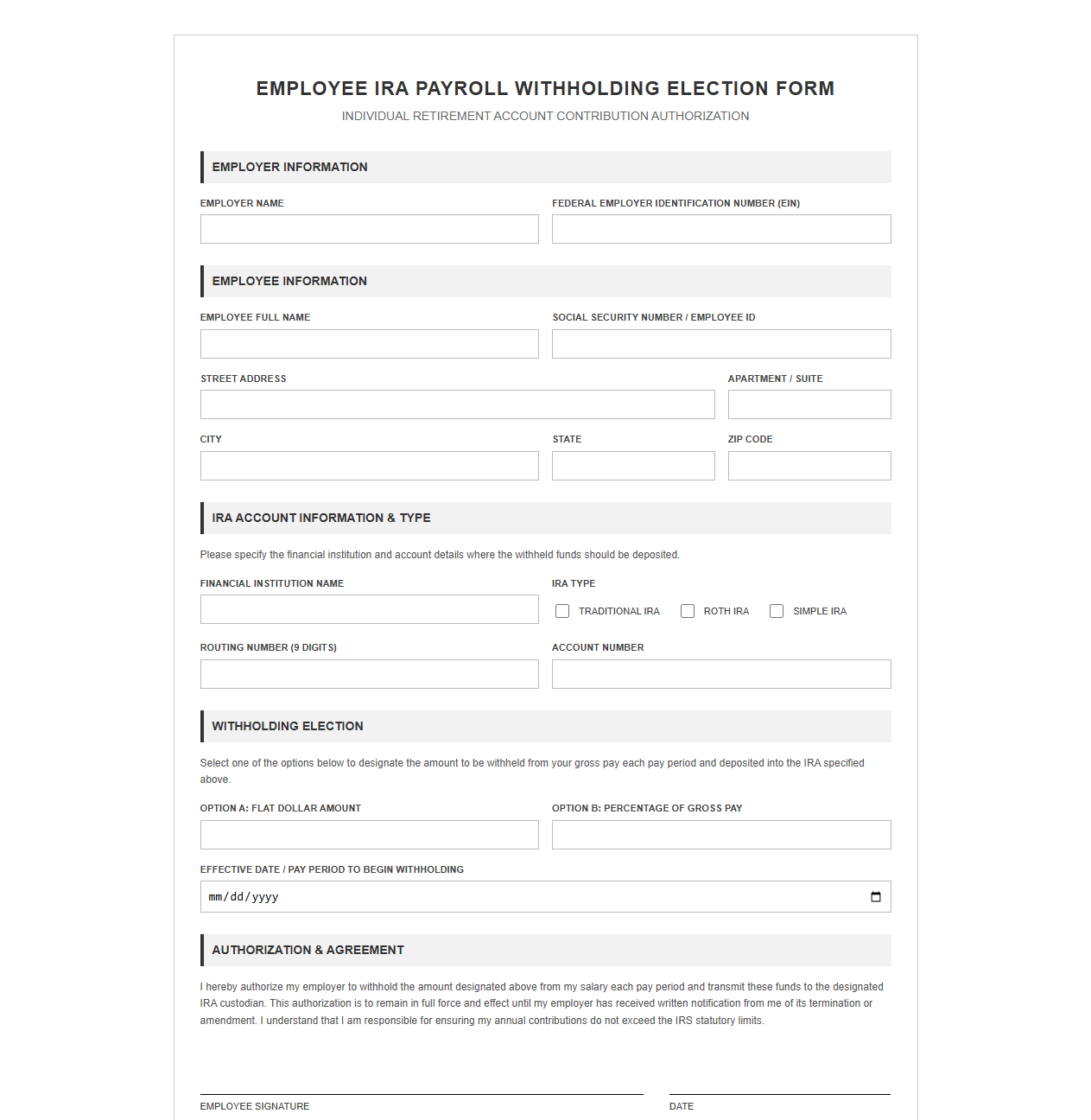

Employee IRA Payroll Withholding Election Form

Download: .PDF

Download: .PDF

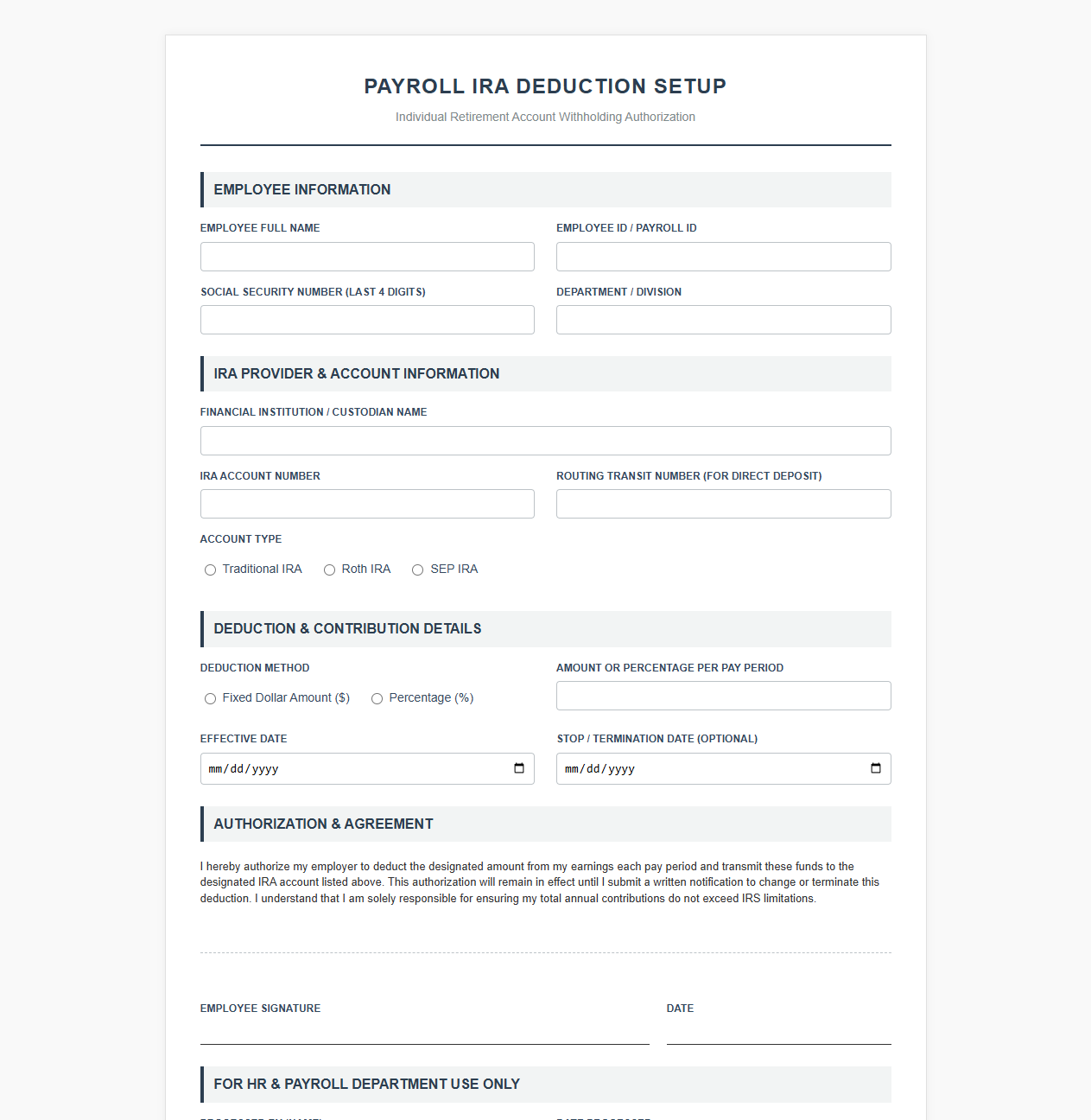

Payroll System IRA Deduction Setup Template

Download: .PDF

Download: .PDF

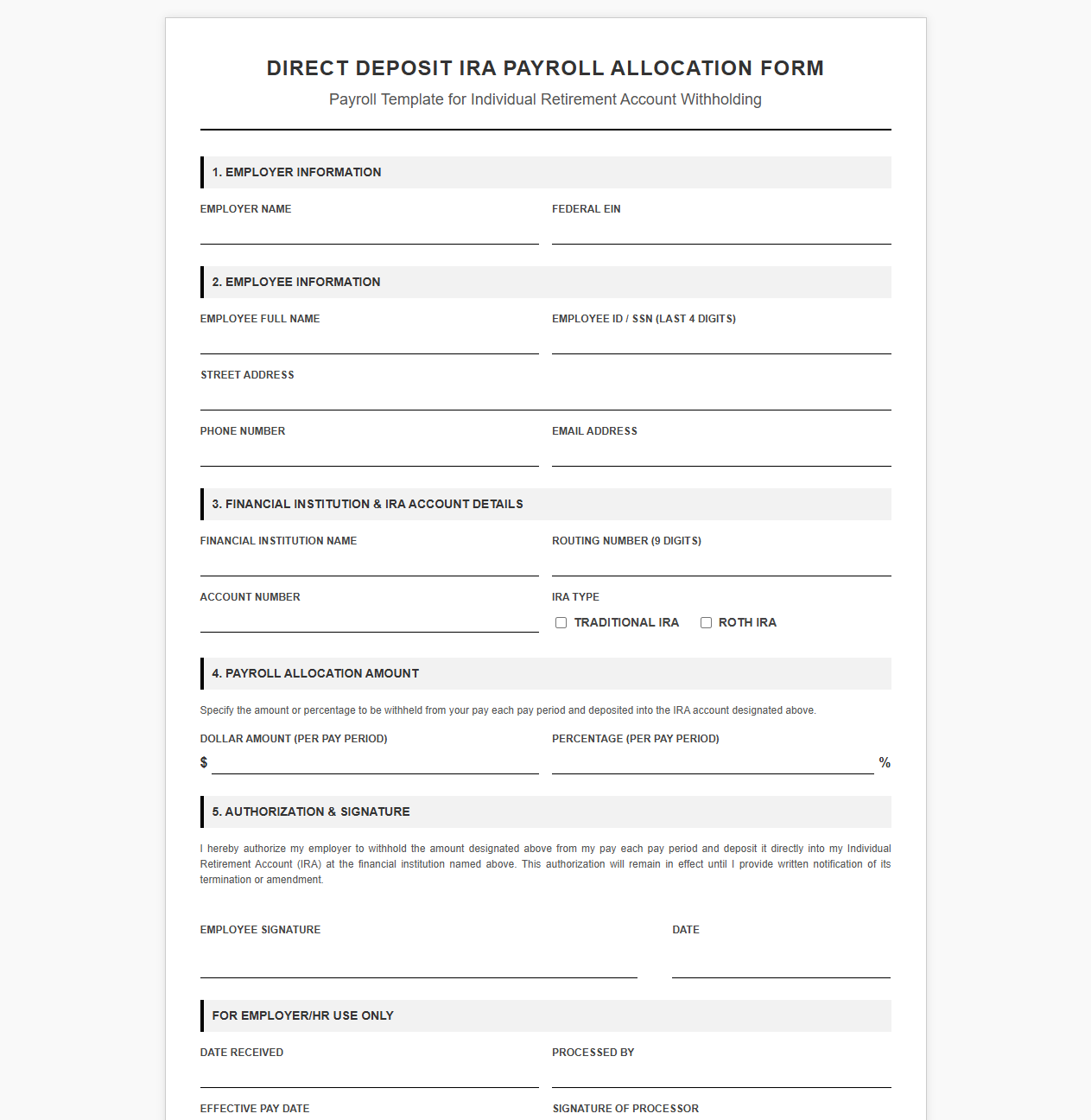

Direct Deposit IRA Payroll Allocation Form

Download: .PDF

Download: .PDF

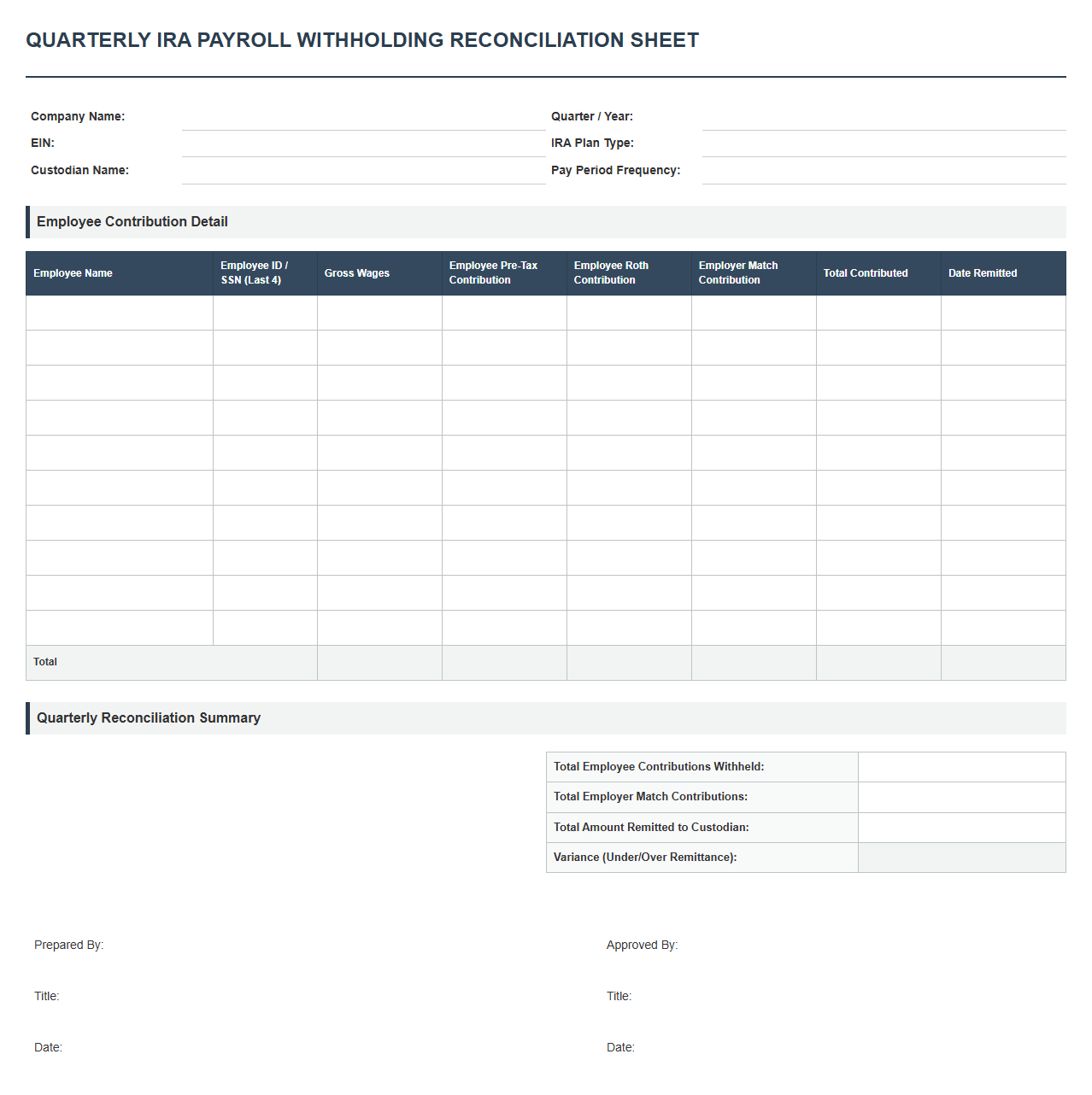

Quarterly IRA Payroll Withholding Reconciliation Sheet

Download: .PDF

Download: .PDF

The High Cost of Manual Payroll Calculations

In the complex landscape of modern business operations, manual data entry remains one of the most volatile liabilities in payroll management. When organizations rely on manual calculations to process retirement deductions, they open the door to compounding mathematical mistakes and administrative oversights. A single misplaced decimal point or misapplied percentage can lead to severe financial penalties and devastating legal repercussions from regulatory bodies like the IRS and the Department of Labor.

Beyond the immediate threat of government fines, these errors directly impact the financial wellness of your workforce. Under-withholding deprives employees of crucial retirement growth, while over-withholding disrupts their immediate cash flow. Trust is difficult to build but incredibly easy to lose; repeated payroll inaccuracies breed employee dissatisfaction and can permanently damage an organization's reputation. Establishing structured, reliable calculations is not just an administrative preference-it is a baseline requirement for corporate survival.

Demystifying IRA Withholding Standards

To establish an accurate deduction system, payroll managers must clearly distinguish between the two primary classifications of Individual Retirement Accounts. Standardizing these designations within your payroll systems prevents catastrophic miscalculations of taxable income.

- Traditional IRA Deductions: These contributions are processed on a pre-tax basis. Subtracting these funds before calculating federal and state income withholding lowers the employee's current taxable income, shifting the tax burden to the retirement phase.

- Roth IRA Deductions: These contributions are processed on a post-tax basis. The payroll system must calculate taxes on the full gross income first, then deduct the Roth contribution from the net pay. This guarantees tax-free withdrawals for the employee during retirement.

Without a standardized template categorization system, payroll administrators risk mixing these tax treatments. Applying post-tax logic to a pre-tax account, or vice versa, triggers incorrect tax reporting, resulting in corrected filings and potential back taxes for both the employer and the employee.

Anatomy of a Compliant Payroll Template

A resilient payroll template relies on structured data architecture to prevent manual calculation errors. By defining specific fields and incorporating rigid validation logic, you can ensure that every subtraction aligns with regulatory expectations.

| Field Name | Data Type | Validation Rule / Formula | Purpose |

|---|---|---|---|

| Gross Pay | Currency | Must be greater than zero | Establishes the base income before any deductions are applied. |

| IRA Type | List Dropdown | Limit choices to Traditional or Roth | Prevents typos and dictates the tax sequencing logic. |

| Contribution Rate | Percentage | Value must be between 0% and 100% | Determines the portion of gross pay earmarked for retirement. |

| Deduction Amount | Formula | Gross Pay multiplied by Contribution Rate | Automates the calculation to eliminate human processing error. |

Step-by-Step Template Integration Guide

Successfully embedding a standardized deduction template into your current HR and accounting systems requires a methodical approach. Follow this progression to transition your workflow safely without disrupting active payroll cycles:

- Export Historical Data: Extract all current employee demographic information and existing retirement selection records from your legacy software database.

- Map the Data Fields: Align the exported data columns precisely with the standardized fields established in your new compliance template.

- Apply Formula Safeguards: Input your automated calculation formulas and lock the calculation cells to prevent accidental manual modifications by payroll staff.

- Run a Parallel Payroll Cycle: Process your next active payroll utilizing both the old system and the new template simultaneously to verify that the mathematical outputs match perfectly.

- Commit to Production: Archive the old manual processes and establish the validated template as the single source of truth for all subsequent pay cycles.

Avoiding the Trap of Over-Contribution

The IRS enforces strict annual caps on retirement contributions, and exceeding these boundaries carries painful financial consequences. When an employee contributes more than the permitted limit, the excess amount is subject to double taxation unless it is identified and corrected before tax-filing deadlines.

"For employees aged 50 and older, catch-up provisions allow for additional contributions beyond standard limits, adding another layer of complexity that payroll systems must dynamically manage to ensure compliance."

Standardized templates mitigate this risk by utilizing integrated logic limits. By applying formulas that reference the employee's year-to-date cumulative contributions, the template can automatically cap deductions the moment the threshold is reached. Relying on automated limits ensures that regulatory compliance is maintained effortlessly, protecting your staff from unexpected tax penalties.

Audit-Proofing Your Retirement Deductions

When state or federal auditors review your payroll registries, they look for consistency, transparency, and a clear paper trail. Standardized templates naturally organize your financial records, making it easy to prove that your processes conform to standard accounting practices.

- Simplified Form W-2 Reporting: Standardized categorization ensures that pre-tax and post-tax contributions are mapped to the correct reporting boxes, such as Box 12, without manual recalculation.

- Instant Year-End Reconciliation: Having uniform columns allows payroll managers to quickly run sum functions to verify that total deducted funds match the totals deposited with the custodian.

- Minimized Human Intervention: Demonstrating to auditors that your formulas are locked and automated reduces the perceived risk profile of your payroll department, shortening audit timelines.

Future-Proofing Payroll with Automation

Standardized templates are an excellent shield against manual errors, but they are only the first phase of modern financial operations. To truly eliminate risk, organizations must begin planning the transition from static worksheets to automated software systems.

Connecting your payroll engine directly to retirement custodians via secure Application Programming Interfaces (APIs) allows for real-time data syncs. This technology ensures that when an employee adjusts their contribution rate on a retirement portal, the change instantly updates your payroll system. Embracing automated integrations streamlines your administrative overhead, protects your organization from compliance risks, and delivers a seamless financial experience for your workforce.

Leave a comment