Payroll professionals frequently grapple with the stressful discovery of Medicare tax withholding errors, a challenge that can quickly disrupt year-end reporting and strain employee relations. Before addressing these miscalculations, however, organizations must first navigate the complex labyrinth of IRS compliance standards and shifting wage thresholds.

Fortunately, utilizing standardized payroll document templates grants finance teams immediate administrative relief, saving valuable time while minimizing audit exposure. While these resources provide a robust foundation, it is important to stipulate that templates require customization to align with your organization's unique payroll systems and state-specific regulations.

Integrating concrete tools-such as a standardized employee correction notice or a Form 941-X reconciliation worksheet-serves as proof of an organized compliance strategy. Below, we examine the essential templates required to resolve withholding discrepancies, detail retroactive adjustment procedures, and outline step-by-step practices to maintain flawless compliance.

Medicare Tax Payroll Deduction Sheet

Download: .PDF

Download: .PDF

Employee Medicare Tax Withholding Calculation Template

Download: .PDF

Download: .PDF

Payroll Ledger with Medicare and Additional Medicare Tax

Download: .PDF

Download: .PDF

Medicare Tax Withholding Payroll Worksheet

Download: .PDF

Download: .PDF

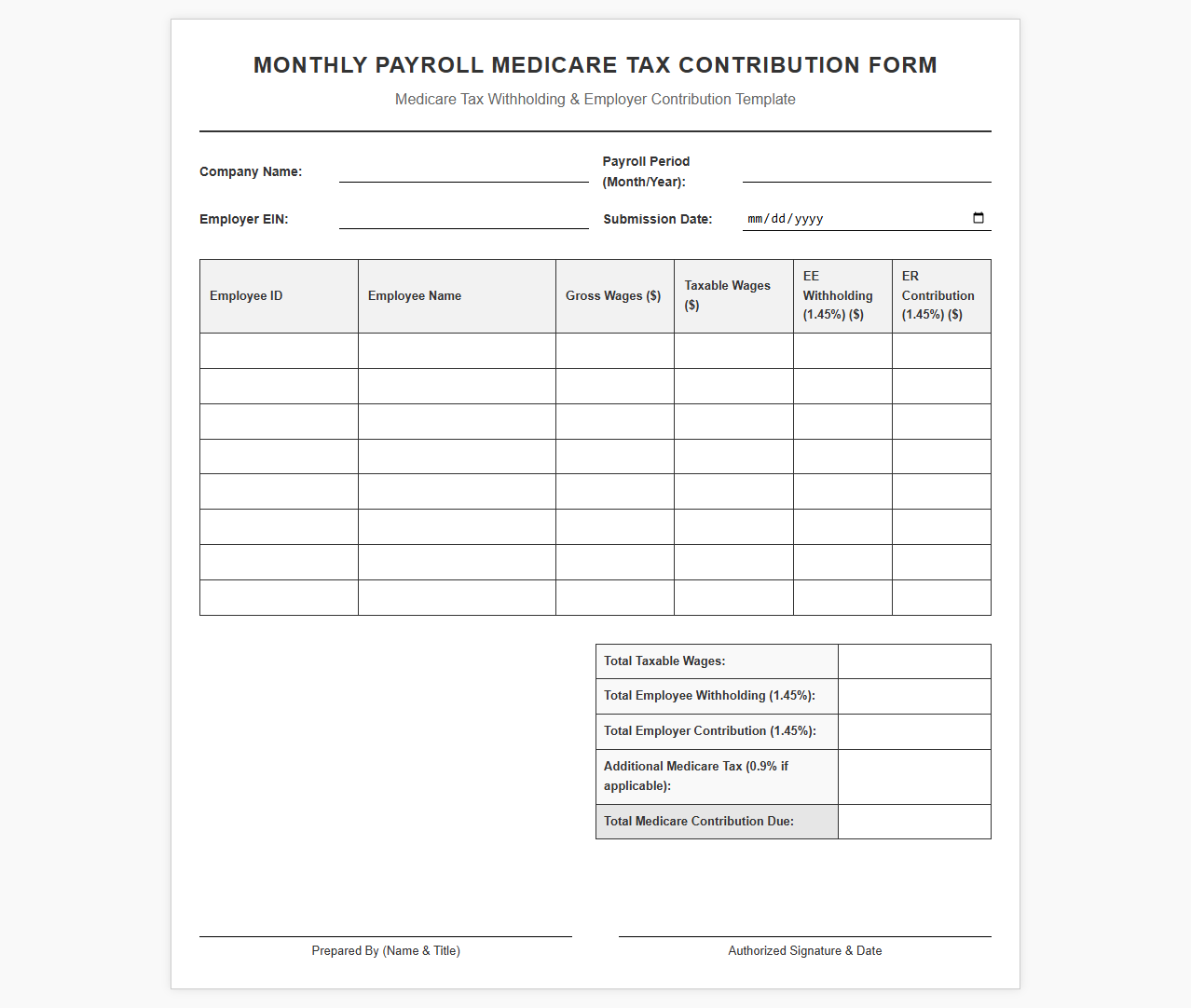

Monthly Payroll Medicare Tax Contribution Form

Download: .PDF

Download: .PDF

Employer Medicare Tax Withholding Tracker

![]() Download: .PDF

Download: .PDF

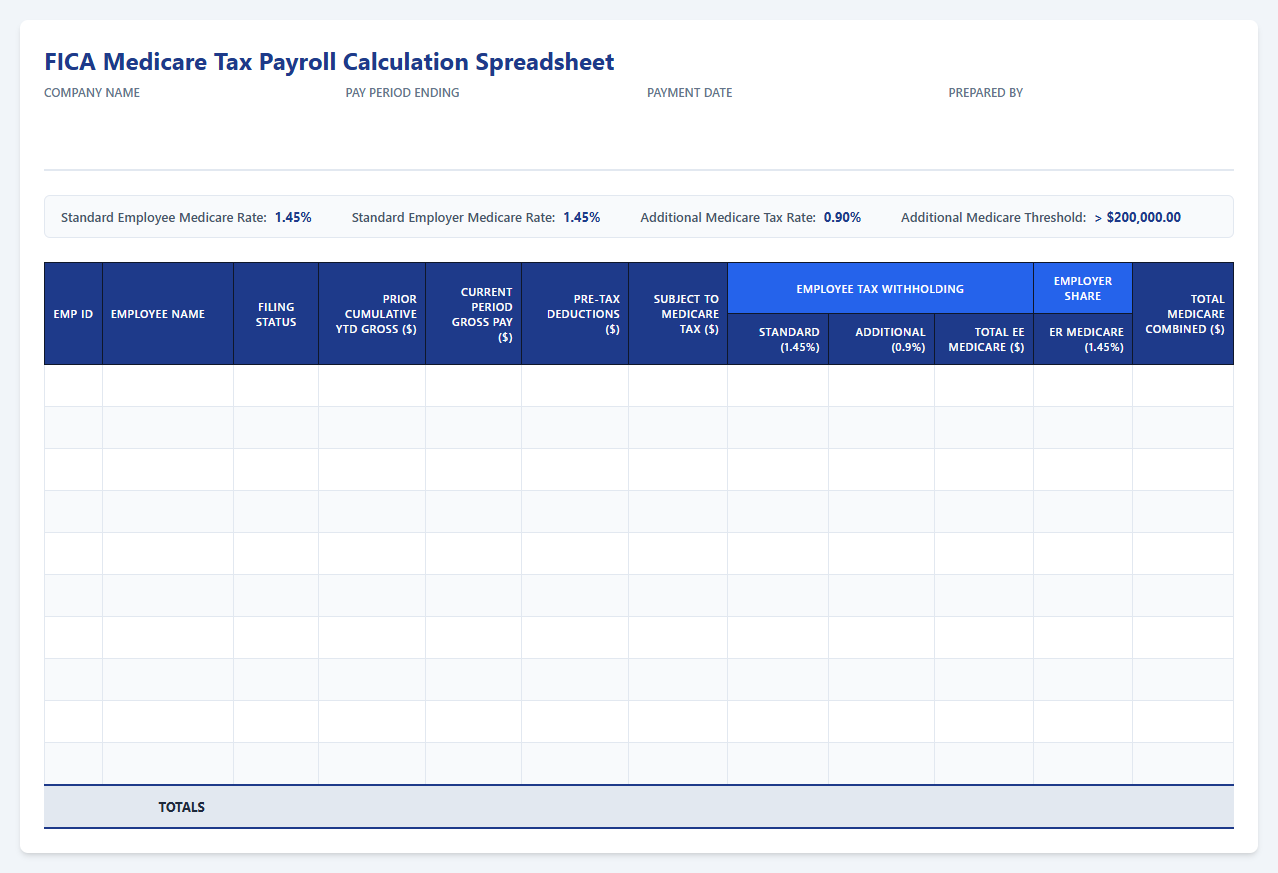

FICA Medicare Tax Payroll Calculation Spreadsheet

Download: .PDF

Download: .PDF

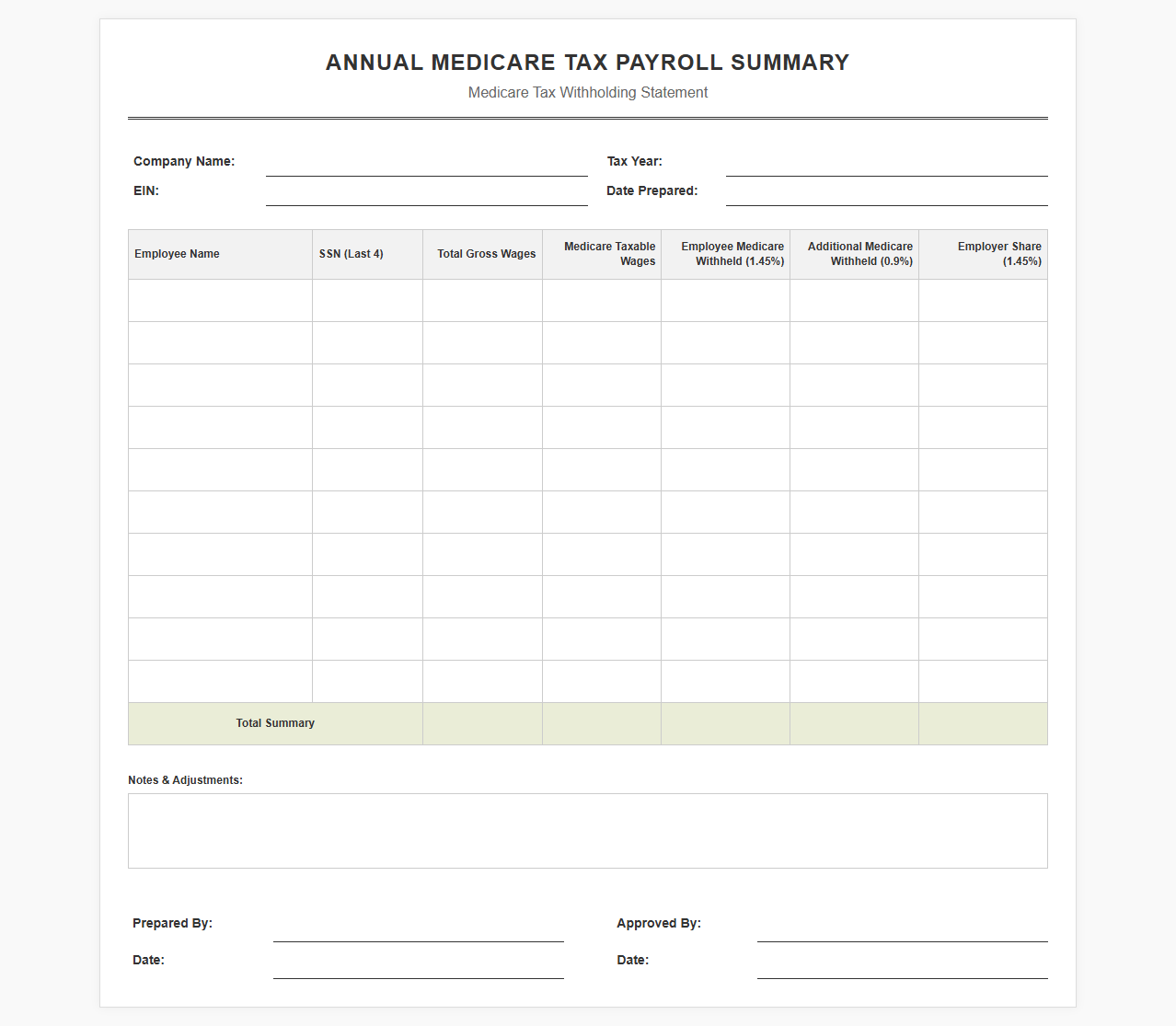

Annual Medicare Tax Payroll Summary Template

Download: .PDF

Download: .PDF

Understanding the Impact of Medicare Tax Withholding Errors

Medicare tax withholding errors are a common yet challenging issue in payroll administration. These discrepancies typically happen because of misconfigured payroll software, failing to track mid-year compensation changes, or overlooking the precise moment an employee crosses the threshold for the Additional Medicare Tax. Because employers are legally required to withhold these taxes accurately, any deviation can quickly lead to systemic payroll errors.

The financial and legal risks of non-compliance are significant. Failing to withhold the correct amount of Medicare tax can trigger IRS audits, substantial penalties, and back-tax interest charges. Additionally, trying to retroactively collect under-withheld funds from employees creates friction and administrative burdens. Standardizing payroll correction templates helps HR teams and payroll administrators resolve issues quickly, reduce manual error rates, and maintain a clear, audit-ready compliance trail.

Identifying Common Medicare Tax Discrepancies

To keep payroll accurate, teams must regularly compare actual withholdings against expected tax liabilities. Discrepancies usually fall into two categories: under-withholding (often caused by failing to apply the extra 0.9% tax once an employee exceeds the $200,000 threshold) and over-withholding. The table below outlines how to detect these issues and the corrective paths required for each scenario.

| Discrepancy Type | Primary Cause | Detection Method | Required Action |

|---|---|---|---|

| Under-Withholding (Standard) | Incorrect wage calculations or misclassified employee status. | Reconcile total Year-to-Date (YTD) wages against 1.45% baseline withholding. | Adjust subsequent payrolls within the same calendar year or file Form 941-X. |

| Additional Medicare Under-Withholding | Failure to trigger the 0.9% rate once YTD wages exceed $200,000. | Identify employees with compensation over $200,000 and verify the extra 0.9% split. | Correct the rate in the system and collect the difference from the employee before year-end. |

| Over-Withholding | System configuration errors or processing deductions twice. | Cross-reference total tax deposits with quarterly Form 941 summaries. | Refund the over-withheld amount to the employee and claim a credit via Form 941-X. |

Template 1: The IRS Form 941-X Error Correction Worksheet

When adjustments span previous quarters, payroll departments must use IRS Form 941-X (Adjusted Employer's Quarterly Federal Tax Return or Claim for Refund). This step-by-step template guides you through calculations specifically for Medicare tax adjustments.

- Identify the calendar quarter where the error occurred and secure the original Form 941 filed for that period.

- Calculate the corrected taxable Medicare wages. For standard wages, multiply by

0.029(representing the combined employer and employee share of 1.45% each). - Navigate to

Line 12of Form 941-X to report adjustments for taxable Medicare wages. Enter the corrected amount, the originally reported amount, and the calculated difference in the corresponding columns. - If the error involves the Additional Medicare Tax, use

Line 13. Calculate the correction using only the employee rate of0.009for wages exceeding $200,000. - Combine the differences from

Line 12andLine 13to determine your total tax adjustment, and proceed to complete Part 4 to detail how the error was discovered.

Template 2: Employee Notification Letter for Withholding Adjustments

When correcting a payroll tax error, clear communication helps maintain employee trust. Use the customizable template below to explain the adjustments made to their paycheck.

Subject: Important Notification Regarding Your Payroll Tax Withholding Dear [Employee Name], During a routine internal audit of our payroll records, we identified a discrepancy in the federal Medicare tax withheld from your compensation during the pay period(s) ending [Date Range]. To ensure full compliance with IRS guidelines, we are required to make a corrective adjustment on your upcoming paycheck dated [Adjustment Pay Date]. Here is a summary of the adjustment: - Originally Withheld: $[Original Amount] - Correct Withholding: $[Correct Amount] - Adjustment Amount: $[Adjustment Amount] (This amount will be deducted/refunded) Please note that this adjustment does not change your overall gross earnings; it simply ensures that your tax contributions are accurately reported to the IRS. If you have any questions or require additional details regarding this correction, please contact the payroll department at [Phone Number/Email]. Sincerely, [Payroll Department / HR Manager Name] [Company Name]

Template 3: Internal Payroll Audit and Correction Log

Maintaining an internal ledger of corrections ensures your organization is prepared for any external audits. This structured format helps track the lifecycle of every payroll correction.

- Log Identifier: A unique tracking number for each incident (e.g., MED-TAX-2023-01).

- Employee Demographics: Full name, employee ID, and department.

- Affected Quarter: The tax year and exact quarter where the withholding error occurred.

- Error Type: Clearly mark if the error was Under-Withholding, Over-Withholding, or Additional Medicare Tax.

- Financial Impact: Gross wages affected, tax amount owed, and tax amount actually withheld.

- Resolution Steps: Dates of employee notification, date Form 941-X was filed, and payroll batch correction numbers.

Best Practices for Preventing Future Medicare Tax Errors

A reactive approach to payroll compliance is costly and time-consuming. Implementing systemic checks is the most reliable way to avoid recurring Medicare tax discrepancies.

- Schedule mid-year payroll audits in June and September to catch and resolve minor errors before the year-end closing process.

- Configure automated alerts in your payroll system to trigger when an employee's cumulative year-to-date earnings reach $180,000, allowing you to double-check their Additional Medicare Tax setup.

- Validate software updates regularly, especially ahead of the first payroll cycle of a new tax year, to confirm that all federal rates and caps match updated IRS regulations.

- Cross-train payroll administrators on the differences between standard FICA tax limits and Additional Medicare Tax thresholds to reduce manual processing errors.

Final Checklist for Compliant Payroll Resolution

Before submitting any adjustment forms or adjusting employee checks, use this final checklist to confirm your correction meets all federal standards.

- Verify the exact quarter and tax year where the discrepancy occurred.

- Confirm if the error involves the standard 1.45% rate, the 0.9% Additional Medicare rate, or both.

- Notify the affected employees in writing before any deductions or credits hit their accounts.

- Double-check all math on Form 941-X worksheets before submission.

- Archive copies of the notification letters, calculation sheets, and filed tax forms in your secure internal compliance folder.

Leave a comment