Navigating the bureaucratic complexities of real estate philanthropy can be a daunting endeavor for both generous donors and non-profit organizations. A single administrative oversight in the documentation process can jeopardize substantial tax benefits or indefinitely delay the property transfer. Before drafting any agreement, it is crucial to recognize that regulatory bodies scrutinize these high-value transactions with extreme rigor, demanding precise alignment with tax codes and property laws.

Utilizing standardized receipt templates grants both parties the legal safeguards and administrative clarity necessary to secure maximum tax deductions and ensure compliance. However, these tools require careful calibration; they must align with strict statutory stipulations, such as mandatory IRS appraisal rules for parcels valued over $5,000. For instance, integrating specific clauses detailing "contemporaneous written acknowledgment" and explicit declarations regarding whether goods or services were exchanged serves as concrete proof of a legally sound transaction.

Below, we will outline the indispensable components of compliant land donation receipts, provide customizable templates, and guide you through the best practices for executing seamless property transfers.

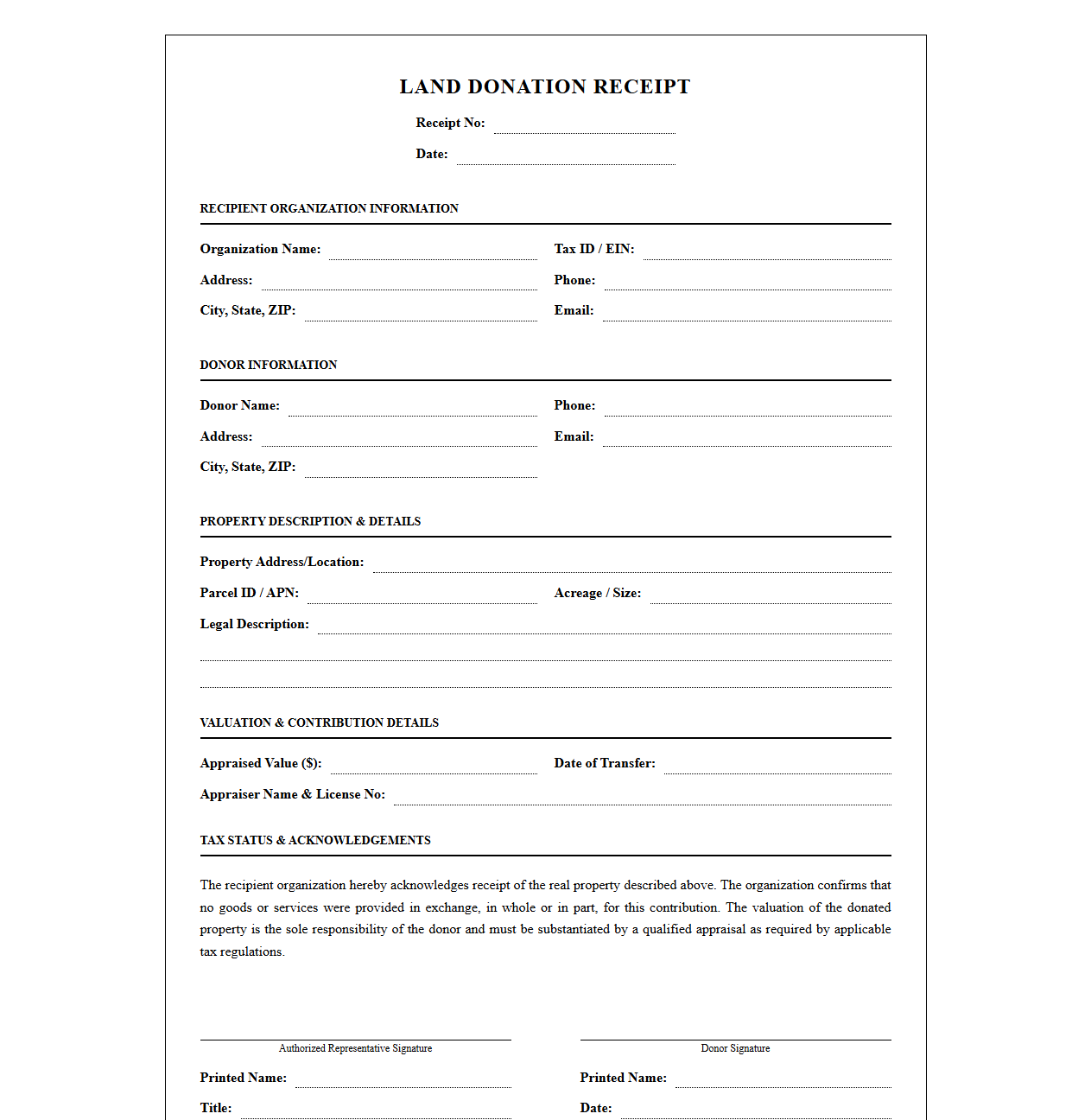

Land Donation Receipt Template

Download: .PDF

Download: .PDF

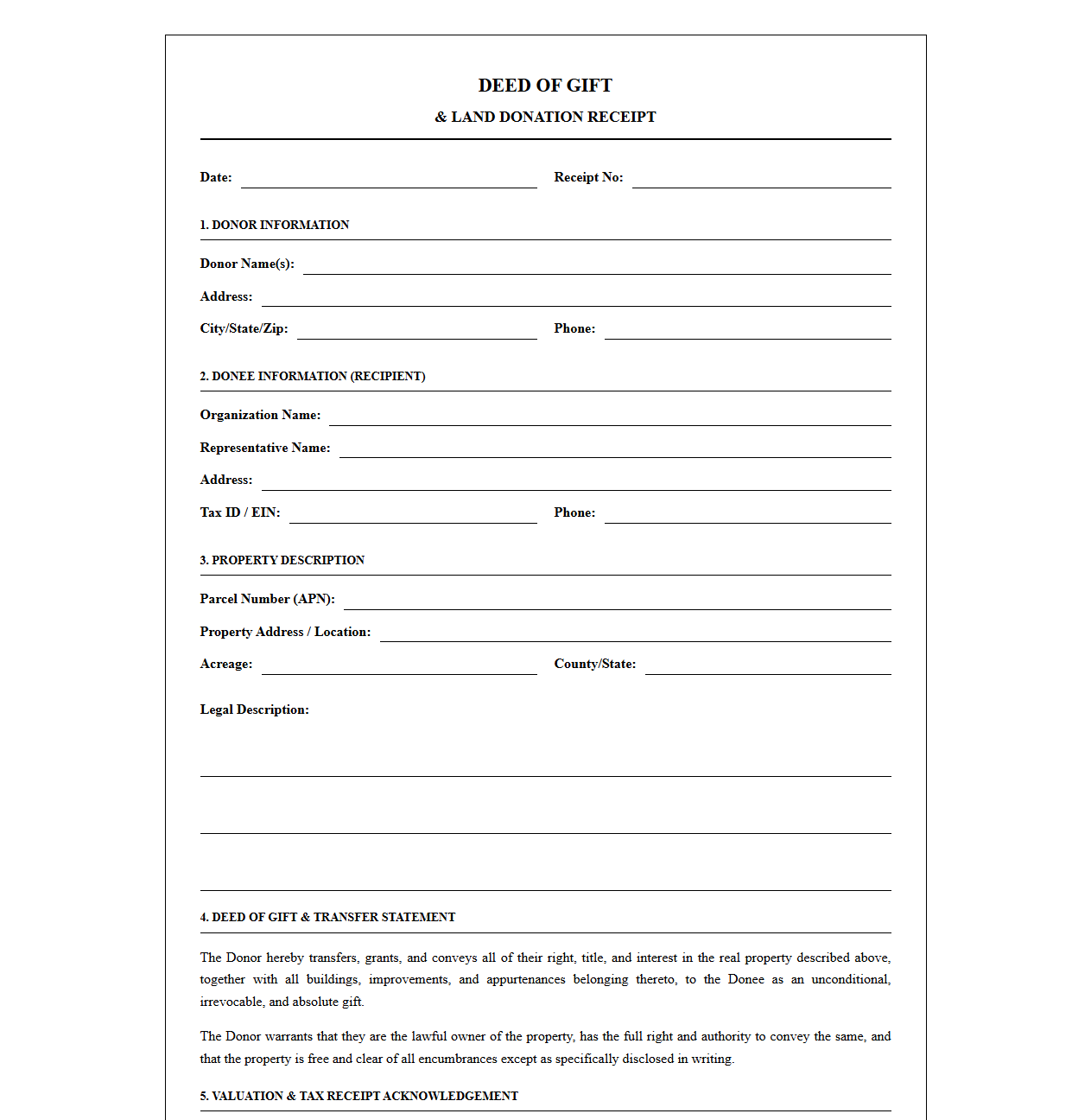

Deed of Gift and Land Donation Receipt

Download: .PDF

Download: .PDF

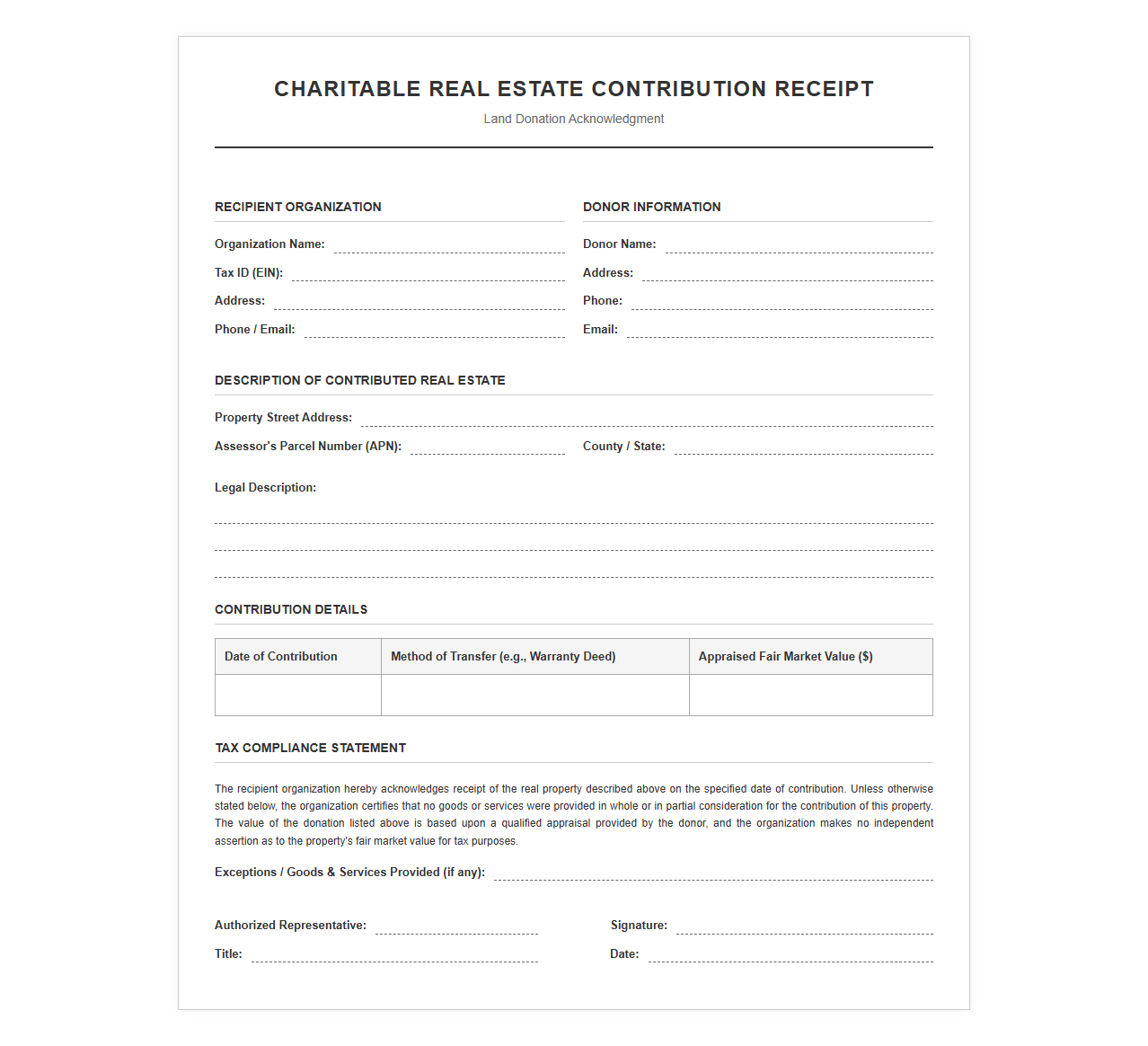

Charitable Real Estate Contribution Receipt

Download: .PDF

Download: .PDF

Nonprofit Land Donation Acknowledgement Template

Download: .PDF

Download: .PDF

Real Property Donation Tax Receipt Template

Download: .PDF

Download: .PDF

Conservation Easement and Land Donation Receipt

Download: .PDF

Download: .PDF

Land Parcel Donation Receipt Form

Download: .PDF

Download: .PDF

Plot of Land Donation Acknowledgement Letter

Download: .PDF

Download: .PDF

Understanding the Legal Framework of Land Donations

Donating real estate to a charitable organization is a powerful philanthropic gesture, but it requires navigating a complex legal landscape. Unlike cash contributions, real property transfers involve significant legal shifts in ownership, potential environmental liabilities, and rigorous tax implications. Failing to adhere to strict regulatory standards can result in the loss of tax benefits for the donor and administrative burdens for the recipient organization.

To ensure the transaction is recognized by tax authorities and legally binding under property law, both parties must commit to strict regulatory compliance, execute proper legal documentation, and obtain a contemporaneous written acknowledgment. Without these foundational elements, the donation may fail to qualify for deduction purposes, leaving both the donor and the non-profit vulnerable to audits and legal disputes.

Essential Tax and Legal Compliance Requirements

The Internal Revenue Service (IRS) and state tax authorities maintain strict rules regarding the deduction of non-cash charitable contributions. For high-value assets like real estate, the burden of proof rests on the taxpayer to demonstrate the validity of the transfer and the accuracy of the property's valuation.

- IRS Form 8283: Donors must file Section B of Form 8283 for non-cash contributions exceeding $5,000, which requires the signature of an authorized official from the receiving charity.

- Qualified Appraisal: For land donations valued over $5,000, a certified appraisal must be completed by a qualified appraiser no earlier than 60 days before the donation date and no later than the tax filing deadline.

- The $500,000 Threshold: For real property donations exceeding $500,000, the donor must attach the full qualified appraisal report to their federal tax return.

- Contemporaneous Written Acknowledgment: The donor must obtain a formal receipt from the charity on or before the earlier of the date the return is filed or the due date of the return.

Core Components of a Land Donation Receipt

A legally compliant land donation receipt is more than a simple thank-you letter; it must contain specific legal declarations to satisfy tax auditing standards.

- Donor Information

- The full legal name, mailing address, and contact details of the individual or entity transferring the property.

- Donee Information

- The legal name of the charitable organization, its Employer Identification Number (EIN), and a statement confirming its active 501(c)(3) status.

- Property Description

- A detailed physical address and the official legal description of the real estate, typically matching the legal language found on the recorded deed.

- Date of Transfer

- The exact calendar date on which the ownership deed was legally transferred to and accepted by the charitable organization.

- Goods and Services Statement

- A mandatory declaration indicating whether the charity provided any goods or services in exchange for the donation, or if the contribution was made entirely as an unconditional gift.

Standard Land Donation Receipt Template

Below is a standard template designed for clean, unconditional land donations. This template is suitable for straightforward transactions where the donor receives no goods, services, or special conditions in exchange for the property.

LAND DONATION ACKNOWLEDGMENT RECEIPT

Date of Receipt: [Date]

Organization Name: [Charity Name]

EIN: [XX-XXXXXXX]

Organization Address: [Street Address, City, State, Zip]

Donor Name: [Donor Full Name]

Donor Address: [Street Address, City, State, Zip]

PROPERTY DESCRIPTION:

The property transferred is located at [Street Address, City, State, Zip] and is legally described as:

[Insert Full Legal Description / Parcel ID Number from the Deed]

DATE OF TRANSFER:

The legal ownership of the property was officially transferred to [Charity Name] on [Date of Deed Recording/Execution].

GOODS AND SERVICES DECLARATION:

[Charity Name] hereby acknowledges receipt of the real property described above.

- No goods or services were provided in exchange for this contribution.

- The contribution was made entirely as an unconditional gift.

Authorized Signature: _____________________________________

Printed Name: [Name of Authorized Representative]

Title: [Title, e.g., Executive Director]

Organization: [Charity Name]Restricted and Conditional Land Donation Receipt Template

When land is donated under specific terms-such as conservation easements, historical preservation restrictions, or municipal zoning covenants-the receipt must explicitly reference these binding conditions.

RESTRICTED LAND DONATION ACKNOWLEDGMENT RECEIPT

Date of Receipt: [Date]

Organization Name: [Charity Name]

EIN: [XX-XXXXXXX]

Organization Address: [Street Address, City, State, Zip]

Donor Name: [Donor Full Name]

Donor Address: [Street Address, City, State, Zip]

PROPERTY DESCRIPTION AND RESTRICTIONS:

The property transferred is located at [Street Address, City, State, Zip] and is legally described as:

[Insert Full Legal Description / Parcel ID Number]

This property is accepted subject to the following covenants, easements, or restrictions:

[Detail specific restrictions, e.g., "The property is subject to a permanent conservation easement restricting commercial development, as recorded in Deed Book XXX, Page YYY."]

DATE OF TRANSFER:

The legal ownership of the property was transferred to [Charity Name] on [Date of Deed Recording/Execution].

GOODS AND SERVICES DECLARATION:

[Charity Name] acknowledges receipt of the real property described above. The sole consideration provided by the organization was the commitment to maintain the property according to the restricted covenants outlined in the transfer agreement. No other goods or services were provided in exchange for this contribution.

Authorized Signature: _____________________________________

Printed Name: [Name of Authorized Representative]

Title: [Title, e.g., President / Trustees Chair]

Organization: [Charity Name]Avoiding Common Pitfalls in Property Valuations

Even minor errors in the timing of valuations or documentation signatures can disqualify a donor's tax deduction. One of the most common issues is a valuation mismatch, where the donor uses an outdated appraisal or assesses the property value based on speculative future developments rather than its current market value.

Critical Warning: The IRS strictly rejects appraisals dated more than 60 days before the physical contribution of the property. Additionally, obtaining an appraisal after filing the tax return is an automatic ground for deduction disallowance.

Another major pitfall is the failure of the charity to sign Form 8283 properly, or executing the donation receipt prior to the formal recording of the deed. Ownership does not transfer when the donor decides to give; it transfers when the deed is legally delivered and accepted under local state laws.

Best Practices for Document Retention and Execution

Securing tax benefits and ensuring a clean legal title requires structured execution and careful record-keeping practices by both the donor and the charity.

- Execute Deed Recording First: Ensure the warranty deed or quitclaim deed is officially recorded with the county recorder of deeds before executing the formal receipt.

- Notarize Every Key Document: Have all signatures on deeds, transfer declarations, and restricted covenants notarized to prevent future challenges to validity.

- Link Documents Internally: Cross-reference the recorded deed number directly within the donation receipt to create a clean audit trail.

- Retain Records Indefinitely: Keep copies of the recorded deed, qualified appraisal, Form 8283, and the signed receipt for at least seven years, though permanent storage is recommended for real estate transactions.

Leave a comment