Corporate tax departments are currently grappling with the immense operational burden of the Corporate Alternative Minimum Tax (CAMT). Navigating these multi-layered regulations often leads to fragmented accounting data and heightened audit risks. Before investing in costly, enterprise-wide software overhauls, organizations must first establish a logical data bridge that aligns GAAP financial statements with complex tax reporting requirements. Utilizing specialized return templates grants tax teams an immediate advantage, transforming chaotic data-gathering into structured, repeatable processes that recover hundreds of planning hours.

While these templates serve as powerful structural frameworks rather than a substitute for professional tax judgment, they provide the precise guardrails needed to manage complex calculations. Specifically, they streamline the tracking of Adjusted Financial Statement Income (AFSI) modifications and intricate tax credit allocations. In this article, we will examine how implementing these specialized templates mitigates compliance risk, optimizes resource allocation, and ensures reporting accuracy.

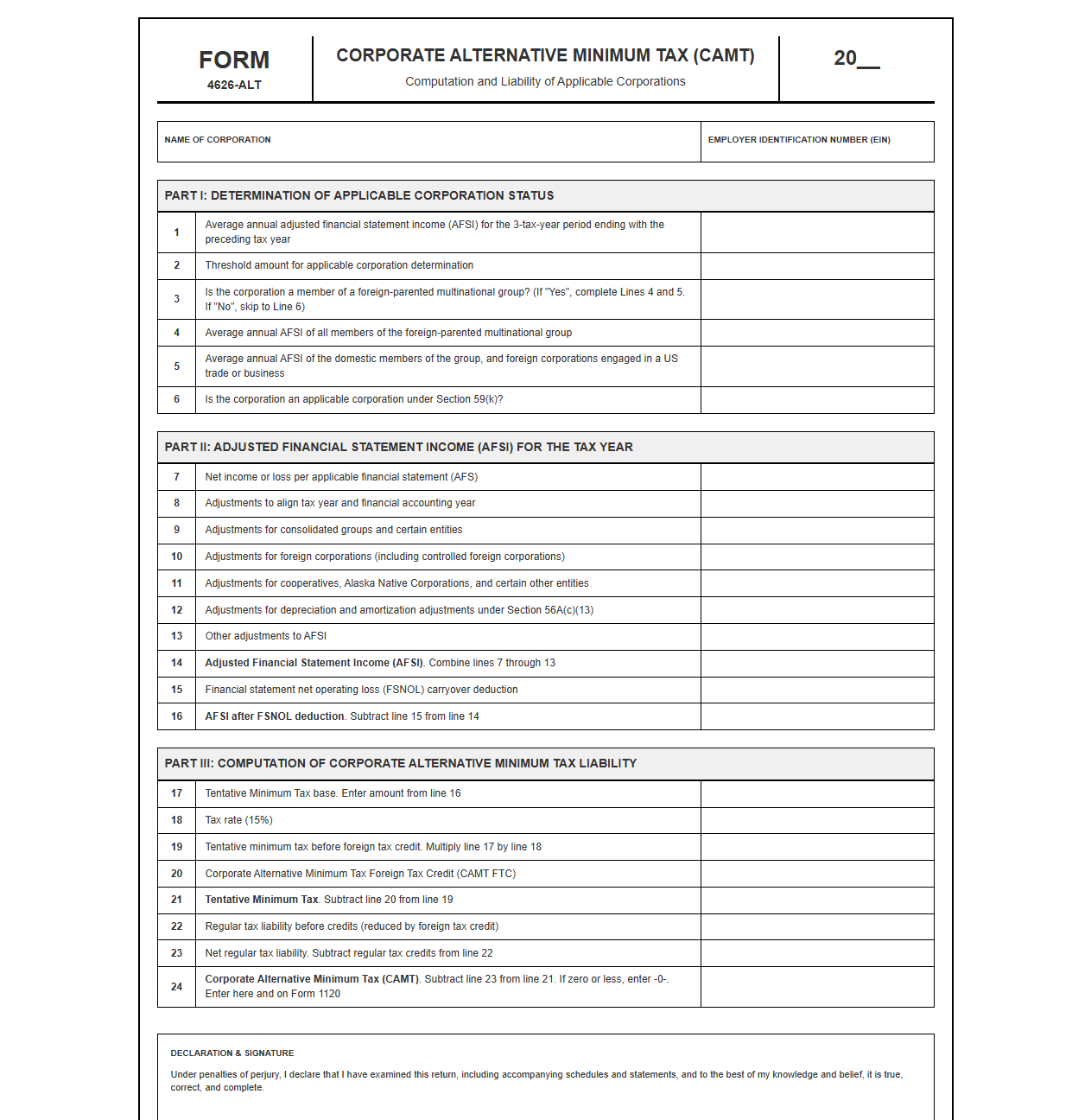

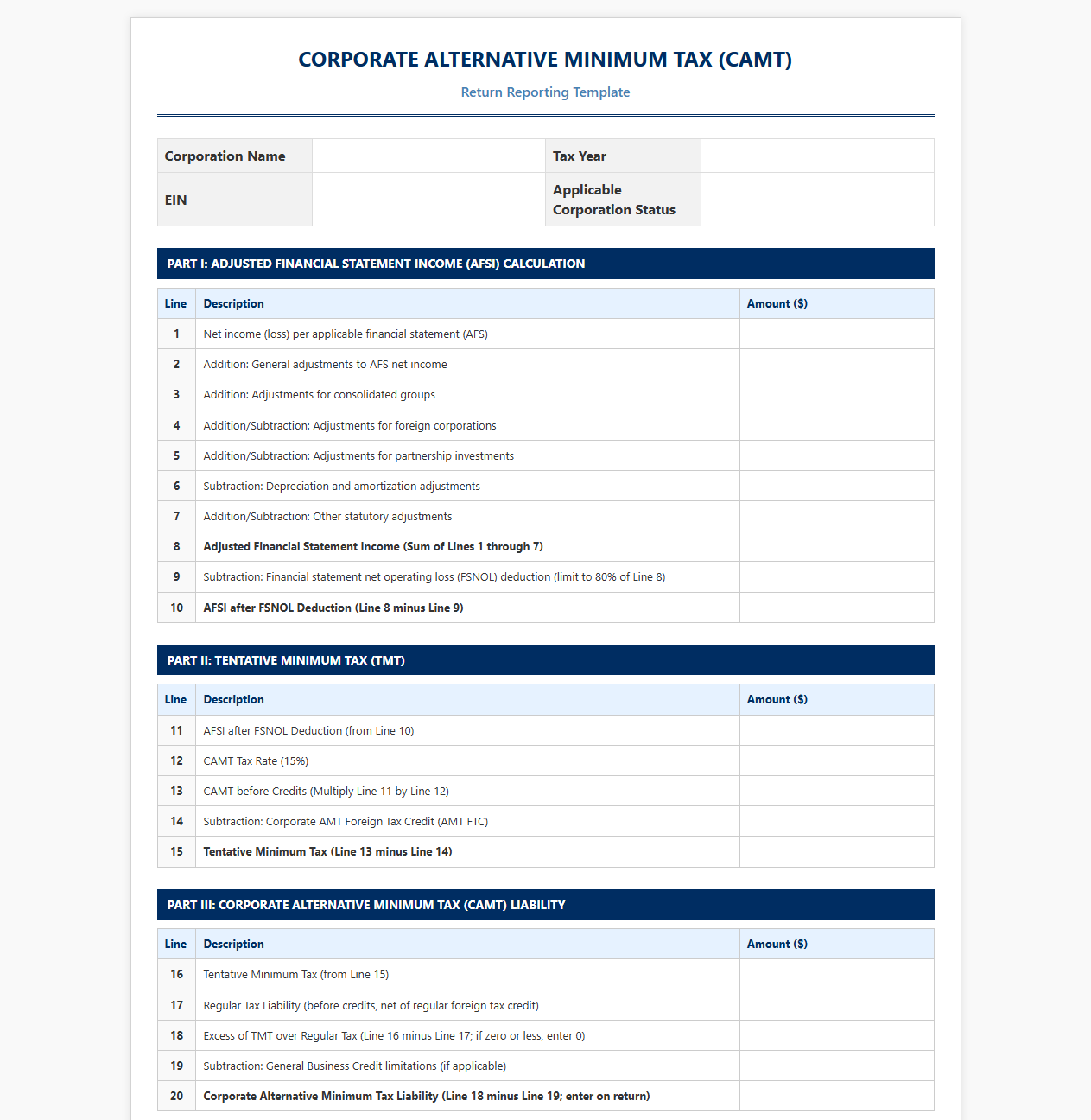

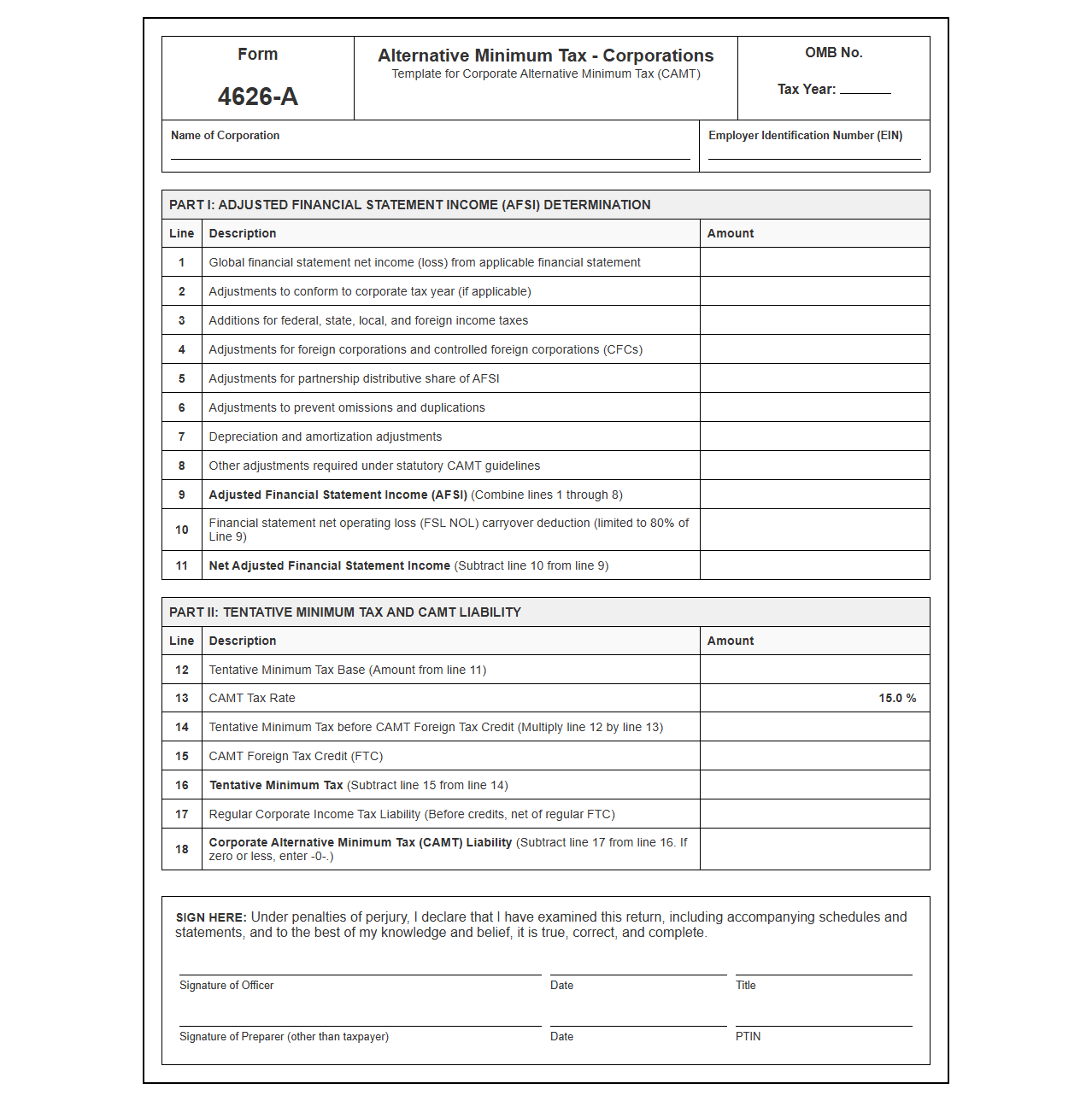

Corporate Alternative Minimum Tax Return Template

Download: .PDF

Download: .PDF

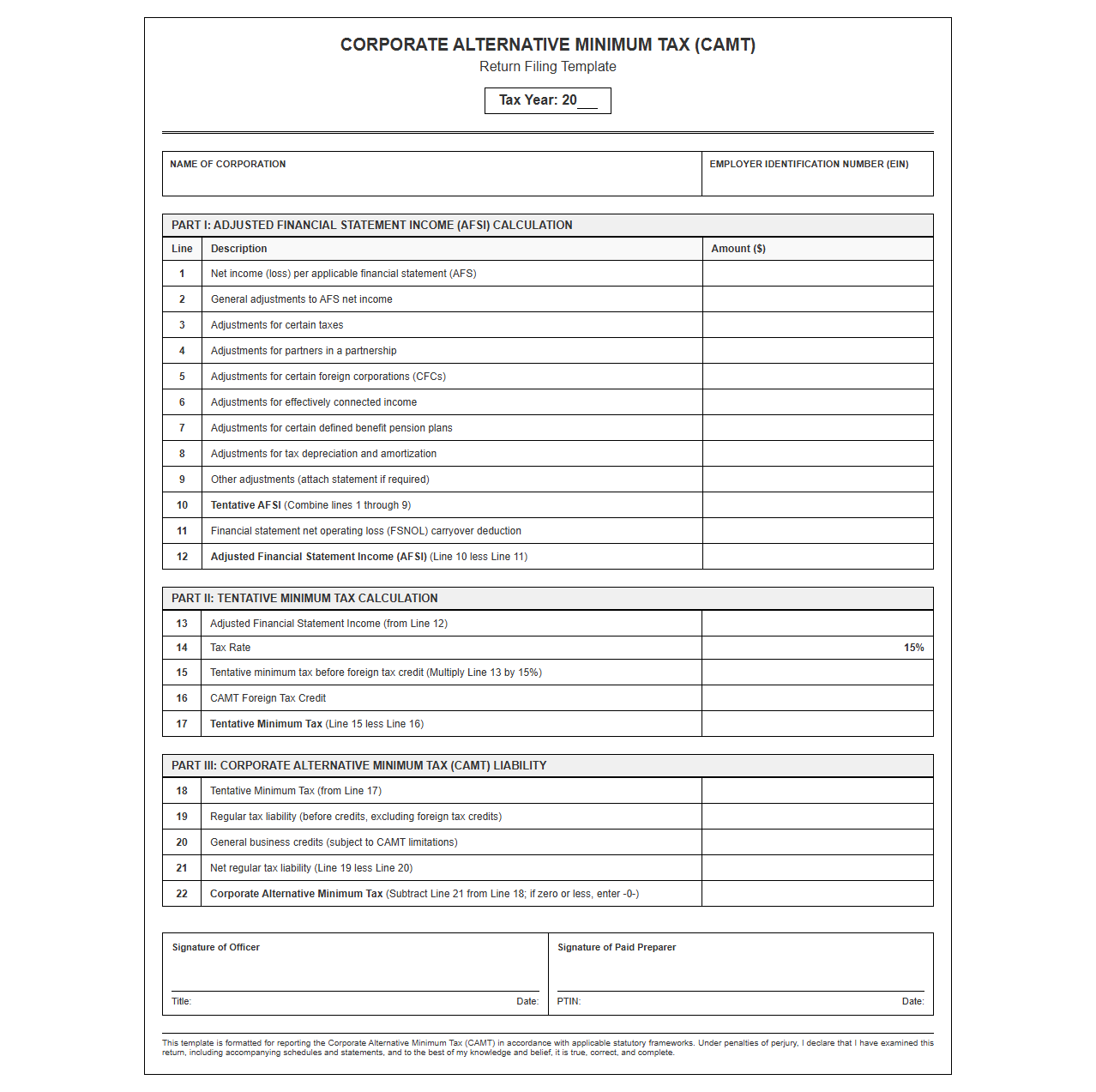

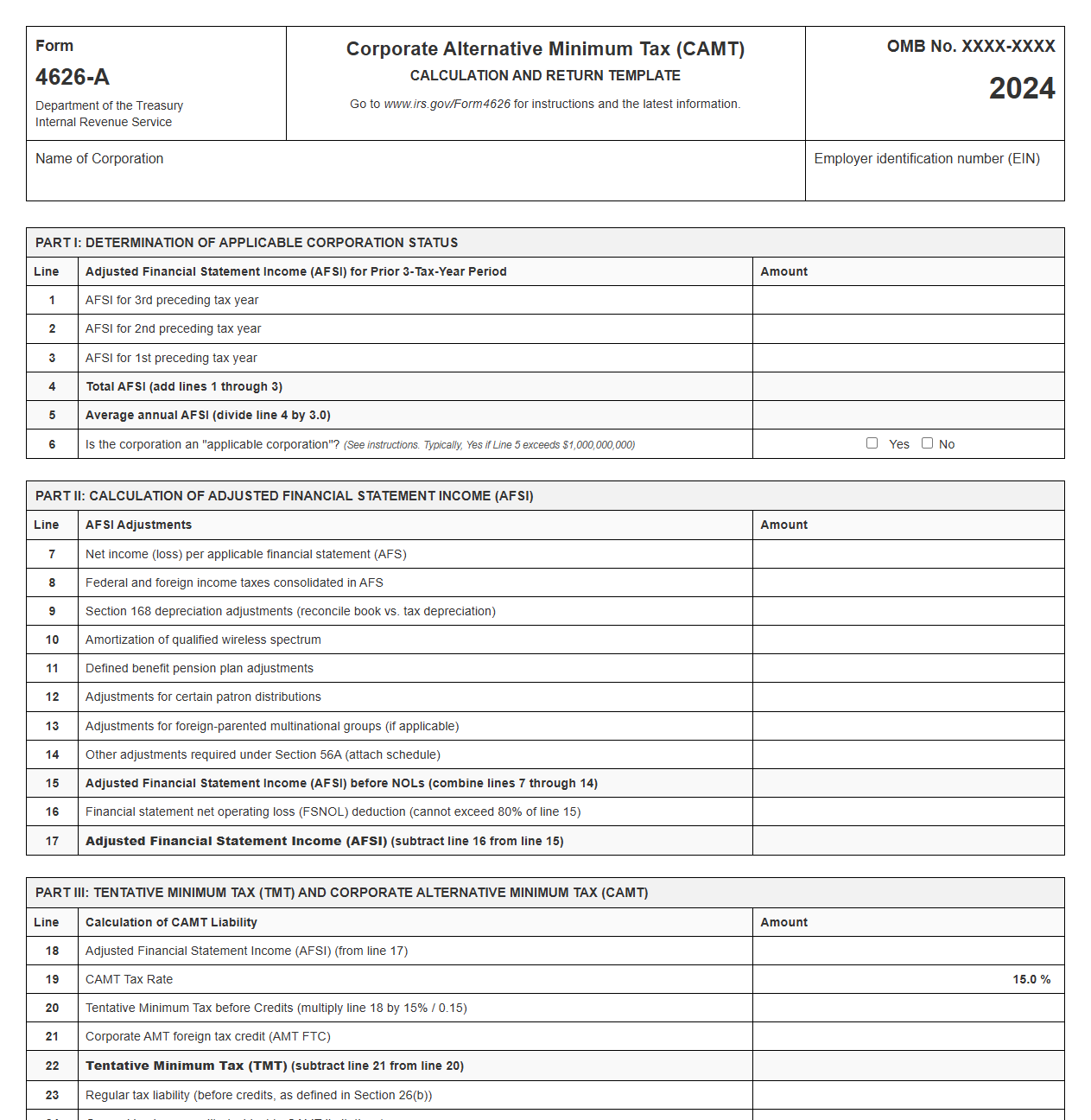

CAMT Return Filing Template

Download: .PDF

Download: .PDF

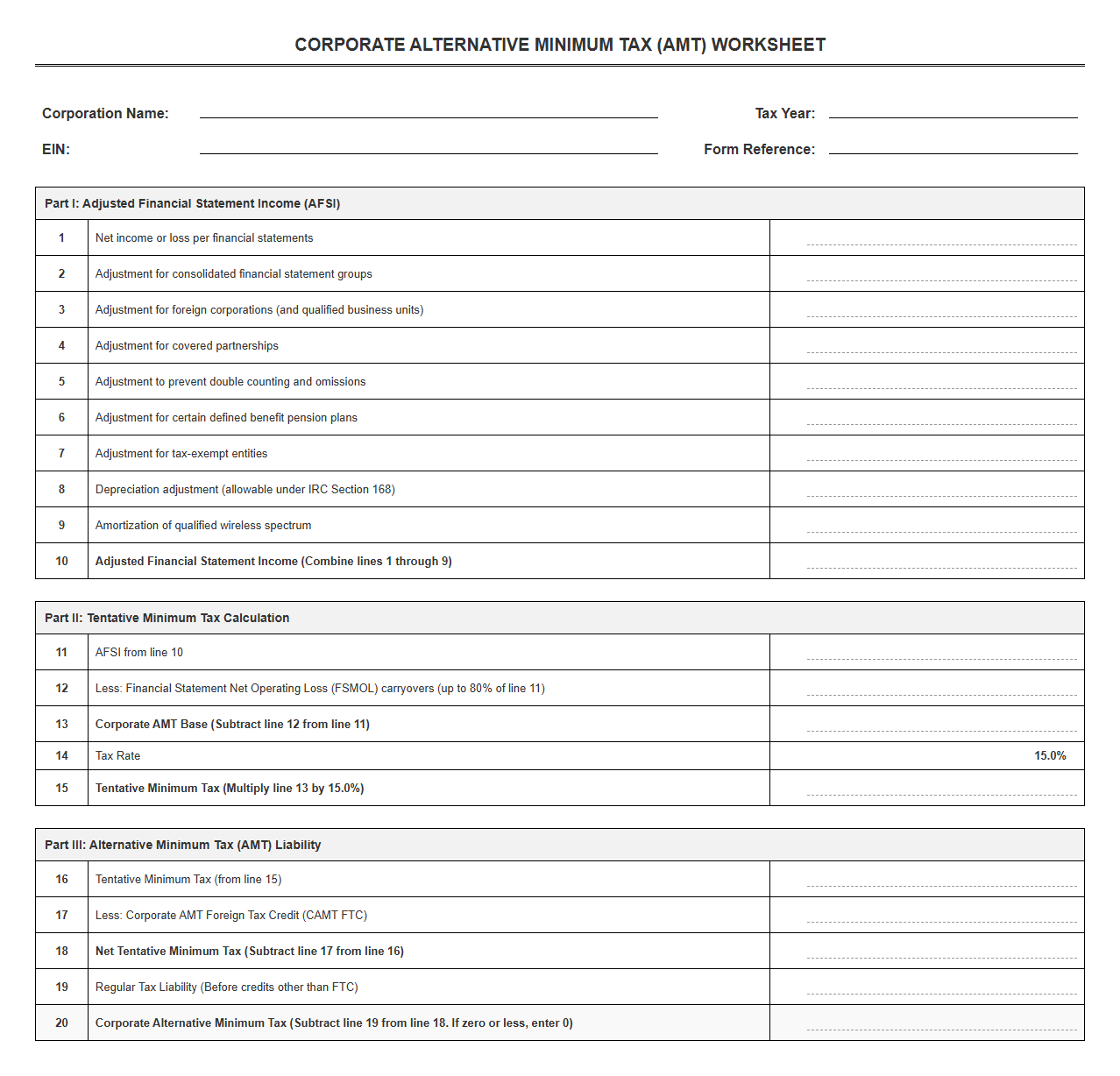

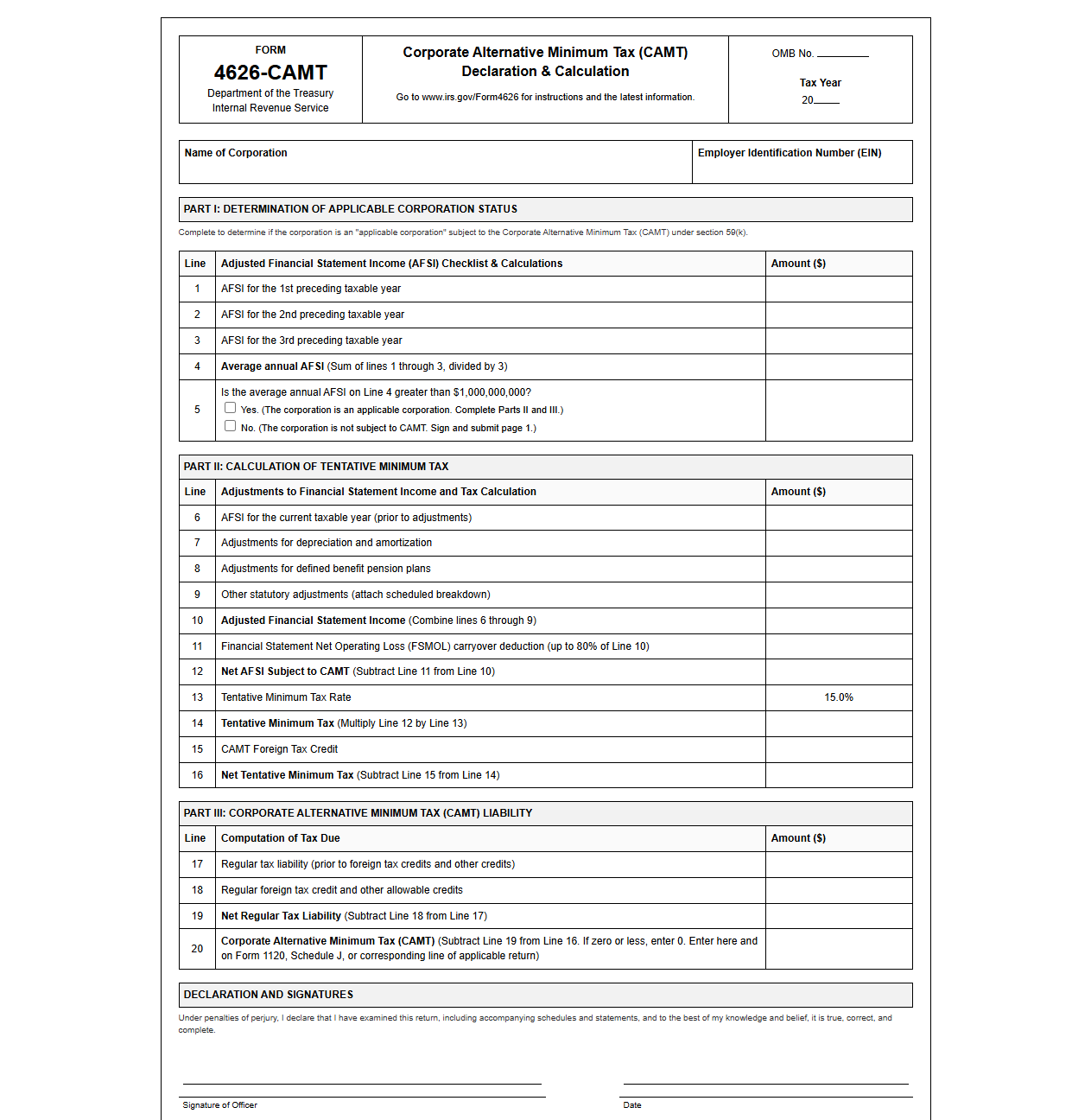

Corporate AMT Tax Return Worksheet

Download: .PDF

Download: .PDF

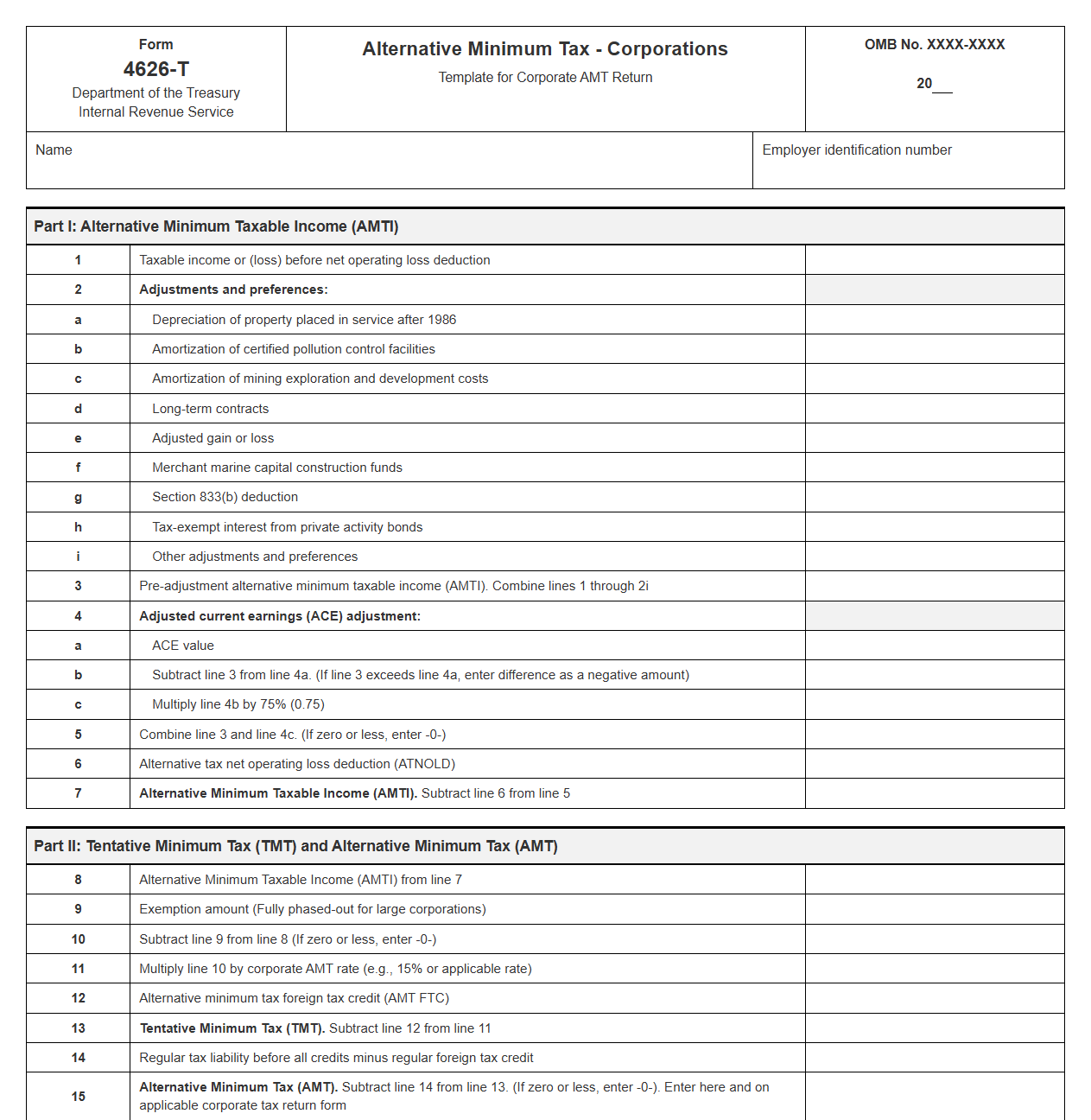

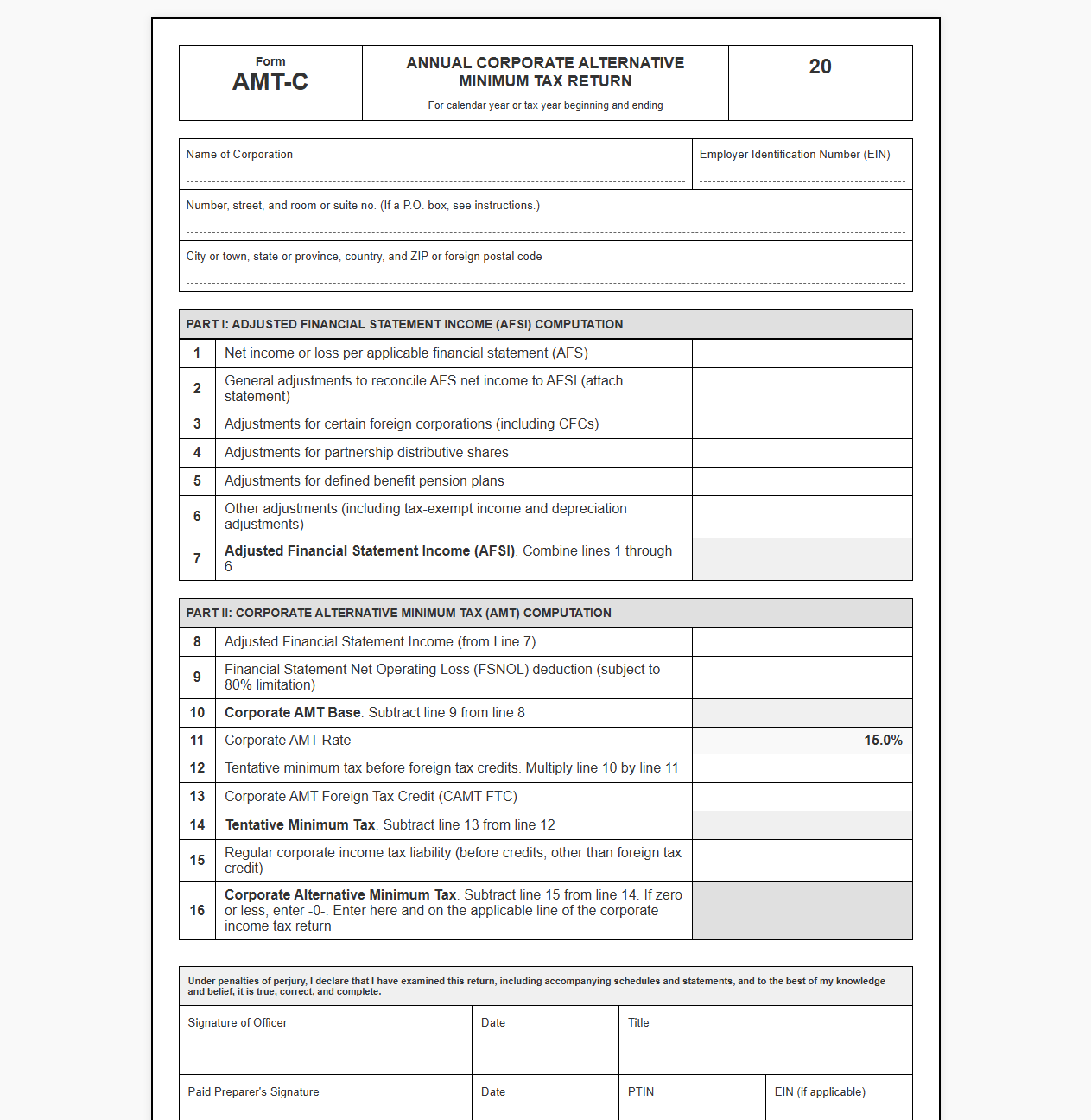

Alternative Minimum Tax Return Template for Corporates

Download: .PDF

Download: .PDF

Corporate Minimum Tax Return Reporting Template

Download: .PDF

Download: .PDF

CAMT Calculation and Return Template

Download: .PDF

Download: .PDF

Corporate Alternative Minimum Tax Declaration Template

Download: .PDF

Download: .PDF

Annual Corporate AMT Return Template

Download: .PDF

Download: .PDF

Corporate Alternative Minimum Tax Filing Form Template

Download: .PDF

Download: .PDF

Navigating the Complexity of the Corporate Alternative Minimum Tax

The introduction of the Corporate Alternative Minimum Tax (CAMT), enacted under the landmark Inflation Reduction Act (IRA), represents one of the most significant shifts in the United States tax landscape in decades. This novel tax regime imposes a fifteen percent minimum tax on the adjusted financial statement income of massive corporations, creating unprecedented compliance burdens for multinational enterprises. Meeting these requirements demands an extraordinary level of precision and coordination. This article explores how corporate tax departments can leverage specialized, structured return templates to streamline data collection, minimize risk, and secure audit-ready compliance.

The Core Compliance Hurdles for Corporate Tax Teams

Navigating the technical landscape of the new corporate minimum tax requires tax departments to solve highly complex calculation and data-matching challenges. Unlike traditional tax adjustments, this regime demands constant tracking of financial reporting and tax differences across various legal entities.

- Determining Adjusted Financial Statement Income (

AFSI) by applying specific statutory modifications to net income. - Tracking persistent and timing-related book-tax differences across international jurisdictions.

- Managing consolidated group complexities, including the allocation of

AFSIamong affiliated entities and non-consolidated book partners. - Evaluating the applicability of safe harbors and depreciation adjustments under evolving administrative guidance.

Enter Specialized Return Templates: A Strategic Solution

To overcome these hurdles, tax departments are turning to dedicated return templates. These templates serve as a translation mechanism, bridging the gap between raw financial accounting data and rigid tax compliance requirements. By standardizing input data, templates ensure that financial figures from disparate source systems are normalized before calculations begin, saving hundreds of hours of manual reconciliation.

Rather than relying on disjointed spreadsheets, tax teams can use centralized templates to establish a single source of truth, making it much easier to defend tax positions during audits and internal reviews.

Essential Features of a High-Performing CAMT Template

Not all calculation tools are created equal. To successfully manage the vast streams of accounting data required, a template must incorporate specific technical capabilities designed to prevent errors and document institutional knowledge.

- Automated AFSI Adjustment Calculators: Pre-built logic to handle specific adjustments such as depreciation, pensions, and foreign source income.

- Historical Data Repositories: Structured tabs to track cumulative attributes, carryforwards, and prior-year determinations.

- Built-In Error Validation Rules: Hard-coded checks that flag inconsistent inputs, out-of-balance balance sheets, or missing entity-level data.

Quantifying the Benefits: Accuracy, Efficiency, and Audit Readiness

| Compliance Metric | Manual Tracking Approach | Template-Driven Approach |

|---|---|---|

| Calculation Speed | Days of manual reconciliation | Minutes of automated processing |

| Error Propensity | High risk of formula breakage | Low risk due to locked formulas |

| Audit Trail Strength | Fragmented documentation trail | Centralized, structured data log |

Best Practices for Integrating Templates into Your Tax Workflow

Successfully adopting templates requires a structured transition plan to ensure that tools are embraced by the compliance team and aligned with existing ERP systems.

- Establish Data Extraction Pipelines: Map financial accounting ledger accounts directly to the corresponding input cells of your template.

- Conduct Team Training Sessions: Train tax professionals on how to utilize the templates, specifically focusing on troubleshooting error flags.

- Implement Continuous Updates: Review and update template logic as the IRS issues new regulations, notices, and administrative guidance.

- Lock Core Formulas: Restrict editing permissions on calculation cells to maintain workbook integrity across different entities.

Future-Proofing Corporate Tax Compliance

Modern tax departments must view the implementation of standardized templates as an investment in sustainable infrastructure. Establishing a robust, template-based process today ensures that your organization remains agile and prepared for any future regulatory expansions.

"The organizations that transition from reactive spreadsheet building to proactive data management are the ones that survive regulatory shifts with minimal operational friction." - Corporate Tax Technology Forum

Leave a comment