Multinational finance teams frequently battle the administrative nightmare of intercompany transaction discrepancies, which stall month-end closes and trigger costly audit flags. As global supply chains grow increasingly matrixed, the sheer complexity of multi-entity accounting further exacerbates this friction, leaving organizations vulnerable to systemic reconciliation errors.

Implementing a standardized sales return document framework offers immediate relief, granting corporate treasuries unprecedented transaction visibility and airtight financial control. However, achieving this efficiency is not a simple software patch; it stipulates a rigorous, cross-departmental alignment of transfer pricing policies and unified Return Merchandise Authorization (RMA) workflows. Without this baseline, operational friction points-such as mismatched currency valuations and disparate ledger entries-will continue to disrupt balance sheets.

This article explores the core components of a standardized intercompany framework, outlining step-by-step methodologies to harmonize cross-entity returns, eliminate valuation bottlenecks, and secure seamless audit readiness.

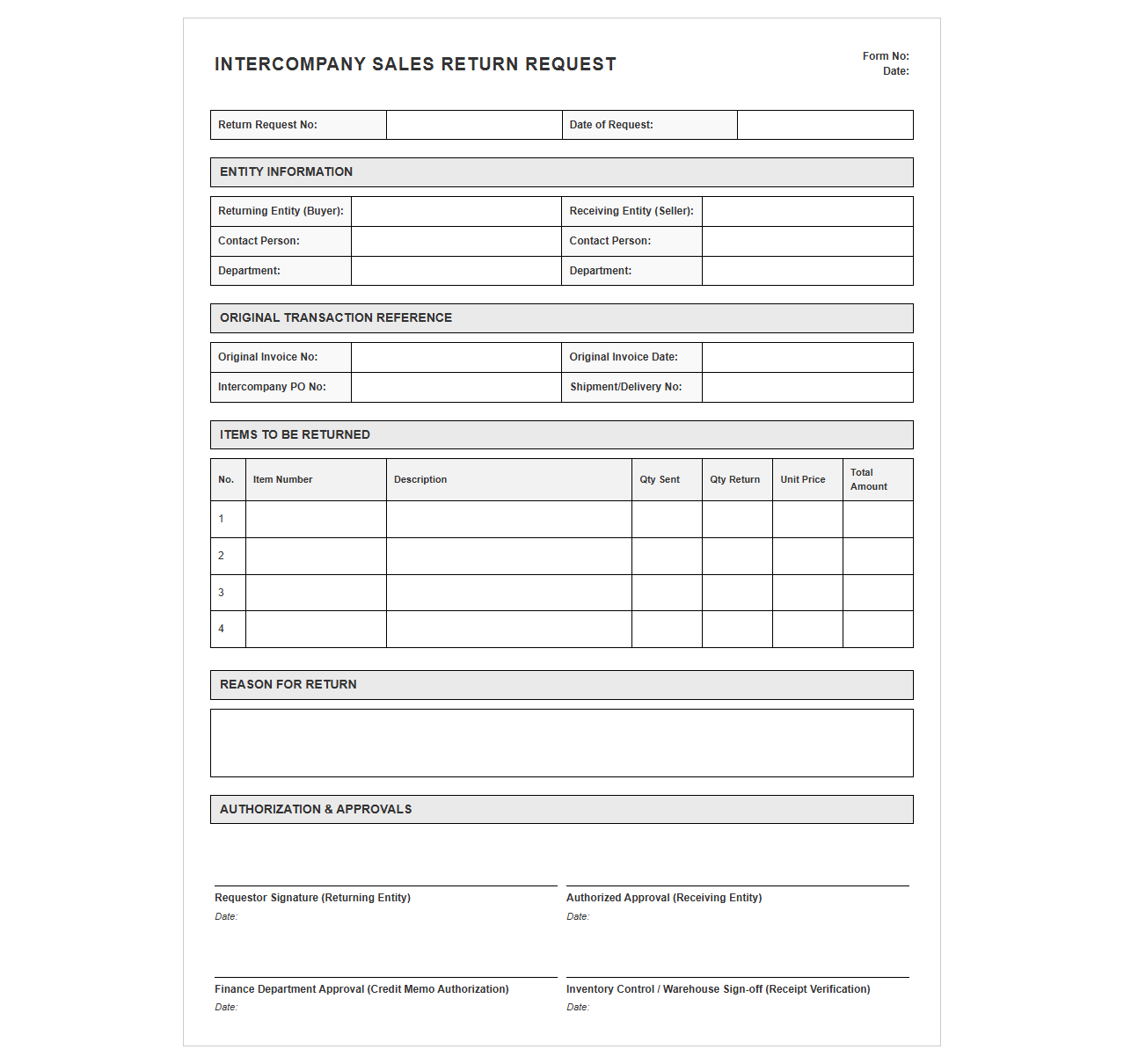

Intercompany Sales Return Request Form

Download: .PDF

Download: .PDF

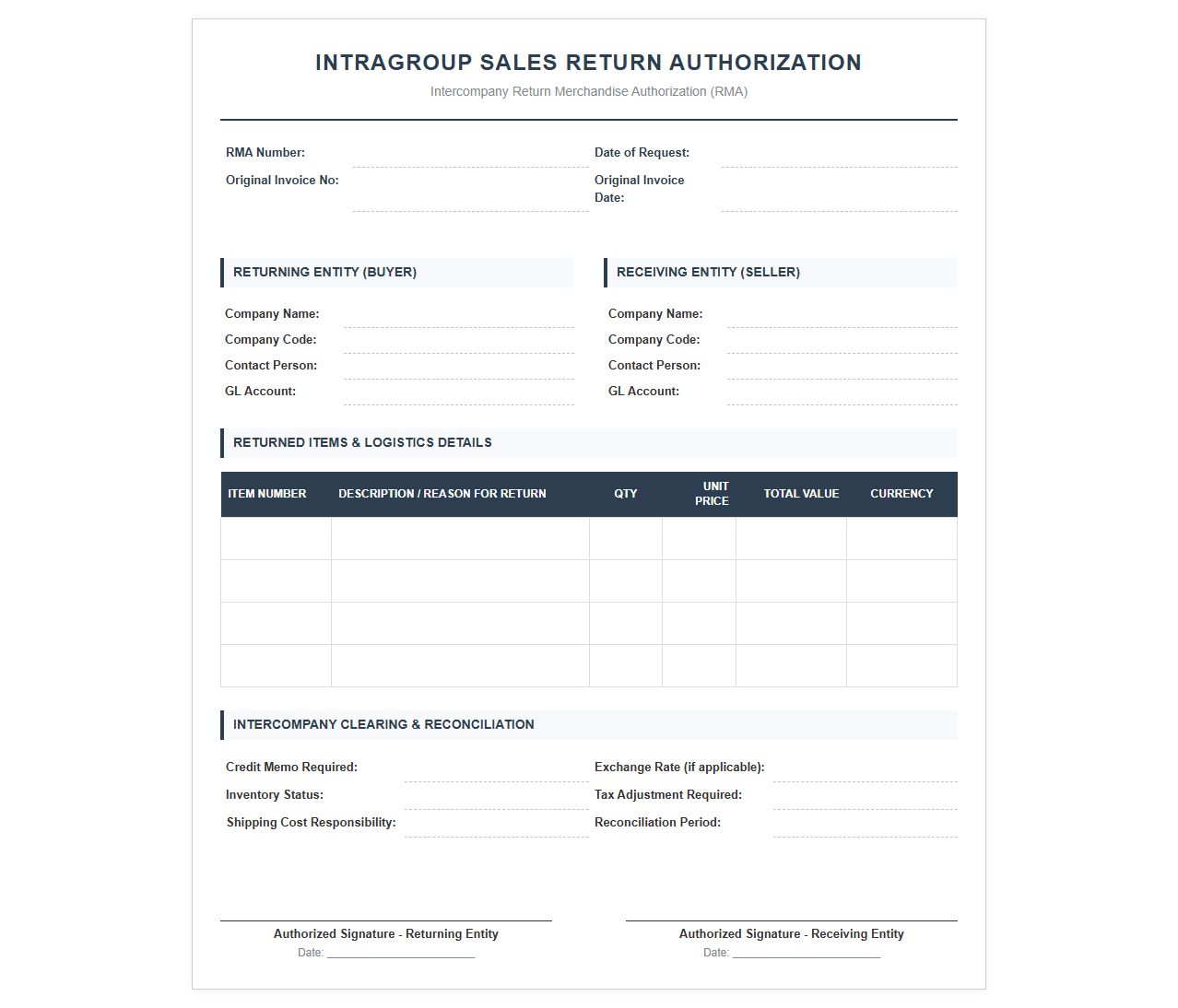

Intragroup Sales Return Authorization Template

Download: .PDF

Download: .PDF

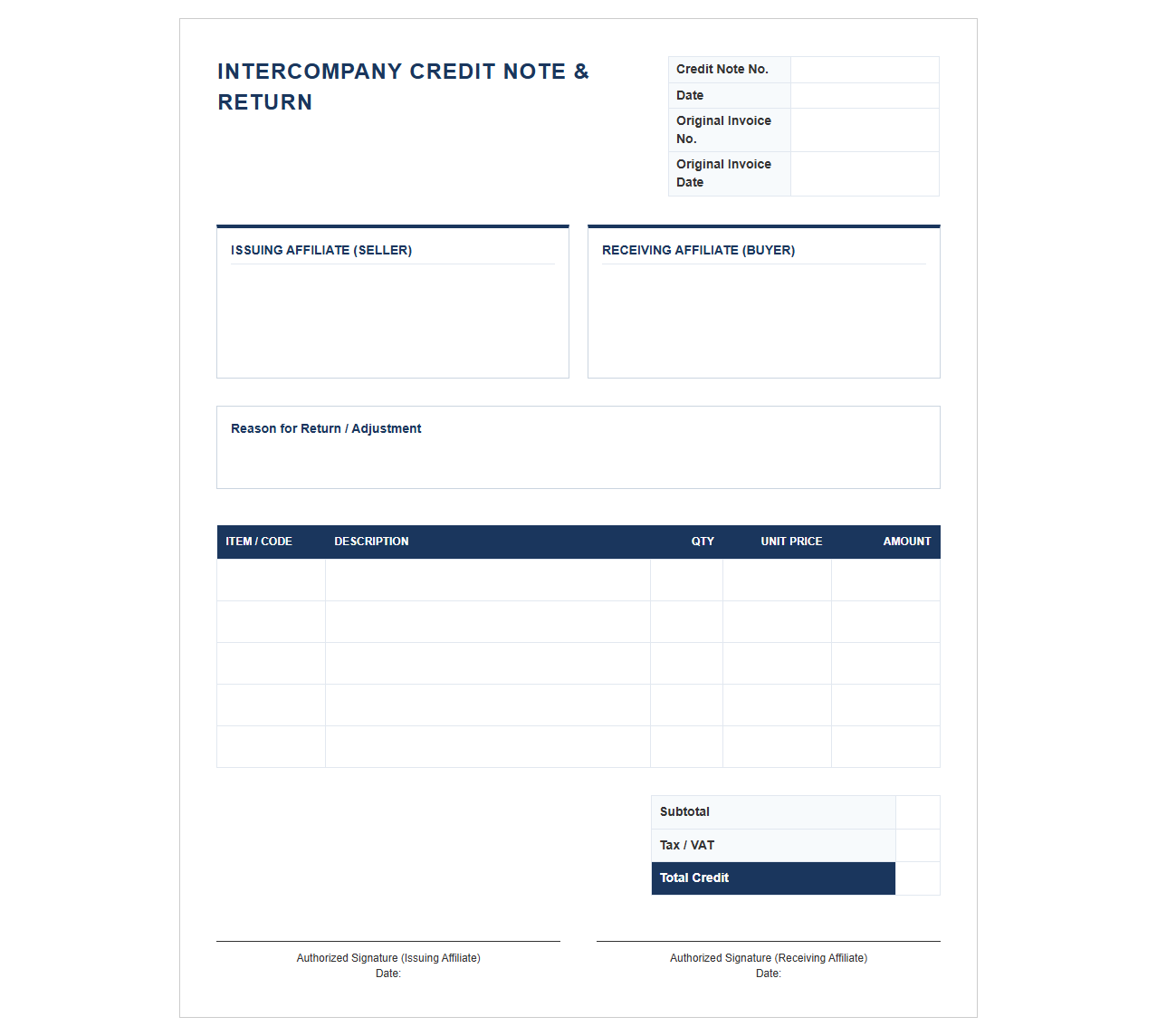

Intercompany Sales Credit Note and Return Template

Download: .PDF

Download: .PDF

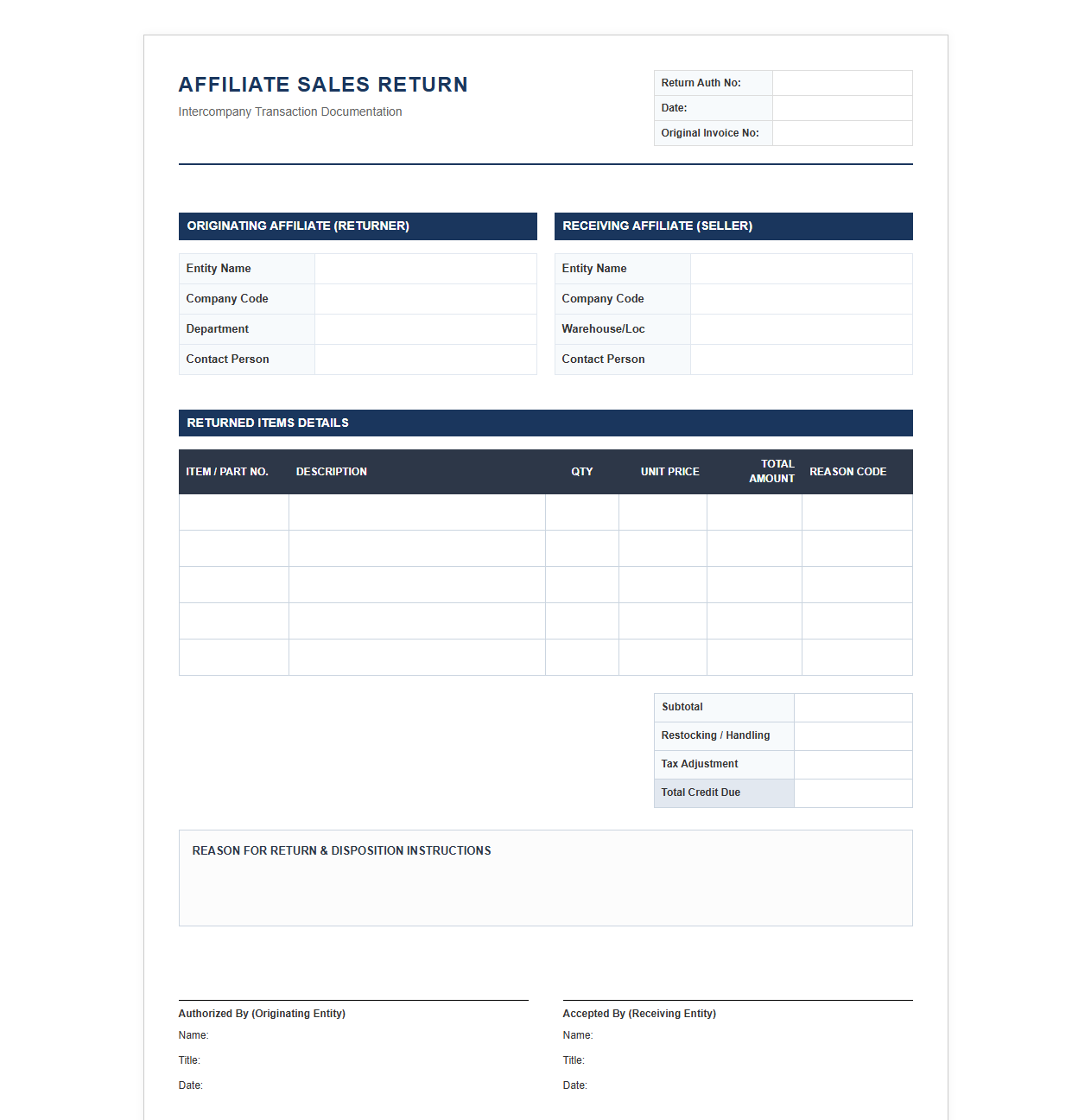

Affiliate Sales Return Documentation Template

Download: .PDF

Download: .PDF

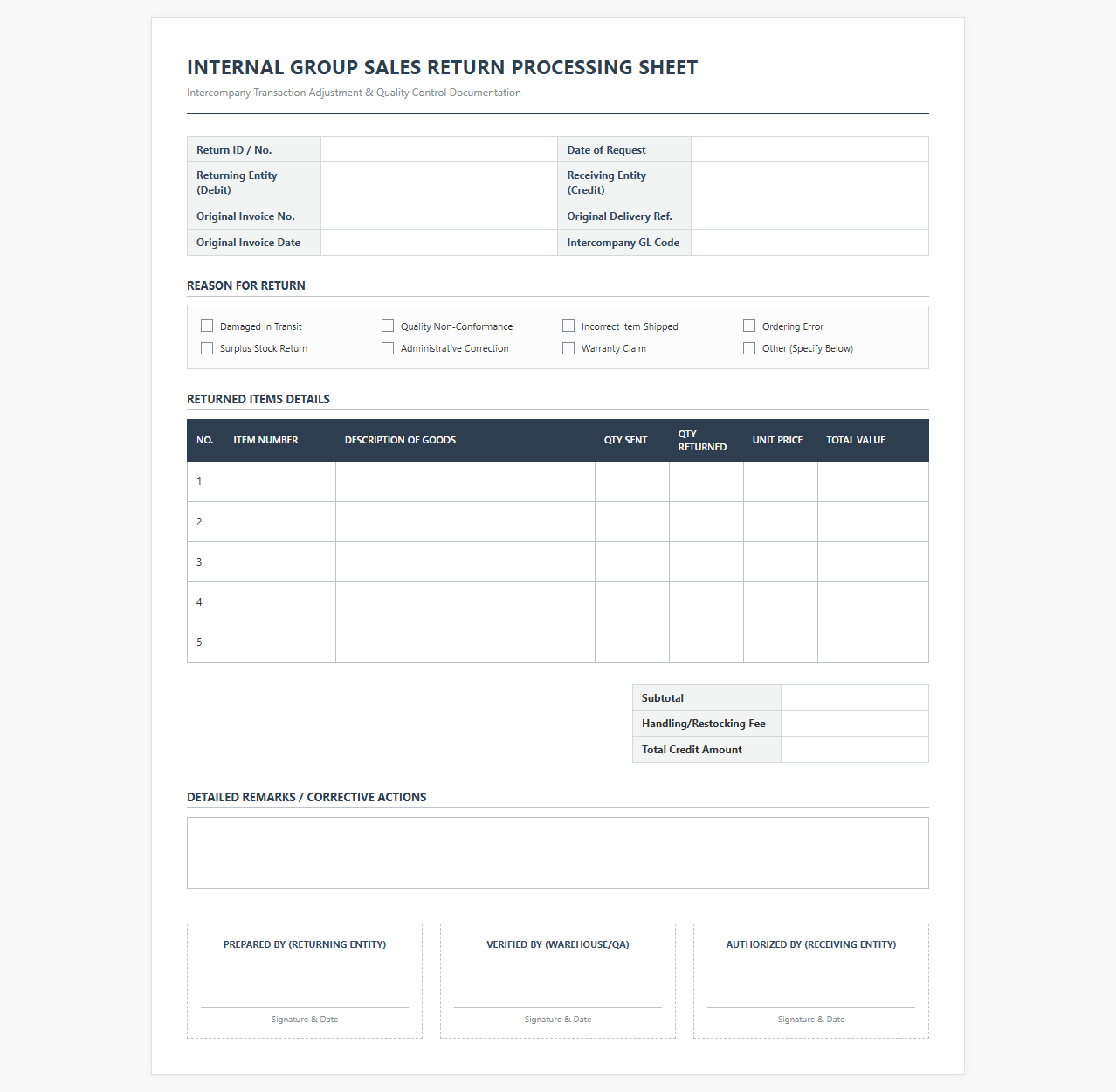

Internal Group Sales Return Processing Sheet

Download: .PDF

Download: .PDF

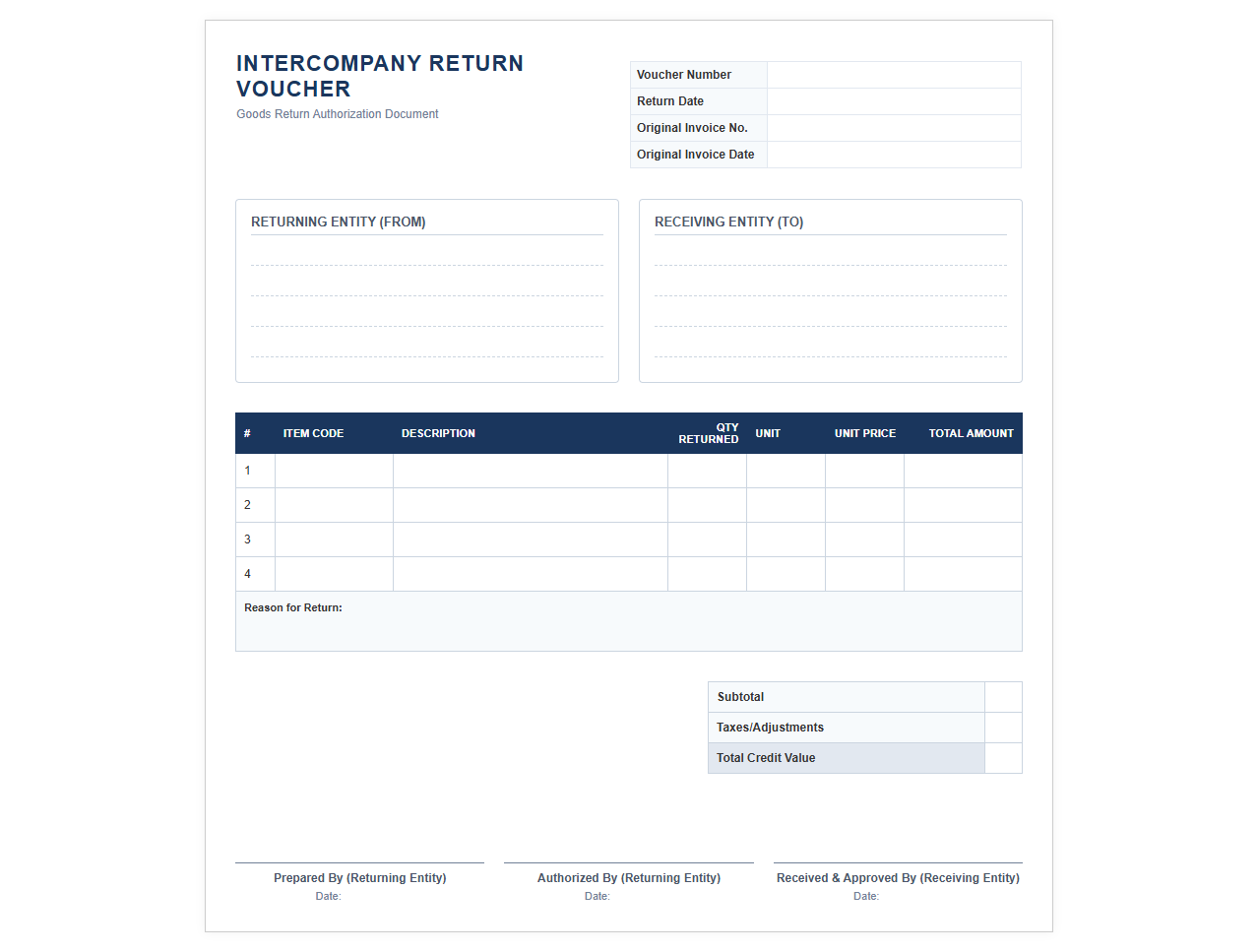

Intercompany Goods Return Voucher Template

Download: .PDF

Download: .PDF

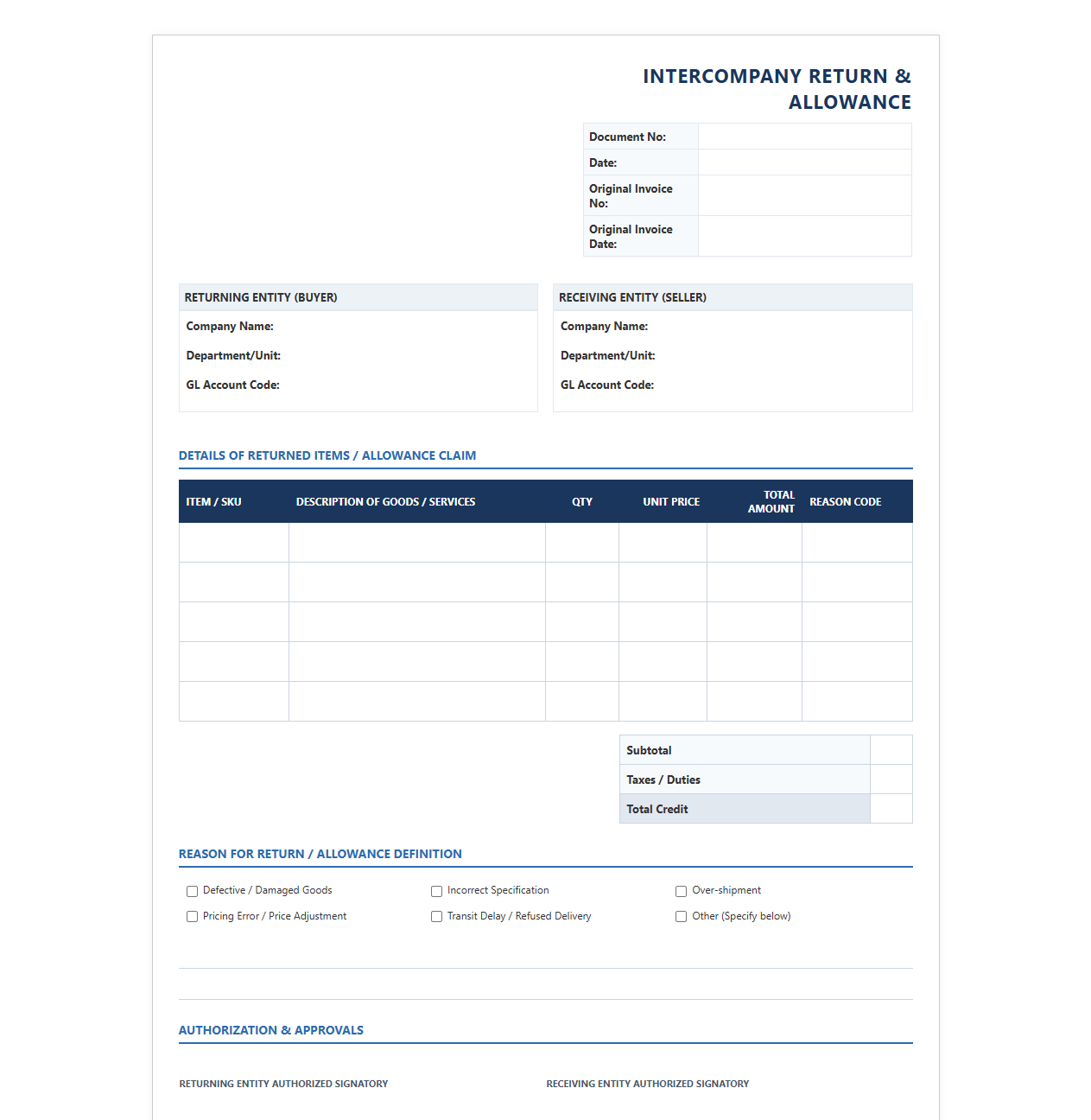

Intercompany Sales Returns and Allowances Form

Download: .PDF

Download: .PDF

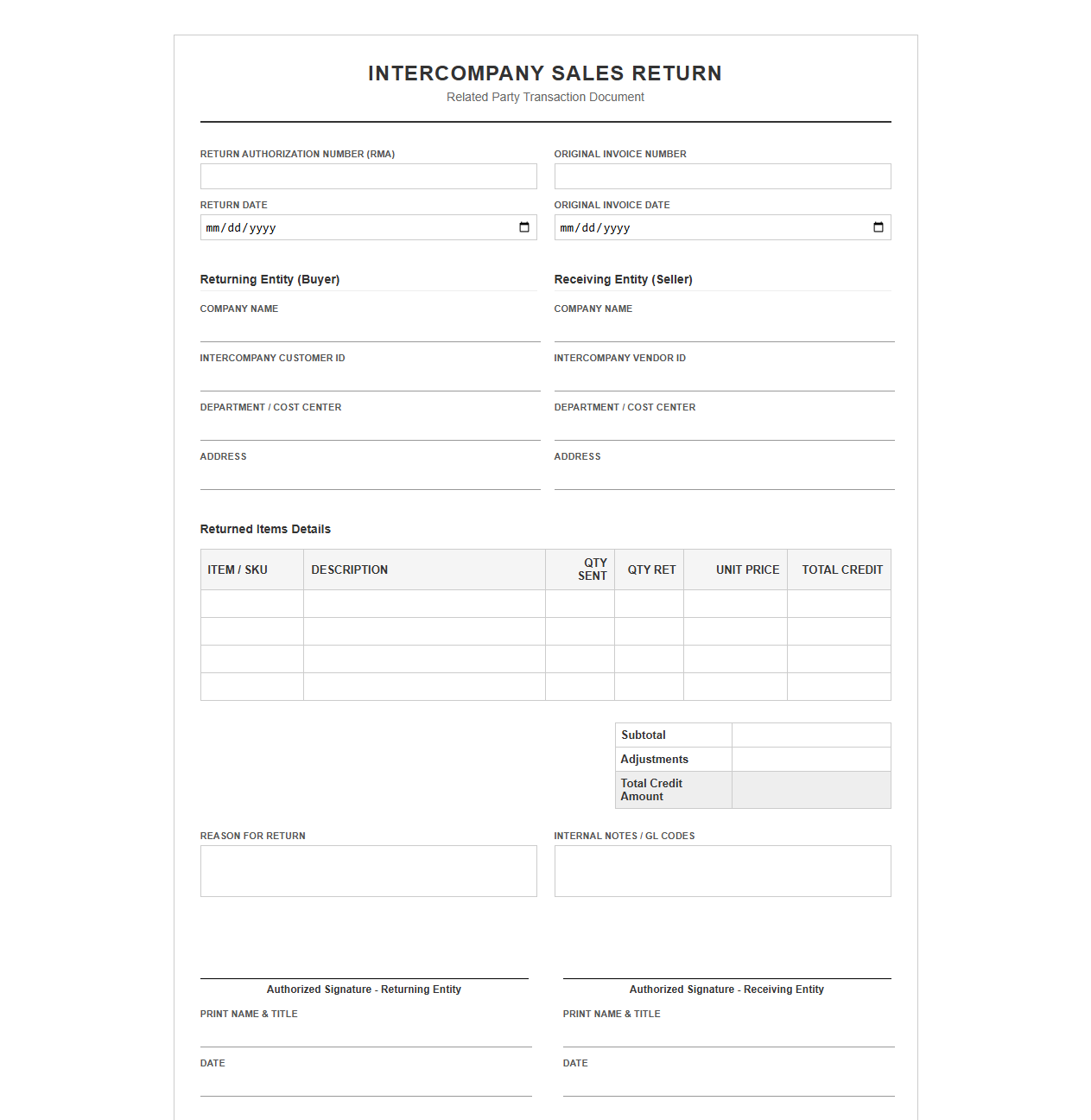

Related Party Sales Return Template

Download: .PDF

Download: .PDF

The Cost of Intercompany Transaction Friction

In multinational corporations, intercompany transactions represent a massive portion of global commerce. However, when goods are returned between subsidiaries, operational friction frequently arises. Discrepancies occur due to mismatched tax rates, differing regional inventory valuation methods, and misaligned currencies. This friction leads to unreconciled balances on balance sheets, delayed financial reporting, and significant resource drain as accounting teams manually trace transaction paths. The financial impact is substantial: inflated administrative costs, write-offs, and increased exposure to tax compliance audits.

Defining the Standardized Return Framework

A standardized intercompany sales return document framework establishes a single, unified set of rules and data formats that both the initiating and receiving entities must follow. By mandating uniform fields and validation rules, organizations eliminate the root causes of asymmetry before transactions hit the general ledger. Standardization acts as the bridge that aligns mismatched accounting periods, currency conversions, and local entity policies.

Establishing a single source of truth for every internal return is the only way to eliminate downstream matching errors and ensure transfer pricing compliance. Global Intercompany Policy Institute

Essential Elements of the Return Document

To ensure seamless reconciliation, the return document must capture specific metadata at the point of origin. This structural data allows automated systems to match returns instantly against the original sales events.

Original_Invoice_ID: A mandatory link to the initial transaction invoice.Reason_Code: Standardized identifiers indicating why the goods were returned.Transfer_Price_Adjustment_Factor: The specific rate used to reconcile margin differences between subsidiaries.Tax_Treatment_Indicator: Tax codes ensuring VAT or GST is treated correctly across borders.

The Step-by-Step Resolution Workflow

Resolving disputed sales returns requires a systematic approach to trace and correct variances. Below is the chronological workflow:

- Identification: Pinpoint the discrepancy by comparing the subledger entries of the shipping and receiving entities.

- Validation: Verify the physical receipt of goods against the return authorization payload.

- Adjustment Generation: Calculate transfer pricing and tax differences using standard adjustment templates.

- Approval: Secure automated or manual sign-off from both participating entity controllers.

- Reconciliation: Post matching journal entries to eliminate the open balances in the consolidated ledger.

Leveraging Automation and ERP Integration

Modern Enterprise Resource Planning (ERP) systems act as the operational backbone for executing standardized intercompany return workflows. By embedding matching rules directly within global ERP instances, organizations can bypass labor-intensive manual steps. Automated matching engines instantly pair return documents with their corresponding original outbound invoices, reconciling currency differences and inventory balances in real time.

These integrations ensure that subledger postings are synchronized immediately across both entities. This level of system alignment reduces human error, frees accounting teams to focus on strategic exceptions, and prevents intercompany imbalances from persisting into the month-end close cycle.

Establishing Cross-Entity Governance

Technology alone cannot solve transaction friction; it must be backed by clear governance. Clear communication protocols define which stakeholder is responsible for initiating a return, how quickly the receiving entity must validate it, and how disputes are handled.

By establishing shared service center ownership and unified KPIs, companies ensure that both subsidiaries treat intercompany transactions with the same rigor as third-party transactions.

Achieving Continuous Financial Alignment

Implementing a standardized return document framework shifts intercompany accounting from a reactive scramble to a proactive discipline. By systematically resolving friction at the point of origin, multinational corporations secure faster month-end closes and significantly reduce the time spent on internal reconciliations. This rigorous structure fosters continuous audit readiness and ensures transfer pricing compliance with tax authorities globally. Elevating the accuracy of intercompany data yields a highly reliable, transparent balance sheet that reflects true corporate performance.

Leave a comment