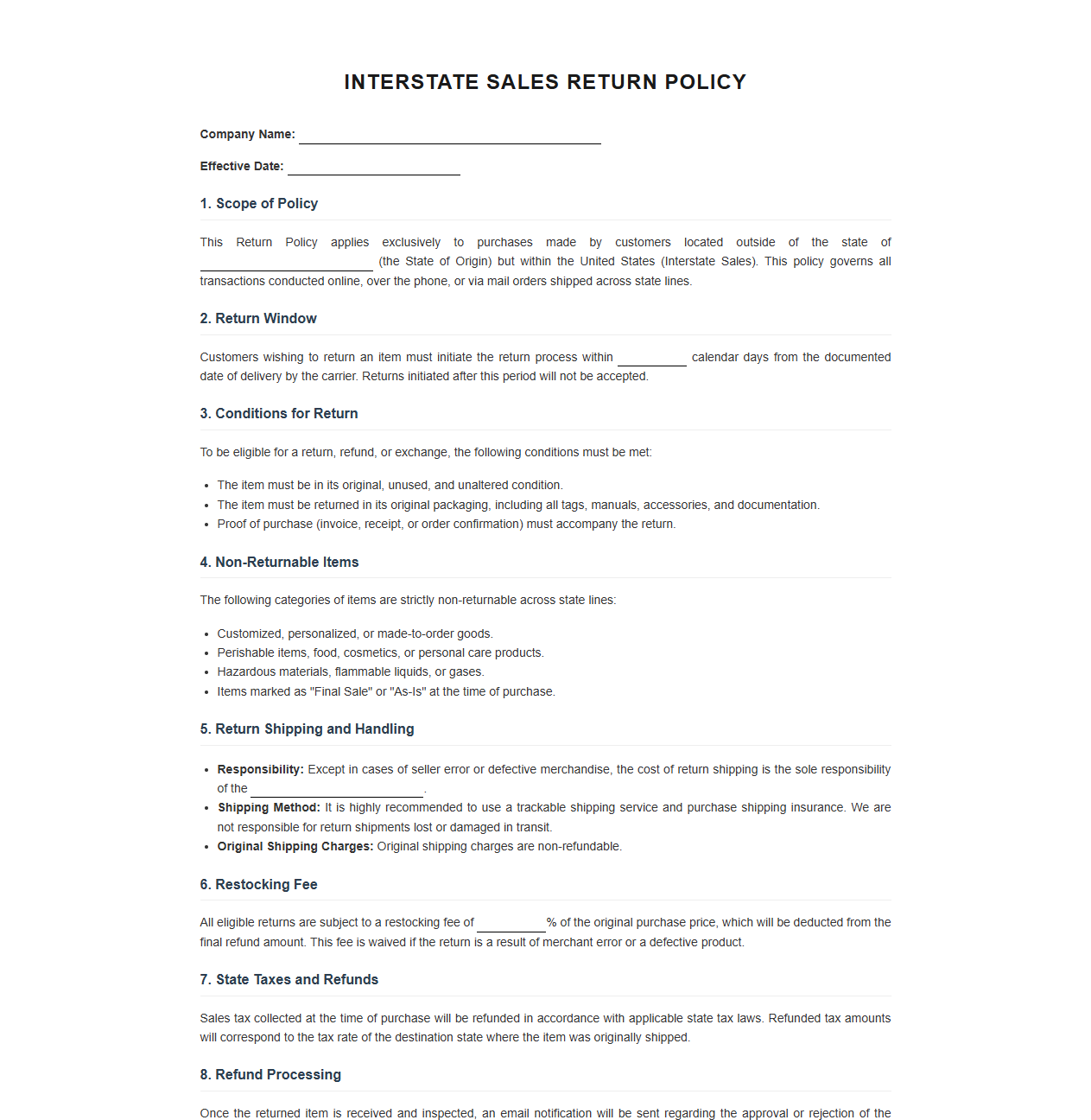

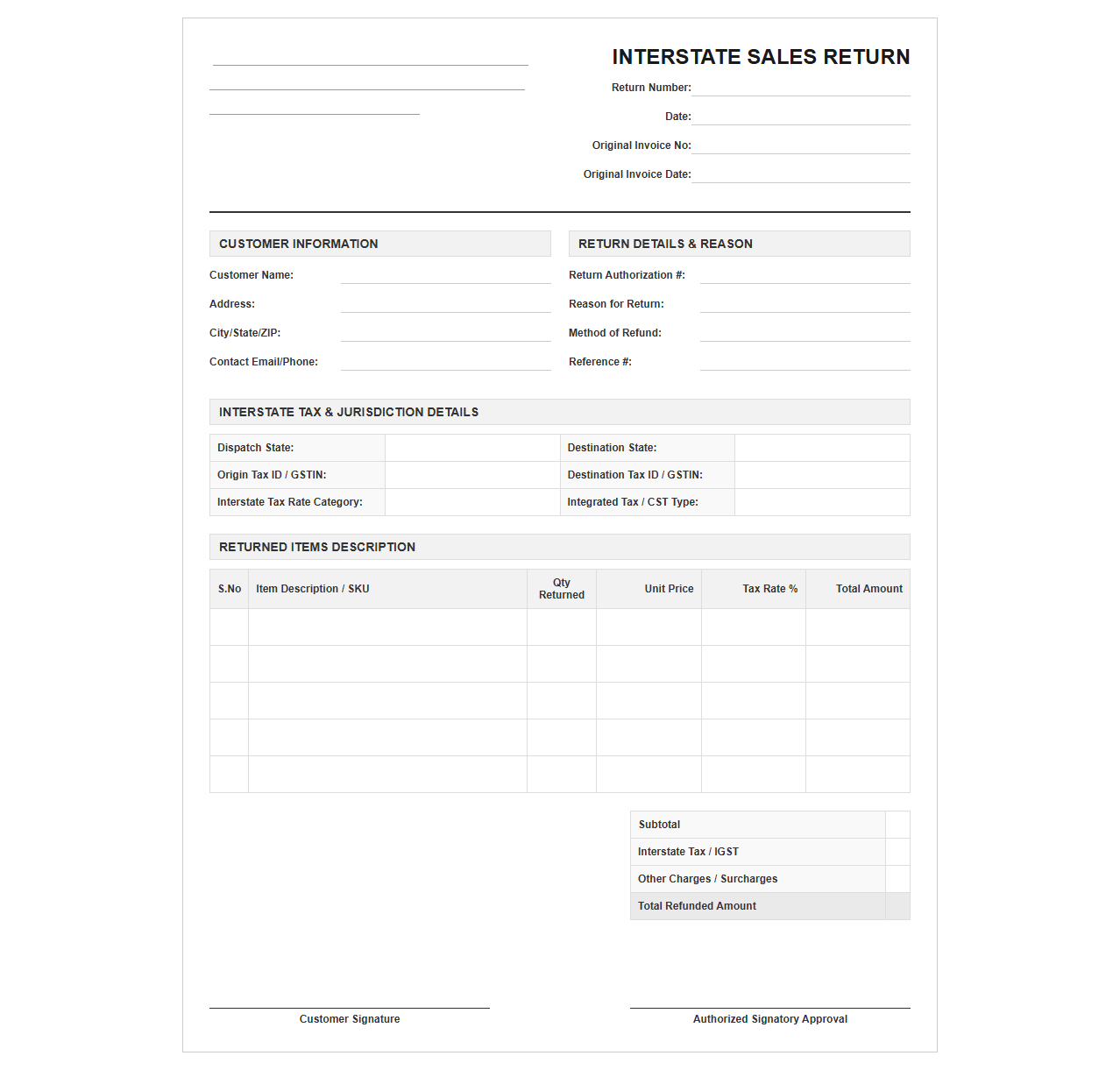

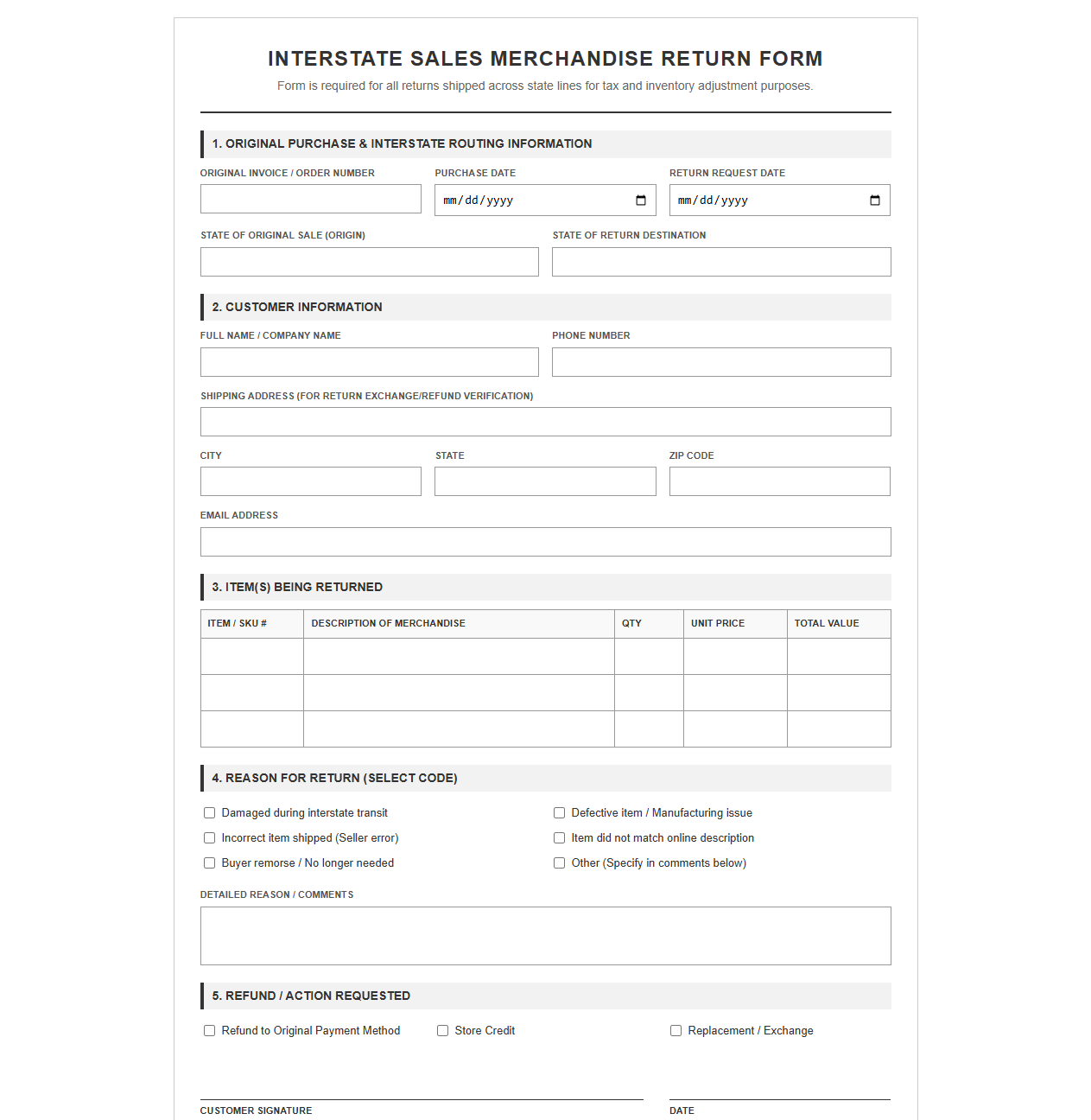

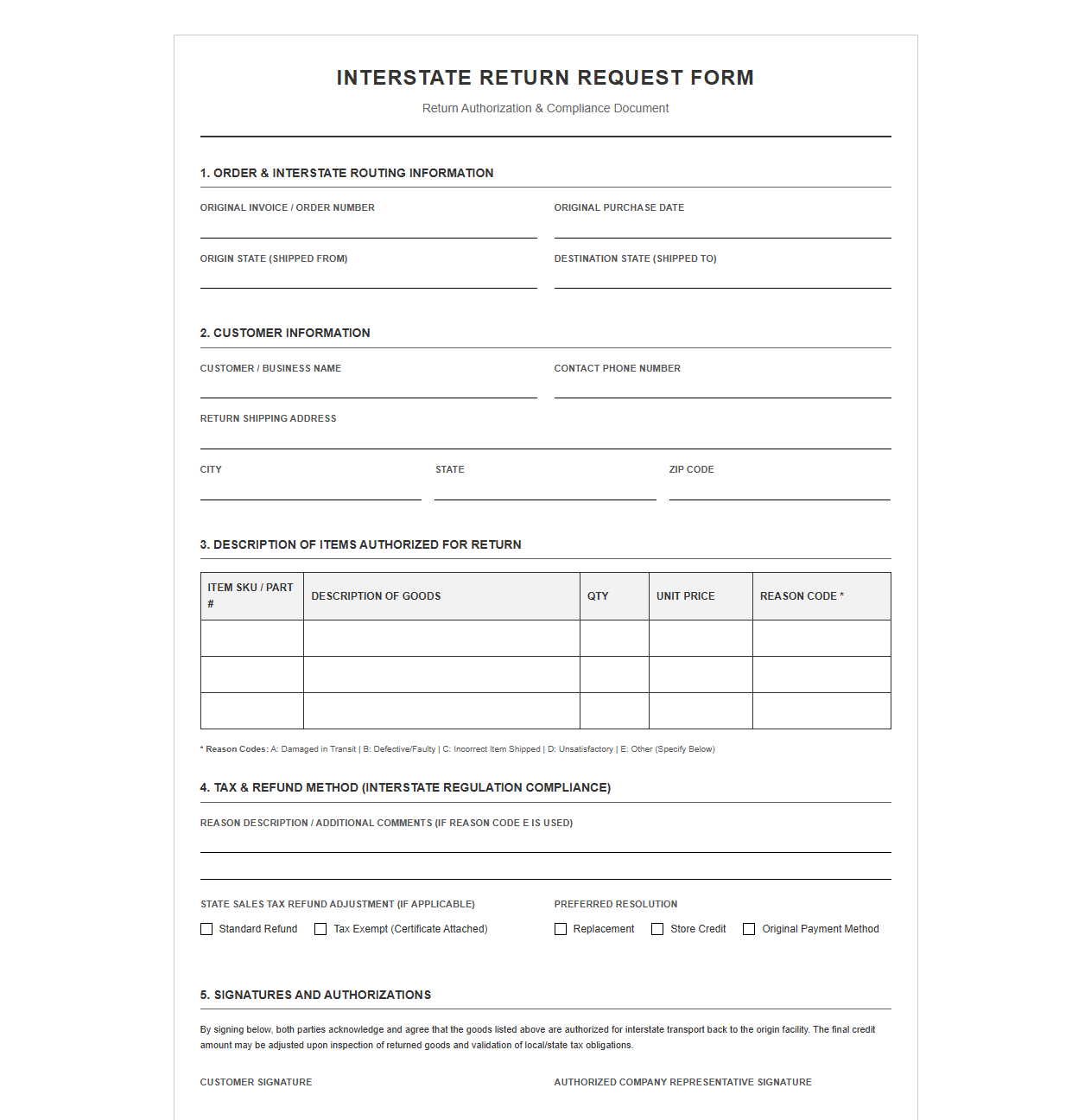

Navigating interstate sales returns is a persistent compliance headache for growing businesses. Reconciling mismatched credit memos across varying state tax jurisdictions frequently leads to administrative bottlenecks, inaccurate refunds, and costly audit exposure. Before attempting to automate these workflows, organizations must first establish a unified administrative baseline that bridges disparate state-level tax regulations.

Implementing standardized documentation templates grants finance teams immediate audit-readiness and recaptures valuable operational hours. However, a key stipulation remains: these tools are not one-size-fits-all and must be carefully calibrated to regional nuances, such as capturing California's CDTFA-101 return-policy requirements or verifying interstate bills of lading for proof of export.

In this guide, we will outline how to construct these compliant frameworks, identify critical data fields required for multi-state returns, and provide customizable templates to secure your tax-compliance workflow.

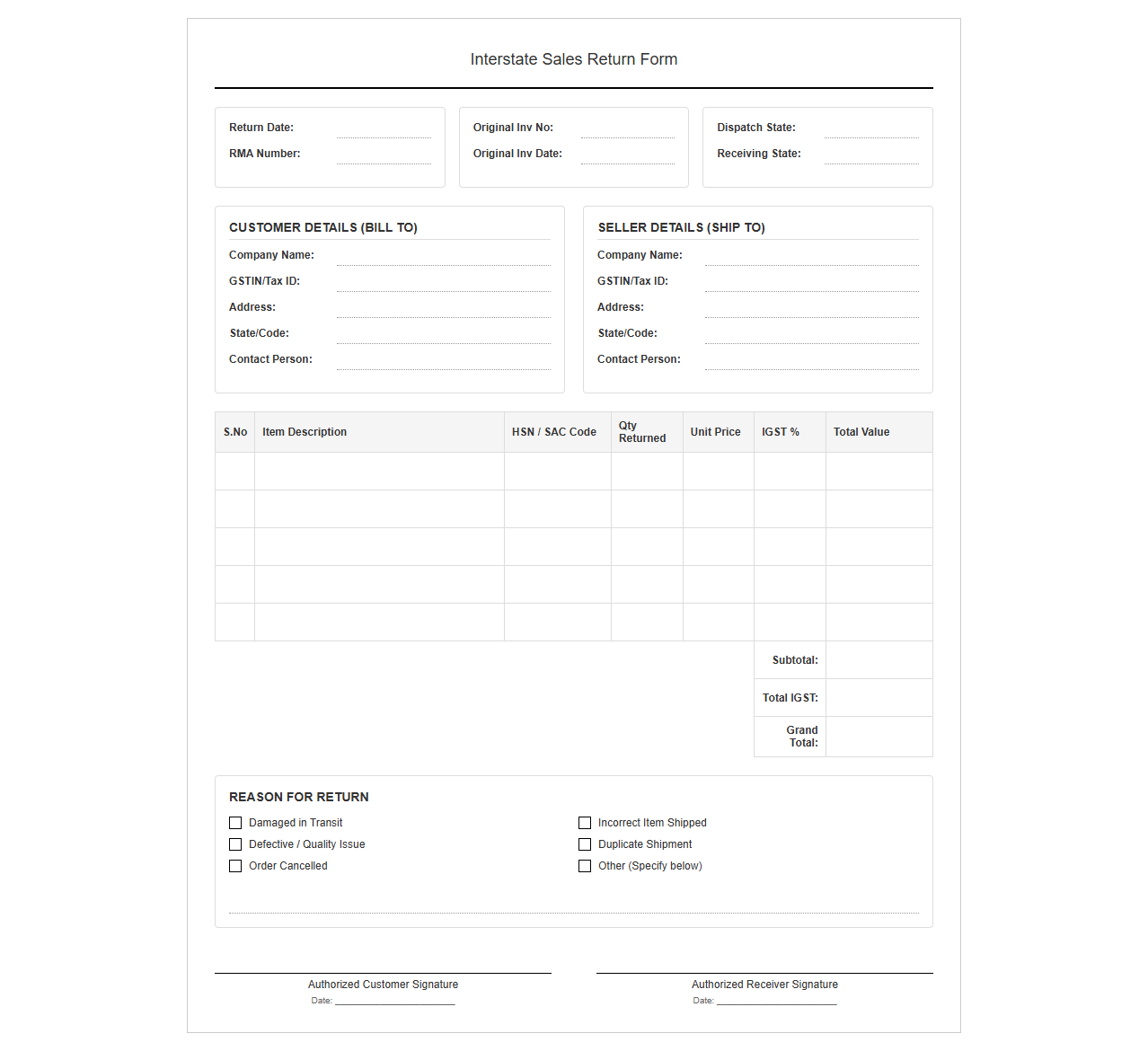

Interstate Sales Return Form Template

Download: .PDF

Download: .PDF

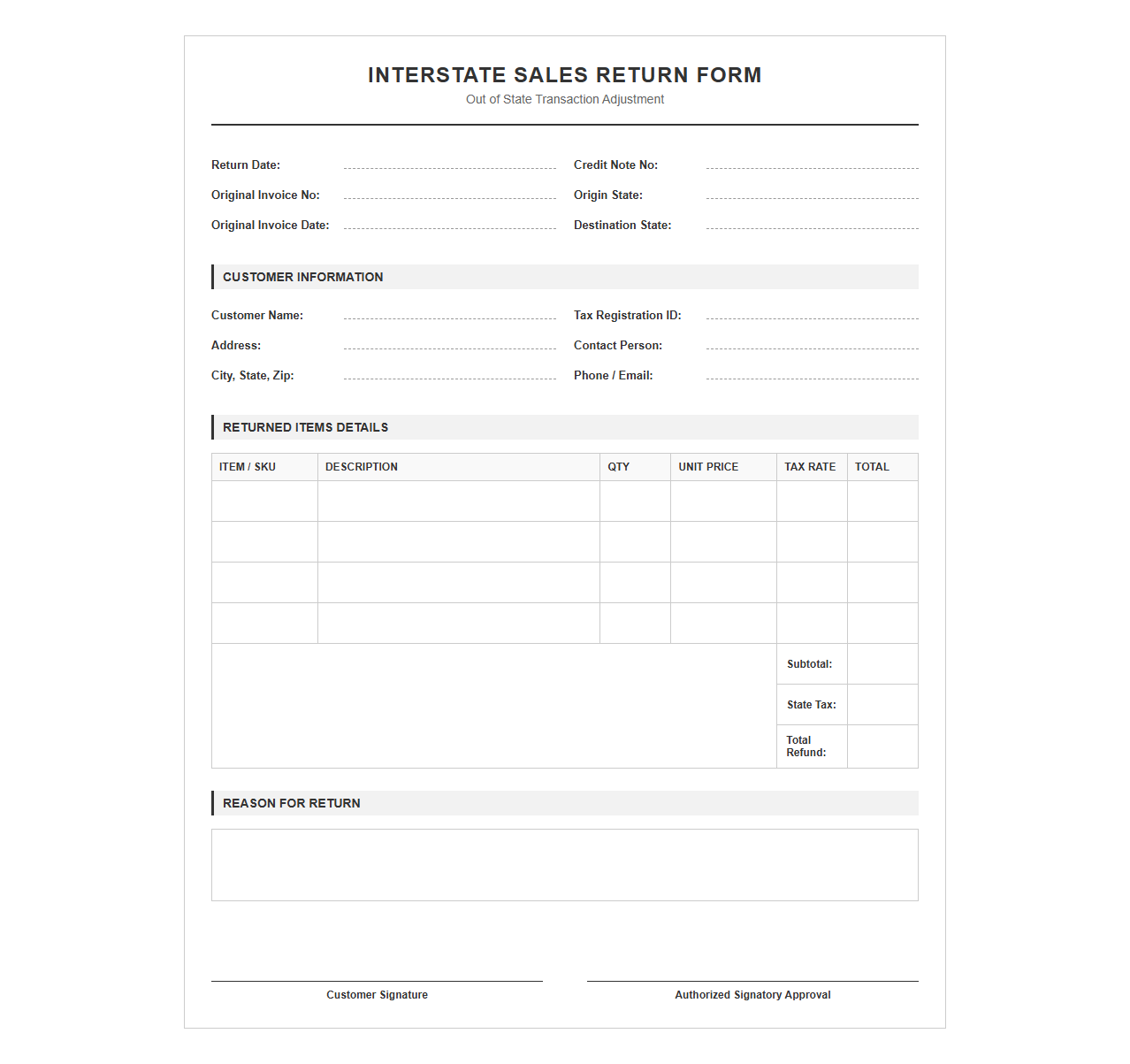

Out of State Sales Return Template

Download: .PDF

Download: .PDF

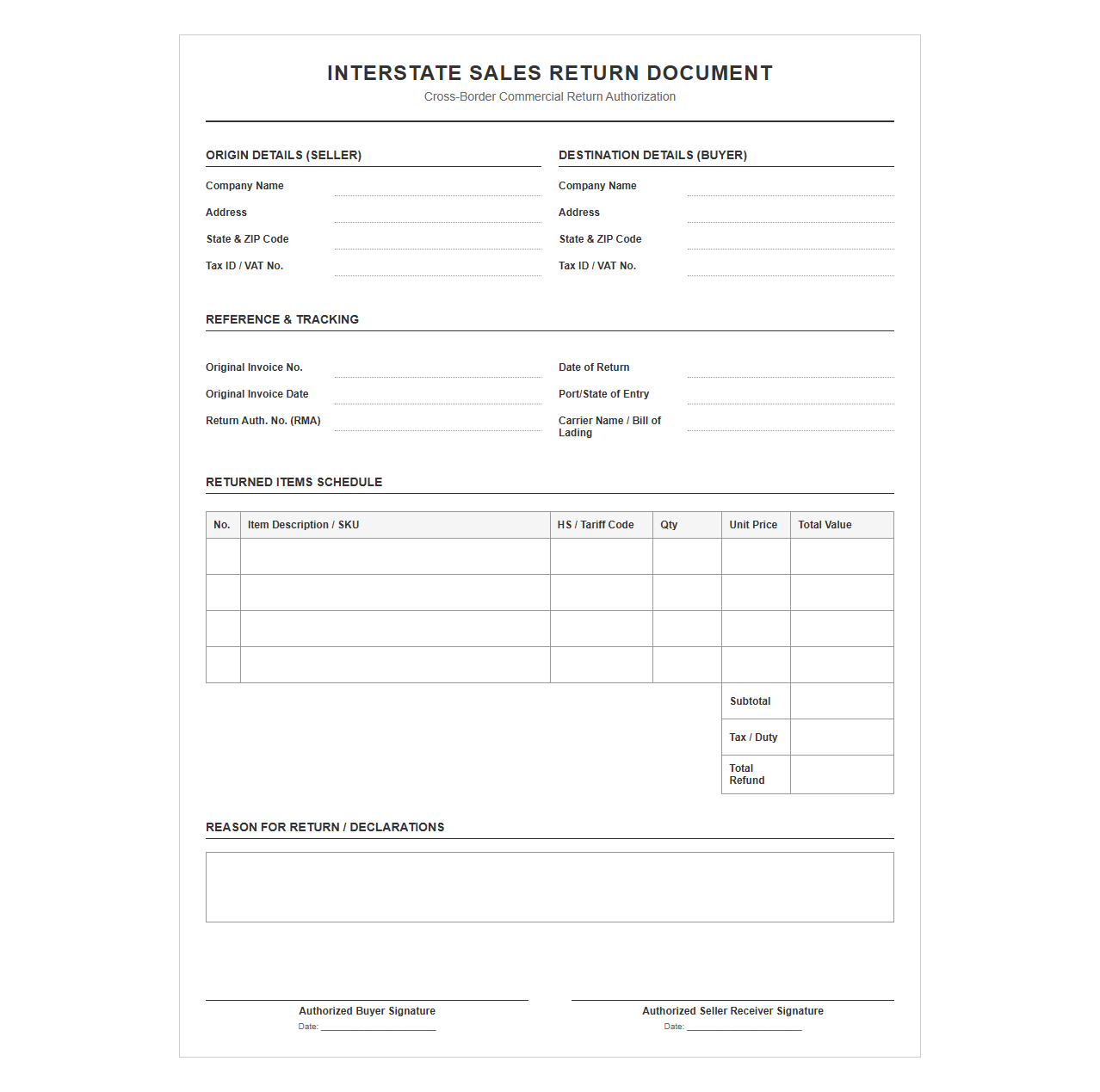

Cross Border Sales Return Document

Download: .PDF

Download: .PDF

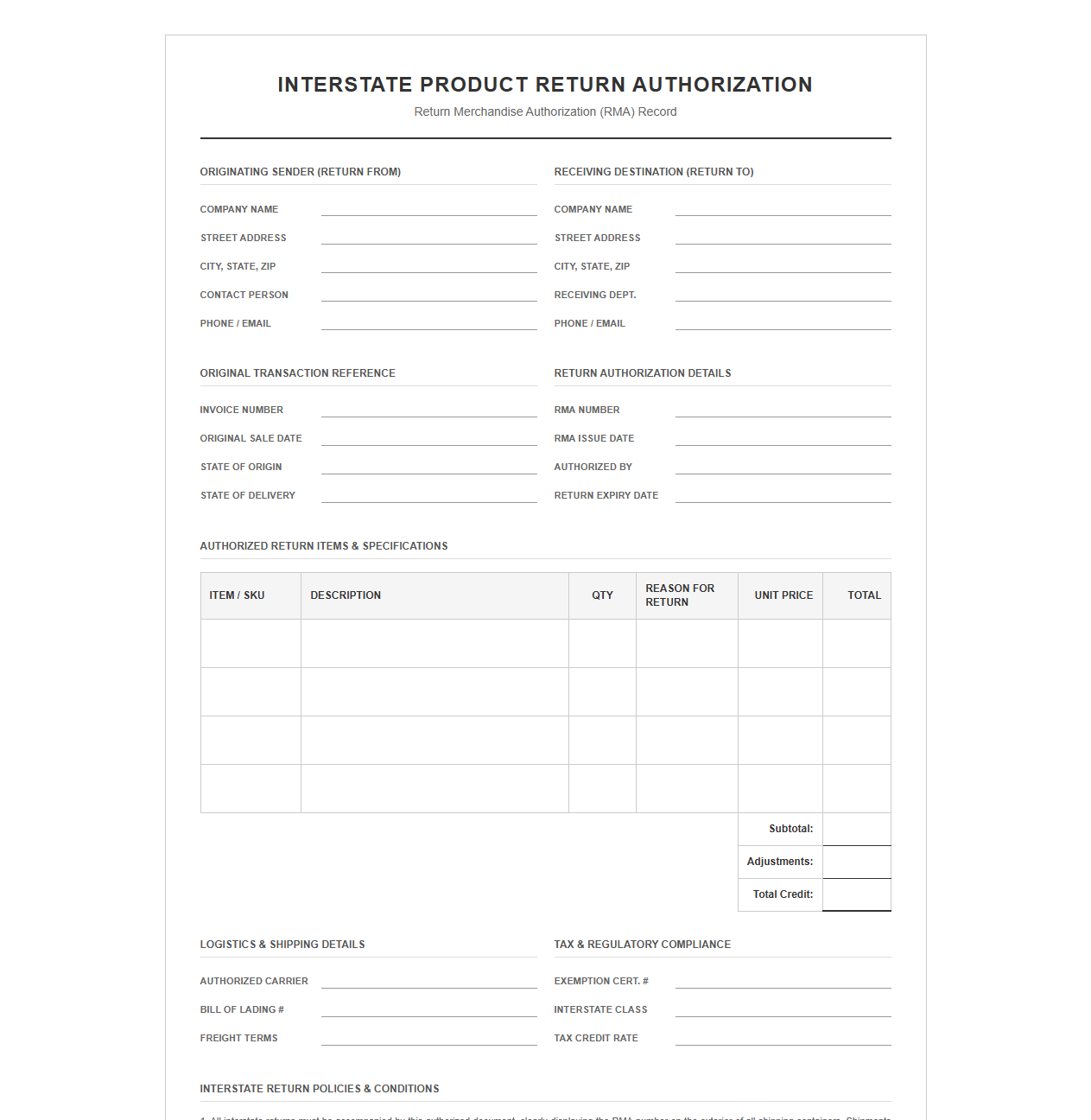

Interstate Product Return Authorization Template

Download: .PDF

Download: .PDF

Return Policy Template for Interstate Sales

Download: .PDF

Download: .PDF

Multi State Sales Return Template

Download: .PDF

Download: .PDF

Interstate Sales Merchandise Return Form

Download: .PDF

Download: .PDF

Return Request Template for Interstate Orders

Download: .PDF

Download: .PDF

Introduction to the Interstate Return Challenge

In the rapidly expanding landscape of modern commerce, cross-border transactions have become the default standard for growth. However, when goods flow backward across state lines, businesses encounter a complex maze of operational friction and legal exposure. Standardizing interstate sales returns has emerged as a critical logistical and legal hurdle for modern B2B and e-commerce companies alike.

Managing reverse logistics is no longer just about restocking inventory; it requires tracking physical movement alongside changing tax liabilities and regional laws. Without a unified, standardized framework, organizations risk operational delays, customer dissatisfaction, and severe compliance failures. A structured return policy is the foundation of scalable, multi-state growth.

Navigating the Regulatory and Tax Compliance Framework

When a product is returned from another state, the financial transaction does not simply reverse itself. Out-of-state returns carry significant tax implications, directly affecting how sales tax liabilities are calculated and reported. Because of the Wayfair decision, physical and economic nexus definitions dictate that even remote sellers must meticulously document when and where a sale was undone to prove they do not owe taxes on refunded revenue.

To mitigate audit risks, companies must implement strict, standardized documentation for every out-of-state return. This guarantees that the business can justify deductions on its state tax returns and demonstrate an unbroken chain of custody for the returned assets.

Essential Components of a Standardized Template

To ensure consistent data collection across all sales channels, organizations must utilize a standardized return document. This template captures the precise financial and geographical data points needed to satisfy tax authorities and streamline warehouse operations.

Every standard return document must include the following mandatory fields:

- Original Invoice Number: The unique identifier linking the return back to the initial transaction and tax rate applied.

- State of Origin and Destination: The physical locations where the journey began and ended, which determines tax jurisdiction boundaries.

- Local Tax Jurisdictions: Detailed county, city, or special district tax codes applicable to the original sale.

- Reason Codes: Standardized classifications (e.g., defective, incorrect item, buyer remorse) required for inventory accounting and tax-exempt return validations.

Step-by-Step Return Documentation Workflow

Processing an interstate return requires a systematic approach to preserve data integrity and maintain tax compliance. Follow this chronological workflow to process and log returned items accurately:

- Initiation and Verification: The customer requests a return, and the system verifies the original purchase details, checking the invoice number and the specific tax jurisdictions involved.

- Authorization and Label Generation: Issue a Return Merchandise Authorization (RMA) containing the correct destination warehouse address to track the physical cross-border movement.

- Physical Inspection and Logging: Once received, the warehouse team inspects the item, confirms its condition, and logs the receipt against the RMA in real time.

- Tax Credit Calculation: Calculate the exact sales tax refund based on the historical tax rates of the customer's jurisdiction at the time of purchase.

- Accounting Reconciliation: Record the transaction in the general ledger, reducing accounts receivable or issuing a refund while adjusting the corresponding state tax liability account.

Managing State-Specific Exceptions and Variations

While a unified core template is essential for operational efficiency, businesses cannot ignore the nuances of localized tax laws. Different states enforce highly specific regulations regarding the timeframe allowed for tax refunds, restocking fees, and return shipping taxability.

"Many jurisdictions do not allow companies to deduct sales tax on returns if the refund occurs outside of a specific window, such as 90 or 180 days from the original purchase date. Adapting to these local rules is mandatory for multi-state merchants." - Interstate Commerce Tax Council Guidelines

Organizations must design their core templates to be modular. This structural flexibility allows regional rules to overlay the standard form, ensuring compliance with strict local tax laws without disrupting the centralized reverse logistics framework.

Digital Integration and Automation Strategies

Manually tracking interstate returns across multiple jurisdictions is highly susceptible to human error. Modern enterprises rely on seamless digital integration to connect return templates directly with their Enterprise Resource Planning (ERP), Customer Relationship Management (CRM), and automated tax engines.

By leveraging automated APIs, a system can automatically execute code when a return is initiated. For example, a system might run a GET /transactions/refund request to pull original tax data, preventing manual entry mistakes. When processing refunds, staff can use keyboard shortcuts like Ctrl + R in their custom ERP interface to auto-populate return templates with verified historical transaction details, ensuring absolute accuracy before the data is committed to the financial database.

Audit Readiness and Document Retention Checklist

Maintaining a secure, organized archive of return transactions is the ultimate defense against aggressive state audits. Tax auditors routinely demand proof of physical returns to validate claims for sales tax refunds and deductions.

The following table outlines the essential retention guidelines and documentation required to maintain audit readiness:

| Document Type | Required Data Fields | Retention Period |

|---|---|---|

| Return Authorization (RMA) | Origin, Destination, Customer ID, Reason Code | 7 Years |

| Proof of Delivery (BOL/Tracking) | Carrier details, Delivery signature, Weight | 5 Years |

| Credit Memo / Tax Refund Receipt | Original tax rate, Refunded amount, Date of refund | 7 Years (Minimum) |

Leave a comment