Managing out-of-state sales returns is a persistent logistical minefield for growing businesses, where navigating conflicting state tax codes and shifting nexus thresholds often leads to costly compliance errors. Before addressing these regulatory hurdles, merchants must recognize that rising interstate transaction volumes demand more than manual tracking; they require a systemic approach to document management.

By implementing standardized compliance templates, organizations grant their accounting departments immediate audit readiness and invaluable peace of mind. Note: While standardized frameworks provide a robust foundation for risk mitigation, they must be periodically updated to align with evolving state-specific legislation.

Utilizing concrete tools-such as standardized Interstate Credit Memorandums and Out-of-State Exemption Affidavits-ensures your audit trail remains unbroken. This article will outline the essential components of these compliant templates, analyze key state-by-state variations, and provide actionable frameworks to streamline your reverse-logistics workflow.

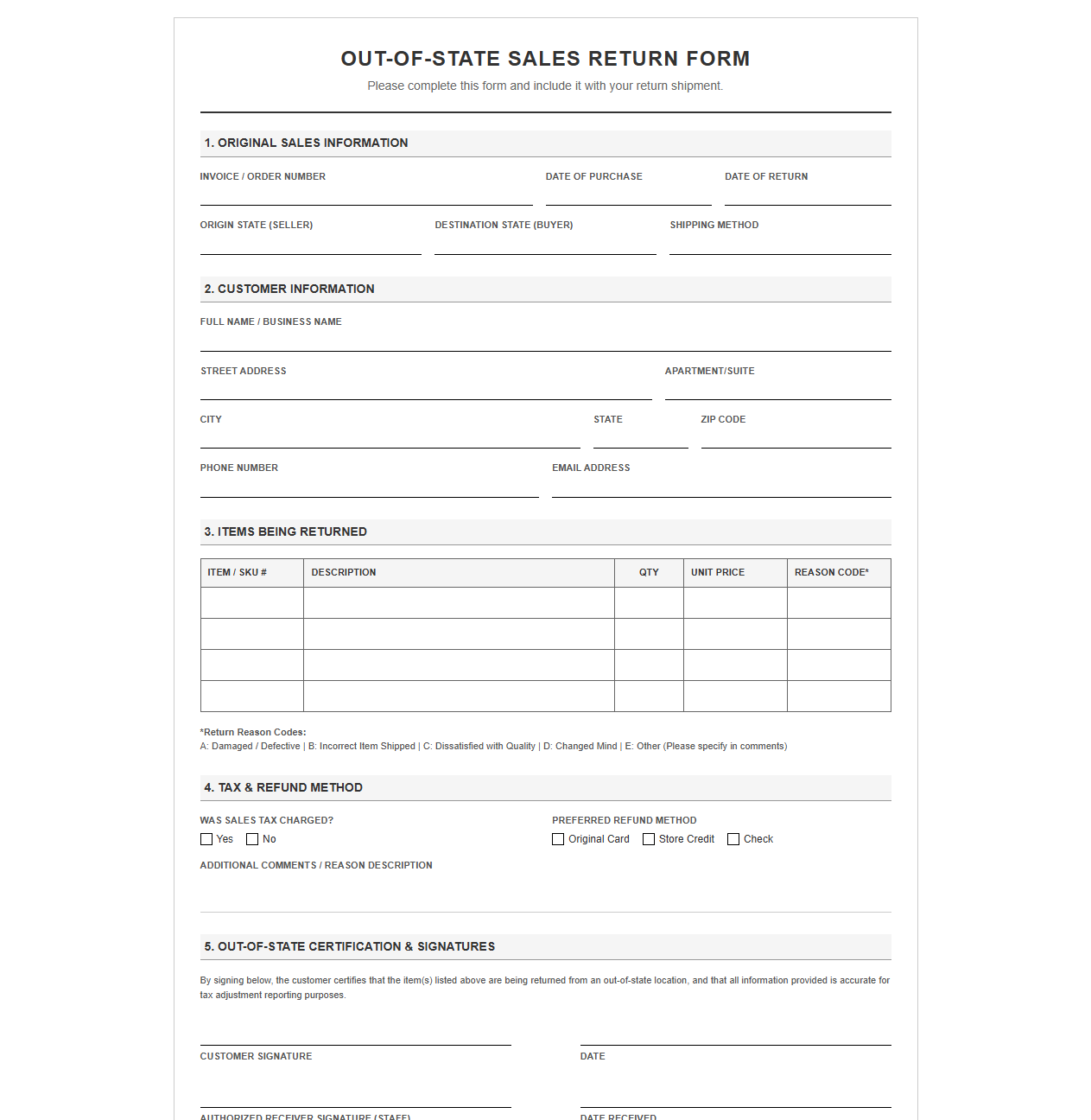

Out-of-State Sales Return Form

Download: .PDF

Download: .PDF

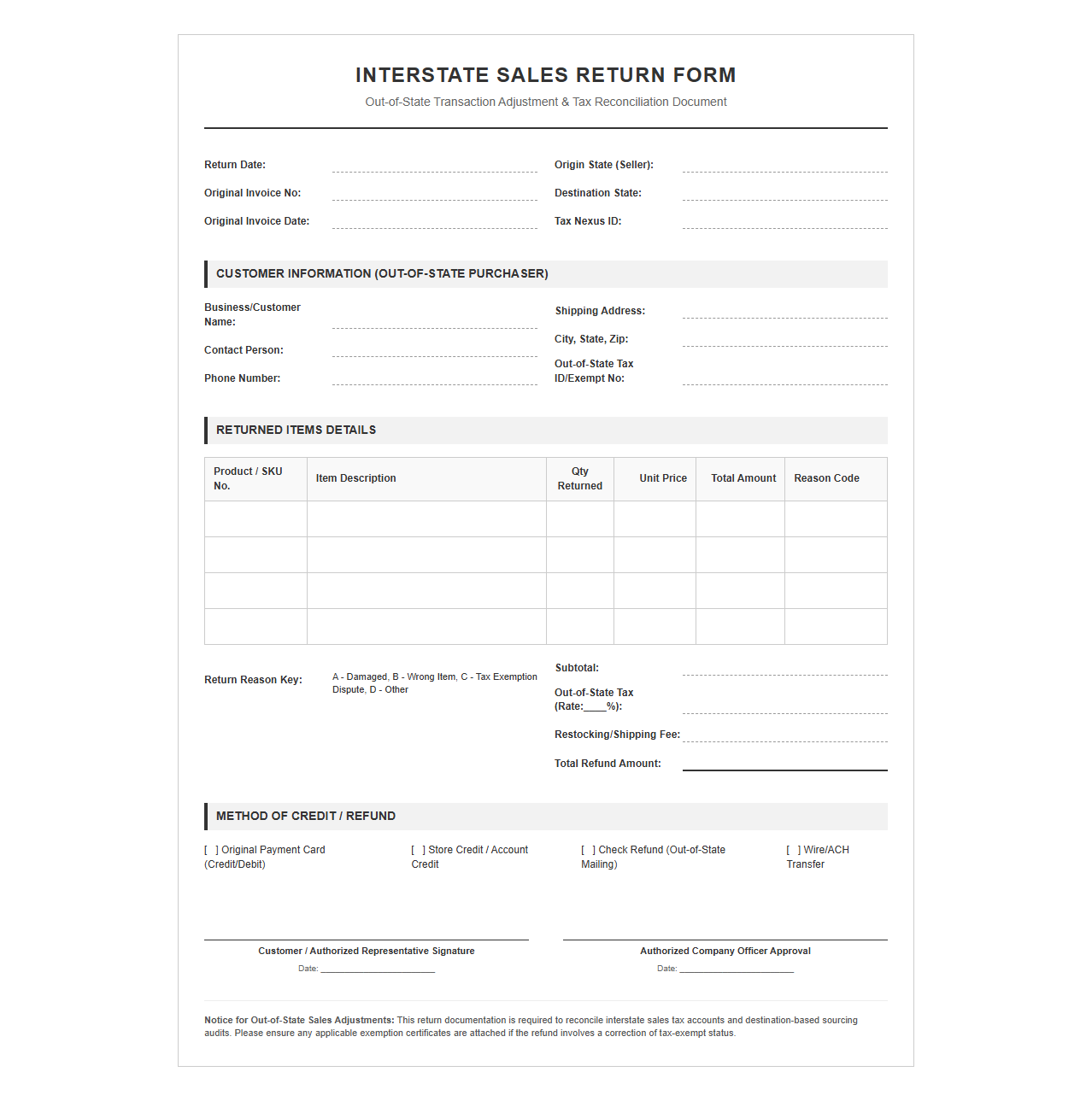

Interstate Sales Return Template

Download: .PDF

Download: .PDF

Cross-State Purchase Return Form

Download: .PDF

Download: .PDF

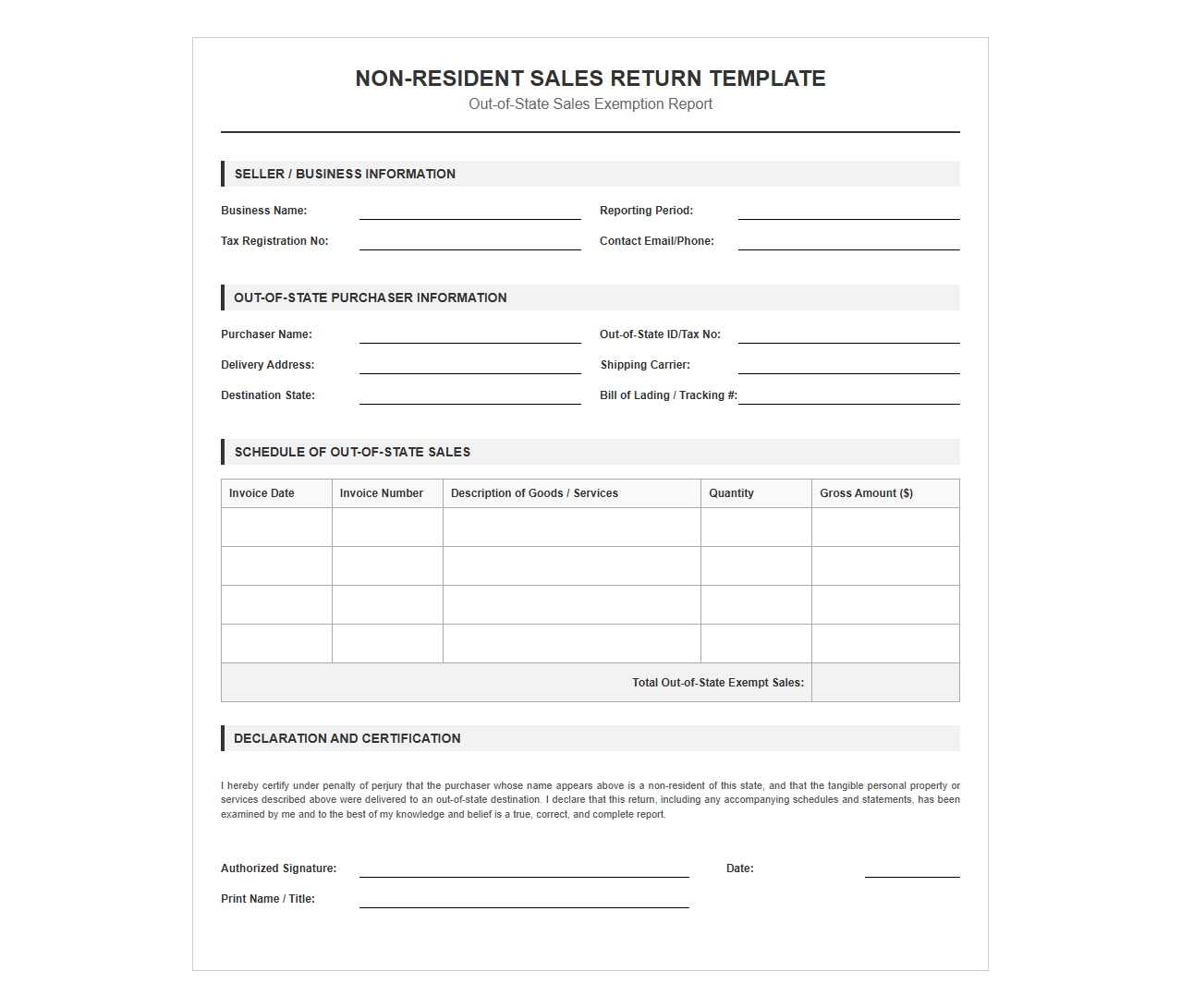

Non-Resident Sales Return Template

Download: .PDF

Download: .PDF

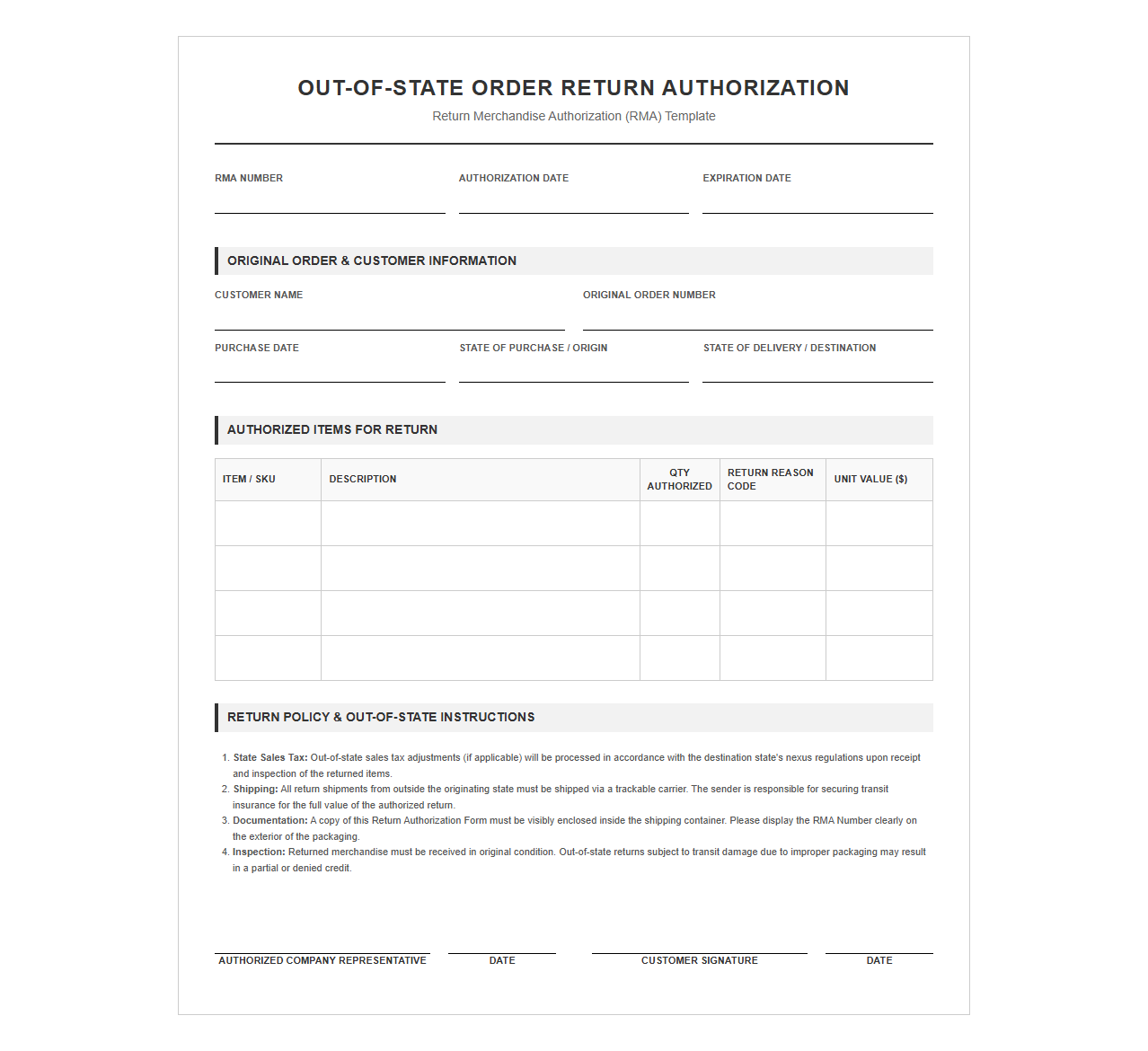

Out-of-State Order Return Authorization Form

Download: .PDF

Download: .PDF

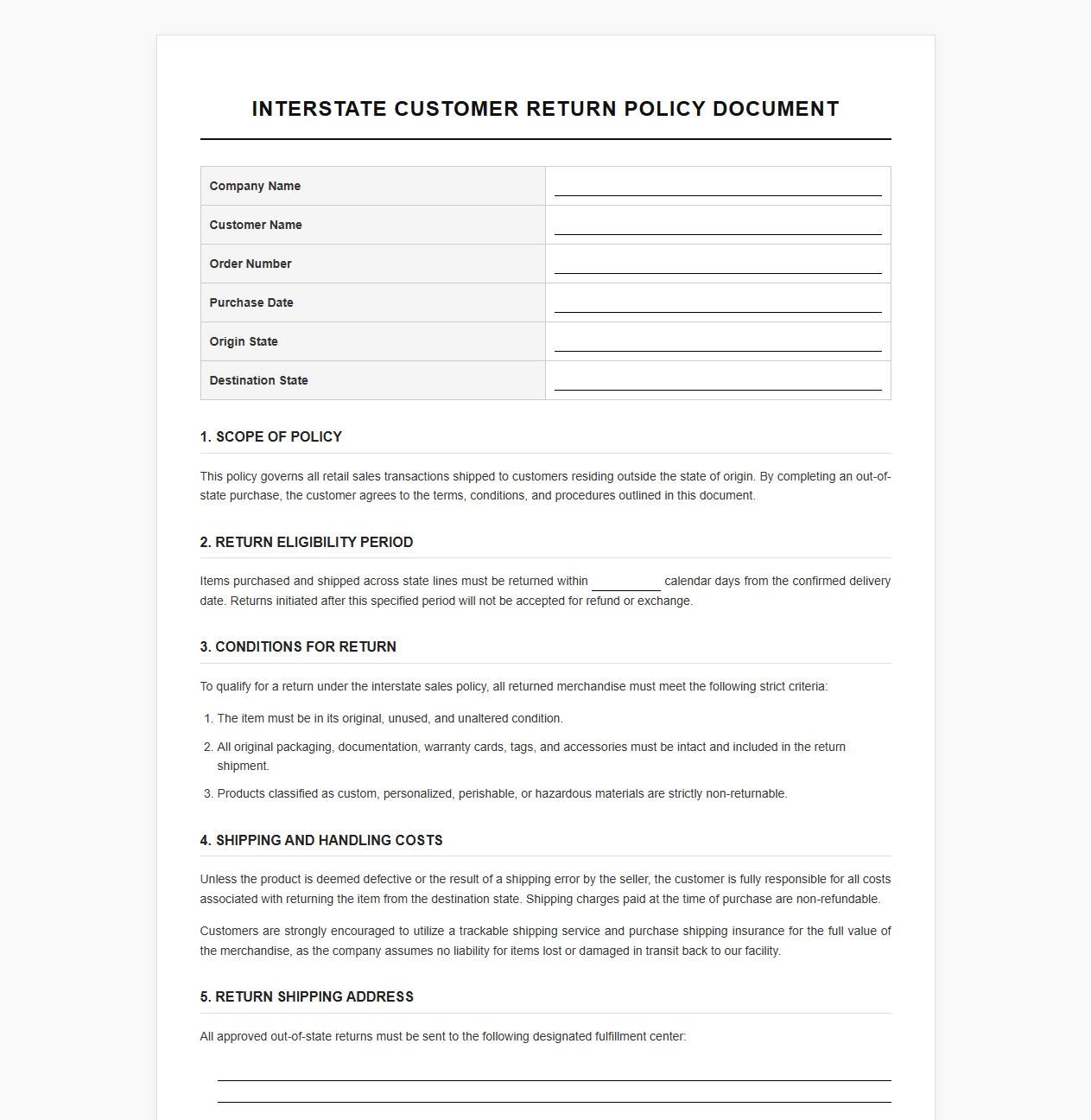

Interstate Customer Return Policy Document

Download: .PDF

Download: .PDF

Cross-Border Sales Return Request Template

Download: .PDF

Download: .PDF

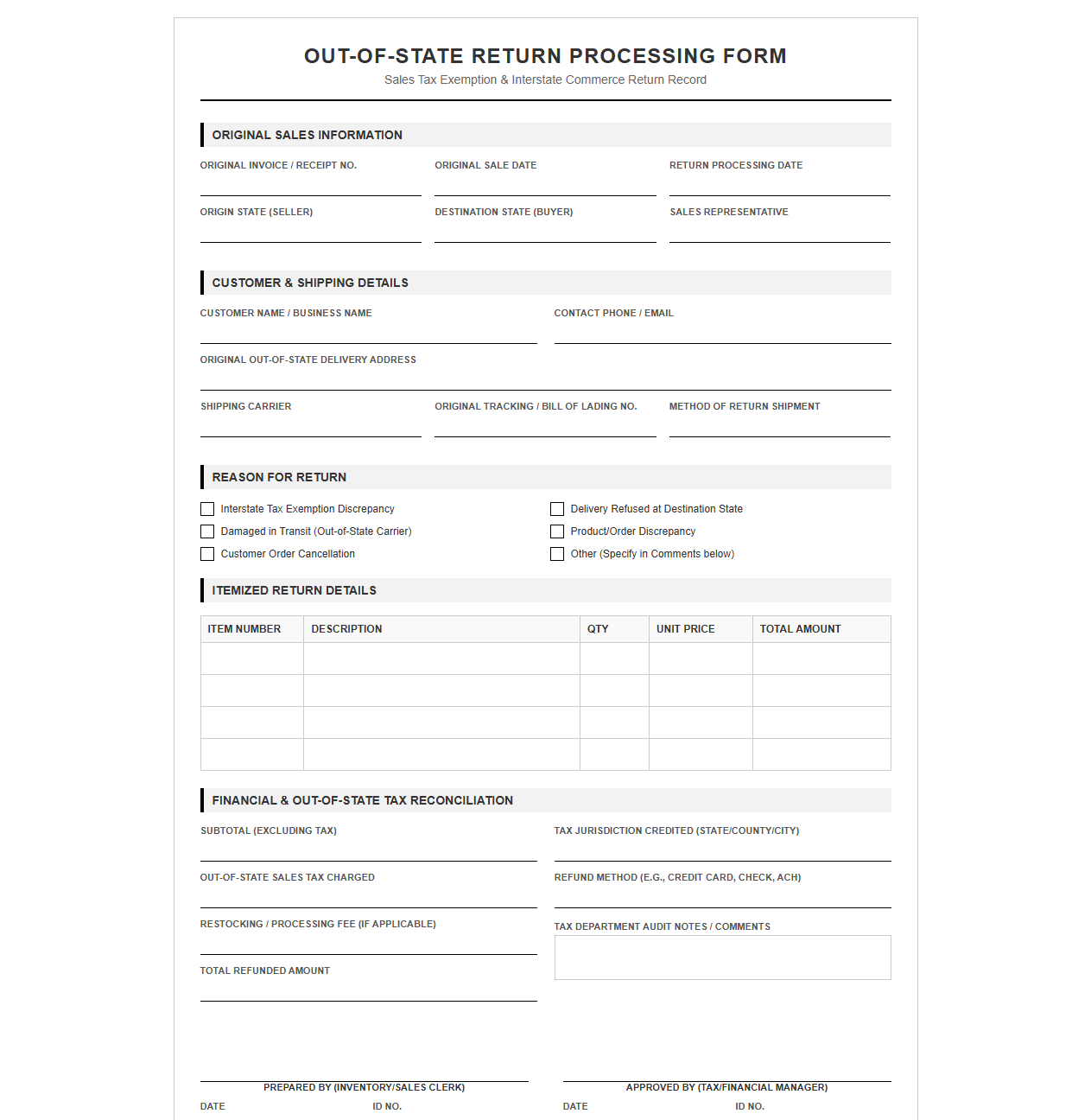

Out-of-State Return Processing Template

Download: .PDF

Download: .PDF

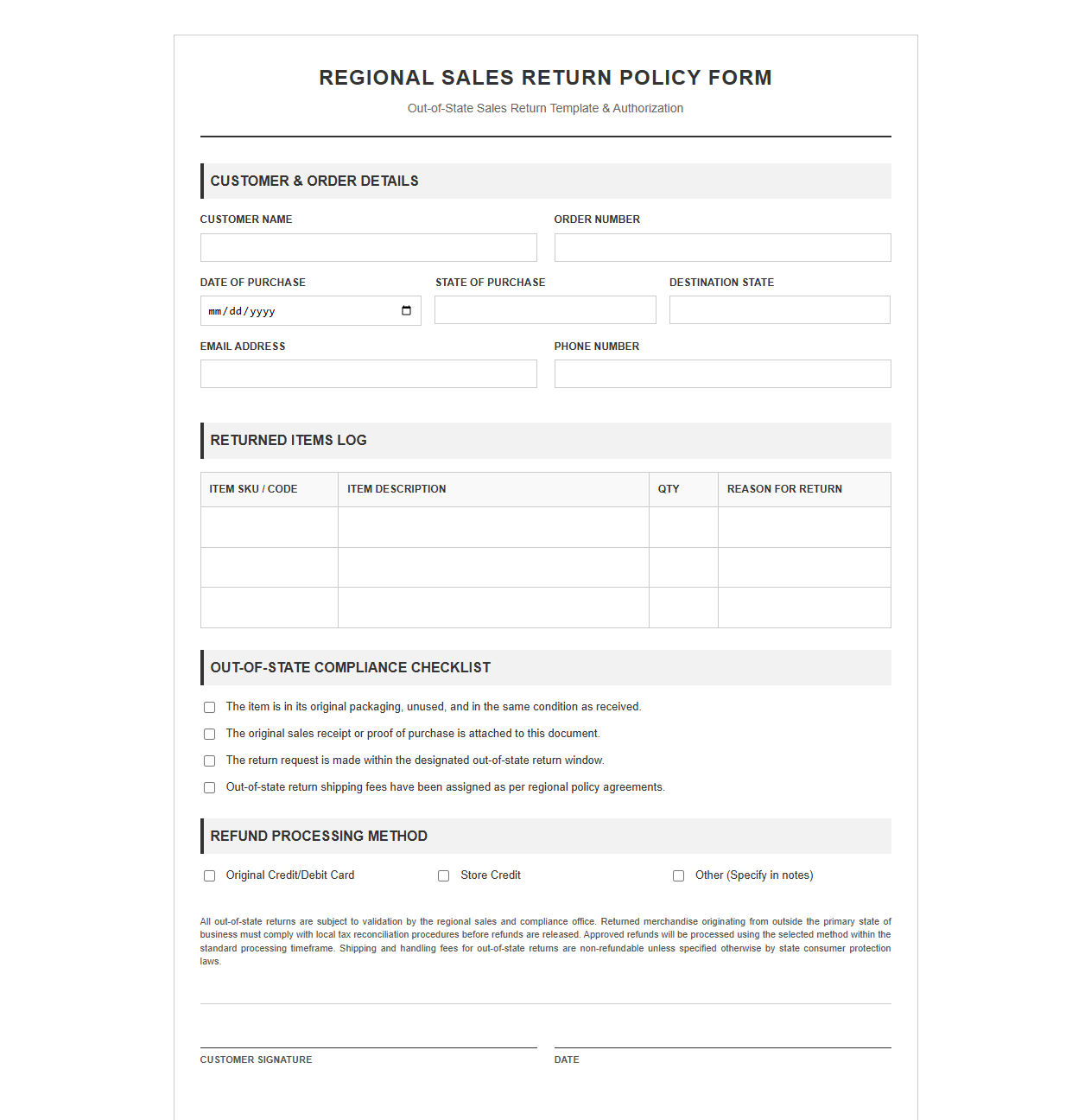

Regional Sales Return Policy Form

Download: .PDF

Download: .PDF

Navigating the Complexity of Interstate Sales Returns

Managing commerce within a single state is challenging enough, but when transactions cross state lines, the logistical hurdles multiply exponentially. For modern businesses, handling out-of-state sales returns involves a complex web of varying regional shipping policies, physical transit risks, and highly intricate tax jurisdictions. A single returned item can trigger a chain reaction of reverse logistics challenges and tax reconciliation errors if not managed with precision. To protect profit margins and maintain operational efficiency, organizations must move away from ad-hoc processes. Standardizing documentation through structured templates is absolutely critical to ensuring that every returned product is tracked, accounted for, and legally compliant, converting a potential operational bottleneck into a seamless, repeatable workflow.

Regulatory Frameworks Governing Out-of-State Returns

Operating across state lines subjects businesses to a complex matrix of federal and state laws. Understanding the legal landscape is the first step toward building an audit-ready reverse logistics process.

The primary regulatory drivers that dictate how out-of-state returns must be documented include:

- Sales Tax Nexus Rules: Physical presence or economic thresholds (such as those established by the Wayfair decision) dictate whether your business must collect and remit sales tax. Returns can alter these economic thresholds and must be documented to prove a reduction in taxable sales.

- The Streamlined Sales and Use Tax Agreement (SSUTA): For participating states, this agreement standardizes definitions and rules, but businesses must still maintain rigorous documentation to prove that tax refunds match the exact jurisdiction where the original purchase occurred.

- State-Specific Destination vs. Origin Sourcing: Depending on whether a state uses origin-based or destination-based sourcing, the tax rate applied to the initial purchase-and subsequently refunded during a return-will vary, requiring exact location tracking.

- Audit Trail Integrity: State tax auditors heavily scrutinize out-of-state transactions. Standardized documents serve as verifiable proof that returned inventory actually crossed state lines and that the corresponding tax credit was legally justified.

Template 1: The Standardized Return Merchandise Authorization (RMA)

The Gateway to Return Tracking

An effective Return Merchandise Authorization (RMA) is the cornerstone of any compliant reverse logistics system. By capturing critical transaction data at the point of origin, businesses can ensure that tax calculations and inventory updates remain accurate across jurisdictions.

| Field Name | Data Type / Format | Compliance Purpose |

|---|---|---|

| Original Invoice Number | Alphanumeric | Links the return directly to the original taxable transaction for audit verification. |

| State of Original Purchase | Two-Letter State Code | Identifies the primary tax jurisdiction responsible for the initial sales tax collection. |

| Localized Tax Jurisdiction | City, County, or ZIP Code | Ensures that local, county, and municipal transit taxes are correctly calculated for refund. |

| Return Reason Code | Standardized Dropdown | Categorizes returns (e.g., damaged, incorrect item) to determine inventory write-offs versus restock status. |

| Item Disposition State | Damaged / Restockable | Informs tax authorities whether the returned asset has been destroyed or returned to active inventory. |

Template 2: Interstate Shipping and Bill of Lading Documentation

Ensuring Safe and Legally Verifiable Transit

When physical assets cross state lines during a return, they enter the jurisdiction of federal transportation agencies and interstate commerce laws. The documentation accompanying the physical shipment must serve as irrefutable proof of transit to justify the reversal of interstate sales tax and verify the location of the inventory.

- Bill of Lading (BOL): This acts as a legal contract between the shipper and the carrier, detailing the exact quantity, weight, and description of the returned goods crossing state lines.

- Interstate Return Shipping Label: A specialized label featuring the origin address, destination warehouse, and the unique RMA barcode to ensure real-time tracking across state borders.

- Consignee Copy: A document retained by the receiving warehouse to verify that the physical goods match the manifest upon arrival, closing the loop on the interstate transfer.

Without these three essential documents, a business cannot legally prove to state auditors that a returned item actually left the customer's state, risking severe penalties and unpaid tax liabilities.

Template 3: Sales Tax Adjustment and Credit Note Template

Reconciling Financial and Tax Records

Issuing a credit note for an out-of-state return requires a clear, itemized breakdown to satisfy financial accounting standards and state tax department audits. Blending the product cost and the tax refund into a single lump sum is a common compliance pitfall.

| Document Title: | Credit Note / Tax Adjustment Memo |

| Original Tax Rate Applied: | 8.25% (State + Local District Tax) |

| Net Product Cost Refunded: | $1,200.00 |

| Sales Tax Refunded: | $99.00 |

| Total Adjusted Credit: | $1,299.00 |

By clearly segregating the product value from the localized tax, financial teams can accurately adjust their tax liabilities in the origin state without distorting overall revenue records.

Best Practices for Implementing Standardized Document Workflows

Deploying templates is only half the battle; integrating them into your daily operations is where true efficiency is realized. Businesses should leverage technology to automate the flow of return documentation, minimizing the need for manual data entry.

- ERP Integration: Map your RMA and credit note templates directly to your Enterprise Resource Planning (ERP) software to automatically reverse revenue and adjust inventory levels across multi-state warehouses.

- CRM Synchronization: Ensure your Customer Relationship Management (CRM) platform pulls data directly from active shipping APIs to keep customer service representatives updated on the status of interstate transits.

- Automated Tax Engine Connections: Connect your return templates to tax calculation engines like Avalara or TaxJar to automatically determine the exact historical tax rate of the purchase state at the moment the credit note is generated.

- Unified Data Validation: Use strict input validation rules on your digital templates to prevent shipping labels from being generated without a verified original invoice number and state tax jurisdiction.

Future-Proofing Your Interstate Return Policy

Establishing robust, standardized return documentation protects your business from costly compliance errors, simplifies the audit process, and preserves customer trust. As state-level tax regulations continue to shift, maintaining static processes is no longer a viable option.

Leave a comment